Equities

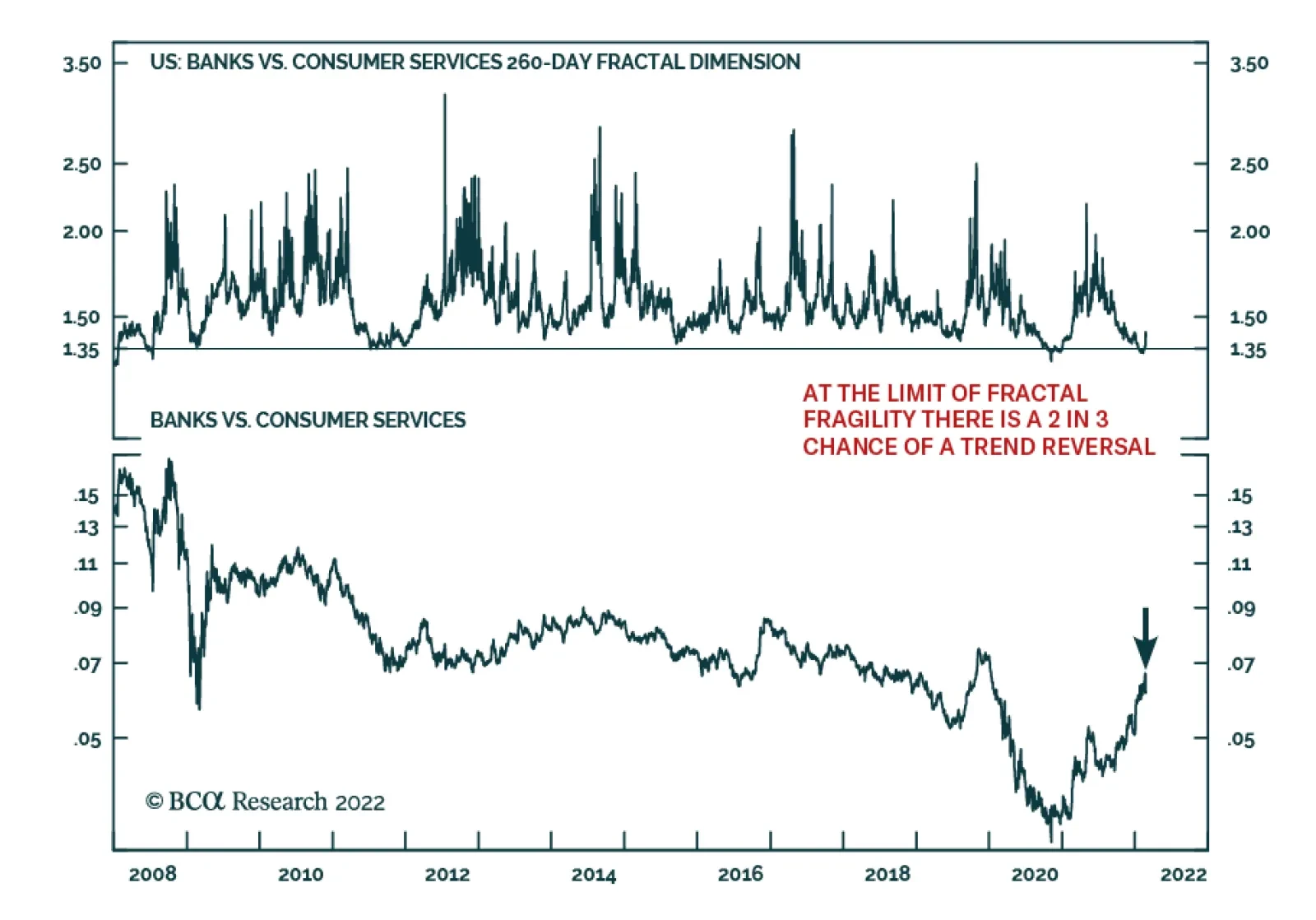

BCA Research’s 260-day fractal dimension is signaling a near term counter-trend reversal in the US Banks sector. For any investment, excessive groupthink and trend following can cause it to reach a point of instability at which the trend is likely to break…

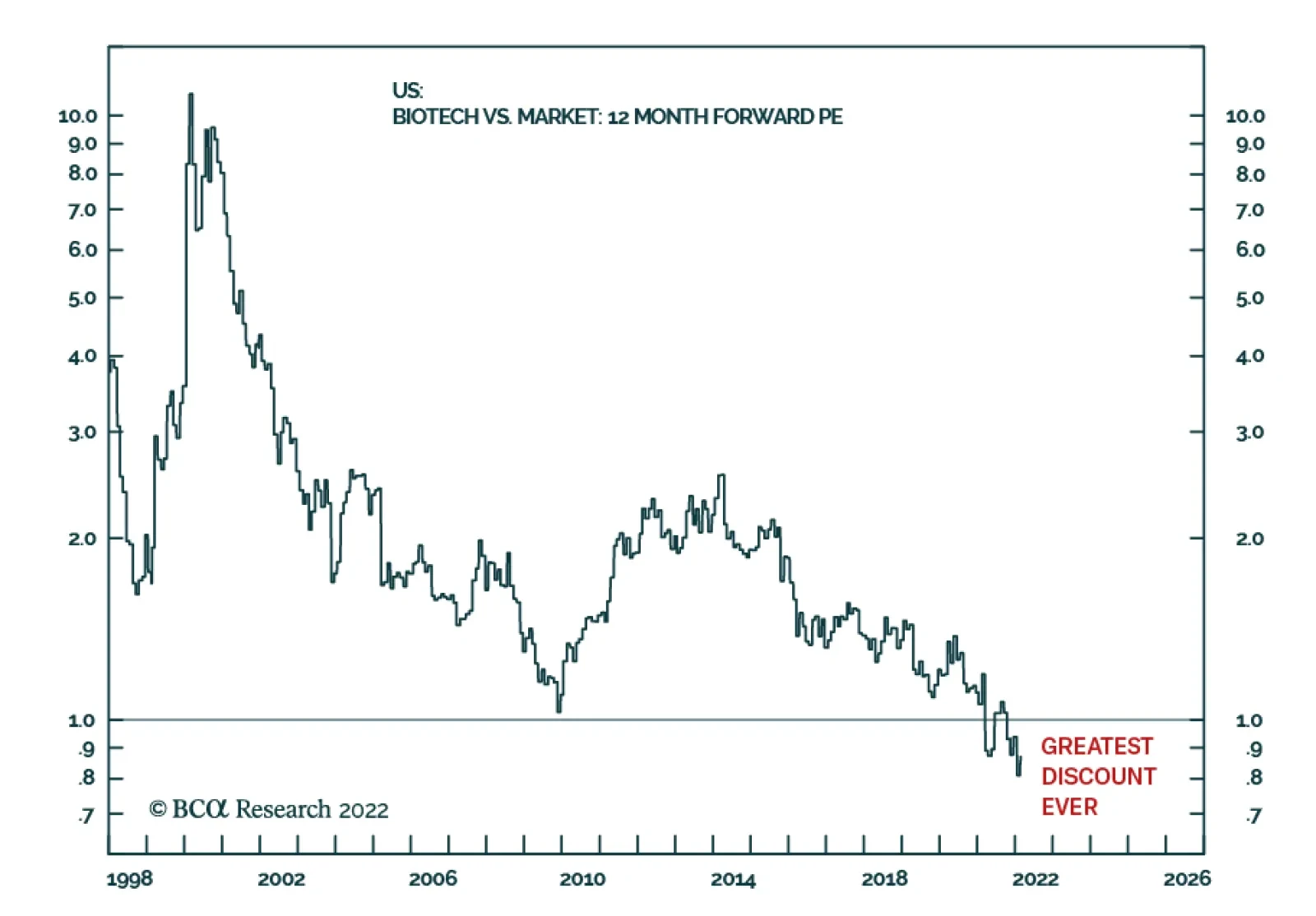

Every now and then comes a rare opportunity to buy a deeply unloved asset at a bargain basement price. The beaten-down biotech sector provides such an opportunity now – as it is trading at its greatest-ever discount to the market. Much of biotech’s…

Executive Summary Through February 24th, our ETF portfolio outperformed its benchmark by 18 basis points. Its risk-friendly orientation helped it generate double that amount of outperformance in its first two weeks but cost it as markets broadly declined over the last two weeks. In line with our fixed income strategists’ recommendation, we are tactically shifting our fixed income positioning to neutral duration from below-benchmark duration. Our longer-run expectation for higher interest rates remains intact. We are not making any portfolio adjustments in response to Russia’s invasion of Ukraine. Although the situation is fluid, we share the BCA house view that the conflict will be narrowly confined to Ukraine and the Black Sea as long as the flow of energy between Russia and the EU continues unabated. Ukraine underscores the potential for volatility to surge from an already elevated base as news items interact with uncertainty about the Fed. We will continue to manage the ETF portfolio with a more tactical bent than we otherwise would. 2022 Rate Hike Expectations Have Gone Too Far

