Equities

BCA Research’s China Investment Strategy service recommends investors with a cyclical investment horizon long MSCI China Value Index /Short MSCI China Growth Index. On a cyclical basis, Chinese investable stocks will not be immune to global market selloffs…

Shares of Facebook’s parent company, Meta Platforms Inc, plummeted 26% on Thursday. The collapse follows Meta’s quarterly report which revealed that daily active users declined by 10 million in Q4. Meta’s woes can partially be blamed on company-specific…

There Is Still Dry Powder!

There Is Still Dry Powder!

2022 has surprised investors with the out-of-the-gate market correction, accompanied by a sharp underperformance of Growth vs. Value as part of repricing of the long-duration assets in the context of the tighter monetary policy. As such, $60 billion more has been allocated towards value than growth mutual funds over the past month – the highest amount since 2002 (top panel). Mean reversion is certainly a risk. A big question is whether there is a significant amount of cash sitting on the sidelines or parked in fixed income mutual funds, waiting to be redeployed into equities? To answer this question, we looked at the net flows into all money markets, retail money fund deposits, and net flows into equities vs. bonds (middle and bottom panels). While YTD’s sharp market correction produced only a small uptick in flows into the money market funds or retail deposits, reallocation from equities into fixed income mutual funds has been running its course throughout 2021. Recently, this trend has started to reverse, with net outflows from equities decelerating. This supports the thesis that market correction was a Growth into Value rotation, without much cash leaving equities. Once a new tighter monetary regime gets priced in, money may flow back into equities from the fixed income mutual funds as There Is (still) No Alternative (TINA) in the environment of rising rates. In addition, it appears that there is plenty of cash sitting in retail money funds that could potentially be redeployed. Bottom Line: It appears that retail investors stayed in equities throughout the correction. However, there is plenty of dry powder sitting on the sidelines in the money market, and bond and income mutual funds, ready to be redeployed into equities, supporting their continued outperformance even in the face of tighter monetary policy.

BCA Research is proud to announce a new feature to help clients get the most out of our research: an Executive Summary cover page on each of the BCA Research Reports. We created these summaries to help you quickly capture the main points of each report through an at-a-glance read of key insights, chart of the day, investment recommendations and a bottom line. For a deeper analysis, you may refer to the full BCA Research Report. In lieu of next week’s report, I will be presenting the quarterly Counterpoint webcast series ‘Where Is The Groupthink Wrong?' I do hope you can join. Executive Summary Spending on goods is in freefall while spending on services is struggling to regain its pre-pandemic trend. If spending on goods crashes to below its previous trend, then there will be a substantial shortfall in demand. The good news is that the freefall in goods spending is leading inflation. With spending on goods now crashing back to earth, inflation will also crash back to earth later this year. Underweight the goods-dominated consumer discretionary sector, and underweight semiconductors versus the broader technology sector. Sell Treasury Inflation Protected Securities (TIPS) and other overbought inflation hedges such as commodities that have not yet corrected. Overbought base metals are particularly vulnerable. Fractal trading watchlist: We focus on nickel versus silver, add tobacco versus cannabis, and update bitcoin, biotech, CAD/SEK, and EUR/CZK. As Spending On Goods Crashes Back To Earth, So Will Inflation

As Spending On Goods Crashes Back To Earth, So Will Inflation

As Spending On Goods Crashes Back To Earth, So Will Inflation

Bottom Line: As spending on goods crashes back to earth, so will inflation, consumer discretionary stocks, semiconductors, and overbought commodities. Feature The pandemic has unleashed a great experiment in our spending behaviour. After a binge on consumer goods, will there be a massive hangover? We are about to find out. The pandemic binge on consumer goods, peaking in the US at a 26 percent overspend, is unprecedented in modern economic history. Hence, we cannot be certain what happens next, but there are three possibilities: We sustain the binge on goods, at least partly. Spending on goods falls back to its pre-pandemic trend. There is a hangover, in which spending on goods crashes to below its previous trend. The answer to this question will have a huge bearing on growth and inflation in 2022-23. After The Binge Comes The Hangover… The pandemic’s constraints on socialising, movement, and in-person contact caused a slump in spending on many services: recreation, hospitality, travel, in-person shopping, and in-person healthcare. Nevertheless, with incomes propped up by massive stimulus, we displaced our spending to items that could be enjoyed within the pandemic’s confines; namely, goods – on which, we binged (Chart I-1). Chart I-1Spending On Goods Is In Freefall

Spending On Goods Is In Freefall

Spending On Goods Is In Freefall

Gradually, we learned to live with SARS-CoV-2, and spending on services bounced back. At the same time, we made some permanent changes to our lifestyles – for example, hybrid office/home working and more online shopping. Additionally, a significant minority of people changed their behaviour, shunning activities that require close contact with strangers – going to the cinema or to amusement parks, using public transport, or going to the dentist or in-person doctors’ appointments. The result is that spending on services is levelling off well short of its pre-pandemic trend (Charts I-2-Chart I-5). Chart I-2Spending On Recreation Services Is Far Below Its Pre-Pandemic Trend

Spending On Recreation Services Is Far Below Its Pre-Pandemic Trend

Spending On Recreation Services Is Far Below Its Pre-Pandemic Trend

Chart I-3Spending On Public Transport Is Far Below Its Pre-Pandemic Trend

Spending On Public Transport Is Far Below Its Pre-Pandemic Trend

Spending On Public Transport Is Far Below Its Pre-Pandemic Trend

Chart I-4Spending On Dental Services Is Far Below Its Pre-Pandemic Trend

Spending On Dental Services Is Far Below Its Pre-Pandemic Trend

Spending On Dental Services Is Far Below Its Pre-Pandemic Trend

Chart I-5Spending On Physician Services Is Far Below Its Pre-Pandemic Trend

Spending On Physician Services Is Far Below Its Pre-Pandemic Trend

Spending On Physician Services Is Far Below Its Pre-Pandemic Trend

Arithmetically therefore, to keep overall demand on trend, spending on goods must stay above its pre-pandemic trend. Yet spending on goods is crashing back to earth. The simple reason is that durables, by their very definition, are durable. Even nondurables such as clothes and shoes are in fact quite durable. Meaning that are only so many cars, iPhone 13s, gadgets, clothes and shoes that any person can binge on before reaching saturation. Indeed, to the extent that our bingeing has brought forward future purchases, the big risk is a period of underspending on goods. Countering The Counterarguments Let’s address some counterarguments to the hangover thesis. One counterargument is that some goods are a substitute for services: for example, eating-in (food at home) substitutes for eating-out; and recreational goods substitute for recreational services. So, if there is a shortfall in services spending, there will be an automatic substitution into goods spending. The problem is that the substitutes are not mirror-image substitutes. Spending on eating-in tends to be much less than on eating-out. And once you have bought your recreational goods, you don’t keep buying them! A second counterargument is that provided the savings rate does not rise, there will be no shortfall in spending. Yet this is a tautology. The savings rate is simply the residual of income less spending. So, to the extent that there is a structural shortfall in services spending combined with a hangover in goods spending, the savings rate must rise – as it has in the past two months. A third counterargument is that the war chest of savings accumulated during the pandemic will unleash a tsunami of spending. Well, it hasn’t. And, it won’t. Previous episodes of excess savings in 2004, 2008, and 2012 had no impact on the trend in spending (Chart I-6). Chart I-6Previous Episodes Of Excess Savings Had No Impact On Spending

