Equities

Executive Summary The Fed will continue to hike rates at a time when global trade is contracting. Earlier this week, Fed Chairman Jerome Powell reiterated that the Fed will not hesitate to hike rates until core consumer price inflation gets closer to 2%. Given that US core consumer price inflation is currently at around 5-6%, a mere rollover in core inflation from current levels will not be enough for the Fed to tone down its hawkishness. Besides, according to Powell, US financial conditions are not yet at a level that is consistent with inflation coming down substantially. China will stick to its dynamic zero-COVID policy this year. The economy will continue to underwhelm as the magnitude and nature of stimulus measures announced thus far are not adequate to produce a recovery. Industrial metal prices and global material stocks are at risk of gapping down. Play these markets on the short side. Commodity Currencies Are Signaling Lower Commodity Prices

Commodity Currencies Are Signaling Lower Commodity Prices

Commodity Currencies Are Signaling Lower Commodity Prices

Bottom Line: It is still dangerous to bottom fish in global equities and risk assets in general. The US dollar has more upside. Continue underweighting EM stocks and credit within global equity and credit portfolios, respectively. Feature The risks to global and EM risk assets are still skewed to the downside. Although investor sentiment on global equities has soured of late, we do not think global or EM equities have made a bottom, and the US dollar has not yet reached an apex. Consequently, absolute-return investors should stay defensive, and global equity portfolios should continue to underweight EM stocks. The Fed and Equities Are Still On A Collision Course Earlier this week, Fed Chairman Jerome Powell reiterated the Fed’s commitment to hiking interest rates until core consumer price inflation gets closer to 2%. Notably, in his speech at a WSJ event on May 17, Powell noted: “This is not a time for tremendously nuanced readings of inflation”… “We need to see inflation coming down in a convincing way. Until we do, we’ll keep going.” Given that US core consumer price inflation is currently at around 5-6%, a mere rollover in core inflation from current levels will not be enough for the Fed to tone down its hawkishness. Chart 1US Core Inflation Will Roll Over But Stay Above 3.5-4% For Now

US Core Inflation Will Roll Over But Stay Above 3.5-4% For Now

US Core Inflation Will Roll Over But Stay Above 3.5-4% For Now

Chart 1 shows the average of core median CPI, core trimmed-mean CPI and core sticky CPI, which are better indicators of genuine inflationary pressures because they are less affected by outliers. Even though core CPI inflation ticked down in April, other core measures such as core median CPI, core trimmed-mean CPI and core sticky CPI continued to rise. These core inflation measures are not likely to ease back to 2% unless economic growth falls below its potential. In his same speech, Chairman Powell also asserted: “We will go until we feel like we are at a place where we can say, ‘Yes, financial conditions are at an appropriate place. We see inflation coming down.’ We will go to that point, and there will not be any hesitation about that.” This means that US financial conditions have not yet tightened enough for the Fed to back down on its hawkishness. Finally, we have been arguing that a wage-price spiral has developed in the US as the labor market has become very tight (Chart 2, top panel). Wages and unit labor costs have been surging. Unit labor costs are the most important driver of US core CPI (Chart 2, bottom panel). Therefore, it will be impossible for the Fed to bring down core inflation toward 2% without a retrenchment in the labor market, i.e., layoffs. Rising unemployment will in turn weigh on household income growth and consumption. Chart 2The US Labor Market Is Very Tight And Wage Growth Is Accelerating

The US Labor Market Is Very Tight And Wage Growth Is Accelerating

The US Labor Market Is Very Tight And Wage Growth Is Accelerating

The cost of borrowing for companies is rising globally, and these periods often coincide with equity selloffs. Notably, surging US high-yield ex-energy corporate bond yields herald lower US share prices ahead (Chart 3, top panel). Similarly, rising EM corporate bond yields foreshadow a further decline in EM ex-TMT share prices (Chart 3, bottom panel). Chart 3Rising Corporate Bond Yields Are Bearish For Stocks

Rising Corporate Bond Yields Are Bearish For Stocks

Rising Corporate Bond Yields Are Bearish For Stocks

On the whole, the Fed and many other central banks will be hiking interest rates at a time when global trade volumes are contracting in H2 2022. As discussed in our report A Whiff Of Stagflation? US and EU imports of consumer goods are set to shrink following the pandemic boom. Chart 4Global Export/Manufacturing Are Heading Into Contraction

Global Export/Manufacturing Are Heading Into Contraction

Global Export/Manufacturing Are Heading Into Contraction

Meantime, rolling lockdowns and extremely weak income growth are depressing domestic demand in China. High food and energy prices as well as rising interest rates are weighing on EM ex-China consumption. The sharp underperformance of global cyclicals equities versus global defensive sectors corroborates our expectation that global manufacturing activity will contract (Chart 4). The trade-weighted US dollar typically benefits from both Fed hikes and a global trade slump. As long as the Fed is hawkish and global exports are contracting, the greenback will continue to appreciate. For now, the US dollar remains in a strong position for further appreciation, especially versus EM currencies (Chart 5). Consistently, the selloff in broad EM risk assets is not yet over. Chart 5EM Currencies: More Downside

EM Currencies: More Downside

EM Currencies: More Downside

A major reversal in the trade-weighted dollar will be a signal that the global macro backdrop is improving and that global share prices and EM risk assets are bottoming. Bottom Line: Although equities have become oversold and investor sentiment is depressed, any rebound will prove to be short lived. The Fed will continue to hike rates at a time when global trade is about to shrink. The global/EM equity selloff has further to run. China: Ordinary Stimulus Despite Extraordinary Conditions Only one thing is currently certain in China: authorities are committed to the dynamic zero-COVID policy. However, most experts outside China believe that it will be very difficult to wholly limit the spread of the easily transmissible Omicron variants, even with such stringent mainland containment policies. As a result, rolling lockdowns are the most likely scenario for China’s regions and cities in 2022. These lockdowns will depress household income, confidence and consumption. Private business investment and hiring will also tank. Have authorities provided enough stimulus to support a recovery in H2 2022? We do not think so. Chinese stimulus has so far been ordinary in nature and in magnitude. Policy easing will likely prove to be insufficient to lift the economy out of the current extraordinary slump. First, Chinese exports are set to shrink in H2 as US and EU consumption of consumer goods revert to their pre-pandemic trend. Demand from EM will remain weak. Second, rising unemployment and under-employment is hindering household income. Generous cash transfers are needed to offset this hit to income. Not only did aggregate retail sales collapse in April, but online sales of goods and service also plunged (Chart 6). It is hard to imagine that private businesses will be investing when consumer spending and exports are weak. Our proxies for the marginal propensity to spend for households and enterprises continue to fall (Chart 7). Chart 6China: Even Online Retail Sales Are Shrinking

China: Even Online Retail Sales Are Shrinking

China: Even Online Retail Sales Are Shrinking

Chart 7China: Household And Enterprise Propensity To Spend Have Been Declining

China: Household And Enterprise Propensity To Spend Have Been Declining

China: Household And Enterprise Propensity To Spend Have Been Declining

Critically, China’s credit impulse, excluding government bond issuance, remains in negative territory (Chart 8). Third, China’s property market is frail. Despite modest policy easing for the real estate market, sentiment among home buyers and developers remains downbeat. Given that the housing sector faces structural headwinds, odds are that buyers and developers might not react to the modest property market easing that authorities have so far provided. It is worth noting that Chinese property stocks seem to have had a structural breakdown, and offshore corporate bonds of real estate developers remain in a bear market (Chart 9). These market patterns corroborate that China's housing market has experienced a structural breakdown. Chart 8Chinese Stimulus Has So Far Been Tame

Chinese Stimulus Has So Far Been Tame

Chinese Stimulus Has So Far Been Tame

Chart 9Chinese Property Market Has Experienced A Structural Breakdown

Chinese Property Market Has Experienced A Structural Breakdown

Chinese Property Market Has Experienced A Structural Breakdown

Finally, even though infrastructure spending is being ramped up, it will prove to be insufficient for the economy to recover from a deep slump. Local governments are facing a major financing shortfall. Land sales – which make up about 40% of local government revenues – have dried up. This will hinder local governments’ ability to finance infrastructure projects. As to Chinese equities, internet/platform stocks have become oversold. However, their long-term outlook remains dismal. As we have been arguing since late 2020, the fundamental case for their de-rating remains intact. This week’s meeting between government officials and technology companies has not produced any positive news. Although the tone from authorities was more balanced, they did not offer any relief from already imposed regulations. Chart 10Implications Of China's Common Prosperity Policies

