Equities

Highlights The market pricing of the ECB is too aggressive. More so than in the US, temporary factors explain the European inflation surge. Energy, taxes, and base effects account for the bulk of the price increases. In contrast to supply shortages, European labor shortages are small and slack will limit wage growth. Despite the lack of near-term inflation risks, European growth prospects are significantly stronger than last decade. As a result, European inflation will settle at a higher level than in the 2010s and will increase durably in the second half of the 2020s. The inflation curve will steepen, as will the yield curve. Banks will continue to outperform, especially compared to the insurance sector. A tactical opportunity to buy European high-yield corporates has emerged. In France, Macron remains the favorite for the 2022 presidential election. Feature Last week’s ECB meeting did nothing to curb the impression among traders that the ECB will start removing monetary accommodation in 2022. The implied policy rate stands at -0.25% one year from now and -0.08% in two years. Meanwhile, Italian 10-year spreads over Germany have increased to 127bps, their highest level since November 2020. This market action rests on the perception that inflationary pressures in the Euro Area are durable. While this line of reasoning may have credence in the US, it is weaker across the Atlantic where the economy shows fewer signs of genuine inflationary pressure. Moreover, the deterioration in peripheral financial conditions further limits the ability of the ECB to withdraw accommodation without a financial accident. Meanwhile, the NGEU program has created a climate where the likelihood of a premature and excessive fiscal tightening is low. Thus, the weak European growth of the past decade will not be repeated. When considering these inflationary and fiscal views, it becomes apparent that the European yield curve has room to steepen further. Consequently, European banks remain attractive and should be bought on dips, especially relative to insurance companies. The EONIA Curve Is Too Aggressive The sudden increase in interest rate hikes priced in the EONIA curve is a consequence of the rapid acceleration in European realized inflation and CPI swaps. Neither are durable. Headline HICP has surged to 4.1% and core CPI towers at 2.1%, their highest reading in 13 and 19 years, respectively. These surges are the reflection of transitory factors: Chart 1The Energy Path-Through

The Energy Path-Through

The Energy Path-Through

Energy prices are lifting HICP and are sipping through to core CPI. Inflation for electricity, gas, and fuel has reached 14.7% and the energy CPI is at 23.5%. Both are moving in line with headline and core CPI (Chart 1). Now that Brent oil and natural gas have increased four and twenty folds since Q2 2020, respectively, their ability to contribute as much to overall inflation has decreased because they are unlikely to appreciate as much again. While oil prices may rise again here, European natural gas will decline meaningfully in the coming months. Tax increases are another important driver of core CPI. Core inflation with constant taxes stand at 1.37%, which is 0.67% below core CPI. In other words, while core CPI is high by the standard of the past decade, once we adjust for tax increases, it stands at normal levels (Chart 2). Base-effects are another dominant ingredient of the surge in European core CPI. The annualized two-year rate of change of the Eurozone’s core CPI stands at 1.11%, which is within the norm of the past seven years and below the rates experienced prior to 2014. In comparison, the annualized two-year core inflation in the US is 2.87%, well outside the range of the past decade (Chart 3). Chart 2Death And Taxes

Death And Taxes

Death And Taxes

Chart 3Controlling For The Base Effect

Controlling For The Base Effect

Controlling For The Base Effect

Inflation remains narrowly based. The Euro Area trimmed-mean CPI stands at 0.22%, or 1.82% below core CPI. Meanwhile, in the US, trimmed-mean CPI has reached 3.5% or 0.5% below core CPI (Chart 4). These figures confirm that the Eurozone inflation increase is more muted and narrower than that of the US. Wages are not experiencing any meaningful shock so far. Negotiated wages are growing at a 1.7% annual rate; meanwhile, the Atlanta Fed Wage Tracker is expanding at 3.6% and is rising even more steadily for low-skill jobs (Chart 5). Chart 4Much More Narrow Than In The US

Much More Narrow Than In The US

Much More Narrow Than In The US

Chart 5Limited Wage Pressures

Limited Wage Pressures

Limited Wage Pressures

Continental Europe’s more limited inflationary pressures compared to the US are a consequence of policy decisions during the crisis. The Euro Area fiscal stimulus in 2020 and 2021 amounted to 11% of 2019 GDP, but output declined by 15% in Q2 2020 and suffered a second dip in Q1 2021. Meanwhile, US fiscal packages amounted to 25% of 2019 GDP, while GDP declined by 10% in Q2 2020. Consequently, the Eurozone’s output gap is -4.1% of GDP, while that of the US has essentially closed. The contrasting nature of the stimuli accentuated the different outcomes created by their respective size. In Europe, governmental support focused on keeping people at work, which left aggregate supply unchanged. In the US, public programs allowed jobs to disappear, but they placed money directly in the pockets of consumers, which caused aggregate demand to rise relative to aggregate supply. In this context, a wage-price spiral is unlikely to develop in Europe as long as the energy crisis does not continue through 2022.

Chart 6

First, the labor shortage problems are less acute in the Eurozone than in the US or the UK. Chart 6 highlights the factors limiting production in various industries. In the industrial sector, the “labor shortages” category has grown, but pale compared to the role of “material and equipment shortages” as a problem. In the services sector, the “weak demand” and “other” categories are greater obstacles to production than the “labor” factor, which remains at Q1 2020 levels (Chart 6, middle panel). Only in the construction sector are “labor shortages” the chief problem, but they still hurt production less than “insufficient demand” did in February 2021, when real estate prices were already strong (Chart 6, bottom panel). Second, labor market slack remains comparable to 2011 levels, when the ECB erroneously increased interest rates to fight energy-driven inflation (Chart 7). Additionally, the rise in persons available to work but not currently seeking employment represent 75% of the increase in labor market slack since Q4 2019. At the crisis peak in Q2 2020, this category accounted for 105% of the increase in labor market slack. This suggests that, as the vaccination campaign continues to progress across the continent; as households use up their savings; and as government supports ebb across Europe, a large share of those who are a part of the labor market slack will start looking for jobs again, which will increase the supply of workers and limit wage pressures. If traders are overly worried about realized inflation remaining high in Europe, they are also over-emphasizing some CPI swap measures that trade above 2%. CPI swaps only tell one part of the inflation expectations story, because they are one and the same as energy prices. Elevated energy prices sap spending power in the rest of the economy, if other inflation expectation measures remain well anchored; thus, rising energy inflation rarely translates into broad-based pricing pressure. For now, our Common Inflation Expectation measure for the Eurozone, based on the New York Fed’s method for the US, is still toward the low-end of its distribution, even though it includes CPI swaps (Chart 8). This confirms that the energy crisis remains a relative-price shock and that it is unlikely to lead to a generalized inflation outburst in the Euro Area.

