Equities

In lieu of next week’s report, I will be presenting a webcast titled ‘The 5 Big Mispricings In The Markets Right Now, And How To Profit From Them’. I do hope you can join. Executive Summary Just as the railway timetables set in train the First World War, central bank timetables for aggressive rate hikes are setting in train a global recession. Demand is already cool, so aggressive rate hikes will take it to outright cold. The risk is elevated because central banks are desperate to repair their damaged credibility on fighting inflation, and it may be their last chance. Inflationary fears and hawkishness from central banks are weighing on bonds and stocks, and it may take some weeks, or months, for inflation fears to recede. But we could be approaching a turning point. By the summer, core inflation should be receding. Furthermore, the fractal structures of the sell-offs in both the 30-year T-bond and the tech-heavy NASDAQ index are approaching points of extreme fragility that have signalled inflection points. Fractal trading watchlist: 30-year T-bond, NASDAQ, FTSE 100 versus Euro Stoxx 50, Netherlands versus Switzerland, and Petcare (PAWZ). US Inflation Is Hot, But Demand Is Not

US Inflation Is Hot, But Demand Is Not

US Inflation Is Hot, But Demand Is Not

Bottom Line: Tactically cautious, but long-term investors who do not need to time the market bottom should overweight bonds and overweight long-duration defensive equities versus short-duration cyclical equities – for example, overweight US versus non-US equities. Feature The First World War, the historian AJP Taylor famously argued, was “imposed on the statesmen of Europe by railway timetables.” Taylor proposed that the railways and their timetables were so central to troop mobilisation – and specifically, the German Schlieffen Plan – that a plan once set in motion could not be stopped. “Once started the wagons and carriages must roll remorselessly and inevitably to their predestined goal.” Otherwise, the whole process would unravel, and an opportunity to demonstrate military credibility would be lost that might never come again. Today, could a global recession be imposed upon us by central bank timetables for aggressive rate hikes? Just as it was difficult to unwind the troop mobilisation that led to the Great War, it will be difficult to back down from the aggressive rate hikes that the central banks have timetabled, at least in the near term. Otherwise, an opportunity to demonstrate inflation fighting credibility would be lost that might never come again. Just as the railway timetables set in train the First World War, central bank timetables for aggressive rate hikes may set in train another global recession. Unfortunately, central banks do not have precision weapons. Quite the contrary, monetary tightening is a blunt instrument which works by cooling overall demand. But demand is already cool, as evidenced by the contraction of the US economy in the first quarter. In their zeal to repair their damaged credibility on fighting inflation, the danger is that central banks take the economy from cool to outright cold. Granted, the US economy was dragged down by a drop in inventories and net exports. But even US domestic demand – which strips out inventories and net exports – is barely on its pre-pandemic trend (Chart I-1). Meanwhile, the euro area economy is still 5 percent below its pre-pandemic trend (Chart I-2). To reiterate, by hiking rates aggressively into economies that are at best lukewarm, central banks are risking an outright recession. Chart I-1US Inflation Is Hot, But Demand Is Not

US Inflation Is Hot, But Demand Is Not

US Inflation Is Hot, But Demand Is Not

Chart I-2Euro Area Inflation Is Hot, But Demand Is Not

Euro Area Inflation Is Hot, But Demand Is Not

Euro Area Inflation Is Hot, But Demand Is Not

Our Three-Point Checklist For A Recession Has Three Ticks My colleague Peter Berezin has created a three-point checklist for a recession: The build-up of an imbalance makes the economy vulnerable to downturn. A catalyst exposes this imbalance. Amplifiers exacerbate the downturn. Is there a major imbalance? You bet there is. The post-pandemic 26 percent overspend on durable goods in the US constitutes one of the greatest imbalances in economic history. Other advanced economies also experienced unprecedented binges on durable goods. The catalyst that is exposing this major imbalance is the realisation that durable goods are, well, durable. So, if you overspent on durables in 2020/21, then the risk is that you symmetrically underspend in 2022/23 (Chart I-3). The post-pandemic 26 percent overspend on durable goods in the US constitutes one of the greatest imbalances in economic history. Meanwhile, a future underspend on goods cannot be countered by an overspend on services because the consumption of services is constrained by time, opportunity, and biology. There is a limit to how often you can eat out, go to the movies, or go to the doctor (Chart I-4). Indeed, for certain services, an underspend will persist, because we have made some permanent post-pandemic changes to our lifestyles: for example, hybrid office/home working and more online shopping and online medical care. Chart I-3An Overspend On Goods Can Be Corrected By A Subsequent Underspend...

An Overspend On Goods Can Be Corrected By A Subsequent Underspend...

An Overspend On Goods Can Be Corrected By A Subsequent Underspend...

Chart I-4...But An Underspend On Services Cannot Be Corrected By A Subsequent Overspend

...But An Underspend On Services Cannot Be Corrected By A Subsequent Overspend

...But An Underspend On Services Cannot Be Corrected By A Subsequent Overspend

Finally, the amplifier that will exacerbate the downturn is monetary tightening. If central banks follow their railway timetables for aggressive rate hikes, a goods downturn will magnify into an outright recession. So, in Peter’s three-point checklist, we now have tick, tick, and tick. Inflation Is Hot, But Demand Is Not If economic demand is at best lukewarm, then what caused the post-pandemic inflation that central banks are now fighting? The simple answer is massive fiscal stimulus combined with the equally massive shift in spending to durable goods. Locked at home and flush with government supplied cash, we couldn’t spend it on services, so we spent it on goods. This created a massive shock in the distribution of demand, out of services whose supply could easily adjust downwards, and into goods whose supply could not easily adjust upwards. For example, airlines could cut back their flights, but auto manufacturers couldn’t make more cars. So, airfares didn’t collapse but used car prices went vertical! The causality from stimulus payments to durable goods spending to core inflation is irrefutable. The causality from stimulus payments to durable goods spending to core inflation is irrefutable. The biggest surges in US durable goods spending all coincided with the government’s stimulus checks (Chart I-5). And the three separate surges in month-on-month core inflation all occurred after surges in durable goods demand (Chart I-6). As further proof, core inflation is highest in those economies where the stimulus checks and furlough schemes were the most generous – like the US and the UK. Chart I-5Stimulus Checks Caused The Surges in Durable Goods Spending

Stimulus Checks Caused The Surges in Durable Goods Spending

Stimulus Checks Caused The Surges in Durable Goods Spending

Chart I-6The Surges In Durable Goods Spending Caused The Surges In Core Inflation

The Surges In Durable Goods Spending Caused The Surges In Core Inflation

The Surges In Durable Goods Spending Caused The Surges In Core Inflation

What Does All This Mean For Investment Strategy? Our high conviction view is that the pandemic’s inflationary impulse combined with the Ukraine war will turn out to be demand-destructive, and thereby ultimately morph into a deflationary impulse. Yet central banks are all pumped up to demonstrate their inflation fighting credibility. Given that this credibility is badly damaged, it may be their last opportunity to repair it before it is shattered forever. To repeat, just as the railway timetables set in train the First World War, central bank timetables for aggressive rate hikes may set in train another global recession. That said, a recession is not inevitable. The interest rate that matters most for the economy and the markets is not the policy rate that central banks want to hike aggressively, it is the long-duration bond yield. A lower bond yield can underpin both the economy and the financial markets, just as it did during the pandemic in 2020. But to the extent that the bond market is following the real economic data, we are in a dangerous phase. Because, as is typical at an inflection point, the real data will be noisy and ambiguous. Meaning it may take some weeks, or months, for inflation fears to be trumped by growth fears. On March 10th, in Are We In A Slow-Motion Crash? we predicted: “On a tactical (3-month) horizon, the inflationary impulse from soaring energy and food prices combined with the choke on growth from sanctions will weigh on both the global economy and the global stock market. As such, bond yields could nudge higher, the global stock market has yet to reach its crisis bottom, and the US dollar will rally” That prediction proved to be spot on! Recession, or no recession, we are still in a difficult period for markets because inflationary fears and hawkishness from central banks are weighing on bonds and stocks, while buoying the US dollar. As such, tactical caution is still warranted. Fractal structures of the sell-offs in both the 30-year T-bond and the tech-heavy NASDAQ index are approaching points of extreme fragility. But we could be approaching a turning point. By the summer, core inflation should be receding. Furthermore, the fractal structures of the sell-offs in both the 30-year T-bond and the tech-heavy NASDAQ index are approaching points of extreme fragility that have reliably signalled previous inflection points (Chart I-7 and Chart I-8). Chart I-7The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