Implications Of China's Common Prosperity Policies

Implications Of China's Common Prosperity Policies

Looking forward, implementing common prosperity policies will be the primary objective of the Communist Party in the coming years. These policies will assure that labor’s share of income will rise further at the expense of corporate profits. Chart 10 demonstrates that the share of labor in national income has been rising since 2011. Conversely, the share operating profits peaked in 2011 and has dropped to a 30-year low. These dynamics will persist as income will continue to be redistributed from shareholders to labor in the majority of industries/companies in China. This is an unfriendly outlook for shareholders, especially foreign ones. Bottom Line: Chinese policy stimulus has so far been insufficient. The economy is in a deep slump, and share prices remain at risk of further decline. Short Industrial Metals And Material Stocks Chart 11Chinese Imports Of Metals Was Shrinking In 2021

Chinese Imports Of Metals Was Shrinking In 2021

Chinese Imports Of Metals Was Shrinking In 2021

Industrial metals’ resilience last year in the face of shrinking Chinese import volumes was unusual (Chart 11). This resilience was probably due to robust DM demand for goods, supply bottlenecks and investors buying commodities as an inflation hedge. As we elaborated in the April 28 report, risks to industrial metals are skewed to the downside. This is despite the fact that agriculture prices will likely rise further, and energy prices will remain volatile due to the geopolitical situation. We continue to recommend investors underweight/short materials stocks and industrial metals for the following reasons: It is ill-advised to play the US inflation story by being long industrial metals and materials stocks. As shown in Chart 2 above, US unit labor costs are driving core inflation, not industrial metals. China accounts for 50-55% of global industrial metal consumption, and since early 2021 the key risk in China has been decelerating demand/deflation not inflation. In fact, commodities have become a crowded hedge against inflation and a global growth slowdown poses a substantial risk to industrial metals. Chart 12 demonstrates that Chinese materials stocks have plunged. We read this as a warning sign for global materials because China is by far the largest consumer of raw materials (excluding energy). Chart 12Chinese Material Stocks Are Signaling Trouble For Global Materials

Chinese Material Stocks Are Signaling Trouble For Global Materials

Chinese Material Stocks Are Signaling Trouble For Global Materials

When share prices of customers are falling, equity prices of suppliers will likely follow. Chart 13 shows that over the past 200 years raw material prices in real US dollar terms (deflated by US headline CPI) have oscillated around a well-defined downtrend. The pandemic surge in commodity prices has pushed raw material prices to two standard deviations above this long-term trend. Chart 13Raw Material Prices (In Real Terms) Are At The Upper End Of A 200-Year Downtrend

Raw Material Prices (In Real Terms) Are At The Upper End Of A 200-Year Downtrend

Raw Material Prices (In Real Terms) Are At The Upper End Of A 200-Year Downtrend

Historically, commodity rallies (and even their secular bull markets) ended when prices reached this threshold. Hence, odds are that industrial commodities might hit a soft spot. Energy prices remain a wild card due to geopolitics. It is critical to note that the raw materials price index shown in Chart 13 does not include energy, gold and semi-precious metals. Finally, shrinking global trade volumes are also negative for raw materials. The average of AUD, NZD and CAD points to lower industrial metal prices (Chart 14). Chart 14Commodity Currencies Are Signaling Lower Commodity Prices

Commodity Currencies Are Signaling Lower Commodity Prices

Commodity Currencies Are Signaling Lower Commodity Prices

Chart 15Bearish Technical Patterns: BHP Share Price And Copper

Bearish Technical Patterns: BHP Share Price And Copper

Bearish Technical Patterns: BHP Share Price And Copper

The share price of BHP, the world’s largest mining company, has put in a major top and is now gapping down (Chart 15, top panel). Copper prices have broken below their 200-day moving average that served as a support in the past 12 months (Chart 15, bottom panel). These market profiles point to more downside. We continue to recommend that investors play this theme in the following ways: Short copper or short copper / long gold; Short global materials / long global industrials; Short ZAR / long USD. Also, we downgraded Brazil early this week partly due to expectations of lower iron ore prices and souring investor attitude toward commodity plays in general. Investment Conclusions Global and EM equities have entered a capitulation phase. It is still dangerous to bottom fish in global equities and risk assets in general. Continue underweighting EM stocks and credit within global equity and credit portfolios, respectively. The US dollar has more upside. Continue shorting the following EM currencies versus the USD: ZAR, PLN, HUF, COP, PEN, PHP and IDR. As we discussed in a recent report, we are approaching a major buying opportunity in EM local currency bonds. However, the US dollar needs to peak for that to transpire. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Strategic Themes (18 Months And Beyond) Equities Cyclical Recommendations (6-18 Months) Cyclical Recommendations (6-18 Months)

Next Thursday May 26, we will hold the BCA Debate – High Inflation: Here To Stay,Or Soon In The Rear-View Mirror? – a Webcast in which I will debate my colleague, Chief Commodity & Energy Strategist, Bob Ryan on the outlook for inflation, and take the side that inflationary fears will soon recede. I do hope you can join us. As such, the debate will replace the weekly report, though we will renew the fractal trading watchlist on our website. Dhaval Joshi Executive Summary The second quarter’s synchronised sell-off in stocks, bonds, inflation protected bonds, industrial metals and gold is an extremely rare star alignment. The last time that the ‘everything sell-off’ star alignment happened was in early 1981 when the Paul Volcker Fed ‘broke the back’ of inflation and turned stagflation into an outright recession. In 2022, the Jay Powell Fed risks doing the same. If history repeats itself, then the template of 1981-82 could provide a useful guide for 2022-23. In which case, bond prices are now entering a bottoming process. Stocks would bottom next. While the near term outlook is cloudy, we expect stock prices to be higher on a 12-month horizon, especially long-duration stocks that are most sensitive to bond yields. But just as in 1981-82, the biggest casualty will be industrial metals, which are likely to suffer at least double-digit losses over the coming year. Fractal trading watchlist: FTSE 100 versus Stoxx Europe 600, Czech Republic versus Poland, Food and Beverages, US REITS versus Utilities, CNY/USD. 2022-23 Could Be An Echo Of 1981-82

2022-23 Could Be An Echo Of 1981-82

2022-23 Could Be An Echo Of 1981-82

Bottom Line: The 1981-82 template for 2022-23 suggests that bonds will bottom first, followed by stocks. But steer clear of gold and industrial metals. Feature Investors have had a torrid time in the second quarter, with no place to hide.1 Stocks are down -10 percent. Bonds are down -6 percent. Inflation protected bonds are down -6 percent. Industrial metals are down -13 percent. Gold is down -6 percent. To add insult to injury, even cash is down in real terms, because the interest rate is well below the inflation rate! (Chart I-1) Chart I-1The 'Everything Sell-Off' In 2022 Last Happened In 1981, When Stagflation Morphed Into Recession

The 'Everything Sell-Off' In 2022 Last Happened In 1981, When Stagflation Morphed Into Recession

The 'Everything Sell-Off' In 2022 Last Happened In 1981, When Stagflation Morphed Into Recession

Such a star alignment of asset returns, in which stocks, bonds, inflation protected bonds, industrial metals, and gold all sell off together, is unprecedented. In the eighty calendar quarters since the inflation protected bond market data became available in the early 2000s there has never been a quarter with an ‘everything sell-off’. Everything Has Sold Off, But Does That Make Sense? The rarity of an ‘everything sell-off’ is because there are virtually no economic or financial scenarios in which all five asset-classes should fall together (Chart I-2 and Chart I-3). Chart I-2An 'Everything Sell-Off' Is Extremely Rare

