Equities

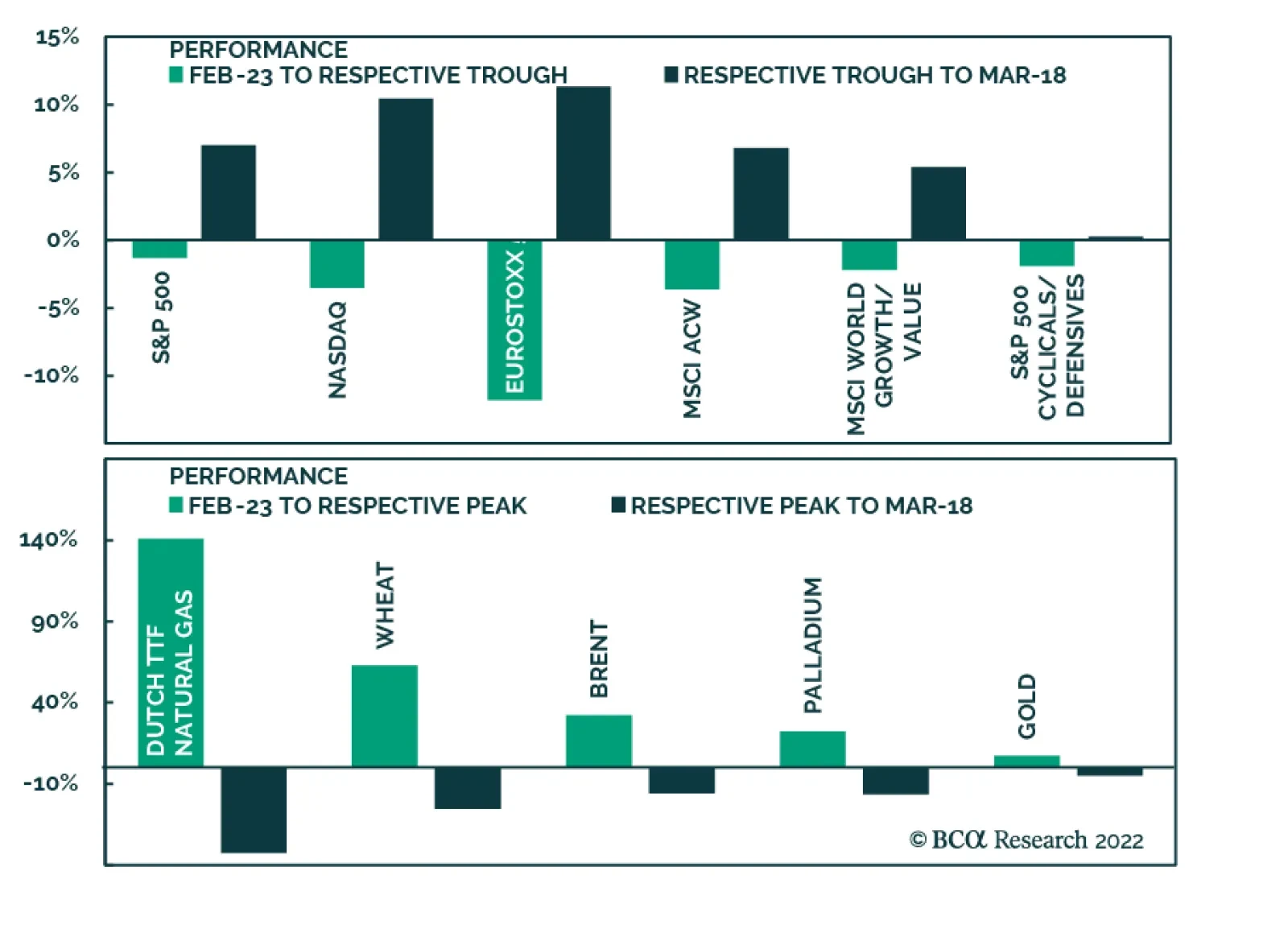

The S&P 500 is up 7% from its March 8 trough, reducing year-to-date losses to 6.4% and bringing gains since the start of the Russian invasion of Ukraine to 5.6%. The trajectory of the Nasdaq is similar: it has recouped all of its losses since the…

Executive Summary Table 1Equity Capitulation Scorecard

Have US Equities Hit Rock Bottom?

Have US Equities Hit Rock Bottom?

We have put together a framework to capture the extent to which recent economic and political developments have been priced in by the equity market. It has seven criteria: Rate stabilization has not materialized yet, monetary conditions will continue to tighten Economic growth expectations do not yet reflect the deteriorating economic backdrop. US GDP forecasts will be downgraded which will be a drag on equity performance Earnings growth expectations need to come down to reflect supply disruptions, raging input prices, and the stronger dollar Oil prices have stabilized which provides support for US equities Valuations have retraced, signaling that the market is reasonably priced Technicals signal that the market is oversold “Black swans”: The effects of the war in Ukraine will be a drag on US equities and are not yet fully priced in. However, China’s pledge to be more investor-friendly is a positive. On balance, risks for US equities slightly outweigh the upside opportunity. Bottom Line: Although many ingredients for a sustainable rally are already in place, our analysis concludes that US equities have not hit rock bottom yet, and time is needed to resolve remaining headwinds. Feature The S&P 500 and NASDAQ are in correction territory, having pulled back 13% and 22%, respectively from their peak. Over the past few months, investors had to process a witches’ brew of staggering inflation, impending monetary tightening, and a war in the heart of Europe. Too much! Related Report US Equity StrategyAre We There Yet? However, over the past couple of days, US equities have staged an aggressive rally: The S&P rebounded 5.5% and the NASDAQ 8%. While we are long-term investors and don’t focus on short-term market moves, we find a recent market turn a good excuse to take a close look at US equities and gauge whether this recent rally is a “dead-cat bounce” or the market has truly bottomed and is in the early stages of a recovery rally. To do so, we have put together a framework to capture the extent to which recent economic and political developments have been priced in by the equity market. “Equity Capitulation” Framework Historically, equities bottomed when bad news had been reflected in expectations, valuations had come down to reflect the new economic reality, and investors had capitulated. Here are our criteria for an equity rebound this economic cycle: Monetary tightening has been priced in and rates have stabilized Economic growth expectations have been downgraded Energy prices have normalized Earnings growth expectations have come down and earnings are unlikely to surprise on the downside Investors have capitulated and sentiment is rock-bottom Valuations have lost their “good times” froth and are attractive There are resolutions of the geopolitical factors that have contributed to market turmoil In this report, we will go through each of the criteria and do our best to gauge whether “we are there yet.” Pricing In Tighter Monetary Policy – Rate Stabilization Is Still Elusive The recent correction of US equities reflects a repricing due to tighter monetary policy. The million-dollar question is how much monetary tightening is priced in and when will rates stabilize? To our minds, this is one of the key conditions for a sustainable bull market. Last week, the Fed raised rates for the first time since 2018. This first rate hike is 0.25 - 0.50, which did not come as a surprise and was broadcast well in advance. The latest dot plot also signals that the Fed expects the target rate to reach 1.75% by the end of 2022, i.e., six more hikes are expected this year. However, a day after the announcement, the market is pricing eight to nine rate hikes (Chart 1), with the Fed rate ending the year at 2.25-2.5%. Thus, the market expects aggressive Fed action and is likely to be positively surprised when the Fed takes a more measured approach than anticipated. This is certainly positive for equities. Chart 1The Market Is Pricing More Hikes In 2022 Then The Fed

The Market Is Pricing More Hikes In 2022 Then The Fed

The Market Is Pricing More Hikes In 2022 Then The Fed

Chart 2Monetary Conditions Will Continue To Tighten

Monetary Conditions Will Continue To Tighten

Monetary Conditions Will Continue To Tighten

However, despite the market coming to terms with an aggressive hiking schedule, monetary conditions are still easy (Chart 2), and real rates are negative. With the Fed’s emphasis on combating inflation, it is reasonable to expect that monetary conditions will continue to tighten, and real rates will rise. Also, nominal rates don’t yet show any signs of stabilization either (Chart 3). What does this mean for equities? Empirical analysis demonstrates that it takes around three months after the first hike for equities to adjust to a new monetary regime and deliver positive returns (Chart 4). Chart 3Rates Have Not Stabilized Yet

Rates Have Not Stabilized Yet

Rates Have Not Stabilized Yet

Chart 4Adjusting to A Tighter Monetary Regime Takes Time

Have US Equities Hit Rock Bottom?

Have US Equities Hit Rock Bottom?