Chart I-8The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The advice for long-term investors who do not need to time the market bottom is: Bonds will ultimately rally. Overweight the 30-year T-bond and the 30-year Chinese bond. Equities will be conflicted between slowing growth which will weigh on cyclical profits, and falling bond yields which will buoy long-duration valuations. Therefore, overweight long-duration defensive sectors and markets versus short-duration cyclical sectors and markets. For example, overweight US versus non-US equities. Fractal Trading Watchlist As just discussed, the sell-offs in the 30-year T-bond and the NASDAQ are approaching points of fractal fragility that have signalled previous turning points. Hence, we are adding both investments to our watchlist. Also added to our watchlist is the outperformance of the FTSE100 versus Euro Stoxx 50, and the underperformance of Netherlands versus Switzerland, both of which are approaching potential reversals. Our final addition is Petcare (PAWZ). After a stellar 2020, Petcare gave back most of its gains in 2021. But this underperformance is now approaching a point of fragility which might provide a new entry point. There are no new trades this week, but the full watchlist of investments at, or approaching, turning points is available on our website: cpt.bcaresearch.com Fractal Trading Watchlist: New Additions A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Chart 1The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

Chart 2The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

Chart 3AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

Chart 4Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Chart 5Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Chart 6US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

Chart 7A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Chart 8Biotech Is A Major Buy

Biotech Is A Major Buy

Biotech Is A Major Buy

Chart 9CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

Chart 10Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Chart 11Norway's Outperformance Could End

Norway's Outperformance Could End

Norway's Outperformance Could End

Chart 12Greece's Brief Outperformance To End

Greece's Brief Outperformance To End

Greece's Brief Outperformance To End

Chart 13BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

Chart 14The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

Chart 15The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

Chart 16Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Chart 17US Homebuilders' Underperformance Has Reached A Potential Turning Point

US Homebuilders' Underperformance Has Reached A Potential Turning Point

US Homebuilders' Underperformance Has Reached A Potential Turning Point

Chart 18Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Chart 19The Rally In USD/EUR Could End

The Rally In USD/EUR Could End

The Rally In USD/EUR Could End

Chart 20The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

Chart 21A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

Chart 22FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

Chart 23Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Fractal Trading System Fractal Trades

Central Bank ‘Railway Timetables’ Are Dragging Us Into Recession

Central Bank ‘Railway Timetables’ Are Dragging Us Into Recession

Central Bank ‘Railway Timetables’ Are Dragging Us Into Recession

Central Bank ‘Railway Timetables’ Are Dragging Us Into Recession

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

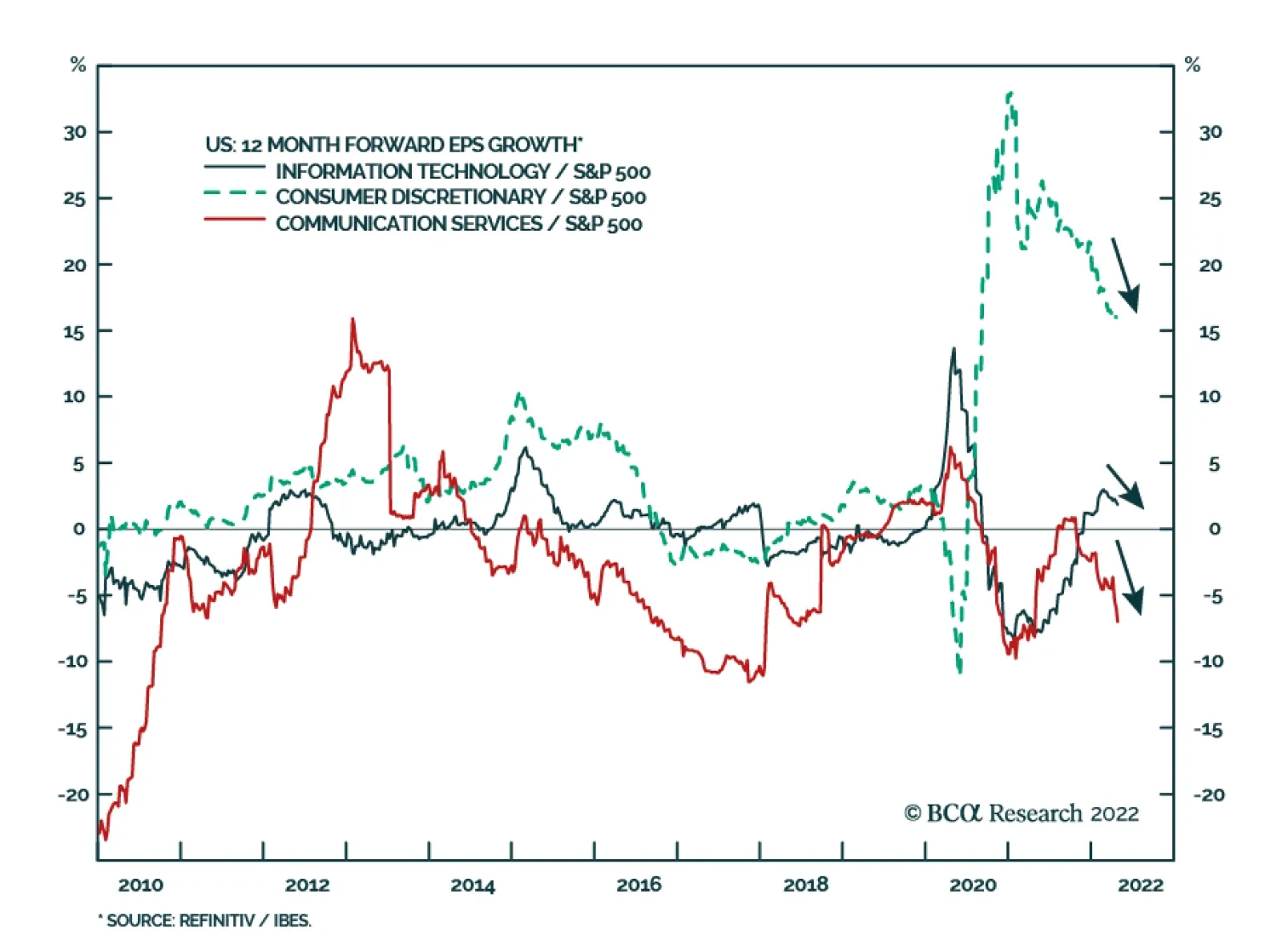

Broadly-defined US technology stocks have been consistently underperforming the S&P 500 since the beginning of the year. Communication Services, Consumer Discretionary, and IT have shed 24%, 20%, and 18% of their value, respectively. Two main headwinds…