2022 Rate Hike Expectations Have Gone Too Far

2022 Rate Hike Expectations Have Gone Too Far

Bottom Line: Russia’s movements of troops and materiel have been weighing on equity markets. Now that it has made its move, the bottom of the range may be near. Feature This is the first of a series of monthly reports devoted to the ETF portfolio we launched at the end of January. Each report will review the previous month’s performance, tracking the portfolio's relative return and highlighting its key contributors. More importantly, it will reassess our forward-looking views and situate them in an asset allocation/portfolio construction context. This monthly report will also be our primary vehicle for making portfolio adjustments, though we will make intra-month changes if market prices or our views change enough to merit them. In the immediate future, the conflict in Ukraine looms large. Russia’s full-scale incursion into Ukraine on February 24th roiled global financial markets, especially in Europe, with US equities executing a stunning reversal, exemplified by the high-beta NASDAQ, which fell 3% in overnight futures trading before recovering all the decline en route to a 3% gain in the live session. The wild action highlighted the potential for volatility to spike while investors are already on edge over unusually high inflation and the Fed’s attempts to contain it. We reiterate that we expect volatility will remain elevated this year and perhaps across the entire rate hiking cycle. Looking Ahead On a call last week, a client asked us if we were more confident or less confident in our views than we were on our quarterly webcast two weeks ago. Though no major new data had arrived in the interim (and Russia had not yet invaded Ukraine), we responded that our conviction level was unchanged to slightly higher, given the comfort we derived from our fixed income colleagues’ well-reasoned argument for why they think rates have peaked in the near term and our own analysis of the University of Michigan consumer sentiment survey respondents’ perceptions of inflation. The Ukraine conflict has the potential to push energy prices higher in the very near term, but it does not alter our six-to-twelve-month view. Chart 1Entering The Fourth Wave Of Persistently High Volatility?

Entering The Fourth Wave Of Persistently High Volatility?

Entering The Fourth Wave Of Persistently High Volatility?

Chart 2A Whole Lot Of Dry Powder ...

A Whole Lot Of Dry Powder ...

A Whole Lot Of Dry Powder ...

We are still constructive on financial markets and the economy, as well, though we expect that geopolitics may well provide a catalyst for rolling surges in the already elevated VIX (Chart 1). The escalation of the Ukraine conflict will temporarily preserve the geopolitical risk premium embedded in crude oil prices, but the evergreen commodity rule that high prices are the best cure for high prices will soon assert itself. Our Commodity & Energy Strategy team projects that oil producers will ramp up supply sufficient to dislodge the risk premium by the end of the year, taking Brent crude down to $85 a barrel, where it expects it will remain throughout 2023. While high oil prices are a tax on economic activity, their adverse effect on the US is mitigated by its status as the world’s largest oil producer. Our positive outlook for the US economy rests on our expectation that flush American households will begin drawing down their mountain of pandemic savings (Chart 2, bottom panel) now that COVID infections are less numerous (Chart 3, top panel) and less serious (Chart 3, bottom panel). As the pandemic wanes, households will regain their full range of consumption options, from dining out and in-person entertainment to travel and lodging. Our base-case outlook has them spending about half of their $2-plus trillion of pandemic savings, but we note that they can draw upon other pools of capital. Household net worth has surged at a record rate over the eight quarters of the pandemic as the value of financial assets and homes surged, and banks are eager to help consumers deploy their idle credit capacity to top up their buying power (Chart 4). Chart 3... Is Ready To Be Deployed Now That Omicron Is Out Of The Way

... Is Ready To Be Deployed Now That Omicron Is Out Of The Way

... Is Ready To Be Deployed Now That Omicron Is Out Of The Way

Chart 4Banks Are Eager To Lend To Consumers

Banks Are Eager To Lend To Consumers

Banks Are Eager To Lend To Consumers

Persistent inflation could erode some of that buying power while weighing on consumer sentiment. The Russia-Ukraine conflict has the potential to push food costs higher along with energy costs, as Ukraine is a top ten producer of both corn and wheat and Russia is a global wheat heavyweight, but emerging markets are likely to bear the brunt of higher agricultural commodity prices as the US and the EU are net exporters of both grains. As detailed below, we expect inflation will soon peak and begin decelerating at a rapid clip, so we do not expect higher prices to weaken the consumption tailwind, no matter what the Ukraine affair may bring. We continue to have very high conviction that the US will grow well above trend in 2022 and expect that S&P 500 earnings per share will grow in the mid-to-high single digits. Yields Have Backed Up Enough (For Now) We expect that volatility will remain elevated throughout this year and perhaps over the course of the Fed’s entire rate-hiking campaign as investors navigate an unfamiliar inflation backdrop and the Fed grapples with the challenges of normalizing monetary policy after a decade and a half of extraordinary accommodation. We have therefore recommended that investors consider adopting a more tactical approach to portfolio management and we are committed to following our own advice in the ETF portfolio. Although our cyclical view of interest rates has not changed – we expect they are ultimately headed higher than bond market participants do – we are persuaded by our fixed income colleagues’ argument that they’ve backed up too much too soon. We are therefore unwinding our below-benchmark duration positioning in the fixed income segment of our portfolio and tactically shifting to benchmark duration. Our colleagues cite several reasons for their call, but they all coalesce around the way that relentless upside inflation surprises have prompted aggressive rate hike expectations. They argue that market participants have overestimated how much the FOMC will hike the fed funds rate this year, as the overnight index swap curve is now pricing in about 150 basis points (bps) of hikes (Chart 5). That is well above the FOMC’s median 75-bps projection in December, and even though the official projection will rise at the March meeting, there is almost no chance that the committee’s guidance will be more hawkish than what the market is already discounting. Since the FOMC cannot surprise to the upside, rate hike expectations cannot push yields any higher for now. Chart 5Interest Rate Markets Have Gotten Ahead Of Themselves

Interest Rate Markets Have Gotten Ahead Of Themselves

Interest Rate Markets Have Gotten Ahead Of Themselves

The uninterrupted run of upside US inflation surprises drove the bond market to ramp up its rate hike expectations, but we expect that US inflation will peak this spring and decelerate rapidly to less uncomfortable levels, even though they will remain well above the Fed’s 2% target. The Manufacturing ISM Prices Paid Index, which leads headline inflation by six months (Chart 6, middle panel), reflects the deceleration in commodity and other input prices that is already underway (Chart 6, top panel). The ISM Supplier Deliveries Indexes suggest that global supply chain pressures have already started to ease (Chart 6, bottom panel). Ukraine disruptions aside, our commodity and energy strategists see oil price momentum losing steam, with Brent crude falling to $85 per barrel in the second half of the year and holding at that level across 2023 (Chart 7). Chart 6Good Tidings From The ISM Survey ...

Good Tidings From The ISM Survey ...

Good Tidings From The ISM Survey ...

Chart 7... And Relief On The Oil Front

... And Relief On The Oil Front

... And Relief On The Oil Front

As COVID recedes and people can resume typical day-to-day activities, consumer spending will continue to shift from goods to services (Chart 8). High-demand goods in categories subject to supply constraints have undergone a natural experiment in surge pricing. With supply at a deficit relative to demand, prices have risen to ration items like new automobiles to purchasers with the greatest time preference. Easing supply chain bottlenecks will help on the supply side of the equation and the new availability of services alternatives – attending live events instead of upgrading home theater and audio systems, going to the gym instead of buying home exercise equipment, taking a summer vacation instead of building a new backyard deck – will help relieve some of the upward pressure on demand. Chart 8When Demand Shifts To Services ...

When Demand Shifts To Services ...

When Demand Shifts To Services ...

Chart 9... Inflation Will Ease

... Inflation Will Ease

... Inflation Will Ease

A shift in spending patterns favoring services will allow headline inflation to move away from extreme double-digit goods inflation to merely elevated services inflation (Chart 9). Chart 10No One Left To Sell

No One Left To Sell

No One Left To Sell

Our colleagues also expect that upward pressure on wages, which has been concentrated in service-sector positions at the low end of the scale, will ease as Omicron fades and workers are able to return to the labor force without fearing for their health. The tightening of financial conditions that has occurred as rates have backed up and equity prices have fallen will cool growth momentum and reduce the potential for overheating. With inflation soon peaking and longer-run inflation expectations having remained well anchored, the Fed will feel less pressure to hike rates according to markets’ accelerated timetable. Finally, Treasury market positioning is now so unbalanced to the short side that investors would appear to be nearly out of selling capacity to push yields higher (Chart 10). Bottom Line: We expect that Treasury yields will ultimately rise much higher than the bond market currently anticipates, but the forces that have pushed them sharply higher since early December are spent. The near-term path of least resistance for bond yields is to the downside and we are shifting to a tactically neutral duration position to prepare for it. Portfolio Changes We are leaving our current equity positioning intact, as it remains appropriate to overweight the energy, industrials and financials sectors while avoiding consumer staples and utilities and maintaining direct out-of-benchmark exposure to the S&P 500 Pure Value Index via RPV and to the S&P SmallCap 600 Index via IJR (please refer to Cyclical ETF Portfolio table on page 11). We are reducing our exposure to the 1- to 3-year segment of the Treasury curve by 200 bps (SHY) and to the 3- to 7-year segment by 60 bps (IEI) and increasing our exposure to the 7- to 10-year segment by 260 bps (IEF) to bring portfolio Treasury duration into balance with the benchmark. We are exiting LQDH, the rate-hedged investment-grade corporate bond ETF, and reallocating the proceeds to its unhedged LQD version to bring corporate bond duration into balance. Portfolio Performance Market volatility and equity declines over the past ten trading days have cut its alpha in half, but the risk-friendly cyclical ETF portfolio we introduced last month has nevertheless outperformed its benchmark by 18 basis points (“bps”) through last Thursday’s close. Our equity positioning accounted for most of the value-add (Chart 11). Rising yields were a significant tailwind given our short duration stance. They also supported our value and small-cap tilts and, to a lesser extent, our overweight position in financials. The surge in energy prices generously rewarded our energy equities overweight (XLE). Chart 11Direct Equity Sector Deviations