Monetary conditions are likely to tighten further. Rate stabilization, which we are looking for, has not materialized just yet. On a positive note, we don’t expect any negative surprises from the Fed. Forecasts Need To Reflect Slowing Economic Growth According to the Bloomberg consensus, economic growth expectations for 2022 are still robust and have not been substantially downgraded (Chart 5). The market still expects the US economy to grow at 3.55%, compared to 3.8% in January, despite monetary tightening, falling ISM PMI readings (Chart 6), and soaring energy costs. The Fed is more realistic about the effects of its policy on economic growth, changing expectations from 4% to 2.8%. The logical conclusion is that more GDP growth downgrades are on the way. The latest reading of the Atlanta Fed stands at only 1.3%. Chart 5Economic Forecasts Do Not Yet Reflect Deteriorating Macro Backdrop

Economic Forecasts Do Not Yet Reflect Deteriorating Macro Backdrop

Economic Forecasts Do Not Yet Reflect Deteriorating Macro Backdrop

Chart 6Surveys Signal Growth A Slow Down

Surveys Signal Growth A Slow Down

Surveys Signal Growth A Slow Down

It is also important to note that both the direct and indirect effects of the war in Ukraine are yet to be reflected in US growth forecasts: Since the beginning of the war, the GSCI Commodities index has increased by 11%. One might argue that soaring commodity prices are a temporary phenomenon and forward curves signal eventual reversion to long-term averages. However, this may take months and even years, and by then, most of the stockpiles and hedges are likely to run out. Growth expectations are likely to fall, or worse yet, economic growth may surprise on the downside. Earnings Expectations Need To Come Down Similar to economic growth forecasts, bottom-up earnings growth expectations have barely budged (Chart 7): The market is still expecting about 9% earnings growth over the next 12 months. However, global supply disruptions and raging input prices are bound to cut into corporate profitability and slow earnings growth. Chart 7Earnings Expectations Have Not Budged

Earnings Expectations Have Not Budged

Earnings Expectations Have Not Budged

To make things worse, the US dollar has appreciated by nearly 10% since the beginning of 2021 (Chart 8). Since companies in the S&P 500 derive 40% from abroad, the strong greenback is bound to translate into softer overseas profits, cutting into the profitability of US multinationals. The effect of a stronger currency will be further exacerbated by the withdrawal of US companies from Russia to protest the war in Ukraine. While most US companies have limited exposure to Russia, there are some that will take a hit: For example, Philip Morris derives 8% of sales from that market. McDonald’s announced that closing its restaurants in Russia will cost $50 million a month or 9% of annual sales. While it is hard to accurately gauge the effect of the war and self-sanctions on US corporate profits, on the margin it is definitely a negative. Chart 8Dollar Has Strengthened Significantly

Dollar Has Strengthened Significantly

Dollar Has Strengthened Significantly

Earnings growth expectations have barely budged, and do not reflect a surge in commodity prices, a war, and slowing economic growth. We posit that downgrades are highly likely, and will be a drag on US equity performance. Oil Prices Have Stabilized The key channel for the war in Ukraine to affect the rest of the world is through the supply of energy. High energy prices present an economic danger because they touch every facet of the economy. Goldman Sachs estimates that spiraling electricity prices have already taken down 900,000 tonnes of aluminum capacity and 700,000 tonnes of zinc capacity in Europe. Certainly, in the past, a jump in the oil price has often been associated with recessions and negative equity returns (Chart 9). Therefore, we consider it a major shot in the arm that the WTI has come down from $130 to $105 on the back of lockdowns in China. This hiatus gives policymakers and oil producers time to negotiate deals and restart production – the onus is on US shale producers and Gulf nations. However, the long-term resolution is yet to be seen. Chart 9Oil Price Increases Have Been Associated With Negative Equity Returns

Oil Price Increases Have Been Associated With Negative Equity Returns

Oil Price Increases Have Been Associated With Negative Equity Returns

Oil price stabilization provides solid support for US equity performance. Valuations – No Longer An Excuse Not To Buy The correction in US equity markets has taken the froth off valuations: The S&P 500 forward multiple has come down from roughly 23x to 19x earnings (Chart 10), with all of the change attributable to multiple contraction. The BCA S&P 500 Valuation Indicator shows that the index is no longer “overvalued” (Chart 11). Outright cheap? No. But valuations can no longer be an excuse not to buy. Also, there are multiple corners of the market that are outright cheap – lots of bottom fishing is already taking place. Chart 10Valuations Have Moderated

Valuations Have Moderated

Valuations Have Moderated

Chart 11The S&P 500 Is No Longer Overvalued...

The S&P 500 Is No Longer Overvalued...

The S&P 500 Is No Longer Overvalued...

Valuations have moderated and the market is reasonably priced. Technicals – The Market Is Oversold While valuation multiples may contract further, most technical and sentiment indicators are flashing capitulation. The AAII Investor Bull/Bear Sentiment Indicator is below its March 2020 reading while the BCA Technical Indicator has shifted towards the oversold zone (Chart 12). It is important to note that this indicator is driven primarily by momentum components – its reading is oblivious to the top-heavy index composition and reflects prospects for large caps. A useful way to look under the index’s hood is to consider the number of stocks that retraced from their highs, currently over 95% of NASDAQ stocks have retraced (Chart 13). This high a reading flashes that the market is oversold, and there are lots of bargains to be had. Chart 12...Or Overbought

...Or Overbought

...Or Overbought

Chart 13Majority Of Stocks Are Oversold

Majority Of Stocks Are Oversold

Majority Of Stocks Are Oversold

Technicals indicate an oversold market. Black Swans Have Landed The war in Ukraine: Optimism about a potential peace deal between Russia and Ukraine seems premature – the conflict is just getting started and neither side will be backing off until it has to surrender unconditionally. However, while the war is contained in Ukraine, and Russian gas is flowing to Europe, any crisis in the equity market would be averted. The war in Ukraine will remain a headwind to global equities for a while. And while the US equity market is insulated from the direct consequences of the crisis, indirect effects will continue to reverberate through its economy for now. The direct and indirect effects of the war in Ukraine will be a drag on US equities and are not yet fully priced in. China pledged to keep capital markets stable and vowed to support overseas stock listings, indicating that regulation of Big Tech will end soon. In addition, it promised to offer support for property developers to minimize their risks. And China’s pledge to be more investor-friendly is believable as in its current stage of economy and with the onset of COVID, the government is in dire need of propping up both the economy and the stock market. Of course, China still presents great uncertainty associated with lockdowns. This is a positive for the US market as there are a number of Chinese companies listed on the US stock exchanges. Putting It All Together Our Equity Capitulation scorecard has seven different criteria, as discussed above. According to our assessment of the economic and market environments, there are two factors that signal near-term equity rebound: Investor capitulation or Technicals, and Energy prices. However, there are still headwinds: Monetary conditions will continue to tighten, economic and earnings growth expectations will be downgraded, and the war in Ukraine is unlikely to end soon. On balance, risks for US equities slightly outweigh the opportunity. The final score is -1, which indicates a mildly negative stance on US equities (Table 1). However, most of the outstanding negatives are likely to be resolved soon (i.e., downward revisions of expectations). Table 1Equity Capitulation Scorecard

Have US Equities Hit Rock Bottom?

Have US Equities Hit Rock Bottom?

Investment Implications Our equity capitulation indicator signals that cautious investors should continue to be underweight equities on the back of monetary tightening, slowing growth, and upcoming downward revision cycles. While Technicals and valuations make equities tempting, volatility in equities is likely to continue, and rallies will probably be short-lived. As always, long-term investors have more latitude in investment decision-making, and we believe that the long-term outlook for equities is positive. Bottom Line Our analysis concludes that US equities have not hit rock bottom yet, although many ingredients are already in place: Valuations are attractive, and equities are outright oversold. While buying equities at these levels is tempting, we recommend patience: Economic growth expectations are still elevated, and bottom-up earnings growth forecasts need to come down to reflect slowing growth and the direct and indirect effects of the war in Ukraine. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Recommended Allocation