Executive Summary Stocks Not Linked To Presidential Approval

Stocks Not Linked To Presidential Approval

Stocks Not Linked To Presidential Approval

President Kennedy’s performance in 1962 would be ideal for the Biden administration in this year’s midterm elections – but today the Russian conflict is less likely to help the Democrats. A threat to the homeland could lift President Biden’s job approval. But most likely inflation and foreign crises will weigh on his approval. A contrarian stock rally would not help Biden’s approval but Biden’s attempts to boost his rating could deliver negative surprises for stocks. US “peak polarization” and Democratic Party policies are negative for the stock market and investor risk appetite over the next zero-to-six months. Our quantitative election models suggest Republicans will win the Senate, though uncertainty will rise as a result of the controversy over the Supreme Court and abortion. Democratic odds of keeping the White House in 2024 are 54.6% but eroding. CLOSE Recommendation (Cyclical) CLOSING Level CLOSING Date RETURN Long Municipal Bonds Vs. Duration Matched Treasuries 93.53 2-MAY-22 -1.50% Bottom Line: Overall Biden policies plus global events are neutral or bullish for US Treasuries while neutral or bearish for US stocks over a tactical time horizon (zero-to-six months). Feature President Biden is doubling down on his support for Ukraine and thus adopting the John F. Kennedy foreign policy playbook of confronting Russia ahead of the US’s midterm elections. Related Report US Political StrategyWar Not Helping Biden So Far Biden’s position today is weaker than Kennedy’s in 1962, so his reaction to Russian aggression will create more market hurdles than it removes. Bad news will come before good news, compounding bearish investor sentiment in the near term. Policy uncertainty should decline after the midterm election on November 8, which is positive for equities in 2023. Democrats Scramble Amid Recession Fear The US economy contracted unexpectedly in the first quarter at an annualized 1.4% rate. The underlying data contained some silver lining – personal consumption grew at 2.7%. But the contraction is bad news for the economy and the ruling Democratic Party. Public approval of Biden’s handling of the economy has fallen to -16.2%. The global economy continues to sputter. Risks to growth are high in Europe and China as well (Chart 1). The US policy response will take shape on the monetary and fiscal level but also on the foreign policy level. First, global risks will not dissuade the Federal Reserve from normalizing interest rates. Chairman Jerome Powell signaled on April 21 that he is willing to hike interest rates 50 basis points at a time to combat core PCE inflation at 5.2%. The market currently expects core inflation to peak at 5.2% while the Fed funds rate will hit 3.3% in 2023 before falling in 2024. The implication is that monetary policy will tighten quickly, even as the economy stutters, which is negative for the US equity market and investor sentiment. However, Fed hawkishness is largely priced. US long-duration treasuries are at or near fair value at 3%, according to our US Bond Strategy. Our US Investment Strategy believes that with the S&P500 already down by 13% so far this year, stocks can begin to grind upward, barring other negative surprises. Chart 1US Slows Amid Global Growth Risks

US Slows Amid Global Growth Risks

US Slows Amid Global Growth Risks

Second, the White House will scramble to try to limit the damage to the Democratic Party in the midterms – with the unintentional result that negative surprises could arise from fiscal policy and especially foreign policy. On the fiscal front, congressional Democrats will redesign their budget reconciliation bill to try to gain a legislative victory. They will need to make it as close to deficit-neutral as possible to avoid fanning inflation. The odds of passage are higher than consensus expectations (26% on PredictIt). But the stock market does not want more government spending or higher taxes in a stagflationary environment. Fiscal policy is still a significant source of uncertainty in 2022, if not in 2023. On the foreign policy front, the greatest trouble looms. Russian aggression has prompted the US and its NATO allies to double down on their support for Ukraine, providing additional arms and aid. Biden’s Secretary of Defense Lloyd Austin said that the US wants to see Ukraine “a democratic country able to protect its sovereign territory … [and] Russia weakened to the point where it can't do things like invade Ukraine.”1 Finland and Sweden are increasingly likely to join NATO, which will antagonize Russia. Russia’s response is not yet known but it has issued aggressive warnings. By cutting off natural gas to Poland and Bulgaria, Moscow is warning that it may cut off natural gas to all Europe. Meanwhile Germany is embracing an oil embargo. A larger energy shock is increasingly likely. Chart 2More Bad News Before Good News

More Bad News Before Good News

More Bad News Before Good News

Bottom Line: Monetary policy hawkishness is largely priced whereas additional fiscal uncertainty and America’s reactive foreign policy are not fully priced. This news is neutral or bullish for US Treasuries while neutral or bearish for US stocks over a tactical time horizon (zero-to-six months) (Chart 2). Biden Can Hurt Stocks, Stocks Cannot Help Biden Before addressing how Biden will try to boost his job approval, we should ask whether approval ratings have any direct impact on financial markets. The answer is largely no – or fleeting at best. During the Trump administration it was easy to get the impression that the president’s approval rating had a substantive impact on the stock market, or at least benefited stocks relative to bonds. After the first year, a correlation developed between presidential approval and the stock-to-bond ratio (Chart 3A, top panel). The passage of tax cuts juiced corporate profits but also suggested that President Trump could get things done, boosting his approval rating. Oddly, however, the relationship continued even after Republicans lost Congress in 2018. Spurious or not, the correlation persisted until Covid-19 erupted. At that point Trump’s approval tanked while the stock market roared on the back of gargantuan monetary and fiscal stimulus. President Biden’s administration started off the same way, with presidential approval falling (the usual honeymoon ended) while stocks rallied relative to bonds (Chart 3A, bottom panel). But Biden’s passage of the American Rescue Plan Act and the bipartisan Infrastructure Investment and Jobs Act in 2021 did not boost his approval rating. Going forward, Biden’s approval rating will probably stabilize at a low level in an inflationary or stagflationary context. Stocks may continue to underperform bonds over a tactical time frame but will not underperform bonds over the cyclical time frame as long as the US avoids a recession. Thus there is not likely to be close correlation between Biden’s approval and the stock-to-bond ratio. From the sector and style perspective, there is also no clear relationship with presidential approval. There may be some basis for seeing Trump’s tax cuts as positive for cyclicals relative to defensives. His term coincided with the second half of a business cycle when growth expanded. But ultimately cyclicals vacillated and went sideways. Moreover growth stocks outperformed value stocks, in accordance with President Obama’s term in office. Yet there was no correlation between Trump’s approval and growth stocks relative to value (Chart 3B, top two panels). In Biden’s case, presidential job approval has no clear correlation with cyclicals relative to defensives. There may be some relationship with value relative to growth stocks but it is far from convincing. Most likely the underlying macroeconomic dynamics that favored value stocks (i.e. recovery, inflation) coincided with Biden’s honeymoon period and then outlasted it. However, if Biden passes a reconciliation bill with tax hikes, the implication should be positive both for value versus growth stocks and for his approval rating (Chart 3B, bottom two panels). Chart 3AStocks Not Linked To Presidential Approval

Stocks Not Linked To Presidential Approval

Stocks Not Linked To Presidential Approval

Chart 3BStocks Not Linked To Presidential Approval

Stocks Not Linked To Presidential Approval

Stocks Not Linked To Presidential Approval

From the above data we can draw a few conclusions. On one hand, the stock-to-bond ratio and cyclicals-versus-defensives could rally again on the back of a resilient global economy and yet Biden’s approval rating could fail to recover. The distribution of wealth means that inflation and rising mortgage rates hit low-to-middle income groups who comprise the bulk of voters. Cyclical assets will rise if the global economy improves relative to the US economy, whereas presidential approval may not. Inflation could subside incrementally with limited benefit to the president. On the other hand, if stocks and cyclical sectors continue to underperform, it will probably be due to even worse economic outcomes that will simultaneously prevent Biden’s approval from recovering. If the economy slows further and inflation remains persistent, disapproval will rise. The problem for investors is that the latter is the likeliest scenario based on the energy supply risks in Europe and China’s difficulties stabilizing growth. The US economy cannot entirely avoid the knock-on effects of slower global growth over the next six months. Bottom Line: There is no stable relationship between presidential approval and the stock market, whether regarding bonds, sectors, or styles. There are occasional correlations that reflect coincidences of macro, market, and political cycles or major policy changes. In today’s context a rebound in cyclical assets may not help the president while a further downturn would hurt him. But the president’s attempts to boost his approval rating could hurt stocks. Inflation And Foreign Wars Tend To Hurt Presidents What can Biden do to boost his approval rating and his party’s odds in the midterm election? Not much. Foreign policy is his best option, though he is limited to a defensive or reactive foreign policy and even then the underlying economy will drive voters the most. Looking at presidential approval over time, upswings occur during periods of economic prosperity and peaks occur amid foreign belligerence that threatens the homeland. Presidential approval has slumped since the subprime mortgage crisis and today it is even lower than under President Obama (Chart 4A). Chart 4APresidential Approval Follows Peace And Prosperity, Not War And Poverty

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Similarly presidential disapproval rises during recessionary and inflationary periods as well as wars and scandals (Chart 4B). The Obama/Trump era saw a rise in disapproval that could resume due to inflation. Foreign wars that do not present a threat to the homeland can increase disapproval. Chart 4BPresidential Approval Follows Peace And Prosperity, Not War And Poverty

