Equities

The crucial question for 2023 is: will the US and UK Beveridge Curves shift back inwards to their pre-pandemic versions, ushering in a soft landing? Or, will we slide down the new post-pandemic Beveridge Curves into recession? Plus: we reveal the most important chart for Europe and the most important chart for China in early 2023.

Why will Chinese consumer spending recover but not its industrial sectors? Will China's reopening boost the global business cycle and inflation? How fast will US core inflation fall and what are the implications for corporate profits? Are global equities pricing in enough bad news/profit contraction?

The BCA Score's safety tilt pays off in a turbulent year. USHQ outperformed the SPY in December and USHQ SMID performed inline with its MSCI US SMID Cap benchmark.

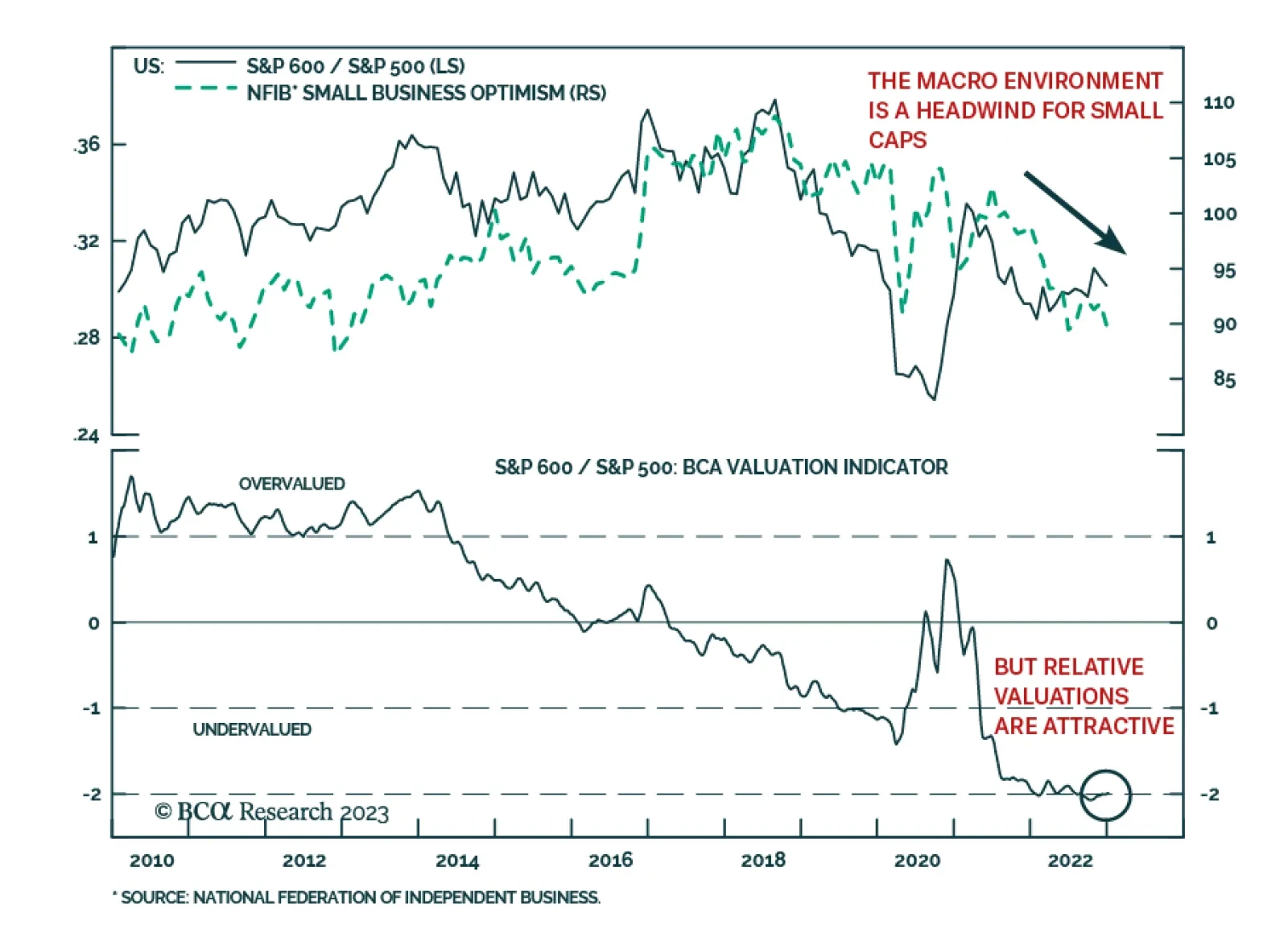

Today we are publishing a charts-only report focused on the key macroeconomic data as well as each GICS1 S&P 500 sector. Many of the charts are self-explanatory; to some we have added a short commentary. The charts cover macro, valuations, fundamentals, technicals, and the uses of cash. Our goal is to equip you with all the data you need to make investment decisions in these sectors.

Relative to beaten-down expectations, global growth will surprise on the upside in 2023. Investors should overweight equities for now but look to turn more defensive in the second half of the year.

How to play China's reopening? What are the dichotomies in the performance of China's plays in financial markets? Why has the Chinese central bank tightened liquidity since October and what has been the impact on local rates and the RMB? Is global growth about to bottom? What is the outlook for EM stocks, currencies, credit markets as well as the broad-trade weighted US dollar?

China's economic recovery will be led by consumer spending on services rather than the industrial sector. The current equity market leadership – outperformance by tech stocks – is unsustainable. Persistent deflationary forces will compel policymakers to inject more liquidity and bring down interest rates to reflate the economy. Hence, the RMB will resume its decline against the USD soon.