Previous Episodes Of Excess Savings Had No Impact On Spending

Previous Episodes Of Excess Savings Had No Impact On Spending

The explanation comes from a theory known as Mental Accounting Bias. This points out that we segment our money into different ‘mental accounts’. And that the main factor that establishes whether we spend our money is which mental account it resides in. The moment we move money from our ‘income’ account into our ‘wealth’ account, our propensity to spend it collapses. Specifically, we will spend most of the money in our ‘income’ mental account, but we will spend little of the money in our ‘wealth’ mental account. Hence, the moment we move money from our income account into our wealth account, our propensity to spend it collapses. Still, this brings us to a fourth counterargument, which claims that even though the ‘wealth effect’ is small, it isn’t zero. Therefore, the recent boom in household wealth will bolster growth. Yet as we explained in The Wealth Impulse Has Peaked, the impact of your wealth on your spending growth does not come from your wealth change. It comes from your wealth impulse, which is fading fast (Chart I-7). Chart I-7The 'Wealth Impulse' Has Peaked

The 'Wealth Impulse' Has Peaked

The 'Wealth Impulse' Has Peaked

Analogous to the more widely-used credit impulse, the wealth impulse compares your capital gain in any year with your capital gain in the preceding year. It is this change in your capital gain – and not the capital gain per se – that establishes the growth in your ‘wealth effect’ spending. Unfortunately, the wealth impulse has peaked, meaning its impact on spending growth will not be a tailwind. It will be a headwind. As Spending On Goods Crashes Back To Earth, So Will Inflation, Consumer Discretionary Stocks, And Overbought Commodities In the fourth quarter of 2021, US consumer spending dipped to below its pre-pandemic trend and the savings rate increased. Begging the question, how did the US economy manage to grow at a stellar 6.7 percent (annualised) rate? The simple answer is that inventory restocking contributed almost 5 percent to the 6.7 percent growth rate. In fact, removing inventory restocking, US final demand came to a virtual standstill in the second half of 2021, growing at just a 1 percent (annualised) rate. Growth that is dependent on inventory restocking is a concern because inventory restocking averages to zero in the long run, and after a massive positive contribution there tends to come a symmetrical negative contribution. If, as we expect, spending on services fails to catch up to its pre-pandemic trend while spending on goods falls back to its pre-pandemic trend, then there will be a demand shortfall. And if there is a hangover, in which spending on goods crashes to below its previous trend, then the demand shortfall could be substantial. As inflation crashes back to earth, so will overbought commodities. The good news is that the freefall in durable goods spending is leading inflation. In this regard, you might be surprised to learn that the US core (6-month) inflation rate has already been declining for five consecutive months. With spending on goods now crashing back to earth, inflation will also crash back to earth later this year (Chart I-8). Chart I-8As Spending On Goods Crashes Back To Earth, So Will Inflation

As Spending On Goods Crashes Back To Earth, So Will Inflation

As Spending On Goods Crashes Back To Earth, So Will Inflation

Sell Treasury Inflation Protected Securities (TIPS) and other overbought inflation hedges such as commodities that have not yet corrected. Given that the level (rather than the inflation) of commodity prices is irrationally tracking the inflation rate, the likely explanation is that investors have piled into commodities as a hedge against inflation. Hence, as inflation crashes back to earth, so will overbought commodities (Chart I-9). Overbought base metals are particularly vulnerable. Chart I-9Overbought Commodities Are Particularly Vulnerable

Overbought Commodities Are Particularly Vulnerable

Overbought Commodities Are Particularly Vulnerable

Fractal Trading Watchlist This week we focus on nickel versus silver, add tobacco versus cannabis, and update bitcoin, biotech, CAD/SEK, and EUR/CZK. To reiterate, overbought base metals are vulnerable, and the 70 percent outperformance of nickel versus silver through the past year has reached the point of fractal fragility that signalled previous major turning-points in 2014, 2016, 2018, and 2020 (Chart I-10). Accordingly, this week’s recommended trade is to go short nickel versus silver, setting the profit target and symmetrical stop-loss at 20 percent. Chart I-10Short Nickel Versus Silver

Short Nickel Versus Silver

Short Nickel Versus Silver

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Bitcoin's 65-Day Fractal Support Is Holding For Now

Bitcoin's 65-Day Fractal Support Is Holding For Now

Bitcoin's 65-Day Fractal Support Is Holding For Now

Biotech Approaching A Major Buy

Biotech Approaching A Major Buy

Biotech Approaching A Major Buy

CAD/SEK Approaching A Sell

CAD/SEK Approaching A Sell

CAD/SEK Approaching A Sell

EUR/CZK At A Bottom

EUR/CZK At A Bottom

EUR/CZK At A Bottom

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Fractal Trading System

After The Pandemic Binge Comes The Pandemic Hangover...

After The Pandemic Binge Comes The Pandemic Hangover...

After The Pandemic Binge Comes The Pandemic Hangover...

After The Pandemic Binge Comes The Pandemic Hangover...

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields ##br##- Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields ##br##- Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields ##br##- Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields ##br##- Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

BCA Research is proud to announce a new feature to help clients get the most out of our research: an Executive Summary cover page on each of the BCA Research Reports. We created these summaries to help you quickly capture the main points of each report through an at-a-glance read of key insights, chart of the day, investment recommendations and a bottom line. For a deeper analysis, you may refer to the full BCA Research Report. Executive Summary The US midterm elections will bring another round of intense polarization and policy uncertainty this year, though the overall stock market today appears well prepared for the most likely result: a GOP victory in House and Senate. Yet our quantitative Senate election model is “too close to call.” It expects Democrats to retain 50 seats in the Senate and hence the thinnest possible majority. We doubt it, subjectively, but the important point is that the Senate will be stymied either way. Indeed, the only way investors could truly be surprised would be if Democrats made a comeback and retained control of both chambers, but this outcome is very unlikely. Voters make up their minds early in the year during midterm elections, so Democrats may not benefit from any softening of inflation later this year. Still, gridlock ensures that domestic policy uncertainty will rise as well as foreign policy uncertainty. The dollar will be resilient, favoring a tactically defensive positioning. Quant Model For US Senate Election