Chart 7

Chart 8Different Inflation Expectations

Different Inflation Expectations

Different Inflation Expectations

Bottom Line: Markets expect a first 10bps ECB rate hike by June 2022 and the deposit rate to be 25bps higher by September 2023. However, unlike in the US, there are few signs that European inflation reflects anything more than higher energy prices, rising taxes, and base effects. Moreover, the stories in the press of labor shortages are exaggerated, while broad-based inflation expectations are not unmoored. In this context, we lean against the EONIA pricing and expect the ECB to increase rates in 2024, at the earliest. Fiscal Policy Unlike Last Decade The 2010s were a lost decade for Europe. GDP only overtook its 2008 peak in 2015. Today, GDP is recovering much faster from the recession than it did twelve years ago, and it is unlikely to relapse as it did back then. Chart 9A Lost Decade

A Lost Decade

A Lost Decade

The European economic underperformance last decade was rooted in fiscal policy. As the top panel of Chart 9 highlights, the fiscal thrust during the GFC was minimal, at 1.3% of GDP, and was rapidly followed by a negative fiscal thrust. Moreover, the ECB unduly tightened policy in 2011 and left peripheral spreads fester at elevated levels between 2011 and 2014. This combination substantially hurt demand, especially in the European periphery. Capex proved particularly vulnerable. It is derived demand and therefore adds considerable variance to GDP. Faced with strong policy headwinds, its share of GDP plunged for most of the decade, which greatly contributed to the European economic malaise (Chart 9, bottom panel). According to the IMF, the Eurozone fiscal thrust will not exert the same drag as it did last decade; hence, capex is also unlikely to repeat its mediocre performance. Instead, the poorer Eastern and Central European economies as well as the weaker peripheral nations will receive a significant fillip from the NGEU program (Chart 10). When the NGEU grants and loans as well as the EU’s Multiannual Financial Framework funds are aggregated together, the EU will provide EUR1.9 trillion funding (adjusted for inflation) to member states over the next five years (Table 1). These sums will prevent any meaningful fiscal retrenchment from taking place.

Chart 10

Table 1Bigger Spending

To Hike Or Not To Hike?

To Hike Or Not To Hike?

The NGEU funds will be particularly supportive for capex. The Recovery and Resilience Facility (RRF), which will be the main instrument to deliver funds across Europe, is heavily weighted toward green transition, reskilling, and digital transformation (Chart 11, top panel). Practically, this spending focuses on electrical, power, water, and broadband infrastructures, as well as renovation and modernization projects (Chart 11, bottom panel). This reinforces the notion that capex is unlikely to follow the same trajectory it did last decade.

Chart 11

The implication of more accommodative fiscal policy and more robust capex is that the European output gap will close much faster than it did after the GFC. Hence, even if we expect the current inflation spike to pass next year, inflation will ultimately settle higher than it did last decade. Moreover, in the second half of the 2020s, European inflation will trend higher as full employment will be achieved. Bottom Line: The Euro Area is unlikely to experience another lost decade like the previous one. European trend growth remains low, but fiscal policy will not be as tight. Consequently, capex will not be as depressed, especially because the NGEU grants will greatly incentivize investments in certain sectors of the economy. As a result, the output gap will close much faster than it did in the 2010s. Moreover, once the current pandemic-driven inflation surge passes, CPI will settle at a higher level than it did last decade and will trend higher durably in the second half of the 2020s. Investment Implications Three main conclusions can be derived from our expectation on European inflation and growth dynamics over the coming decade. First, the inflation yield curve will steepen meaningfully. Today, near-term CPI swaps are lifted by energy markets and 2-year CPI swaps are 20bps above 20-year CPI swaps (Chart 12). From 2012 to 2020, 20-year CPI swaps stood between 30 bps and 150 bps above short maturity ones. Second, a steeper inflation curve, along with greater inflation risk toward the end of the decade will cause the European term premium to normalize from its -1.21% level. This will allow German 10-year yields to rise and the European yield curve to steepen (Chart 13). Chart 12Long-Term Inflation Expectations Have Upside

Long-Term Inflation Expectations Have Upside

Long-Term Inflation Expectations Have Upside

Chart 13A Steeper German Yield Curve

A Steeper German Yield Curve

A Steeper German Yield Curve

Third, higher German yields and a steeper curve will greatly benefit European banks (Chart 14, top panel). This pattern will be especially evident against insurance firms, which have massively outperformed deposit-taking institutions over the past seven years as yields fell (Chart 14, bottom panel). Additionally, banks’ balance sheets have become more robust than they once were and NPLs are unlikely to rise meaningfully as a result of government guarantees and easy fiscal policy (Chart 15). Investors should go long bank/short insurance on a cyclical basis. Chart 14Long Bank / Short Insurance

Long Bank / Short Insurance

Long Bank / Short Insurance

Chart 15Imporving Balance Sheets

Imporving Balance Sheets

Imporving Balance Sheets

A Tactical Buying Opportunity In European High-Yield Corporate Bond Market Chart 16Tactical Buying Opportunity

Tactical Buying Opportunity

Tactical Buying Opportunity

The 40 basis points widening in European high-yield spreads has created a tactical buying opportunity. Inflation fears spurred by rising energy prices and by input prices are the likely culprit behind the recent spread widening (Chart 16). Although US junk spreads have already narrowed significantly, European high-yield corporate bond spreads are still 40 bps wider than at the beginning of September. The 12-month breakeven spread, which measures the degree of spread widening required over a 12-month period for corporate bond returns to break even with a duration-matched position in government bond securities, now ranks at its 20th percentile, from 10th (Chart 16, second panel). Spreads will narrow back to near post-crisis lows before year-end on both an absolute and breakeven basis: First, monetary and fiscal policy remain very accommodative. Importantly, Spain and Italy will receive large shares of the NGEU funds until 2026. Second, growth will remain above trend despite recent inflation worries. Third, the European default rate is still falling, leaving the worst of the default cycle behind (Chart 16, third panel). Finally, our bottom-up Corporate Health Monitor signals improving corporate health, which historically coincides with narrowing spreads (Chart 16, bottom panel). Bottom Line: The recent widening in European high-yield spreads represents a short window of opportunity to buy the dip. Beyond this timeframe, a more cautious approach toward European credit is appropriate, as the ECB will become less active in the bond market. A French Update

Chart 17

Last month, French President Emmanuel Macron unveiled a EUR30 billion investment plan aimed at supporting and fostering industrial and tech “champions of the future.” This new plan comes on top of the EUR100 billion recovery package that was announced in September 2020 to face the pandemic. While these investments will be made across many sectors of the French economy, the focus will be the French tech and energy sectors (Chart 17, top panel). This announcement comes six months before the next presidential election and amid the emergence of Eric Zemmour as a potential far-right candidate. However, Zemmour’s candidacy is unlikely to alter our expectation that Macron will be re-elected in 2022. Recent polls that include Zemmour as a potential candidate in the first-round show that he is appealing to Marine Le Pen’s voter base (Chart 17, bottom panel). Meanwhile, former Prime Minister Edouard Philippe—who would have made a formidable opponent to Macron had he decided to run—announced the creation of his own party with the objective of supporting Macron’s re-election campaign. Chart 18Recent Developments Support These Trades

Recent Developments Support These Trades

Recent Developments Support These Trades

These political developments come as the French health and economic picture keeps improving. Although the vaccination pace has slowed in France, 68% of the population is fully vaccinated and 76% of the population has received at least one dose. Thus, the healthcare system continues to weather well recent COVID waves. Moreover, business confidence remains robust and reached its highest reading since July 2007, despite supply issues holding back production. The French jobs market is also recovering, with the unemployment rate expected to fall to 7.6% in Q3 from 8% in Q2. The introduction of a new investment plan, the emergence of a far-right candidate and Edouard Philippe’s newfound support, and the COVID-19 and economic developments bode well for President Macron’s chances at re-election. This implies additional French reforms over the next five years that aim to suppress unit labor costs and to make French exports more competitive vis-à-vis their main competitor, Germany. As a result, investors should overweight French industrial stocks relative to German ones (Chart 18, top panel). Meantime, additional investment in the French tech is bullish for a sector that is inexpensive relative to its European peers. Overweight French tech equities relative to European ones (Chart 18, panel 2 and 3). Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Jeremie Peloso, Associate Editor JeremieP@bcaresearch.com Tactical Recommendations

To Hike Or Not To Hike?