Executive Summary Ebbing Stagflation Fear Will Prompt Rerating

Ebbing Stagflation Fear Will Prompt Rerating

Ebbing Stagflation Fear Will Prompt Rerating

European inflation will rise further before peaking this summer. Core CPI will reach between 2.8% and 3.2% by year-end before receding. The combination of stabilizing growth and the eventual peak in inflation will cause stagflation fears to recede. European assets have greater upside. Cyclicals, small-caps, and financials will be major beneficiaries of declining stagflation fears. The underperformance of UK small-cap stocks is nearing its end. UK large-cap equities are a tactical sell against Eurozone and Swedish shares. TACTICAL INCEPTION DATE RETURN SINCE INCEPTION (%) COMMENT EQUITIES Buy European & Swedish Equities / Sell UK Large Caps Stocks 03/21/2022 Bottom Line: Stagflation fears are near an apex as commodity inflation recedes. A peak in these fears will allow European asset prices to perform strongly over the coming quarters. Despite a glimmer of hope that Ukraine and Russia may find a diplomatic end to the war, the reality on the ground is that the conflict has intensified. Although the hostilities are worsening and the European Central Bank (ECB) surprised the markets with its hawkish tone, European assets have begun to catch a bid. The crucial question for investors is whether this rebound constitutes a new trend or a counter-trend move? Our view about Europe is optimistic right now. The path is not a direct line upward. The recent optimism about the outcome of the Russia-Ukraine talks is premature; however, we are getting to the point when markets are becoming desensitized to the war and energy prices are losing steam. Moreover, the increasing number of statements by Chinese economic authorities pointing toward greater stimulus and support to alleviate the pain created by China’s stringent zero-COVID policy are another positive omen. Higher Inflation For Some Time European headline inflation is set to exceed 7% this summer and core CPI will increase between 2.8% and 3.2% by the end of 2022. Related Report European Investment StrategySpring Stagflation The main force that will push inflation higher in Europe remains commodity prices. Energy inflation is extremely strong at already 32% per annum (Chart 1). It will increase further because of both the recent jump in Brent prices to EUR122/bbl on March 8 and the upsurge in natural gas prices, which were as high as EUR212/MWh on the same day before settling to EUR106/MWh last Friday. The impact of energy prices will not be limited to headline inflation and will filter through to core CPI (Chart 1, bottom panel). The average monthly percentage change in the Eurozone core CPI inflation stands at 0.25% for the past six months (compared to an average of 0.09% over the past ten years), or the period when energy-prices inflation has been the strongest. Assuming monthly inflation remains at such an elevated level, annual core CPI will hit 3.3% in the Eurozone by the end of 2022 (Chart 2). Chart 2Core CPI to Rise Further

Core CPI to Rise Further

Core CPI to Rise Further

Chart 1Energy Inflation: Alive And Well

Energy Inflation: Alive And Well

Energy Inflation: Alive And Well

The picture is not entirely bleak. Many forces suggest that these inflationary forces will recede before year-end in Europe. Energy prices are peaking, which is consistent with a diminishing inflationary impulse from that space. We showed two weeks ago that the massive backwardation of oil curves, the heavy bullish sentiment, and the high level of risk-reversals were consistent with a severe but transitory adjustment in the energy market. Oil markets will experience further volatility, as uncertainty around peace/ceasefire negotiations continues to evolve in Ukraine. Nonetheless, the peak in energy prices has most likely been reached. BCA’s energy strategists expect Brent to average $93/bbl in 2022 and in 2023. The potential for a decline in headline CPI after the summer is not limited to energy prices. Dramatic moves in the commodity market, from metals to agricultural resources, have made headlines. Yet, the rate of change of commodity prices is decelerating, hence, the commodity impulse to inflation is slowing sharply. As Chart 3 shows, this is a harbinger of a slowdown in European headline CPI. Related Report European Investment StrategyFallout From Ukraine Looking beyond commodity markets, the recent deceleration in European economic activity also suggests weaker inflation in the latter half of 2022. Germany will likely suffer a recession because it already registered a negative GDP growth in Q4 2021. Q1 2022 growth will be even worse because of the country’s high exposure to both China and fossil fuel prices. More broadly, the recent deceleration in the rate of change of both the manufacturing and services PMIs is consistent with an imminent peak in the second derivative of goods and services CPI (Chart 4). Chart 3Commodity Impulse Is Peaking

Commodity Impulse Is Peaking

Commodity Impulse Is Peaking

Chart 4Inflation's Maximum Momentum Is Now

Inflation's Maximum Momentum Is Now

Inflation's Maximum Momentum Is Now

Underlying drivers of inflation also remain tame in Europe. European negotiated wages are only expanding at a 1.5% annual rate, which translates into unit labor costs growth of 1% (Chart 5). This contrast with the US, where wages are expanding at a 4.3% annual rate. A peak in inflation, however, does not mean that CPI readings will fall below the ECB’s 2% threshold anytime soon. The European economy continues to face supply shortages that the Ukrainian conflict exacerbates (Chart 6). Moreover, the recent wave of COVID-19 in China increases the risk of disruptions in supply chains, as highlighted by the closure of Foxconn factories in Shenzhen. Finally, inflation has yet to peak; mathematically, it will take a long time before it falls back below levels targeted by Frankfurt. Chart 5The European Labor Market Is Not Inflationary

The European Labor Market Is Not Inflationary

The European Labor Market Is Not Inflationary

Chart 6Not Blemish-Free

Not Blemish-Free

Not Blemish-Free

Bottom Line: European headline inflation will peak this summer, probably above 7%. Additionally, core CPI is likely to reach between 2.8% and 3.2% in the second half of 2022. As a result of a decline in the commodity impulse, inflation will decelerate afterward, but it will remain above the ECB’s 2% target for most of 2023. Hopes For Growth Two weeks ago, we wrote that Europe was facing a stagflation episode in the coming one to two quarters, but that, ultimately, economic activity will recover well. Recent evidence confirms that assessment. Chart 7A Coming Chinese Tailwind?

A Coming Chinese Tailwind?

A Coming Chinese Tailwind?

The tone of Chinese policymakers is becoming more aggressive, in favor of supporting the economy. On March 16, Vice-Premier Liu He highlighted that Beijing was readying to support property and tech shares and that it will do more to stimulate the economy. True, this response was made in part to address the need to close cities affected by the sudden spike of Omicron cases around China. Nonetheless, the global experience with Omicron demonstrates that, as spectacular and violent the surge in cases may be, it is short-lived. Meanwhile, the impact of stimulus filters through the economy over many months. As a result, Europe will experience the impact of China’s Omicron-induced slowdown, while it also suffers from the growth-sapping effects of the Ukrainian conflict; however, it will also enjoy the positive effect on growth of a rising credit impulse over several subsequent quarters (Chart 7). Beyond China, the other themes we have discussed in recent weeks remain valid. First, European fiscal policy will become looser, as governments prepare to fight the slowdown caused by the war, while also increasing infrastructure spending to wean Europe off Russian energy. Moreover, European military spending is well below NATO’s 2% objective. This will not remain the case, as military expenditure may leap from less than EUR100bn per year to nearly EUR400bn per year over the coming decade. Second, European spending on consumer durable goods still lags well behind the trajectory of the US. With the energy drag at its apex today, consumer spending on durable goods will be able to catch up in the latter half of the year, especially with the household savings rate standing at 15% or 2.5 percentage points above its pre-COVID level. Bottom Line: European growth will be very low in the coming quarters. Germany is likely to face a technical recession as Q1 2022 data filters in. Nonetheless, Chinese stimulus, European fiscal support, pent-up demand, and a declining energy drag will allow growth to recover in the latter half of the year. As a result, we agree with the European Commission estimates that European growth will slow markedly this year. Market Implications In the context of a transitory shock to European economic activity and a coming peak in inflation, European stock prices have likely bottomed. Chart 8Depressed Sentiment To Help Beta

Depressed Sentiment To Help Beta

Depressed Sentiment To Help Beta

Sentiment has reached levels normally linked with a durable market floor. The NAAIM Exposure Index has fallen to a point from which global markets often recover. Europe’s high beta nature increases the odds that European equities will greatly benefit in that context (Chart 8). Valuations confirm that sentiment toward European assets has reached a capitulation stage. The annual rate of change of the earnings yields in the earnings yields has hit 73%, which is consistent with a market bottom (Chart 9). More importantly, the change in European forward P/E tracks closely our European Stagflation Sentiment Proxy (ESSP), based on the difference between the Growth and Inflation Expectations’ components of the ZEW survey (Chart 10). For now, our ESSP indicates that stagflation fears in Europe have never been so widespread, but these fears will likely dissipate as energy inflation declines. This process will lift European earnings multiples. Chart 9Bad News Discounted?

Bad News Discounted?

Bad News Discounted?

