Equities

Highlights Several factors point to both an improvement and a deterioration in economic and financial market conditions, underscoring that the 6- to 12-month investment outlook is unavoidably uncertain. On the one hand, the US will likely avoid a recession over the coming year, slowing headline inflation will boost real wages and lower the equity risk premium, bond yields will not move much higher this year, and US services spending will support consumption as the pandemic continues to recede in importance. These are positive factors that will work to support economic activity and risky asset prices. On the other hand, the US will likely experience a recession scare focused on the housing market, the European economy may contract, Omicron’s spread in China threatens a further rise in shipping costs and a trade shock for Europe, and US inflation expectations may unanchor despite a falling inflation rate. For now, investors should remain minimally-overweight stocks over a 6- to 12-month time horizon, although that assessment may change in either a bullish or bearish direction over the coming several months. Within a global equity allocation, we recommend that investors maintain a neutral regional stance. The larger risk of a recession in Europe than in the US would normally imply that investors should be overweight US stocks, but euro area stocks have already underperformed global stocks significantly since Russia’s invasion of Ukraine. Within a fixed-income portfolio, we recommend that investors maintain a modestly short duration stance despite our forecast that long-maturity bond yields will not increase much this year. More nimble investors should be neutral duration, and should test a long stance if US data releases begin to exhibit meaningfully negative surprises. The US dollar is likely to strengthen over the near term, but we expect it to be lower a year from today. The Scourge Of Harry Truman US President Truman famously lamented the need for “one-handed” economists. His complaint reflected how essential it is for economic policymakers to receive clear advice about the best path forward. Investors understandably have even less tolerance for ambiguity than Truman did about the macro landscape and the attendant investment implications. However, there are times when the economic and financial market outlook is unavoidably uncertain. The current economic and geopolitical environment easily qualifies as one of those instances. Several factors point to both an improvement and a deterioration in economic and financial market conditions, which we review in detail below. The likely avoidance of a recession in the US over the coming year suggests that investors should remain minimally-overweight stocks over a 6- to 12-month time horizon, although that assessment may change in either a bullish or bearish direction over the coming several months. What Could Go Right The US Will Likely Avoid A Recession Over The Coming Year Chart I-1The Odds Of A US Recession Are Currently Low

The Odds Of A US Recession Are Currently Low

The Odds Of A US Recession Are Currently Low

We downgraded our odds of an above-trend 2022 growth scenario in last month’s report,1 but noted that a stagflation-lite environment of below-trend growth and above-target inflation was a more likely outcome than recession. We based this assessment on our view that the US neutral rate of interest is likely higher than the Fed and investors expect, which we discussed at length in past reports.2 Chart I-1 highlights that our recession probability indicator also supports this view, as it does not yet signal that a recession is on the horizon.3 Table I-1 highlights the components of the model (which is significantly influenced by the Conference Board’s LEI), and shows that the model is not providing a meaningful warning signal. The Fed funds rate component of the model will likely flash red next month following the FOMC meeting, and we have listed it as providing a warning signal in Table I-1. But rising rates themselves have not proven to be a particularly timely indicator of a recession; this is similarly true with rising inflation expectations and oil prices. We noted in last month’s report that a surge in oil prices has not been an especially consistent indicator of a recession since 2000. Table I-1The Components Of Our Recession Model Are Not Yet Flashing A Warning Sign

May 2022

May 2022

The yield curve component of the model is based on the spread between the 10-year Treasury yield and the 3-month T-bill yield in order to minimize false recession signals, and we agree that the 10-year / 2-year spread has better leading properties. But even the latter curve measure has recently moved back into positive territory (Chart I-2), which will certainly qualify as a false yield curve signal if a recession is avoided over the coming 18 months. Within the components of the Conference Board’s LEI, Table I-1 highlights that there have been signs of weakness from the manufacturing sector, consumer expectations, and the credit market. Chart I-3 aggregates the deviation of six of these components from their trend, and shows that they have indeed been consistent with a significant slowdown in economic activity. Chart I-2The 2/10 Yield Curve Is No Longer Inverted

The 2/10 Yield Curve Is No Longer Inverted

The 2/10 Yield Curve Is No Longer Inverted

Chart I-3The Weakest Components Of The Conference Board's LEI Are Not Yet Signaling A Recession

The Weakest Components Of The Conference Board's LEI Are Not Yet Signaling A Recession

The Weakest Components Of The Conference Board's LEI Are Not Yet Signaling A Recession

However, two caveats are warranted. First, part of this weakness reflects the ongoing shift from goods to services spending, unraveling the massive surge in goods spending that occurred during the pandemic (Chart I-4). Second, Chart I-3 highlights that similar weaknesses occurred in the past outside of the context of a recession, most notably in 1995/1996, in the aftermath of the 1994 bond market crisis; in 1998/1999, following the Long-Term Capital Management (LTCM) crisis; in 2015, following the collapse in oil prices; and, finally, in 2018/2019, in response to the Trump administration’s trade war. None of these instances resulted in a contraction in output. Headline Inflation Is Likely To Come Down Headline consumer price inflation is currently extremely high in the US. Rising prices do not just reflect energy, food, or pandemic-related effects. Chart I-5 highlights that trimmed mean CPI and PCE inflation rates have accelerated significantly since last summer, and are currently running at 6% and 3.6% year-over-year rates, respectively. Chart I-4Part Of The Weakness In Manufacturing Activity Indicators Reflects A Shift In Spending From Goods To Services

Part Of The Weakness In Manufacturing Activity Indicators Reflects A Shift In Spending From Goods To Services

Part Of The Weakness In Manufacturing Activity Indicators Reflects A Shift In Spending From Goods To Services

Chart I-5There Is More To High Inflation Than Food, Energy, And Pandemic-Related Effects...

There Is More To High Inflation Than Food, Energy, And Pandemic-Related Effects...

There Is More To High Inflation Than Food, Energy, And Pandemic-Related Effects...

However, it seems likely that inflation has peaked in the US (or is about to do so), even abstracting from base effects.Chart I-6 highlights that the one-month rate of change in trimmed mean measures seemingly peaked in October and January, and shows that the level of used car prices also appears to be trending lower (panel 2). The ongoing shift away from goods to services spending noted above will also push core ex-COVID-related consumer prices lower. Finally, BCA’s Commodity & Energy strategy service is forecasting that Brent crude oil prices will average roughly $90/bbl for the remainder of the year, which would likely bring US gasoline prices back toward $3.50/gallon and will lower both headline inflation and energy passthrough effects to core prices (Chart I-7). Chart I-6... But The Rate Of Headline Inflation Has Likely Peaked

... But The Rate Of Headline Inflation Has Likely Peaked

... But The Rate Of Headline Inflation Has Likely Peaked

Chart I-7Our Forecast For Oil Implies US Gasoline Prices Will Fall

Our Forecast For Oil Implies US Gasoline Prices Will Fall

Our Forecast For Oil Implies US Gasoline Prices Will Fall

A meaningful deceleration in inflation will help reverse some of the recent decline in real wage growth that has occurred, and will likely lower the equity risk premium (see Section 2 of this month’s report). Long-Maturity Bond Yields Will Not Move Much Higher This Year Chart I-8Our Inflation Probability Model Is Signaling Core Inflation That Is Roughly In Line With The Fed's Latest Forecast

Our Inflation Probability Model Is Signaling Core Inflation That Is Roughly In Line With The Fed's Latest Forecast

Our Inflation Probability Model Is Signaling Core Inflation That Is Roughly In Line With The Fed's Latest Forecast

Chart I-8 highlights that our inflation probability model is currently signaling core PCE inflation of roughly 4.3% over the coming year. This is only moderately above the Fed’s forecast for this year, suggesting that a moderation in the rate of inflation makes it more likely that the Fed will raise rates in line with, or only moderately above, what was projected in the March Summary of Economic Projections (1.9% by the end of this year, and 2.8% by the end of 2023). By contrast, Chart I-9 highlights that the OIS curve is pricing the Fed funds rate at 80 basis points higher by the end of this year than what the Fed projected in March, suggesting that the bar for further hawkish surprises is quite high. We agree that the Fed will likely front-load a good portion of its planned tightening this year, and we agree that a 50 basis point hike is likely next month and also possibly in June. However, it is quite possible that the Fed will ultimately raise rates over the coming year at a slower pace than investors currently anticipate, which would lower yields at the front end of the curve. Chart I-9The Bar For Further Hawkish Surprises From The Fed Is Quite High