To Hike Or Not To Hike?

Cyclical Recommendations

To Hike Or Not To Hike?

To Hike Or Not To Hike?

Structural Recommendations

To Hike Or Not To Hike?

To Hike Or Not To Hike?

Closed Trades

Image

Currency Performance Fixed Income Performance Equity Performance

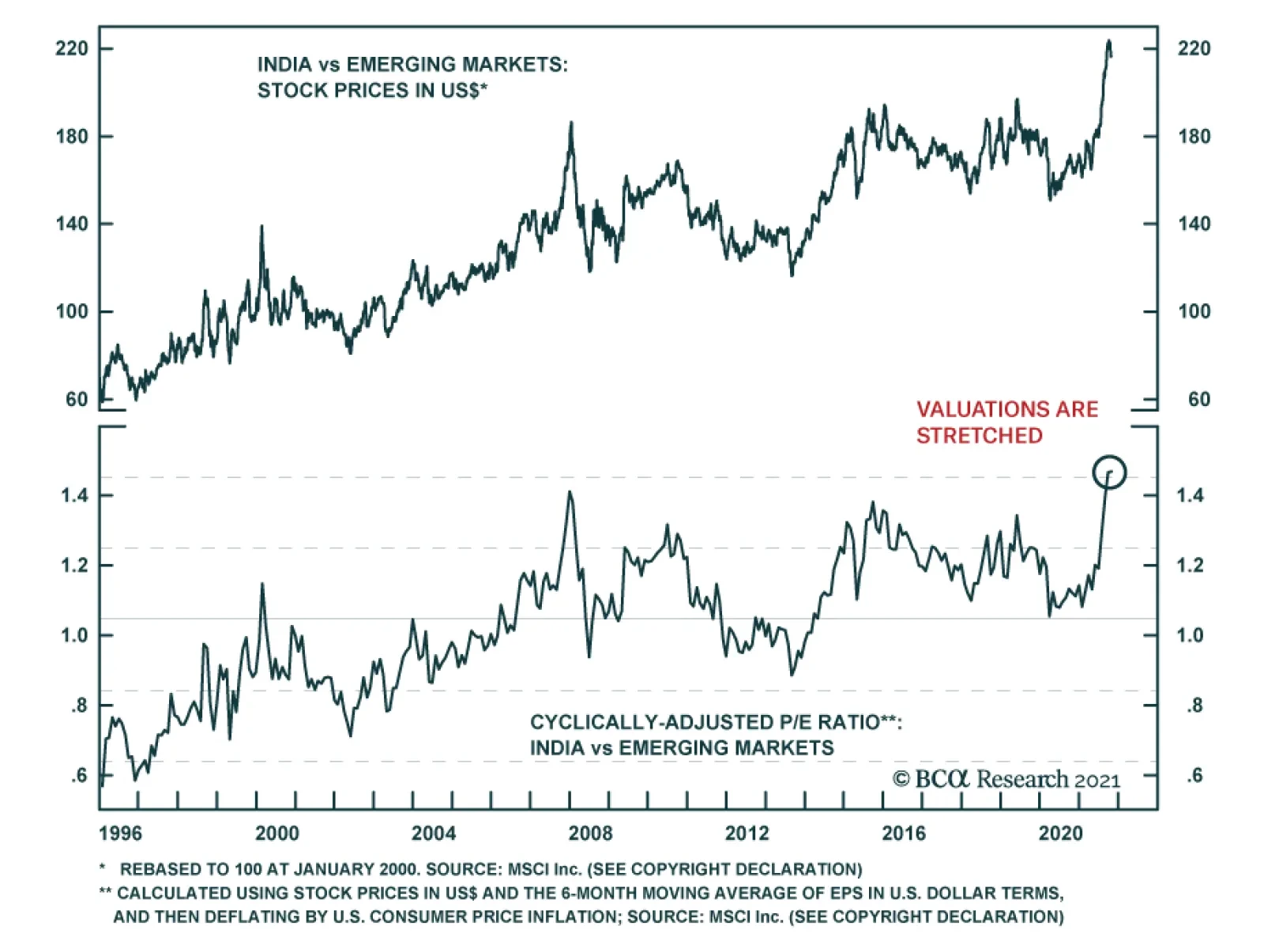

The rally in Indian equities appears to be losing some steam. The MSCI India index is down nearly 4% over the past two weeks. This follows a spectacular 26% rally since Q2. The recent slump comes amid concerns that valuations are getting stretched and news…

In this report we examine the risk of stagflation by comparing the current environment to that of the late-1960s and 1970s. Today, investors cannot rule out the possibility of a stagflationary outcome, for four reasons: long-term household inflation expectations have risen significantly over the past year; fiscal policy has been expansionary; monetary policy will remain expansionary at the Fed’s projected terminal Fed funds rate; and component shortages and price increases linked to energy market and supply chain disruptions may persist or worsen over the coming year. However, the strong demand-pull inflationary dynamics that existed in the late-1960s were mostly absent in the lead-up to the pandemic, supply-chain issues are in part due to strong goods demand and supply disruptions that will eventually dissipate, and economic agents do not expect severe price pressures to persist beyond the pandemic. On balance, this points to a stagflationary outcome over the coming 6-24 months as a risk, but not a likely event. Investors should use the Misery Index, which is the sum of the unemployment rate and headline PCE inflation, as a real-time stagflation indicator. The Misery Index underscores that the US economy is unlikely to experience true stagflation unless the unemployment rate rises. A portfolio of the US dollar, the Swiss Franc, and industrial commodities may serve as a useful hedge for investors who are concerned about absolute return prospects in a world in which long-maturity bond yields are rising and risks of stagflationary dynamics are present. Chart II-1The Misery Index Reflects The Risk Of Stagflation

The Misery Index Reflects The Risk Of Stagflation

The Misery Index Reflects The Risk Of Stagflation

Over the past several weeks, concerns about a possible return to 1970s-style stagflation have re-emerged significantly in the minds of many investors. These investors have pointed toward similarities between the current environment and that of the 1970s, including shortages limiting output, a snarled global trade and logistical system, and rising energy prices. Chart II-1 highlights that the US “Misery Index” – the sum of the unemployment rate and headline PCE inflation – rose again over the past several months to high single-digit territory, after having fallen dramatically from April 2020 to February of this year. Panel 2 of Chart II-1 highlights that last year's rise in the Misery Index was driven almost entirely by the unemployment rate, whereas the current level is due to a combination of a modestly elevated unemployment rate and a pronounced acceleration in inflation. The headline PCE deflator has risen above 4%, a level that has not been reached since 1991 during the First Gulf War. In this report, we examine the risk of stagflation by comparing the current environment to that of the late 1960s and 1970s. We conclude that while investors cannot rule out the possibility of a stagflationary outcome, there are important differences that point toward a stagflation outcome over the coming 6-24 months as a risk, not a likely event. We conclude by highlighting assets that may produce absolute returns in a world in which long-maturity bond yields are rising and risks of stagflationary dynamics are present. Revisiting The 1960s And 70s Chart II-2The 1960s Laid The Groundwork For Elevated Inflation