March 2022 Cyclical ETF Portfolio Review

March 2022 Cyclical ETF Portfolio Review

Widening spreads since the beginning of the year were a headwind to our positioning within the fixed-income space (Chart 12). Our overweight to variable-rate preferred stocks (VRP) as an alternative to dearly priced bonds was the main detractor. Chart 12Fixed Income Deviations

March 2022 Cyclical ETF Portfolio Review

March 2022 Cyclical ETF Portfolio Review

Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Jennifer Lacombe Associate Editor jenniferl@bcaresearch.com Cyclical ETF Portfolio

March 2022 Cyclical ETF Portfolio Review

March 2022 Cyclical ETF Portfolio Review

On Friday the PBoC boosted liquidity support in the financial system by injecting $45.8 billion through seven-day reverse repo agreements. This is the greatest liquidity injection since September 2020. There are two main reasons why the PBoC typically…

Executive Summary Stronger Capex Than Last Decade

Fallout From Ukraine

Fallout From Ukraine

The fog of war continues, but the worst potential outcome for the market—a freeze of Russian energy exports to Europe—has been avoided. Energy inflation is reaching its apex. Markets will remain volatile in the near term as uncertainty remains elevated in the coming days. Moreover, a transition from a recovery driven by consumer durable goods to services remains a hurdle against near-term European outperformance. Italian bonds and European banks are attractive, but it is not yet prudent to plunge headfirst into the euro. The longer-term consequences of the conflicts point toward greater capex and public deficits in Europe. This will boost the neutral rate of interest and European yields. Industrials and defense stocks are also key structural beneficiaries. Bottom Line: Keep hedges in place for the near term, as uncertainty remains rife. Buy Italian bonds and European banks, which will benefit from ECB support. Industrials still face near-term hurdles but should be a structural overweight position in European equity portfolios, along with financials and defense stocks. Feature The situation in Ukraine is reaching a climax. Following Russia’s recognition of the breakaway Luhansk and Donetsk People’s Republics (LPR and DPR) and its invasion of Ukraine, the S&P 500 entered correction territory. Importantly, the Dow Jones Euro Stoxx 50 is now down 10% since its January 5th high, which validates our repeated call over the past four weeks to hedge risk asset portfolios by selling EUR/CHF and EUR/JPY. An international conflict has begun and a human tragedy is unfolding; but, at the time of writing, it looks like the worst-case scenario for markets will be avoided. Germany is folding Nord Stream 2 indeterminably and Western allies have imposed painful economic sanctions on Russia. However, an expulsion of the SWIFT payment system is not in the cards. This is crucial because it greatly limits the risk that Russia will stop sending natural gas and oil to the EU. Ultimately, neither Russia nor the EU wants this outcome, since it imposes an enormous loss of revenues on the former (which needs hard currency to finance its war) and guarantees a recession for the latter (Chart 1). The war will still cost Europe. European natural gas prices surged again on Thursday, rising by more than 60% intraday. While a spike above EUR200/MWh is unlikely in the absence of an oil embargo, 20% of European natural gas imports pass through Ukraine. The conflict suggests that these flows will remain disrupted for now and that natural gas prices will remain between EUR80/MWh and EUR100/MWh for the next few months. This translates into elevated energy and electricity costs for the EU (Chart 2). Chart 1A European Recession Averted

Fallout From Ukraine

Fallout From Ukraine

Chart 2Peaking But Elevated

Fallout From Ukraine

Fallout From Ukraine

Chart 3Ebbing Energy Inflation

Fallout From Ukraine

Fallout From Ukraine

Oil markets are set to peak soon. The run-up in Brent prices in recent weeks was largely driven by geopolitical concerns. With the odds of an oil embargo declining, the pressure on Brent will also recede. Bob Ryan, BCA’s commodity and energy strategist, believes that Saudi Arabia, the UAE, and Kuwait will increase their own production in coming weeks to burnish their credentials as reliable oil producers, especially if oil experiences more turmoil. Bob expects crude prices to drop to $85/bbl by the second half of 2022. These dynamics are important because they imply that European headline inflation will soon peak. Yes, the recent spike in natural gas prices will keep energy inflation higher for a few more months, but, ultimately, ebbing base effects will bring down energy CPI. As Chart 3 highlights, even if Brent and natural gas prices stay at today’s levels for the remainder of the year, their year-on-year inflation rates will collapse, which will drive HICP lower. Near-Term Market Dynamics In this context, what to do with European assets? It is probably still too early to abandon our hedges, but we will likely do so next week or soon after. While the market has probably bottomed, prudence remains of prime consideration as a war is taking place and the situation on the ground may deteriorate. Chart 4A Buying Opportunity

Fallout From Ukraine

Fallout From Ukraine

The clearest near-term investment implication comes for European peripheral bonds. Italian spreads have widened significantly in the wake of the hawkish pivot by the ECB (Chart 4). However, we argued that, when interest rate expectations priced in 50bps of the hike for 2022, the move was excessive and that only one ECB hike in the fourth quarter was likely this year. Now that the Ukrainian crisis is reaching a climax, even some of the ECB’s most hawkish members, such as Robert Holzmann, Governor of the Austrian National Bank, indicate that the removal of liquidity will be slower than originally anticipated. This means that the ECB is likely to continue to backstop the European peripheral bond markets. Italian and Greek bonds, which offer spreads of 165bps and 249bps over German bunds, are appealing in light of this explicit backstop. European financials are another attractive buy. Investors should buy banks outright. As Chart 5 highlights, all the major Eurozone countries’ banking stocks have suffered widespread selloffs. However, the exposure to Russian debt is limited at $67 billion (Chart 6). Additionally, the European yield curve slope is unlikely to flatten significantly from here. The ECB will limit the upside in the German 2-year yields by not hiking until Q4 2022, while the terminal rate proxy in Europe has significant upside from here. A steeper yield curve will boost the appeal of banks, especially in a context in which peripheral spreads are likely to narrow. Chart 5Too Much Of A Dive

Fallout From Ukraine

Fallout From Ukraine

Chart 6Limited Russian Exposure

Fallout From Ukraine

Fallout From Ukraine

The outlook for the euro is more complex. Narrower peripheral spreads would boost the euro’s appeal, a cheap currency currently trading at a 17% discount to its PPP fair value. EUR/USD also trades at a 5% discount to the BCA Intermediate-Term Timing Model, which suggests that considerable bad news is already embedded in the exchange rate (Chart 7). The fact that the EUR/USD did not close below its January 27th low in the face of a major war on European soil adds to the notion that the euro already embeds a significant risk premium. However, there are still ample reasons to worry about additional volatility in the coming week or so. The ECB is sounding less hawkish, while the Fed is not changing its tone. Meanwhile, 1-month and 3-month risk reversals are not at levels consistent with a bearish capitulation, which suggests that the euro could suffer one last wave of liquidation (Chart 8). Thus, we are not buying the euro yet and are willing to forego the first few cents of gains for a clearer signal. Chart 7EUR/USD Is Cheap

Fallout From Ukraine

Fallout From Ukraine

Chart 8Sentiment Could Get More Negative

Fallout From Ukraine

Fallout From Ukraine

Circling back to the equity front, European equities had become very oversold after the 14-day RSI fell below 30. The diminishing risk of an energy crisis will also help. However, global equities face more risks than just Ukraine. As we wrote earlier this week, the transition away from consumer durable goods as the driver of global growth to services will involve some adjustments for stocks, especially in an environment in which the Fed is allowing global monetary conditions to deteriorate (Chart 9). Thus, the window of volatility in stocks is unlikely to close in the near term. The relative performance of European equities vis-a-vis the US is complex as well. European equities have undone most of the relative gains accrued so far in 2022 (Chart 10). On the one hand, the global growth transition will hurt European equities more than US ones, as a result of their greater exposure to manufacturing activity. Additionally, high energy costs are more of a problem for Europe right now than the US. On the other hand, the continued hawkishness of the Fed is likely to limit the ability of tech stocks to extend the rebound that began last Thursday. As a result, the most likely pattern is for some churning in the relative performance of Europe and the US in the coming week. Chart 10Vanishing Outperformance

