Equities

China is on the verge of experiencing a full range of deflation. Poor domestic demand will likely continue into 1H 2023 amid the ailing housing market, subdued private-sector sentiment and the zero-Covid policy, warranting a cautious stance on Chinese equities.

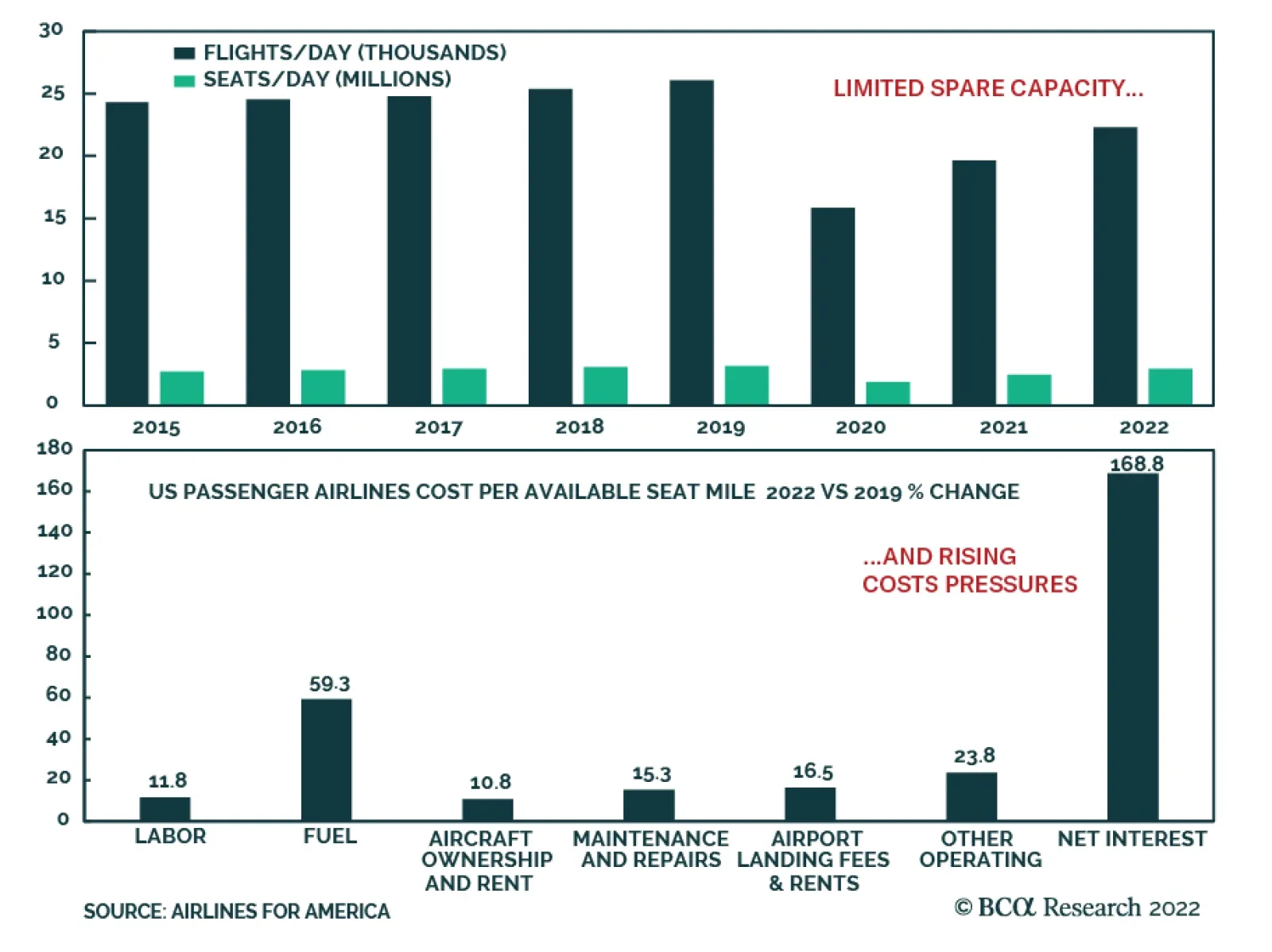

Airlines have staged an impressive recovery this year, exceeding all expectations. While companies are optimistic, we are cautious. Just as pent-up demand for travel will fade, headwinds from slowing growth and high inflation will intensify. While it is highly likely that Airlines will continue to rally into the yearend, we will stick to our underweight as our three-to-six-month outlook remains negative.

The latest CPI and PPI releases, the modestly less hawkish turn in Fed officials’ comments and evidence that consumers continue to spend with some relish support our constructive near-term views on equities and the economy.

Go long the Kensho Space index over a cyclical horizon on the back of growing public and private investment, rising national security interests, declining sector costs, and heightened geopolitical risk.

The kinked supply framework helps explain why US inflation rose so suddenly shortly after the pandemic began and why the economy is likely to experience a benign disinflation over the next six months.

The conditions for a sustainable rally in Chinese stocks have not been met. In this report we discuss the four signposts which we will closely monitor to gauge when it will be warranted to upgrade our stance on Chinese equities both in absolute terms and relative to the global stock benchmark.