The 1960s Laid The Groundwork For Elevated Inflation

The 1960s Laid The Groundwork For Elevated Inflation

The first step in judging the risk of a return to 1970s-style stagflation is to review, in a detailed way, what caused those conditions. Investors are well aware of the role that two separate energy price shocks played in raising prices and damaging output during this period, but they are less cognizant of the impact that a persistent period of above-trend output and significant labor market tightness had in setting up the conditions for sharply higher inflation. This focus of investors on energy prices partially reflects the fact that the Misery Index increased most visibly in the 1970s and that policymakers in the 1960s may not have realized how extensively economic output was running above its potential. With the benefit of hindsight, Chart II-2 illustrates the extent to which inflationary pressures built up in the 1960s, well before the first oil price shock in 1973. The chart shows that the unemployment rate was below NAIRU – the non-accelerating inflation rate of unemployment – for 70% of the time during the 1960s, and that inflation had already responded to this in the latter half of the decade. Annual headline PCE inflation was running just shy of 5% at the onset of the 1970 recession; it fell to 3% in the aftermath of the recession, but had already begun to reaccelerate in the first half of 1973. Following the 1973/1974 recession, inflation did decelerate significantly, falling from 11-12% to 5% in headline terms, and from 10% to 6% in core terms. But the pace of price appreciation did not fall below 5-6% in the second half of the 1970s, despite a significant and sustained rise in the unemployment rate above its natural rate. The 1975 to 1978 period is especially important for investors to understand, because it is arguably the clearest period of true stagflation in the 1970s. The fact that the Misery Index rose sharply during two major oil price shocks is not particularly surprising in and of itself, given the direct impact of energy prices on headline consumer prices; it is the fact that the index remained so elevated between these shocks, the result of persistently high inflation in the face of significant labor market slack, that is most relevant to investors. There are two reasons that both inflation and unemployment remained high during this period. First, labor market slack was sizeable during these years because the US economy was more energy-intensive in the 1970s than it is today. Chart II-3 highlights that goods-producing employment lagged overall employment growth from late 1973 to late 1977, underscoring that the rise in oil prices significantly impacted jobs growth in energy-intensive industries.

Chart II-3

Second, it is clear that the combination of demand-pull inflation in the late 1960s and the predominantly cost-push inflation of the 1970s led to expectations of persistent inflation among households and firms. The original Phillips Curve, as formulated by New Zealand economist William Phillips in the late 1950s, described a negative relationship between the unemployment rate and the pace of wage growth. Given the close correlation between wage and overall price growth at the time, the Phillips Curve was soon extended and generalized to describe an inverse relationship between labor market slack and overall price inflation. But the experience of the 1970s highlighted that inflation expectations are also an important determinant of inflation, a realization that gave birth to the expectations-augmented (i.e. “modern-day”) Phillips Curve (more on this below). The Stagflation Era Versus Today

Chart II-

Table II-1 presents a stagflation “threat matrix,” representing the Bank Credit Analyst service’s assessment of the various factors that could potentially contribute to a stagflationary environment today, relative to what occurred in the 1960s and 1970s. While we acknowledge that there are some similarities today to what occurred five decades ago, the most threatening factors have been present for a shorter period of time and appear to have a smaller magnitude than what occurred during the stagflationary era. In addition, key factors, such as the visibility available to policymakers and investors about household inflation expectations and the potential output of the economy, would appear to reduce significantly the risk of a stagflationary outcome today. We discuss each of the factors presented in Table II-1 below: Fiscal & Monetary Policy Chart II-4Government Spending Last Cycle Looked Nothing Like The 1960s

Government Spending Last Cycle Looked Nothing Like The 1960s

Government Spending Last Cycle Looked Nothing Like The 1960s

The persistently tight labor market that contributed to the inflationary buildup in the 1960s occurred as a result of easy fiscal and monetary policy. Chart II-4 highlights that the contribution to real GDP growth from government expenditure and investment was very elevated in the 1960s. Chart II-5 shows that a positive output gap in the late 1960s and the first half of the 1970s is well explained by the fact that 10-year US government bond yields were persistently below nominal GDP growth. The relationship between the stance of monetary policy and the output gap only meaningfully diverged in the latter half of the 1970s, during the true stagflationary era that we noted above. Chart II-5Easy Monetary Policy Juiced Aggregate Demand In The 60s And Early 70s

Easy Monetary Policy Juiced Aggregate Demand In The 60s And Early 70s

Easy Monetary Policy Juiced Aggregate Demand In The 60s And Early 70s

Chart II-6Monetary Policy Today Is Extremely Easy

Monetary Policy Today Is Extremely Easy

Monetary Policy Today Is Extremely Easy

Today, it is clear that the stance of fiscal policy has recently been extraordinarily easy, and 10-year US government bond yields have remained well below nominal GDP growth for the better part of the last decade. Relative to estimates of potential nominal GDP growth, 10-year Treasury yields are the lowest they have been since the 1970s (Chart II-6). Ostensibly, this supports concerns that policy might contribute to a stagflationary outcome. These concerns were raised by Larry Summers in March, when he described the Biden administration’s fiscal policy as the “least responsible” that the US has experienced in four decades and warned of the potential inflationary consequences of overheating the economy.1 But there are two important counterpoints to these concerns. First, easy fiscal policy this cycle has followed a period during the last economic cycle in which government spending contributed to the most sustained drag on economic activity since the 1950s. Unlike the 1960s, the unemployment rate has been below NAIRU for only a third of the time over the past decade. In addition, Chart II-7 highlights that fiscal thrust will turn to fiscal drag next year, underscoring the temporary nature of the massive burst in fiscal spending that has occurred in response to the pandemic. Under normal circumstances, the fiscal drag implied by Chart II-7 would substantially raise the risks of a recession next year, but we have noted in previous reports that a significant amount of excess savings remain to support spending and employment. The net impact of these two factors results in a reasonable expectation that the US economy will return to maximum employment next year, but this is a far cry from the 1960s when the unemployment rate was below its natural rate for 70% of the decade.

Chart II-7

Based on conventional measures, US monetary policy has been easy for a decade, but easy monetary policy did not begin to contribute positively to a rise in household sector credit growth last cycle until 2014/2015. This underscores that the natural rate of interest (“R-star”) did fall during the early phase of the last economic expansion. However, we argued in an April report that R-star was likely rising in the latter half of the last expansion,2 and we believe that the terminal Fed funds rate is likely higher than what the Fed is currently projecting, barring any additional negative policy shocks. Thus, while we do not believe that the duration of easy monetary policy over the past decade has laid the groundwork for a major rise in prices, it is now clearly positively contributing to aggregate demand and does risk a future overshoot in prices if long maturity bond yields remain well below the pace of economic growth for a sustained period of time. The Impact Of Shortages Chart II-8Gasoline Shortages Plagued The US Economy In The 1970s

Gasoline Shortages Plagued The US Economy In The 1970s

Gasoline Shortages Plagued The US Economy In The 1970s

Gasoline shortages occurred during the oil shocks of the 1970s and are a key similarity that some investors point toward when comparing the situation today with the stagflationary era. Chart II-8 highlights that the annual growth in real personal consumption expenditures on energy goods and services fell into negative territory on six occasions in the 1970s, although it was most pronounced during the two oil price shocks and their resulting recessions. Today, the impact of shortages appears to be broader than what occurred in the 1970s, but less impactful and not likely to be as long-lasting. Chart II-9 highlights that the OPEC oil embargo of 1973 raised the global oil bill by 2.4% of global GDP and permanently raised the price of oil. The global oil bill will only be fractionally above its pre-pandemic level in 2022, with oil prices at $80/bbl, and, while it is true that US gasoline prices have risen significantly, they are not higher than they were from 2011-2014 (Chart II-10). Chart II-9$80/bbl Oil Is Not Onerous

