Equities

Erdogan will most likely lose the Turkish election but it could go onto a second round. A strong opposition majority in the assembly would justify a tactical overweight in Turkish equities on a relative basis. For now, go long Turkish equity volatility.

There is a 50:50 chance of experiencing a major deflationary shock in the next two years, and an even greater likelihood on a longer timeframe. The good news is that several assets provide a good insurance against this risk, and that this insurance is now cheap. Plus we highlight a compelling commodity pair-trade.

This week we are sending you a transcript of my conversation with one of China’s most prominent and influential pro-market economists. Topics raised during my conversation with this Chinese expert may offer our clients important insights and provide context into recent developments in China’s economy.

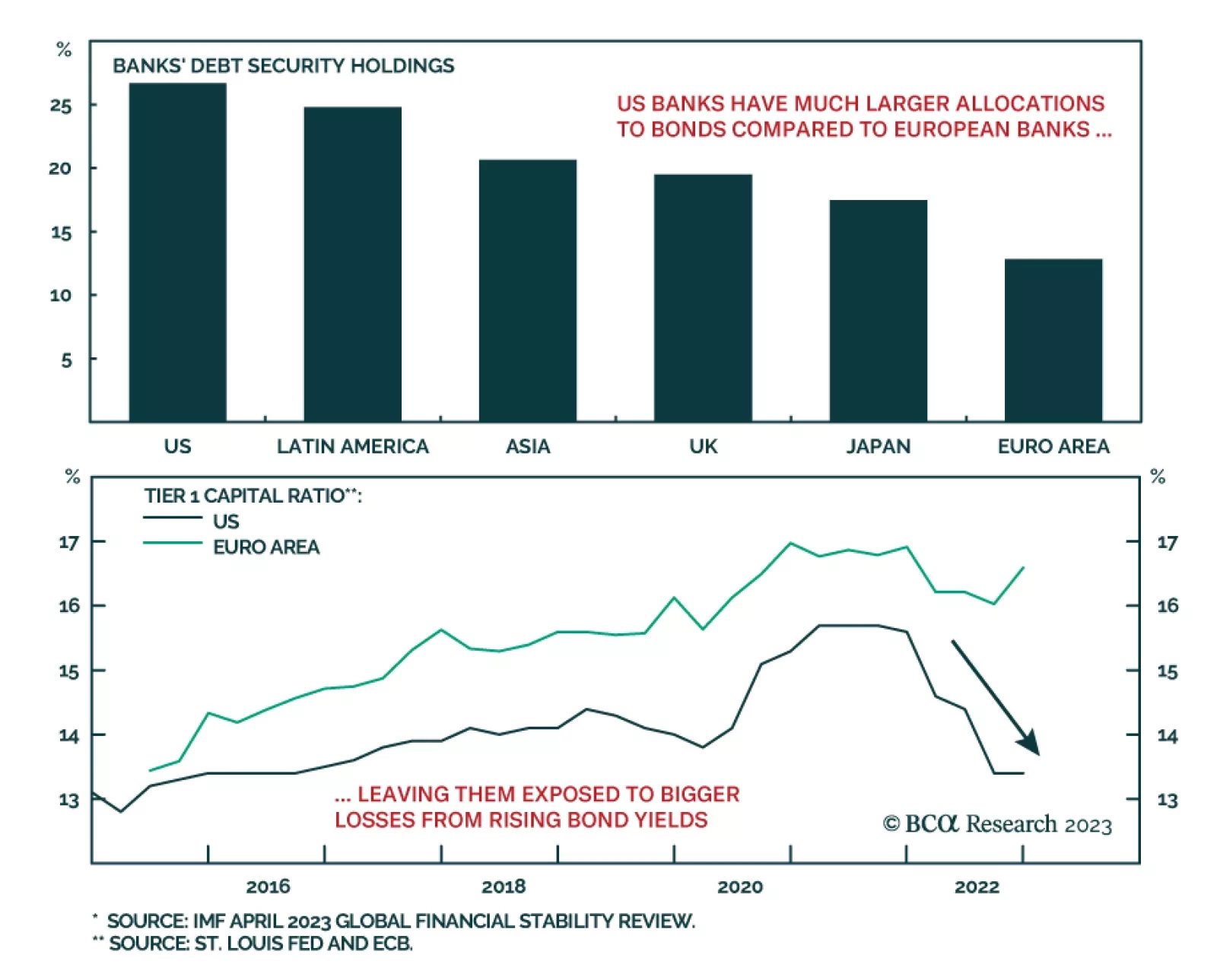

Although our take has not changed yet, the immediate emergence of a second wave of banking system stresses poses a new threat to our constructive near-term economic and market views and will have to be monitored carefully.

If the recession begins this year, it is unlikely to be mild, because inflation will not have fallen by enough to allow the Fed to cut rates aggressively. In contrast, if the recession starts in 2024 or later, when inflation is likely to be much lower, the Fed will be able to cushion the blow. Our base case remains a 2024 recession but the risks around that view have increased in light of recent banking stresses.

Indian EPS growth is set for major disappointments vis-à-vis the lofty expectations. Weak domestic demand amid tight fiscal and monetary policy entails more downside in stock prices. Stay underweight.