Equities

Falling inflation will allow bond yields to decline in the major economies over the next few quarters. As such, we recommend that investors shift their duration stance from underweight to neutral over a 12 month-and-longer horizon and to overweight over a 6-month horizon. Structurally, however, a depletion of the global savings glut could put upward pressure on yields.

In Section I, we note that while recent inflation developments point to some supply-side and pandemic-related disinflation, they also point to potentially stickier inflation over the coming several months. The inflation, monetary policy, and geopolitical outlook remains sufficiently risky that an overweight stance towards equities within a global multi-asset portfolio is not justified, and we continue to recommend a neutral stance for now. This month’s Section II is a guest piece written by Martin Barnes. Martin, who retired from BCA Research as Chief Economist last year after a long and illustrious career, discusses the outlook for government debt and the possibility of an eventual crisis.

We recommend that investors use the following framework to think about whether potential disinflation would be bullish or bearish for share prices: disinflation will prove to be bullish for global share prices if it is due to an improvement in supply-side dynamics, but bearish if it is demand driven. We believe it is the latter.

It takes time for wage inflation to die. So, if 2022 was the year that central banks’ monster tightening killed bond and stock market valuations, then 2023 will be the year that it finally reaches the economy and kills profits, jobs, and the wage inflation that has so far refused to die. This means that commodity prices have substantial further downside, while healthcare relative performance has substantial further upside.

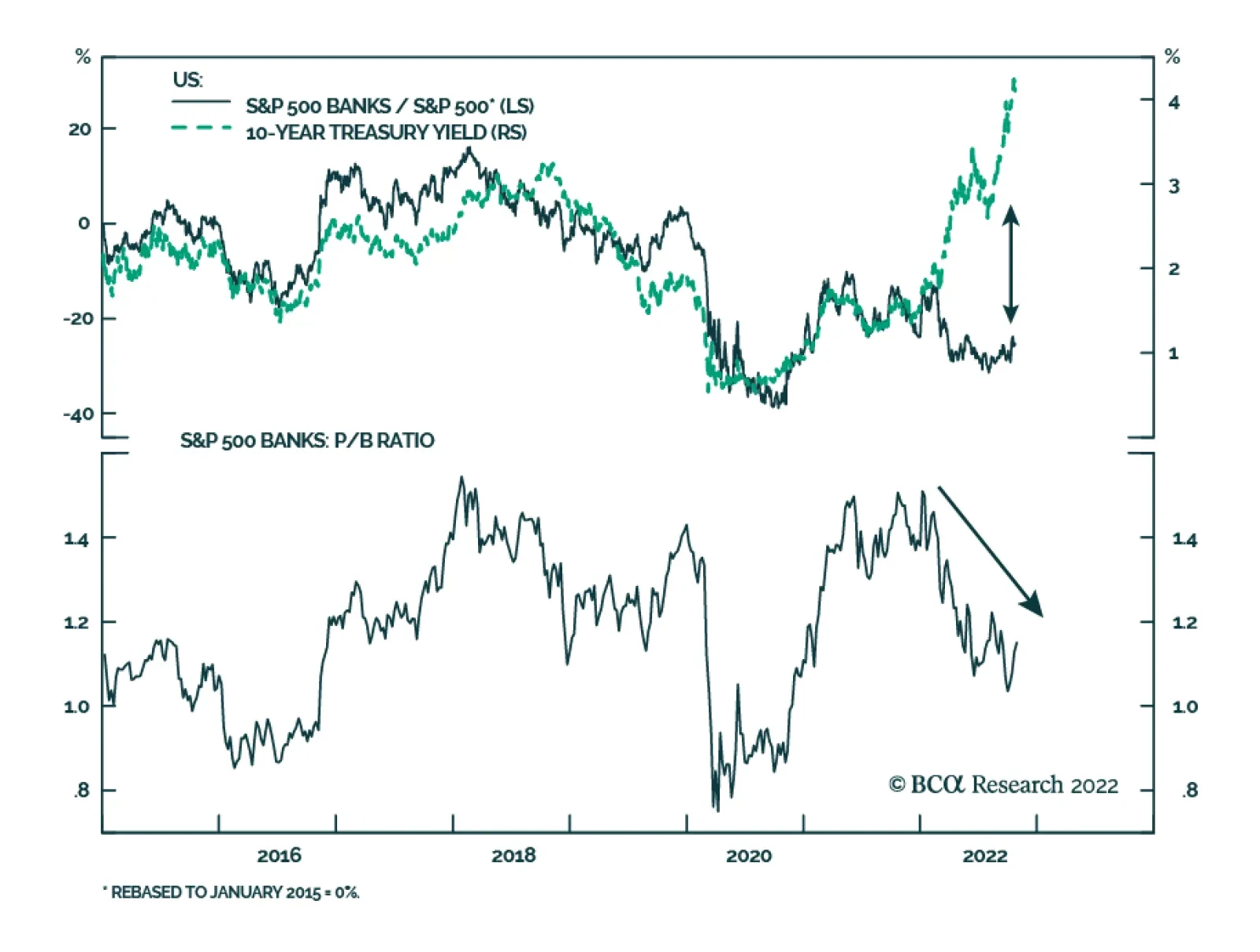

On their third quarter earnings calls, the largest banks indicated that their household and business customers remain in surprisingly robust shape. We interpret their observations as supporting our constructive near-term take on the economy and financial markets.