Fallout From Ukraine

Fallout From Ukraine

Chart 9Tightening US Liquidity Conditions

Fallout From Ukraine

Fallout From Ukraine

For the remainder of the year, we expect the European equity outperformance to re-establish itself in view of the favorable relative profits picture for 2022, a topic that we will explore more deeply in the coming weeks. Bottom Line: The near-term outlook for European assets remains extremely murky. Not only is a war in Ukraine a major threat that can hurt sentiment further, but European assets still have to handle the short-term implications of a change in global growth leadership away from goods consumption. Nonetheless, the dovish message of the ECB in the wake of the Ukrainian invasion suggests that the collapse in Italian bonds and European banks in recent weeks is overdone. European stocks will likely continue to churn against US stocks in the near term but outperform for the remainder of the year. The sell-off in the euro is advanced, but prudence prevents us from buying EUR/USD today. Keep short EUR/CHF and short EUR/JPY hedges in place for now. Longer-Term Implications The crisis in Ukraine heightens Europe’s need to diversify its energy sourcing away from Russia. However, this is not a transition that can be executed on a dime. It will take years. For now, Europe remains dependent on Russian energy, which greatly limits the EU’s options. However, time offers many more possibilities. First, kicking Russia out of SWIFT will become feasible, because it will increase the robustness of the SPFS payment system, allowing Russia to receive funds for its energy, even if it is out of SWIFT. Second, and most importantly, time will allow Europe to find new energy sources. For example, Qatari LNG is often mentioned as a potential replacement for Russian natural gas. Qatar currently does not have the capacity to service Europe extensively, while fulfilling its previous contractual obligations, but the expansion of the production in its North Field East will increase capacity to 126MTPA by 2027. The LNG export capacity of the US may also increase over the coming years. Even if Qatar and the US could send enough LNG to satisfy the hole left by Russia tomorrow, Europe would not be able to accept delivery, as it does not have enough terminals to accommodate these shipments. Thus, investments in that sector will expand. Chart 11The Renewables Envelope Will Expand

Fallout From Ukraine

Fallout From Ukraine

Chart 12Nuclear Skepticism Remains

Fallout From Ukraine

Fallout From Ukraine

Most importantly, Europe will accelerate its transition toward renewable energy. Renewables are already a major focus of the NGEU program (Chart 11). However, we expect that, for the remainder of the decade, the NGEU program will be enlarged to allow greater investments in that space. Not only does it fit European green goals, but this policy would also increase the region energy security. More investment in nuclear electricity production is also possible but lacks popular support (Chart 12). The main message of these observations is that European infrastructure spending is likely to remain elevated in the coming years. As a result, industrial stocks may face some near-term headwinds as the global economy transitions away from the consumer goods-buying binge of COVID-19, but they will ultimately benefit greatly from an expansion of the capital stock around the world. Another long-term theme derived from the current crisis is that European defense stocks will fare well on a structural basis. The current crisis will force greater European unity. The presence of a common enemy will incentivize European nations to increase military spending, especially as the US continues to pivot toward Asia. Investors should overweight these stocks. In terms of bond market developments, more military spending and investment in energy infrastructures means that European budget deficits will be wider than if the Ukrainian crisis had not emerged. More accommodative fiscal policy will support aggregate demand, which will feed through greater capex (Chart 13). Thus, the experience of the last decade, whereby aggregate demand was curtailed by unnecessarily stringent European fiscal policy, will not be repeated. This confirms our expectation that the neutral rate of interest will rise in Europe and that Europe will escape an environment of zero rates (Chart 14). Therefore, German bunds yields have upside, the yield curve can steepen, and the outlook for European financials is positive on a long-term basis, not just on a near-term one. Chart 13Stronger Capex Than Last Decade...

Fallout From Ukraine

Fallout From Ukraine

Chart 14...Means Higher Yields And A steeper Curve

Fallout From Ukraine

Fallout From Ukraine

Chart 15Ebbing Fixed-Income Outflows?

Fallout From Ukraine

Fallout From Ukraine

Finally, the picture for the euro is murky. On the one hand, its inexpensiveness is a major advantage while a higher neutral rate of interest will limit the European fixed-income outflows that have plagues the Euro for the past decade (Chart 15). However, if we are correct that European capex will increase and that budget deficits will remain wider than in the last decade, this also means that the European current account surplus will narrow as excess savings recede. This implies that one of the key underpinnings of the euro will dissipate. In the end, productivity will be the long-term arbiter of the exchange rate. Europe still lags behind the US on this front, which augurs poorly for the performance of the euro (Chart 16). Reforms and capex may save the day, but it is too early to make this call. Chart 16The Productivity Handicap

Fallout From Ukraine

Fallout From Ukraine

Bottom Line: The events in Ukraine portend a structural shift in European capex. Europe will need to ween itself off its Russian energy dependency, which will require major investments in LNG facilities and renewable power. Moreover, European defense spending will rise. These will continue to support fiscal and infrastructure spending. As a result, industrials will benefit from a structural tailwind, as will European defense stocks. These same forces will put upward pressure on European risk-free yields, which will benefit beleaguered European financials and banks. The long-term outlook for the euro is murkier. More research must be conducted before making a definitive directional bet. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Tactical Recommendations Cyclical Recommendations Structural Recommendations

Highlights The Russian invasion of Ukraine is a geopolitical incident that is likely to be limited in scope. A wholesale energy cutoff to Europe is the chief risk to global economic activity, but the sanction response from the US and EU does not point to this outcome. This implies that a large geopolitical risk premium may linger over the very near term, but that equities and other risk assets will ultimately recover. We continue to expect above-trend growth and above-target inflation in the US and other developed economies this year. Q1 growth in the US is likely to be closer to 4% after removing the effect of changing inventories, and incoming information still points to the view that the pandemic will continue to recede in importance over the coming several months. Given the magnitude of the rise in consumer prices in the US and other developed economies, above-trend growth also underpins the significantly hawkish monetary policy shift that has recently occurred. There are legitimate arguments in favor of a very aggressive pace of Fed tightening. Still, our view is that seven rate hikes from the Fed over the coming 12 months is likely too aggressive: A peak in headline inflation over the coming months will help restrain longer-term household inflation expectations, the surge in wage growth continues to reflect pandemic-driven labor market distortions that could unwind, and a significant further flattening of the yield curve – despite likely being a false signal of a recession – would probably cause a temporary period of tighter financial conditions that the Fed would respond to. We believe it is likely that the Fed will initially seek to raise interest rates at a pace that is in line with current market pricing, but that it will likely slow the pace at some point beyond the next 3-4 months. As such, we expect that the Fed will ultimately end up raising interest rates 5 or 6 times over the coming year, less than investors currently expect. The case for aggressive ECB hikes was weak even before Russia’s invasion of Ukraine. European core inflation is nowhere near as strong as it is in the US, and nominal output in the euro area has not yet recovered to its pre-pandemic trend (in heavy contrast to the US). Russia’s invasion has caused a disruption of natural gas flows that will keep European gas prices at elevated levels, and aggressive tightening in response risks repeating the mistakes the ECB made in 2008 and 2011 when it raised rates in the face of an ultimately deflationary supply shock. On a 6-12 month time horizon, we are only likely to recommend downgrading global stocks once 5-year/5-year forward US Treasury yields break above 2.5%, barring a more severe shock to global economic activity from the Ukrainian crisis than currently appears likely. On Russia’s Invasion Of Ukraine Yesterday, BCA Research published a Special Alert in response to Russia’s invasion of Ukraine.1 In the report, we outlined Russia’s motivation for invading, and noted that it will not withdraw troops until it has changed the government and seized key territories – such as coastal regions to ensure the long-term ability to blockade the country. Crucially, we noted that while the US and EU will levy sweeping sanctions against Russia, that the EU would not halt Russian energy exports. We regard the decision to maintain Russia’s access to the SWIFT system as consistent with that view. Given this, we believe that the Russian invasion of Ukraine is a geopolitical incident that is likely to be limited in scope. A wholesale energy cutoff to Europe is the chief risk to global economic activity, but the sanction response from the US and EU does not point to this outcome. This implies that a large geopolitical risk premium may linger over the very near term, but that growth, inflation, and monetary policy will ultimately return as the drivers of equities and other risk assets over the coming weeks and months. Beyond Ukraine: Growth, Inflation, And Monetary Policy In The DM World Chart I-1Recent US Data Has Looked Smoewhat Stagflationary