An 'Everything Sell-Off' Is Extremely Rare

An 'Everything Sell-Off' Is Extremely Rare

Chart I-3An 'Everything Sell-Off' Is Extremely Rare

An 'Everything Sell-Off' Is Extremely Rare

An 'Everything Sell-Off' Is Extremely Rare

A scenario dominated by rising inflation is bad for bonds, but good for inflation protected bonds, especially relative to conventional bonds. Yet inflation protected bonds have not outperformed either in absolute or relative terms. A scenario of rising inflation should also support the value of stocks, industrial metals and certainly gold, given that all three are, to varying degrees, ‘inflation hedges.’ Yet the prices of stocks, industrial metals, and gold have all plummeted. The rarity of an ‘everything sell-off’ is because there are virtually no economic or financial scenarios in which all asset classes should fall together. Conversely, a scenario dominated by slowing growth is bad for industrial metal prices, but good for conventional bond prices – as bond yields decline on diminished expectations for rate hikes. Yet conventional bonds have sold off. What about a scenario dominated by both rising inflation and slowing growth – which is to say, stagflation? In this case, we would expect inflation protected bonds to perform especially well. Meanwhile, with the economy still growing, the prices of industrial metals should not be collapsing, as they have been recently. In a final scenario of an imminent recession we would expect stocks, industrial metals and even gold to sell off, but conventional bonds to perform especially well. The upshot is there are virtually no economic scenarios in which stocks, bonds, inflation protected bonds, industrial metals, and gold plummet together, as they have recently. So, what’s going on? To answer, we need to take a trip back to the 1980s. 1981 Was The Last Time We Had An ‘Everything Sell-Off’ Inflation protected bonds did not exist before the late 1990s. But considering the other four asset-classes – stocks, bonds, industrial metals, and gold – to find the last time that they all fell together we must travel back to 1981, the time of Margaret Thatcher, Ronald Reagan, and the Paul Volcker Fed. And suddenly, we discover spooky similarities with the current Zeitgeist. Just like today, the world’s central banks were obsessed with ‘breaking the back’ of inflation, which, like a monster in a horror movie, kept appearing to die before coming back with second and third winds (Chart I-4). Chart I-4In 1981, Just As In 2022, Central Banks Would 'Do Whatever It Takes' To Kill Inflation

In 1981, Just As In 2022, Central Banks Would 'Do Whatever It Takes' To Kill Inflation

In 1981, Just As In 2022, Central Banks Would 'Do Whatever It Takes' To Kill Inflation

Just like today, the central banks were desperate to repair their badly damaged credibility in managing the economy. As the biography “Volcker: The Triumph of Persistence” puts it: “He restored credibility to the Federal Reserve at a time it had been greatly diminished.” And just like today, central bankers hoped that they could pilot the economy to a ‘soft landing’, though whether they genuinely believed that is another story. Asked at a press conference if higher interest rates would cause a recession, Volcker replied coyly “Well, you get varying opinions about that.” 2022 has spooky similarities with 1981. In fact, in its single-minded aim ‘to do whatever it takes’ to kill inflation, the Volcker Fed hiked the interest rate to near 20 percent, thereby triggering what was then the deepest economic recession since the Depression of the 1930s (Chart I-5 and Chart I-6). With hindsight, it was a price worth paying because the economy then began a quarter century of low inflation, steady growth, and mild recessions – a halcyon period for which the Volcker Fed’s aggressive tightening in the early 1980s have been lauded. Chart I-5In 1981, The Fed Hiked Rates To Near 20 Percent...

In 1981, The Fed Hiked Rates To Near 20 Percent...

In 1981, The Fed Hiked Rates To Near 20 Percent...

Chart I-6...And Thereby Morphed Stagflation Into Recession

...And Thereby Morphed Stagflation Into Recession

...And Thereby Morphed Stagflation Into Recession

Granted, the problems of 2022 are a much scaled down version of those in 1981, yet there are spooky similarities – a point which will not have gone unnoticed by the current crop of central bankers. It is no secret that Jay Powell is a big fan of Paul Volcker. The Echoes Of 1981-82 In 2022-23 The answer to why everything sold off in early 1981 is that central banks took their economies from stagflation to outright recession, and the risk is that the same happens again in 2022-23 (Chart I-7). Chart I-7The Echoes Of 1981-82: Aggressive Rate Hikes In 2022-23 Will Morph Stagflation Into Recession

The Echoes Of 1981-82: Aggressive Rate Hikes In 2022-23 Will Morph Stagflation Into Recession

The Echoes Of 1981-82: Aggressive Rate Hikes In 2022-23 Will Morph Stagflation Into Recession

In the transition from stagflation fears to recession fears, everything sells off because first the stagflation casualties get hammered, and then the recession plays get hammered. This leaves investors with no place to hide, as no mainstream asset is left unscathed. Just as in 1981, a transition from stagflation fears to recession fears likely explains the recent ‘everything sell-off’ because the sell-off in April was most painful for the stagflation casualties – bonds. Whereas, the sell-off in May has been most painful for the recession casualties – industrial metals and stocks. In a stagflation that morphs to recession, everything sells off. What happens next? The template of 1981-82 could provide a useful guide. Bond prices bottomed first, in the late summer of 1981, as it became clear that the economy was entering a downturn which would exorcise inflation. Of the three other asset classes – all recession casualties – stocks continued to remain under pressure for the next few months but were higher 12 months later. Gold fell another 30 percent, though rebounded sharply in 1982. But the greatest pain was in the industrial metals, which fell another 30 percent and did not recover their highs for several years (Chart I-8). Chart I-82022-23 Could Be An Echo Of 1981-82

2022-23 Could Be An Echo Of 1981-82

2022-23 Could Be An Echo Of 1981-82

2022-23 could be an echo of 1981-82, with bond prices now entering a bottoming process. Stocks would bottom next, with one difference being a quicker recovery than in 1981-82 because of their higher sensitivity to bond yields. While the near term outlook is cloudy, we expect stock prices to be higher on a 12 month horizon, especially long-duration stocks that are most sensitive to bond yields. But just as in 1981-82, the biggest casualty of a stagflation that morphs into a recession will be the overvalued industrial metals, which are likely to suffer at least double-digit losses over the coming year. Fractal Trading Watchlist This week’s new additions are Czech Republic versus Poland, and Food and Beverages versus the market, which appear overbought. And US REITS versus Utilities, and CNY/USD, which appear oversold. Finally, our new trade recommendation is to underweight the FTSE 100 versus the Stoxx Europe 600. The resource heavy FTSE 100 is especially vulnerable to our anticipated sell-off in commodities, and its recent outperformance is at a point of fragility that has marked previous turning points (Chart I-9). Set the profit target and symmetrical stop-loss at 5 percent. Chart I-9FTSE 100 Outperformance Is Near Exhaustion

FTSE 100 Outperformance Is Near Exhaustion

FTSE 100 Outperformance Is Near Exhaustion

Fractal Trading Watchlist: New Additions Chart I-10Czech Outperformance Near Exhaustion

Czech Outperformance Near Exhaustion

Czech Outperformance Near Exhaustion

Chart I-11Food And Beverage Outperformance Near Exhaustion CHART 1

Food And Beverage Outperformance Near Exhaustion CHART 1

Food And Beverage Outperformance Near Exhaustion CHART 1

Chart I-12US REITS Are Oversold Versus Utilities CHART 12

US REITS Are Oversold Versus Utilities CHART 12

US REITS Are Oversold Versus Utilities CHART 12

Chart I-13CNY/USD At A Support Level

CNY/USD At A Support Level

CNY/USD At A Support Level

Chart 1The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

Chart 2The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

Chart 3AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

Chart 4Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Chart 5Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Chart 6US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

Chart 7A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Chart 8Biotech Is A Major Buy

Biotech Is A Major Buy

Biotech Is A Major Buy

Chart 9CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

Chart 10Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Chart 11Norway's Outperformance Could End

Norway's Outperformance Could End

Norway's Outperformance Could End

Chart 12Greece's Brief Outperformance To End

Greece's Brief Outperformance To End

Greece's Brief Outperformance To End

Chart 13BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

Chart 14The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

Chart 15The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

Chart 16Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Chart 17Homebuilders Versus Healthcare Services Has Turned

Homebuilders Versus Healthcare Services Has Turned

Homebuilders Versus Healthcare Services Has Turned

Chart 18Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Chart 19The Rally In USD/EUR Could End

The Rally In USD/EUR Could End

The Rally In USD/EUR Could End

Chart 20The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

Chart 21A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

Chart 22FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

Chart 23Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Chart 24The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