May 2022

May 2022

If short-maturity yields are flat or trend modestly lower over the coming year, then a significant further rise in long-maturity yields would likely necessitate a major shift in neutral rate expectations on the part of investors or the Fed. We believe that such a shift will eventually occur, as the economic justification for long-maturity bond yields well below trend rates of economic growth disappeared in the latter half of the last economic expansion. However, we noted in last month’s Special Report that a low neutral rate outlook has become entrenched in the minds of investors and the Fed, and is only likely to change once the Fed funds rate rises meaningfully and a recession does not materialize.4 BCA’s fixed-income team currently recommends that investors maintain a neutral duration stance; the Bank Credit Analyst service is more inclined to recommend a modestly short stance. However, the key point for investors is that another significant rise in long-maturity bond yields is unlikely over the coming year, which is positive for economic activity and investor sentiment. The Pandemic Will Recede In Importance, Supporting Services Spending Chart I-10COVID Hospitalizations And Deaths Remain Low In The DM World

COVID Hospitalizations And Deaths Remain Low In The DM World

COVID Hospitalizations And Deaths Remain Low In The DM World

While the pandemic is clearly not over in China (discussed below), it is likely to continue to recede in importance in the US and other highly vaccinated, and relatively highly exposed DM economies. Despite the fact that confirmed cases of COVID-19 have risen in the DM world in March and April, Chart I-10 highlights that there has been very little increase in ICU patients or deaths. A recent study from the US CDC suggests that 58% of the US population overall and more than 75% of younger children have been infected with the SARS-COV-2 virus since the start of the pandemic.5 When combined with a vaccination rate close to 70%, that signals an extraordinarily high national immunity to severe illness from the disease. Chart I-11 also highlights that deliveries of Pfizer’s Paxlovid continue to climb in the US, a drug that seemingly works against all known variants and has been found to reduce hospitalizations from COVID significantly if taken within the first five days of symptoms. Given that the decline in services spending that we showed in Chart I-4 has been clearly linked to the pandemic, we expect that a slowing pandemic will continue to support services spending. Goods spending is normally a more forceful driver of economic activity than is the case for services spending, but the magnitude of the recent contribution to growth from services spending has been absolutely unprecedented in the post-World War II economic environment (Chart I-12). This underscores that a continued recovery in services spending relative to its pre-pandemic trend will provide a ballast to overall consumer spending as goods spending continues to normalize. Chart I-11Paxlovid To The Rescue!

Paxlovid To The Rescue!

Paxlovid To The Rescue!

Chart I-12Real Services Spending Will Continue To Be A Forceful Driver Of US Economic Activity

Real Services Spending Will Continue To Be A Forceful Driver Of US Economic Activity

Real Services Spending Will Continue To Be A Forceful Driver Of US Economic Activity

What Could Go Wrong The US Will Likely Experience A Recession Scare Chart I-13US Housing Affordability Has Cratered, In Large Part Due To Surging House Prices

US Housing Affordability Has Cratered, In Large Part Due To Surging House Prices

US Housing Affordability Has Cratered, In Large Part Due To Surging House Prices

Despite our view that the US economy will avoid a recession over the coming year, it seems likely that investors will experience a recession scare at some point over the coming 6 to 12 months. Even though it has recently moved back into positive territory, the inversion of the 2-10 yield curve has set the scene for a recessionary overtone to any visible weakness in the US macro data over the coming months. We noted above that the manufacturing and goods-producing sectors of the US economy are likely to slow as spending returns to services. More importantly, the extremely sharp increase in mortgage rates will likely cause at least a temporary slowdown in US housing activity, even if that slowdown does not ultimately prove to be contractionary.Chart I-13 highlights that the recent increase in mortgage rates will cause US housing affordability to deteriorate back to 2007 levels. While rising mortgage rates will be the proximate cause of this deterioration in affordability, panel 2 highlights that the real culprit has been a significant increase in house prices relative to income. There is strong evidence pointing to the fact that US real residential investment has been too weak since the global financial crisis (GFC).6 We agree that high prices will likely spur additional housing construction (which will support growth). But over the nearer-term, the sharp deterioration in affordability may imply that house price appreciation will have to fall below the rate of income growth, which would represent a very sharp correction in house price gains that would almost assuredly appear recessionary for a time. The European Economy May Contract We have discussed the risk of a European recession in past reports, and noted that it would be almost certain to occur in a scenario in which Russia’s energy exports to Europe were to be completely cut off. We continue to see this as an unlikely scenario, although the odds have increased significantly of late in light of Russia’s halt of gas supplies to Bulgaria and Poland and Germany’s apparent acceptance of an oil embargo against Russia. However, Chart I-14 highlights that a recession, at least a technical one, may occur in Germany even if its imports of Russian natural gas are not interrupted. The chart shows that the German IFO business climate indicator for manufacturing has deteriorated more than the Markit PMI has, and panel 2 highlights that IFO-reported service sector sentiment is considerably worse than what was suggested by the Markit services PMI. Chart I-15 highlights that European stocks are not fully priced for a European recession, either in relative or absolute terms. This underscores the risk to global equities if real euro area growth falls meaningfully below current consensus expectations of 1.9% this year. Chart I-14German Business Sentiment Suggests A Possible Recession

German Business Sentiment Suggests A Possible Recession

German Business Sentiment Suggests A Possible Recession

Chart I-15Euro Area Stocks Are Not Fully Priced For A European Recession

Euro Area Stocks Are Not Fully Priced For A European Recession

Euro Area Stocks Are Not Fully Priced For A European Recession

Omicron Will Continue To Spread In China Table I-2The Ports Of Shanghai and Ningbo Are Quite Important To Chinese Trade Flows

May 2022

May 2022

Confirmed cases of COVID-19 have surged in China over the past two months, and it is now clear that the country’s zero-tolerance policy will fail to contain the spread of the disease. We initially downgraded the odds of our above-trend growth scenario in our January report specifically in response to the risk that the Omicron variant of the virus posed to China.7 That risk that is now manifesting itself most acutely in Shanghai, but also increasingly in other coastal and northeastern provinces. Chart I-16COVID Restrictions In China Are Causing Significant Delays In Suppliers' Delivery Times

COVID Restrictions In China Are Causing Significant Delays In Suppliers' Delivery Times

COVID Restrictions In China Are Causing Significant Delays In Suppliers' Delivery Times

China’s COVID surge has two implications for the global economic and financial market outlook. The first is that the surge has led to increased port congestion and shipping delays, which clearly threaten to cause a further rise in global shipping costs. We have noted in past reports that shipping costs from China to the West Coast of the US surged following the one month shutdown of the port of Yantian last year. Table I-2 highlights that the ports of Shanghai and nearby Ningbo handle nearly 30% of China’s total ocean shipping volume. Chart I-16 highlights that road traffic restrictions in the Yangtze River Delta have caused significant delays in suppliers’ delivery times, further raising the risk of bottlenecks that may take months to clear. Chart I-17China's Battle With Omicron Further Raises The Risk Of A Euro Area Recession

