Equities

In this <i>Strategy Outlook</i>, we present the major investment themes and views we see playing out next year and beyond.

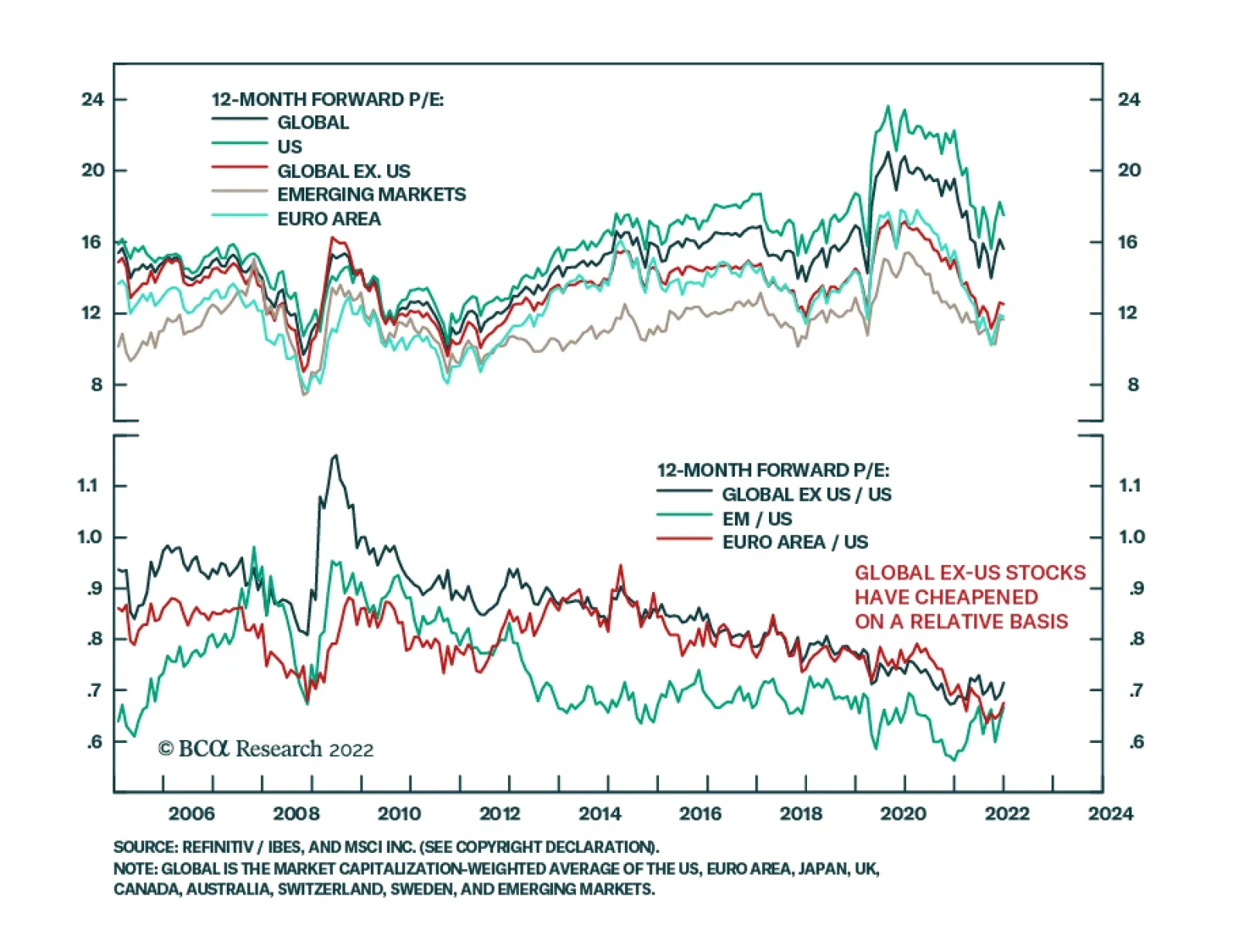

For the first time in decades, the Fed is raising rates while the US Leading Economic Indicator has fallen into contractionary territory and the global manufacturing PMI’s new orders sub-index has dropped below 50. Hence, the outlook for global stocks is currently poor. However, the underperformance of EM equities versus the US is in a late stage. We are putting EM stocks on an upgrade watch list and recommend buying EM domestic bonds opportunistically.