Chart 25The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

Chart 26Czech Outperformance Near Exhaustion

Czech Outperformance Near Exhaustion

Czech Outperformance Near Exhaustion

Chart 27Food And Beverage Outperformance Near Exhaustion CHART 1

Food And Beverage Outperformance Near Exhaustion CHART 1

Food And Beverage Outperformance Near Exhaustion CHART 1

Chart 28US REITS Are Oversold Versus Utilities CHART 12

US REITS Are Oversold Versus Utilities CHART 12

US REITS Are Oversold Versus Utilities CHART 12

Chart 29CNY/USD At A Support Level

CNY/USD At A Support Level

CNY/USD At A Support Level

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 The returns are based on the S&P 500, the 10-year T-bond, the 10-year Treasury Inflation Protected Security (TIPS), the LMEX index, and gold. Fractal Trading System Fractal Trades

Markets Echo 1981, When Stagflation Morphed Into Recession

Markets Echo 1981, When Stagflation Morphed Into Recession

Markets Echo 1981, When Stagflation Morphed Into Recession

Markets Echo 1981, When Stagflation Morphed Into Recession

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

BCA Research’s European Investment Strategy service concludes that a temporary pullback in the performance of UK equities relative to Euro Area stocks is likely in the second half of 2022. UK stocks enjoy a structural tailwind relative to Euro Area shares.…

Executive Summary UK Stocks Are Close To A Bottom

UK Stocks Are Close To A Bottom

UK Stocks Are Close To A Bottom

The UK economic outlook has greatly deteriorated. Weak global growth and punishing energy inflation will cause activity to contract over the next 12 months. Cost-push pressures will drag inflation above 10% in 2022. Moreover, demand-pull inflation highlights problems with the supply-side of the economy. UK yields have downside relative to those in the Euro Area. GBP/USD will bottom once global stock prices find a floor. EUR/GBP possesses more upside. UK stocks will enjoy a structural tailwind relative to their Eurozone counterparts as a result of a secular bull market in commodity prices. Nonetheless, UK equities are likely to underperform in the second half of 2022. UK small-cap stocks are massively oversold compared to large-cap shares; however, a peak in energy inflation must take place for small-cap equities to stage a rebound. TACTICAL INCEPTION DATE RETURN SINCE INCEPTION (%) COMMENT Overweight UK Gilts Within European Fixed-Income Portfolios 05/16/2022 Cyclical Buy European Healthcare Equities / Sell UK Healthcare Equities 05/16/2022 Tactical Buy European Financials Equities / Sell UK Financials Equities 05/16/2022 Tactical Bottom Line: British Gilts will outperform because of the weakness in UK economic activity, but the trade-weighted pound will remain under pressure. The performance of UK large-cap names is mostly independent from the state of the British economy. The commodity secular bull market will create a potent tailwind for this market. However, a better entry point lies ahead. The Bank of England’s (BoE) latest policy meeting was a cold shower for market participants and their aggressive interest rate pricing in the SONIA curve. Money markets expected a peak in the Bank Rate of 2.7% in 2023, but the BoE’s new Market Participants Survey is calling for it to peak at 1.75% before easing off to 1.5% in 2024. The UK economy is in trouble. Inflation is high and broad-based, which explains why investors are pricing in such an aggressive path for the Bank Rate. Yet, economic activity is weakening and could even contract in early 2023. The BoE clearly puts more weight on growth than investors do. What are the implications of the inflation, growth, and policy outlook for British assets? BCA has upgraded its view on UK bonds to overweight within global fixed income portfolios. We expect more softness in the pound versus the euro. UK large-cap stocks will continue to trade in line with energy dynamics, which means it is still too early to buy British small-cap equities. In the meantime, UK financial and healthcare names will underperform their Euro Area counterparts. Growth To Weaken Further The -0.1% month-over-month GDP contraction in March underscores that UK economic activity has already decelerated sharply. However, the deterioration is only starting. Most sectors of the economy show ominous signs for the quarters ahead. Consumer Sector The biggest hurdle facing UK consumers, like most of their European neighbors, is the surge in inflation, particularly energy and food prices. Safety nets are looser than on the continent, and UK households’ real disposable income are contracting sharply. The impact of this weakening of activity is already visible. UK consumer confidence is falling in line with the knock to real disposable income (Chart 1, top panel). Moreover, real retail sales have already slowed sharply, and the BRC Like-For-Like Retail Sales measure is contracting on an annual basis (Chart 1, bottom panel). As a result, the outlook for consumption is worsening. Ofgem, the UK gas and electricity market regulator, lifted its energy price cap by 54% on April 1st and plans to increase it again by an expected 40% in October. Consequently, the BoE anticipates the share of households’ disposable income spent on energy to hit 7.7% by the end of the year — its highest level since the early 1980s (Chart 2). Chart 1Falling Real Incomes Hurt

Falling Real Incomes Hurt

Falling Real Incomes Hurt

Chart 2Intensifying Energy Drag

Intensifying Energy Drag

Intensifying Energy Drag

The savings cushion developed during the pandemic will not be enough to prevent weaker retail sales. More than 40% of households plan to dip into their existing savings and curtail their savings rate; however, UK excess savings skew heavily toward the richer households. Poorer households with low savings are the ones who spend the largest share of their income on energy (Chart 3), and they are also the ones with a higher marginal propensity to consume. Thus, the knock to these households portends further weakness in consumption volumes. Chart 3The Poor Are Hit Harder

Is UK Stagflation Priced In?

Is UK Stagflation Priced In?

Chart 4No Salvation From Housing

No Salvation From Housing

No Salvation From Housing

Housing is unlikely to save the day. While house prices and housing transactions are robust (Chart 4, top panel), mortgage approvals are declining rapidly and average sales per chartered surveyors are also softening (Chart 4, bottom panels), which suggests housing activity will slow. Rising mortgage rates are a problem. Since January, the quoted rates on mortgages with 90% LTV and 75% LTV are up 65bps and 70bps, respectively, which is hurting housing marginal demand. Moreover, 20% of the UK’s mortgage stock carries variable rates, which further hurts aggregate demand. Business Sector The business sector is also feeling the crunch from rapidly rising energy and input costs. It also dreads the deterioration in consumer sentiment and its implication for future final demand. Chart 5Dwindling Capex Outlook

Dwindling Capex Outlook

Dwindling Capex Outlook

Business confidence is falling abruptly. The CBI Inquiry Business Optimism measure has fallen to its lowest level since the beginning of the pandemic in 2020, when the UK GDP was contracting at a 21% annualized rate (Chart 5). Unsurprisingly, the collapse in business confidence prompted a rapid slowdown in CAPEX. The BoE’s Agents Survey reports that 40% of UK firms have unsustainably low profit margins because of rising input prices and partial pass-through. As a result of financial stress, further capex weakness is likely in the coming quarters. The impact on overall activity of these expanding worries is evident. UK industrial production has slowed very sharply and is now a meager 0.7% on an annual basis. The situation will degrade. Export growth remains strong, which is helping the business sector; however, the rapid slowdown in global industrial production indicates that UK exports will follow suit (Chart 5, second panel). This will have a knock-on effect on corporate profits (Chart 5, bottom panel), which will depress capex further. Other Considerations Chart 6No Offset From The Government

No Offset From The Government

No Offset From The Government

The problems of the private sector may be encapsulated in one indicator. After a surge that boosted GDP, the UK’s nonfinancial private sector’s credit impulse is rapidly contracting (Chart 6), which confirms that risks to activity are building. The public sector will not provide an offset. According to the IMF Fiscal Monitor’s projections, the UK’s fiscal thrust will equal -3.3% of GDP in 2022 and -1.4% in 2023, even after the small giveaways from Chancellor Rishi Sunak’s Spring Statement (Chart 6, bottom panel). Together, these developments confirm our view that UK GDP may also flirt with a recession in the coming 12 months. Bottom Line: The UK economy is facing potent headwinds and activity is set to contract over the coming quarters. Surging energy costs are hurting household consumption and businesses are cutting investment. This time around, government spending is unlikely to come to the rescue, at least not until further pain is inflicted on the UK’s private sector. The BoE expects output to contract in early 2023, with which we agree. Inflation: The Worst Of Both Worlds UK headline inflation is likely to move into double digits territory before year-end. Worrisomely, it will also be more stubborn than that of the Eurozone, because it goes beyond higher food and energy input costs. Essentially, the UK suffers from both the cost-push inflation plaguing the rest of Europe and the demand-pull inflation witnessed in the US. Chart 7Continued Pass-Through

Is UK Stagflation Priced In?

