Equities

Stock buybacks have surged following last year’s pandemic-induced collapse. This trend reflects the solid US economic environment. Companies engage in buyback activity when they are in solid financial standing. Robust economic activity in the US has been…

BCA Research’s European Investment Strategy service concludes that European equities are likely to withstand higher yields in 2022. To begin with, BCA Research’s US Bond strategists anticipate a modest rise in Treasury yields to 2.25% in…

Highlights 2022 will be a year of economic normalization. We hope that even if we can’t leave COVID behind, we will learn to live with it. Economic growth will remain strong, but it will be trending down towards its long-term average, while inflation will cool off somewhat on the back of the resolution of supply chain bottlenecks and waning pent-up demand. Monetary conditions will tighten, and 10-year rates will move up towards the 2-2.25% mark. Corporate profitability will return to trend. The likely deceleration in earnings growth and margin contraction will be driven by a combination of factors: A slowdown in top-line growth, a decline in corporate pricing power, and increases in labor and input costs. The US economy is firmly in the slowdown stage of the business cycle. However, growth is coming off high levels, and this phase is likely to be prolonged, and this is by no means a death knell for the bull market. Yet, during the slowdown, returns tend to be lower than during the recovery and expansion phases of the business cycle, and volatility is heightened. We expect an S&P 500 total return of just under 8% – the net result of robust revenue growth and some return compression from profit margins and equity multiples. Point estimates are difficult in finance, so we will characterize this return expectation as in the middle single digits. Overweight Small vs. Large for the following reasons: First, Small is expected to outperform in an environment of rising rates - A BCA view for 2022. Second, Small is cheap. Third, the profitability of Small has improved dramatically which attests to the ability of smaller companies to efficiently manage their operations even under duress. Last, while Small is trading with a 25% discount to Large on a forward PE basis, its earnings growth over the next 12 months is expected to be double of Large, 20% vs. 10%. We are neutral in our Growth/Value allocation, but we find the argument of rates rising and Value outperforming highly compelling. Our neutral position will be a great launching pad towards overweighting value stocks at the first whiff of rising long rates. In the meantime, we choose a selective exposure to value sectors by the means of our hand-picked cyclical themes. Overweight Cyclicals vs. Defensives as the pandemic will recede in importance in 2022: Every time COVID fears subside, Cyclicals outperform Defensives. Pent-up demand has not yet waned, hindered by supply shortages and shipping delays. Further, rising rates is an environment favorable for Cyclicals at the expense of Defensives. Within Cyclicals, we prefer the following sectors and themes: Consumers are flush with cash and there is strong pent-up demand for services and selected consumer goods like services: Overweight Hotels, Restaurants, Cruises, Amusement Parks, and Casinos, along with Commercial and Professional Services. Also, overweight Healthcare Equipment and Services which benefits from the backlog in elective procedures. New Capex Cycle: Businesses bring their supply chains back to the US and excess consumer demand has driven the need for expanded capacity. Capex intentions are on the rise. Overweight Construction and Engineering, Building Materials, and Capital Goods. New Credit Cycle: Early signs that both consumer and business lending is picking up. Rising rates will also lend a helping hand to Banks – overweight Overweight Energy as demand for oil is robust on the back of global recovery and chronic underinvestment in Capex. Underweight resource stocks, which are exposed to a slowdown in China. The US housing market should post a solid performance next year on the back of the structural demand tailwinds: Since GFC, around five million houses were underbuilt. This supply shortage also coincides with millennials, a cohort that has 11 million more people compared to the previous generation, starting families. Overweight Real Estate and Homebuilders Multi-year structural themes are Millennials, Generation Z, EV revolution, and Cybersecurity. 2022 will be a big year for the new technology themes. We are reading about gene editing, the metaverse, 3D printing, and cleantech. We will be sure to share what we learn in a series of Special Reports. Feature House Views Last Week, BCA published its annual outlook, a transcript of our yearly discussion with the firm’s long-time clients, Mr. X and his daughter, Ms. X. In this document, we discussed the major themes for 2022. Below are some of the main conclusions: The COVID-19 pandemic is likely to recede in importance next year. The effect of the recently discovered Omicron variant remains unknown, but we expect any negative economic impact that occurs to be limited to the first half of the year. A receding pandemic will lay the groundwork for a more normal labor market, prices, and the supply of both goods and services. We expect actual inflation will come in lower next year than what short-maturity inflation expectations currently suggest. Economic growth in advanced economies will be above trend for the year on average, and we expect the US and euro area output gaps to close in 2022. Any economic activity disrupted by Omicron in the first half of 2022 will likely shift into the second half of the year. Above-trend growth will be supported by easy monetary policy, a shift in spending from goods to services, and a sizeable amount of excess savings that will support overall consumer spending. A reacceleration in Chinese economic activity is more likely in the latter half of next year rather than in the coming six months.

Chart 0

Stocks will outperform bonds in 2022, but equity market returns will be in the single-digit territory – the net result of robust revenue growth and some return compression from profit margins and equity multiples. Equity market volatility may increase in the lead-up to US monetary policy tightening at the end of the year, but we expect only a moderate rise in long-maturity bond yields—which will not threaten economic activity or cause a major decline in equity multiples. Equity investors should favor small-cap over large-cap stocks in 2022. Small-cap stocks tend to outperform when bond yields are rising, and relative valuation levels are attractive. We generally favor cyclical sectors next year but stretched relative performance versus defensives means that we expect to rotate away from cyclicals at some point over the coming year. A window exists for value outperformance versus growth in 2022, in response to higher long-maturity government bond yields. We do recommend the former over the latter. Brent oil prices will average around $80-81/bbl next year, essentially flat from pre-Omicron levels. The US dollar may remain strong over the coming few months, depending on the extent of the economic impact from the Omicron variant. Beyond that, the dollar’s countercyclical nature, above-trend global growth, and overbought conditions suggest that investors should bet on a lower dollar. In this report, we will explore the implications of the above views for US Equities. 2022 Is A Year Of Normalization If 2021 passed under the banner of recovery, 2022 will be a year of economic normalization. We hope that even if we can’t leave COVID behind, we will learn to live with it, variants and all, and it will become less disruptive to the economy and our personal lives. As such, economic growth will remain strong, but it will be trending down towards its long-term average, while inflation will cool off somewhat on the back of the resolution of supply chain bottlenecks and waning pent-up demand. Monetary conditions will tighten, and 10-year rates will move up towards the 2-2.25% mark. US Economic Growth And Corporate Profitability Will Return To Trend The economy is expected to grow at a robust pace next year (7.3% nominal GDP growth), albeit slower than this year (Chart 1). After a growth surge on the back of the post-COVID recovery, the economy has entered the slowdown phase of the business cycle. Economic growth is poised to shift closer to its long-term trend in 2022. Corporate profitability is also expected to trend lower next year (Chart 2). While corporate earnings in 2021 have been impressive, this performance is unlikely to be repeated, as the unique circumstances of the pandemic and the recovery are giving way to more ordinary business conditions. Amid the pandemic and during the early innings of recovery, companies have cut costs aggressively, improved productivity, while lower interest rates have reduced debt servicing burdens, and a weaker dollar has boosted overseas earnings. As the economy restarted, sales growth surged, and corporate pricing power was on the rise thanks to significant pent-up demand for goods and services and consumers being flush with cash. Chart 1Economic Growth Will Return To Trend

Economic Growth Will Return To Trend

Economic Growth Will Return To Trend

Chart 2Sales Growth Is Poised To Slow

Sales Growth Is Poised To Slow

Sales Growth Is Poised To Slow

In 2022, earnings growth will return to trend (Chart 3). The likely deceleration in earnings growth and margin contraction (Chart 4) next year will be driven by a combination of factors: First and foremost, a slowdown in top-line growth, a decline in corporate pricing power, i.e., the ability of companies to raise prices, which has been diminished by consumers’ income increasing slower than inflation.

Chart 3

Chart 4Profit Margins Are Set To Compress

Profit Margins Are Set To Compress

Profit Margins Are Set To Compress

In the meantime, the tight labor market is putting upward pressure on wage growth (Chart 5). Labor costs are singlehandedly the largest expense, hovering around 50% of sales, dwarfing all the other expense items. Input costs are also on the rise with PPI soaring, cutting into corporate profitability (although we do expect PPI to decelerate) (Chart 6). Chart 5Wage Growth Is Accelerating

Wage Growth Is Accelerating

Wage Growth Is Accelerating

Chart 6Corporate Pricing Power Has Been Waning

Corporate Pricing Power Has Been Waning

Corporate Pricing Power Has Been Waning

In addition, there are a few minor expenses that are set to rise in 2022: Capex recovery will push up depreciation expense, interest expense is set to go up because of rising rates and corporate re-leveraging, and taxes are projected to increase, especially for the US multinationals exposed to the international minimum tax. And of course, there is also an appreciating dollar, diminishing the translated value of overseas profits. While each of these line items is minor, in concert they will have a noticeable adverse effect on corporate profitability. We provide analysis of the S&P 500 margins in Marginally Worse and Sector Margin Scorecard reports. 2022: Pedestrian Returns And Higher Volatility The US economy is firmly in the slowdown stage of the business cycle. However, growth is coming off high levels, and this phase is likely to be prolonged, and this is by no means a death knell for the bull market. Yet, during the slowdown, returns tend to be lower than during the recovery and expansion phases of the business cycle (Chart 7). Slowdowns are also usually accompanied by heightened volatility.