Recent US Data Has Looked Smoewhat Stagflationary

Recent US Data Has Looked Smoewhat Stagflationary

BCA Research presented three possible growth and inflation scenarios for this year in our 2022 Annual Outlook report. Our base case scenario, to which we assigned 60% odds, was one of above-trend growth and above-target inflation. We assigned 30% odds to a “stagflation-lite” scenario of above-target inflation with below-trend growth, and a 10% chance of a recession. Since we published our Annual Outlook, we raised the odds of the second, stagflation-lite scenario – mostly due to the impact that the Omicron variant of COVID-19 could have on the Chinese supply chain. But until recently, US economic data was also looking somewhat stagflationary: US real GDP only grew at a 2.3% annualized basis in Q3, and the strong Q4 number was mostly boosted by inventories. Real goods spending has slowed over the past few months without a major increase in services spending, and US auto production continues to be restrained by semiconductor shortages (Chart I-1). Supply-side constraints on production and spending have occurred against the backdrop of a significant acceleration in US consumer prices, the combination of which seemingly points more to the second growth and inflation scenario that we outlined, rather than our base case. However, our view is that above-trend growth in the US and other developed economies remains the most likely outcome this year, even given ongoing supply-side constraints and Russia’s invasion of Ukraine. In addition to the sizeable amount of excess savings that have been accumulated during the pandemic and the enormous increase in household net worth that has occurred over the past two years, two other factors point to above-trend DM growth. In the US, following the release of the January retail sales report, the Atlanta Fed GDPNow model is forecasting below-trend growth for Q1, but with a -2.3% contribution from the change in private inventories. Chart I-2 highlights that the Atlanta Fed’s model is projecting 3.6% annualized growth in Q1 of final sales of domestic product, a measure of GDP that excludes the effect of changing inventories (whose contribution to growth averages to zero over time). This would be above the trend rate of real GDP growth, and would represent an acceleration relative to the past few quarters. Beyond the next few months, the other factor pointing to above-trend growth is the indication that the pandemic will indeed continue to recede in importance over the course of the year, in line with what we laid out in our Annual Outlook. Chart I-3 highlights that the Omicron-driven surge in hospitalizations in G7 countries has been short-lived, and Chart I-4 highlights that deliveries of Pfizer’s anti-viral treatment Paxlovid, while still in their early stages, have begun. Chart I-2Q1 US Economic Growth Likely To Be Above-Trend

Q1 US Economic Growth Likely To Be Above-Trend

Q1 US Economic Growth Likely To Be Above-Trend

Chart I-3Hospitalizations Are Falling Sharply

Hospitalizations Are Falling Sharply

Hospitalizations Are Falling Sharply

In a recent study, Paxlovid was found to have an 89% efficacy in preventing COVID hospitalizations and deaths, with less serious adverse events or discontinuations than the placebo group.2 Its high effectiveness against all SARS-CoV-2 variants suggests that its increased deployment over the course of the year should significantly reduce the impact of COVID-19 on the medical system as well as lower the fear of the disease amongst consumers, even as new variants of the virus emerge and spread around the world. Consequently, it is likely that the output gap in advanced economies will turn positive this year despite ongoing supply-side constraints unless Russian energy exports to the EU are ceased, triggered either by a European boycott or a Russian embargo. Prior to Russia’s invasion, consensus growth expectations implied above-trend growth for this year (Chart I-5), which we see as consistent with the base case growth and inflation view that we presented in our Annual Outlook if Russian energy exports continue. However, given the magnitude of the rise in consumer prices in the US and other developed economies, above-trend growth also underpins the significantly hawkish monetary policy shift that has occurred over the past 2 months. Chart I-5We Agree With Consensus Expectations For Growth This Year

We Agree With Consensus Expectations For Growth This Year

We Agree With Consensus Expectations For Growth This Year

Chart I-4US Paxlovid Deliveries Are Creeping Higher

US Paxlovid Deliveries Are Creeping Higher

US Paxlovid Deliveries Are Creeping Higher

The Case For, And Against, Aggressive Fed Tightening Just since the beginning of the year, investors have moved to price in an additional 100 basis points of rate hikes from the Fed (Chart I-6). Earlier this month, comments by St. Louis Fed President James Bullard signaling his desire for a full percentage point of interest rate hikes by July had a sizeable effect on US Treasury yields, with market participants still pricing in meaningful odds of a 50 basis point rate hike in March despite recent pushback from key Fed officials and Russia’s invasion of Ukraine. Chart I-6The Monetary Policy Outlook Has Shifted Rapidly In A Hawkish Direction

The Monetary Policy Outlook Has Shifted Rapidly In A Hawkish Direction

The Monetary Policy Outlook Has Shifted Rapidly In A Hawkish Direction

Last year, The Bank Credit Analyst service warned on several occasions that a return to maximum employment was likely to occur faster than investors expected, and that a hawkish shift from the Fed was probable. We noted in our July report that the cumulative odds of a rate hike by some point in Q2 2022 were close to 40%,3 and in our September Special Report we reinforced the view that a mid-2022 rate hike was likely.4 Still, even relative to our (then) comparatively hawkish expectations, the monetary policy outlook has shifted very aggressively towards more and earlier rate hikes. This shift has partially occurred due to the labor market dynamics that we projected last year, but also due to a significant broadening of inflation over the past four months. Chart I-7 highlights that the 6-month rate of change in US core CPI excluding cars and COVID-impacted services was not meaningfully different in October than it was in the latter half of late-2019, in heavy contrast to overall headline and core inflation. However, over the past four months this measure has accelerated by 175 basis points, highlighting that inflationary pressures are becoming broader – and that an earlier and more forceful response from the Fed may be warranted. Chart I-7US Inflation Has Broadened, And Quickly So

US Inflation Has Broadened, And Quickly So

US Inflation Has Broadened, And Quickly So

Does the broadening in US inflationary pressure that has occurred over the past few months justify the seven rate hikes currently expected by investors over the coming year? We present the detailed case for and against that view below, and conclude that seven rate hikes over the coming 12 months is likely too aggressive. The Case For Aggressive Tightening The most prominent argument in favor of aggressive Fed rate hikes is not just to slow the pace of inflation, but to address the fact that broadening inflationary pressures risk unanchoring inflation expectations. As we discussed in our January 2021 Special Report,5 inflation is determined not just by the output gap, but as well by inflation expectations. Economic slack, changes in imported goods prices, and idiosyncratic shocks all cause core inflation to cyclically fluctuate, but those fluctuations are relative to a level that is determined by inflation expectations – not the Fed’s inflation target. It is only if inflation expectations are consistent with the Fed’s target that actual inflation will equal that target, abstracting from the business cycle and other distorting events. A deeply negative output gap for several years following the global financial crisis caused inflation expectations to be vulnerable to shocks, and the collapse in oil prices in 2014 served as a large enough surprise that expectations unanchored to the downside. This event ultimately motivated the Fed’s introduction of its average inflation targeting policy, but Chart I-8 highlights that inflation expectations are no longer chronically low and that they may unanchor to the upside without meaningfully tighter monetary policy. A temporary period of higher food prices stemming from Russia’s invasion of Ukraine also raises the risk of unanchored inflation expectations among households. The second argument in favor of aggressive Fed rate hikes is that the unemployment rate has essentially fallen back to its pre-pandemic level, and median wage growth has already risen to its strongest level in 20 years (Chart I-9). Given that a large amount of excess savings and a very significant wealth effect are likely to continue to support aggregate demand, the inference is that overall wage growth may accelerate significantly further as the unemployment rate continues to fall. Chart I-8Inflation Expectations Are No Longer Depressed

Inflation Expectations Are No Longer Depressed

Inflation Expectations Are No Longer Depressed

Chart I-9Wage Growth Has Risen Very Significantly

Wage Growth Has Risen Very Significantly

Wage Growth Has Risen Very Significantly

The third argument in favor of rapid tightening is that the natural/neutral rate of interest is likely higher than both investors and the Federal reserve believe, meaning that monetary policy is even easier today than is generally recognized. We have written about this issue at length: in March 2020 we explained why the most cited measure of “R-star” was wrong,6 and noted in our April 2021 Special Report why we no longer believe that a gap between interest rates and trend rates of economic growth are justified. This perspective also suggests that investors should look past the quasi-recessionary signal currently being flagged by the 2/10 yield curve, as curve inversion is likely to be a false signal of a recession – as it was in 2019 (see Box I-1). BOX I-1 The Sino-US Trade War, The Yield Curve, And The COVID-19 Pandemic The US yield curve has historically provided a highly reliable signal of the likelihood of a recession. Investors have taken an inverted yield curve as a sign that short-term interest rates have risen to a level that is not likely to be sustained over the longer term, meaning that monetary policy has become tight. An inverted yield curve has indeed preceded several US recessions, although its track record at predicting contractions globally has been less reliable. While it is a counterfactual assertion, we believe that the yield curve provided a false signal when it inverted in 2019. Clearly the inversion did not predict the COVID-19 pandemic; the question is whether the US would have experienced a recession had the pandemic not occurred. In our view, the evidence does not point to that conclusion. Charts I-B1 and I-B2 highlight that the yield curve responded to an economic slowdown that was mostly caused by the Sino-US trade war, as well as an ongoing slowdown in Chinese credit growth and economic activity. It does not appear to have occurred due to interest rates having risen to a level that would be unsustainable absent these non-monetary shocks. Chart I-B1The Yield Curve Inverted Well After The Trade War Hit…