Is UK Stagflation Priced In?

The UK’s cost-push inflation will worsen in the second half of the year and could lift headline CPI above 10% by Q4 2022. Its main driver will be the Ofgem’s second energy cap increase scheduled for October, which is expected to increase household energy costs by 40%. Companies will also try to pass through a greater proportion of their rising costs to their consumers to protect their depleted margins. So far, the BoE’s Agents Survey reveals that on average, UK firms have passed through 80% of their non-labor input cost increases (Chart 7, top panel). In all the sectors surveyed, expected price increases are set to accelerate compared to the past 12 month and may even reach 14% in the manufacturing sector and 8% in the consumer goods sector (Chart 7, bottom panel). Demand-pull inflation is also present in the UK, unlike the rest of Europe, with core CPI at 5.7%, high service inflation, and rapidly rising wage growth. The key problem is an overheating labor market exacerbated by labor supply problems. By the end of 2021, the UK recorded 600 thousand inactive people more than before the pandemic, or individuals who are of working age but outside of the labor force and not seeking a job. This has compressed the labor participation rate to 63%, or the lowest level since the 2011-2012 period (Chart 8). So far, not even rapid wage gains have incentivized these persons to seek employment. The impact of Brexit further curtails the supply of labor. Since the pandemic began, the size of the working age population has decreased by 100 thousand as EU citizens have moved back home (Chart 8, second panel). Labor demand, however, is not weak. Job vacancies have surged to an all-time high of 1.3 million, or a ratio of one job vacancy per unemployed worker. Moreover, according to the BoE’s Agents Survey, the proportion of firms reporting recruitment difficulties is extremely elevated (Chart 8, third panel). As a result of weak labor supply but strong labor demand, wages are rising rapidly (Chart 8, bottom panel), with the KPMG/REC Indicator of pay higher than 6%. Chart 8Labor Market Tightness

Labor Market Tightness

Labor Market Tightness

Chart 9Poor Productivity Weighs On Trend GDP

Poor Productivity Weighs On Trend GDP

Poor Productivity Weighs On Trend GDP

Rapidly increasing wages and underlying inflation are indicative of a greater malaise. UK GDP is still 3.6% below its pre-COVID trend, while US GDP has already moved past its previous peak. Yet, wages and underlying inflation are just as strong in both economies. This suggests that the UK trend GDP has slowed more than in the US and that aggregate demand is colliding more rapidly with the constraint created by a weaker potential GDP. Labor supply is not the only culprit behind the slowdown in UK’s trend GDP. Since Brexit, UK capex has been particularly weak, which has depressed productivity growth and suppressed trend GDP further (Chart 9). Bottom Line: The BoE expects UK headline CPI inflation to move above 10% before the end of the year. We agree with this assessment. Cost-push inflation will remain strong in response to additional increases in regulated energy prices this fall and greater pass-through from businesses. Meanwhile, the labor market is overheated because of weak labor supply and surging job vacancies. The UK core inflation is likely to be sticky as Brexit weighs on the country’s trend GDP, which causes aggregate demand to surpass aggregate supply easily. Investment Implications The investment implications of the UK’s weak growth and strong inflation outlook are far reaching. Fixed Income Implications BCA’s Global Fixed Income Strategy service upgraded UK government bonds to overweight from underweight in their global fixed income portfolios. We heed this message and move to overweight UK Gilts relative to German Bunds within European fixed income portfolios. Chart 10The BoE's Dovish Justification

The BoE's Dovish Justification

The BoE's Dovish Justification

The BoE’s forecast calls for a deeply negative output gap as well as a rising rate of unemployment in 2023 and 2024. According to the BoE’s model, these dynamics will weigh on headline CPI next year (Chart 10). We take the BoE at its word when it communicated a gentler pace of rate hikes than was anticipated by the SONIA curve. The BoE believes that the weakness in the UK’s trend GDP growth weighs on the country’s neutral rate of interest. Thus, there is a limited scope before higher interest rates hurt economic activity. Since the BoE already foresees a poor growth outcome and weaker inflation next year, this view of the neutral rate logically results in a shallow path of interest rate increases. In other words, the BoE is not the Fed. This view prompts our fixed income colleagues to expect the SONIA curve to move toward the gentler rhythm of interest rate hikes proposed by the BoE. As a corollary, it implies that Gilt yields have more downside. More specifically, BCA sees room for UK-German yields spreads to narrow. Investors have expected the BoE to be significantly more hawkish than the European Central Bank (ECB), and a partial convergence in expected interest rate paths is likely. Moreover, UK yields have a higher beta than German ones. As a result, the current wave of risk aversion driven by global growth fears should cause an outperformance of UK government bonds compared to German ones. Currency Market Implications The outlook for GBP/USD depends on the evolution of overall market conditions. If risk assets remain under pressure, so will Cable. Chart 11Cable And EM Stocks

Cable And EM Stocks

Cable And EM Stocks

A durable bottom in GBP/USD will coincide with a rebound in EM equities (Chart 11). The correlation between these two assets most likely reflects the UK’s current account deficit of 2.8% of GDP in 2021. Large external financing needs render the currency very sensitive to global liquidity conditions and thus, to the dollar’s trend and global risk aversion, as is the case with EM assets. Peter Berezin, BCA Chief Global Strategist, expects global stocks to rebound in the near future, which will lift EM equities in the process. Interestingly, GBP/USD does not correlate with the relative performance of EM shares. Thus, a rebound in Cable does not contradict BCA’s Emerging Market Strategy service’s view that EM stocks are likely to underperform further in the coming months. Chart 12A Big Handicap For the GBP vs the EUR

A Big Handicap For the GBP vs the EUR

A Big Handicap For the GBP vs the EUR

BCA’s Foreign Exchange strategy team sees further upside in EUR/GBP, toward the 0.9 level. 2-year yield differentials between the UK and Germany are likely to narrow in response to the downgrade of the SONIA curve. Importantly, the wide UK current account deficit necessitates higher real interest rates to prop the pound against the euro because the Eurozone current account surplus stands at 2.3% of GDP. However, neither the 2-year nor 10-year real rates are higher in the UK than they are in the Euro Area (Chart 12). Additionally, even the nominal yield premium of UK bonds vanishes once they are hedged into euros. UK hedged 2-year bonds yield 50bps less than their German counterparts, and 10-year Gilts offer 80bps less than Bunds, which limits continental inflows into the UK. Equity Market Implications UK stocks are pro-cyclical, and their absolute performance will bottom in tandem with global equities. The near-term outlook for global equities remains clouded by the confluence of global growth fears, a weaker CNY, and tighter monetary policy around the world. Meanwhile, UK stocks are very cheap, trading at a forward P/E ratio of 11. They are tactically oversold and are lagging forward earnings (Chart 13). Relative to global equities, the performance of UK stocks will continue to track that of global energy firms compared to the broad market. The heavy exposure of UK large-cap indices to oil and gas stocks has been a major asset since energy shares have become market darlings (Chart 14). Chart 13UK Stocks Are Close To A Bottom

UK Stocks Are Close To A Bottom

UK Stocks Are Close To A Bottom

Chart 14UK Large-Caps Are About Oil

UK Large-Caps Are About Oil

UK Large-Caps Are About Oil

At the time of writing, Sweden and Finland have yet to officialize their membership application to NATO, but BCA’s Geopolitical Strategy team assigns a high probability to this outcome. Russia will not stand idly by, especially as the EU threatens to cut their oil imports. Consequently, a deeper energy embargo is increasingly likely, which should prompt a temporary but violent rally in oil and natural gas prices. This process should sustain a few more weeks of outperformance from UK large-cap shares relative to the rest of the world. Chart 15The UK vs The Eurozone: Cheap But Overbought