Chart 7

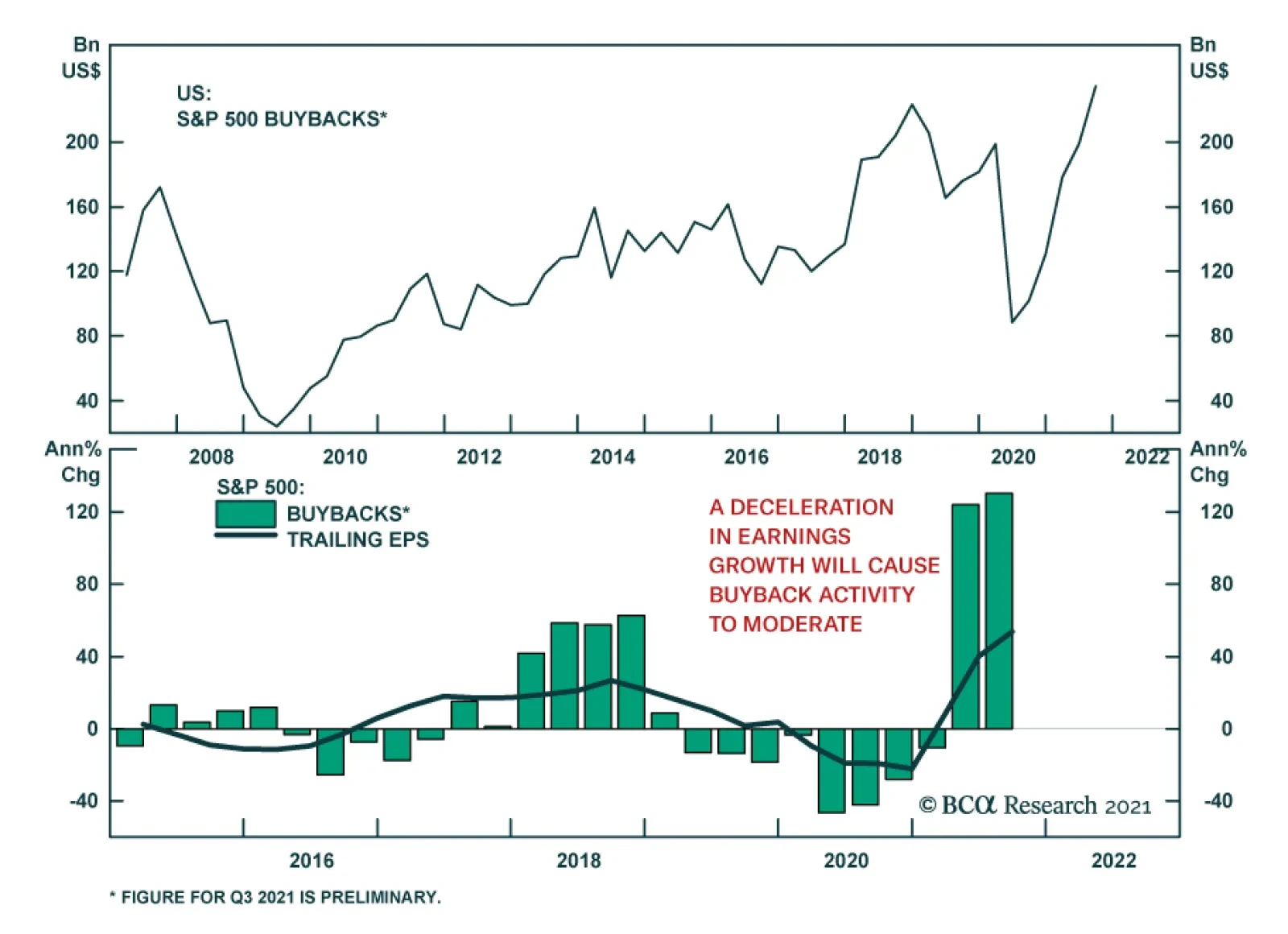

The TINA trade is still on – there are few inexpensive asset classes, and yield is hard to come by. With rates expected to rise, equities are still a more attractive alternative to bonds (Chart 8). Equities are real assets that do a good job protecting investments from rising prices (that is until inflation triggers tighter monetary policy). With rate hikes still a few quarters away, the party is continuing. There is still a lot of liquidity sloshing around looking for attractive corners of the market. This is manifested in positive equity inflows and a “buy-on-dips” mentality, which, so far, has precluded any major market corrections. Buybacks are on the rise – many corporations have had bumper profits and are returning cash to shareholders (Chart 9). This trend is exacerbated by the current administration’s hostility to M&A activity.

Chart 8

Chart 9Buybacks Are Reverting To The Pre-pandemic Level

Buybacks Are Reverting To The Pre-pandemic Level

Buybacks Are Reverting To The Pre-pandemic Level

Returns: Multiple Expansion Passes Baton To Earnings Growth Multiple expansion was a key driver of returns in 2020. In 2021, the baton was passed to earnings growth, which contributed 40% to realized returns this year (Chart 10). 2022 will be more like 2021 than 2020. Multiple expansion is highly unlikely as it tends to be a driver of returns during the recovery stage of the business cycle when the market anticipates economic rejuvenation. Furthermore, valuations are already elevated. When the S&P 500 is trading at over 21x forward earnings, the probability of negative returns over the next 12 months has historically been around 65% (Chart 11). While we believe that there are many factors supporting equities delivering positive returns next year, it is hard to be overly optimistic.

Chart 10

Chart 11

Hence, it will be earnings growth again that will rule the day in 2022, with a little help from dividends and buybacks. However, while earnings growth is a key driver of returns, it is expected to slow from the current levels, returning to its historical trend (Chart 12). The blockbuster returns of 2021 will be in the rear-view mirror. Chart 12Earnings Growth Is Slowing

Earnings Growth Is Slowing

Earnings Growth Is Slowing

Total Return Estimate: Mid-To-High Single Digits Above-trend economic growth and consumer price inflation point to revenue growth in the high single digits, and this would normally serve as a conservative estimate for earnings growth given that profit margins have been trending higher since the beginning of the 2009 economic recovery. However, margins are expected to compress in 2022, and earnings growth to decelerate. We proxy sales growth to nominal GDP growth of 7.6%. With margins expected to contract, the best scenario for the degree of operating leverage for the S&P 500 is a historical average of 0.96, translating sales growth into earnings growth of 7.3% (Table 1). For reference, sell-side analysts expect S&P 500 earnings to grow by 8% in 2022 (Chart 13). S&P 500 PE NTM stands at 20.5 which, historically, on average, is about three points below realized PE LTM in 12 months. We assume that PE LTM at the end of 2022 will be 25.6, or a 1.6% contraction from the 25.2 multiple today. Table 12022 S&P 500 Price Target And Total Return Estimate

2022 Key Views: US Equities

2022 Key Views: US Equities

Chart 13

With an average historical dividend yield of 2.2%, we get: (1+7.3%)*(1-1.6%)*(1+2.2%) = 7.9% - Total Return Estimate 4,591*(1+7.3%)*(1-1.6%) =~ 4,850 - Price Target We expect an S&P 500 total return of just under 8% – the net result of robust revenue growth and some return compression from profit margins and equity multiples. Point estimates are difficult in finance, so we will characterize this return expectation in the middle single digits. The rate of multiple contraction, earnings growth, and dividend yield in 2022 are just educated guesses. Sector And Styles Key Views Small Vs. Large Cap: It Is Finally A Small World 2021 was a tumultuous year for small caps. After a strong outperformance at the beginning of the year on the back of a recovery trade, this asset class has been languishing since March, with each new attempt for a prolonged rally failing (Chart 14). Over the year, small caps have become extremely cheap and unloved, trading at 16x forward earnings with a 25% discount to Large. The BCA Valuation Indicator for Small vs. Large is standing more than two standard deviations below its long-term average. So why was Small so unloved considering two blockbuster reporting seasons with earnings growth of more than 200%? Even on an annualized basis, since 2019 Small has delivered 47% annualized growth compared to 14% from Large (Chart 15). Moreover, smaller companies have been successful in repairing their balance sheets, which now look much healthier. Chart 14Small Had A Tumultuous Year