Chart 10Ebbing Stagflation Fear Will Prompt Rerating

Ebbing Stagflation Fear Will Prompt Rerating

Ebbing Stagflation Fear Will Prompt Rerating

Earnings revisions will likely bottom soon as well. The ESSP is currently consistent with a dramatic decline in European net earnings revisions (Chart 10, bottom panel). It will take a few more weeks for lower earnings revisions to be fully reflected. However, they follow market moves and, as such, the 17% decline in the MSCI Europe Index that took place earlier this year already anticipates their fall. Consequently, as stagflation fears recede, earnings revisions will rise in tandem with equity prices. Chart 11Maximum Pressure On Corporate Spreads

Maximum Pressure On Corporate Spreads

Maximum Pressure On Corporate Spreads

A decline in stagflation fears is also consistent with a decrease in European credit spreads in the coming months (Chart 11). This observation corroborates the analysis from the Special Report we published jointly with BCA’s Global Fixed-Income Strategy team last week. In terms of sectoral implications, a decline in stagflation fears is often associated with a rebound in the performance of small-cap equities relative to large-cap ones (Chart 12, top panel). This reflects the greater sensitivity of small-cap equities to domestic economic conditions compared to large-cap stocks. Moreover, small-cap equities had been oversold relative to their large-cap counterparts but now, momentum is improving (Chart 12). As a result, it is time to buy these equities. Similarly, financials have suffered greatly from the recent events associated with the Ukrainian conflict. European financial institutions have not only been penalized for their modest exposure to Russia, they have also historically declined when stagflation fears are prevalent (Chart 13). This relationship reflects poor lending activity when the economy weakens, and the risk of a policy-induced recession caused by high inflation. Financials will continue their sharp rebound as stagflation fears dissipate. Chart 13Financials Have Suffered Enough

Financials Have Suffered Enough

Financials Have Suffered Enough

Chart 12Small-Caps Time To Shine

Small-Caps Time To Shine

Small-Caps Time To Shine

The dynamics in inflation alone are very important. As Table 1 highlights, in periods of elevated inflation over the past 20 years, financials underperform the broad market by 11.3% on average. It is also a period of pain for small-cap equities and cyclicals. Logically, exiting the current environment will offer opportunities in European cyclical equities and for financials in particular. Table 1Who Suffers From High Inflation?

Is Europe Turning The Corner?

Is Europe Turning The Corner?

Chart 14Long Industrials & Materials / Short Energy

Long Industrials & Materials / Short Energy

Long Industrials & Materials / Short Energy

Finally, a pair trade buying industrials and materials at the expense of energy makes sense today. Materials and industrials suffer relative to energy equities when stagflation rises, especially in periods when these fears reflect rising energy pressures (Chart 14). A reversal in relative earnings revisions in favor of materials and industrials will propel this position higher. Bottom Line: Sentiment toward European assets reached a selling climax in recent weeks. Stagflation fears in Europe have reached an apex, and their reversal will lift both multiples and earnings revisions in the subsequent quarters. Diminishing stagflation fears will also boost the appeal of European corporate credit, contributing to an easing in financial conditions. Small-cap stocks, cyclicals, and financials will reap the greatest benefits from this adjustment. Going long materials and industrials at the expense of energy stocks is an attractive pair trade. Key Risk: A Policy Mistake The view above is not without risks. The number one threat to European growth and assets is a policy mistake from the ECB. On March 10, 2022, the ECB’s policy statement and President Christine Lagarde’s press conference showed that the Governing Council (GC) will decrease asset purchases faster than anticipated. Chart 15Will The ECB Repeat It Past Mistakes?

Will The ECB Repeat It Past Mistakes?

Will The ECB Repeat It Past Mistakes?

It is important to keep in mind the dynamics of 2011. Back then, the ECB opted to increase interest rates as European headline CPI was drifting toward 2.6% on the back of rising energy prices. According to our ESSP, the April 2011 interest rates hike took place at the greatest level of stagflation fears recorded until the current moment (Chart 15). Lured by rising inflation, the ECB ignored underlying weaknesses in European economic activity, which wreaked havoc on European financial markets and growth. If the ECB were to increase rates as growth remains soft, a similar outcome would take place. For now, the ECB’s communications continue to de-emphasize the need for rate hikes in the near term, which suggests that the GC is cognizant of the risk created by weak growth over the coming months. Waiting until next year, when activity will be stronger and the output gap will be closed, will offer the ECB a better avenue to lift rates durably. This risk warrants close monitoring of the ECB’s communication over the coming months. If headline inflation does not peak by the summer, the ECB is likely to repeat its past error, which will substantially hurt European assets. Our optimism is tempered by this threat. UK Outperformance Long In The Tooth? Last week, the Bank of England (BoE) increased the Bank Rate by 25bps to 0.75%, in a move that was widely expected. Yet, the pound fell 0.7% against the euro and gilt yields fell 6 bps. This market reaction reflected the BoE’s choice to temper its forward guidance. The central bank is now expected to increase interest rates to 2.2% next year, before they decline in 2024. The dovish projection of the BoE shows the MPC’s concerns over the impact of higher energy costs and rising National Insurance contributions on household spending. In the BoE’s opinion, the economy is very inflationary right now, but it will slow, which will mitigate the inflationary impact down the road. We share the BoE’s worries about the UK’s near-term economic outlook. The combination of higher taxes, higher interest rates, and rising energy costs will have an impact on growth. However, the rapid decline in small-cap stocks, which have massively underperformed their large cap-counterparts, already discounts considerable bad news (Chart 16). Additionally, small-cap equities relative to EPS have begun to stabilize, while relative P/E and price-to-book ratios have also corrected their overvaluations. In this context, UK small-cap equities are becoming attractive. Chart 17UK vs Eurozone: A Stagflation Bet

UK vs Eurozone: A Stagflation Bet

UK vs Eurozone: A Stagflation Bet

Chart 16UK Small-Cap Stocks Have Purged Their Excesses

UK Small-Cap Stocks Have Purged Their Excesses

UK Small-Cap Stocks Have Purged Their Excesses

In contrast to small-cap stocks, UK large-cap equities have greatly benefited from the global stagflation scare. The UK large-cap benchmark had the right sector mix for the current environment, overweighting defensive names as well as energy and resources. It is likely that when stagflation fears recede, UK equities will undo their outperformance (Chart 17). Technically, UK equities are massively overbought against Euro Area and Swedish stocks, both of which have been greatly impacted by stagflation fears and their pro-cyclical biases (Chart 18 & 19). An attractive tactical bet will be to sell UK large-cap stocks while buying Eurozone and Swedish equities, as energy inflation declines and as China’s stimulus boosts global industrial activity in the latter half of 2022 Bottom Line: Move to overweight UK small-cap stocks within UK equity portfolios. Go long Euro Area and Swedish equities relative to UK large-cap stocks as a tactical bet. Chart 18UK Overbought Relative To Euro Area...

UK Overbought Relative To Euro Area...

UK Overbought Relative To Euro Area...

Chart 19… And Sweden

... And Sweden

... And Sweden

Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Tactical Recommendations Cyclical Recommendations Structural Recommendations Closed Trades

Executive Summary Investors Think The Fed Will Not Be Able To Raise Rates Much Above 2%

Is A Higher Neutral Rate Good Or Bad For Stocks?

Is A Higher Neutral Rate Good Or Bad For Stocks?

The neutral rate of interest is 3%-to-4% in the United States. This is substantially higher than the market estimate of around 2%. It is also higher than the central tendency range for the Fed’s terminal interest rate dot, which remained at 2.3%-to-2.5% following this week’s FOMC meeting. If the neutral rate turns out to be higher than expected, this is arguably good news for stocks over the short-to-medium term because it lowers the risk that the Fed will accidentally induce a recession this year by bringing rates into restrictive territory. Over a longer-term horizon of 2-to-5 years, however, a higher neutral rate is bad news for stocks because it means that investors will eventually need to value equities using a higher discount rate. It also means that the Fed could find itself woefully behind the curve in normalizing monetary policy. Bottom Line: Global equities will rise over the next 12 months as the situation in Ukraine stabilizes, commodity prices recede, and inflation temporarily declines. Stocks will peak in the second half of 2023 in advance of a second, and currently unexpected, round of Fed tightening beginning in late-2023 or 2024. Dear Client, Instead of our regular report next week, we will be sending you a Special Report written by Matt Gertken, BCA Research’s Chief Geopolitical Strategist, discussing the geopolitical implications of the war in Ukraine. We will be back the following week with the GIS Quarterly Strategy Outlook, where we will explore the major trends that are set to drive financial markets in the rest of 2022 and beyond. As always, I will hold a webcast discussing the outlook the week after, on Thursday, April 7th. Best regards, Peter Berezin Chief Global Strategist https://www.linkedin.com/in/peter-berezin-1289b87/ https://twitter.com/BerezinPeter A Two-Stage Fed Tightening Cycle The FOMC raised rates by 25 basis points this week, the first of seven rate hikes that the Federal Reserve has telegraphed in its Summary of Economic Projections for the remainder of 2022. We expect the Fed to follow through on its planned rate hikes this year, but then go on pause in early-2023, as inflation temporarily comes down. However, the Fed will resume raising rates in late-2023 or 2024 once inflation begins to reaccelerate and it becomes clear that monetary policy is still too easy. This second round of monetary tightening is currently not anticipated by market participants. If anything, investors think the Fed is more likely to cut rates than raise rates towards the end of next year (Chart 1). The Fed’s own views are not that different from the markets’: The central tendency range for the Fed’s terminal interest rate dot remained at 2.3%-to-2.5% following this week’s FOMC meeting, with the median dot actually ticking lower to 2.4% from 2.5% (Chart 2).