Biden's Cold War And Culture War

Biden's Cold War And Culture War

The takeaway is that a homeland threat from abroad could temporarily lift the president’s approval but it will not last for long unless the underlying economic malaise is cured. The problem for Biden is that the most immediate foreign policy challenges emanate from oil producers whose reactions exacerbate the inflation problem (Russia, Iran). Biden may or may not keep relations steady with China, where disputes could drive up import prices. Bottom Line: A reactive foreign policy could provoke a threat to the homeland that boosts the president’s job approval. But more likely the weakening economy, high inflation, and foreign crises that add to inflation will hurt the president. Biden And The Kennedy Playbook President Kennedy’s experience in 1962 presents the best case for Democrats but the underlying economic and political context are different and damaging for Biden. Comparing today’s situation to comparable midterm election years, the negative outlook for Biden and the Democrats becomes clear. Comparable midterm elections feature high international tensions, high inflation, or low presidential approval on a net basis. Today the “Misery Index” (unemployment plus inflation) is comparable to the minimum levels in midterm years in the 1970s – and higher than the maximum levels in other midterm years (Table 1). The House and Senate losses during periods of high misery and low presidential approval are substantial. Table 1Misery And Midterms

Biden's Cold War And Culture War

Biden's Cold War And Culture War

The 1962 midterm election is a notable exception. The Cuban Missile Crisis and Kennedy’s handling of it minimized the Democratic Party’s losses that year, with only four seats lost in the House, plus a gain of three seats in the Senate. Compare this to the typical midterm election, with an average of 27 lost seats in the House (31 for Democrats) and four seats lost in the Senate (five for Democrats) (Table 2). Table 2Kennedy’s Cuban Missile Crisis Midterm, 1962

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Kennedy’s net approval averaged 55% that year, whereas Biden’s today stands at -11%. A threat to the homeland could boost Biden’s approval but today’s likeliest conflicts would worsen inflation if they occurred. The Misery Index stands at 11% this year compared to 6% in 1962. Most importantly, in the Cuban Missile Crisis, the Russians recognized that America would always care about Cuba’s status more than Russia because it posed a proximate strategic threat. Americans had more at stake and could take greater risks to prevent Cuba from hosting nuclear arms. Today, while the US is not trying to supply Ukraine or Finland with nuclear weapons, NATO membership would expand the US nuclear umbrella. Americans do not seem prepared to recognize that Russia will always care more about Ukraine’s and Finland’s status than Americans will. Russians have more at stake and can take greater risks. Thus while Biden’s foreign policy could easily provoke a crisis with Russia, Biden may not get the better end of the crisis like Kennedy did. Meanwhile financial markets will suffer from the spike in tensions. Bottom Line: Biden’s doubling down on support for Ukraine and NATO enlargement suggest that he does not have an interest in reducing tensions with Russia ahead of the midterm election. Yet Biden is unlikely to get the better of any reactive foreign policy that escalates tensions – at least not in time for the midterms. This dynamic is negative for US and global stocks and risk assets. Election Quant Model Updates The Philadelphia Federal Reserve released a second update to its state-level coincident indicators in April, enabling us to update our quant models for the Senate election in 2022 and presidential election in 2024. The model still predicts that Democrats will lose two Senate seats, producing a Republican majority of 52-48 (Chart 5). Arizona and Georgia are the two states in which Democrats won Senate seats in 2022 but are expected to flip to the Republican side. Arizona and Pennsylvania remain toss-up states (odds of Democratic victory range from 45%-55%) but are inching downward toward likely Republican victories. Chart 5GOP Tipped To Take The Senate (Quant Election Model, April 2022)

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Democrats shed probability in all states once again. Odds fell the most in Arizona (-1.08 percentage point since the last update in early April) followed by North Carolina (-1.03ppt) and Pennsylvania (-0.98ppt). In seven states the Democratic odds of victory fell by more than 0.5ppts, including Arizona and Nevada (Chart 6). Overall the probability for Democrats retaining control of the Senate now stands at 48.2% (down 0.2ppt). These odds are higher than consensus even though they agree with the consensus on expecting Republican victory. Online betting markets like PredictIt are pricing in Republican control at around 79%, up 3ppt from our last update. This is overstated and the new controversy over the Supreme Court and abortion will fire up Democratic voters, making the Senate race closer to what our model suggests. Chart 6Democrats Falter Across Senate Races: AZ, PA, NC

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Looking ahead to 2024, our presidential election model still predicts 308 Electoral College votes for the Democratic Party, a number that has not changed since the 2020 election (Chart 7). Democrats have a 54.6% chance overall of retaining the White House. Chart 7Biden Still Tipped For 2024 (Quant Election Model, April 2022)

Biden's Cold War And Culture War

Biden's Cold War And Culture War

The trend is negative for the incumbent party. North Carolina slipped out of the toss-up category and into Republican category – i.e. Democrats now have only a 44% chance of winning it. Democrats’ odds of winning Florida moved lower – it is now in toss-up territory at 54%, which comes closer to our subjective judgment that Republicans are favored there. The toss-up states have remained well anchored in the range of 40%-60% since 2020 and will play a pivotal role in future predictions. Generally the trend is for falling odds that Democrats will win these states (PA, FL, NC, AZ, and GA). Both Pennsylvania and Florida account for a combined 49 electoral votes and Florida is probably more Republican-leaning than the model says. If the three critical Rust Belt states (Pennsylvania, Wisconsin, Michigan) slip into toss-up territory then the model will be flagging serious trouble for Democrats. But a lot can happen between now and 2024. In the latest update Democrats are shedding probability of winning in all states, although to a lesser degree than the past two updates. Economic data, while still negative for the incumbent party, may be deteriorating less rapidly. Biden’s approval rating improved marginally since our last update and we expect it to stabilize, albeit at a low level. Michigan recorded the largest decline in Democratic odds of victory (-1.07ppt) followed by Minnesota (-0.79ppt) and New Hampshire (-0.78ppt). Democrats shed more than 0.5ppts from their odds of victory in twelve states, nine of which they won in 2022 (Chart 8). Chart 8Democrats Shedding Odds Of Winning States In 2024

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Bottom Line: Republicans are favored to take the Senate (as well as the House) in 2022. Democrats are slightly favored to retain the White House in 2024, though the model is optimistic by granting Florida to the Democrats and the election odds look to be razor-thin yet again. Investment Takeaways As we go to press, the unusual leak of a draft opinion of Supreme Court Justice Samuel Alito has roiled US politics. The draft argues that the landmark court case of Roe Versus Wade should be overturned. This incident reflects our “Peak Polarization” theme – that polarization will remain very disruptive in the short term yet subside over the long term. It also suggests an activist effort to escalate the culture wars ahead of the midterm election, which we have argued would be the case and implies that more unrest will follow from this event. Whether the Supreme Court overturns the landmark Roe versus Wade ruling of 1973, the battle for women voters will help sustain election-year policy uncertainty, as women’s approval for Democrats will start to recover (Chart 9). Investor sentiment will remain bearish in the very near term. A series of hurdles need to be cleared before we close our tactical long DXY trade and defensive sector tilt. We are closing our long municipal bond relative to Treasury trade for a loss of 1.5% (Chart 10). Chart 9Women Are Key Constituencies In The Midterm

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Chart 10Municipal Trade Fizzled Out Despite Strong Local Government Finance

Municipal Trade Fizzled Out Despite Strong Local Government Finance

Municipal Trade Fizzled Out Despite Strong Local Government Finance

The overall analysis of US politics is neutral or bullish for US Treasuries while neutral or bearish for US stocks over a tactical time horizon (zero-to-six months). If recession is avoided at the critical juncture this year, then 2023 will see a rising stock market as the economy expands and political risks fall. Matt Gertken Senior Vice President Chief US Political Strategist mattg@bcaresearch.com Footnotes 1 Peter Weber, “Defense Secretary Lloyd Austin says U.S. believes Ukraine can win, wants to 'see Russia weakened,'” The Week, April 25, 2022, theweek.com. Strategic View Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Table A2Political Risk Matrix