Small Had A Tumultuous Year

Small Had A Tumultuous Year

Chart 15

Small was out of favor as investors fretted about an economic slowdown (Chart 16), the Delta variant (along with the other Greeks), razor-thin margins, and the ability of smaller companies to navigate the economy, plagued with supply bottlenecks and labor shortages. Yet, we went overweight Small vs. Large back in October and are still sticking to our guns. First, Small, which has higher allocations to Cyclicals, such as Financials and Industrials, is expected to outperform in the environment of rising rates (Chart 17) - A BCA view for 2022. Second, in a market where most asset classes are exuberantly expensive, Small is cheap. Third, the profitability of Small has improved dramatically, which attests to the ability of smaller companies to efficiently manage their operations even under duress, as well as to pass costs on to their customers. Last, while Small is trading with a 25% discount to Large on a forward PE basis, its earnings growth over the next 12 months is expected to be double that of Large, 20% vs. 10%. The froth in expectations for the earnings growth of Small has also come down from its peak at 88% and now appears to be a low bar to clear. Chart 16Small Earnings Growth Expectations Are Reasonable And Profitability Has Rebounded

Small Earnings Growth Expectations Are Reasonable And Profitability Has Rebounded

Small Earnings Growth Expectations Are Reasonable And Profitability Has Rebounded

Chart 17Small Is Expected To Outperform In The Environment Of Rising Rates

Small Is Expected To Outperform In The Environment Of Rising Rates

Small Is Expected To Outperform In The Environment Of Rising Rates

What are the risks to this call? If economic growth disappoints, and the yield curve continues its relentless flattening, signifying a Fed policy mistake or the onset of another COVID Greek, Small is bound to underperform. Margins are narrow and continued cost pressures, especially surging labor costs, have the potential to dent small caps’ profitability. Yet, on a balance of probabilities of such an outcome vs. attractive valuations and fundamentals, this is a risk we are willing to take. Growth Vs. Value: Be Nimble The story of Growth vs. Value is similar to that of Large vs. Small. Value had a fantastic run as the pandemic started to recede, but then as worries about the Delta variant emerged, Growth took over yet again. Over the past year, Growth outperformed Value by 11%, and by 18% over just the last 26 weeks. As a result of such a strong run, Growth has become very expensive, trading at 29x forward multiples, which is a 80% premium to Value (which is trading at 16x). The Growth/Value BCA Valuation indicator is nearly 3 standard deviations above average, and from a statistical perspective, is 99% likely to mean revert. What makes this valuation discrepancy absurd is that both asset classes are bound to deliver roughly the same earnings growth over the next year, i.e., 10%. What is the deal? Just like Small vs. Large, this year, Value vs. Growth has been strongly linked to the 30-year Treasury yield (Chart 18). This has not always been the case in the past, but since the onset of the pandemic, very long-maturity bond yields have done a good job at explaining the relative performance of these asset classes. Growth is overweight Technology, which has been a star of the “work from home” theme. Further, falling long rates inflate the present value of cash flows and earnings of the growth stocks. In the meantime, Value is highly exposed to Financials, which have a hard time maintaining their profitability during times of falling rates and flattening yield curves. Apart from sector composition, Growth as an asset class has also become synonymous with quality, which comes to the rescue at times of heightened risk aversion and uncertainty. This is usually accompanied by falling rates. Indeed, profit margins for Growth are 7% higher than for Value. Since 2019, the annualized earnings growth of Growth is 14.4% compared to 9.8% for Value. The difference is even more dramatic for Sales growth: 6.5% for Growth vs. -1.1% for Value (Chart 19). Chart 18US Value Versus Growth Is Strongly Correlated With Interest Rates

US Value Versus Growth Is Strongly Correlated With Interest Rates (CHART 18)

US Value Versus Growth Is Strongly Correlated With Interest Rates (CHART 18)

Chart 19

However, while we observe that Growth is more reliable for churning out strong numbers, falling sales of Value indicate substantial pent-up demand for products and services. Value also thrives in the environment of robust economic growth and the steepening yield curve. We are currently neutral in our Growth/Value allocation, but we find the argument of rates rising and Value outperforming highly compelling. Our neutral position will be a great launching pad towards overweighting value stocks at the first whiff of rising long rates. In the meantime, we choose a selective exposure to value sectors by the means of our hand-picked cyclical themes. We have also retained some exposure to Growth by staying with our overweights to Technology and Pharma, as a means of protecting our portfolio from the kind of volatility we have experienced because of the Omicron scare and the Fed’s policy adjustments. Growth Is Robust And COVID Is Receding: Overweight Cyclicals Cyclical sectors have significantly outperformed Defensives this year (by 12%), benefiting from economic reopening and ubiquitous pent-up demand both from businesses and consumers. Despite a strong run and exceeding the pre-pandemic peak (Chart 20), Cyclicals have room to move higher when compared with the prevailing levels in 2010-2011, but that period reflected resource price levels that we are unlikely to see in the coming year. Yet, we expect further outperformance of Cyclicals in 2022. Chart 20Cyclicals/Defensives Performance Has Exceeded Pre-Pandemic Peak

Cyclicals/Defensives Performance Has Exceeded Pre-Pandemic Peak

Cyclicals/Defensives Performance Has Exceeded Pre-Pandemic Peak

Chart 21Cyclicals Rally When COVID Fears Reced

Cyclicals Rally When COVID Fears Reced

Cyclicals Rally When COVID Fears Reced

We do hope that the pandemic will recede in importance in 2022: Every time COVID fears subside, Cyclicals outperform Defensives (Chart 21). Pent-up demand has not yet waned, hindered by supply shortages and shipping delays. For many cyclical sectors, such as Consumer Discretionary, Financials, Real Estate, and Industrials, annualized sales growth from 2019 to 2021 is below historical levels, suggesting that there is room for catchup growth (Chart 22).

Chart 22

One of the cornerstones of the BCA outlook is that rates will rise. This is an environment favorable for Cyclicals. Defensive sectors tend to underperform when bond yields are rising, as many of them are heavily indebted and have somewhat fixed cash flows because of regulations (Utilities, Telecoms) or strong competition from cheaper substitutes (Pharma amid challenges from generics and biosimilars). Cyclicals are not that much more expensive than Defensives (22x vs. 19x forward earnings) and are trading with a 13% premium. The Cyclical/Defensive Valuations Indicator has come down from three to two standard deviations (Chart 23). Despite a modest valuations premium, earnings of Cyclical sectors are expected to grow at 25% while Defensives will only grow at 6% over the next 12 months. In short, Cyclicals are more attractive than Defensives as a group, but we prefer a granular approach and handpick cyclical sectors that we expect to thrive in the current macroeconomic environment and have favorable sales and earnings growth prospects. Later in the report, we will discuss some of our cyclical sector picks. Chart 23Relative Valuations Of Cyclicals Have Come Down But Are Still Rich

Relative Valuations Of Cyclicals Have Come Down But Are Still Rich

Relative Valuations Of Cyclicals Have Come Down But Are Still Rich

Despite Worries About Inflation, Consumers Still Have Money To Spend: Overweight Consumer Services The US government has supported consumers during the lockdowns with a series of helicopter cash drops to all Americans, enumerated in trillions of dollars. As a result, even nine months after the last cash disbursement, consumers are sitting on $2.3 trillion in excess savings (Chart 24). Extremely loose fiscal and monetary policy have lifted household net worth by 128% of GDP (Chart 25). And while consumers do indeed worry about inflation, expecting it to rise to 7.5% in 12 months, there is still plenty of dry powder sitting in their bank accounts. Chart 24Consumers And Businesses Have A Lot Of Dry Powder

Consumers And Businesses Have A Lot Of Dry Powder

Consumers And Businesses Have A Lot Of Dry Powder

Chart 25Household Wealth Has Soared

Household Wealth Has Soared

Household Wealth Has Soared

Consumer spending on goods has been above the pre-pandemic trend for months and has recently turned. In the meantime, spending on services is still below pre-pandemic levels, suggesting that there is plenty of pent-up demand (Chart 26). Specifically, spending on sports clubs, public transportation, personal care, medical services, and professional services are still below pre-pandemic levels. Pent-up demand will boost Consumer Services, and we recommend overweights to Hotels, Restaurants, Cruises, Amusement Parks, and Casinos, along with Commercial and Professional Services. Further, while pent-up demand for goods has generally been met, there are still pockets of demand out there due to shortages, such as for automobiles and selected consumer durables. We are also overweight Healthcare Equipment and Services which benefits from the backlog in elective procedures. Chart 26Spending On Services Is Still Below The Pre-pandemic Trend

Spending On Services Is Still Below The Pre-pandemic Trend

Spending On Services Is Still Below The Pre-pandemic Trend

New Capex Cycle: Overweight Industrials Industrials is another cyclical sector that we favor. Supply chain disruptions have demonstrated for many businesses that they need to bring their supply chains back to the US, launching the US Manufacturing Renaissance. Also, excess consumer demand has driven the need for expanded capacity. For months now, manufacturers have been inundated with orders (Chart 27). The industrial sector is also exposed to the restocking of inventories and is poised to benefit from the Infrastructure Bill. Therefore, Industrials will continue to benefit from the surge in capital expenditures, as evidenced by the sharp increase in US core capital goods orders. Capex intentions have been on the rise as well (Chart 28). Chart 27Producers Inundated With Orders And Need More Capacity

Producers Inundated With Orders And Need More Capacity

Producers Inundated With Orders And Need More Capacity

To profit from this emerging trend, we are overweight Construction and Engineering, Building Materials, and Capital Goods. Chart 28Surge In Capital Expenditure Will Benefit Industrials