March 2022

March 2022

Chart I-B2…And The Economy Started Improving After The Inversion

March 2022

March 2022

In addition, the signal from the yield curve lagged that of the equity market: Chart I-B1 highlights that the US equity market fell just shy of 20% eleven months before the yield curve inverted. In fact, stock prices were rising sharply just prior to the emergence of the pandemic in response to expectations of monetary easing and the Phase I US trade deal, and the US Markit manufacturing and services PMIs were also turning up. None of these signs point to the likelihood of a contraction in US output had the COVID-19 pandemic not emerged. The key point for investors is that an inversion of the yield curve, were it to occur over the coming 12-18 months, would not necessarily signal a recession unless it were coupled with a major non-monetary shock. It would, however, be significant from a strategy standpoint, as the Fed would likely take it as a sign of tightening financial conditions. The Case Against Aggressive Fed Action Chart I-10Inflation Expectations Have Risen, But Are Not Out Of Control

Inflation Expectations Have Risen, But Are Not Out Of Control

Inflation Expectations Have Risen, But Are Not Out Of Control

There are several counterpoints to the arguments noted above, as well as a few additional reasons to suggest that 7 rate hikes over the coming year is too aggressive. First, on the issue of inflation expectations, while it is true that expectations are no longer chronically low, longer-term expectations have not yet exceeded their pre-global financial crisis (GFC) range (Chart I-10). In addition, despite the temporary spike in energy and food prices stemming from Russia’s invasion of Ukraine, headline inflation is likely to peak at some point over the coming months, which will act to restrain longer-term household inflation expectations. Importantly, inflation is likely to peak even without any Fed tightening. A comparison of the recent pace of advance in both headline and core CPI suggests that the former has up to 200 basis points of downside if crude oil prices remain at $100/bbl. Our Commodity & Energy Strategy team expects that Russia’s invasion of Ukraine will prompt increased production from core OPEC producers to reduce the elevated risk premium and allow refiners to boost inventories. We now expect Brent oil to average $85/bbl in the second half of 2022, implying eventual deflation from energy prices and a slowdown in the pace of advance in headline CPI over the coming months – potentially below that of core. That would represent a very significant easing in headline inflation relative to current levels, and we do not expect that long-term household expectations for inflation would rise much further in such a scenario. The easing in the prices paid component of the ISM manufacturing index also points to an imminent peak in headline inflation and, by extension, household inflation expectations (Chart I-11). Second, while it is true that overall wage growth has recently accelerated quite significantly, it is still the case that this is being driven by the lowest-paid workers. Chart I-12 highlights that 1st and 2nd quartile wage growth are between 0.4-1.2% higher than they were prior to the pandemic, but that 3rd and 4th quartile wage growth is either the same or lower. Chart I-12Lower-Pay Wage Inflation Is Due To The Pandemic...

Lower-Pay Wage Inflation Is Due To The Pandemic...

Lower-Pay Wage Inflation Is Due To The Pandemic...

Chart I-11The Prices Paid Components Of Manufacturing PMIs Also Points To Lower Headline Inflation

The Prices Paid Components Of Manufacturing PMIs Also Points To Lower Headline Inflation

The Prices Paid Components Of Manufacturing PMIs Also Points To Lower Headline Inflation

This surge in wages for low-paid workers largely reflects pandemic-driven labor market distortions, rather than excess demand. Chart I-13 highlights that real US services spending remains close to 5% below its pre-pandemic trend, and Table I-1 highlights that the leisure & hospitality industry now accounts for the vast majority of the jobs gap relative to pre-pandemic levels. Chart I-14 also highlights that while the leisure & hospitality jobs gap is smaller in red states than in blue states (which may be disproportionately affected by lost services jobs in central business districts due to work-from-home policies), it is still larger today that it was during the depths of the 2008/2009 recession. Chart I-13...Not Excessive Services Demand

...Not Excessive Services Demand

...Not Excessive Services Demand

The key takeaway from Table I-1 and Charts I-13 and I-14 is that rising 1st and 2nd quartile wage growth is being caused by labor scarcity in low paying industries, which we attribute to the fact that working conditions in these jobs became more difficult during the pandemic and the fact that many of these positions involve close contact with customers. And clearly, raising interest rates will not hasten the return of leisure & hospitality workers to the labor market. Table I-1Leisure & Hospitality And Education Now Make Up Almost All Of The US Jobs Gap

March 2022

March 2022

Chart I-14The Leisure & Hospitality Employment Gap Does Not Seem Related To Work-From-Home Trends

The Leisure & Hospitality Employment Gap Does Not Seem Related To Work-From-Home Trends

The Leisure & Hospitality Employment Gap Does Not Seem Related To Work-From-Home Trends

Third, even though we think the natural/neutral rate of interest is higher than both investors and the Federal reserve believe and that the yield curve provided a false signal of a recession in 2019, a significant further flattening of the yield curve would probably cause a tightening in financial conditions, at least for a time. The Fed is unlikely to be dissuaded from raising rates due to a valuation-driven decline in equity prices, but it is likely to respond to market-based signals of a material slowdown in economic activity – even if those signals ultimately prove to be false. The yield curve is an important reflection of how far bond investors believe the economic cycle has progressed (Chart I-15), and an increase in short-term interest rates at the pace that investors are currently expecting would flatten the 2/10 yield curve very close to (or into) negative territory. It seems likely that a rapid flattening in the curve would precipitate a growth scare in financial markets for a time, leading to falling equity prices (due to concerns about earnings, not just valuation), a rising US dollar, and a widening in corporate credit spreads. Chart I-15For The Fed, The Yield Curve Is An Important Market Indicator Of A Recession

For The Fed, The Yield Curve Is An Important Market Indicator Of A Recession

For The Fed, The Yield Curve Is An Important Market Indicator Of A Recession

To conclude on this point, the Fed will feel that it is justified in hiking rates aggressively while inflation is well above its target levels and the unemployment rate is low and falling, but it is likely to change this assessment if financial markets begin to behave in a way that signals a rising risk of a significant slowdown in jobs growth. That would lead to a tactical period of weakness for risky asset prices, but it would ultimately be cyclically positive if the Fed revises its pace of tightening to a rate that is slower than investors currently expect. Our View Netting out the arguments presented above, the Fed may initially seek to raise interest rates at a pace that is in line with current market pricing, but it will likely slow that pace at some point beyond the next 3-4 months. As such, we expect that the Fed will ultimately end up raising interest rates 5 or 6 times over the coming year, less than investors currently expect. Our view also has important implications for the euro area interest rate outlook, given the significantly weaker case for aggressive ECB action that existed even before Russia’s invasion of Ukraine. A Flimsy Case For Aggressive ECB Rate Hikes, Even Before Russia’s Invasion Chart I-16The European Inflation Situation Is Not As Bad As In The US

The European Inflation Situation Is Not As Bad As In The US

The European Inflation Situation Is Not As Bad As In The US

At the early-February ECB meeting, President Christine Lagarde signaled a more hawkish outlook for euro area monetary policy than investors had been expecting. Since the beginning of the year, the OIS market has moved to price-in roughly 70 bps of hikes over the coming 12 months, German 2-year bund yields have risen 20 basis points, and 10-year yields have risen back into positive territory. Italian and Greek 10-year yield spreads (relative to Bunds) have risen by 35 and 90 basis points, respectively. From our perspective, investors are pricing a too-aggressive path for the ECB policy rate, and we would probably characterize an ECB decision to raise rates in line with current market expectations as a policy mistake. As highlighted in a recent report by my colleague Mathieu Savary, BCA’s Chief European Strategist, several arguments support this view. First, Chart I-16 highlights that euro area core inflation is running at a considerably slower rate than headline inflation or core inflation in the US, and that our core inflation diffusion index for the euro area has peaked. It is true that core inflation is much higher in Germany than in other key euro area economies, and it is also true that aggregate euro area core inflation is above the ECB’s 2% target. But high German core inflation is seemingly driven by particularly acute passthrough effects from high natural gas prices, and recent IMF research underscores that over half of the increase in German manufacturing price inflation has occurred due to supply shocks rather than demand (Chart I-17). Chart I-18 shows that expectations for euro area inflation and actual wage growth do not, in any way, suggest that the ECB’s 2% target is under threat, underscoring that aggressive tightening over the coming several months risks repeating the mistakes the ECB made in 2008 and 2011 when it tightened policy in the face of an ultimately deflationary supply shock. Chart I-17German Core Inflation Is Being Disproportionately Driven By Supply Shocks

March 2022

March 2022

The second argument is that nominal output in the euro area has not yet recovered to its pre-pandemic trend, in heavy contrast to the US (Chart I-19). This is particularly true for Italy and Spain, and reflects the nature of the euro area fiscal response to the COVID-19 pandemic. Chart I-20 highlights that the cumulative growth in euro area disposable income has been lower than what would have been expected absent the pandemic, unlike what occurred in the US and Canada – two countries that provided sizeable direct transfers to households as part of their fiscal response. Chart I-19Key Euro Area Economies Have Recovered Far Less Than The US Has