$80/bbl Oil Is Not Onerous

$80/bbl Oil Is Not Onerous

Chart II-10US Gasoline Prices Are High, But They Have Been Higher

US Gasoline Prices Are High, But They Have Been Higher

US Gasoline Prices Are High, But They Have Been Higher

It is certainly true that global shipping costs have skyrocketed and that this is contributing to the increase in US consumer prices. We estimate, however, that this increase in shipping costs as a share of GDP is no more than a quarter of the impact of the 1973 increase in oil prices, without the attendant negative effects on US goods-producing employment that occurred in the 1970s. If anything, surging shipping costs create an incentive to re-shore manufacturing production, which would contribute positively to US goods-producing employment. We also do not expect the rise in shipping costs to be meaningfully permanent, i.e., shipping costs may ultimately settle at a higher level than they were in late-2019, but at a much lower level than what prevails today. Chart II-11A Tight Labor Market Is Causing Wage Growth To Pick Up

A Tight Labor Market Is Causing Wage Growth To Pick Up

A Tight Labor Market Is Causing Wage Growth To Pick Up

Semiconductor and labor shortages would appear to represent a more salient threat of stagflation in the US, as the domestic production of motor vehicles cannot occur without key inputs and a tight labor market is already contributing to an acceleration in wage growth (Chart II-11). As we noted in Section 1 of our report, auto production significantly impacted growth in the third quarter. However, Chart II-12 highlights that, for now, the breadth of impact of these shortages appears to be limited: the production component of the ISM manufacturing index remains in expansionary territory, industrial production of durable manufacturing excluding motor vehicles and parts has not broken down, and both housing starts and building permits remain above pre-pandemic levels despite this year’s downtrend in permits. Chart II-12Shortages Do Not Yet Seem To Be Broad-Based

Shortages Do Not Yet Seem To Be Broad-Based

Shortages Do Not Yet Seem To Be Broad-Based

A physical shortage of components is a less relevant factor for the services side of the economy, which appears to have re-accelerated meaningfully in October. The services sector is more considerably impacted by shortages in the labor market, which seem to be linked to a still-low labor force participation rate. We noted in our September report that the decline in the participation rate has significantly overshot what would be implied by the ongoing pace of retirements. Chart II-13 highlights that this has occurred not just because of a significant retirement effect, but also because of the shadow labor force (people who want a job but are not currently looking for work) and family responsibilities. We expect that the recent expiry of expanded unemployment insurance benefits, a steady rise in the immunity of the US population, an abating Delta wave of COVID-19, and a likely upcoming reduction in school/classroom closures once the Pfizer/BioNTech vaccine is approved for school-age children will likely ease the labor shortage issue over the coming several months.

Chart II-13

Output Gap Uncertainty It remains a debate among economists why policymakers maintained such easy monetary policy in the 1960s and 1970s, but Chart II-14 highlights that uncertainty about the size of the output gap may have contributed to too-low interest rates. The chart shows the unemployment rate compared with today's estimate of NAIRU, alongside a simple proxy for policymakers’ real time estimate of the natural rate of employment: the cumulative average unemployment rate in the post-war environment. To the extent that policymakers used past averages of the unemployment rate as their guide for NAIRU, Chart II-14 highlights how they may have underestimated the degree to which output was running above its potential level in the 1960s, and would not have even concluded that output was above potential in the early 1970s. Chart II-14Policymakers Overestimated Labor Market Slack In The 60s And 70s

Policymakers Overestimated Labor Market Slack In The 60s And 70s

Policymakers Overestimated Labor Market Slack In The 60s And 70s

Chart II-15Policymakers Know That NAIRU Is Likely At Or Below 4%

Policymakers Know That NAIRU Is Likely At Or Below 4%

Policymakers Know That NAIRU Is Likely At Or Below 4%

Today, the environment is quite different, because the acceleration in wage growth at the tail end of the last expansion gives policymakers and investors a good estimate of where NAIRU is. Chart II-15 highlights that wage growth accelerated in 2018/2019 in response to a sub-4% unemployment rate, which is consistent with both the Fed’s NAIRU estimate of 3.5-4.5% and Fed Vice Chair Richard Clarida’s expressed view that a 3.8% unemployment rate likely constitutes maximum employment (barring any issues with the breadth and inclusivity of the labor market recovery). It is possible that the pandemic has structurally lowered potential output, which could mean that policymakers may no longer rely on the wage growth / unemployment relationship that existed in the latter phase of the last expansion. However, we do not find any credible arguments that would support the notion of a structurally lower level of potential output: the pandemic is likely to end at some point in the not-too-distant future, the negative impact of working-from-home policies on office properties and employment in central business districts is not sizeable,3 and productivity may have permanently increased in some industries because of the likely stickiness of a hybrid work culture. The Behavior Of Inflation Expectations Chart II-16Rising Long-Term Expectations Have Merely Normalized (For Now)

Rising Long-Term Expectations Have Merely Normalized (For Now)

Rising Long-Term Expectations Have Merely Normalized (For Now)

One parallel to the argument that policymakers may have underestimated the degree of labor market tightness in the 1960s and early 1970s is the fact that they did not yet understand that inflation expectations are an important determinant of actual inflation, nor were they able to monitor them even if they did. Most credible surveys of inflation expectations began in the 1980s, and policymakers in the 1960s and 1970s were guided by the original Phillips Curve that solely related inflation to unemployment. Today, policymakers have the experience of the stagflationary episode to serve as a warning not to allow inflation expectations to get out of control, and both policymakers and investors have reliable measures of inflation expectations for households and market-participants. Chart II-16 highlights that households expect significant inflation over the coming year, but also expect prices over the longer term to rise at a pace that is almost exactly in line with their average from 2000-2014. The Rudd Controversy: (Adaptive) Inflation Expectations Do Matter One potential criticism of the idea that inflation expectations are signaling a low risk of higher future inflation has emerged through arguments made by Jeremy Rudd, a Federal Reserve economist. In a recent paper, Rudd questioned the view that households’ and firms’ expectations of future inflation are a key determinant of actual inflation; he suggested instead that relatively stable inflation since the mid-1990s might reflect a situation in which inflation simply does not enter workers’ employment decisions and expectations are irrelevant. Rudd’s paper was primarily addressed to policymakers who view inflation dynamics in a highly quantitative light. A full response to the paper would be mostly academic and thus not especially relevant to investors; however, we would like to highlight three points related to the Rudd piece that we feel are important.4 First, we disagree with Rudd’s argument that the trend in inflation has not responded to changes in economic conditions since the mid-1990s. Chart II-17 highlights that while the magnitude of the relationship has shifted, the trend in inflation relative to a measure of long-term expectations based on prior actual inflation has mimicked that of the output gap. The fact that inflation was (ironically) too high during the early phase of the last economic cycle provides some support for Rudd’s inflation responsiveness view, although we would still point toward the Fed’s strong record of maintaining low and stable inflation, its active communication with the public in the years following the global financial crisis, and the fact that a recovery began and the output gap began to (slowly) close as the best explanation for the avoidance of deflation during that period. Second, we agree with Rudd’s point that regime shifts in inflation’s responsiveness to economic conditions can occur, and that adaptive measures of inflation expectations, and even surveys of inflation, may not capture such a shift in real time. Chart II-18 shows that the 2014-2016 period was a good example of this, when adaptive expectations as well as household survey measures of long-term inflation expectations both lagged the actual decline in inflation that was caused by a collapse in the price of oil. Chart II-17The Trend In Inflation Continues To Respond To Economic Conditions