China's Battle With Omicron Further Raises The Risk Of A Euro Area Recession

China's Battle With Omicron Further Raises The Risk Of A Euro Area Recession

The second implication of China’s COVID surge is that China’s contribution to global growth is at risk of declining significantly further, at least for a time. If Chinese economic activity slows sharply in response to the lockdowns and a further spread of the disease, we fully expect Chinese policymakers to provide further stimulus to support household income in line with what occurred in DM countries two years ago. In addition, some investors have argued that reduced commodity demand from China is actually desirable in the current environment, as it would further reduce inflationary pressure in the US and other developed economies. However, Chart I-17 highlights that Chinese import growth has already slowed very significantly, which has clearly impacted euro area exports. European exports to China are not predominantly commodity-based, and it is yet unclear whether the form of stimulus that Chinese policymakers will introduce will be particularly import-intensive. As such, China’s failure to contain Omicron further adds to the risk of the European recession we noted above, and threatens our view that US headline inflation will trend lower this year. Inflation Expectations May Unanchor Despite Slowing Inflation We discussed above that US inflation will decelerate this year and that this may allow the Fed to raise interest rates at a slower pace than currently expected by market participants. One risk to this view is the possibility that inflation expectations may unanchor to the upside, despite an easing in inflation. Even though inflation expectations have not trended in a different direction than actual inflation since the GFC, Chart I-18 highlights that this has occurred in the past (from 2001-2006). In our view, the level of inflation that is likely to prevail over the coming two years will be an extremely important determinant of whether inflation expectations break above their post-2000 range. For now, Chart I-18 highlights that the Fed’s expectation for core inflation this year is reasonable, but it remains an open question whether core inflation will decelerate below 3% next year as the Fed is forecasting. This is notable, because US core PCE inflation peaked at a rate of 2.6% during the 2002-2007 economic expansion, which is the period when stable long-dated inflation expectations were prevalent. Chart I-19 highlights that market-based inflation expectations are currently challenging or have risen above their 2004-2014 average. We noted in last month’s report that long-dated household inflation expectations will be historically low, even if inflation decelerates in line with what near-dated CPI swaps are forecasting. Chart I-18Inflation Expectations May Still Unanchor Even If The Inflation Rate Comes Down

Inflation Expectations May Still Unanchor Even If The Inflation Rate Comes Down

Inflation Expectations May Still Unanchor Even If The Inflation Rate Comes Down

Chart I-19Market-Based Inflation Expectations May Soon Rise Above Pre-GFC Range

Market-Based Inflation Expectations May Soon Rise Above Pre-GFC Range

Market-Based Inflation Expectations May Soon Rise Above Pre-GFC Range

The bottom line for investors is that a slowing of inflation over the coming several months may not be enough to prevent long-term inflation expectations from rising. That raises the risk of an even more aggressive pace of interest rates than currently expected by investors, because the Fed is determined to avoid repeating the mistakes of the 1970s when rising inflation expectations led to a wage-price spiral that required years of comparatively tight monetary policy to correct. By contrast, the Fed will view a temporary income-statement recession stemming from a sharp rise in interest rates as the lesser of two evils. A recession to prevent a long-lasting wage-price spiral would also probably be better for investors over the longer run, but a recession would clearly imply a significant decline in risky asset prices at some point over the coming two years were it to occur. Investment Conclusions Chart I-20Despite The Risks Facing Europe, Euro Area Stocks Are Not A Clear Underweight Candidate

Despite The Risks Facing Europe, Euro Area Stocks Are Not A Clear Underweight Candidate

Despite The Risks Facing Europe, Euro Area Stocks Are Not A Clear Underweight Candidate

From the perspective of allocating to risky assets, the most important question for investors to answer is whether the US is likely to experience a recession over the coming year. As we noted above, in our view the answer is “no”, which implies that US earnings growth will remain positive and that investors should not be underweight stocks within a global multi-asset portfolio. It is true that earnings can decline outside of the context of a recession, but we discuss in Section 2 of our report that this has almost always been associated with a significant contraction in profit margins. The factors that have historically been associated with a nonrecessionary decline in profit margins may occur later this year, but our indicators so far point more to flat margins rather than a significant decline. For now, investors should remain minimally-overweight stocks over a 6 to 12 month time horizon, although that assessment may change in either a bullish or bearish direction over the coming several months. Within a global equity allocation, we recommend that investors maintain a neutral regional allocation. The larger risk of a recession in Europe than in the US would normally imply that investors should be overweight US stocks, but euro area stocks have already underperformed global stocks significantly since Russia’s invasion of Ukraine. Chart I-15 highlighted that they will underperform further if euro area growth turns negative. It is not clear, however, if that risk warrants an underweight stance today, especially considering the enormous valuation advantage offered by euro area stocks versus their US counterparts and the fact that the euro has already fallen to a five-year low (Chart I-20). Chart I-21Favor A Neutral Stance Towards Cyclical Stocks Versus Defensives