Key Euro Area Economies Have Recovered Far Less Than The US Has

Key Euro Area Economies Have Recovered Far Less Than The US Has

Chart I-18Euro Area Inflation Expectations And Wage Growth Do Not Signal The ECB's Inflation Target Is Under Threat

Euro Area Inflation Expectations And Wage Growth Do Not Signal The ECB's Inflation Target Is Under Threat

Euro Area Inflation Expectations And Wage Growth Do Not Signal The ECB's Inflation Target Is Under Threat

Third, Russia’s invasion has caused a disruption of natural gas flows via Ukraine that will keep European gas prices at elevated levels even beyond the winter period, which will have a negative impact on the euro area economy. Chart I-21 highlights that European natural gas prices are now seven times as high as they were at the beginning of 2021. Unlike the prior rise in European natural gas prices, which was somewhat related to global demand for goods, the post-invasion surge is a pure supply shock – echoing our point about the ECB’s previous policy mistakes. Chart I-20Euro Area Disposable Income Is Lower Than Its Pre-Pandemic Trend, In Contrast To The US

March 2022

March 2022

Chart I-21Russia's Invasion of Ukraine Has Created A Pure Natural Gas Supply Shock

Russia's Invasion of Ukraine Has Created A Pure Natural Gas Supply Shock

Russia's Invasion of Ukraine Has Created A Pure Natural Gas Supply Shock

The fact that Italy’s nominal economic recovery has been comparatively weak has helped explain the rise in its 10-year government bond yield relative to 10-year German Bunds. Allowing for a further economic recovery in those countries before raising rates would let the ECB ultimately increase rates further down the road – and thus exit more cleanly from negative policy rates in Europe. Our European Strategy Team continues to expect that the ECB is on track to raise interest rates only once in Q4 2022, to be then followed by more aggressive hikes in 2023. Investment Conclusions For fixed-income investors, the investment implications of policy rates moving higher over the coming year at a pace that is less rapid than currently expected would normally imply that an at or above-benchmark duration stance is warranted. However, Chart I-22 highlights that there is still upside for 10-year US Treasury yields even in a scenario where the Fed raises rates at a pace of 100 basis points per year. As such, we continue to recommend that investors remain short duration on a 6-12 month time horizon, although we agree with BCA’s fixed-income team’s recommendation to tactically raise duration to neutral given the potential for the European energy crisis to worsen further and the fact that 10-year US Treasury yields do not have as much upside on a cyclical basis as they did when we published our Annual Outlook.7 For equities, we do not find the case for a tactical downgrade to be compelling at current levels, given that global stocks have already fallen 10% from their mid-November highs. Over the near term, we expect the continued underperformance of euro area equities, be we doubt that the negative economic impact of higher natural gas and oil prices would persist beyond a 0-3 month time horizon. On a 6-12 month time horizon, our expectation that monetary policy will tighten at a less aggressive pace than investors expect suggests that the earnings risk to global stocks is not substantial, underscoring that a meaningful contraction in equity multiples would likely be required for stocks to register negative 12-month returns from current levels. In the US, business surveys suggest that sales growth is set to slow to a still-healthy level, and that profit margins are likely to be flat over the coming year (Chart I-23). This is in line with the view that we presented in our Annual Outlook, namely that US earnings growth in 2022 would be driven mainly by top-line growth. Chart I-22Investors Should Still Be Cyclically Short Duration

Investors Should Still Be Cyclically Short Duration

Investors Should Still Be Cyclically Short Duration

Chart I-23Surveys Imply Strong Revenue Growth And Flat Margins, And Thus Positive Earnings Growth

Surveys Imply Strong Revenue Growth And Flat Margins, And Thus Positive Earnings Growth

Surveys Imply Strong Revenue Growth And Flat Margins, And Thus Positive Earnings Growth

Chart I-24Still No Sign That The Secular Stagnation Narrative Is Under Attach. That Is Good For Stocks.

Still No Sign That The Secular Stagnation Narrative Is Under Attach. That Is Good For Stocks.

Still No Sign That The Secular Stagnation Narrative Is Under Attach. That Is Good For Stocks.

Similarly, the risk of a serious interest rate-driven contraction in equity multiples over the coming year does not appear to be elevated. Investors are far more inclined to use long-maturity bond yields to discount future cash flows than short-term interest rates, and we have noted that the rise in long-maturity bond yields is necessarily self-limiting unless investor expectations about the natural/neutral rate of interest change. Chart I-24 highlights that despite an extremely rapid shift in monetary policy outlook amid the highest US headline inflation in 40 years, 5-year/5-year forward US Treasury yields remain only fractionally above 2%. This underscores that fixed-income investors will need to see evidence that a progressively higher Fed funds rate is not disrupting economic activity before they are likely to abandon the secular stagnation narrative. While the equity risk premium will remain elevated over the near term due to the situation in Ukraine, the bond market’s continued belief in secular stagnation will likely support equity multiples – at least for the remainder of the year. As such, we recommend that investors position in favor of the following over the coming 6-12 months: Overweight equities versus long-maturity government bonds Overweight value versus growth stocks Short duration within a fixed-income portfolio, with a neutral tactical overlay Overweight speculative-grade corporate bonds with a credit portfolio Overweight non-resource cyclicals versus defensives and small caps versus large Short the US dollar versus major currencies Jonathan LaBerge, CFA Vice President The Bank Credit Analyst February 25, 2022 Next Report: March 31, 2022 II. Canada: How High Can Rates Rise? The buildup of excessive household debt in Canada over the past two decades has occurred because of outsized demand for housing, not because of the impact of constrained housing supply on house prices. Outsized demand for housing has occurred because interest rates have been persistently too low, pointing to the need for the Bank of Canada to tighten monetary policy in order to prevent even further leveraging. The burden of Canada’s household sector debt may exceed its pre-pandemic level next year given current market expectations for the path of rate hikes. This implies that the prior peak in the Canadian policy rate (1.75%) likely reflects a high-end estimate of the neutral rate of interest in Canada. Regulatory changes have occurred in recognition of Canada’s extreme levels of household debt. Although a massive decline in Canadian house prices would cause a very severe recession, it would not likely precipitate a Lehman-style collapse of the Canadian financial system. Over the next twelve months, investors should position favorably toward CAD-USD. As the Canadian policy rate approaches our estimate of the neutral rate, a short CAD position and an overweight stance towards long-maturity Canadian bonds versus US Treasurys will likely be warranted. Within a global equity portfolio, exposure to relatively high-yielding Canadian banks should not be reduced until hard evidence of a significant slowdown in the housing market emerges. The outlook for monetary policy in advanced economies has shifted rapidly in a hawkish direction over the past few months. While we believe that the Fed and other central banks will end up raising interest rates this year fewer times than investors currently expect, it is clear that monetary policy will tighten in the DM world over the coming 12-18 months. This has raised the question of how high policy rates may rise before monetary policy begins to restrict economic activity. Some investors have specifically focused this question on countries like Canada, which has a highly indebted household sector and has seen house prices rise at a 7% average annual pace for the past 20 years. In this report, we explore the root cause of Canada’s extreme household debt and argue against the constrained housing supply view. Instead, we conclude that persistently low interest rates have fueled excessive housing demand and that the prior peak in the Canadian policy rate (1.75%) probably reflects a high-end estimate of the neutral rate of interest in Canada – in contrast with that of the US. Finally, we note that the regulatory changes that have occurred in recognition of the risk from excessive household debt suggest that a massive decline in Canadian house prices would not likely precipitate a Lehman-style collapse of the Canadian financial system – it would, however, clearly cause a severe recession. Over the next twelve months, investors should position favorably toward CAD-USD. As the Canadian policy rate approaches our estimate of the neutral rate, a short CAD position and an overweight stance towards long-maturity Canadian bonds versus US Treasurys will likely be warranted. Within a global equity portfolio, exposure to relatively high-yielding Canadian banks should not be reduced until hard evidence of a significant slowdown in the housing market emerges. The Root Cause Of Canada’s Extreme Household Debt Chart II-1Canadian Households Are Massively Indebted

Canadian Households Are Massively Indebted

Canadian Households Are Massively Indebted

Relative to disposable income, Canadian household debt has risen substantially over the past two decades. Chart II-1 highlights that Canada’s household debt to disposable income ratio has risen by 180% since 2000, and is currently over 50 percentage points higher than that in the US, even when nonfinancial noncorporate debt is included in the latter.8 Rising Canadian household indebtedness is a problem that is well known to investors, policymakers, regulators, banks, and consumers themselves. Organizations such as the IMF have repeatedly warned that excess household debt poses a potential economic stability risk. In the years prior to the pandemic, policymakers have responded with a series of macroprudential measures designed to limit speculation and foreign ownership in the housing market and to reduce the incremental risk to the economy posed by new borrowers. When asked why Canadian households have leveraged themselves so significantly over the past 20 years, most market commentators in Canada point to insufficient housing supply as the main driver of excessive house prices. Given normal ongoing demand for housing, they argue, persistent supply-side pressure on housing prices will naturally lead to a rising stock of debt relative to income. According to this narrative, the solution to Canada’s housing crisis is centered squarely on incentives to build more homes. Raising interest rates to cool mortgage demand will simply exacerbate the housing affordability problem, while simultaneously discouraging additional residential investment needed to decrease home prices structurally. Chart II-2The Supply Of Non-Apartment Dwellings Has Indeed Declined Over Time...

