Equities

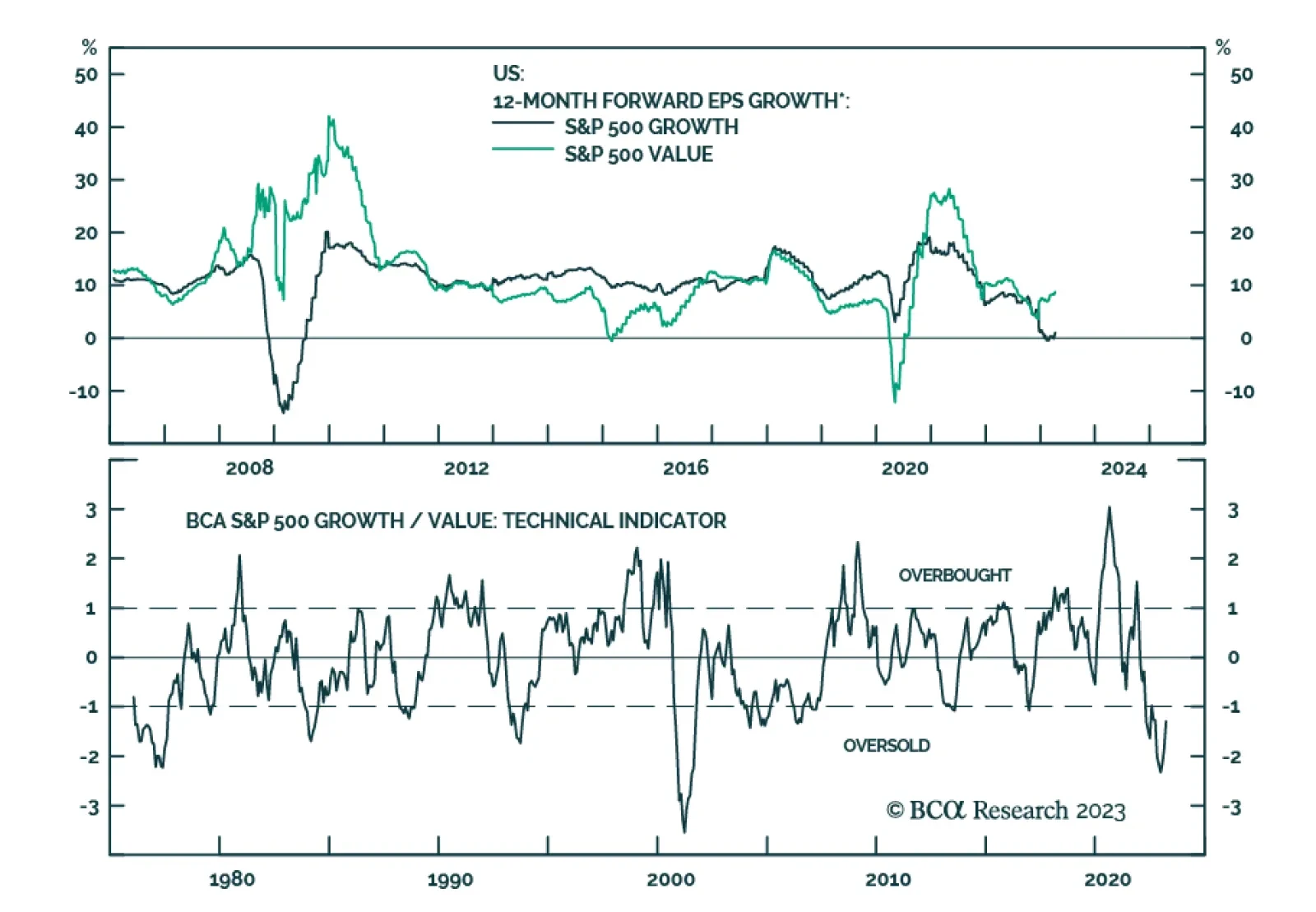

The YTD market rally was driven by outperformance of high-quality growth stocks which offer protection in uncertain times. As growth continues to slow, high-quality growth stocks should continue to do well. Hence, we are moving to overweight Growth vs. Value.

