Equities

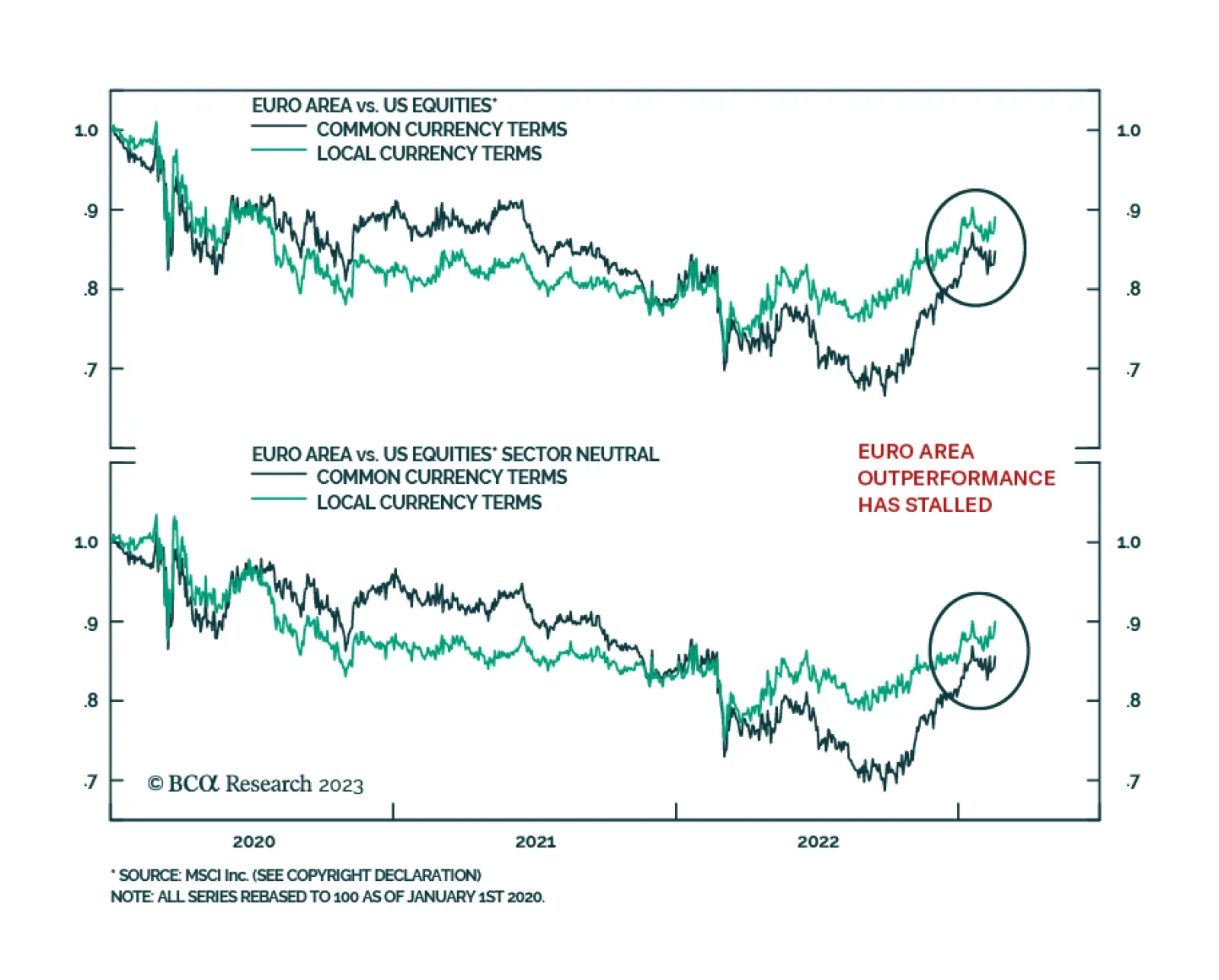

Great Power Rivalry is taking another leg up as Russia and China further align their geopolitical interests. Investors should stay long USD-CNY, favor defensives over cyclicals, and markets like North America and DM Europe that have less exposure to geopolitical risk.

In Section I, we address the recent improvement in several data releases over the past three months, and explain why we do not believe that these developments have increased the odds of a soft landing. US monetary policy likely became tight in November, which has started the recessionary clock. We continue to recommend a conservative investment stance over the coming 6-12 months that anticipates eventually lower long-maturity bond yields. In Section II, we explain why the Fed’s unreasonably low neutral rate forecast is the main risk to a conservative investment stance over the coming year, as it could lead to interest rates falling back into easy territory before a recession begins. For now, this remains a possible but not probable outcome.