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Table A3US Political Capital Index

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Chart A1Presidential Election Model

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Chart A2Senate Election Model

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Table A4APolitical Capital: White House And Congress

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Table A4BPolitical Capital: Household And Business Sentiment

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Table A4CPolitical Capital: The Economy And Markets

Biden's Cold War And Culture War

Biden's Cold War And Culture War

Executive Summary More Chinese Households Intend To Save Than To Invest

More Households Intend To Save Than To Invest

More Households Intend To Save Than To Invest

The Politburo meeting last Friday signaled that China is determined to achieve the 5.5% annual growth target set earlier this year. Policymakers vowed to accelerate the implementation of existing pro-growth measures and hinted that they may scale up stimulus due to domestic challenges and external uncertainties. However, Chinese policymakers are facing an “impossible trinity” of eliminating domestic COVID cases and avoiding an overshoot as they stimulate the economy, while trying to achieve a high rate of economic expansion. The Politburo did not mention any plans to boost income and consumption via direct fiscal transfers to households, a sector that has been a weak link in China’s economy in the past two years. China’s consumption growth and demand for housing will not recover any time soon without meaningful aids to shore up household income. Bottom Line: Policy stimulus measures announced so far fall short of what is required to lift the economy. Given constraints on household consumption and the property market, China’s economic growth is set to underwhelm and Chinese stock prices will underperform their global counterparts. China’s top leaders have pledged to provide more support to the economy. The Politburo meeting last week indicated that the 5.5% growth target set for 2022 will be maintained and stimulus measures will be accelerated. Chinese stocks in both on- and offshore markets rebounded sharply following the positive rhetoric. Related Report Emerging Markets StrategyA Whiff Of Stagflation? In our view, however, Chinese authorities are facing an “impossible trinity” as they simultaneously attempt to achieve three goals: (1) pursuing a dynamic zero-Covid policy, (2) delivering decent economic growth, and (3) not resorting to “irrigation-style” massive stimulus. The pro-growth measures announced last week by the government lack the needed elements to generate a quick and strong rebound in the economy, particularly in the household and property sectors. Hence, the rebound in Chinese stock prices will unlikely progress into a cyclical rally (over a 6- to 12-month time span). We maintain our neutral allocation in Chinese onshore stocks and an underweight stance on the MSCI China Index, within a global portfolio. An “Impossible Trinity” The messages from the Politburo meeting highlight policymakers’ determination to shore up the economy. However, the authorities are not backing away from the zero-COVID policy, which is taking a heavy toll as cities are forced into lockdown to contain outbreaks. In addition, the Politburo reiterated the housing policy principle that “housing is for living, not for speculation” and did not mention concrete measures to boost household consumption. Thus, the biggest challenge for China to achieve its growth target this year is how to normalize economic activity without resorting to another round of “irrigation-style” stimulus while keeping domestic COVID cases at bay. In an environment of frequent lockdowns, monetary and fiscal easing have limited effect as the private and household sectors are averse to taking risks. China’s zero-COVID policy comes with hefty economic costs. April’s PMI showed sharp declines in a wide range of business activities due to the prolonged lockdown in Shanghai and several other cities (Chart 1). The new orders, new export orders, and imports subindexes in the manufacturing PMI and services PMI, all fell to their lowest levels since Q1 2020 when COVID first hit China (Chart 2). Chart 1April PMIs Show Widespread Declines In Business Activities

April PMIs Show Widespread Declines In Business Activities

April PMIs Show Widespread Declines In Business Activities

Chart 2PMI Subindexes Fell To Lowest Levels Since Q1 2020

PMI Subindexes Fell To Lowest Levels Since Q1 2020

PMI Subindexes Fell To Lowest Levels Since Q1 2020

Going forward, even if China manages to avoid a Shanghai-style month-long lockdown, the dynamic zero-COVID policy will have devastating ramifications on the economy. Notably, March economic data from the city of Shenzhen, China’s technology center, suggests that even a week-long lockdown has had large impact on the local economic activity. Chart 3Severe Economic Disruptions In Shenzhen Due To A Week-Long City Lockdown

Severe Economic Disruptions In Shenzhen Due To A Week-Long City Lockdown

Severe Economic Disruptions In Shenzhen Due To A Week-Long City Lockdown

In contrast with the extensive outbreak in Shanghai, Shenzhen was able to contain its COVID cases at an early stage and endured a citywide lockdown for only one week in mid-March. However, Shenzhen’s export growth contracted by 12.8% year-on-year (YoY) in March, a stark contrast from the 14.7%YoY increase in exports on a national level. The city’s imports fell by 11.9%YoY, also significantly lower than China’s total import growth, which was flat (Chart 3). Retail sales of consumer goods in Shenzhen shrank by 1.6%YoY in March and home sales plummeted by a stunning 90%YoY during the week of March 13-20. On the national level, the Politburo has called for an acceleration in infrastructure investment through frontloading local government special purpose bonds (SPB) and fast-tracking infrastructure project approvals. However, the lack of details has created questions regarding the magnitude of incremental stimulus, or whether the stepped-up policy effort will involve an increase in SPB or a general bond quota for local governments. Chart 4Construction Activity Started Softening In March, Before Shanghai Lockdown

Construction Activity Started Softening In March, Before Shanghai Lockdown

Construction Activity Started Softening In March, Before Shanghai Lockdown

The stringent COVID containment methods will also undermine the effectiveness of China’s pro-growth measures. As expected, China’s construction activity PMI tumbled in April amid the lockdowns, but the new orders and business expectations components in the construction PMI had already started to slide in March (Chart 4, top and middle panels). Moreover, employment in the labor-intensive construction sector also declined substantially in March and April (Chart 4, bottom panel). The deterioration in these indicators is consistent with our view that even short and less draconian lockdowns spark considerable disruptions in business activities. Bottom Line: There is a low likelihood that China will deviate from its existing zero-COVID policy for the rest of this year. As such, boosting the economy via stimulus will be challenging due to frequent interruptions to economic activities. No Bazooka For Consumers China’s household consumption, which accounts for about 40% of the country’s aggregate demand, has been a weak link in the economy during the past two years. Last week’s Politburo meeting pledged to stabilize employment, create new jobs and encourage hiring from small and medium enterprises (SMEs). However, there was no mention of any large-scale fiscal transfer to households via cash or subsidy payments, which suggests that pro-consumer measures are not in the stimulus package. Chart 5Retail Sales In China Have Been The Weak Link In The Economy In The Current Cycle

Retail Sales In China Have Been The Weak Link In The Economy In The Current Cycle

Retail Sales In China Have Been The Weak Link In The Economy In The Current Cycle

China’s retail sales growth has been muted in the current business cycle, a deviation from past economic recoveries when a revival in the general economy and moderate pro-consumption stimulus helped to lift household spending growth substantially above the rate of nominal GDP expansion (Chart 5). Since the pandemic, however, government stimulus to the household sector has been insufficient to revive consumption, due to the negative impact lockdowns have on both labor market demand and the service sector activities. Compared with the US and Europe, China’s fiscal transfer to the household sector has been very limited since the first wave of COVID in early 2020 (Chart 6). Local governments handed out vouchers in Q2 2020 aimed at boosting consumption, but the amounts were dismal and have had a minimal effect on the sector. Chart 6IMF Fiscal Monitor Database: Fiscal Response To The COVID-19 Pandemic

China’s Trilemma

China’s Trilemma

Presently the RMB value in direct payments to the household sector is even smaller: some cities including Shenzhen distributed consumption vouchers ahead of the May holiday week. Nonetheless, the total value of consumption vouchers this year is estimated at around RMB 2billion. The amount, even with a multiplier effect of 3 on consumption, will be less than 0.1% of China’s monthly retail sales in nominal value. Hence, the coupons are unlikely to make any significant difference to the aggregate household spending. Bottom Line: Household consumption will be severely curtailed as lockdowns wreak havoc on the economy and household income, and the government so far has not provided meaningful direct transfers to the public. Rebound In Housing Demand Doubtful The Politburo encouraged local governments to further relax local housing policies, such as lowering mortgage rates and down payment ratios, and easing restrictions on home sales and purchases. However, we do not expect that these policies alone will restore homebuyers’ confidence amid short-term factors such as COVID outbreaks/lockdowns, and longer-term factors like slowing household income growth, high household debt and poor demographics (Chart 7A and 7B). Chart 7AProperty Market Is Challenged By Slower Household Income Growth, High Household Income Debt And Poor Demographics