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Bottom Line: While we expect Republicans to win both the House and the Senate in 2022, our quant model says the Senate is too close to call. Value has bottomed on a structural time frame but the coming months will be challenging and we recommend growth stocks tactically. Feature This report updates our quantitative models for the 2022 Senate and 2024 presidential elections (Chart of the Week). As always, we use the quantitative modeling as a complement to our qualitative analysis. Formal modeling helps to question our assumptions and views. It is not a substitute for empirical analysis and good judgment, whether in economics or politics. Our qualitative analysis utilizes the geopolitical method, a method based on realist political theory, in which we analyze the concrete checks and balances (constraints) that prevent policymakers from achieving their objectives. We then assign scenario probabilities and compare with BCA Research macro and market views to identify investment risks and opportunities. Advantage Republicans In Midterm Elections Our base case for the midterm election is a Republican victory in both the House of Representatives and the Senate. This outlook is consensus in online betting odds (Chart 1). However, the consensus may be underestimating the Democrats in the Senate election. The Senate is still in play and that is where investors should focus this year. However, the only true risk to expectations would be Democrats keeping the House and Senate. Every other scenario involves different shades of gridlock. Democrats can only hold onto both chambers if a shock event occurs that massively upsets expectations. Such a shock would have to be devastating for the Republicans, as it would go against long-established political cycles and current trends. The implication would be a rare chance to pass major legislation on partisan lines: corporate tax hikes and social programs cut out of the current “Build Back Better” planning. Online betters currently give this Democratic scenario a 10% probability: it is essentially a “black swan” and would be inflationary on the margin. Chart 1Midterm Election Odds Favor Republicans

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Other scenarios are more or less disinflationary as Republicans in the opposition will attempt to rein in government spending: If Republicans win both chambers, then they will have an impetus to pass legislation and it is more likely that they will do so, as President Biden could find common ground (a la Bill Clinton after 1994). But if Republicans win only the House, then they will only be capable of obstruction and brinksmanship, a la the “Tea Party” Republicans of 2010-16. This scenario would be disinflationary and would heighten political risks such as the risk of a national debt default over a refusal to raise the debt ceiling in 2023. Bottom Line: The only midterm election outcome that could surprise US markets in a major way in 2022 would be a Democratic victory in both houses of Congress. But the consensus is right to put the odds of that at 10%. Otherwise the midterm scenarios are just different shades of gridlock, albeit with higher policy uncertainty under a split Congress. Republicans Highly Likely To Take The House We have not yet unveiled our House Election model but here we can make some preliminary predictions. The opposition party has gained seats in the House in 90% of the midterm elections since 1862 (incumbent party gained seats four out of 40 times). Exceptions are rare (e.g. 1902, 1934, 1998, and 2002) and not applicable to the 2022 context so far.1 About 47 seats in the House are thought to be competitive this year, compared to around 75 in 2018, 81 in 2010, and 38 in 2002. Of the 47 competitive seats, 30 are especially competitive, with 18 Democratic and 12 Republican. Four Democratic seats are wide open to competition, i.e. lacking an incumbent, the same as four Republican seats. However, more Democrats (29) are stepping down than Republicans (13), a sign that Democratic incumbents recognize cyclical patterns turning against them.2 President Biden has a net negative approval rating (53% disapprove while 42% approve), similar to President Trump in 2018, when Republicans lost 42 seats in the House. Presidential approval has a significant correlation with House losses for the president’s party since the end of World War II. This is especially true when taking the average of presidential approval and his party’s support in the generic congressional ballot. By this measure Democrats are lined up to lose 40 House seats, whereas they only need to lose a net of five to lose control. The nation’s woes are unlikely to improve significantly in time for the election: Inflation is surging and real wages are collapsing (Chart 2). Even if economists observe inflation rolling over before the election, voter inflation expectations will lag, and will be brought into the ballot box. Americans are the unhappiest they have been since the 1970s, as a consequence of the pandemic, the economy, toxic society and politics, and other factors (Chart 3). Chart 2Consumers Facing Rising Prices Amid Declining Incomes

Consumers Facing Rising Prices Amid Declining Incomes

Consumers Facing Rising Prices Amid Declining Incomes

Chart 3Unhappiness Reaches New High

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

A rebound in consumer confidence is not enough to save Biden’s party from losses at the ballot box, as President Obama learned in 2010 and 2014 (Chart 4). Similarly a big drop in confidence can hurt the president in the midterms even if confidence recovers in time for the vote, as happened to Republicans in 2018. Biden has another foreign policy crisis on his hands (Russia), after losing trust on his handling of Afghanistan, and may have more crises to deal with by November (Iran, Latin America). If a crisis hits the oil price, as with Russia or Iran, then prices at the pump will go higher, as we discussed in “Biden’s External Risks.” As for the immigration surge, while it will not concern the business community during a time of labor shortage and inflation, it will concern voters, especially in border states like Arizona (Chart 5). The current surge is historic and may come back to haunt the Democrats. Chart 4Lackluster Consumer Confidence Won't Help Democrats

Lackluster Consumer Confidence Won't Help Democrats

Lackluster Consumer Confidence Won't Help Democrats

Chart 5Immigration Crisis Looms On Southern Border

Immigration Crisis Looms On Southern Border

Immigration Crisis Looms On Southern Border

Republicans will benefit slightly from the post-2020 congressional redistricting. Democrats will probably not make substantial gains as a result of Republican infighting in the primaries, though it could make a big difference in the Senate. We will revisit the latter two issues in future reports (redistricting and Republican primaries) but they only matter if Democrats make a significant comeback in opinion. Otherwise the general swing of public opinion will swamp these marginal effects in the House elections. Worst of all for Democrats, evidence shows that voters tend to make up their minds early in the year. That is when the correlation is strongest between the generic congressional opinion poll and the vote share of elections, though for Democrats in particular late-year polling is equally significant (Chart 6). Chart 6AMidterm Voters Mostly Decided At The Start Of The Year

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Chart 6BMidterm Voters Mostly Decided At The Start Of The Year

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

What could lift the Democrats’ odds? The following factors: The relevance of the Covid-19 pandemic will wane. The economy, while slowing, will continue expanding and unemployment will be very low (Chart 7). Democrats are still somewhat likely to pass a reconciliation bill with the most popular parts of their “Build Back Better” agenda. Democrats will use social “wedge issues” to mobilize their political base. A racialized battle over the Supreme Court nomination and any conservative Supreme Court ruling on abortion may mobilize African Americans and women. It is possible, not likely, that a foreign policy crisis could generate a lasting patriotic backlash against foreign insults, as we discussed last week. This dynamic is relevant given our Geopolitical Strategy’s 75% odds of new Russian military action in Ukraine. A lot can change in nine months during rapidly changing and highly polarized contests in which every marginal vote matters. Bottom Line: While Republicans are highly likely to retake control of the House, the Senate is still in competition. Chart 7Economy Will Slow, Unemployment To Remain Low