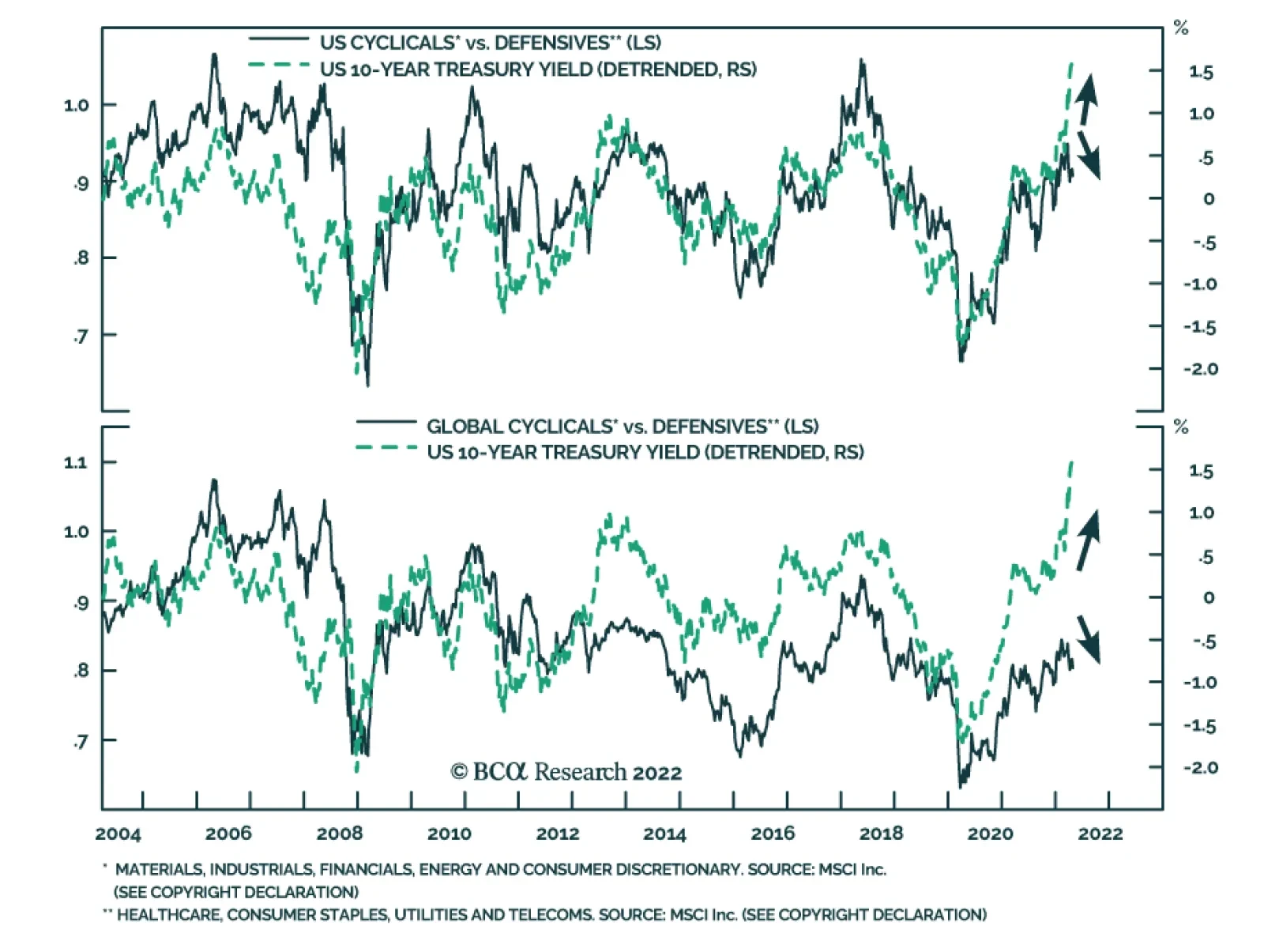

Favor A Neutral Stance Towards Cyclical Stocks Versus Defensives

Favor A Neutral Stance Towards Cyclical Stocks Versus Defensives

Within the dimensions of the equity market, Chart I-21 highlights that the outperformance of cyclicals versus defensives was already late at the onset of Russia’s invasion of Ukraine, and that the uptrend in relative performance has seemingly ended. Still, a moderately overweight stance toward stocks overall does not especially support an underweight stance toward cyclicals; therefore, we recommend a neutral stance over the coming year. We continue to recommend that investors (modestly) favor value stocks over growth stocks on the basis of better value and as a hedge against potentially higher long-maturity yields, although we acknowledge that most of the outsized outperformance of growth stocks during the pandemic has already reversed. Despite their recent underperformance, we continue to favor global small-cap stocks over their large-cap peers, as they are now unequivocally inexpensive and have seemingly already priced in a likely recession scare in the US later this year (Chart I-22). Within a fixed-income portfolio, we recommend that investors maintain a modestly short duration stance despite our forecast that long-maturity bond yields will not increase much this year. We are wary of recommending a neutral duration stance given the possibility that investors or the Fed may upwardly revise their neutral rate expectations earlier than we anticipate; however, investors are also likely to see long-maturity yields come down for a time in response to a housing market slowdown over the coming several months. More nimble investors should be neutral duration, and should test a long stance if US data releases begin to exhibit meaningfully negative surprises. Finally, while we are bearish toward the dollar on a 6- to 12-month time horizon, it is likely to strengthen over the near term. Chart I-23 highlights that our composite technical indicator for the US dollar is now clearly in overbought territory. We expect that a downtrend will begin once the war in Ukraine reaches a durable conclusion and clarity about the economic impact of the spread of Omicron in China – and the likely policy response – emerges. Chart I-22The Selloff In Small Caps Seems Overdone

The Selloff In Small Caps Seems Overdone

The Selloff In Small Caps Seems Overdone

Chart I-23US Dollar And Indicator The Dollar Is Ripe For A Major Pullback Beyond Likely Near-Term Strength

US Dollar And Indicator The Dollar Is Ripe For A Major Pullback Beyond Likely Near-Term Strength

US Dollar And Indicator The Dollar Is Ripe For A Major Pullback Beyond Likely Near-Term Strength

Jonathan LaBerge, CFA Vice President The Bank Credit Analyst April 28, 2022 Next Report: May 26, 2022 II. The US Equity Market: A Fundamental, Technical, And Value-Based Review All four of our US Equity indicators are currently pointing in a bearish direction. Our Monetary Indicator has fallen to a three decade low, our Technical Indicator has broken into negative territory, our Valuation Indicator still signals extreme equity pricing, and our Speculation Indicator does not yet support a contrarian buy signal. Still, we do not expect a US recession over the coming year, which implies that S&P 500 revenue growth will stay positive. Nonrecessionary earnings contractions are rare, and are almost always associated with a significant contraction in profit margins. Our new profit margin warning indicator currently suggests the odds of falling margins are low, although the risks may rise later this year. Stocks are extremely expensive, but rich valuations are being driven by extremely low real bond yields, rather than investor exuberance. Valuation is unlikely to impact US stock market performance significantly over the coming year unless long-maturity bond yields rise substantially further. Technical analysis of stock prices has a long and successful history at boosting investment performance, which ostensibly suggests that investors should be paying more attention to technical conditions in the current environment. However, technical trading rules have been less helpful in expansionary environments when inflation is above average and when stock prices and bond yields are less likely to be positively correlated (as is currently the case). As such, the recent technical breakdown of the US equity market may simply reflect a reduced signal-to-noise ratio associated with these economic and financial market regimes. For now, we see our indicators as supportive of a cautious, minimally-overweight stance toward stocks within a multi-asset portfolio over the coming 6 to 12 months. Rising odds of a recession, declining profit margins, and a large increase in investor or Fed expectations for the neutral rate of interest are the most significant threats to the equity market, the risks of which should be monitored closely by investors. In Section 1 of our report, we reviewed why a recession in the US is unlikely over the coming 6 to 12 months. However, we also highlighted that the risks to the economic outlook are meaningful and that an aggressively overweight stance toward risky assets is currently unwarranted. During times of significant uncertainty, investors should pay relatively more attention to long-term economic and financial market indicators with a reliable track record. In this report we begin by briefly reviewing the message from our US Equity Indicators, and then turn to a deeper examination of the top-down outlook for earnings, the determinants of rich valuation in the US stock market, and whether investors should rely on technical indicators in the current environment. We conclude that, while an indicator-based approach is providing mixed signals about the US equity market, we generally see our indicators as supportive of a cautious, minimally-overweight stance toward stocks within a multi-asset portfolio. Aside from tracking the risk of a recession, investors should be closely attuned to signs of a contraction in profit margins or shifting neutral rate expectations as a basis to reduce equity exposure to below-benchmark levels. A Brief Review Of Our US Equity Indicators Chart II-1Our Equity Indicators Are Pointing In A Bearish Direction

Our Equity Indicators Are Pointing In A Bearish Direction

Our Equity Indicators Are Pointing In A Bearish Direction

Chart II-1 presents our US Equity Indicators, which we update each month in Section 3 of our report. We highlight our observations below: Chart II-1 shows that our Monetary Indicator has fallen to its lowest level since 1995, when the Fed surprised investors and shifted rapidly in a hawkish direction. The indicator is most acutely impacted by the speed of the rise in 10-year Treasury yields and a massive surge in the BCA Short Rate Indicator to levels that have not prevailed since the late 1970s (Chart II-2). Our Technical Indicator has recently broken into negative territory, which we have traditionally interpreted as a sign to sell stocks. The indicator has been dragged lower by a deterioration in stock market breadth across several tracked measures and by weak sentiment (Chart II-3). The momentum component of the indicator is fractionally positive but is exhibiting clear weakness. Our Valuation Indicator continues to highlight that US equities are extremely overvalued relative to their history, despite the recent sell-off in stock prices. Our Speculation Indicator arguably provides the least negative signal of our four indicators, at least from a contrarian perspective. In Q1 2021, the indicator nearly reached the all-time high set in March 2000, but it has since retreated significantly and has exited extremely speculative territory. While this may eventually provide a positive signal for stocks, equity returns have historically been below average during months when the indicator declines. Thus, the downtrend in the Speculation Indicator still points to weakness in stock prices, at least over the nearer term. Chart II-2Our Monetary Indicator Is Falling In Part Because Of Surging Interest Rate Expectations

Our Monetary Indicator Is Falling In Part Because Of Surging Interest Rate Expectations

Our Monetary Indicator Is Falling In Part Because Of Surging Interest Rate Expectations

Chart II-3All Three Components Of Our Technical Indicator Are Falling

All Three Components Of Our Technical Indicator Are Falling

All Three Components Of Our Technical Indicator Are Falling

In summary, all four of our US Equity indicators are currently pointing in a bearish direction, which clearly argues against an aggressively overweight stance favoring equities within a multi-asset portfolio. At the same time, we reviewed the odds of a US recession over the coming year in Section 1 of our report and argued that a recession is not likely over the coming 12 months. Thus, one key question for investors is whether a nonrecessionary contraction in earnings is likely over the coming year. We address this question in the next section of our report, before turning to a deeper examination of the relative importance of equity valuation and technical indicators. Gauging The Risk Of A Nonrecessionary Earnings Contraction Chart II-4Nonrecessionary Earnings Declines Usually Occur Due To Falling Margins

Nonrecessionary Earnings Declines Usually Occur Due To Falling Margins

Nonrecessionary Earnings Declines Usually Occur Due To Falling Margins

Based on S&P data, there have been five cases since 1960 when 12-month trailing earnings per share fell year-over-year, while the economy continued to expand (Chart II-4). Sales per share growth remained positive in four of these cases (panel 2), underscoring that falling profit margins have been mostly responsible for these nonrecessionary earnings declines. We have noted our concern about how elevated US profit margins have become and have argued that a significant further expansion is not likely to occur over the coming 12-24 months.8 To gauge the risk of a sizeable decline in margins over the coming year, we construct a new indicator based on the seven instances when S&P 500 margins fell outside the context of a recession. This includes two cases when margins fell but earnings did not (because of buoyant revenue growth). We based the indicator on these five factors: Changes in unit labor cost growth to measure the impact of wage costs on firm profitability; Lagging changes in commodity prices as a proxy for material costs; The level of real short-term interest rates as a proxy for borrowing costs; Changes in a sales growth proxy to measure the impact of operating leverage on margins; And changes in the ISM manufacturing index to capture any residual impact on margins from the business cycle. Chart II-5The Odds Of A Nonrecessionary Profit Margin Contraction Are Currently Low