The pandemic gave older Americans and Brits a massive carrot and stick to retire early. The carrot being a surge in wealth, the stick being a risk to health. In other major economies, the carrots and sticks were smaller or non-existent. Hence, the shortage of older workers, and the resulting wage inflation, is a specific US and UK problem. We go through the important economic and investment implications for 2023.

Investors should maintain a conservative and defensive strategy until recession risks are clearly reduced.

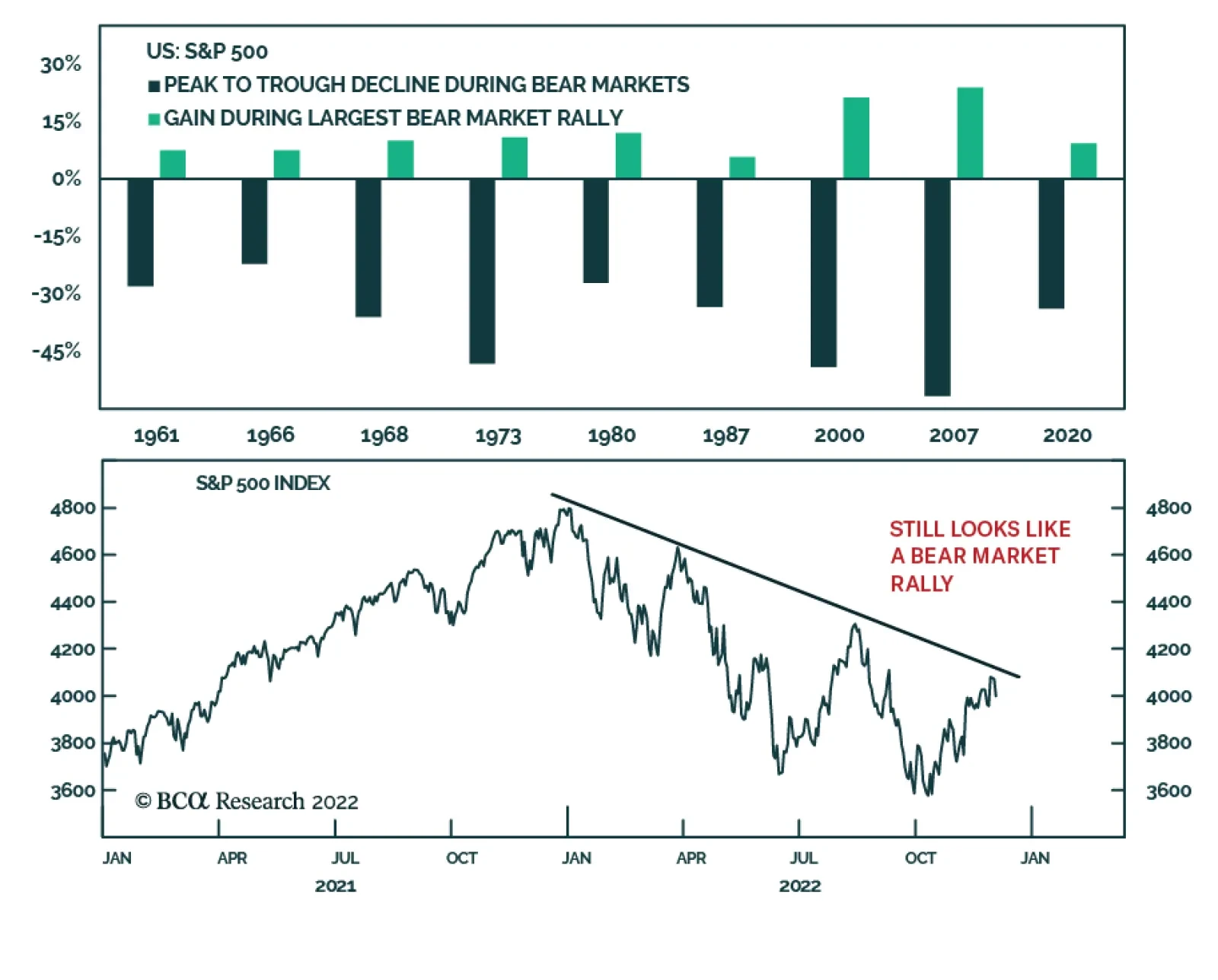

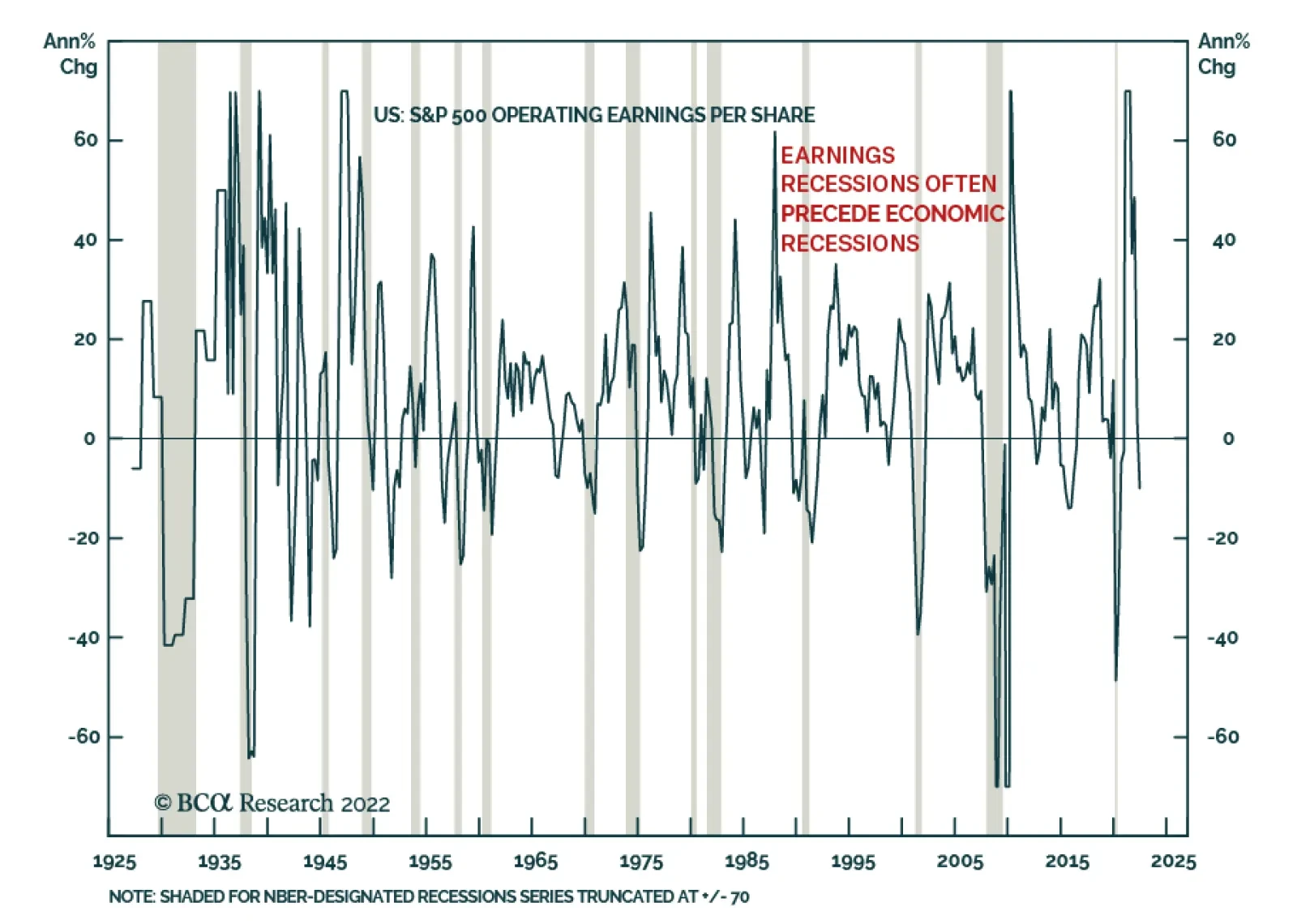

2023 will be another challenging year for the US equity market, characterized by the Fed’s battle with inflation, slowing economic growth, and earnings contraction. The S&P 500 is likely to reach new lows in the first half of the year falling as much as 20-25%, only to rebound sharply in the second half, once all the bad news is priced in.

Labor market strength and consumers’ evident willingness to dip into their pandemic savings keep our optimistic consumer thesis intact. We remain tactically overweight equities.

European inflation will decline through 2023, which will greatly help households and consumption. But can European inflation remain low after that?