Economy Will Slow, Unemployment To Remain Low

Economy Will Slow, Unemployment To Remain Low

The Senate Leans GOP But Still In Play The Senate is more competitive than the House in this year’s election, as 20 Republican seats are up for grabs versus only 14 Democratic seats. About nine of these seats are truly competitive, compared to 13 in 2018, 11 in 2010, and 15 in 2002.3 Only one Democrat is stepping down, in the very blue state of Vermont, whereas five Republicans are stepping down, three of which from competitive states. Hence Democrats have a better chance of picking up Republican seats in North Carolina and Pennsylvania than otherwise. However, even here, Democrats only have a one-seat margin of safety. A net loss of a single seat will yield control of the chamber. Our quantitative model relies on the following six variables: State-level economic health Incumbent party margin of victory in state’s previous Senate race (i.e. 2020) The incumbent president’s net average approval rating Average net support rate of incumbent party in generic congressional ballot A dummy variable for the generic ballot, for statistical purposes A “time for change” penalty for any party that has controlled the Senate for six or more years The model’s results are shown in Chart 8. Currently the model says the status quo will hold, with a 50/50 split in the Senate. Democrats lose Georgia but gain Pennsylvania and hence the balance of power stays the same, as Vice President Kamala Harris casts any tie-breaking vote. Chart 8Senate Quant Election Model Points To Even Split

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Specifically the model says: Arizona is a toss-up but leans Democratic, with 55% odds. Pennsylvania is a toss-up but switches to the Democrats with 54% odds. North Carolina is a toss-up but leans Republican with 47% odds. Georgia switches to the Republican side and is no longer viewed as a toss-up at 43% odds. Looking at the change in these election probabilities since November 2020, North Carolina has seen the biggest drop for the Democrats, followed by Arizona (Chart 9). Democratic odds are worsening in four states, while Republican odds are worsening in three states. Since North Carolina and Pennsylvania are losing their Republican incumbents, this change in odds is a problem for the GOP. By contrast, Democrats are running incumbents in the four states where they are vulnerable. The problem for Democrats, again, is that voters make up their minds early. The closest correlation between the generic party polling and the incumbent party’s performance in the Senate in a midterm election occurs in February at 94% (Chart 10). Chart 9Senate Model: Change In Predicted Probability

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Senate elections, like all American elections, are increasingly nationalized.4 This is evident in the 75% correlation we find between the generic polls and the performance of the incumbent party in the Senate (Chart 10 again). So, for example, while one might view Senator Mark Kelly of Arizona as likely to win given the incumbent advantage and the fact that he is a former astronaut and US Navy captain, and he may indeed win, nevertheless a national wave of anti-incumbent feeling could overwhelm his re-election bid. Still, state effects could matter. To examine these from a macro perspective we look at each state’s Misery Index (inflation plus unemployment) compared to the national average in Chart 11. Here are the notable takeaways: Chart 10Midterm Voters Mostly Decided At The Start Of The Year

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Chart 11AState Level Miseries Point To Risks For Democrats In GA And AZ…

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Chart 11B… And To Republicans In PA And WI

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Misery in Arizona, Georgia, and Pennsylvania is higher than average and rising – negative news for Democrat Kelly, Democrat Raphael Warnock, and the yet-to-be-decided Republican candidate in Pennsylvania. Misery in Florida is also slightly above the national average and rising, though Senator Marco Rubio is likely secure. Wisconsin misery is lower than national average and rising (possibly hurting Republican incumbent Senator Ron Johnson). North Carolina misery is lower than national average and falling (helping the yet-to-be-decided Republican candidate). In other words, Misery Indexes support our model’s findings, yet suggest that Democrats face a headwind in Arizona – where our model is also flagging an important risk for Democrats. In sum, our model’s direction of change suggests Democrats will lose another seat and thus the Senate. Going forward, the key moving parts are the economy and the president’s and his party’s approval ratings. There is a chance that these variables will bottom early in the year and improve later, which underscores that the Senate will remain competitive. What investors can be certain about is that Democrats are extremely unlikely to make significant seat gains in the Senate. So even if they retain control, it will be with the thinnest of possible majorities, and hence the Senate will only be capable of passing bipartisan Republican-authored House bills – or vetoing Republican House bills to save the president from having to veto them. It is also certain that Republicans will fall far short of the 67 votes they would need to remove Biden from office, if House Republicans find or invent a reason to impeach him. Bottom Line: The Senate outcome is too close to call but subjectively we doubt Democrats will pull it off given the negative macro trends cited above. Our Senate election model gives 51% odds that Democrats will retain a de facto majority with 50 seats. 2024 Presidential Vote: Odds Favor Democrats For Now The US presidential election is 34 months away. Investors need to be prepared for any outcome, including another contested election. But it is important to have a base case – especially because a Republican (or Democratic) victory in both House and Senate in 2022 would open up the prospect of single-party control in 2025, which has much bigger policy implications than various shades of gridlock. As a rule of thumb, investors should think of presidential elections as a referendum on the incumbent party, not the president’s person, for the prior four years of material performance. Thus Democrats are currently favored to keep the White House. Voters will feel better than they did in 2020, which suffered a triple crisis of pandemic, recession, and unrest. Significant changes must occur to alter this trajectory – such as a recession, Biden’s stepping down, or a humiliating foreign policy defeat.5 Our quantitative model supports this view: it currently gives a 55.2% chance of Democratic victory in the Electoral College (Chart 12). Chart 12US Election 2024: Quant Model Tips Dems

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Our model relies on the following four variables: State economic health Incumbent party margin of victory in the previous election A penalty for parties that have held the White House for two terms (not applicable in 2024) The president’s approval rating (level) Interestingly our model produces 308 electoral votes for Biden, compared to his actual 306 in 2020, except that some states trade places: Democrats win Florida while Republicans take back Arizona and Georgia. Specifically the model says: North Carolina is a toss-up state but leans Republican. Wisconsin is a toss-up state but just slightly leans Democratic. Florida and Pennsylvania have moved above toss-up range into the Democratic camp. Arizona and Georgia have slipped beneath the toss-up range into the Republican camp. Looking at the change in each state’s odds of voting for the incumbent, Democrats’ chances are falling in eight states while Republicans chances are falling in three states (Chart 13). Wisconsin and Arizona are seeing the most substantial drops, followed by Pennsylvania. Thus the current direction of change is negative for Democrats as one would expect. Biden’s thin margin of victory in 2020 and weak approval ratings make him vulnerable, so the economic performance will largely determine the model’s results going forward. If Biden avoids a recession, that may be enough to retain the White House according to the model. Florida is an interesting case. The model gives a 59% chance it will go to the Democrats. We are suspicious of this outcome but it suggests investors should not take a Republican victory there for granted. Consider: Chart 13Presidential Model: Change In Predicted Probability