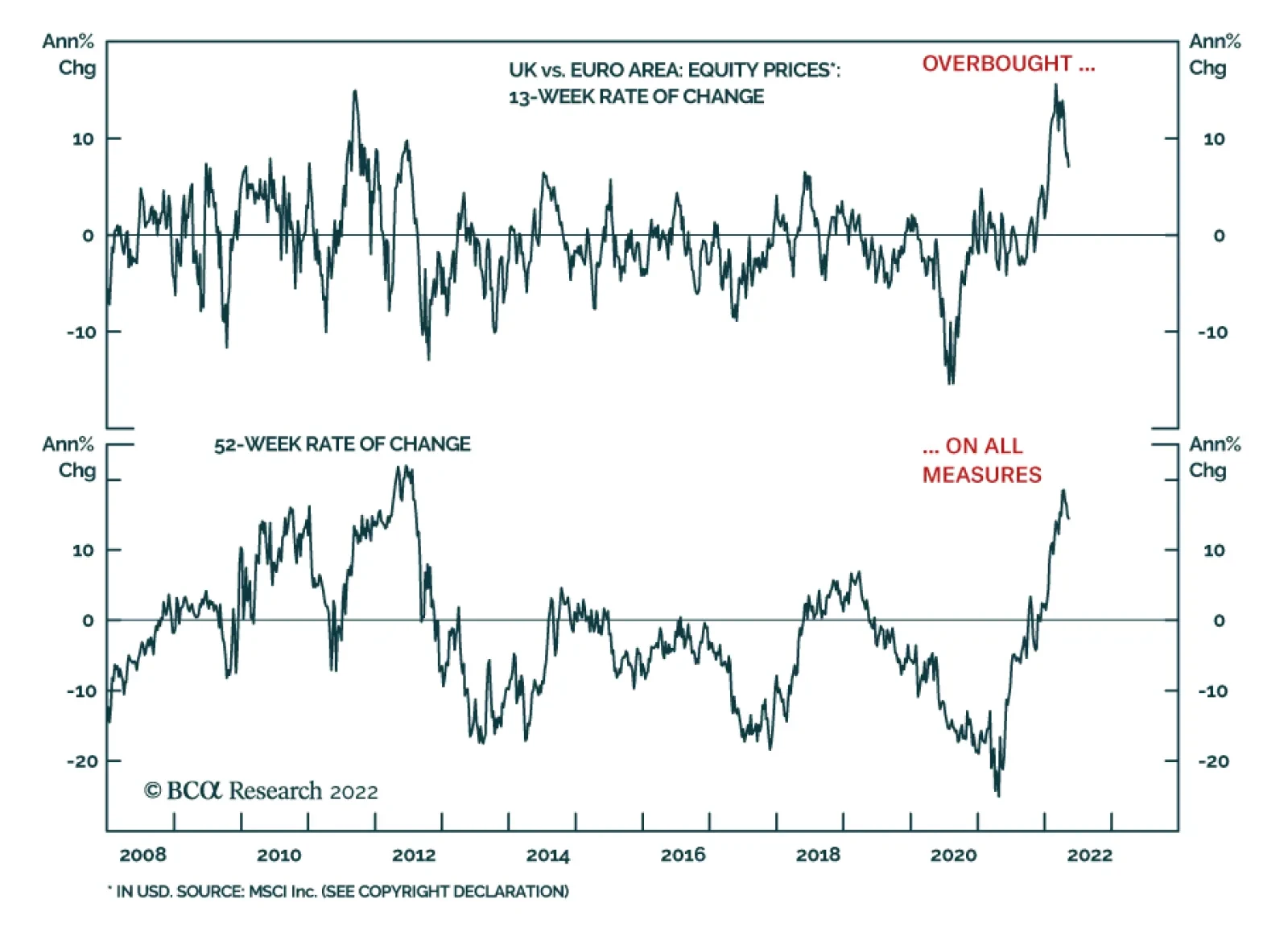

The UK vs The Eurozone: Cheap But Overbought

The UK vs The Eurozone: Cheap But Overbought

Structurally, UK equities are likely to remain well supported. A pullback in relative performance later this year is possible once oil prices ease off as BCA’s Commodity and Energy team expects. However, the oil market will stay tight for years to come because of the investment dearth observed since 2014-2015, when OPEC 2.0 started its market-share war. According to Bob Ryan, BCA’s Chief Commodity Strategist, it will take years of high returns in the sector to attract the capital needed to lift energy capex enough to line up supply with demand. Thus, energy remains a structurally favored sector, which will boost the cheap UK market’s appeal. UK stocks enjoy a structural tailwind relative to Euro Area shares. They remain cheap, because they still trade at a significant historical discount (Chart 15). Moreover, relative earnings are moving decisively in favor of UK stocks, something that is unlikely to change, even if the UK economy contracts. Ultimately, UK large-cap names derive the bulk of their profits from overseas and the structural tailwind of a secular commodity bull market will continue to assert itself on relative profits. Nevertheless, UK shares have also become extremely overbought, which raises the risk of a pullback in the second half of the 2022 (Chart 15, third and fourth panel). The recent outperformance of UK stocks relative to those of the Eurozone has been larger than what sectoral biases explain. An equal-sector weights version of the UK MSCI has outperformed a similarly constructed Euro Area index by 9.6% year-to-date. Chart 16Waiting For Catalysts To A Eurozone Rebound

Waiting For Catalysts To A Eurozone Rebound

Waiting For Catalysts To A Eurozone Rebound

A tactical rectification of the overbought conditions in the performance of UK equities relative to those of the Euro Area will require an ebbing of stagflation fears in the Euro Area (Chart 16, top panel). This implies that investors looking to buy Eurozone equities are waiting for a stabilization in the energy market (that is, waiting for clarity about Sweden’s and Finland’s NATO decision as well as Russia’s response). It also means that the Chinese economy must stabilize, since Eurozone equities are more sensitive to the evolution of the Chinese credit impulse than UK ones (Chart 16, second panel). Nonetheless, BCA’s Global Fixed Income Strategy team’s view on UK-German spreads is consistent with an eventual tactical pull back in the relative performance of UK stocks vis-à-vis Euro Area ones (Chart 16, bottom panel). Two pair trades make attractive vehicles to bet on an underperformance of UK stocks relative to those of the Euro Area in the second half of 2022. The first one is to sell UK financials at the expense of Euro Area financials. Historically, a decline in UK Gilt yields relative to their German equivalent strongly correlates with an underperformance of UK financials (Chart 17). The second one is to sell UK healthcare names relative to those in the Eurozone. The relative performance of healthcare shares has greatly outpaced relative earnings and is now hitting a critical resistance level (Chart 18). Moreover, UK healthcare firms are exceptionally overbought relative to their Euro Area competitors. Importantly, those two trades display little correlation to the broad market trend. Chart 17Challenges To UK Financials

Challenges To UK Financials

Challenges To UK Financials

Chart 18UK Healthcare: Running Ahead Of Itself

UK Healthcare: Running Ahead Of Itself

UK Healthcare: Running Ahead Of Itself

Finally, UK small-cap stocks are becoming attractive relative to their large-cap counterparts, although the timing remains risky. Unlike the internationally focused large-cap indices, small-cap shares are a direct bet on the health of the UK domestic economy. Hence, small- and mid-cap names have massively underperformed the FTSE-100 as market participants sniffed out the poor outlook for UK economic activity (Chart 19). They are now extremely oversold relative to large-cap names and their overvaluation has been corrected. The main problem with small-cap shares is the lack of a catalyst to rectify their oversold conditions. The most likely candidate for such a reversal would be a peak in energy inflation, considering it stands at the crux of the headwinds that UK consumption and growth face. However, energy CPI will not peak until later this fall and thus, the pain on UK households will build until then. As a result, wait for a clear sign that energy inflation recedes before entering a long UK small-cap / short UK large-cap contrarian trade (Chart 20). Chart 19Bombed Out Small-Caps...

Bombed Out Small-Caps...

Bombed Out Small-Caps...