The Supply Of Non-Apartment Dwellings Has Indeed Declined Over Time...

The Supply Of Non-Apartment Dwellings Has Indeed Declined Over Time...

We hold a different perspective. We do agree that there are some limitations on the supply side that likely are unduly boosting prices of certain dwelling types. For example, the Greenbelt that surrounds Ontario’s Golden Horseshoe region - a permanently protected area of land - has likely constrained some housing activity, and Chart II-2 highlights that single detached, semi-detached, and row/townhouses have fallen significantly as a share of overall housing completions. Apartments and other dwellings now account for a clear majority of new housing construction in Canada. However, there is a great deal of evidence positioned against the view that supply-side factors are the primary cause of outsized housing inflation and, by extension, a massive increase in Canadian household debt to GDP: Based on real residential investment, the pace of housing construction in Canada has not fallen relative to GDP or the population. Chart II-3 highlights that, compared with the US, residential investment has trended higher over the past 20 years. Based on Canadian housing completion data, Chart II-4 highlights that the number of completions has generally kept pace with half of the change in Canada’s population, a ratio that is easily consistent with two or more people per household. In addition, the chart highlights that the periods when houses were completed at a below-average rate relative to population growth have not been the same as when Canadian household debt has increased relative to disposable income. Chart II-3...But Overall Real Residential Investment Has Kept Pace With Canada's GDP And Population

...But Overall Real Residential Investment Has Kept Pace With Canada's GDP And Population

...But Overall Real Residential Investment Has Kept Pace With Canada's GDP And Population

Chart II-4Housing Supply Has Not Been The Main Driver Of Rising Canadian Indebtedness

Housing Supply Has Not Been The Main Driver Of Rising Canadian Indebtedness

Housing Supply Has Not Been The Main Driver Of Rising Canadian Indebtedness

Chart II-5Prices For All Canadian Property Types Have Surged Over The Past Two Decades

Prices For All Canadian Property Types Have Surged Over The Past Two Decades

Prices For All Canadian Property Types Have Surged Over The Past Two Decades

If the rise in Canadian household indebtedness has been caused by the increasing scarcity of single-detached, semi-detached, and row/townhouses, then we would expect to see a persistent and growing divergence between overall Canadian house prices and those of apartment/condominiums. Chart II-5 highlights that this is not the case: while apartment/condo prices have at times grown at a slower rate than overall home prices over the past 15 years (as in the period from 2011 to 2016), they have also at times grown at a faster rate. The chart clearly highlights that the Canadian housing market is driven by a common factor, and that average house price gains have not been significantly different across property types over time. Similarly, if a scarcity of housing supply was the main driver of rising house prices and household debt, we would not expect to see a significant increase in the homeownership rate. Chart II-6 highlights that the Canadian homeownership rate did rise substantially from the mid-1990s to 2016 (the last available datapoint). While it is not clear what the sustainable or “equilibrium” homeownership rate is, it is notable that the most recent datapoint was not significantly lower than the peak rate reached in the US following that country’s massive housing bubble. Finally, Chart II-7 reiterates a point we made in our June 2021 Special Report: in several economies (including Canada), interest rates have remained well below levels that macroeconomic theory would traditionally consider to be in equilibrium over the past two decades. This has occurred alongside significant household sector leveraging. Chart II-7Too-Low Interest Rates Have Fueled Rising Household Indebtedness In Canada (And Other DM Economies)

Too-Low Interest Rates Have Fueled Rising Household Indebtedness In Canada (And Other DM Economies)

Too-Low Interest Rates Have Fueled Rising Household Indebtedness In Canada (And Other DM Economies)

Chart II-6The Canadian Homeownership Rate Has Risen Significantly, Pointing To Excess Housing Demand

March 2022

March 2022

These factors strongly point to rising household debt levels as being driven by demand-side rather than supply-side factors – demand that has been fueled by persistently low interest rates. How High Can The Bank Of Canada Raise Interest Rates? Over the next 12 months, investors expect the Bank of Canada (BoC) to raise interest rates by 180 basis points, in line with the Fed (Chart II-8). Over the longer term, the BoC believes that interest rates will average between 1.75% and 2.75%. In the US, the 2/10 yield curve has flattened significantly in response to the Fed’s hawkish shift, and neither the explosion in headline consumer price inflation nor the Fed’s about face have significantly raised the market’s longer-term expectations for interest rates (which are even below the Fed’s estimates). In Canada, investors expect essentially the same long-term interest rate outlook, as evidenced by 5-year / 5-year forward government bond yields (Chart II-9). Chart II-8Investors Expect A Similar Magnitude Of Tightening In Canada And The US Over The Next Year...

Investors Expect A Similar Magnitude Of Tightening In Canada And The US Over The Next Year...

Investors Expect A Similar Magnitude Of Tightening In Canada And The US Over The Next Year...

Chart II-9...And A Similar Average Interest Rate Over The Longer Term

...And A Similar Average Interest Rate Over The Longer Term

...And A Similar Average Interest Rate Over The Longer Term

As in the case in the US, the hawkish shift among major central banks has left investors asking how high the BoC can raise interest rates, and what implications that might have for Canadian assets – especially the CAD and long-maturity Canadian government bonds. In our view, the best way for investors to assess the impact of rising interest rates on the private sector – especially a highly indebted one – is to project the impact that an increase in interest rates will have on the debt service ratio (DSR). The burden of servicing debt, rather than the stock of debt relative to income, is the right way to measure the impact of shifting monetary policy because it considers the combined effect of changes in leverage, income, and interest rates. The primary drawback of debt service ratio analysis is that the question of sustainability must be answered empirically. In countries experiencing an ever-rising debt service ratio, it can be difficult for investors to judge where the breaking point will be. Cross-country comparisons may sometimes be helpful in this respect, but Chart II-10 highlights that BIS estimates for household debt service ratios vary widely even among advanced economies. However, in Canada, the 2017-2019 tightening cycle provides a useful framework. As we anticipated in a 2017 Special Report,9 the rise in Canadian interest rates during that period caused the household debt service ratio to exceed the level reached in 2007, which contributed to a collapse in Canadian house price appreciation to its lowest level since the global financial crisis (Chart II-11). The decline in house prices during this period was also caused by the introduction of new macroprudential measures (particularly the introduction of a minimum qualifying rate for mortgages, more commonly referred to as a mortgage “stress test” rule), but the impact of higher interest rates was likely significant. Chart II-11The Last Tightening Cycle In Canada Contributed Significantly To A Major Slowdown In Canadian House Prices

The Last Tightening Cycle In Canada Contributed Significantly To A Major Slowdown In Canadian House Prices

The Last Tightening Cycle In Canada Contributed Significantly To A Major Slowdown In Canadian House Prices

Chart II-10Private Sector Debt Service Ratios Vary Significantly Across DM Countries

Private Sector Debt Service Ratios Vary Significantly Across DM Countries

Private Sector Debt Service Ratios Vary Significantly Across DM Countries

Chart II-11 highlights that the Canadian household debt service ratio collapsed during the pandemic, which seems to suggest that the Bank of Canada has ample room to raise interest rates. However, the decline in the DSR occurred not only because of falling interest rates, but also because of the significant excess savings amassed as a result of the pandemic. As in the US, excess savings in Canada were the result of reduced spending on services and the generation of significant excess income from government transfers (see Chart I-20 from Section 1 of this month’s report). These fiscal transfers will eventually disappear, implying that the Canadian household DSR is artificially low. Chart II-12 shows our estimate of the evolution of the overall Canadian household sector DSR based on the following assumptions: Mortgage rates rise in line with market expectations for the change in the policy rate Government transfers fall back to their pre-pandemic trend Disposable income growth ex-transfers grows in line with consensus expectations for nominal GDP growth The overall debt-to-disposable income ratio, using our estimate for total disposable income, remains flat. The chart highlights that the Canadian household sector DSR may exceed its pre-pandemic level next year, and that a 1.75% policy rate is the threshold at which the DSR will hit a new high. The implication of our projection is that the re-acceleration in household sector debt that has occurred during the pandemic, shown in Chart II-13, will again contribute to a significant slowdown in the Canadian housing market as the BoC begins to raise interest rates as in 2018/2019. It also implies that the prior peak in the Canadian policy rate probably reflects a high-end estimate of the neutral rate of interest in Canada. Chart II-12Market Expectations For The Canadian Policy Rate Imply A Record High Debt Burden

Market Expectations For The Canadian Policy Rate Imply A Record High Debt Burden

Market Expectations For The Canadian Policy Rate Imply A Record High Debt Burden

Chart II-13Canadian Household Loan Growth Has Reaccelerated During The Pandemic

Canadian Household Loan Growth Has Reaccelerated During The Pandemic

Canadian Household Loan Growth Has Reaccelerated During The Pandemic