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

While we gave President Trump 45% odds of winning in 2020, we predicted he would win Florida due to the state’s partisan leaning.6 That leaning has probably not changed much, although Governor Ron DeSantis’s latest approval rating is only at 45%. However, the six-month change in Florida’s coincident economic indicator has fallen 0.6% since November 2020 and the Misery Index is rising above the national average, as noted above. If Biden loses Florida but the rest of our model is correct, Democrats will retain the White House with 279 electoral college votes. That would leave Wisconsin as the decisive battleground. Yet Wisconsin is very tenuously in their camp today, so any change in the model that gives Florida back to the Republicans would likely give them Wisconsin as well … The result of Biden losing Arizona, Georgia, and Wisconsin (among other combinations) would be a 269-269 tie in the electoral college, in which each state’s delegation to the House of Representatives would have a single vote. A Republican win in the House in 2022 would thus result in a Republican White House in another explosive contested election. But let’s not get ahead of ourselves, 2024 is more than two years away. Bottom Line: Our presidential model gives a 55% chance that Democrats will retain the White House in 2024. Subjectively we agree. A Democratic defeat in 2022 will not rule out a Democratic victory in 2024, especially if Biden is alive and kicking, given the incumbent advantage. But economic factors will largely determine how the model evolves over the next 34 months. Our model also suggests the Electoral College math will be close and that another contested election is possible. Investment Takeaways Based on the current stock market correction, financial markets have priced a fair amount of policy uncertainty already. And this report suggests the midterms merely offer different shades of gridlock. However, Biden’s external risks – namely conflict with Russia – could cause further risk-off moves. And uncertainty will increase as midterms get closer. US policy uncertainty is falling relative to the rest of the world (Chart 14). This is positive for King Dollar, at least over a tactical time frame. The Fed’s interest rate liftoff is also positive for the dollar. Chart 14Lower US Uncertainty In The Near Future Supports The DXY

Lower US Uncertainty In The Near Future Supports The DXY

Lower US Uncertainty In The Near Future Supports The DXY

Hence on a short-term basis, the stock-to-bond ratio can fall further and cyclicals can fall further relative to defensives. Tactically we recommend going long growth versus value stocks (Chart 15). Value has surged in the New Year and the dollar and rate hikes will counteract that, as well as any global energy shock that kills demand. Chart 15Tactically Go Long Growth Versus Value

Tactically Go Long Growth Versus Value

Tactically Go Long Growth Versus Value

However, this is a tactical call. Otherwise, we remain in line with the BCA House View, which favors stocks over bonds and a weaker dollar over the next 12 months. Matt Gertken Senior Vice President Chief US Political Strategist mattg@bcaresearch.com Guy Russell Research Analyst guyr@bcaresearch.com Footnotes 1 Brookings Institution, “Losses by the President’s Party in Midterm Elections, 1862-2014,” Vital Statistics on Congress, February 8, 2021, www.brookings.edu. 2 For the number of competitive seats, see Cook Political Report, cookpolitical.com, and Fair Vote, fairvote.org. 3 See footnotes 1 and 2 above. In addition see the Green Papers, “General Election 2002 – Contests to Watch,” October 25, 2002, thegreenpapers.com, and Ken Rudin, “2010 Senate Ratings: 11 Seats Seen As Tossups; GOP With At Least 3 Pickups,” NPR, July 9, 2010, npr.org. 4 See Joel Sievert and Seth C. McKee, “Nationalization in U.S. Senate and Gubernatorial Elections,” American Politics Research 47:5 (2019), pp. 1036-1054. 5 Our qualitative presidential election framework relies heavily on the work of Professor Allan Lichtman, American University. See our updated Lichtman-style checklist in BCA US Political Strategy, “Biden Is Underwater But His Legislation Will Float,” September 8, 2021, bcaresearch.com. 6 See BCA Research Geopolitical Strategy, “Upgrading Trump’s Odds of Re-Election,” October 26, 2020, bcaresearch.com. See also my interview on Bloomberg’s The Tape Podcast, “Full Blue Sweep Will Push Biden To Left,” July 13, 2020, Bloomberg.com. Strategic View Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Table A2Political Risk Matrix

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Table A3US Political Capital Index

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Chart A1Presidential Election Model

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Chart A2Senate Election Model

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Table A4APolitical Capital: White House And Congress

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Table A4BPolitical Capital: Household And Business Sentiment

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Table A4CPolitical Capital: The Economy And Markets

US Midterm 2022: Different Shades Of Gridlock

US Midterm 2022: Different Shades Of Gridlock

Kicking Off Q4 Earnings Season

Kicking Off Q4 Earnings Season

With 184 S&P 500 companies having reported Q4-2021 earnings, it’s time to take a tab of the interim results. So far, the blended earnings growth rate is 26%, while the actual reported growth rate is 33%. The blended sales growth rate is 13%, while the actual reported rate is 19%. Blended earnings and sales, excluding energy, currently stand at 17% and 9% respectively. Analysts expect Q4-2021 earnings to be 2.4% below the Q3-2021 level. The majority of the companies reporting have easily exceeded analysts’ forecasts: 79% of companies delivered a positive earnings surprise (the long-term average is 66% and the prior four-quarter average is 84%), with Comm Services, Industrials, and Technology leading the pack. In terms of the magnitude of the EPS beats, the overall number currently stands at 4% with Tech in the avant-garde. While this number is strong by historical standards, it appears low compared to recent history: From Q3-2020, earnings surprises were in double digits, ranging from 10% to 22%. The big theme for the current earnings season remains inflation and rising costs. Last week, despite delivering a 19% earnings surprise, CAT shares gapped lower as the company warned about a hit to its margins even as sales climbed. The other S&P 500 members have also guided lower with 59 negative and 34 positive pre-announcements, resulting in an N/P ratio of 59/34=1.7 (Q3-2021 N/P ratio was 0.8). Negative guidance is a key reason for the ubiquitous negative returns following the earnings reports. Clearly, the growth slowdown and margin compression, which we flagged back in October, are only now being priced in by the market. In terms of Q1-2022 earnings expectations, growth is expected to slow to 7%. On a sector level, earnings of Consumer Discretionary, Financials, and Communication Services sectors are expected to contract.