The Odds Of A Nonrecessionary Profit Margin Contraction Are Currently Low

The Odds Of A Nonrecessionary Profit Margin Contraction Are Currently Low

Chart II-5 presents the indicator, which is shaded both for recessionary periods and the seven nonrecessionary margin contraction episodes we identified. While the indicator does not perfectly predict margin contractions outside of recessions, it did signal 50% or greater odds of a margin contraction in four of the seven episodes we examined, and signals high odds of a contraction in margins during recessions. Among the three cases in which the indicator failed to indicate falling margins during an expansion, two of those failures were episodes when earnings growth did not ultimately contract. The inability to explain the 1997-1998 margin contraction is the most relevant failure of the indicator, in addition to two false signals in 1963 and 1988. Still, the approach provides a useful framework to gauge the risk of falling profit margins, and the results provide an interesting and somewhat surprising message about the relative importance of the factors we included. We would have expected that accelerating wages would have been the most significant factor explaining nonrecessionary profit margin declines. Wages were highly significant, but they were the second most important factor behind our sales growth proxy. Lagged commodity prices were the third most significant factor, followed by real short-term interest rates. Changes in the ISM manufacturing index were least significant, underscoring that our sales growth proxy already captures most of the effect of the business cycle on profit margins. This suggests that operating leverage is an important determinant of margins during economic expansions, and that investors should be most concerned about declining profit margins when both revenue growth is slowing significantly and wage growth is accelerating. The indicator currently points to low odds of a nonrecessionary margin contraction, but this is likely to change over the coming year. We expect that all five of the factors will evolve in a fashion that is negative for margins over the coming twelve months: While the pace of its increase is slowing, median wage growth continues to accelerate, even when adjusting for the fact that 1st quartile wage growth is growing at an above-average rate (Chart II-6). Combining the latter with higher odds of at or below-trend growth this year implies that unit labor costs may rise further over the coming twelve months. Analysts expect S&P 500 revenue growth to slow nontrivially over the coming year (Chart II-7). Current expectations point to growth slowing to a level that would still be quite strong relative to what has prevailed over the past decade; however, accelerating wage costs in lockstep with decelerating revenue growth is exactly the type of combination that has historically been associated with falling margins during economic expansions. Chart II-6Wage Growth Is Accelerating...

Wage Growth Is Accelerating...

Wage Growth Is Accelerating...

Chart II-7...And Revenue Growth Is Set To Slow

...And Revenue Growth Is Set To Slow

...And Revenue Growth Is Set To Slow

Although these are less impactful factors, the lagged effect of the recent surge in commodity prices will also weigh on margins over the coming year, as will rising real interest rates and a likely slowdown in manufacturing activity in response to slower goods spending. In addition to our new indicator, we have two other tools at our disposal to track the odds of a decline in profit margins over the coming year. First, Chart II-8 illustrates that an industry operating margin diffusion index does a decent job at leading turning points in S&P 500 profit margins, despite its volatility. And second, Chart II-9 highlights that changes in the sales and profit margin diffusion indexes sourced from the Atlanta Fed’s Business Inflation Expectations Survey have predicted turning points in operating sales per share and margins over the past decade. Chart II-9 does suggest that profit margins may not rise further, but flat margins are not likely to be a threat to earnings growth over the coming year if a recession is avoided (as we expect). Chart II-8Sector Diffusion Indexes Are Not Signaling A Major Warning Sign For Margins...

Sector Diffusion Indexes Are Not Signaling A Major Warning Sign For Margins...

Sector Diffusion Indexes Are Not Signaling A Major Warning Sign For Margins...

Chart II-9...Neither Are The Atlanta Fed Business Sales And Margin Diffusion Indexes

...Neither Are The Atlanta Fed Business Sales And Margin Diffusion Indexes

...Neither Are The Atlanta Fed Business Sales And Margin Diffusion Indexes

The conclusion for investors is that the odds of a decline in profit margins over the coming year are elevated and should be monitored, but are seemingly not yet imminent. In combination with expectations for slowing revenue growth, this implies, for now, that earnings growth over the coming year will be low but positive. Valuation, Interest Rates, And The Equity Risk Premium As noted above, our Valuation Indicator continues to highlight that US Equities are extremely overvalued relative to their history. Our Valuation Indicator is a composite of different valuation measures, and we sometimes receive questions from investors asking about the seemingly different messages provided by these different metrics. For example, Chart II-10 highlights that equity valuation has almost, but not fully, returned to late-1990 conditions based on the Price/Earnings (P/E) ratio, but is seemingly more expensive based on the Price/Book (P/B) and especially Price/Sales (P/S) ratios. In our view, this apparent discrepancy is easily resolved. Relative to the P/E ratio, both the P/B and especially P/S ratios are impacted by changes in aggregate profit margins, which have risen structurally over the past two decades because of the rising share of broadly-defined technology companies in the US equity index (Chart II-11). Barring a major shift in the profitability of US tech companies over the coming year, we do not see discrepancies between the P/E, P/B, or P/S ratios as being particularly informative for investors. As an additional point, we also do not see the Shiller P/E or other cyclically-adjusted P/E measures as providing any extra information about the richness or cheapness of US equities today, as these measures tend to move in line with the 12-month forward P/E ratio (Chart II-12). Chart II-10US Equities Are Extremely Overvalued, Based On Several Valuation Metrics

US Equities Are Extremely Overvalued, Based On Several Valuation Metrics

US Equities Are Extremely Overvalued, Based On Several Valuation Metrics

Chart II-11Tech Margins Have Caused Stocks To Look Especially Expensive On A Price/Sales Basis

Tech Margins Have Caused Stocks To Look Especially Expensive On A Price/Sales Basis

Tech Margins Have Caused Stocks To Look Especially Expensive On A Price/Sales Basis

In our view, rather than focusing on different measures of valuation, it is important for investors to understand the root cause of extreme US equity prices, as well as what factors are likely to drive equity multiples over the coming year. As we have noted in previous reports, the reason that US stocks are extremely overvalued today is very different from the reason for similar overvaluation in the late 1990s. Charts II-13 and II-14 present two different versions of the equity risk premium (ERP), one based on trailing as reported earnings (dating back to 1872), and one based on twelve-month forward earnings (dating back to 1979). Chart II-12The Shiller P/E Ratio Does Not Convey Any 'New' Information About Valuation

The Shiller P/E Ratio Does Not Convey Any 'New' Information About Valuation

The Shiller P/E Ratio Does Not Convey Any 'New' Information About Valuation

Chart II-13The Equity Risk Premium Is In Line With Its Historical Average…

The Equity Risk Premium Is In Line With Its Historical Average

The Equity Risk Premium Is In Line With Its Historical Average

The ERP accounts for the portion of equity market valuation that is unexplained by real interest rates, and the charts highlight that the US ERP is essentially in line with its historical average based on both measures, in sharp contrast to the stock market bubble of the late 1990s. This underscores that historically low interest rates well below the prevailing rate of economic growth are the root cause of extreme equity overvaluation in the US (Chart II-15), meaning that very rich pricing can be thought of as “rational exuberance.” Chart II-14…In Sharp Contrast To The Late 1990s

...In Sharp Contrast To The Late 1990s

...In Sharp Contrast To The Late 1990s

Chart II-15US Equities Are Extremely Expensive Because Bond Yields Are Extremely Low