Chart 20…Need A Peak In Energy Inflation

...Need A Peak In Energy Inflation

...Need A Peak In Energy Inflation

Bottom Line: In line with our expectations that UK growth will worsen significantly in the quarters ahead, we follow the BCA Global Fixed Income team and move to overweight UK government bonds within European fixed income portfolios. While we expect GBP/USD will bottom once global risk assets find a floor, BCA’s Foreign Exchange Strategy team also anticipates Sterling to depreciate further relative to the euro. Because of their large energy and materials exposure, UK large-cap equities will enjoy a structural outperformance relative to Euro Area large-cap indices on the back of a secular bull market in commodities. However, a temporary pullback in the UK’s relative performance is likely in the second half of 2022. Selling UK financials and UK healthcare stocks relative to their Eurozone counterparts offers a compelling approach to implement this view. Finally, UK small-caps are oversold relative to large-caps, but we recommend investors wait until energy CPI peaks when a relative rebound may emerge. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Tactical Recommendations Cyclical Recommendations Structural Recommendations

Executive Summary Favor ASEAN And The Philippines

Favor ASEAN And The Philippines

Favor ASEAN And The Philippines

Southeast Asia is suffering from fading macro and geopolitical tailwinds but there are still investment opportunities on a relative basis. The peace dividend, globalization dividend, and demographic dividend are all eroding and will continue to erode, though there are relative winners and losers. The Philippines and Thailand are most secure; the Philippines and Indonesia are least dependent on trade; and the Philippines and Vietnam have the highest potential GDP growth. Geopolitical risk premiums have risen for Russia, Eastern Europe, China, and will rise for the Middle East. This leaves ASEAN states as relatively attractive emerging markets. Trade Recommendation Inception Date Return LONG PHILIPPINES / EM EQUITIES 2022-05-12 LONG ASEAN / ACW EQUITIES 2022-05-12 Bottom Line: ASEAN’s geopolitical outlook is less ugly than many other emerging markets. Cyclically, go long ASEAN versus global equities and long Philippine equities versus EM. Feature Chart 1Hypo-Globalization A Headwind For Trading States

Hypo-Globalization A Headwind For Trading States

Hypo-Globalization A Headwind For Trading States

The Philippines elected its second “strongman” leader in a row on May 9, provoking the usual round of editorials about the death of liberalism. Investors know well by now that such political narratives do as much to occlude economic reality as to clarify it. Still, there is a fundamental need to understand the changing global political order since it will ultimately impact the investment landscape. If the global order stabilizes – e.g. US-Russia and US-China relations normalize – then trade and investment may recover from recent shocks. A new era of “Re-Globalization” could ensue. Asia Pacific would be a prime beneficiary as it is full of trading economies (Chart 1). Related Report Geopolitical StrategySecond Quarter Outlook 2022: When It Rains, It Pours By contrast, if Great Power Rivalry escalates further, then trade and investment will suffer, the current paradigm of Hypo-Globalization will continue, and East Asia’s frozen conflicts from 1945-52 will thaw and heat up. Asian states will have to shift focus from trade to security and their economies will suffer relative to previous expectations. How will Southeast Asia fare in this context? Will it fall victim to great power conflict, like Eastern Europe? Or will it keep a balance between the great powers and extract maximum benefits? Three Dividends Three dividends have underpinned Southeast Asia’s growth and prosperity in recent decades: 1. Peace Dividend – A relative lack of war and inter-state conflict. 2. Globalization Dividend – Advantageous maritime geography and access to major economies. 3. Demographic Dividend – Young demographics and strong potential GDP growth. All three of these dividends are eroding, so the macro and geopolitical investment case for ASEAN has weakened relative to twenty years ago. Nevertheless in a world where Russia, China, and the Gulf Arab markets face a higher and persistent geopolitical risk premium, ASEAN still offers attractive investment opportunities, particularly if the most geopolitically insecure countries are avoided. Peace Dividend Favors The Philippines And Thailand Since the end of the US and Chinese wars with Vietnam, military conflicts in Southeast Asia have been low intensity. Lack of inter-state conflict encouraged economic prosperity and security complacency. The five major Southeast Asian nations saw military spending decline since the 1990s and only Vietnam spends more than 2% of GDP (Chart 2). Chart 2Peace Brought Prosperity

Southeast Asia: Favor The Philippines

Southeast Asia: Favor The Philippines

Unfortunately that is about to change. China has large import dependencies, an insufficient tradition of sea power, and feels hemmed in by its geography and the US alliance system. Beijing’s solution is to build and modernize its navy and prepare for potential conflict with the US, particularly over Taiwan. The result is rising tension across East Asia, including in Southeast Asia and the South China Sea. The ASEAN states fear China will walk over them, China fears they will league with the US against China, and the US tries to get them to do exactly that. Hence ASEAN’s defense spending has not kept up with its geopolitical importance and will have to rise going forward. Consider the following: Vietnam risks conflict with China. Vietnam has the most capable and experienced naval force within ASEAN due to its sporadic conflicts with China. Its equipment is supplied mainly by Russia, pitting it squarely against China’s Soviet or Soviet-inspired equipment. But Russia-China ties are tightening, especially after Russia’s divorce with Europe. While Vietnam will not reject Russia, it is increasingly partnering with the United States. The pandemic added to the Vietnamese public’s distrust of China, which is ancient but has ramped up in recent years due to clashes in the South China Sea. While Vietnam officially maintains that it will never host the US military, it is tacitly bonding with the US as a hedge against China. Yet Vietnam does not have a mutual defense treaty with the US, so it is vulnerable to Chinese military aggression over time. Indonesia distances itself from China. Rising security tensions are also forcing Indonesia to change its strategy toward China. Indonesia lacks experience in naval warfare and is not a claimant in the territorial disputes in the South China Sea. It is reluctant to take sides due to its traditionally non-aligned diplomatic status, its military culture of prioritizing internal stability (which is hard to maintain across thousands of islands), and China’s investment in its economy. However, China is encroaching on Indonesia’s exclusive economic zone and Indonesia has signaled its displeasure through diplomatic snubs and high-profile infrastructure contracts. Indonesia is trying to bulk up its naval and air capabilities, including via arms purchases from the West. Malaysia distances itself from China. Malaysia and the Philippines have the weakest naval forces and both face pressure from China’s navy and coast guard due to maritime-territorial disputes. But while the Philippines gets help from the US and its allies and partners, Malaysia has no such allies. Traditionally it was non-aligned. Instead it utilizes economic statecraft, as it has often done against more powerful countries. It recently paused Chinese economic projects in the country to conduct reviews and chose Ericsson over Huawei to build the 5G network. Ongoing maritime and energy disputes will motivate defense spending. The Philippines preserves alliance with United States. Outgoing President Rodrigo Duterte tried but failed to strengthen ties with China and Russia. Beijing continued to swarm the Philippines’ economic zone with ships and threaten its control of neighboring rocks and reefs. Ultimately Duterte renewed his country’s Visiting Forces Agreement with the US in July 2021. The newly elected President “Bong Bong” Marcos is even less likely to try to pivot away from the US. Instead the Philippines will work with the US to try to deter China. Thailand preserves alliance with United States. Thailand is the most insulated from the South China Sea disputes and often acts as mediator between China and other ASEAN states. However, Thailand is also a formal US defense ally and assisted with logistics during the Korean and Vietnamese wars. While US military aid was suspended after the 2014 military coup, non-military aid from the US continued. The State Department certified Thailand’s return to democracy in 2019, relations were normalized, and the annual Cobra Gold exercise resumed in 2020. The US’s hasty normalization shows Thailand’s importance to its regional strategy. On their own, the ASEAN states cannot counter China – they are simply outgunned (Chart 3). Hence their grand strategy of balancing Chinese trade relations with American security relations. Chart 3Outgunned By China