Surge In Capital Expenditure Will Benefit Industrials

Surge In Capital Expenditure Will Benefit Industrials

New Credit Cycle: Overweight Banks 2021 was a blockbuster year for banks on the back of the booming M&A and IPO activity. However, to achieve sustainable profitability, they need to jumpstart the loan growth process. Both businesses and consumers have repaired their balance sheets, and the re-leveraging cycle is set to commence to finance Capex and higher price tag purchases like autos. There are early signs that lending is likely to pick up next year (Chart 29). According to JPM: “The customers who typically contribute to credit card loan growth are starting to spend the savings built up from the pandemic at a faster clip, suggesting they could be getting closer to taking on debt again.” Credit card spending is recovering (Chart 30). Chart 29Early Innings Of A New Credit Cycle

Early Innings Of A New Credit Cycle

Early Innings Of A New Credit Cycle

Chart 30Consumers Are Borrowing Again

Consumers Are Borrowing Again

Consumers Are Borrowing Again

While sell-side analysts anticipate that margins will decline, we believe that they may surprise on the upside: High operating leverage, improving pricing power, and growing demand for loans will contribute to strong profitability. Further, the BCA house view is 10-year rates rising to 2.0 – 2.25% in 2022, which will support net interest margins. Energy Sector Vs. Materials Energy profit margins are linked to underlying commodity prices. The BCA Commodity and Energy strategists’ view is that the medium-term supply/demand backdrop is highly supportive of the current energy pricing dynamics and that the oil price is expected to stay high, at around its current level, for the next two years. They also note that upside price risk is increasing going forward, due to inadequate Capex. Although the price of oil has risen above the break-even level, energy companies are reluctant to invest in Capex due to pressure from shareholder activists and newly found financial discipline (Chart 31). As a result, prices are likely to remain high until “high prices cure high prices.” In the meantime, energy producers are returning cash to shareholders – a unique bonus in the current world starved for yields. Oil demand is expected to stay robust on the back of the global economic recovery, especially with an increase in consumption by airlines that are resuming international travel. Case in point: ExxonMobil (XOM) “anticipates demand improvement in its downstream segment with a continued economic recovery.” Chart 31Chronic Underinvestment Is Driving Up Price Of Oil

Chronic Underinvestment Is Driving Up Price Of Oil

Chronic Underinvestment Is Driving Up Price Of Oil

Chart 32A Slowdown In China Is Hurting Demand For Raw Materials

A Slowdown In China Is Hurting Demand For Raw Materials

A Slowdown In China Is Hurting Demand For Raw Materials

Resource stocks, on the other hand, may not meaningfully outperform in 2022, at least not consistently – our views on China imply that metals and mining stocks may at least passively underperform in the first half of the year (Chart 32). US Housing Rally Still Has Legs To Run On The US housing market should post a solid performance next year on the back of the structural demand tailwinds: Since the GFC, around five million houses were underbuilt. This supply shortage also coincides with millennials, a cohort that has 11 million more people compared to the previous generation, starting families. The data is also reflective of the supply/demand mismatch with inventories of new and existing homes for sale, and the homeowner vacancy rate at all-time lows, and housing prices exploding higher. At the same time, US building permits are still below the two million SAAR print that historically marked previous housing cycle peaks (Chart 33). The implication is that the current housing boom still has room to go further, benefiting US homebuilders as they monetize the supply/demand mismatch. Homebuilder sentiment rose to a six-month high in November. Tack on the 80bps sell-off in the 30-year US Treasury yield that translates into more affordable mortgage rates for consumers, and there is little that can undercut the US housing market throughout 2022. We are bullish on both the Real Estate and Homebuilders sectors. However, we would be remiss not to mention risks to this call: The performance of the real estate market is highly dependent on the direction of the rates. If long rates rise substantially, this sector will be in the crosscurrents of housing shortages and less affordable mortgages. However, the 2-2.25% 10-year yield that BCA anticipates by end -2022 should not put a significant dent into house ownership affordability. Chart 33Housing Shortages Will Drive Multi-Year Outperformance of Real Estate And Homebuilders

Housing Shortages Will Drive Multi-Year Outperformance of Real Estate And Homebuilders

Housing Shortages Will Drive Multi-Year Outperformance of Real Estate And Homebuilders

Risks To The Outlook Rising rates are a key condition for our sector and style calls to pan out. However, if supply chain bottlenecks do not clear soon, inflation will not slow down meaningfully, and the US economy will enter a rising price-wage spiral. The Fed will realize that it is behind the curve and will start hiking rates aggressively, i.e., faster than the pace currently anticipated by the market. As a result, economic growth will disappoint, and the unemployment rate will rise. The yield curve will continue flattening with long rates staying range-bound or moving lower. In this scenario, Growth and Defensives will outperform, while Small, Value and Cyclicals will underperform. Multi-Year Structural Themes To finish, we want to remind clients of our long-term themes, which we expect to continue to pan out next year. Millennials Are Not Coming Of Age; They Are Already Here According to the US Census Bureau, millennials (born 1982 to 2000), are the US's largest living generation and represent more than one-quarter of the US population. This is a generation that is highly educated, and relatively unburdened by debt. While in the past, this generation was perceived as “forever young,” it is rapidly showing signs of maturing: Joining the labor force, starting families, and shopping for houses and cars, thereby pushing consumption up. However, millennials’ consumption basket is different, with an emphasis on new technology, homeownership, electric vehicles, and green energy. ETFs that capture the theme are MILN and GENY. Gen Z Is Coming Of Age And Has Money To Spend Generation Z in the US includes 62 million people born between 1997 and 2012. With $143B in buying power in the US alone, making up nearly 40% of all consumer sales, Gen Z wields increasing influence over consumer trends. This is the first generation of digital natives—they simply can’t remember the world without the internet. They are the early adopters of the new digital ways to bank, get medical treatments, and learn. Gen Z is joining the workforce and replacing retiring baby boomers. We have created a Gen Z basket with stocks representing fintech, investing and crypto, online gaming, quality-over-price, and some others. There are no ETFs just yet that capture this emerging theme. Cybersecurity Is A Must-Have Global digital transformation as well as rising geopolitical tensions create fertile ground for attacks by both cybercriminals and malicious state actors. The cyber defenses of most private and public companies are still ill-prepared, and the space is poised for robust growth since cybersecurity is a “must-have” for survival. This growing market has attracted a plethora of new cybersecurity players who provide cloud-based SaaS solutions and are well-versed in deploying AI and ML to counter cyber threats. While many of these companies are still young with relatively small capitalization, their potential is enormous. We recommend tactical and structural overweights to the theme. The following ETFs provide exposure to the theme: BUG, CIBR, and HACK. EV Revolution The auto industry is undergoing a major technological disruption. This process is expensive and perilous yet presents an enormous future earnings growth opportunity. And all the ingredients for success are in place: The proliferation of new technologies, government support, changing consumer preferences, and a surging US economy. This tide will lift all boats: Legacy and EV-only auto manufacturers and suppliers as well as EV ecosystem players. We are bullish on the sector on a 12-month investment horizon. ETFs are DRIV, IDRIV, KARS, BATT, and LIT. What We Are Researching For 2022 2022 will be a big year for the new technology themes. Some are brand new, while others have been around for a while. We are reading about gene editing, the metaverse, 3D printing, and cleantech. We will be sure to share what we learn in a series of Special Reports. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Recommended Allocation

Highlights The risk to European stocks from higher yields is overstated for 2022. Not only do equities possess a valuation cushion compared to bonds, but also the stock returns/bond yields correlation remains positive. This positive correlation is only two decades old, and it is a consequence of the stabilization of inflation and inflation expectations, which caused bond yield changes to mostly reflect adjustment in anticipated economic activity. As long as the recent inflation upsurge peters off next year, the equity/yield correlation will remain positive in 2022. Despite this sanguine short-term view, the long-term outlook is fraught with risks because next year’s inflation decline will be temporary; inflation is on a secular uptrend. The equity returns/bond yield correlation will become negative toward the middle of the decade, which will create a major headwind for the secular returns of both stocks and bonds. Feature Extremely low yields and elevated valuations constitute a potentially toxic mix for the equity outlook next year. The logic is straightforward: if yields rise enough, nosebleed multiples will become unjustifiable and the stock market will crash. Chart 1Protection Against Higher Yields