Image

Chart 2The Fed Is Still In The Secular Stagnation Camp

The Fed Is Still In The Secular Stagnation Camp

The Fed Is Still In The Secular Stagnation Camp

A Higher Neutral Rate

Image

Our higher-than-consensus view of where US rates will eventually end up reflects our conviction that the neutral rate of interest is somewhere between 3% and 4%. One can think of the neutral rate as the interest rate that equates the amount of investment a country wants to undertake at full employment with the amount of savings that it has at its disposal.1 Anything that reduces savings or increases investment would raise the neutral rate (Chart 3). As we discussed last month, a number of factors are likely to lower desired savings in the US over the next few years: Households will spend down their accumulated pandemic savings. US households are sitting on $2.3 trillion (10% of GDP) in excess savings, the result of both decreased spending on services during the pandemic and the receipt of generous government transfer payments (Chart 4). Household wealth has soared since the start of the pandemic (Chart 5). Conservatively assuming that households spend three cents of every additional dollar in wealth, the resulting wealth effect could boost consumption by nearly 4% of GDP.

Image

Chart 5Net Worth Has Soared Since The Pandemic

Net Worth Has Soared Since The Pandemic

Net Worth Has Soared Since The Pandemic

The household deleveraging cycle has ended (Chart 6). Household balance sheets are in good shape. After falling during the initial stages of the pandemic, consumer credit has begun to rebound. Banks are easing lending standards on consumer loans across the board. Baby boomers are retiring. They hold over half of US household wealth, considerably more than younger generations (Chart 7). As baby boomers transition from savers to dissavers, national savings will decline. Chart 6US Household Deleveraging Pressures Have Abated

US Household Deleveraging Pressures Have Abated

US Household Deleveraging Pressures Have Abated

Chart 7Baby Boomers Have Amassed A Lot Of Wealth

Is A Higher Neutral Rate Good Or Bad For Stocks?

Is A Higher Neutral Rate Good Or Bad For Stocks?

Government budget deficits will stay elevated. Fiscal deficits subtract from national savings. While the US budget deficit will come down over the next few years, the IMF estimates that the structural budget deficit will still average 4.9% of GDP between 2022 and 2026 compared to 2.0% of GDP between 2014 and 2019 (Chart 8). On the investment front: The deceleration in trend GDP growth, which depressed investment spending, has largely run its course.2 According to the Congressional Budget Office, real potential GDP growth fell from over 3% in the early 1980s to about 1.9% today. The CBO expects potential growth to edge down only slightly to 1.7% over the next few decades (Chart 9). Chart 8Fiscal Policy: Tighter But Not Tight

Is A Higher Neutral Rate Good Or Bad For Stocks?

Is A Higher Neutral Rate Good Or Bad For Stocks?

Chart 9Much Of The Deceleration In Potential Growth Has Already Happened

Much Of The Deceleration In Potential Growth Has Already Happened

Much Of The Deceleration In Potential Growth Has Already Happened

After moving broadly sideways for two decades, core capital goods orders – a leading indicator for capital spending – have broken out to the upside (Chart 10). Capex intention surveys remain upbeat (Chart 11). The average age of the nonresidential capital stock currently stands at 16.3 years, the highest since 1965 (Chart 12). Chart 10Positive Signs For Capex (I)

Positive Signs For Capex (I)

Positive Signs For Capex (I)

Similar to nonresidential investment, the US has been underinvesting in residential real estate (Chart 13). The average age of the housing stock has risen to a 71-year high of 31 years. The homeowner vacancy rate has plunged to the lowest level on record. The number of newly finished homes for sale is half of what it was prior to the pandemic. Chart 11Positive Signs For Capex (II)

Positive Signs For Capex (II)

Positive Signs For Capex (II)

Chart 12An Aging Capital Stock

An Aging Capital Stock

An Aging Capital Stock

Chart 13Housing Is In Short Supply

Housing Is In Short Supply

Housing Is In Short Supply

The New ESG: Energy Security and Guns The war in Ukraine will put further pressure on the neutral rate, especially outside of the United States. Chart 14European Capex Should Recover

European Capex Should Recover

European Capex Should Recover

After staging a plodding recovery following the euro debt crisis, European capital spending received a sizable boost from the launch of the NextGenerationEU Recovery Fund (Chart 14). Capital spending will rise further in the years ahead as European governments accelerate efforts to make their economies less reliant on Russian energy. Meanwhile, European governments are trying to ease the burden from rising energy costs. France has introduced a rebate on fuel starting on April 1st. It is part of a EUR 20 billion package aimed at cutting heating and electricity bills. Other countries are considering similar measures. European military spending will also rise. Germany has already announced that it will spend EUR 100 billion more on defense. European governments will also need to boost spending to accommodate potentially several million Ukrainian refugees. A Smaller Chinese Current Account Surplus? Chart 15Will China Be A Source Of Excess Savings?

Will China Be A Source Of Excess Savings?

Will China Be A Source Of Excess Savings?

The difference between what a country saves and invests equals its current account balance. Historically, China has been a major exporter of savings, which has helped depress interest rates abroad. While China’s current account surplus has declined as a share of its own GDP, it has remained very large as a share of global ex-China GDP, reflecting China’s growing weight in the global economy (Chart 15). Many analysts assume that China will double down on efforts to boost exports in order to offset the drag from falling property investment. However, there is a major geopolitical snag with that thesis: A country that runs a current account surplus must, by definition, accumulate assets from the rest of the world. As the freezing of Russia’s foreign exchange reserves demonstrates, that is a risky proposition for a country such as China. Rather than increasing its current account surplus, China may seek to bolster its economy by raising domestic demand. This could be achieved by either boosting domestic investment on infrastructure and/or consumption. Notably, the IMF’s latest projections foresee China’s current account surplus falling by more than half between 2021 and 2026 as a share of global ex-China GDP. If this were to happen, the neutral rate in China and elsewhere would rise. The Path to Neutral: The Role of Inflation If one accepts the premise that the neutral rate in the US is higher than widely believed, what will the path to this higher rate look like?

Image

The answer hinges critically on the trajectory of inflation. If inflation remains stubbornly high, the Fed will be forced to hike rates by more than expected over the next 12 months. In contrast, if inflation comes down rapidly, then the Fed will be able to raise rates at a more leisurely pace. As late as early February, one could have made a strong case that US inflation was set to fall. The demand for goods was beginning to moderate as spending shifted back towards services. On the supply side, the bottlenecks that had impaired goods production were starting to ease. Chart 16 shows that the number of ships anchored off the coast of Los Angeles and Long Beach has been trending lower while the supplier delivery components of both the ISM manufacturing and nonmanufacturing indices had come off their highs. Since then, the outlook for inflation has become a lot murkier. As we discussed last week, the war in Ukraine is putting upward pressure on commodity prices, ranging from energy, to metals, to agriculture. BCA’s geopolitical team, led by Matt Gertken, expects the war to worsen before a truce of sorts is reached in a month or two. Meanwhile, a new Covid wave is gaining momentum. New daily cases are rising across Europe and have exploded higher in parts of Asia (Chart 17). In China, the number of new cases has reached a two-year high. The government has already locked down parts of the country encompassing 37 million people, including Shenzhen, a major high-tech hub adjoining Hong Kong. Chart 17Covid Cases Are On The Rise Again In Some Countries

Is A Higher Neutral Rate Good Or Bad For Stocks?

Is A Higher Neutral Rate Good Or Bad For Stocks?

Most new cases in China and elsewhere stem from the BA.2 subvariant of Omicron, which appears to be at least 50% more contagious than Omicron Classic. Given its extreme contagiousness, China may be forced to rely on massive nationwide lockdowns in order to maintain its zero-Covid strategy. While such lockdowns may provide some relief in the form of lower oil prices, the overall effect will be to worsen supply-chain disruptions. Watch For Signs of a Wage-Price Spiral As the experience of the 1960s demonstrates, the relationship between inflation and unemployment is inherently non-linear: The labor market can tighten for a long time with little impact on prices and wages, only for a wage-price spiral to suddenly develop once unemployment falls below a certain threshold (Chart 18). Chart 18A Wage-Price Spiral Was Ignited By Very Low Unemployment Levels In The 1960s

Is A Higher Neutral Rate Good Or Bad For Stocks?

