Equities

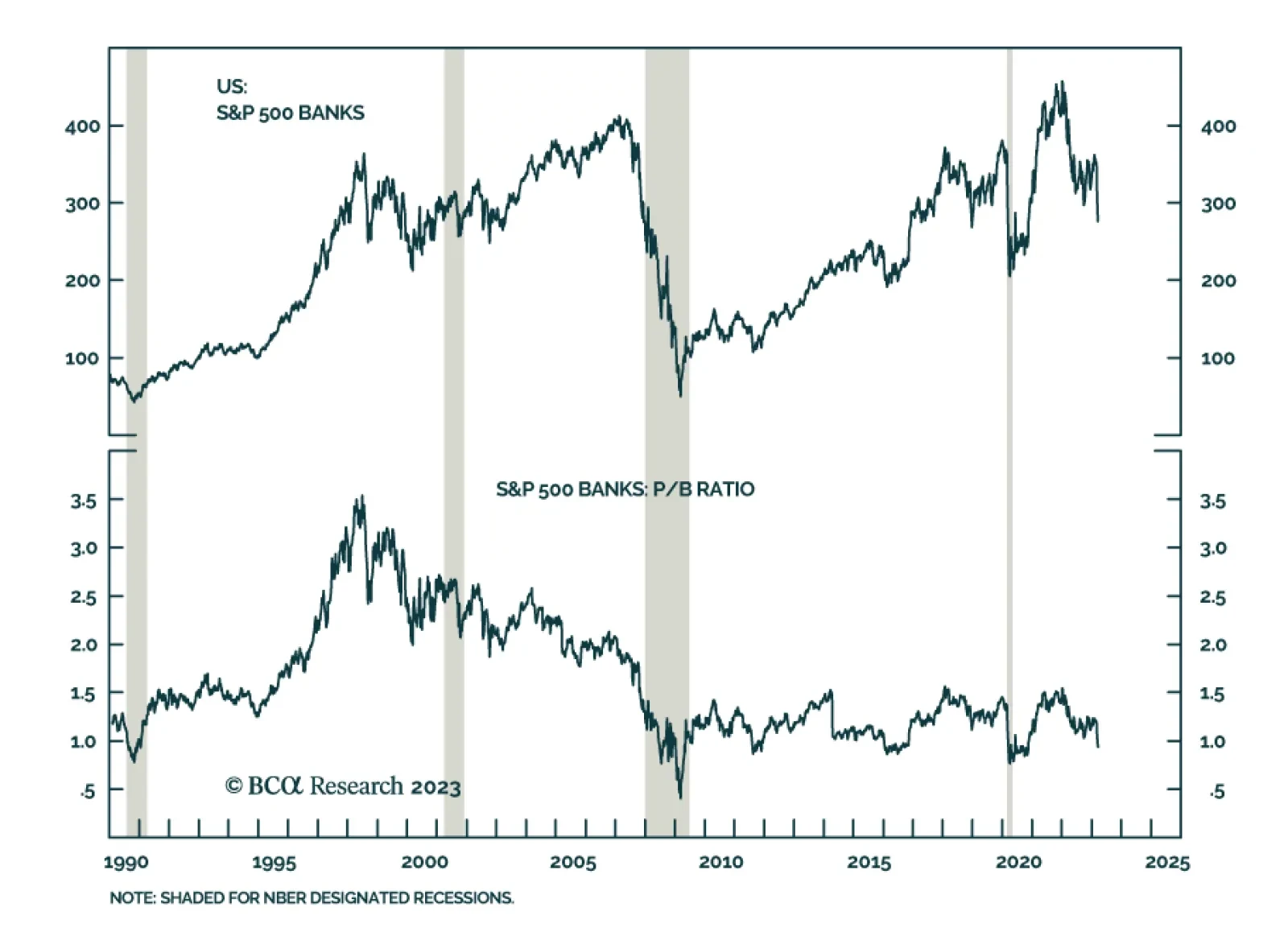

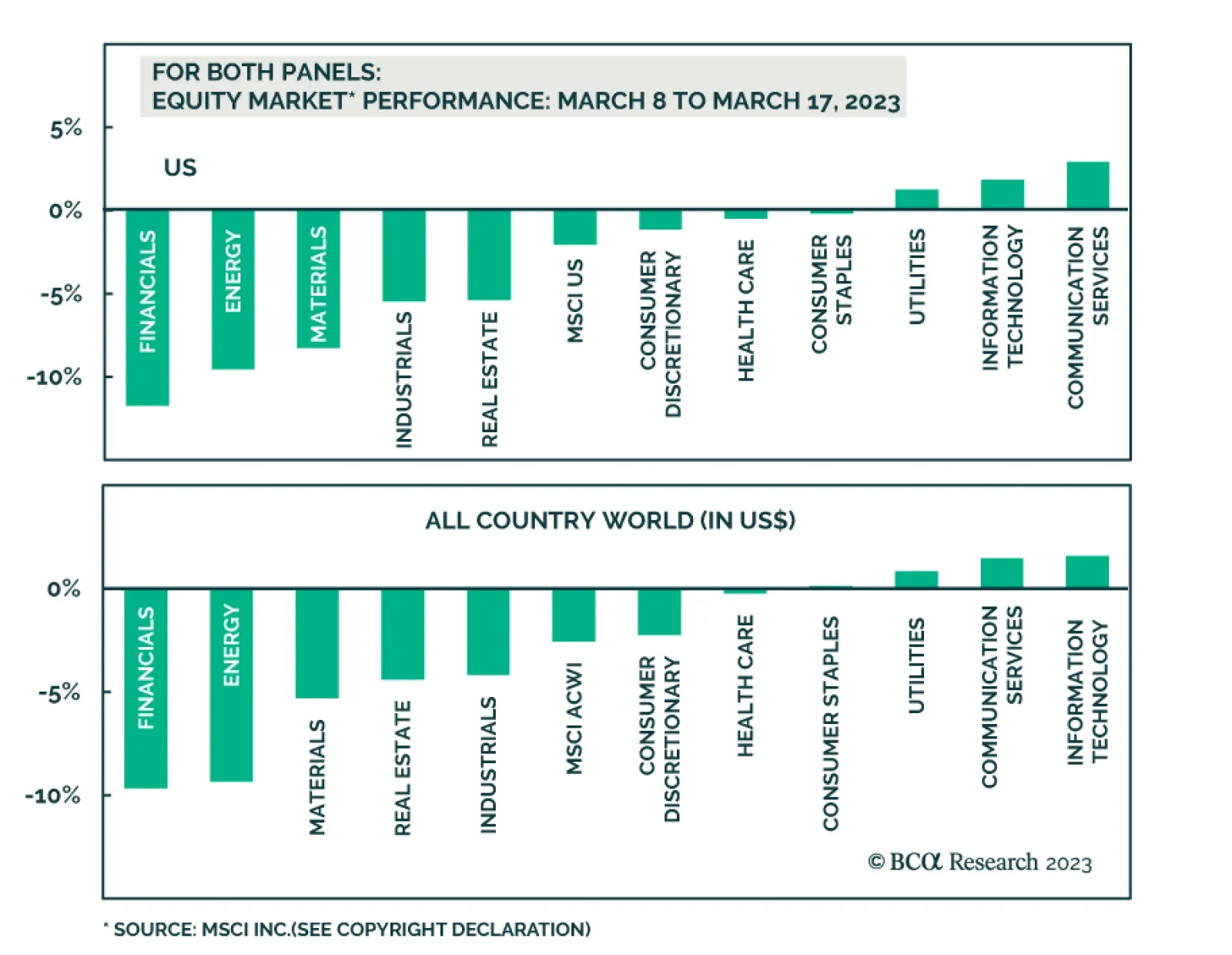

The banking crisis has hit European shores and engulfed CS; is this all bad news for Europe or have the odds of a policy mistake declined?

The turmoil in US regional banks will weigh on economic growth. Arguably, it would be better for the broader stock market if growth slowed because banks became more conservative in their lending than if it slowed because the Fed had to raise rates to over 6%. In both cases, economic growth would decelerate but at least in the former scenario, the discount rate applied to earnings would not be as high.

The odds of achieving a goldilocks scenario in the US where inflation drops amidst robust growth are low. If US bank woes do not escalate, the Fed will continue hiking amid a contraction in US corporate profits and global trade. The recovery in China’s industrial economy will disappoint. Commodity prices are breaking down.

Bank failures are another ‘canary in the coal mine’ warning that a US recession is imminent, yet stocks, bonds, and the oil price are still a long way from fully pricing it.

The growth and inflation profiles of the three central European countries are set to diverge. The outlook for Polish and Hungarian Bonds are not attractive anymore. Book profits on them. Instead, initiate a new trade: pay Polish / receive Czech 10-year swap rates.

Generative AI is a major technological breakthrough that holds tremendous economic and investment promise and will have sweeping effects on wide swaths of the economy. We are bullish on generative AI as a long-term investment theme. However, at the moment we observe hallmarks of an investment frenzy. We believe that there will be a more attractive entry point for patient investors.