The Trend In Inflation Continues To Respond To Economic Conditions

The Trend In Inflation Continues To Respond To Economic Conditions

Chart II-18Surveyed Inflation Expectations Can Lag, But This Time They Led

Surveyed Inflation Expectations Can Lag, But This Time They Led

Surveyed Inflation Expectations Can Lag, But This Time They Led

But Chart II-18 also shows that long-term household survey measures of inflation led the rise in actual inflation (and thus our adaptive expectations measure) last year, underscoring that these measures are likely more reliable indicators today of whether a major regime shift is occurring. As noted above, long-term expectations have risen significantly relative to what prevailed prior to the pandemic, but this has merely raised expectations from extraordinarily depressed levels back to the average that prevailed prior to (and immediately after) the global financial crisis. Therefore, household expectations are not yet at dangerous levels. Chart II-19Unit Labor Costs Modestly Lead Inflation, But Are Far From Extreme

Unit Labor Costs Modestly Lead Inflation, But Are Far From Extreme

Unit Labor Costs Modestly Lead Inflation, But Are Far From Extreme

Third, one of the core observations in Rudd’s paper is that unit labor cost (ULC) growth leads the trend in inflation, which he argued was evidence against the idea that expectations of future inflation are a key determinant of actual inflation. Chart II-19 highlights that Rudd is correct that ULC growth modestly leads inflation (especially core inflation), but we disagree with his conclusion that it argues against the importance of expectations. As we noted in Section 2 of our January 2021 Bank Credit Analyst,5 one crucial aspect of the expectations-augmented, or “modern-day” Phillips Curve is that, if inflation expectations are largely formed based on the experience of past inflation, then inflation is ultimately determined by three dimensions of the output gap: whether it is rising or falling, whether it is above or below zero, and how long it has been above or below zero. Our view is that ULC growth is fundamentally linked to slack in the labor market, which is directly incorporated in output gap measures. As we noted above, investors currently have a good estimate of the magnitude of the output/employment gap, meaning that it is possible to track the inflationary consequences of prevailing aggregate demand. As a final point about ULC growth, Chart II-19 highlights that while the five-year CAGR of unit labor costs is currently running at its strongest pace since the global financial crisis, investors should note that it remains well below the levels that prevailed in the late-1960s when persistently above-potential output laid the groundwork for a massive inflationary overshoot. Conclusions And Investment Strategy Our review of the 1960s and 1970s highlights that stagflation is a phenomenon in which supply-side shocks raise prices of key inputs to production, which lowers output and raises unemployment. Energy price shocks in the 1970s occurred after a long period of policy-driven above-trend growth in the 1960s, meaning that both demand-pull and cost-push inflation contributed to stagflation in the 1970s. Today, investors cannot rule out the possibility of a stagflationary outcome, for four reasons: long-term household inflation expectations have risen significantly over the past year; fiscal policy has been very expansionary; monetary policy will remain expansionary at the Fed’s projected terminal Fed funds rate; and component shortages and price increases linked to energy market and supply chain disruptions may persist or worsen over the coming year. Chart II-20It Is Not Stagflation If The Unemployment Rate Continues To Fall

It Is Not Stagflation If The Unemployment Rate Continues To Fall

It Is Not Stagflation If The Unemployment Rate Continues To Fall

However, the strong demand-pull inflationary dynamics that existed in the late-1960s were mostly absent in the lead-up to the pandemic, supply-chain issues are in part the result of strong goods demand and disruptions that are clearly linked to the pandemic (and thus will eventually dissipate), and long-term inflation expectations are behaving differently than short-term expectations, signaling that economic agents do not expect severe price pressures to persist beyond the pandemic. Policymakers also have more visibility about the magnitude of economic / labor market slack than they did during the stagflationary era and better tools to track inflation expectations. On balance, this points to a stagflationary outcome over the coming 6-24 months as a risk, but not as a likely event. Using the Misery Index as real-time stagflation indicator, investors should note that the US economy is not likely experiencing true stagflation unless the unemployment rate rises. Chart II-20 highlights that there is no evidence yet of a contraction in goods-producing or service-producing jobs. Even if goods-producing employment slows meaningfully over the coming few months as a result of component shortages, the unemployment rate is still likely to fall if services spending normalizes, as it would imply that the gap in services-producing employment, which is currently 20% of the level of pre-pandemic goods-producing employment, will continue to close. Investors have been focused on the issue of stagflation because its occurrence would imply a sharply negative correlation between stock prices and bond yields. This is not our base case view, but we have highlighted that months with negative returns from both stocks and long-maturity bonds tend to be associated with periods of monetary policy tightening (or in anticipation of such periods). As we discussed in Section 1 of our report, we do expect the Fed to raise interest rates next year. We do not see a rise in bond yields to levels implied by the Fed’s interest rates projections as being seriously threatening to economic activity, corporate earnings growth, or equity multiples. But the adjustment to higher long-maturity bond yields may unnerve equity investors for a time, implying temporary periods of a negative stock price / bond yield correlation. Table II-2 highlights that, since 1980, commodities, the US dollar, and the Swiss franc have typically earned positive returns during non-recessionary months in which stock and long-maturity bond returns are negative. While the dollar is not likely to perform well in a stagflationary scenario, Chart II-21 highlights that CHF-USD and industrial commodities performed quite well in the late-1970s. As such, a portfolio of these three assets might serve as a useful hedge for investors who are concerned about absolute return prospects in a world in which long-maturity bond yields are rising and risks of stagflationary dynamics are present.

Chart II-

Chart II-21The Swiss Franc and Raw Industrials Did Well During The Stagflationary Era

The Swiss Franc and Raw Industrials Did Well During The Stagflationary Era

The Swiss Franc and Raw Industrials Did Well During The Stagflationary Era

Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Footnotes 1 “Summers Sees ‘Least Responsible’ Fiscal Policy in 40 Years,” Bloomberg News, March 20, 2021. 2 Please see The Bank Credit Analyst “R-star, And The Structural Risk To Stocks,” dated March 31, 2021, available at bca.bcaresearch.com 3 Please see The Bank Credit Analyst “Work From Home “Stickiness” And The Outlook For Monetary Policy,” dated June 24, 2021, available at bca.bcaresearch.com 4 Rudd, Jeremy B. (2021). “Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?),” Finance and Economics Discussion Series 2021-062. Washington: Board of Governors of the Federal Reserve System. 5 Please see The Bank Credit Analyst “The Modern-Day Phillips Curve, Future Inflation, And What To Do About It,” dated December 18, 2021, available at bca.bcaresearch.com