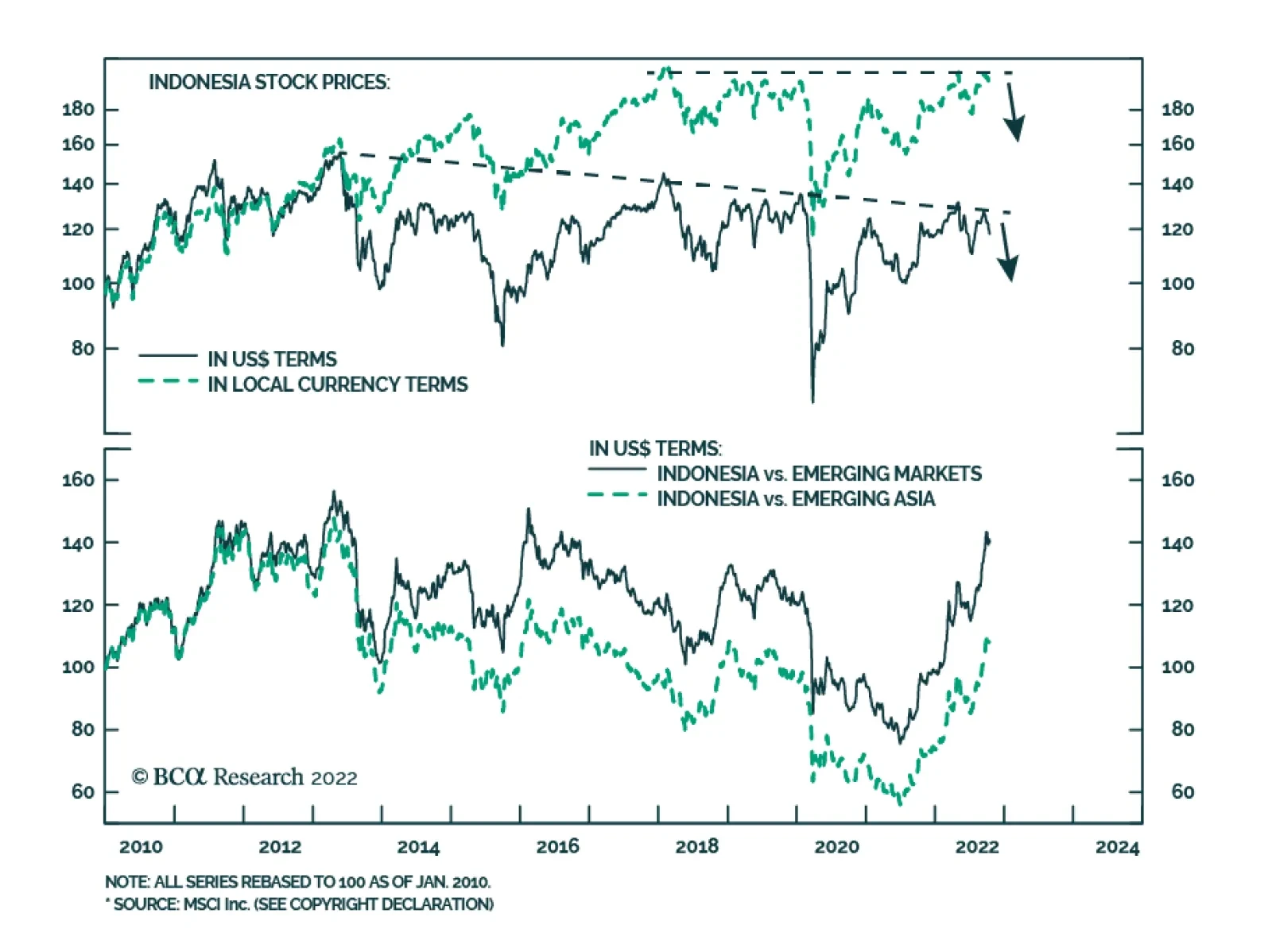

Favor US and Southeast Asian stocks over global stocks. Stay underweight China, Hong Kong, and Taiwan.

The September CPI report was disappointing, but we still see several signs pointing to a rapid decline in inflation. Our constructive near-term view on stocks and the economy remains intact.