Is A Higher Neutral Rate Good Or Bad For Stocks?

Chart 19Wage Growth Has Picked Up, But Mostly At The Bottom End Of The Income Distribution

Wage Growth Has Picked Up, But Mostly At The Bottom End Of The Income Distribution

Wage Growth Has Picked Up, But Mostly At The Bottom End Of The Income Distribution

For the time being, a wage-price spiral does not appear imminent. While wage growth has picked up, most of the increase in wages has occurred at the bottom end of the income distribution (Chart 19). Chart 20More Low-Wage Employees Should Return To Work

More Low-Wage Employees Should Return To Work

More Low-Wage Employees Should Return To Work

Low-wage workers have not returned to the labor force to the same extent as higher-wage workers (Chart 20). However, now that extended unemployment benefits have lapsed and savings deposits are being drawn down, the incentive to resume work will strengthen. An influx of workers back into the labor market will cap wage growth, at least for this year. Long-Term Inflation Expectations Still Contained A sudden increase in long-term inflation expectations can be a precursor to a wage-price spiral because the expectation of higher prices can induce consumers to shop now before prices rise further, while also incentivizing workers to demand higher wages. Reassuringly, long-term inflation expectations have not risen that much. Expected inflation 5-to-10 years out in the University of Michigan survey registered 3.0% in March, down a notch from 3.1% in February (Chart 21). While the widely followed 5-year, 5-year forward TIPS inflation breakeven rate has climbed to 2.32%, it is still at the bottom of the Fed’s comfort zone of 2.3%-to-2.5% (Chart 22).3 Chart 21Long-Term Inflation Expectations Remain Contained (I)

Long-Term Inflation Expectations Remain Contained (I)

Long-Term Inflation Expectations Remain Contained (I)

Chart 22Long-Term Inflation Expectations Remain Contained (II)

Long-Term Inflation Expectations Remain Contained (II)

Long-Term Inflation Expectations Remain Contained (II)

Chart 23The Magnitude Of Damage Depends On How Long The Commodity Price Shock Lasts

Is A Higher Neutral Rate Good Or Bad For Stocks?

Is A Higher Neutral Rate Good Or Bad For Stocks?

Moreover, the jump in market-based inflation expectations since the start of the war in Ukraine has been fueled by rising oil prices. The forwards are pointing to a fairly pronounced decline in the price of crude and most other commodity prices over the next 12 months (Chart 23). If that happens, inflation expectations will dip anew. Investment Implications The neutral rate of interest is higher in the United States than widely believed. A higher neutral rate is arguably good for stocks over the short-to-medium term because it lowers the risk that the Fed will accidentally induce a recession this year by bringing rates into restrictive territory. Over a longer-term horizon of 2-to-5 years, however, a higher neutral rate is bad news for stocks because it means that investors will eventually need to value stocks using a higher discount rate. It also means that the Fed could find itself woefully behind the curve in normalizing monetary policy. While the war in Ukraine and yet another Covid wave could continue to unsettle markets for the next month or two, global equities will be higher in 12 months than they are now. With inflation in the US likely to temporarily come down in the second half of the year, bond yields probably will not rise much more this year. However, yields will start moving higher in the second half of next year as it becomes clear that policy rates still have further to rise. The bull market in stocks will end at that point. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 These savings can either by generated domestically or imported from abroad via a current account deficit. 2 Theoretically, there is a close relationship between trend growth and the equilibrium investment-to-GDP ratio. For example, if real trend growth is 3% and the capital stock-to-GDP ratio is 200%, a country would need to invest 6% of GDP net of depreciation to maintain the existing capital stock-to-GDP ratio. In contrast, if trend growth were to fall to 2%, the country would only need to invest 4% of GDP. 3 The Federal Reserve targets an average inflation rate of 2% for the personal consumption expenditures (PCE) index. The TIPS breakeven is based on the CPI index. Due to compositional differences between the two indices, CPI inflation has historically averaged 30-to-50 basis points higher than PCE inflation. This is why the Fed effectively targets a CPI inflation rate of about 2.3%-to-2.5%. View Matrix

Is A Higher Neutral Rate Good Or Bad For Stocks?

Is A Higher Neutral Rate Good Or Bad For Stocks?

Special Trade Recommendations Current MacroQuant Model Scores

Is A Higher Neutral Rate Good Or Bad For Stocks?

Is A Higher Neutral Rate Good Or Bad For Stocks?

Executive Summary Major EM’s Defense Spends Will Be Comparable To That Of Developed Countries

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Tectonic geopolitical trends are taking shape in Emerging Markets (EMs) today that will leave an indelible imprint on the next decade. First, EMs have gone on a relatively unnoticed public debt binge at a time when the economic prospects of the median EM citizen have deteriorated. This raises the spectre of sudden fiscal populism, aggressive foreign policy or social unrest in EMs. China, Brazil and Saudi Arabia appear most vulnerable to these risks. Second, the defense bill of major EMs could be comparable to that of the top developed countries of the world in a decade from now. Investors must brace for EMs to play a central role in the defense market and in wars, in the coming years. To profit from ascendant geopolitical risks in China, we reiterate shorting TWD-USD and the CNY against an equal-weighted basket of Euro and USD. To extract most from the theme of EM militarization, we suggest a Long on European Aerospace & Defense relative to European Tech stocks. Trade Recommendation Inception Date Return LONG EUROPEAN AEROSPACE & DEFENSE / EUROPEAN TECH EQUITIES (STRATEGIC) 2022-03-18 Bottom Line: Even as EMs are set to emerge as protagonists on the world stage, investors must prepare for these countries to exhibit sudden fiscal expansions, bouts of social unrest or a newfound propensity to initiate wars. The only way to dodge these volatility-inducing events is to leverage geopolitics to foresee these shocks. Feature Only a few weeks before Russia’s war with Ukraine broke out, a client told us that he was having trouble seeing the importance of geopolitics in investing. “It seems like geopolitics was a lot more relevant a few years back, with the European debt crisis, Brexit, and Trump. Now it does not seem to drive markets at all”, said the client. To this we gave our frequent explanation which is, “Our strategic themes of Great Power Struggle, Hypo-Globalization, and Nationalism/Populism are now embedded in the international system and responsible for an observable rise in geopolitical risk that is reshaping markets”. In particular we highlighted our pessimistic view on both Russia and Iran, which have incidentally crystallized most clearly since we had this client conversation. Related Report Geopolitical StrategyBrazil: The Road To Elections Won't Be Paved With Good Intentions Globally key geopolitical changes are afoot with Russia at war. In the coming weeks and months, we will write extensively about the dramatic changes we see taking shape in the realm of geopolitics and investing. We underscored the dramatic geopolitical realignment taking place as Russia severs ties with the West and throws itself into China’s arms in a report titled “From Nixon-Mao To Putin-Xi”. In this Special Report we highlight two key geopolitical themes that will affect emerging markets (EMs) over the coming decade. The aim is to help investors spot these trends early, so that they can profit from these tectonic changes that are sure to spawn a new generation of winners and losers in financial markets. (For BCA Research’s in-depth views on EMs, do refer to the Emerging Markets Strategy (EMS) webpage). Trend #1: Beware The Wrath Of EMs On A Debt Binge Chart 1The Pace Of Debt Accumulation Has Accelerated In Major EMs