Highlights The circumstances of the pandemic improved in October, but data highlighting the economic consequences of the Delta wave grew more severe. US economic activity slowed meaningfully in the third quarter, driven by lower car sales and a slowdown in services spending. The imminent vaccination of school-aged children, and signs that services activity and spending are increasing, will likely raise labor force participation, boost education employment, and hasten the return of real services spending back to pre-pandemic levels. Investors have the right bond view, but the wrong reason. Investors believe that the Fed will be forced to raise interest rates earlier than it currently expects to prevent an out-of-control rise in prices, whereas it will likely do so because of a quicker return to maximum employment. Bond yields are likely to move higher over the coming year, but this will be driven by real yields, not inflation expectations. Once the Fed begins to raise interest rates, investors should be on the lookout for signs that market expectations for the real natural rate of interest, or “R-star,” are rising. The Fed’s terminal rate projection is well below nominal potential GDP growth, and a gap between these two measures no longer makes sense. Stocks are likely to generate mid-single digit returns next year, which will beat the returns offered by bonds and cash. But stocks will generate much lower returns compared with those enjoyed by investors over the past year. A benign rise in long-maturity bond yields argues for the outperformance of value versus growth stocks over the coming year. Cyclical stocks are now becoming stretched versus defensives on an equally-weighted basis; stay overweight for now, but a downgrade to neutral may be in the cards at some point next year. Feature Chart I-1The Waning Impact Of Delta

The Waning Impact Of Delta

The Waning Impact Of Delta

Over the past month, the focus of investors has shifted from day-to-day developments to the consequences of the Delta wave of the pandemic. Chart I-1 highlights that, while an estimate of the COVID-19 reproduction rates in advanced economies has recently inched higher, it remains below one and hospitalizations continue to trend lower in most major economies. UK hospitalizations have increased over the course of the month, but remain at a level that is a quarter of their January peak – despite an elevated pace of confirmed cases. In the US, both these cases and hospitalizations continue to fall, trends that are likely to be reinforced by the vaccination of children over the coming weeks. A 50-60% vaccination rate for school-aged children would increase the US vaccination rate by 4-5 percentage points. Vaccinating all children at this rate would increase the total vaccination rate by 7-8 percentage points. In combination with a meaningful level of natural immunity, the vaccination of children is likely to bring the US very close to, if not above, the non-accelerating hospitalization rate of immunity (or “NAHRI”).1 The Delta Hangover While the circumstances of the pandemic improved in October, the economic consequences grew more severe. US economic activity slowed meaningfully in the third quarter, as highlighted by yesterday’s advance release. Chart I-2 highlights that durable goods spending subtracted almost three percentage points from Q3 growth, and that most other components of GDP contributed less to growth in Q3 than in Q2.

Chart I-2

The significant slowdown in Q3 growth is disappointing, but several factors point toward the conclusion that it is not likely to be sustained: Chart I-3Services PMIs Are Pointing To A Stronger Q4

Services PMIs Are Pointing To A Stronger Q4

Services PMIs Are Pointing To A Stronger Q4

The Delta wave very likely impacted services spending, which we have highlighted is likely to drive overall consumption over the coming year. Given the ongoing impact of semiconductor shortages on the availability of new cars, it is not surprising that a slowdown in services spending resulted in a significant slowdown in overall growth. After having declined significantly in Q3, Chart I-3 highlights that the US, UK, French, and Japanese October flash services PMI rose anew, underscoring that recent services weakness have been closely linked to the Delta variant of COVID-19 (whose impact is now waning). Chart I-3 also highlights that the US services PMI is currently at a level that has been historically consistent with solid real PCE growth. Finally, while it is true that manufacturing PMIs are being supported by supplier deliveries components, the October output component of the US Markit manufacturing index remained in expansionary territory, as was the case in Germany, Japan, and the UK (despite month-over-month declines in these components). Chart I-4 highlights that Q3’s real GDP reading was highly anomalous relative to the pace of jobs growth in the quarter, based on the relationship between the two since the global financial crisis. In quarters in which real GDP growth was 1% or less than implied by the trendline shown in Chart I-4, real GDP accelerated in the subsequent quarter 80% of the time. In conjunction with a pickup in services activity in October, this suggests that growth will be meaningfully stronger in Q4.

Chart I-4

Chart I-5Global Growth Is Peaking, But A Major Downturn Is Unlikely

Global Growth Is Peaking, But A Major Downturn Is Unlikely

Global Growth Is Peaking, But A Major Downturn Is Unlikely

Chart I-5 shows our global Nowcast indicator, alongside our global LEI. Our Nowcast indicator is a high-frequency measure of economic activity that is designed to predict global industrial production. The chart shows that both the Nowcast and global LEI are declining, but that this decline is occurring from an extremely elevated level. The global economy is at an inflection point in terms of the pace of growth, but Chart I-5 still points to above-trend growth – and certainly not a major cyclical downturn. The expectation of a slowdown in growth in Q3 has significantly raised concerns about a possible return to 1970s-style stagflation in the minds of many investors. We address this topic in depth in this month’s Special Report, and conclude that, while investors cannot rule out the possibility of stagflation, there are important differences that point toward a stagflationary outcome over the coming 6-24 months as a risk, not a likely event. We note in our report that the risk of stagflation can be monitored in real time by tracking the Misery Index, which is the sum of headline PCE inflation and the unemployment rate. Currently, the Misery Index is elevated relative to the average of the past 30 years, but it is meaningfully lower than it was during the latter half of the 1970s. This also underscores that true stagflation is only likely to occur if the unemployment rate rises, which means that the economic and financial market outlook over the coming year is strongly tied to the pace of jobs growth (even more so than usual). Table I-1 presents an industry breakdown of the jobs gap relative to pre-pandemic levels, sorted by industries with the largest gap. The table highlights that leisure and hospitality, government, and education and health services jobs continue to account for two-thirds of the five million jobs gap, with the latter two largely reflecting the same effect: 60% of the government jobs gap is accounted for by state and local government education-related employment.

Chart I-

Chart I-6Leisure And Hospitality Employment Tracks The Hotel Occupancy Rate

Leisure And Hospitality Employment Tracks The Hotel Occupancy Rate

Leisure And Hospitality Employment Tracks The Hotel Occupancy Rate

US education employment has been impacted by school and classroom closures, which we noted above are likely to end once school-aged children are vaccinated against the disease. Chart I-6 highlights that leisure and hospitality employment is clearly predicted by the US hotel occupancy rate, which wobbled over the past few months as a result of the Delta wave of the pandemic. Correspondingly, monthly growth in leisure and hospitality employment slowed in August and September. Taken together, the imminent vaccination of school-aged children and signs that services activity and spending are increasing will likely raise labor force participation, boost education employment, and hasten the return of real services spending back to pre-pandemic levels. The Bond Market Outlook Chart I-7The Market Now Agrees With Us About The Timing Of Fed Rate Hikes...

The Market Now Agrees With Us About The Timing Of Fed Rate Hikes...

The Market Now Agrees With Us About The Timing Of Fed Rate Hikes...