Kicking Off Q4 Earnings Season

Kicking Off Q4 Earnings Season

Bottom Line: This earnings season results are consistent with our theme of earnings growth and profitability coming off the high levels and normalizing. The market is currently pricing in this new normal under a new “tighter” monetary regime.

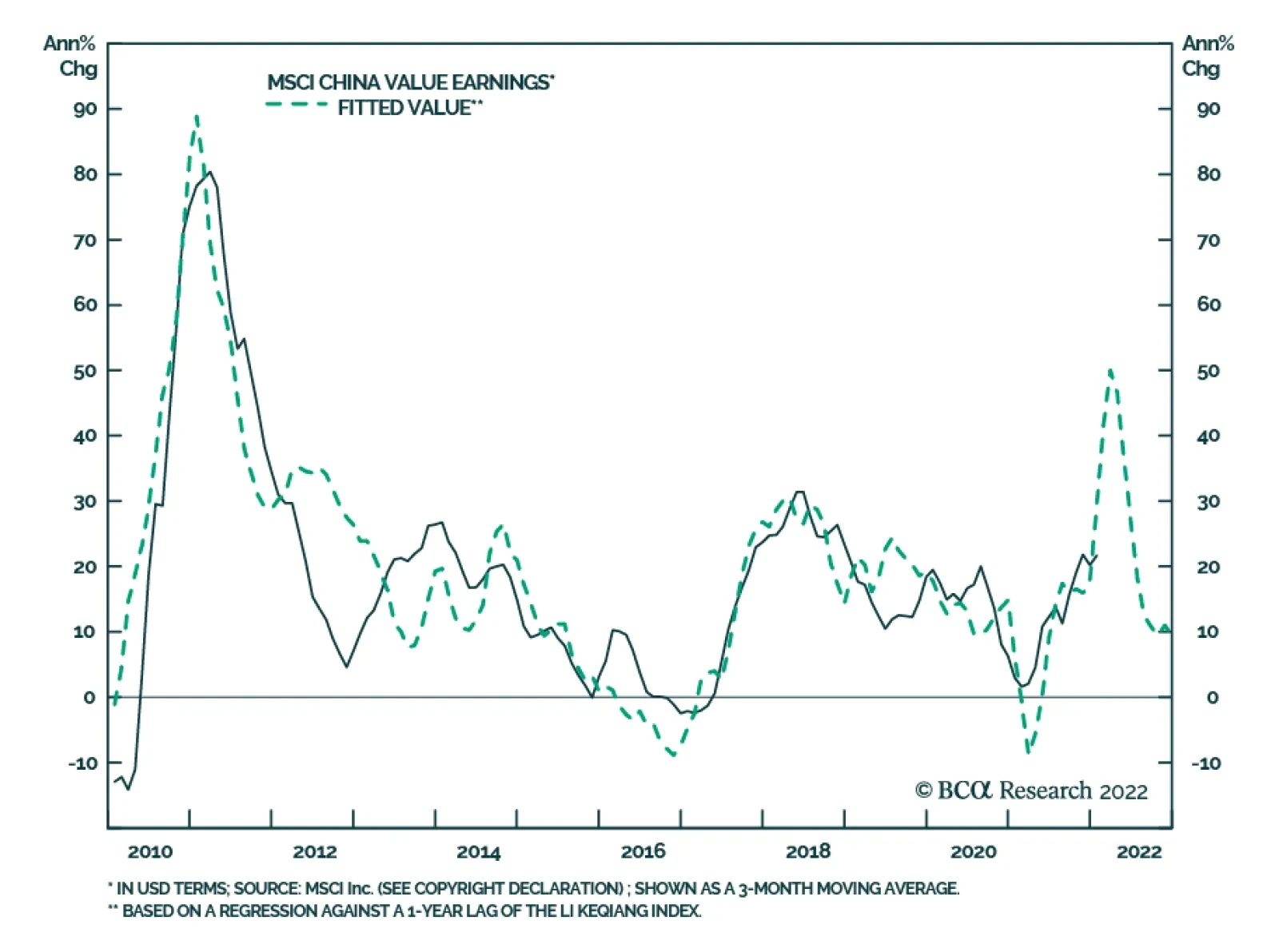

BCA Research is proud to announce a new feature to help clients get the most out of our research: an Executive Summary cover page on each of the BCA Research Reports. We created these summaries to help you quickly capture the main points of each report through an at-a-glance read of key insights, chart of the day, investment recommendations and a bottom line. For a deeper analysis, you may refer to the full BCA Research Report. Dear Clients, On behalf of the China Investment Strategy team, I would like to wish you a very happy, healthy, and prosperous Chinese New Year of the Tiger! Gong Xi Fa Chai, Best regards, Jing Sima China Strategist Executive Summary Chinese Investable Value Stocks Earnings Growth Will Likely Stabilize By Mid-2022

Chinese Investable Value Stocks Earnings Growth Will Likely Stabilize By Mid-2022

Chinese Investable Value Stocks Earnings Growth Will Likely Stabilize By Mid-2022

Chinese investable stocks passively outperformed their global counterparts in the first month of the year. However, we do not think January’s outperformance in the aggregate MSCI China Index will be sustained beyond the next six months. On a cyclical basis, when global stocks recover, growth stocks will likely underperform value stocks. The tech-heavy MSCI China Index is therefore less attractive to investors than other EM and developed market (DM) equities that are more value centric. Chinese investable ex-tech stocks are cheaply valued versus their global peers. Even if the earnings recovery in 2H22 are modest, Chinese investable value stocks are still attractive on a risk-reward basis. For investors that look to increase exposure to China on a cyclical basis, we recommend long Chinese investable value stocks while minimizing exposure to the tech sector. CYCLICAL RECOMMENDATIONS (6 - 18 MONTHS) INITIATION DATE RETURN SINCE INCEPTION (%) COMMENT EQUITIES Long MSCI China Value Index /Short MSCI China Growth Index 02-02-22 Bottom Line: We expect the tech sector’s passive outperformance in January to be short lived. Value stocks in Chinese investable equities, on the other hand, offer a better risk-reward profile relative to their TMT peers and for investors with a 6- to 12-month investment horizon. Feature Chart 1Chinese Investable Stocks Passively Outperformed In January This Year