US Equities Are Extremely Expensive Because Bond Yields Are Extremely Low

US Equities Are Extremely Expensive Because Bond Yields Are Extremely Low

Chart II-16The Equity Risk Premium Is Fairly Well Explained By The Misery Index

The Equity Risk Premium Is Fairly Well Explained By The Misery Index

The Equity Risk Premium Is Fairly Well Explained By The Misery Index

Over the longer term, the risks to US equity valuation are clearly to the downside, as we detailed in our October 2021 report.9 But over the coming 6 to 12 months, US equity multiples are likely to be flat or modestly up in the US. As we noted in Section 1 of our report, a significant further rise in long-maturity bond yields will likely necessitate a major shift in neutral rate expectations on the part of investors and the Fed, which we think is more likely a story for next year than this year. And Chart II-16 highlights that the ERP has historically been well explained by the sum of unemployment and inflation (the Misery Index), which should come down over the coming several months as inflation moderates and the unemployment rate remains low. To conclude, it is absolutely the case that US equities are extremely expensive, but this fact is unlikely to impact US stock market performance significantly unless long-maturity bond yields rise substantially further. Technical Analysis Amid A Shifting Economic Regime Technical analysis of financial markets, and especially stocks, has a long history. It has also provided disciplined investors with significant excess returns over time. A simple stock / bond switching rule based on whether stock prices were above their nine-month moving average at the end of the previous month has significantly outperformed since the 1960s, earning an average excess annual return of 1.3% relative to a 60/40 stock/bond benchmark portfolio (Chart II-17). This outsized performance has come at the cost of only a minor increase in portfolio volatility. Ostensibly, then, investors should be paying more attention to equity technical conditions in the current environment, which we noted above are not positive. Our Technical Indicator has recently broken into negative territory, and the S&P 500 has clearly fallen back below its 200-day moving average. However, Chart II-17 presented generalized results over long periods of time. Over the past two decades, investors have been able to rely on a durably negative correlation between stock prices and bond yields to help boost portfolio returns from technically-driven switching rule strategies. Chart II-18 highlights that this correlation has been much lower over the past two years than has been the case since the early 2000s, raising the question of whether similar switching strategies are viable today. In addition, there is the added question of whether technical analysis is helpful to investors during certain types of economic and financial market regimes, such as high inflation environments. Chart II-17Technically-Driven Trading Rules Have Historically Provided Investors With A Lot Of Alpha

Technically-Driven Trading Rules Have Historically Provided Investors With A Lot Of Alpha

Technically-Driven Trading Rules Have Historically Provided Investors With A Lot Of Alpha

Chart II-18Switching-Rule Strategies May Not Work As Well When Stock Prices And Bond Yields Are Not Positively Correlated

Switching-Rule Strategies May Not Work As Well When Stock Prices And Bond Yields Are Not Positively Correlated

Switching-Rule Strategies May Not Work As Well When Stock Prices And Bond Yields Are Not Positively Correlated

To test whether the message from technical indicators may be relied upon today, we examine the historical returns from a technically-driven portfolio switching strategy during nonrecessionary months under four conditions that reflect the economic and political realities currently facing investors: months when both stock and bond returns are negative; months of above-average inflation; months of above-average geopolitical risk; and the 1970s, when the Misery Index was very elevated. In all the cases we consider, the switching rule is simple: whether the S&P 500 index was above its nine-month moving average at the end of the previous month. If so, the rule overweights equities for the subsequent months; if not, the rule overweights a comparatively risk-free asset. We consider portfolios with either 10-year Treasurys or 3-month Treasury bills as the risk-free asset, as well as a counterfactual scenario in which cash always earns a 1% annual rate of return (to mimic the cash returns currently available to investors). Table II-1 presents the success and whipsaw rate of the trading rule. Table II-2 presents the annualized cumulative returns from the strategy. The tables provide three key observations: As reflected in Chart II-17, both Tables II-1 and II-2 highlight that simple technical trading rules have historically performed well, and that outperformance has occurred in both recessionary and nonrecessionary periods. Relative to nonrecessionary periods overall, technical trading rules have underperformed during the particular nonrecessionary regimes that we examined. It is the case not only that these strategies have performed in inferior ways during these regimes, but also that they were less consistent signals in that they generated significantly more “whipsaws” for investors. Among the four nonrecessionary regimes that we tested, technical indicators underperformed the least during periods of above-average geopolitical risk, and performed abysmally during nonrecessionary (but generally stagflationary) months in the 1970s. Table II-1During Expansions, Technically-Driven Switching Rules Underperform…

May 2022

May 2022

Table II-2…When Inflation Is High And When Stocks And Bonds Lose Money

May 2022

May 2022

The key takeaway for investors is that technical analysis is likely to be helpful for investors to improve portfolio performance as we approach a recession but may be less helpful in an expansionary environment in which inflation is above average and when stock prices and bond yields are less likely to be positively correlated. Investment Conclusions Echoing the murky economic outlook that we detailed in Section 1 of our report, our analysis highlights that an indicator-based approach is providing mixed signals about the US equity market. On the one hand, all four of our main equity indicators are currently providing a bearish signal, and the risk of a nonrecessionary contraction in S&P 500 profit margins over the coming year is elevated – albeit seemingly not imminent. On the other hand, our expectation that the US will not slip into recession over the coming year implies that revenue growth will stay positive, which has historically been associated with expanding earnings. In addition, US equity multiples are likely to be flat or modestly up, and the recent technical breakdown in the S&P 500 may simply reflect a reduced signal-to-noise ratio that appears to exist in expansionary environments in which inflation is high and the stock price / bond yield correlation is near-zero or negative. Netting these signals out, we see our equity indicators as supportive of a cautious, minimally-overweight stance toward stocks within a multi-asset portfolio. The emergence of a recession, declining profit margins, and a significant increase in investor or Fed expectations for the neutral rate of interest are the most significant threats to the equity market. We will continue to monitor these risks and adjust our investment recommendations as needed over the coming several months. Stay tuned! Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Gabriel Di Lullo Research Associate III. Indicators And Reference Charts As discussed in this month’s Section 2, BCA’s equity indicators do not paint an optimistic picture for stock prices. Our monetary indicator is at its weakest point in almost three decades, our valuation indicator continues to highlight that stocks are overvalued, and both our sentiment and technical indicators have broken down. An eventual easing in the latter two measures will ultimately prove positive for equities, but this will likely happen only once they reach extremes. Investors should be at most modestly overweight stocks versus bonds over the coming year. Forward equity earnings are likely pricing in too much of an increase in earnings per share over the coming year. Net earnings revisions and net positive earnings surprises have rolled over considerably, although there is no meaningful sign yet of a decline in the level of forward earnings. Earnings growth is more likely than not to be positive over the coming year, but will be modest. Within a global equity portfolio, we recommend a neutral stance towards cyclicals versus defensives, as well as a neutral regional equity stance. Euro area stocks are not a clear underweight candidate despite the risk of a European recession. Within a fixed-income portfolio, the 10-Year Treasury Yield has very little further upside over the coming year, arguing for a modestly short duration stance. We do not believe that the Fed will end up raising rates to a level higher than investors are forecasting over the coming year. Commodity prices continue to rise in a broad-based fashion following Russia’s invasion of Ukraine, and our composite technical indicator highlights that they remain significantly overbought. We expect oil and food prices to come down over the coming year, but there is a risk to that assessment. Russia aggression has very likely sped up Europe’s decarbonization timeline, suggesting that investors should be tactically, cyclically, and structurally bullish on industrial metals prices. US and global LEIs have rolled over from very elevated levels. Our global LEI diffusion index has declined very significantly, but this likely reflects the outsized impact of a few emerging market countries. Leading and coincident indicators remain decently strong, and we do not expect a recession in the US over the coming year. However, the odds of a stagflationary-lite outcome of above-target inflation and at-or-below-trend growth have increased because of the war. EQUITIES: Chart III-1US Equity Indicators

US Equity Indicators

US Equity Indicators

Chart III-2Willingness To Pay For Risk

Willingness To Pay For Risk

Willingness To Pay For Risk

Chart III-3US Equity Sentiment Indicators

US Equity Sentiment Indicators

US Equity Sentiment Indicators

Chart III-4US Stock Market Breadth

US Stock Market Breadth

US Stock Market Breadth

Chart III-5US Stock Market Valuation

US Stock Market Valuation

US Stock Market Valuation

Chart III-6US Earnings

US Earnings

US Earnings

Chart III-7Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Chart III-8Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