Property Market Is Challenged By Slower Household Income Growth, High Household Income Debt And Poor Demographics

Property Market Is Challenged By Slower Household Income Growth, High Household Income Debt And Poor Demographics

Chart 7BProperty Market Is Challenged By Slower Household Income Growth, High Household Income Debt And Poor Demographics

Property Market Is Challenged By Slower Household Income Growth, High Household Income Debt And Poor Demographics

Property Market Is Challenged By Slower Household Income Growth, High Household Income Debt And Poor Demographics

China’s household sector was struggling prior to recent lockdowns. The growth rate of national disposable income per capita slowed by more than two percentage points (in nominal terms) in Q1 this year compared with Q4 2019 (Chart 7A, top panel). In addition, the PBoC’s quarterly urban depositor survey (released before the Shanghai lockdown) in Q1 showed subdued confidence in future household income (Chart 8). Households’ willingness to save hit a record high and is even more elevated than in early 2020; on the other hand, the propensity to invest has dropped to a multi-year low (Chart 9). Chart 8Chinese Households' Subdued Confidence In Future Income

Chinese Households' Subdued Confidence In Future Income

Chinese Households' Subdued Confidence In Future Income

Chart 9More Households Intend To Save Than To Invest

More Households Intend To Save Than To Invest

More Households Intend To Save Than To Invest

Chart 10Chinese Households' Declining Appetite For Purchasing Real Estate Assets

Chinese Households' Declining Appetite For Purchasing Real Estate Assets

Chinese Households' Declining Appetite For Purchasing Real Estate Assets

Despite lower interest rates and easier monetary conditions, Chinese consumers’ medium- to long-term loans continued to trend down in Q1, which indicates a declining appetite for purchasing real estate assets and durable goods (Chart 10). COVID-related restrictions have exacerbated matters and weighed heavily on the demand for housing. Home sales from 30 Chinese cities were down by 56% in April from a year ago (Chart 11). House prices have started to deflate in tier-3 cities. Deflation will likely spread to tier-1 and -2 cities due to a pandemic-driven decline in income and confidence. Furthermore, the unemployment rate has picked up, especially among younger workers (Chart 12). Job and income dynamics normally improve after the overall economic cycle bottoms. Therefore, without any measures to boost household income, the demand for housing will remain a drag on the economy in the near term. Chart 11Home Sales Worsened In April Amid COVID Flareups In Major Cities

Home Sales Worsened In April Amid COVID Flareups In Major Cities

Home Sales Worsened In April Amid COVID Flareups In Major Cities

Chart 12Labor Market Dynamics Deteriorated Rapidly

Labor Market Dynamics Deteriorated Rapidly

Labor Market Dynamics Deteriorated Rapidly

Bottom Line: The real estate market has been vital to business cycle recoveries in China since 2009. However, the property market will not recover anytime soon without a substantial boost to household income and a normalization in social and economic activities. Investment Conclusions The policy rhetoric from the Politburo meeting helped to shore up market confidence last Friday. Nevertheless, we do not think that the stimulus measures will be sufficient to produce a rapid business cycle recovery or a sustainable stock market rally (Chart 13A and 13B). Chart 13AIt Is Too Early To Call A Bottoming In Chinese Stocks

It Is Too Early To Call A Bottoming In Chinese Stocks

It Is Too Early To Call A Bottoming In Chinese Stocks

Chart 13BIt Is Too Early To Call A Bottoming In Chinese Stocks

It Is Too Early To Call A Bottoming In Chinese Stocks

It Is Too Early To Call A Bottoming In Chinese Stocks

Given the negative forces from rolling lockdowns and shrinking demand, China’s economy requires a massive government stimulus via direct transfers to households and SMEs. Yet, Beijing is neither ready to abandon its dynamic zero-Covid policy nor provide “irrigation-type” stimulus, especially for households and the property market. The policy stimulus measures announced so far still fall short of what is required to lift the economy. In light of the constraints on household consumption and the property market, economic growth in China is set to underwhelm and stock prices will likely underperform their global counterparts. Jing Sima China Strategist jings@bcaresearch.com Strategic Themes Cyclical Recommendations

Executive Summary Three Problems For European EPS

Three Problems For European EPS

Three Problems For European EPS

The Chinese economic slowdown in response to COVID lockdowns represents a major headwind for European profits in 2022. Weaker global growth creates another hurdle. The energy crisis is the third major problem for European profit growth this year. European profits must be revised downward for 2022, but the impact on 2023 EPS will be small. Cyclical sectors are particularly exposed to these three headwinds, which will hurt profitability this year. The recent relative strength in industrials and materials earnings is likely to buckle in response to weaker global growth, while the defensive characteristics of healthcare and communication services will shine. Within defensive sectors, favor healthcare and communication services versus utilities and consumer staples. Bottom Line: A downward revision of European profits will constrain the ability of European equities to rally in the coming quarters; however, it does not portend another major down leg in European stocks. Nonetheless, the downward revision still points to further underperformance of cyclical equities. Within the defensive sectors, healthcare and communication services are more appealing than utilities and consumer staples shares. The earnings season has begun. According to the MSCI index, Eurozone profit margins are at a 14-year high following a sharp rebound in profits after the pandemic-induced collapse of 2020. Faced with a war in Ukraine and surging inflation, investors worry that this robust profit picture will not last. We share these worries. The near-term outlook for European profits has deteriorated significantly. While the inflation surge amplified by the Ukrainian crisis is an important problem for European firms, it is not the only one. European businesses must also cope with the effect of a growth slowdown in the US goods sector. Moreover, Chinese growth is likely to plunge in response to the tightening lockdowns across the country. As a result, we fear that current earnings estimates for 2022 are too optimistic. Nonetheless, European stocks are unlikely to collapse further. The valuation cushion amassed during the first quarter market shake-out already embeds some downside for 2022 earnings. Additionally, 2023 earnings have much more limited downside than this year’s EPS. Three Problems For European EPS Chart 1European Earnings Profile

European Earnings Profile

European Earnings Profile

Three major problems indicate that the current European earnings estimates for 2022 are too optimistic: namely, China’s economic slowdown, a global economic deterioration, and the consequences of the Ukrainian war on the European economy (Chart 1). China’s Slowdown This publication has regularly highlighted that, even if the Chinese credit impulse is already trying to bottom, the lagged effect of the previous slowdown in credit flows would continue to hurt European growth in the first half of 2022. China’s COVID outbreak and Beijing’s severe policy response only accentuate this headwind. European profits are even more sensitive to Chinese economic fluctuation than European economic activity, which points to a meaningful drag on profitability. Many relationships highlight our concerns: So far, the weakness in the Chinese credit impulse is still consistent with a rapid deterioration of forward earnings growth and could lead to a contraction in forward EPS (Chart 2, top panel). The Chinese new orders index is falling rapidly. The elevated likelihood that China endures even more lockdowns in the coming months implies a sharper drop in orders and further weakness in European EPS (Chart 2, second panel). The CNY is depreciating again, which often coincides with a deflationary shock in global industrial goods that Europe produces. Unsurprisingly, a weaker RMB correlates well with narrowing operating profit margins in the Eurozone (Chart 2, bottom panel). Korean business conditions are deteriorating in response to the softening of the Chinese economy. A weaker RMB will further hurt business sentiment in the peninsula, especially if Chinese lockdowns broaden. The Korean economy is a key barometer of global business conditions because of its high cyclicality. BCA’s EM strategy team anticipates an additional softening in Korea, which portends weaker European profits and margins (Chart 3). Chart 2China's Troubles Trouble Europe Profits