Chinese Investable Stocks Passively Outperformed In January This Year

Chinese Investable Stocks Passively Outperformed In January This Year

Chinese investable stocks dropped by 5% in January from December last year, giving up a 3% gain in the first three weeks (Chart 1). Still, the MSCI China Index outperformed global stocks by 2%. Some media reports stated that global investors have been drawn to Chinese offshore equities for their relatively cheap valuations and China’s easier monetary policy compared with other major economies . In our January 19 report we recommended investors tactically (0 to 6 months) upgrade the MSCI China Index to overweight within a global equity portfolio, based on the notion that the MSCI China Index would passively outperform since it would fall less than global equities. We maintain this view but do not expect the outperformance in aggregate Chinese investable stocks to endure on a cyclical basis. Our judgment is that while both China’s investable TMT (technology, media, and telecommunications) and ex-TMT stocks have been deeply discounted versus global stocks, beyond the next six months the investable TMT stocks will likely be a drag on the aggregate MSCI China Index. Thus, for investors looking for trades to increase their cyclical exposure to Chinese stocks, we recommend minimize their exposure to the tech sector. Meanwhile, we continue to favor onshore stocks versus their offshore counterparts, despite cheaper relative valuations in offshore stocks. We will discuss our view of the onshore market in next week’s report. A Valuation Catch-Up A valuation catch-up, as opposed to an improvement in China’s economic fundamentals, appears to be driving the passive outperformance in Chinese investable stocks. Our assessment is based on the following observations: Chart 2Chinese Stocks Normally Fall In Risk-Off Environment

Chinese Stocks Normally Fall In Risk-Off Environment

Chinese Stocks Normally Fall In Risk-Off Environment

The beta of Chinese investable stocks has been steadily increasing over the past few years, versus both EM and global stocks. The high beta and pro-risk nature of Chinese investable stocks suggest their prices should fall in a risk-off market. Generally investors would not favor Chinese stocks during global market selloffs. Chart 2 shows that both EM and global stock benchmarks have fallen below their 200-day moving averages. Therefore, investors have been buying Chinese stocks against a risk-off market backdrop because Chinese stocks offer better risk-reward profile either due to their favorable valuations or higher earnings growth. It is simplistic to assume that investors favor Chinese investable stocks because of the country’s easier monetary policy versus the rest of the world. Chinese A-share stocks, which valuations are neutral, have been selling off more than the offshore stocks (Chart 3). Chinese onshore tech company stocks also suffered large losses in January, similar to their US peers (Chart 3, middle and bottom panels). Therefore, the divergence in the relative performance between the Chinese onshore and offshore markets suggests that discounted valuations in offshore Chinese stocks rather than economic fundamentals have driven the relative gains in the investable bourse. The mirror image in regional equity performance this year compared with last year also suggests that factors other than monetary policy explain equity dynamics (Chart 4). While the tech-heavy US bourse was the worst performer among major indices, markets that generated the greatest returns in 2021 have suffered the biggest losses so far in 2022. This phenomenon suggests that investors may be locking in last year’s gains, which is accentuating the underperformance of 2021’s winners and the outperformance of last year’s losers. Chart 42022 Is A Mirror Image Of 2021

Chinese Investable Stocks In A Global Equity Selloff

Chinese Investable Stocks In A Global Equity Selloff

Chart 3Chinese Onshore Stocks Followed The Global Market Downtrend

Chinese Onshore Stocks Followed The Global Market Downtrend

Chinese Onshore Stocks Followed The Global Market Downtrend

Bottom Line: Chinese investable stocks ended January with a much smaller loss than their global peers. The relative outperformance in the MSCI China Index has been mainly driven by its cheaper valuations relative to its global peers. Complacency Risk And Chinese Investable Stocks We see the recent global stock market selloff as a sharp reduction in complacency in the market, particularly in the high-flying tech sector (Chart 5). The correction in global tech stock prices will likely continue for a few months while the market digests a sudden rise in bond yields. As such, the prices in Chinese offshore tech companies will also fall in absolute terms but can still passively outperform their global counterparts, given their deeply discounted relative valuations. Nonetheless, several factors make us cautious about the exposure of China's outsized tech sector beyond the next six months. Hence, our overweight stance on Chinese investable stocks (in relative terms) is limited to the short term (i.e. in the next 0 to 6 months). The growth rates of the 12-month trailing and forward earnings for global tech stocks are both above the 85th percentiles (Chart 6). This indicates that a substantial amount of profit growth has already been priced into global tech stocks, raising the risk of earnings disappointment in the next 6 to 12 months. By contrast, China's TMT-stock 12-month trailing and forward earnings have fallen to below the 25th percentiles (Chart 6, bottom panel). This suggests that the global exuberance in tech earnings is less priced in among Chinese TMT stocks. Chart 5A Sharp Complacency Reduction In The Tech Sector

A Sharp Complacency Reduction In The Tech Sector

A Sharp Complacency Reduction In The Tech Sector

Chart 6Global Tech Earnings Growth Remains Significantly Stretched

Global Tech Earnings Growth Remains Significantly Stretched

Global Tech Earnings Growth Remains Significantly Stretched

However, as noted in our previous reports, Chinese growth/tech companies’ price discount relative to their earnings reflects structural risks that investors are pricing in. These structural headwinds may not intensify in the near term but are not going away either. The regulatory backdrop has not improved enough to justify a sustained faster multiple expansion in China’s internet giants. Beijing continues to rein in its internet behemoths and tighten regulations related to data. It is not yet clear what impact some of the new regulations announced last year will have on the tech sector’s business models. At the very least, antitrust regulations will chip away at the competitive advantage of these tech titans. Furthermore, China's investable TMT sector appears to be a domestic consumer play and thus, likely to weaken in the coming 6 to 12 months given the poor outlook for consumption (Chart 7). Even though China has stepped up its policy support for the aggregate economy, its stringent measures to counter the domestic COVID situation will significantly weigh on its service sector and consumption. The downbeat prospect on China's housing market will also curb consumption growth based on the expectations for employment and income dynamics (Chart 8). Chart 7Outlook For Chinese Internet Sales Remains Downbeat