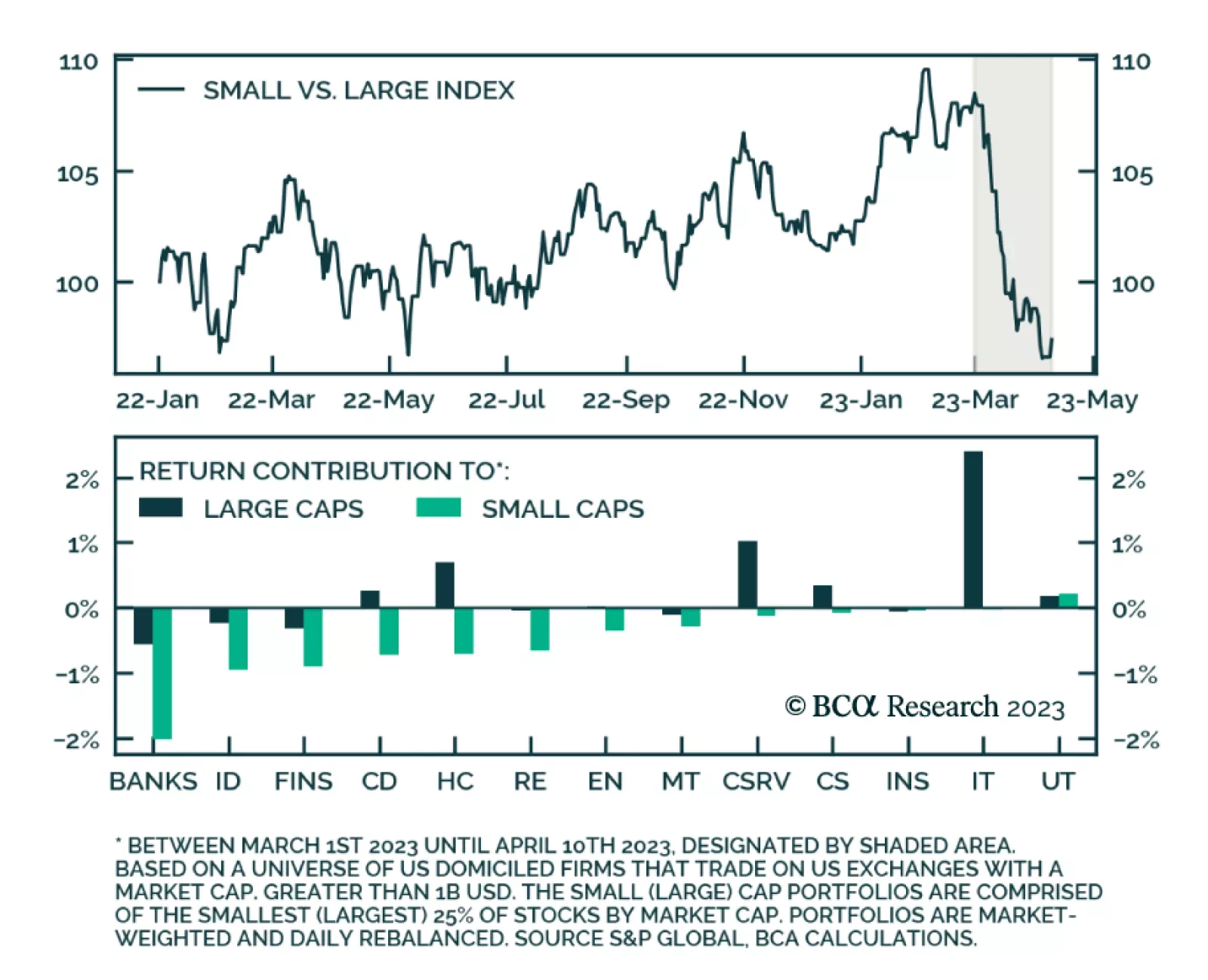

Investors and regulators would be foolishly complacent if they didn’t consider the possibility that the banking turmoil could reduce credit availability and slow economic activity, but the most recent data suggest that the aggregate banking system is bouncing back nicely.

We Introduce our new macro models for the Eurozone’s equity earnings, which include sectoral forecasts. Find out what they predict for the next six-to-nine months.

A benign disinflation is probable during the remainder of 2023. Unfortunately, just when most people become convinced that a recession has been avoided, a recession will begin.

There are several widespread market narratives regarding US inflation, the Fed’s policy, global manufacturing/trade and China’s recovery that we disagree with. In this report, we explain our reasoning and where it puts us in terms of investment strategies.

Innovative Tech will face macroeconomic headwinds in a new “higher for longer” interest regime. Yet, the long-term opportunity of the cohort is tremendous. Investors need to be judicious with the timing of adding new capital to these themes to bolster long-term returns.