Since 1970, the track record of US housing recessions as the ‘canary in the coal mine’ for economic recessions is a perfect four out of four: 1974; 1980; 1990; and 2007. If this perfect track record continues, the current US housing recession presages an economic recession that starts in 2023. We discuss the investment implications.

Long-term drivers, including the growing ability of banks to returns cash to shareholders, point toward a strong structural performance for European financials. However, the ECB’s aggressive tightening campaign could still spoil the party.

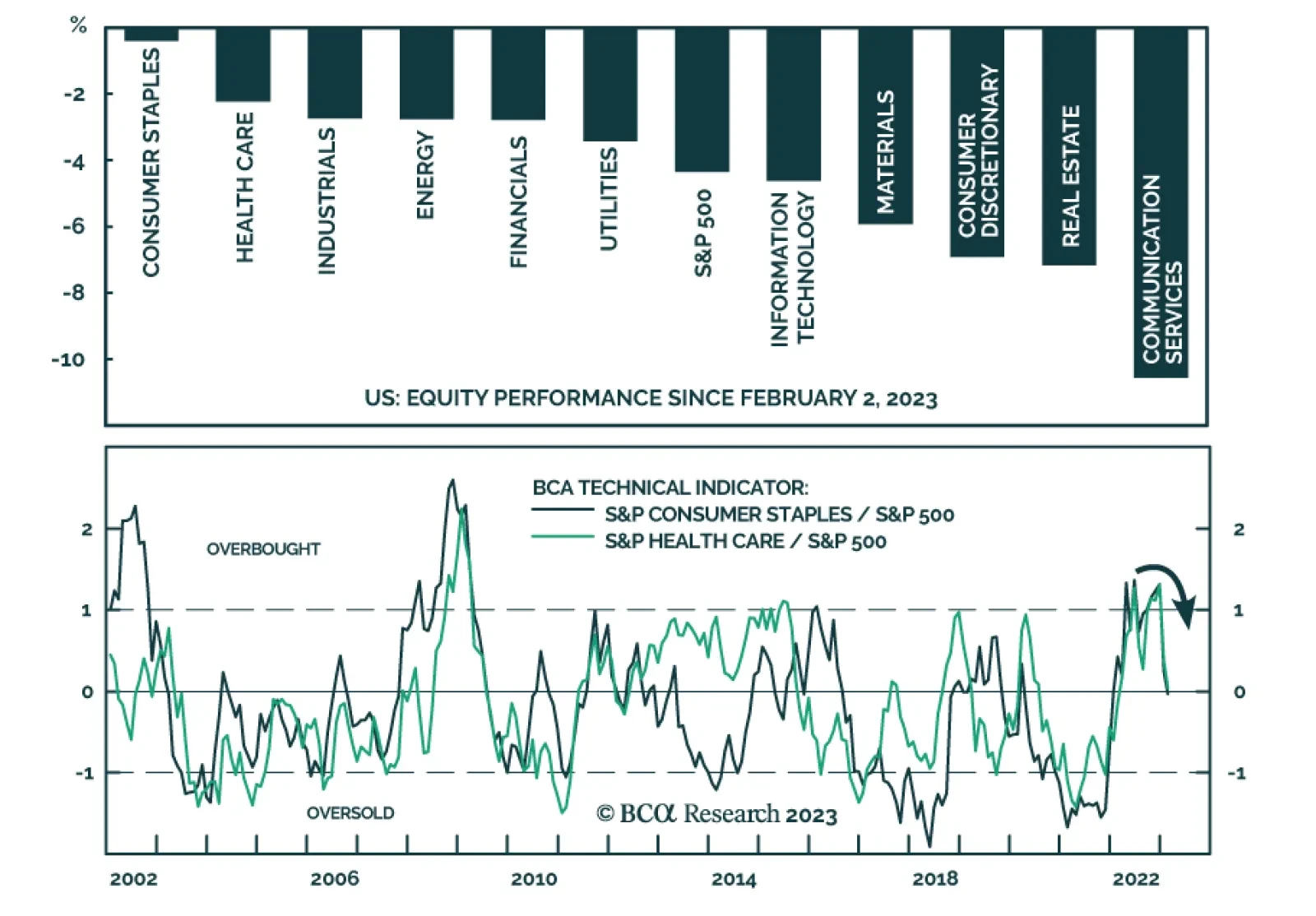

The US equity market is in the midst of an earnings contraction driven by slowing sales growth – a manifestation of the weakening economic demand and loss of corporate pricing power that accompany disinflation. The telecommunications industry is a defensive industry that faces many challenges: Low growth, cut-throat competition, and incessant demands for capital investment.

We refresh our 2023 plan of attack to reflect the latest data and several rounds of discussions with clients in virtual and face-to-face meetings. We continue to expect a meaningful first-half rally in the S&P 500, despite revising our expected terminal fed funds rate 25 basis points higher.