Outlook For Chinese Internet Sales Remains Downbeat

Outlook For Chinese Internet Sales Remains Downbeat

Chart 8Housing Market Slump A Significant Drag On Household Consumption

Housing Market Slump A Significant Drag On Household Consumption

Housing Market Slump A Significant Drag On Household Consumption

Chart 9Rising Rates Are A Tailwind For Value Stocks

Rising Rates Are A Tailwind For Value Stocks

Rising Rates Are A Tailwind For Value Stocks

Lastly, we expect the pace of increases in bond yields to slow and global equities to trend higher beyond the next couple months. In this case, we are not convinced that Chinese investable stocks will continue to outperform their global peers. The reason for our skepticism is that in a climate of rising interest rates, growth stocks tend to underperform value ones (Chart 9). Given that China's TMT sector’s weight (43%) is considerably higher than the global benchmark (30%), Chinese investable stocks will underperform once valuations in China’s TMT stocks catch up to be in line with those of the global tech sector. Bottom Line: From a valuation perspective, Chinese investable stocks currently look reasonable. In the next a few months when global tech stocks continue to sell off, Chinese offshore tech companies and stocks in general will likely passively outperform their global peers. However, from a risk-reward standpoint and beyond the next six months, the MSCI China Index is at a disadvantage due to a high concentration of stocks in the tech sector. Investment Conclusions On a cyclical basis, Chinese investable stocks will not be immune from global market selloffs due to the offshore market’s high volatility and positive correlation with global stocks. In addition, the MSCI China Index will likely underperform global equities in an up market because of a higher-than-average stake in tech stocks. As such, in a global portfolio we continue to favor onshore stocks over the investable bourse, despite cheaper relative valuations in offshore market equities. Next week’s report will discuss our views on the onshore market. Meanwhile, given the risks facing stocks in China’s tech sector, we propose a new trade recommendation for investors with a cyclical time horizon: long MSCI China Value Index /Short MSCI China Growth Index. The trade will increase cyclical exposure to Chinese offshore stocks, while minimizing stake in the offshore tech sector. The MSCI's China growth index is almost entirely made up of TMT equities, meaning that a relative value play will effectively mimic an ex-TMT position. Extremely cheap valuations in Chinese ex-TMT equities versus global stocks indicate that investors have already priced in a degree of weakness in China's economy (Chart 10). We remain alert to the possibility of a more pronounced near-term slowdown in the business cycle, but we expect China’s economy to regain its footing and stabilize by mid-2022. Our model shows that earnings will decelerate sharply in 1H22 (Chart 11). However, even if the upcoming stimulus and earnings recovery in 2H22 are modest, Chinese value stocks are still attractive on a risk-reward basis given the sizeable valuation discount levied on China relative to global stocks. Chart 10Chinese Investable Value Stocks Are Trading At A Huge Discount Versus Global

Chinese Investable Value Stocks Are Trading At A Huge Discount Versus Global

Chinese Investable Value Stocks Are Trading At A Huge Discount Versus Global

Chart 11Chinese Investable Value Stocks Earnings Growth Will Likely Stabilize By Mid-2022

Chinese Investable Value Stocks Earnings Growth Will Likely Stabilize By Mid-2022

Chinese Investable Value Stocks Earnings Growth Will Likely Stabilize By Mid-2022

Jing Sima China Strategist jings@bcaresearch.com Strategic Themes Cyclical Recommendations Tactical Recommendations

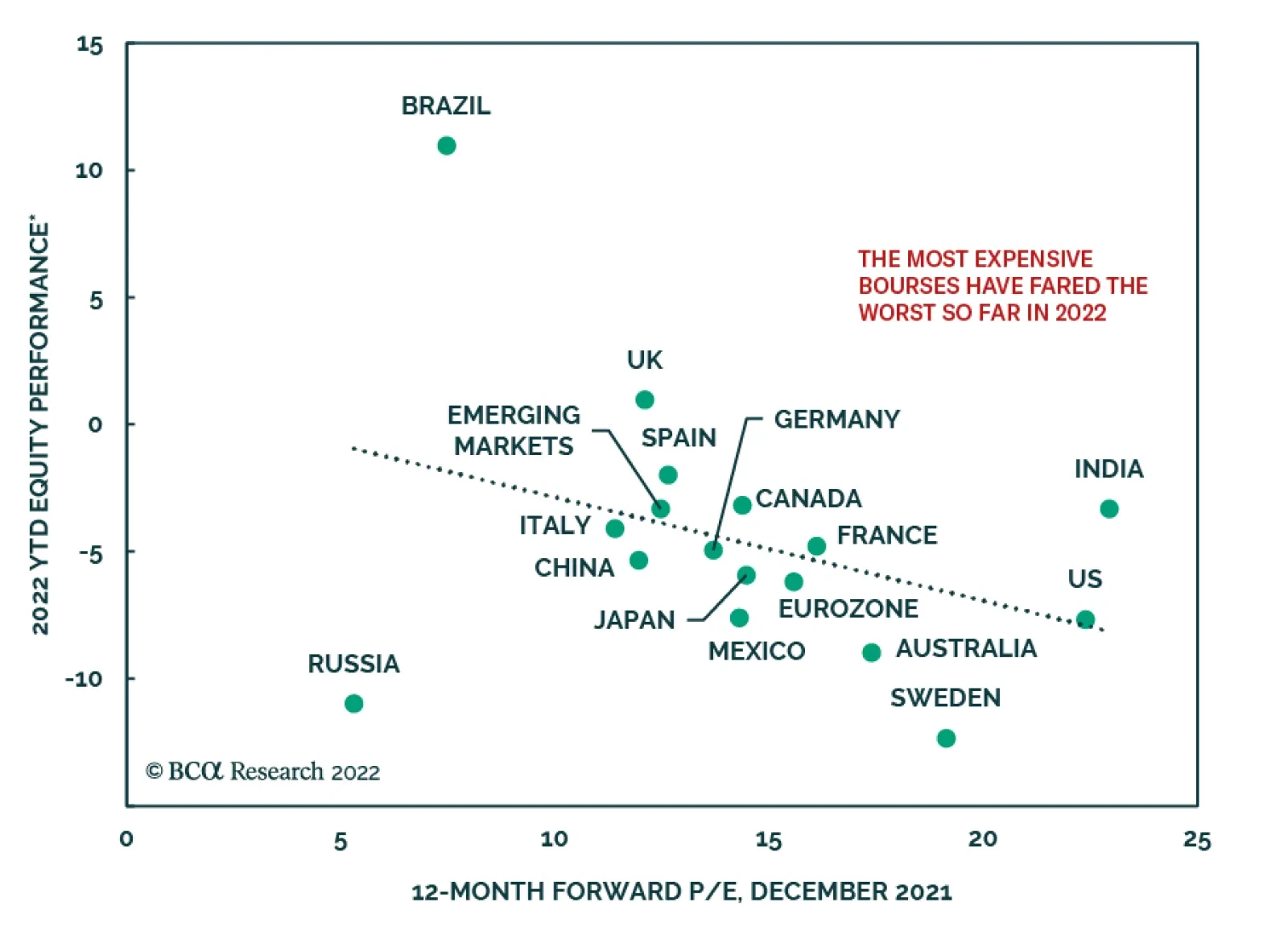

The rapid rise in government bond yields has weighed down on the performance of global equity markets in January (see Market Focus). In an Insight on Tuesday, we showed that global equities that entered the year with the richest valuations have generally sold…

Global equity markets whose valuations were most expensive going into this year have been hit hardest by the recent equity tumult (see Market Focus). Such has been the fate of US stocks: by the end of last week, the S&P 500 was down 7% so far this year,…

The climb up in government bond yields following the Fed’s late-2021 hawkish pivot is the trigger for the selloff in equity markets globally this month. However, the hit to equities has not been uniform across all global markets. In an insight last week, we…