Equities

In Section I, we discuss the implications of the banking crisis that emerged in March. We do not expect what happened in the US or Europe to morph into a full-blown meltdown of the financial system, but this month’s events will likely lead to a further tightening in bank lending standards, raising further the odds of a US recession over the coming year. We continue to recommend an underweight stance toward risky assets versus government bonds over the coming 6-12 months, and defensive positioning within a global equity portfolio. In Section II, we estimate the impact of recently-passed US legislation on US business investment over the structural horizon and conclude that it will indeed boost capex growth over the coming several years. Assets poised to benefit from this trend will likely underperform over the coming year but should be bottom-fished following the next recession.

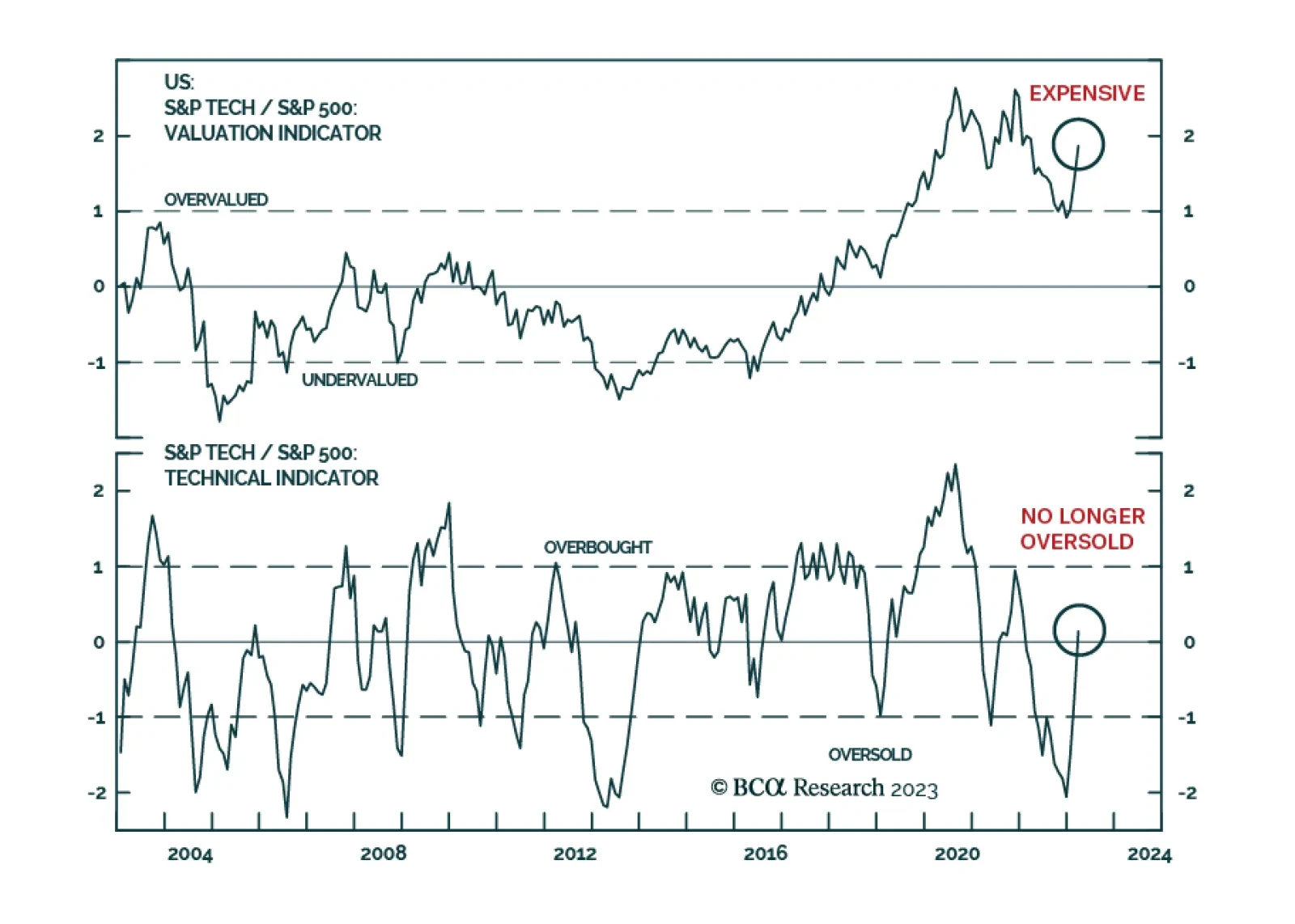

It is a big mistake to think that rate cuts or lower bond yields will ease credit conditions. Quite the contrary. After an aggressive tightening of monetary policy, the first rate cuts always coincide with much tighter credit conditions. We discuss the implications for credit, government bonds and equities. Plus, we find a startling anomaly in equity sector performance.