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Investors are generally aware of the debt build-up that has taken place in the developed world since Covid-19. The gross public debt held by the six most developed countries of the world (spanning US, Japan, Germany, UK, France and Italy) now stands at an eye-watering $60 trillion or about 140% of GDP. This debt pile is enormous in both absolute and relative terms. But at the same time, the debt simultaneously being taken on by EMs has largely gone unnoticed. The cumulative public debt held by eight major EMs today (spanning China, Taiwan, Korea, India, Brazil, Russia, Saudi Arabia and Turkey) stands at $20tn i.e., about 70% of GDP. Whilst the absolute value of EM debt appears manageable, what is worrying is the pace of debt accumulation. The average public debt to GDP ratio of these EMs fell over the early 2000s but their public debt ratios have now doubled over the last decade (Chart 1). EMs have been accumulating public debt at such a rapid clip that the pace of debt expansion in EMs is substantially higher than that of the top six developed countries (Chart 1). These six DMs have a larger combined GDP than the eight EMs with which they are compared. Related Report Geopolitical StrategyIndia's Politics: Know When To Hold 'Em, Know When To Fold 'Em (For in-depth views on China’s debt, do refer to China Investment Strategy (CIS) report here). Now developed countries taking on more debt makes logical sense for two reasons. Firstly, most developed countries are ageing, and their populations have stopped growing. So one way to prop up falling demand is to get governments to spend more using debt. Secondly, this practice seems manageable because developed country central banks have deep pockets (in the form of reserves) and their central banks are issuers of some of the safest currencies of the world. But EMs using the same formula and getting addicted to debt at an earlier stage of development is risky and could prove to be lethal in some cases. Also distinct from reasons of macroeconomics, the debt binge in EMs this time is problematic for geopolitical reasons. This Time Is Different EMs getting reliant on debt is problematic this time because their median citizen’s economic prospects have deteriorated. Growth is slowing, inflation is high, and job creation is stalling; thereby creating a problematic socio-political backdrop to the EM debt build-up. Growth Is Slowing: In the 2000s EMs could hope to grow out of their social or economic problems. The cumulative nominal GDP of eight major EMs more than quadrupled over the early 2000s but a decade later, these EMs haven not been able to grow their nominal GDP even at half the rate (Chart 2). Inflation Remains High: Despite poorer growth prospects, inflation is accelerating. Inflation was high in most major EMs in 2021 (Chart 3) i.e., even before the surge seen in 2022. Chart 2Major EM’s Growth Engine Is No Longer Humming Like A Well-Tuned Machine

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Chart 3Despite Slower Growth, Inflation In Major EMs Remains High

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Rising Unemployment: Employment levels have improved globally from the precipice they had fallen into in 2020. But unemployment today is a far bigger problem for major EMs as compared to developed markets (Chart 4). If the economic miseries of the median EM citizen are not addressed, then they can produce disruptive sociopolitical effects that will fan market volatility. This problem of rising economic misery alongside a rapid debt build-up, can also be seen for the next tier of EMs i.e. Mexico, Indonesia, Iran, Poland, Thailand, Nigeria, Argentina, Egypt, South Africa and Vietnam. While the average public debt to GDP ratios of these EMs fell over the early 2000s, the pace of debt accumulation has almost doubled over the last decade (Chart 5). Furthermore, the growth engine in these smaller EMs is no longer humming like a well-tuned machine and inflation remains at large (Chart 5). Chart 4Unemployment - A Bigger Problem In Major EMs Today

Unemployment - A Bigger Problem In Major EMs Today

Unemployment - A Bigger Problem In Major EMs Today

Chart 5Smaller EMs Must Also Deal With Rising Debt, Alongside Slowing Growth

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Chart 6The Debt Surge In EMs This Time, Poses Unique Challenges

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

History suggests that periods of economic tumult are frequently followed by social unrest. The eruption of the so-called Arab Spring after the Great Recession illustrated the power of this dynamic. Then following the outbreak of Covid-19 in 2020 we had highlighted that Turkey, Brazil, and South Africa are at the greatest risk of significant social unrest. We also showed that even EMs that looked stable on paper faced unrest in the post-Covid world, including China and Russia. In this report we take a decadal perspective which reveals that growth is slowing, and debt is growing in EMs. Given that EMs suffer from rising economic miseries alongside growing debt and lower political freedoms (Chart 6), it appears that some of these markets could be socio-political tinderboxes in the making. Policy Implications Of The EM Debt Surge “As it turns out, we don't 'all' have to pay our debts. Only some of us do.” – David Graeber, Debt: The First 5,000 Years (Melville House Publishing, 2011) The trifecta of fast-growing debt, slowing growth and/or low political freedoms in EMs can add to the volatility engendered by EMs as an asset class. Given the growing economic misery in EMs today, politicians will be wary of outbreaks of social unrest. To quell this unrest, they may resort broadly to fiscal expansion and/or aggressive foreign policy. Both of these policy choices can dampen market returns in EMs. Chart 7India's Performance Had Flatlined Post Mild Populist Tilt

India's Performance Had Flatlined Post Mild Populist Tilt

India's Performance Had Flatlined Post Mild Populist Tilt

Policy Choice #1: More Fiscal Spending Despite High Debt Policymakers in some EMs may respond by de-prioritizing contentious structural reforms and prioritizing fiscal expansion. The Indian government’s decision to repeal progressive changes to farm laws in late 2021, launch a $7 billion home-building program in early 2022 and withholding hikes in retail prices of fuel, illustrates how policymakers are resorting to populism despite high public debt levels. As a result, it is no surprise that MSCI India had been underperforming MSCI EM even before the war in Ukraine broke out (Chart 7). Brazil is another EM which falls into this category, while China’s attempts to run tighter budgets have failed in the face of slowing growth. Policy Choice #2: Foreign Policy Aggression EMs may also adopt an aggressive foreign policy stance. Russia’s decision to invade Ukraine, Turkey’s interventions in several countries, and China’s increasing assertiveness in its neighboring seas and the Taiwan Strait provide examples. Wars by EMs are known to dampen returns as the experience of the Russian stock market shows. Russian stocks fell by 14% during its invasion of Georgia in 2008 and are down 40% from 24 February 2022 until March 9, 2022, i.e. when MSCI halted trading. If politicians fail to pursue either of these policies, then they run the risk of social unrest erupting due to tight fiscal policy or domestic political disputes. In fact, early signs of social discontent are already evident from large protests seen in major EMs over the last year (see Table 1). Table 1Social Unrest In Major EMs Is Already Ascendant

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Bottom Line: The last decade has seen major EMs go on a relatively unnoticed public debt binge. This is problematic because this debt surge has come at a time when economic prospects of the median EM citizen have deteriorated. Politicians will be keen to quell the resultant discontent. This raises the specter of excessive fiscal expansion, aggressive foreign policy, and/or social unrest. All three outcomes are negative from an EM volatility perspective. Trend #2: The Rise And Rise Of EM Defense Spends Great Power Rivalry is an outgrowth of the multipolar structure of international relations. This theme will drive higher defense spending globally. In this report we highlight that even after accounting for a historic rearmament in developed countries following Russia’s invasion of Ukraine, a decade from now EMs will play a key role in driving global military spends. The defense bill of the six richest developed countries of the world (the US, Japan, Germany, UK, France and Italy) will increasingly be rivaled by that of the top eight EMs (China, Taiwan, Korea, India, Brazil, Russia, Saudi Arabia and Turkey). While key developed markets like Japan and Germany in specific (and Europe more broadly) are now embarking on increasing defense spends, the unstable global backdrop will force EMs to increase their military budgets as well. The combination of these forces could mean that the top eight EM’s defense spends could be comparable to that of the top six developed markets in a decade from now i.e., by 2032 (Chart 8). This is true even though the six DMs have a larger GDP. The assumptions made while arriving at the 2032 defense spend projections include: Substantially Higher Pace Of Defense Spends For Developed Countries: To reflect the fact that Russia’s invasion of Ukraine will trigger a historical wave of armament in developed markets we assume that: (a) NATO members France, Germany and Italy (who spent about 1.5% of GDP on an average on defense spends in 2019) will ramp up defense spending to 2% of GDP by 2032, (b) US and UK i.e. NATO members who already spend substantially more than 2% of GDP on defense spends will still ‘increase’ defense spends by another 0.4% of GDP each by 2032 and finally (c) Japan which spends less than 1% of GDP on defense spends today, in a structural break from the past will increase its spending which will rise to 1.5% of GDP by 2032. China And Hence Taiwan As Well As India Will Boost Spends: To capture China’s increasingly aggressive foreign policy stance and the fact that India as well as Taiwan will be forced to respond to the Chinese threat; we assume that China increases its stated defense spends from 1.7% of GDP in 2019 to 3% by 2032. Taiwan follows in lockstep and increases its defense spends from 1.8% of GDP in 2019 to 3% by 2032. India which is experiencing a pincer movement from China to its east and Pakistan to its west will have no choice but to respond to the high and rising geopolitical risks in South Asia. The coming decade is in fact likely to see India’s focus on its naval firepower increase meaningfully as it feels the need to fend off threats in the Indo-Pacific. India currently maintains high defense spends at 2.5% of GDP and will boost this by at least 100bps to 3.5% of GDP by 2032. Defense Spending Trends For Five EMs: For the rest of the EMs (namely Russia, Saudi Arabia, South Korea and Brazil), the pace of growth in defense spending seen over 2009-19 is extrapolated to 2032. For Turkey, we assume that defense spends as a share of GDP increases to 3% of GDP by 2032. Extrapolation Of Past GDP Growth For All Countries: For all 14 countries, we extrapolate the nominal GDP growth calculated by the IMF for 2022-26 as per its last full data update, to 2032. This tectonic change in defense spending patterns has important historical roots. Back in 1900, UK and Japan i.e., the two seafaring powers were top defense spenders (Chart 9). Developed countries of the world continued to lead defense spending league tables through the twentieth century as they fought expensive world wars. Chart 8Major EM’s Defense Spends Will Be Comparable To That Of Developed Countries