Protection Against Higher Yields

Protection Against Higher Yields

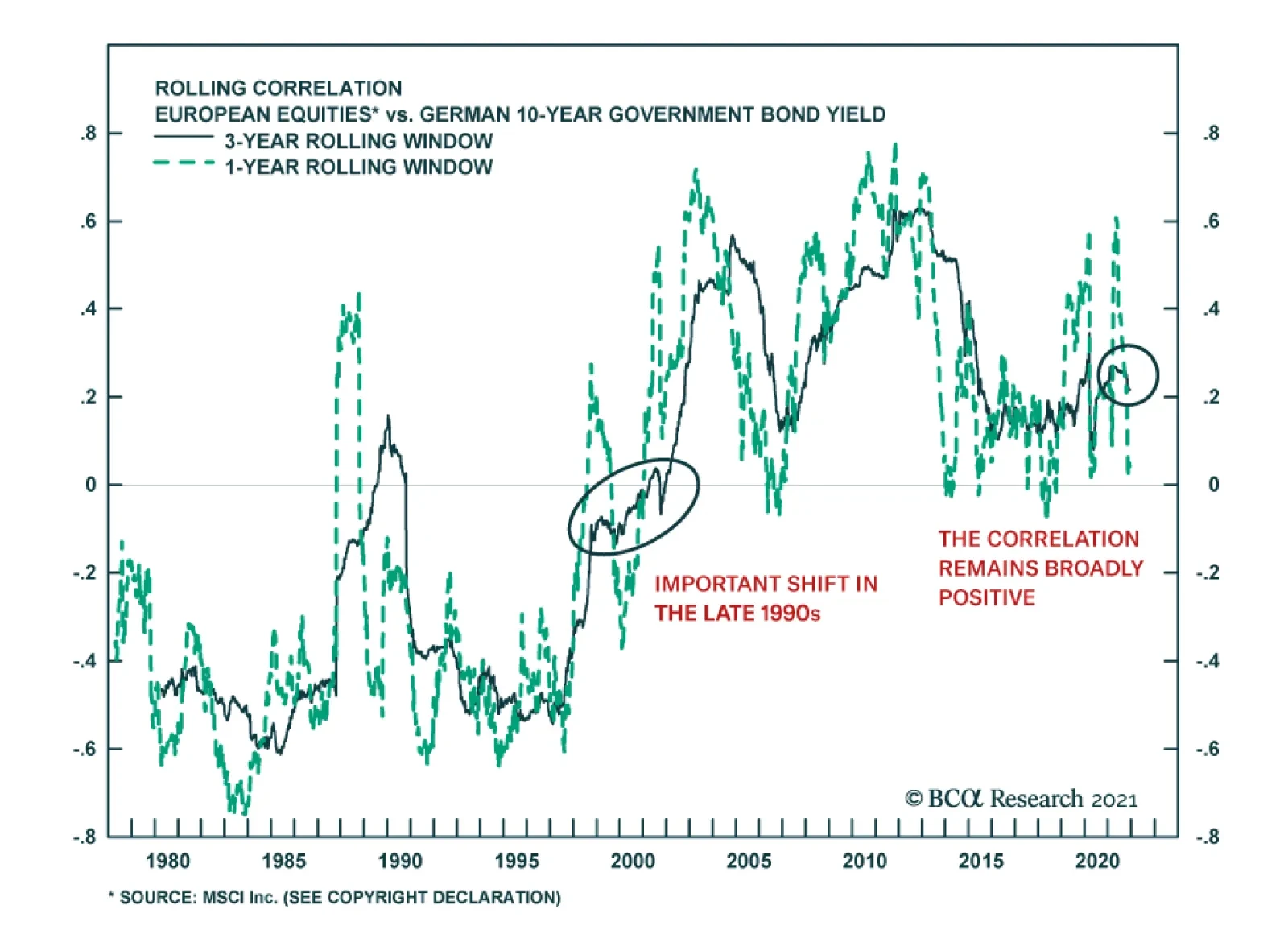

The picture is more complex and instead, European equities are likely to withstand higher yields. To begin with, BCA Research’s US Bond strategists anticipate a modest rise in Treasury yields to 2.25% in 2022, and our Global Fixed-Income strategists foresee an even more limited increase in German rates. Moreover, as we showed in our 2022 Key Views piece published last week, European equities embed a large valuation cushion in the form of a significant premium in their dividend yield relative to Bund yields (Chart 1). The correlation between yields and equities is another facet that will impact the effect of higher yields on the equity bull market. For now, it is premature to conclude that the positive correlation between yields and the absolute performance of European equities is poised to turn negative again in 2022. However, over the next couple of years, such a correlation reversal will take place, because inflation expectations are increasingly likely to become unmoored to the upside. Stocks Like Higher Yields Over the past two decades, one of the major financial market paradoxes has been the relationship between equity prices and bonds yields. Since 1998, the weekly returns of the MSCI Euro Area equity benchmark have correlated positively with the change in 10-year German yields (Chart 2). However, prior to the late 1990s, changes in bond yields and stocks prices were negatively correlated. Chart 2For Two Decades, Bond Yields And Stocks Prices Have Moved Together

For Two Decades, Bond Yields And Stocks Prices Have Moved Together

For Two Decades, Bond Yields And Stocks Prices Have Moved Together

The key to the shifting relationship between stocks and bonds is the link between yields and economic activity. Stock returns have always been procyclical because earnings are the most important driver of equity returns (Chart 3). However, bond yields have become increasingly pro-cyclical over time. Today, Bund yields and the German LEI move in tandem, but, prior to 1986, their five-year rolling correlation was negative (Chart 4). Chart 3Stocks Follow Earnings Who Follow Growth

Stocks Follow Earnings Who Follow Growth

Stocks Follow Earnings Who Follow Growth

Chart 4Shifting Link Between Bunds And German Growth

Shifting Link Between Bunds And German Growth

Shifting Link Between Bunds And German Growth

The positive correlation between German growth and German yields sheds light on why the correlation between yields and stocks is now positive, but it does not explain why this positive link emerged in the late 1990s and not earlier. Financial asset prices reflect global phenomena. Stock indices in advanced economies overrepresent multinationals which are affected by global economic fluctuations. Meanwhile, capital is fungible and flows freely across borders. As a result, German bond yields are not the unique factor that matters to the correlation between equities and stock. Instead, the behavior of global yields and equities is critical. Chart 5Living In The Shadow Of The Asian Crisis

Living In The Shadow Of The Asian Crisis

Living In The Shadow Of The Asian Crisis

According to this logic, the correlation between global yields and global growth becomes important. As Chart 5 illustrates, the relationship between global bond returns and global economic activity became much closer around 1998 than it was prior to this date. The key turning point was the Asian crisis of 1997/98. Why was the Asian crisis so fundamental? It was the end state of the disinflationary trend started under Federal Reserve Chairman Paul Volker. After the Asian crisis, the region’s newly industrialized economies switched from chronic current account deficits to chronic surpluses, which added to the global supply of savings. Moreover, Asian economies became hypercompetitive because of severely devalued exchange rates, which limited pricing power around the world. Finally, the Chinese economy became a force to be reckoned with and its share of global trade expanded massively. Together, these forces amplified competitive pressure around the world and made every inflation uptick self-limiting. The impact of the shock is visible in the inflation data. As Chart 6 shows, core inflation in the US and in the G7 has been stable since 1998, capped near 2.5%, except for 2021. Additionally, after the Asian crisis, the volatility of core inflation collapsed among both the G7 and Eurozone economies (Chart 7). Chart 62.5%, A 20-Year Old Ceiling

2.5%, A 20-Year Old Ceiling

2.5%, A 20-Year Old Ceiling

Chart 71998: RIP CPI Volatility

1998: RIP CPI Volatility

1998: RIP CPI Volatility

The effect of this steady inflation was to stabilize inflation expectations. Thus, after 1998, the most important driver of bond price annual changes has been fluctuations in anticipated real economic activity, which explains why the relationship between global bond returns and the global LEI became much tighter afterward (Chart 5, on page 4). This result is crucial to understand the impact of higher yields for equities. It suggests that, if rising yields reflect improving economic growth, then the correlation between yields and stocks will remain positive and equities may climb higher along with mounting long-term interest rates. Bottom Line: Higher yields do not necessarily portend the end of the equity bull market. Stock prices and bond yields have been positively correlated since the Asian crisis of 1997/98 because fluctuating growth expectations drive most of the change in yields. As long as this remains the case, equities can handle higher yields. Can The Correlation Shift Sign Again? The correlation between equities and bonds is not static. There are threats that could restore both temporarily or permanently the negative correlation between changes in bond yields and stock returns that prevailed prior to 1998. A Temporary Correlation Shift? Since their March 2020 lows, 10-year yields have increased 94bps and 51bps in the US and Germany, respectively. Meanwhile, the MSCI Eurozone equity benchmark is up 78%. We are clearly not yet in an environment in which rising long-term interest rates hurt stocks. In the short term, the correlation between yield changes and equity returns may turn negative if yield moves into constraining territory—this is to say, if they rise enough to risk a recession. In more academic terms, this equates to rates moving above the neutral rate of interest, or r-star. Chart 8A Long Way To Go Before Policy Becomes Tight

A Long Way To Go Before Policy Becomes Tight

A Long Way To Go Before Policy Becomes Tight

There is little indication that interest rates are moving above this level in the short term. US and European policy rates remain well below Taylor rule estimates of equilibrium (Chart 8), which suggests that policies are still highly accommodative. The most worrisome signal comes from the slope of the yield curve. Since March 2021, the US 2-/10-year yield curve has flattened by 76bps to 81bps and, since October 2021, the same yield curve has flattened by 23bps to 35bps in Germany. Moreover, the 20-/30-year US yield curve became inverted in October 2021. These dynamics may indicate that policy is already on the verge of becoming too tight, even if only five interest rate hikes are expected in the US over the next two years. Chart 9Term Premia Are Still Negative