FIXED INCOME: Chart III-9US Treasurys And Valuations

US Treasurys And Valuations

US Treasurys And Valuations

Chart III-10Yield Curve Slopes

Yield Curve Slopes

Yield Curve Slopes

Chart III-11Selected US Bond Yields

Selected US Bond Yields

Selected US Bond Yields

Chart III-1210-Year Treasury Yield Components

10-Year Treasury Yield Components

10-Year Treasury Yield Components

Chart III-13US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

Chart III-14Global Bonds: Developed Markets

Global Bonds: Developed Markets

Global Bonds: Developed Markets

Chart III-15Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

CURRENCIES: Chart III-16US Dollar And PPP

US Dollar And PPP

US Dollar And PPP

Chart III-17US Dollar And Indicator

US Dollar And Indicator

US Dollar And Indicator

Chart III-18US Dollar Fundamentals

US Dollar Fundamentals

US Dollar Fundamentals

Chart III-19Japanese Yen Technicals

Japanese Yen Technicals

Japanese Yen Technicals

Chart III-20Euro Technicals

Euro Technicals

Euro Technicals

Chart III-21Euro/Yen Technicals

Euro/Yen Technicals

Euro/Yen Technicals

Chart III-22Euro/Pound Technicals

Euro/Pound Technicals

Euro/Pound Technicals

COMMODITIES: Chart III-23Broad Commodity Indicators

Broad Commodity Indicators

Broad Commodity Indicators

Chart III-24Commodity Prices

Commodity Prices

Commodity Prices

Chart III-25Commodity Prices

Commodity Prices

Commodity Prices

Chart III-26Commodity Sentiment

Commodity Sentiment

Commodity Sentiment

Chart III-27Speculative Positioning

Speculative Positioning

Speculative Positioning

ECONOMY: Chart III-28US And Global Macro Backdrop

US And Global Macro Backdrop

US And Global Macro Backdrop

Chart III-29US Macro Snapshot

US Macro Snapshot

US Macro Snapshot

Chart III-30US Growth Outlook

US Growth Outlook

US Growth Outlook

Chart III-31US Cyclical Spending

US Cyclical Spending

US Cyclical Spending

Chart III-32US Labor Market

US Labor Market

US Labor Market

Chart III-33US Consumption

US Consumption

US Consumption

Chart III-34US Housing

US Housing

US Housing

Chart III-35US Debt And Deleveraging

US Debt And Deleveraging

US Debt And Deleveraging

Chart III-36US Financial Conditions

US Financial Conditions

US Financial Conditions

Chart III-37Global Economic Snapshot: Europe

Global Economic Snapshot: Europe

Global Economic Snapshot: Europe

Chart III-38Global Economic Snapshot: China

Global Economic Snapshot: China

Global Economic Snapshot: China

Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Gabriel Di Lullo Research Associate Footnotes 1 Please see The Bank Credit Analyst "April 2022," dated March 31, 2022, available at bca.bcaresearch.com 2 Please see The Bank Credit Analyst "Do Excess Savings Explain Low US Interest Rates?" dated March 31, 2022, and "R-star, And The Structural Risk To Stocks," dated March 31, 2021, available at bca.bcaresearch.com 3 Please see US Investment Strategy/ US Bond Strategy Special Report "Gauging The Risk Of Recession: Slowdown Or Double-Dip?" dated August 16, 2010, available at usbs.bcaresearch.com 4 Please see The Bank Credit Analyst "Do Excess Savings Explain Low US Interest Rates?" dated March 31, 2022, available at bca.bcaresearch.com 5 Clarke, KE, JM Jones, Y Deng, et al. Seroprevalence of Infection-Induced SARS-CoV-2 Antibodies — United States. September 2021–February 2022. 6 Please see The Bank Credit Analyst "Global House Prices: A New Threat For Policymakers," dated May 27, 2021, available at bca.bcaresearch.com 7 Please see The Bank Credit Analyst "January 2022," dated December 23, 2021, available at bca.bcaresearch.com 8 Please see The Bank Credit Analyst “OUTLOOK 2022: Peak Inflation – Or Just Getting Started?” dated December 1, 2021, available at bca.bcaresearch.com 9 Please see The Bank Credit Analyst “The “Invincible” US Equity Market: The Longer-Term Outlook For US Stocks In Relative And Absolute Terms,” dated September 30, 2021, available at bca.bcaresearch.com

Executive Summary Using the real yield on inflation protected bonds as a gauge of the long-term real interest rate is possibly the biggest mistake in finance. The ultra-low real yield on inflation protected bonds captures nothing more than a stampede for inflation protection overwhelming a tiny supply of inflation protected bonds. The long-term real interest rate embedded in the US bond and US stock markets is likely to be significantly higher than the -0.2 percent real yield on US inflation protected bonds. Long-term investors should overweight conventional bonds and stocks versus inflation protected bonds. On a 6-12 month horizon, overweight both US bonds and US stocks. With core inflation on the cusp of rolling over and global growth decelerating, the end is in sight for the sell-offs both in long duration bonds and in the stock market. Fractal trading watchlist: High dividend stocks, and MSCI Hong Kong versus MSCI China. The Low ‘Real Bond Yield’ Just Reflects A Massive Demand For Inflation Protection

The Low 'Real Bond Yield' Just Reflects A Massive Demand For Inflation Protection

The Low 'Real Bond Yield' Just Reflects A Massive Demand For Inflation Protection

Bottom Line: The end is in sight for the sell-offs both in long duration bonds and in the stock market. Feature “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so” One of my favourite quotes, ostensibly attributed to Mark Twain, warns us that trouble doesn’t come from what you don’t know. Rather, trouble comes from what you think you know for certain but turns out to be wrong. In economics and finance the “what you know for sure that just ain’t so” is the long-term real interest rate. In economics and finance the “what you know for sure that just ain’t so” is the long-term real interest rate. The long-term real interest rate is arguably the most fundamental concept in economics and finance. It encapsulates the risk-free real return on savings, and it is embedded in the returns offered by all assets such as bonds and equities. The trouble is, the way that most people quantify the long-term real interest rate turns out to be wrong. Specifically, most people define the long-term real interest rate as the real yield on (10-year) inflation protected bonds, which now stands at -0.2 percent in the US and -2.3 percent in the UK. US and UK inflation protected bonds will of course deliver the negative long-term real returns that their yields offer. So, most people believe that the long-term real interest rate is still depressed, permitting many rate hikes from the Federal Reserve and Bank of England before monetary policy becomes ‘restrictive’, and providing a massive cushion to asset valuations before they become expensive.This commonly held belief is arguably the biggest mistake in finance. The Long-Term Real Interest Rate Is Not What You Think The biggest mistake in finance stems from the confluence of two factors: first, the inflation protected bond market is the only true hedge against inflation; and second, it is tiny. Compared with the $45 trillion US equity market and the $25 trillion T-bond market, the Treasury Inflation Protected Securities (TIPS) market is worth just $1.5 trillion. Many other economies do not even have an inflation protected bond market! The ultra-low real yield on inflation protected bonds captures nothing more than the massive imbalance between huge demand for inflation hedges and tiny supply. When the price level surges, as it has recently, stock and bond investors have a fiduciary duty to seek an inflation hedge, even if they are shutting the stable door after the horse has bolted (Chart I-1). With at least $70 trillion worth of investors all wanting a piece of the $1.5 trillion TIPS market, the demand for TIPS surges, meaning that their real yield collapses. Therefore, the ultra-low real yield on inflation protected bonds captures nothing more than the massive imbalance between huge demand for inflation hedges and tiny supply. Chart I-1When The Price Level Surges, Investors Flood Into Inflation Protected Bonds