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Chart 9Back In 1900, Developed Countries Like UK And Japan Were Top Military Spenders

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Chart 10By 2000, EMs Had Begun Spending Generously On Armament

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

But things began changing after WWII. Jaded by the world wars, developed countries began lowering their defense spending. By the early 2000s EMs had now begun spending generously on armament (Chart 10). The turn of the century saw growth in developed markets fade while EMs like China and India’s geopolitical power began rising (Chart 11). Then a commodities boom ensued, resulting in petro-states like Saudi Arabia establishing their position as a high military spender. The confluence of these factors meant that by 2020 EMs had becomes major defense spenders in both relative and absolute terms too (Chart 12). Going forward, we expect the coming renaissance in DM defense spending in the face of Russian aggression, alongside rising geopolitical aspirations of China, to exacerbate this trend of rising EM militarization. Chart 11The 21st Century Saw Developed Countries’ Geopolitical Power Ebb

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Chart 12EMs Today Are Top Military Spenders, Even In Absolute Terms

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Why Does EM Weaponizing Matter? History suggests that wars are often preceded by an increase in defense spends: Well before WWI, a perceptible increase in defense spending could be seen in Austria-Hungary, Germany, and Italy (Chart 13). These three countries would go on to be known as the Triple Alliance in WWI. Correspondingly France, Britain and Russia (i.e., countries that would constitute the Triple Entente) also ramped up military spending before WWI (Chart 14). Chart 13Well Before WWI; Austria-Hungary, Germany, And Italy Had Begun Ramping Up Defense Spends

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Chart 14The ‘Triple Entente’ Too Had Increased Defense Spends In The Run Up To WWI

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

History tragically repeated itself a few decades later. Besides Japan (which invaded China in 1937); Germany and Italy too ramped up defense spending well before WWII broke out (Chart 15). These three countries would come to be known as the Axis Powers and initiated WWII. Notably, Britain and Russia (who would go on to counter the Axis Powers) had also been weaponizing since the mid-1930s (Chart 16). Chart 15Axis Powers Had Been Increasing Defense Spends Well Before WWII

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Chart 16Allied Powers Too Had Been Increasing Defense Spends In The Run Up To WWII

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Chart 17Militarily Active States Have Been Ramping Up Defense Spends

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Russia, Ukraine, Turkey and Gulf Arab states like Iraq have been involved in wars in the recent past and noticeably increased their defense budgets in the lead-up to military activity (Chart 17). Given that a rise in military spending is often a leading indicator of war and given that EMs are set to spend more on defense, it appears that significant wars are becoming more rather than less likely, which Russia’s invasion of Ukraine obviously implies. A large number of “Black Swan Risks” are clustered in the spheres of influence of Russia, China, and Iran, which are the key powers attempting to revise the US-led global order today (Map 1). Map 1Black Swan Risks Are Clustered Around China, Russia & Iran

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Distinct from major EMs, eight small countries pose meaningful risks of being involved in wars over the next. These countries are small (in terms of their nominal GDPs) but spend large sums on defense both in absolute terms (>$4 billion) and in relative terms (>4% of GDP). Incidentally all these countries are located around the Eurasian rimland and include Israel, Pakistan, Algeria, Iran, Kuwait, Oman, Ukraine and Morocco (Map 2). In fact, the combined sum of spending undertaken by these countries is so meaningful that it exceeds the defense budgets of countries like Russia and UK (Chart 18). Map 2Eight Small Countries That Spend Generously On Defense

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Chart 188 Countries Located Near The Eurasian Rimland, Spend Large Sums On Defense

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Bottom Line: As EM geopolitical power and aspirations rise, the defense bill of top developed countries will be challenged by the defense spending undertaken by major EMs. On one hand this change will mean that certain EMs may be at the epicenter of wars and concomitant market volatility. On the other hand, this change could spawn a new generation of winners amongst defense suppliers. Investment Conclusions In this section we highlight strategic trades that can be launched to play the two trends highlighted above. Trend #1: Beware The Wrath Of EMs On A Debt Binge Investors must prepare for EMs to witness sudden fiscal expansions, unusually aggressive foreign policy stances, and/or bouts of social unrest over the next few years. The only way to dodge these volatility-inducing events in EMs is to leverage geopolitics to foresee socio-political shocks. Using a simple method called the “Tinderbox Framework” (Table 2), we highlight that: Table 2Tinderbox Framework: Identifying Countries Most Exposed To Socio-Political Risks

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Within the eight major EMs; China, Brazil, Russia and Saudi Arabia face elevated socio-political risks. Amongst the smaller ten EMs, these risks appear most elevated for Egypt, South Africa and Argentina. It is worth noting that Brazil, South Africa and Turkey appeared most vulnerable as per our Covid-19 Social Unrest Index that we launched in 2020. We used the tinderbox framework in the current context to fade out effects of Covid-19 and to add weight to the debt problem that is brewing in EMs. Client portfolios that are overweight on most countries that fare poorly on our “Tinderbox Framework” should consider actively hedging for volatility at the stock-specific level. To profit from ascendant geopolitical risks in China, we reiterate shorting TWD-USD and the CNY against an equal-weighted basket of Euro and USD. China’s public debt ratio is high and social pressures may be building with limited valves in place to release these pressures (Table 2). The renminbi has performed well amid the Russian war, which has weighed down the euro, but China faces a confluence of domestic and international risks that will ultimately drag on the currency, while the euro will benefit from the European Union’s awakening as a geopolitical entity in the face of the Russian military threat. Trend #2: EM’s Will Drive Wars In The 21st Century Wars are detrimental to market returns.1 Furthermore, as the history of world wars proves, even the aftermath of a war often yields poor investment outcomes as wars can be followed by recessions. It is in this context that investors must prepare for the rise of EMs as protagonists in the defense market, by leveraging geopolitics to identify EMs that are most likely to be engaged in wars. While we are not arguing that WWIII will erupt, investors must brace for proxy wars as an added source of volatility that could affect EMs as an asset class. To profit from these structural changes underway we highlight two strategic trades namely: 1. Long Global Aerospace & Defense / Broad Market Thanks to the higher spending on defense being undertaken by major EMs, global defense spends will grow at a faster rate over the next decade as compared to the last. We hence reiterate our Buy on Global Aerospace & Defense relative to the broader market. 2. Long European Aerospace & Defense / European Tech Up until Russia invaded Ukraine and was hit with economic sanctions, Russia was the second largest exporter of arms globally accounting for 20% global arms exports. With Russia’s ability to sell goods in the global market now impaired, the two other major suppliers of defense goods that appear best placed to tap into EM’s demand for defense goods are the US (37% share in the global defense exports market) and Europe (+25% share in the global defense exports market). Chart 19American Defense Stocks Have Outperformed, European Defense Stocks Have Underperformed

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

Chart 20Defense Market: Russia’s Loss Could Be Europe’s Gain

Beware EMs That Borrow Too Much Or Wage War

Beware EMs That Borrow Too Much Or Wage War

But given that (a) American aerospace & defense stocks have rallied (Chart 19) and given that (b) France, Germany, and Italy are major suppliers of defense equipment to countries that Russia used to supply defense goods to (Chart 20), we suggest a Buy on European Aerospace & Defense relative to European Tech stocks to extract more from this theme. In fact, this trade also stands to benefit from the pursuance of rearmament by major European democracies which so far have maintained lower defense spends as compared to America and UK. This view from a geopolitical perspective is echoed by our European Investment Strategy (EIS) team too who also recommend a Long on European defense stocks and a short on European tech stocks. Ritika Mankar, CFA Editor/Strategist ritika.mankar@bcaresearch.com Footnotes 1 Please see: Andrew Leigh et al, “What do financial markets think of war in Iraq?”, NBER Working Paper No. 9587, March 2003, nber.org. David Le Bris, “Wars, Inflation and Stock Market Returns in France, 1870-1945”, Financial History Review 19.3 pp. 337-361, December 2012, ssrn.com. Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Regional Geopolitical Risk Matrix

Executive Summary Profit Margins Are Headed Lower; So Are Equity Multiples

Profit Margins Are Headed Lower; So Are Equity Multiples

Profit Margins Are Headed Lower; So Are Equity Multiples