Term Premia Are Still Negative

Term Premia Are Still Negative

A curve flattening episode is the normal course of events when central banks become less accommodative; it is not a sign of impending doom. Instead, an inverted yield curve is the indication that the policy rate is above r-star. After all, if interest rates genuinely constrain growth, they will slow economic activity in the future, which will necessitate lower rates and generate a negative curve slope. We are not there yet. Moreover, the term-premium remains negative across major advanced economies, which suggests that a recessionary signal will come from a deeper yield-curve inversion than in the past (Chart 9). Chart 10Upside To The Terminal Rate

Upside To The Terminal Rate

Upside To The Terminal Rate

Another factor likely to allow yields to rise without killing the equity market is that the expected terminal rate of interest remains too low, as we wrote in our 2022 Key Views piece last week. Historically, it is common for the expected terminal rate to rise as central banks begin to lift interest rates, especially if the economy handles the first hikes well. Today, the expected terminal rate is below the levels that prevailed after the GFC, despite a much firmer economy unburdened by private sector deleveraging and excessive fiscal tightening (Chart 10). As such, we anticipate the expected terminal rate to increase, which will limit how quickly the yield curve will flatten next year even if the Fed elevates interest rates and the ECB aggressively downshifts its pace of asset purchases once the PEPP ends. Chart 11Long-Term Inflation Expectations Are Not A Concern, Yet

Long-Term Inflation Expectations Are Not A Concern, Yet

Long-Term Inflation Expectations Are Not A Concern, Yet

Under this aperture, the biggest risk for stocks remains inflation. Further acceleration in inflation, especially if it pushes the 5-year/5-year forward inflation breakeven rate above the Fed’s comfort zone (Chart 11), could hurt stocks. Essentially, investors would price in a shift in the monetary policy environment whereby risks of a severe tightening would increase. However, as we recently wrote, the odds are mounting that short-term inflation will soon peak. Oil inflation is ebbing, while transportation costs are declining and supply bottlenecks are beginning to ease. Moreover, money growth in the US and the Eurozone, which proved relevant variables to explain inflation this year, is also waning (Chart 12). Finally, a mounting number of global central banks are tightening policy, which implies that maximum accommodation is behind us (Chart 13) In this context, we expect the positive correlation between stock returns and yield changes to remain broadly positive. A short-term rise in yields could easily contribute to equity market volatility and may even cause a deeper stock market correction than any experienced since April 2020. However, this will prove to be a temporary phenomenon, and thus we remain buyers of the dip. Chart 12Slowing Money Supply Growth, At Last

Slowing Money Supply Growth, At Last

Slowing Money Supply Growth, At Last

Chart 13Global Policy Is Becoming Less Easy

Global Policy Is Becoming Less Easy

Global Policy Is Becoming Less Easy

A Longer-Term Correlation Shift? A shift in the long-term correlation between equity returns and bond yield changes is a much more meaningful risk to stocks than short-term changes. BCA expects inflation to peak in the short term, but this will only be part of a stop-and-go process. Inflation is on a structural uptrend and so, any decline in 2022 and early 2023 will morph into renewed pressure, after the global output gap becomes positive again by the end of next year. Chart 14A Deflationary Tailwind Is Gone

A Deflationary Tailwind Is Gone

A Deflationary Tailwind Is Gone

Many structural forces are moving away from deflationary to inflationary. True, technological progress remains a deflationary anchor. However, this downward pressure on inflation is no longer buttressed by a deepening of globalization (Chart 14). Moreover, because of the rise of populism around the world over the past five years, fiscal policy is unlikely to move back to the austere Washington Consensus that dictated governance from President Reagan up to the moment President Trump took power. Additionally, ageing across advanced economies and China, as well as the so-called “Great Resignation,” will constrain the expansion of the global supply side. This background suggests that the period of flat inflation that prevailed from 1998 to 2020 is ending. As a corollary, inflation expectations will embark on a multi-year upward drift. This process is likely to loosen the correlation between economic activity and yields. As a result, the period of positive correlation between yield changes and equity returns is in its last innings. This will represent a major difficulty for asset allocators over the next ten to twenty years, as it points to poor long-term real returns for both bonds and stocks. Bottom Line: The correlation between stock returns and bond yield changes is likely to remain positive in 2022, which implies that European stocks will eke out another year of positive returns, despite BCA’s house view that yields will rise. However, the long-term outlook is more problematic. The growing likelihood that inflation is making a secular upturn means that the two-decades old positive correlation between equity returns and bond yield change will become negative again around the middle of the decade. This shift will have a profound and deleterious impact on both stocks’ and bonds’ secular returns. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Tactical Recommendations

The Correlation Convolution

The Correlation Convolution

Cyclical Recommendations

The Correlation Convolution

The Correlation Convolution

Structural Recommendations

The Correlation Convolution

The Correlation Convolution

Closed Trades Currency Performance Fixed Income Performance Equity Performance

Highlights The helicopter drops are over, … : The economic impact payments and supplemental unemployment insurance benefits may have stopped, but their full impact has yet to be felt. … but fiscal and monetary policy will continue to support demand, … : US households are sitting on more than $2 trillion of excess pandemic savings. If they were to spend just half of their stash over the next two or three years, the economy would gain a steady tailwind. … and the macro backdrop will remain equity-friendly, … : Monetary policy will be less accommodative going forward but it will remain solidly supportive of markets and the economy across all of 2022. … so investors should stick around for one last round: Equities and spread product outperform when monetary policy is easy. As long as COVID-19 doesn’t spring a nasty surprise, the expansion will continue and risk assets will once again generate positive excess returns over Treasuries and cash. Feature BCA editors’ annual sit-down with Mr. and Ms. X provides a welcome opportunity to gather our thoughts for the coming year and review how this year’s calls panned out. Looking back to this time last year,1 our risk-friendly recommendations performed well as the rationale behind them proved to be sound. Financial markets thrived in the wake of monetary and fiscal policy measures intended to err on the side of providing too much accommodation. The policy efforts were massive, and their support for markets and the economy has yet to be fully exhausted; indeed, their lengthy half-life is a key pillar of our sanguine 2022 outlook. Unlike last December, investors cannot look forward to peak accommodation in the year ahead; the peak is behind us and monetary and fiscal stimulus will be throttled back. The Fed is currently deliberating how much to accelerate its taper timetable, with an eye toward gaining the flexibility to hike rates sooner than previously planned. The hawkish turn foreshadowed by Chair Powell two weeks ago in Congressional testimony unsettled markets somewhat, but it is important to note that monetary policy settings are merely on track to become less accommodative – they are nowhere near crossing the line to restrictive and will not approach it anytime soon. Investors can be certain that markets will enjoy ample policy support across all of 2022 and we expect that equities will still be in a bull market when Mr. and Ms. X return to discuss the outlook for 2023. We are on board with the BCA consensus as detailed in the Bank Credit Analyst’s 2022 outlook.2 Early indications suggest that the Omicron variant will not be enough of a threat to provoke a negative growth surprise and we expect that the pandemic will recede in importance as the year unfolds. As it fades, supply chains should become less snarled, easing the near-term pressures that have been pushing prices higher. We expect that markets are overestimating inflation in the near term and that growth will be robust in the US and other developed economies. Despite the dialing back of some accommodation, monetary policy will remain easy, supporting economic activity and market valuations. We foresee another year of solidly positive excess returns for risk assets. The Economy Is Firing On All Cylinders You wouldn’t necessarily know it to talk with investors, much less consumer confidence survey respondents, but aggregate demand is surging and ought to remain robust going forward. Households are in fantastic shape. Although their net worth growth slowed in the third quarter, its 13% annualized seven-quarter (1Q20 through 3Q21) pace is within a whisker of all-time highs (Chart 1). They have accumulated $2.3 trillion of excess savings since the pandemic began and have plenty of capacity to borrow to augment their spending power. Just about anyone who wants a job can have one: the ratio of job openings to unemployed workers is making new highs (Chart 2) and the share of people in the labor force filing initial jobless claims is approaching the all-time lows set before the pandemic (Chart 3). Chart 1The Wealth Effect Will Support Consumption

The Wealth Effect Will Support Consumption

The Wealth Effect Will Support Consumption

Chart 2More Jobs Than People Without Them ...

More Jobs Than People Without Them ...

More Jobs Than People Without Them ...

Businesses are on a solid financial footing, as well. Debt as a share of net worth is near the lower end of its typical range since the high yield bond market got going in the late ‘80s (Chart 4). Borrowing costs are scraping all-time lows (Chart 5) and profit margins are wide (Chart 6). Banks and fixed income asset managers are falling all over themselves to lend to businesses and will continue to do so while default rates remain low. Chart 3... And Almost No Layoffs

... And Almost No Layoffs

... And Almost No Layoffs

Chart 4Corporations Have Less Debt And More Equity, ...

Corporations Have Less Debt And More Equity, ...