China's Troubles Trouble Europe Profits

China's Troubles Trouble Europe Profits

Chart 3Listen to Korea

Listen to Korea

Listen to Korea

Global Economic Weakness The global growth weakness goes beyond China’s troubles. US economic activity is slowing down in response to higher yields, higher inflation, and the disappearance of pent-up demand following a splurge on goods by consumers during the pandemic. As a result, Q1 GDP growth fell to -1.4% from a quarterly annualized rate of 5.5% in Q4 2021. The weakness in the ISM New Orders-to-Inventory ratio points to continued softness through Q2. EM are not immune to these vulnerabilities either. EM consumers are suffering greatly from surging food and fuel costs. Moreover, EM interest rates continue to rise briskly and the ensuing liquidity removal points to fainter growth ahead. Chart 4The Weaker ISM NOI Is Worrisome

The Weaker ISM NOI Is Worrisome

The Weaker ISM NOI Is Worrisome

The impact of weaker global economic activity on European earnings is straightforward: A falling US ISM New Orders-To-Inventories ratio is a prelude both to slower earnings growth and to narrower profit margins in the Eurozone (Chart 4). Global exports growth has collapsed to 5.5% from more than 20% prior year and is likely to deteriorate further. Historically, weaker global shipments are associated with a slowdown in European forward earnings growth (Chart 4, third panel). Global economic surprises have rebounded this year, but, as we showed two weeks ago, they are likely to move back below zero in the near future. This is a noisy series, but negative surprises often prompt downward revisions to earnings estimates. The Energy Shock Europe is facing an exceptional energy shock that is hurting the region’s growth prospects. Now that Russia is curtailing gas shipments to Poland and Bulgaria, more energy disruptions are likely, which will further hamper domestic growth prospects across the region, while simultaneously elevating the cost of goods sold for firms. However, not all countries will be hit equally by a Russian energy embargo among the major economies. Germany and Italy have the most to lose, while France and the UK are the least at risk (Chart 5). The impact of an oil supply shock on European earnings is negative. When oil prices rise because of strong global aggregate demand, European earnings handle rising energy prices well because the increasing sales volume creates a powerful offset. However, our simple model that accounts for the evolution of oil demand and global policy uncertainty highlights that we do not face a demand shock, but rather a supply shock (Chart 6), which implies that most sectors will suffer from higher energy prices. Chart 5Varying Vulnerabilities To Russia’s Energy Showdown

The Three Forces Hurting European Earnings

The Three Forces Hurting European Earnings

Chart 6Oil's Rally Is Supply-Driven

Oil's Rally Is Supply-Driven

Oil's Rally Is Supply-Driven

Chart 7European Margins Under Pressure

European Margins Under Pressure

European Margins Under Pressure

The inflation passthrough from energy to everything else is not strong enough to protect profit margins. Yes, HICP is elevated, but European PPIs are rising much more rapidly. Historically, such an inability to pass on higher production costs results in slower European profits growth and contracting operating profit margins (Chart 7). The current weakness in consumer confidence and the expected drag on business confidence underscore that pricing power will likely deteriorate from here, which will accentuate the negative impact on profits from the current energy shock. Wage Costs: Not A Problem For Now Wage costs are the one bright spot for European profit margins. European negotiated wages are expanding at a very low rate of 1.6%. Unit labor costs are only expanding at 2.4%, a rate similar to last decade when European core inflation averaged 1%. Chart 8Wages Do Not Hurt Margins

Wages Do Not Hurt Margins

Wages Do Not Hurt Margins

Historically, rising wage rates correlate with rising profitability, not declining margins (Chart 8). This relationship seems paradoxical, but European wages only increase when global aggregate demand is very strong. Due to the degree of operating leverage of European equities, the impact of robust aggregate demand on revenues swamps the impact of accelerating wage growth on production costs. Hence, it will probably take a wage growth rate much higher than the experience of the past 20 years for salaries to start hurting margins. While this is possible, we are many quarters away from this risk becoming reality. Bottom Line: European forward earnings estimates for 2022 are far too elevated in view of the headwinds European businesses are currently facing. The combination of weaker Chinese economic activity, slowing global growth, and a supply-driven energy shock will force significant downward revisions to this year’s EPS. Related Report European Investment StrategyPlenty Of Risks For Cyclical Stocks 2023 EPS should fare better. Chinese authorities are increasingly supporting their economy and this stimulus will impact activity when the lockdowns end. This process will prompt a boom later this year. Global growth will recover once the energy shock recedes. Decelerating European PPI will also help profit margins recover. Following their severe decline in the first quarter, European equities have already embedded a significant valuation cushion to compensate for the transitory shock to earnings. European stocks will not be able to advance meaningfully while 2022 earnings estimates weaken, but they are unlikely to make new lows either. Three Problems For Cyclicals vs Defensives The same three factors that hurt the outlook for European profits for 2022 also confirm that cyclical equities should underperform defensives in the near term. China’s Slowdown Cyclicals are extremely sensitive to a Chinese economic slowdown: The past weakness in the Chinese credit impulse is consistent with a further downgrade of the profit expectations for European cyclicals stocks compared to that of their defensive peers (Chart 9). A deterioration in China’s PMI New Orders heralds a period of weakness in the earnings of cyclical equities. A weak Chinese yuan leads to poor relative earnings (Chart 9). The deterioration in Korean business confidence and the poor performance of Korean equities also leads to weakness in both the earnings and profit margins of cyclical equities relative to those of defensive stocks (Chart 9). Global Growth Weakness The earnings outlook for cyclical sectors relative to defensives is negatively affected by slowing global economic activity: A deterioration in global economic surprises often results in a period of anemic cyclicals’ earnings (Chart 10). The rapidly declining ISM New Orders-to-Inventories ratio is synonymous with underperforming cyclicals’ earnings as well as a contraction in their relative profit margins because of their heightened degree of operating leverage (Chart 10). Weaker global exports confirm the continued risks to cyclicals’ earnings. Chart 9China Is A Threat To Cyclical Equities

China Is A Threat To Cyclical Equities

China Is A Threat To Cyclical Equities

Chart 10Global Growth Threatens Cyclical Stocks

Global Growth Threatens Cyclical Stocks

Global Growth Threatens Cyclical Stocks

The Energy Shock There is no clear relationship between energy prices and the outlook for the profits of cyclical equities relative to those of defensive stocks. Nonetheless, we may deduce that, if elevated energy prices hurt aggregate profits, they will also hurt cyclical profits, since the latter exacerbate the fluctuation of the former. Moreover, Europe’s elevated stagflation risk is consistent with sagging profits for cyclicals relative to those of defensives, because cyclicals experience greater pain from deteriorating economic activity than the benefit they enjoy from higher inflation. Bottom Line: The problems faced by the Chinese economy as well as the risks to global growth are consistent with an underperformance of the profits of cyclical stocks compared to those of defensive equities. Moreover, while higher energy prices are not necessarily a problem for cyclical equities, the elevated perceived stagflation risk is consistent with downward revisions for the relative earnings of cyclicals. This picture indicates that cyclical equities are still vulnerable to some downside relative to the broad market in the near term. A Look at Individual Sectors Chart 11Sectoral Degrees Of Operating Leverage

The Three Forces Hurting European Earnings

The Three Forces Hurting European Earnings

We may distill the impact of China’s problems, the global economic slowdown, and the energy shock on sectoral earnings. A simple starting point is to look at their degree of operating leverage. Based on this observation, financials and consumer discretionary stocks are the sectors most at risk from weaker revenue growth, while utilities are the least exposed (Chart 11). A more complete picture may be gleaned from each sector’s pricing power. Energy Chart 12Improving Energy Margins

Improving Energy Margins

Improving Energy Margins

The energy sector enjoys a significant margin tailwind from the oil supply shock (Chart 12). Nonetheless, this boost is long in the tooth and a pullback is likely if Brent falls toward the $94/bbl level expected by BCA’s Commodity & Energy team in the second half of 2022, and $88/bbl level in 2023. Hence, it is likely that the near-term benefits for the energy sector’s profits are already fully discounted and that the sector could suffer a significant setback in the coming quarters. Industrials The pricing power of industrials (as approximated by the gap between CPI and PPI) is still strong, which creates a tailwind for relative earnings (Chart 13). However, this robustness is under threat in the current environment in which global industrial production, global trade, and global capital goods orders are decelerating (Chart 14). Hence, a period of downgrade for the earnings of industrials relative to the broad market is likely in the coming months. Chart 13Robust Pricing Power For Industrials...

