Equities

In EM ex-China, growth will continue decelerating. Some economies will experience an outright recession, while most will have a growth recession. Nearly every single economy will experience a cyclical drop in inflation (with the exception of Turkey).

China's reopening is much more positive for the Chinese economy than it is for the rest of the world, as it will boost its domestic service sector activity and consumer spending much more than the industrial economy. A slowdown in Chinese industrial activity will put downward pressure on its demand for raw materials and energy, helping the world avoid another spike in inflation. Upgrade Macau casinos to overweight as the key beneficiaries of reopening. Off-shore TMT and bank shares face structural headwinds.

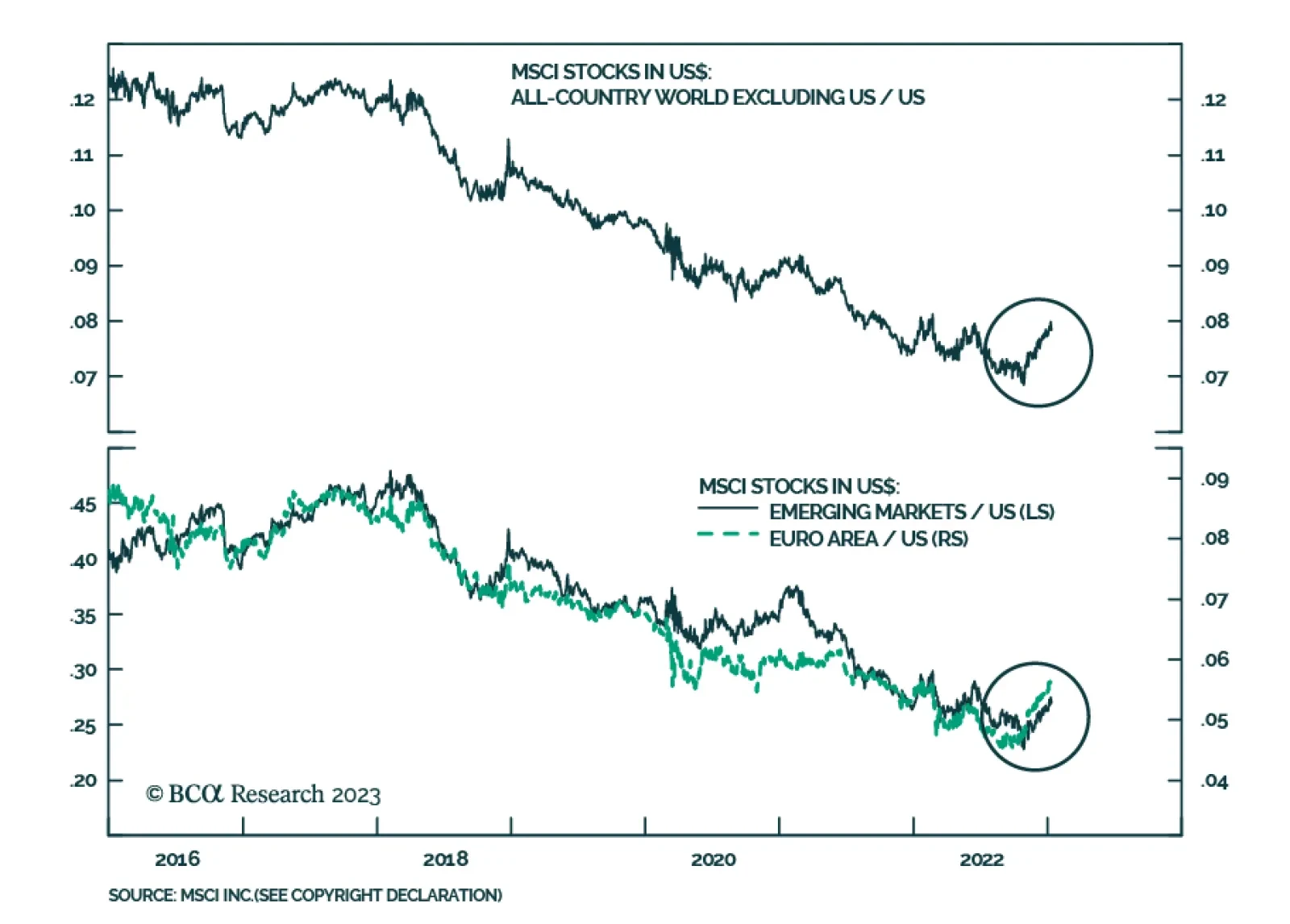

In response to lower energy prices and China’s reopening, European assets prices are outperforming. Will the ECB spoil the party?

While the housing downturn will be fairly mild in the US, it will be more severe abroad. Continue to favor bonds of countries whose housing fundamentals will limit rate hikes.

We measure the effects of inflation and growth cycles on the returns of various assets using the four-quadrant approach, where we classify periods into the following buckets: Slowing inflation/slowing growth (slowdown), rising growth/slowing inflation (goldilocks), rising growth/rising inflation (overheating), and slowing growth/rising inflation (stagflation). Our analysis provides insight into the coming macro environment. As growth and inflation begin to decline, the best choices for asset allocators will be fixed income, precious metals, CTAs and timberland.