Southeast Asia: Favor The Philippines

Southeast Asia: Favor The Philippines

Chart 4Opinion Shifts Against China

Southeast Asia: Favor The Philippines

Southeast Asia: Favor The Philippines

In recent decades, with the US divided and distracted, they sought to entice China through commercial deals, in hopes that it would reduce its encroachments on the high seas. This strategy failed, as China’s expansion of economic and military influence in the region is driven by China’s own imperatives. Beijing’s lack of transparency about Covid-19 also sowed distrust. As a result, public opinion became more critical of China and defensive of national sovereignty (Chart 4). Southeast Asia will continue trading with China but changing public opinion, the US-China clash, and tensions in the South China Sea will inject greater geopolitical risk into this once peaceful and prosperous region. Military weakness will also lead the ASEAN states to welcome the US, EU, Japan, and Australia into the region as economic and security hedges against China. This trend risks inflaming regional tensions in the short run – and China may not be deterred over the long run, since its encroachments in the region are driven by its own needs and insecurities. Decades of under-investment in defense will result in ASEAN rearmament, which will weigh on fiscal balances and potentially economic competitiveness. Investors should not take the past three decades of peace for granted. Bottom Line: Vietnam (like Taiwan) is in a geopolitical predicament where it could provoke China’s wrath and yet lacks an American security guarantee. The Philippines and Thailand benefit from American security guarantees. Indonesia and Malaysia benefit from distance from China. All of these states will attempt to balance US and China relations – but in the future that means devoting more resources to national security, which will weigh on fiscal budgets and take away funds from human capital development. Waning Globalization Dividend Favors Indonesia And The Philippines All the ASEAN states rely heavily on both the US and China for export markets. This reliance grew as trade recovered in the wake of the global pandemic (Chart 5). Now global trade is slowing down cyclically, while US-China power struggle will weigh on the structural globalization process, penalizing the most trade-dependent ASEAN states relative to their less trade-dependent neighbors. So far US-China economic divorce is redistributing US-China trade in a way that is positive for Southeast Asia. China is rerouting exports through Vietnam, for example, while the US is shifting supply chains to other Asian states (Chart 6). The US will accelerate down this path because it cannot afford substantively to reengage with China’s economy for fear of strengthening the Russo-Chinese bloc. Chart 5Trade Rebounded But Hypo-Globalization Will Force Domestic Reliance

Trade Rebounded But Hypo-Globalization Will Force Domestic Reliance

Trade Rebounded But Hypo-Globalization Will Force Domestic Reliance

Chart 6ASEAN’s Exports To US Surge Ahead Of China’s

ASEAN's Exports To US Surge Ahead Of China's

ASEAN's Exports To US Surge Ahead Of China's

Hence the US will become more reliant on Southeast Asian exporters. Whatever the US stops buying from China will have to be sourced from other countries, so countries that export a similar basket of goods will benefit from the switch. Comparing the types of goods that China and ASEAN export to the US, Thailand is the closest substitute for China, whereas Malaysia is the farthest (Chart 7). That is not to say that Malaysia will suffer from US-China divorce. It is already ahead of China in exporting high-tech goods to the US, which is the very reason its export profile is so different. In 2020, 58% of Malaysia’s exports to the US are high-tech versus 35% for China’s. At the same time, Southeast Asian exports to China may not grow as fast as expected – cyclically China’s economy may accelerate on the back of current stimulus efforts, but structurally China is pursuing self-sufficiency and import substitution via a range of industrial policies (“Made in China 2025,” “dual circulation,” etc). These policies aim to make Chinese industrials competitive with European, US, Japanese, and Korean industrials. But they will also make China more competitive with medium-tech and fledging high-tech exports from Southeast Asia. Thus while China will keep importing low value products and commodities, such as unrefined ores, from Southeast Asia, imports of high-tech products will be limited due to China’s preference for indigenous producers. US export controls will also interfere with ASEAN’s ability to export high-tech goods to China. (In order to retain their US trade, in the face of Chinese import substitution, ASEAN states will have to comply with US export controls at least partially.) Even the low-to-medium tech goods that China currently imports from Southeast Asia may not grow as fast in the coming years as they have in the past. The ten provinces in China with the lowest GDP per capita exported a total of $129 billion to the world in 2020, whereas China’s imports from the top five ASEAN states amounted to $154 billion USD in 2020 (Chart 8). If Beijing insists on creating a domestic market for its poor provinces’ exports, then Southeast Asian exports to China will suffer. China might do this not only for strategic sufficiency but also to avoid US and western sanctions, which could be imposed for labor, environmental, human rights, or strategic reasons. Chart 7The US Sees Thailand And Vietnam As Substitutes For China

Southeast Asia: Favor The Philippines

Southeast Asia: Favor The Philippines

Chart 8China Threatens ASEAN With Import Substitution

Southeast Asia: Favor The Philippines

Southeast Asia: Favor The Philippines

Chart 9Trade Rebound Increased Exposure To US, China

Trade Rebound Increased Exposure To US, China

Trade Rebound Increased Exposure To US, China

China, unlike the US during the 1990s and 2000s, cannot afford to open up its doors and become a ravenous consumer and importer of all Asia’s goods. This would be a way to buy influence in the region, as the US has done in Latin America. But China still has significant domestic development left to do. This development must be done for the sake of jobs and income – otherwise the Communist Party will face sociopolitical upheaval. Malaysia, Vietnam, and Thailand are the most vulnerable to China’s dual circulation strategy because of their sizeable exports to China, which stand at 12%, 15% and 7.6% of GDP respectively (Chart 9). Even though the Southeast Asian states have formed into a common market, and have joined major new trade blocs such as the CPTPP and RCEP, they will not see unfettered liberalization within these agreements – and they will not be drawn exclusively into China’s orbit. Instead they will face a China that wishes to expand export market share while substituting away from imports. The US and India, which are not part of these new trade blocs, will still increase their trade with ASEAN, as they will seek to substitute ASEAN for China, and ASEAN will be forced to substitute them for China. Thus globalization will weaken into regionalization and will not provide as positive of a force for Southeast Asia as it did over the 1980s-2000s. Going forward, the new paradigm of Hypo-Globalization will weigh on trade-dependent countries like Malaysia, Vietnam, and Thailand relative to their neighbors. Within this cohort, Malaysia and the Philippines will benefit from selling high-tech goods to the US, while Thailand and Vietnam will benefit from selling low- and mid-tech goods. China will remain a huge and critical market for ASEAN states but its autarkic policies will drive them to pursue other markets. Those with large and growing domestic markets, like Indonesia and the Philippines, will weather hypo-globalization better than their neighbors. Vietnam, Malaysia, and Thailand are all extremely dependent on foreign trade and hence vulnerable if international trade linkages weaken. Bottom Line: Global trade is likely to slow on a cyclical basis. Structurally, Hypo-Globalization is the new paradigm and will remove a tailwind that super-charged Southeast Asian development over the past several decades. Indonesia and the Philippines stand to suffer least and benefit most. Potential Growth Dividend Favors The Philippines And Vietnam Countries that can generate endogenous growth will perform the best under hypo-globalization. Indonesia, the Philippines, and Vietnam have the largest populations within ASEAN. But we must also take into account population growth, which contributes directly to potential GDP growth. A domestic market grows through population growth and/or income growth. For example, China benefitted from its growing population but now must switch to income generation as its population growth is stagnating. In Southeast Asia, the Philippines, Malaysia, and Indonesia have the highest population growth, while Thailand has the lowest. Thai population growth is even weak compared to China. The total fertility rate reinforces this trend – it is highest in Philippines but lowest in Thailand (Chart 10). A population that is too young or too old needs significant support that diverts resources away from the most productive age group. Philippines and Indonesia have the lowest median age, while Thailand has the highest. The youth of Indonesia and Philippines will come of age in the next decade, augmenting labor force and potential GDP growth. By contrast, Vietnam and especially Thailand, like China, will be weighed down by a shrinking labor force in the coming decade (Chart 11). Chart 10Fertility Rates Robust In ASEAN

Southeast Asia: Favor The Philippines

Southeast Asia: Favor The Philippines

Chart 11Falling Support Ratio Weighs On Thailand, Vietnam

Southeast Asia: Favor The Philippines

Southeast Asia: Favor The Philippines

Hence Indonesia and Philippines will prosper while Thailand, and to some extent Vietnam, lack the ability to diversify away from trade through domestic market growth. Malaysia sits in the middle: it is trade dependent and has the smallest population, but it has a young and growing population, and its labor force is still growing. Yet falling population growth is not a disaster if productivity and income growth are high. Productivity trends often contrast with population trends: Indonesia had the weakest productivity growth despite having a large, young, and growing population, while Vietnam had the strongest growth, despite a population slowdown. In fact Vietnam has the strongest productivity growth in Southeast Asia, at a 5-year, pre-pandemic average of 6.3%, followed by the Philippines (Chart 12A). By comparison China’s productivity growth averaged between 3%-6.6%, depending on the data source. Chart 12AProductivity And Potential GDP

Productivity And Potential GDP

Productivity And Potential GDP

Chart 12BProductivity And Potential GDP

Productivity And Potential GDP

Productivity And Potential GDP

Chart 13Capital Formation Favors Philippines

Capital Formation Favors Philippines

Capital Formation Favors Philippines