Corporations Have Less Debt And More Equity, ...

Chart 5... But Debt Has Never Cost Less ...

... But Debt Has Never Cost Less ...

... But Debt Has Never Cost Less ...

Chart 6... And Profit Margins Are Wide

... And Profit Margins Are Wide

... And Profit Margins Are Wide

Financial conditions will remain highly accommodative despite the Fed’s and other major developed world central banks’ moves to make them less easy at the margin. Below-equilibrium policy rates will continue to encourage financed purchases of homes, autos and other durable goods and entice investment via low hurdle rates. If sovereign bond yields rise modestly in 2022 in line with our high-conviction base case, governments won’t feel any pressure to tighten the fiscal screws. That may nourish modern monetary theory fantasies to the ultimate detriment of public finances, but it should ensure that all three engines of domestic demand – households, businesses and government – will hum in 2022. Omicron has reminded everyone that the pandemic is not over, but the shadow it casts on public health and economic activity is set to shrink. Booster shots of the Pfizer vaccine apparently provide effective protection, and Omicron’s mutations will not allow it to evade Merck’s and Pfizer’s soon-to-be-approved antiviral pills. The availability of pills to treat those who contract COVID could possibly be a game-changer in terms of neutralizing its global threat. Distributing shelf-stable pills is vastly simpler than delivering vaccines that need to be transported at temperatures below -70 degrees Fahrenheit. The Earnings Bar Has Been Set Very Low Our constructive view would not translate into risk friendly investment strategy if asset prices already discounted it or were expecting something even better. Just as the economy is on a better path than consumers seem to perceive and investors believe can persist, S&P 500 earnings per share are poised to grow over the next four quarters by more than the bottom-up analyst consensus expects. As compared to the simple annualized run rate of last quarter’s earnings ($215.76, or $53.89 times 4), the analyst consensus is calling for effectively no growth ($215.87) over the four quarters through 3Q22. That is a surprising prediction based on two sets of empirical evidence. First, earnings typically rise outside of recessions (Chart 7). Second, analysts have consistently forecast that forward four-quarter earnings would top the run rate of the last reported quarter’s earnings for four decades (Chart 8). This year, though, analysts have repeatedly called for quarter-over-quarter declines in earnings (Table 1), only to have reported numbers shred their estimates by jaw-dropping margins, just as they have in all six full quarters since COVID-19 arrived (Chart 9). We interpret the phase shift in the magnitude of earnings beats as evidence that companies have surprised themselves by how much they’ve been able to increase efficiency and/or cut costs during the pandemic. Our interactions with the investment community suggest that it has also been surprised but views the gains as one-off events that are unlikely to continue. Chart 7Earnings Declines Outside Of Recessions Are Rare

Earnings Declines Outside Of Recessions Are Rare

Earnings Declines Outside Of Recessions Are Rare

Chart 8This Has Been An Odd Time To Expect 40-Year Lows In Earnings Growth

This Has Been An Odd Time To Expect 40-Year Lows In Earnings Growth

This Has Been An Odd Time To Expect 40-Year Lows In Earnings Growth

Table 1Grim Expectations

2022 Key Views: Stay For One More Round

2022 Key Views: Stay For One More Round

Expectations of sequentially declining earnings would fit if the economy were flirting with falling below stall speed, as it regularly did during the sluggish post-GFC expansion. But they are completely at odds with the Bloomberg economist consensus that GDP will grow at a 5% real annualized rate this quarter and 3.9% in calendar 2022 (Table 2). Over time, S&P 500 revenue growth should converge with nominal GDP growth, so the current expectations for around 10% and 7% annualized nominal GDP growth in 4Q21 and 2022, respectively, are a decent starting point for estimating S&P 500 revenue growth over those periods. While we expect that S&P 500 profit margins have peaked, we do not foresee a sharp decline in 2022, and operating leverage should ensure that high single-digit revenue growth will translate into healthy earnings gains.

Chart 9

Table 2Above-Trend Growth Ahead

2022 Key Views: Stay For One More Round

2022 Key Views: Stay For One More Round

Bottom Line: The S&P 500 should have no trouble topping consensus estimates that foresee next to no growth in earnings over the next four quarters. There is ample room for corporate earnings to surprise to the upside. Our Major Disagreement With Markets Differences of opinion make markets and our biggest one pertains to the future direction of interest rates. We think the widespread conviction that the Fed will be unwilling or unable to raise the fed funds above 2%, if that, lest it crush financial markets and the real economy is way off base. The majority of investors seem to have taken the decade between the crisis and the pandemic as evidence that rates will remain very low for very long. Many of them must be buying the longer end of the Treasury curve in anticipation that an expedited liftoff date is the first step on the path to the next recession (Chart 10). Chart 10The Bond Market Sees Ice, Not Fire

The Bond Market Sees Ice, Not Fire

The Bond Market Sees Ice, Not Fire

The risk asset selloff that ensued in December 2018 after the FOMC marched the fed funds rate up to 2.5% looms large in the markets’ minds and feeds the widespread view that an ambitious program of rate hikes will pull the rug out from under financial assets and the economy. Many investors have also been conditioned by the post-crisis decade to assume that inflation cannot exceed 2% for a sustained period. The market view is rooted in honest-to-goodness evidence, but we think it is of little relevance now, given the way the massive pandemic fiscal stimulus programs have altered the backdrop. In the space of thirteen months from March 2020 through March 2021, Congress passed bills injecting over $5 trillion of aid – 25% of a year’s GDP – into the economy. The Herculean effort contrasted sharply with the skittish disbursement of less than 5% of GDP on the Bush and Obama administrations’ watch from 2008 through 2010. The aftermath of the crisis demonstrated that even multiple rounds of QE do not by themselves trigger inflation, especially if demoralized households and businesses are disinclined to borrow money to consume or invest, and chastened banks are subjected to regulatory strictures forcing them to maintain sizable new capital buffers and discouraging them from making any but plain-vanilla loans to highly rated borrowers. The Bernanke Fed’s three rounds of QE presumably tamped down interest rates, but the cash that bought the Treasury and agency securities barely tiptoed into the wider world before the primary dealer banks sent it right back to the Fed as excess reserves. With banks hiding their QE money under the mattress, the money supply didn’t expand in any notable way after the crisis. Thanks to Congress’ series of 2020-21 helicopter drops, the money supply has been growing at rates that would make the late Paul Volcker’s head spin (Chart 11). Inflation is fiendishly more complicated than Milton Friedman’s always-and-everywhere dictum suggests, but there’s now a whole lot of money chasing a limited amount of goods, services and assets. We expect that a receding pandemic will allow greater quantities of goods and services to be produced, and that securities underwriters and their clients are hard at work ramping up asset supply, but inflation has far more of a chance to gain traction now than it did in the decade before the pandemic. Chart 11Bringing "Always And Everywhere" Back Into Vogue?

Bringing "Always And Everywhere" Back Into Vogue?

Bringing "Always And Everywhere" Back Into Vogue?

We therefore think the lower-for-longer and lower-for-ever crowd will find itself offsides at some point in the next few years. We do not think it will get its comeuppance in 2022, however, as we see long yields rising only modestly, with the 10-year Treasury yield ending next year at 2-2.25%. Though we expect the fed funds rate will end the upcoming hiking cycle well north of 2%, bringing about the end of the bull markets in equities and credit, and quite possibly inducing the next recession, we do not think markets will abandon their new-normal rates view by the end of next year. This story will be continued, likely with a greater sense of urgency, in our 2023 outlook. Investment Recommendations Consistent with the foregoing, we make the following recommendations for 2022: Overweight equities in multi-asset portfolios. Although they are not cheap, and may experience a turbulent ride in 2022 as inflation concerns wax and wane, COVID-19 infections periodically surge and the Fed tries to adjust its messaging and actions on the fly, stocks should continue to generate sizable positive excess returns over Treasuries and cash. Overweight cyclical sectors and underweight defensive sectors within equity portfolios. If we’re right to be constructive on the global economy, Energy, Industrials, Materials and Financials are better positioned to benefit than Health Care, Staples and Utilities. Overweight small-cap equities versus large-cap equities. The S&P 600 SmallCap Index has greater exposure to our cyclicals-over-defensives call and our US Equity Strategy colleagues highlight that its constituents are cheaper than the S&P 500’s and are projected to have better earnings growth. Adding small-cap exposure to equity portfolios aligns with our constructive view on the economy and markets. Underweight fixed income in multi-asset portfolios. Underweight Treasuries within bond portfolios. Maintain below-benchmark duration within bond portfolios. Though we do not expect the bond market to see things entirely our way next year, we think the long end of the yield curve will shift out somewhat. We therefore have little appetite for duration and Treasuries and expect spread product will outperform Treasuries and high-yield corporate bonds will outperform investment-grade corporates. Consider hybrid alternatives to traditional fixed income securities. When we roll out our multi-asset ETF portfolio next month, it will include a hybrid bucket of income-generating assets to help multi-asset investors seeking income find low-beta destinations with a fighting chance of generating positive real total returns. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 Please see the December 14, 2020 US Investment Strategy Report, "2021 Key Views: It’s The Policy, Stupid." 2 Please see the December 2021 Bank Credit Analyst, "OUTLOOK 2022: Peak Inflation – Or Just Getting Started?"