Robust Pricing Power For Industrials...

Robust Pricing Power For Industrials...

Chart 14...But For How Long?

...But For How Long?

...But For How Long?

Financials Chart 15Financials Are Under Siege

Financials Are Under Siege

Financials Are Under Siege

The relative pricing power1 of financials is rapidly deteriorating, despite the recent increase in German yields (Chart 15). Moreover, it is likely to remain weak in a context in which core CPI has yet to decrease. Finally, the potential for a European recession in 2022, or at least, a severe growth slowdown, should lift non-performing loans. As a result, this sector’s earnings could experience a significant downgrade in the near term. Tech The sector’s pricing power was in an uptrend, but it has started to deteriorate in recent quarters (Chart 16). This evolution indicates that that tech earnings and profit margins are likely to suffer relative to the broad market, especially in light of the sector’s high degree of operating leverage. Consumer Discretionary Stocks This sector is suffering from a complete collapse of its pricing power (Chart 17). Additionally, tumbling consumer confidence in Europe and around the world is a significant drag on near-term sales. Consequently, earnings growth as well as profit margins are likely to lag the overall market. Chart 16Crucial Tech Tailwind Dwindling

Crucial Tech Tailwind Dwindling

Crucial Tech Tailwind Dwindling

Chart 17A Problem For Consumer Discretionary Stocks

A Problem For Consumer Discretionary Stocks

A Problem For Consumer Discretionary Stocks

Materials European materials sector’s profit margins stand at a 19-year high compared to that of the broad market. However, relative profit growth has collapsed. The bad news for the sector is that its pricing power is rapidly deteriorating because of surging input costs. It suggests that relative profit growth will become negative as relative profit margins contract (Chart 18). Utilities The pricing power of utilities is plunging because retail electricity prices are not rising as fast as input costs. The negative impact of this adverse pricing on profit margins is consequential (Chart 19). Governments around Europe are likely to continue to pressure this sector to limit the increase in electricity prices to households, which means that utilities are likely to lag other defensive sectors. Chart 18Materials' Outlook Deteriorating Materially

Materials' Outlook Deteriorating Materially

Materials' Outlook Deteriorating Materially

Chart 19Crunch Time For Utilities

Crunch Time For Utilities

Crunch Time For Utilities

Consumer Staples Chart 20Staples Under Duress

Staples Under Duress

Staples Under Duress

The consumer staples sector is facing a similar pricing power problem to that of consumer discretionary stocks: input costs are rising rapidly relative to selling prices (Chart 20). Nonetheless, the earnings of staples will prove more resilient than that of their discretionary counterparts because the staples’ sales volumes are less sensitive to both deteriorating global consumer confidence and falling household real incomes. However, consumer staples equities have already greatly outperformed consumer discretionary stocks. Thus, much of the good news in terms of relative earnings is well discounted and the additional outperformance will be limited. Healthcare Chart 21Healthcare Stocks Still Have Pricing Power

Healthcare Stocks Still Have Pricing Power

Healthcare Stocks Still Have Pricing Power

The pricing power of the healthcare sector remains positive, but it is not as strong as it was ten years ago. Hence, profits growth has scope to improve further compared to the rest of the market (Chart 21). Beyond favorable pricing power dynamics, the industry is insulated from weaker global growth relative to the rest of the broad market. Importantly, the healthcare sector sports one of the lowest degrees of operating leverage in Europe, which will also boost its relative profitability in the current environment. Healthcare is our top defensive sector right now, despite its valuation premium. Communication Services Chart 22Telecom Will Prove Resilient

Telecom Will Prove Resilient

Telecom Will Prove Resilient

The profit growth and profit margins of the European communication services sectors are already under duress because pricing power remains negative. Nonetheless, the contraction in relative growth rates of earnings is extended (Chart 22). Telecom revenues did not benefit from a boost when the economy rebounded after the economic contraction in 2020. This stability is now an asset because the sector will not struggle from slowing global economic activity. In this context, the cheap communication services sector remains an attractive defensive play in Europe. Bottom Line: Looking at sectors individually confirms that the outlook for profit growth is worse for cyclicals than it is for defensive stocks. The recent relative strength in industrials and materials earnings is likely to buckle in response to weaker global growth, while the defensive characteristics of healthcare and communication services will shine. Utilities are under stress, as they stand at the confluence of higher energy prices and the explicit desire of politicians to limit the impact of these higher energy costs on households. Favor healthcare and communication services versus utilities and consumer staples. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Footnotes 1 In the case of financials, we use core CPI as a proxy for the sector’s costs. Eurostat does not publish a PPI for the sector and the main costs are related to labor costs. Tactical Recommendations Cyclical Recommendations Structural Recommendations

Listen to a short summary of this report. Executive Summary Second Fastest Hiking Cycle Ever?

Monthly Portfolio Update: Can The Fed Achieve A Soft Landing? Hint: It Doesn’t Have A Good Track Record

Monthly Portfolio Update: Can The Fed Achieve A Soft Landing? Hint: It Doesn’t Have A Good Track Record

Can the Fed achieve a soft landing, bringing inflation back to its 2% target without causing growth to slow significantly below trend? It has managed this only once in the past (in 2004). Every other cycle triggered a recession or, at best, a fall in the PMI to below 50. Recession is not a certainty. A higher neutral rate than in the past – partly due to the build-up of household savings – means the economy may be unusually robust this time. But the risk is high. We recommend a neutral weighting in equities, with a tilt to more defensive positioning: Overweight the US, and a focus on quality and defensive growth sectors. China’s slowdown is particularly worrying. We expect the RMB to fall, which will put downward pressure on other Emerging Markets.

Monthly Portfolio Update: Can The Fed Achieve A Soft Landing? Hint: It Doesn’t Have A Good Track Record

Monthly Portfolio Update: Can The Fed Achieve A Soft Landing? Hint: It Doesn’t Have A Good Track Record

Bottom Line: Investors should maintain low-risk portfolio positioning until the outcome of the sharp tightening of financial conditions is clearer. Recommended Allocation

Monthly Portfolio Update: Can The Fed Achieve A Soft Landing? Hint: It Doesn’t Have A Good Track Record

Monthly Portfolio Update: Can The Fed Achieve A Soft Landing? Hint: It Doesn’t Have A Good Track Record

The key to the performance of financial markets over the next year is whether the Fed and other central banks can kill inflation without killing economic growth. This is not impossible. But the risk that aggressive tightening of monetary policy triggers a recession – or at best a sharp slowdown – is high. Investors should maintain relatively low-risk portfolio positioning. If the Fed raises rates in line with what the futures market is projecting – by 286 basis points over the next 12 months – it will be the second fastest tightening on record, after only the “full Volcker” of 1980-1981 (Chart 1). Other central banks, even in countries and regions with much weaker growth than the US, are predicted to tighten almost as aggressively (Table 1). At the same time, the Fed will start to run down its balance-sheet rapidly; we estimate its holdings of US Treasurys will fall by more than $1 trillion by end-2023 (Chart 2). What was the impact on the economy of previous Fed hiking cycles? It varied, but on only one occasion in the past 50 years (2004) was there neither a recession nor a fall of the Manufacturing ISM to below 50 in the two years or so following the first hike (Table 2).1 The ISM (and other global PMIs) falling to below 50 is important because that is typically the dividing line between equities outperforming bonds and vice versa (Chart 3). Chart 1Second Fastest Hiking Cycle Ever?

Monthly Portfolio Update: Can The Fed Achieve A Soft Landing? Hint: It Doesn’t Have A Good Track Record

Monthly Portfolio Update: Can The Fed Achieve A Soft Landing? Hint: It Doesn’t Have A Good Track Record

Table 1Futures Projected Interest Rate Hikes

Monthly Portfolio Update: Can The Fed Achieve A Soft Landing? Hint: It Doesn’t Have A Good Track Record