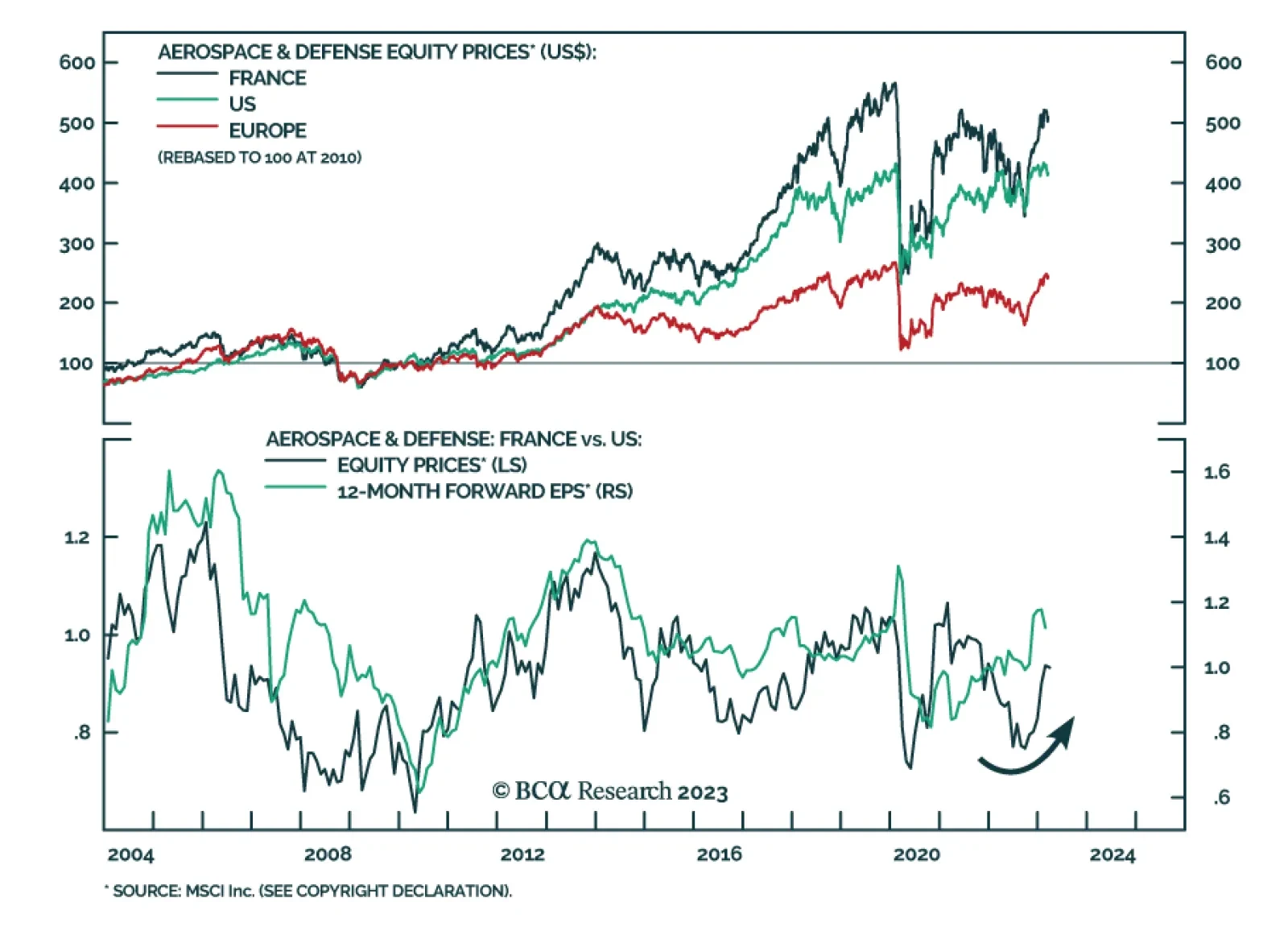

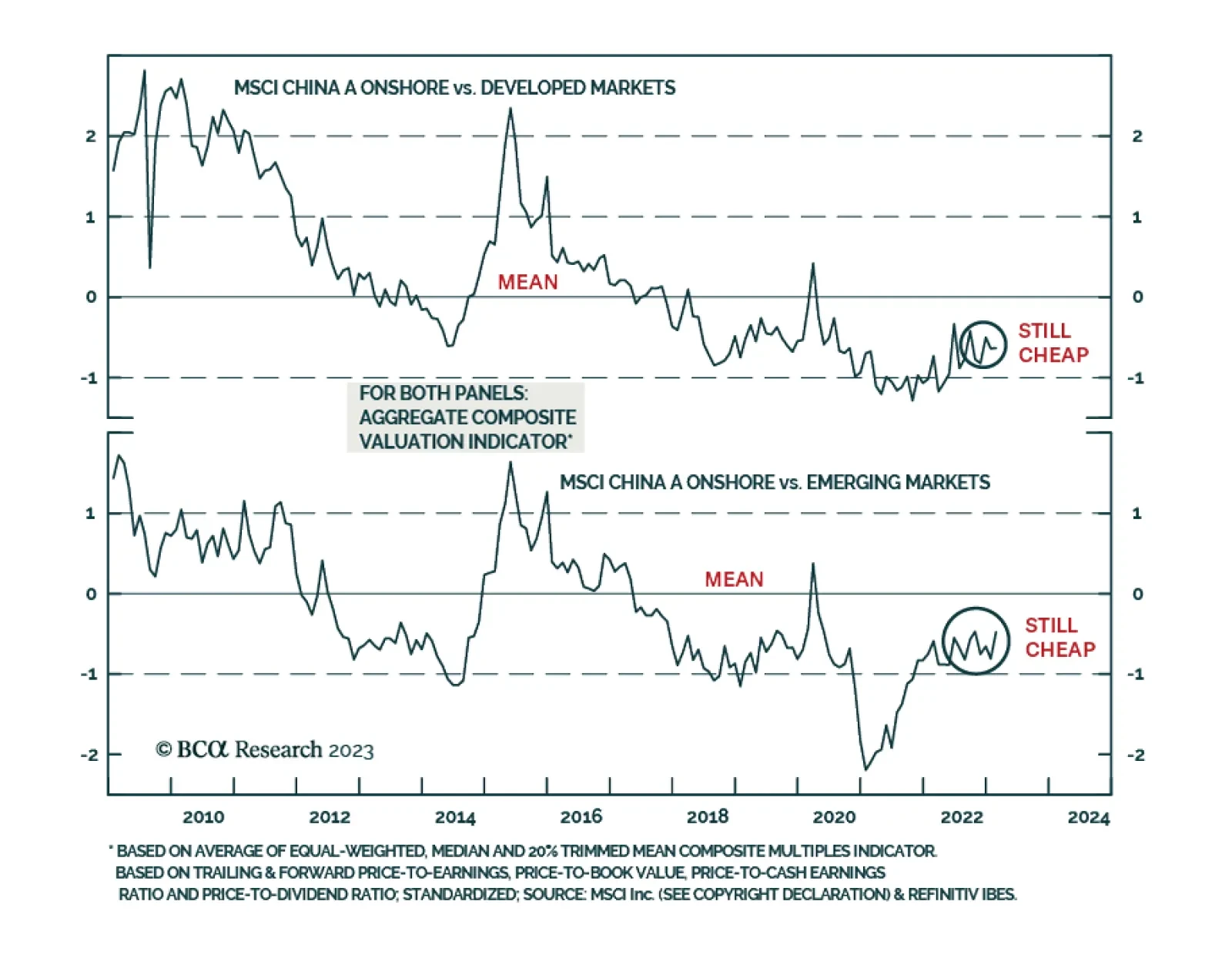

Chinese onshore stocks are attractive on a risk-reward basis relative to their global counterparts. If the global equity bear market continues, our bias is that Chinese onshore stock prices will also drop, but they will likely fall by less than their global peers.

It is too early to know whether the drop in bond yields will offset the drag on growth from tighter lending standards. But if it does, the net effect on equity valuations could be positive. This is enough to justify a modest tactical overweight to equities, with the proviso that investors should look to reduce equity exposure later this year in advance of a mild recession in 2024.

US financial instability reinforces our bearish investment outlook by weighing on economic growth and corporate earnings while also increasing US policy uncertainty and geopolitical risk.

Have global equity markets reached a riot point? Is the Fed going on hold a sufficient condition for stocks to stage a cyclical rally? If not, what would be needed to produce such a rally? Does the Fed’s recent balance sheet expansion foreshadow a rise in the US money supply? This report provides answers to all these questions.