When The Price Level Surges, Investors Flood Into Inflation Protected Bonds

When The Price Level Surges, Investors Flood Into Inflation Protected Bonds

The proof comes from the perfect positive correlation between the oil price and so-called ‘inflation expectations.’ As a surging oil price drives down the 10-year TIPS yield relative to the 10-year T-bond yield, this difference in yields – which is the commonly accepted definition of expected inflation through 2022-32 – also surges (Chart I-2and Chart I-3). This perfect positive correlation also applies to the so-called ‘5-year, 5-year forward’ inflation rate, the expected inflation rate through 2027-32 (Chart I-4). Chart I-2Inflation Expectations Just Track The Oil Price

Inflation Expectations Just Track The Oil Price

Inflation Expectations Just Track The Oil Price

Chart I-3Inflation Expectations Are Just A Mathematical Function Of The Oil Price

Inflation Expectations Are Just A Mathematical Function Of The Oil Price

Inflation Expectations Are Just A Mathematical Function Of The Oil Price

Chart I-4Even The ‘5-Year, 5-Year Forward’ Inflation Expectation Just Tracks The Oil Price

Even The '5-Year, 5-Year Forward' Inflation Expectation Just Tracks The Oil Price

Even The '5-Year, 5-Year Forward' Inflation Expectation Just Tracks The Oil Price

Yet this observed positive correlation between the oil price and inflation expectations is nonsensical, because the reality is the exact opposite! The higher the price level at a given moment, the lower will be the subsequent inflation rate. This is just basic maths. The subsequent inflation rate is the future price divided by the current price, so dividing by a higher price results in a lower number. The empirical evidence over the last 50 years confirms this. The higher the oil price, the lower the subsequent inflation rate (Chart I-5). Chart I-5But A Higher Oil Price Means Lower Subsequent Inflation

But A Higher Oil Price Means Lower Subsequent Inflation

But A Higher Oil Price Means Lower Subsequent Inflation

As the price level surges, subsequent inflation declines, both in theory and in practice. Hence, we should subtract a smaller number from the nominal bond yield to get a higher long-term real interest rate. In other words, all else being equal, the impact of a higher price level is to lift the long-term real interest rate. To repeat, the very low real yield on inflation protected bonds just captures the stampede of inflation hedging demand overwhelming a tiny supply (Chart I-6). Given this distortion, the real yield on inflation protected bonds is likely not the long-term real interest rate embedded in the much larger bond and stock markets. Right now, the long-term real interest rate embedded in the bond and stock markets is likely to be significantly higher than the -0.2 percent real yield on TIPS. Chart I-6The Low ‘Real Bond Yield’ Just Reflects A Massive Demand For Inflation Protection

The Low 'Real Bond Yield' Just Reflects A Massive Demand For Inflation Protection

The Low 'Real Bond Yield' Just Reflects A Massive Demand For Inflation Protection

To which the obvious rejoinder is: if the real yield embedded in conventional bonds and stocks is much higher than in inflation protected bonds, why does the market not arbitrage it away? The simple answer is that the market will arbitrage it away, but in slow motion. This is because the mispricing between expected and realised inflation will crystallise in real time, and not ahead of it. Nevertheless, this slow motion arbitrage provides a compelling opportunity for patient long-term investors. Overweight conventional bonds and stocks versus inflation protected bonds. The Best Way To Value The Stock Market Given that we cannot use the yield on inflation protected bonds as a reliable measure of the long-term real interest rate embedded in stock prices, it is also a big mistake to value equities versus the real bond yield. In The Case Against A ‘Super Bubble’ (And The Case For) we explained the much better way to value equities. The basic idea is that the cashflows of any investment can be condensed into one future ‘lump sum payment’. So, we just need to know the size of this lump sum payment, and then to calculate its present value. The US stock market tracks (the 30-year T-bond price) multiplied by (profits expected in the year ahead). For a stock market, the size of the payment just tracks current profits multiplied by ‘a structural growth constant’, and the present value just tracks the value of an equal duration bond. For example, the duration of the US stock market is the same as that of the 30-year T-bond, at around 25 years.1 It follows that the US stock market price should track: (The 30-year T-bond price) multiplied by (profits expected in the year ahead) multiplied by (a structural growth constant) To the extent that the structural growth outlook for profits does not change, we can simplify the expression to: (The 30-year T-bond price) multiplied by (profits expected in the year ahead) This approach might seem simplistic, yet it perfectly explains the US stock market’s evolution both over the past 40 years (Chart I-7) and over the past year (Chart I-8). Specifically, in 2022 to date, the major drag on the US stock market has been the sell-off in the 30-year T-bond. Chart I-7The US Stock Market = The 30-Year T-Bond Price Times Profits (40 Year Chart)

The US Stock Market = The 30-Year T-Bond Price Times Profits (40 Year Chart)

The US Stock Market = The 30-Year T-Bond Price Times Profits (40 Year Chart)

Chart I-8The US Stock Market = The 30-Year T-Bond Price Times Profits (1 Year Chart)

The US Stock Market = The 30-Year T-Bond Price Times Profits (1 Year Chart)

The US Stock Market = The 30-Year T-Bond Price Times Profits (1 Year Chart)

For the foreseeable future, we expect profit growth to be lacklustre, keeping the 30-year T-bond price as the dominant driver of the US stock market. With core inflation on the cusp of rolling over and global growth decelerating, the end is in sight for the sell-off in long duration bonds and therefore for the sell-off in the stock market. On a 6-12 month horizon, overweight both US bonds and US stocks. Fractal Trading Watchlist This week, we note that the MSCI index outperformance of Hong Kong versus Chinese has reached a point of fragility on its 260-day fractal structure that has signalled previous major turning points in 2015, 2016, 2018, 2019, and 2020. Therefore, we have added this to our watchlist of investments that are at or approaching turning points, which is available in full on our website: cpt.bcaresearch.com We also highlight that the strong rally in high dividend stocks (the ETF is HDV) is vulnerable to correction if, as we expect, bond yields stabilise or reverse (Chart I-9). Accordingly, the recommended trade is to short high dividend stocks (HDV) versus the 10-year T-bond, setting the profit target and symmetrical stop-loss at 6 percent. Chart I-9The Outperformance Of High Dividend Stocks Is Vulnerable To Reversal

The Outperformance Of High Dividend Stocks Is Vulnerable To Reversal Fractal Trading Watch List

The Outperformance Of High Dividend Stocks Is Vulnerable To Reversal Fractal Trading Watch List

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

Chart 1The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

Chart 2The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

Chart 3AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

Chart 4Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Chart 5Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Chart 6US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

Chart 7Bitcoin's 65-Day Fractal Support Is Holding For Now

Bitcoin's 65-Day Fractal Support Is Holding For Now

Bitcoin's 65-Day Fractal Support Is Holding For Now

Chart 8A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Chart 9Biotech Is A Major Buy

Biotech Is A Major Buy

Biotech Is A Major Buy

Chart 10CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

Chart 11Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Chart 12Norway's Outperformance Could End

Norway's Outperformance Could End

Norway's Outperformance Could End

Chart 13Greece's Brief Outperformance To End

Greece's Brief Outperformance To End

Greece's Brief Outperformance To End

Chart 14BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

Chart 15The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

Chart 16The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

Chart 17Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Chart 18US Homebuilders' Underperformance Has Reached A Potential Turning Point

US Homebuilders' Underperformance Has Reached A Potential Turning Point

US Homebuilders' Underperformance Has Reached A Potential Turning Point

Chart 19Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Chart 20The Rally In USD/EUR Could End

The Rally In USD/EUR Could End

The Rally In USD/EUR Could End

Chart 21The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 The duration of any investment quantifies how far into the future its cashflows lie, by averaging those cashflows into one theoretical future ‘lump sum’. Defined mathematically, it is the weighted average of the times of its cashflows, in which the weights are the present values of the cashflows. For a bond, the duration also equals the percentage change in the bond price for every 1 percent change in its yield. Fractal Trading System Fractal Trades

This Is The Biggest Mistake In Finance: The Real Interest Rate

This Is The Biggest Mistake In Finance: The Real Interest Rate

This Is The Biggest Mistake In Finance: The Real Interest Rate

This Is The Biggest Mistake In Finance: The Real Interest Rate

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Executive Summary Allies Still Have Faith In USD

Allies Still Have Faith In USD

Allies Still Have Faith In USD