Highlights 1. How will the pandemic resolve? 2. Will services spending recover to its pre-pandemic trend? 3. Will we spend our excess savings? 4. How will central banks react to inflation? 5. Will cryptocurrencies continue to eat gold’s lunch? 6. How fragile is Chinese real estate? 7. Will there be another shock? Fractal analysis: Personal goods versus consumer services. Feature Chart of the WeekWill Services Spending Recover To Its Pre-Pandemic Trend?

Will Services Spending Recover To Its Pre-Pandemic Trend?

Will Services Spending Recover To Its Pre-Pandemic Trend?

“Judge a man by his questions, not by his answers” The quotation above is often misattributed to Voltaire instead of its true author, Pierre-Marc-Gaston de Lévis. Irrespective of the misattribution, we agree with the maxim. Asking the right questions is more important than finding answers to the wrong questions. In this vein, this report takes the form of the seven crucial questions for 2022 (and our answers). 1. How Will The Pandemic Resolve? As new variants of SARS-CoV-2 have arrived like clockwork, the number of new global cases of infection and the virus reproduction rate have formed a near-perfect mathematical ‘sine wave’. This near-perfect sine wave will propagate into 2022 (Chart I-2). Chart I-2The Pandemic's Sine-Wave Will Propagate Into 2022

The Pandemic's Sine-Wave Will Propagate Into 2022

The Pandemic's Sine-Wave Will Propagate Into 2022

But how will this sine wave of infections translate into mortality, morbidity, and stress on our healthcare systems? As we explained in RNA Viruses: Time To Tell The Truth, the answer depends on the specific combination of contagiousness, immuno-evasion, and pathogenicity of each variant. Yet none of this should come as any surprise. Flus and colds also come in waves, which is why we call them flu and cold seasons. And the morbidity of a given flu and cold season depends on the aggressiveness of that season’s flu and cold variant. So, just like the flu and the cold, Covid will become an endemic respiratory disease which comes in waves. The trouble is that our under-resourced health care systems can barely cope with a bad flu season, let alone with an additional novel disease that can be worse than the flu. Hence, until we add enough capacity to our healthcare systems, expect more disruptions to economic activity from periodic non-pharmaceutical interventions such as travel bans, vaccine passports, and face-mask mandates. 2. Will Services Spending Recover To Its Pre-Pandemic Trend? The pandemic has given us a crash course in virology and epidemiology. We now understand antigens, antibodies, and ‘reproduction rates.’ We understand that a virus transmits as an aerosol in enclosed unventilated spaces, and that singing, and yelling eject this viral aerosol. We understand that vaccinations for RNA viruses have limited longevity, do not prevent reinfections, and that certain environments create ‘super-spreader’ events. Armed with this new-found awareness, a significant minority of people have changed their behaviour. Services which require close contact with strangers – going to the dentist or in-person doctors’ appointments, going to the cinema or to amusement parks, or using public transport – are suffering severe shortfalls in demand. Given that this change in behaviour is likely long-lasting, demand for these services is unlikely to regain its pre-pandemic trend in 2022 (Charts I-3 - I-6). Chart I-3Dental Services Are Far Below The Pre-Pandemic Trend

Dental Services Are Far Below The Pre-Pandemic Trend

Dental Services Are Far Below The Pre-Pandemic Trend

Chart I-4Physician Services Are Far Below The Pre-Pandemic Trend

Physician Services Are Far Below The Pre-Pandemic Trend

Physician Services Are Far Below The Pre-Pandemic Trend

Chart I-5Recreation Services Are Far Below The Pre-Pandemic Trend

Recreation Services Are Far Below The Pre-Pandemic Trend

Recreation Services Are Far Below The Pre-Pandemic Trend

Chart I-6Public Transportation Is Far Below The Pre-Pandemic Trend

Public Transportation Is Far Below The Pre-Pandemic Trend

Public Transportation Is Far Below The Pre-Pandemic Trend

Therefore, to keep overall demand on trend, spending on goods will have to stay above its pre-pandemic trend. This will be a tough ask. Durables, by their very definition, last a long time. Even clothes and shoes, though classified as nondurables, are in fact quite durable. Meaning that are only so many cars, iPhone 13s, gadgets, clothes and shoes that any person can own before reaching saturation. If, as we expect, spending on goods falls back to its pre-pandemic trend, but spending on services does not recover to its pre-pandemic trend, then there will be a demand shortfall in 2022 (Chart of the Week). 3. Will We Spend Our Excess Savings? If spending falls short of income – as it did through the pandemic – then, by definition, our savings have gone up. Many people claimed that this war chest of savings would unleash a tsunami of spending. Well, it didn’t. And, it won’t. Previous episodes of excess savings in 2004, 2008, and 2012 had no impact on the trend in spending (Chart I-7).

Image

The explanation comes from a theory known as Mental Accounting Bias. The theory states that we segment our money into different accounts, which are sometimes physical, sometimes only mental, and that our willingness to spend money depends on which mental account it occupies. This contrasts with standard economic theory which assumes that money is perfectly fungible, meaning that a dollar in a current (checking) account is no different to a dollar in a savings or investment account. In practice, money is not fungible, because we attach different emotions to our different mental accounts. A dollar in our current account we will gladly spend, but a dollar in our savings account we will not spend. Hence, the moment we move the dollar from our current account into our savings account, our willingness to spend it collapses. This explains why consumption trends have no connection with windfall income receipts once those income receipts end up in our savings mental or physical account. Pulling all of this together, the war chest of savings accumulated during the pandemic is unlikely to change the overall trend in spending. 4. How Will Central Banks React To Inflation? The real story of the current ‘inflation crisis’ is that while goods and commodity prices have surged exactly as expected in a positive demand shock, services prices have not declined as would be expected in the mirror-image negative demand shock. The result is that aggregate inflation has surged even though aggregate demand has not (Chart I-8 and Chart I-9). Chart I-8Goods Prices Have Reacted To A Positive Demand Shock...

Goods Prices Have Reacted To A Positive Demand Shock...

Goods Prices Have Reacted To A Positive Demand Shock...

Chart I-9...But Service Prices Have Not Reacted To A Negative Demand Shock

...But Service Prices Have Not Reacted To A Negative Demand Shock

...But Service Prices Have Not Reacted To A Negative Demand Shock

Why have services prices remained resilient despite a massive negative demand shock? One answer, as explained in question 2, is that much of the shortfall in services demand is due to behavioural changes, which cannot be alleviated by lower prices. If somebody doesn’t go to the dentist or use public transport because he is worried about catching Covid, then lowering the price will not lure that person back. In fact, the person might interpret the lower price as a signal of greater risk, and might become more averse. In technical terms, the price elasticity of demand for certain services has flipped from its usual negative to positive. This creates a major problem for central banks, because if the price elasticity of services demand has changed, then surging aggregate inflation is no longer a reliable indicator of surging aggregate demand. To repeat, inflation is surging even though aggregate demand is barely on its pre-pandemic trend. Hence in 2022, central banks face a Hobson’s choice. Choke demand that does not need to be choked, or turn a blind eye to inflation and risk losing credibility. 5. Will Cryptocurrencies Continue To Eat Gold’s Lunch? Most of the value of gold comes not from its economic utility as a beautiful, wearable, and electrically conductive metal, but from its investment value as a hedge against the debasement of fiat money. The multi-year investment case for cryptocurrencies is that they are set to displace much of gold’s investment value. Still, to displace gold’s investment value, cryptocurrencies need to match its other qualities: an economic utility, and limited supply. A cryptocurrency’s economic utility comes from its means of exchange for the intermediation services that its blockchain provides. For example, if you issue a bond or smart-contract using the Ethereum blockchain, then you must pay in its cryptocurrency ETH. Which gives ETH an economic utility. Furthermore, the number of blockchains that will succeed as go-to places for intermediation services will be limited, and each cryptocurrency has a limited supply. Thereby, the supply of cryptocurrencies that have a utility is also limited. With an economic utility, a limited supply, and drawdowns that are becoming smaller, cryptocurrencies can continue to displace gold’s dominance of the $12 trillion anti-fiat investment market. Therefore, the cryptocurrency asset-class can continue its strong structural uptrend, albeit punctuated by short sharp corrections (Chart I-10). Chart I-10Cryptocurrencies Will Continue To Displace Gold's Investment Value

Cryptocurrencies Will Continue To Displace Gold's Investment Value

Cryptocurrencies Will Continue To Displace Gold's Investment Value

The corollary is that the structural outlook for gold is poor. 6. How Fragile Is Chinese Real Estate? A decade-long surge in Chinese property prices has lifted Chinese valuations to nosebleed levels. According to global real estate specialist Savills, prime real estate yields in China’s major cities are now barely above 1 percent, and the world’s five most expensive cities are all in China: Hangzhou, Shenzhen, Guangzhou, Beijing, and Shanghai (Chart I-11).

Chart I-11