A continued normalization of the labor market over the coming 6-12 months argues in favor of Fed rate hikes next year, which is a view that we have maintained for several months. Recently, investors have come to agree with us, by moving forward their expectations for the Fed funds rate (Chart I-7). However, Chart I-8 highlights that investors have the right view for the wrong reason. The chart highlights that US government bond yields have risen entirely due to inflation expectations and that real yields have fallen. This means that investors believe that the Fed will be forced to raise interest rates earlier than it currently expects to prevent an out-of-control rise in prices, whereas we believe that they will do so because of a return to maximum employment. The implication for investors is that bond yields are still likely to rise over the coming year, but that higher yields are likely to occur alongside falling inflation expectations. This trend underscores that common hedges against inflation, such as precious metals and the relative performance of TIPS, are likely to underperform over the coming year. We have noted in previous reports that the fair value for long-maturity government bond yields implied by the Fed’s interest rate projections is not likely threatening for equity multiples, and certainly not for economic activity. A September 2022 rate hike, coupled with a pace of three hikes per year and a 2.5% terminal Fed funds rate, implies that 10-year Treasury yields will rise to 2.15% over the coming year, which would be only modestly higher than the level that prevailed prior to the pandemic (Chart I-9). Chart I-8...But For The Wrong Reason

...But For The Wrong Reason

...But For The Wrong Reason

Chart I-9Higher Bond Yields Are Unlikely To Be Restrictive Next Year

Higher Bond Yields Are Unlikely To Be Restrictive Next Year

Higher Bond Yields Are Unlikely To Be Restrictive Next Year

However, once the Fed begins to raise interest rates, investors should be on the lookout for signs that market expectations for the real natural rate of interest, or “R-star,” are rising. The Fed’s terminal rate projection is well below nominal potential GDP growth, and, while a gap between these two measures made sense in the years following the global financial crisis, this no longer appears to be the case. Chart I-10 highlights that real household mortgage liabilities began to contract sharply in 2006, and did not turn positive on a year-over-year basis until the end of 2016. It is likely that R-star was falling or weak during this period, but the correlation between the two series clearly shifted in the latter phase of the last economic cycle. Chart I-11 emphasizes this point by highlighting that the household debt service ratio is now the lowest it has been since the 1970s, underscoring the capacity that US consumers have to withstand higher interest rates. Chart I-10R-star Fell Post-GFC, For A Time

R-star Fell Post-GFC, For A Time

R-star Fell Post-GFC, For A Time

Chart I-11Today, US Households Have A Lot Of Capacity To Tolerate Higher Rates

Today, US Households Have A Lot Of Capacity To Tolerate Higher Rates

Today, US Households Have A Lot Of Capacity To Tolerate Higher Rates

We doubt that investor expectations for the terminal rate will rise significantly before the Fed begins to normalize monetary policy, but it may happen. In addition, the Fed may begin raising interest rates next year as soon as late in the summer or early in the fall, which would locate the liftoff date within our 6-12 month investment time horizon. As such, our base case view is that a rise in interest rates over the coming year will not be threatening to the equity market, but this view may change at some point next year. Equities: Expect Modest Returns In 2022 A benign increase in long-maturity bond yields in 2022 suggests that equity multiples will neither contribute to, nor subtract from, equity returns. As such, return expectations for equities should be centered around expected earnings growth.

Chart I-

Table I-2 presents consensus estimates for nominal GDP growth, S&P 500 revenue growth, and earnings growth for 2022. The table highlights that expectations for revenue growth estimates appear to be reasonable, given that bottom-up analysts continue to expect an expansion in profit margins next year. Chart I-12 highlights that margins have already risen back above their pre-pandemic high, and that this is true for both tech and ex-tech sectors. Chart I-12US Profit Margins Have Already Risen To Record Levels

US Profit Margins Have Already Risen To Record Levels

US Profit Margins Have Already Risen To Record Levels

We doubt that further increases in profit margins will be sustained next year. It is possible that margins will actually decline – a view that was recently espoused by our US Equity Strategy service.2 Risks to profit margins underscore that stocks are likely to generate mid-single digit returns next year, which will beat the returns offered by bonds and cash. But stocks will generate much lower returns compared with those enjoyed by investors over the past year. Within the equity market, we remain of the view that even a benign rise in long-maturity bond yields argues for the outperformance of value versus growth stocks over the coming year. Chart I-13 highlights that the rolling one-year correlation between relative global growth versus value stock prices and the US 10-year Treasury yield has become increasingly negative over time, which bodes well for value. We also continue to recommend that investors favor small over large caps and cyclicals over defensives, although cyclical stocks are now becoming stretched versus defensives on an equally-weighted basis as they are closing in on their 2018 highs (Chart I-14). We think it is too early to position against cyclicals, but a downgrade to neutral may be in the cards at some point next year. Chart I-13Growth Will Underperform Value If Long-Maturity Bond Yields Rise

Growth Will Underperform Value If Long-Maturity Bond Yields Rise

Growth Will Underperform Value If Long-Maturity Bond Yields Rise

Chart I-14Cyclicals Are Starting To Look Stretched Versus Defensives

Cyclicals Are Starting To Look Stretched Versus Defensives

Cyclicals Are Starting To Look Stretched Versus Defensives

Investment Conclusions Next month’s report will feature BCA’s 2022 outlook, as well as a transcript of our recently held annual discussion with Mr. X and his daughter Ms. X (who joined his family office a couple of years ago). Our annual outlook will provide a detailed walkthrough of our views for the upcoming year, as well as answers to sobering questions raised by Mr. X and Ms. X about the longer-term outlook. For now, we recommend that investors stick with a pro-cyclical view, favoring the following assets: Global stocks over bonds A short-duration position within a government bond portfolio Speculative-grade corporate bonds within a credit portfolio Global ex-US stocks vs US, focused on DM ex-US Global value versus growth stocks Cyclicals versus defensives, and small versus large caps Major currencies versus the US dollar Jonathan LaBerge, CFA Vice President The Bank Credit Analyst October 29, 2021 Next Report: November 30, 2021 II. Gauging The Risk Of Stagflation In this report we examine the risk of stagflation by comparing the current environment to that of the late-1960s and 1970s. Today, investors cannot rule out the possibility of a stagflationary outcome, for four reasons: long-term household inflation expectations have risen significantly over the past year; fiscal policy has been expansionary; monetary policy will remain expansionary at the Fed’s projected terminal Fed funds rate; and component shortages and price increases linked to energy market and supply chain disruptions may persist or worsen over the coming year. However, the strong demand-pull inflationary dynamics that existed in the late-1960s were mostly absent in the lead-up to the pandemic, supply-chain issues are in part due to strong goods demand and supply disruptions that will eventually dissipate, and economic agents do not expect severe price pressures to persist beyond the pandemic. On balance, this points to a stagflationary outcome over the coming 6-24 months as a risk, but not a likely event. Investors should use the Misery Index, which is the sum of the unemployment rate and headline PCE inflation, as a real-time stagflation indicator. The Misery Index underscores that the US economy is unlikely to experience true stagflation unless the unemployment rate rises. A portfolio of the US dollar, the Swiss Franc, and industrial commodities may serve as a useful hedge for investors who are concerned about absolute return prospects in a world in which long-maturity bond yields are rising and risks of stagflationary dynamics are present. Chart II-1The Misery Index Reflects The Risk Of Stagflation

The Misery Index Reflects The Risk Of Stagflation

The Misery Index Reflects The Risk Of Stagflation

Over the past several weeks, concerns about a possible return to 1970s-style stagflation have re-emerged significantly in the minds of many investors. These investors have pointed toward similarities between the current environment and that of the 1970s, including shortages limiting output, a snarled global trade and logistical system, and rising energy prices. Chart II-1 highlights that the US “Misery Index” – the sum of the unemployment rate and headline PCE inflation – rose again over the past several months to high single-digit territory, after having fallen dramatically from April 2020 to February of this year. Panel 2 of Chart II-1 highlights that last year's rise in the Misery Index was driven almost entirely by the unemployment rate, whereas the current level is due to a combination of a modestly elevated unemployment rate and a pronounced acceleration in inflation. The headline PCE deflator has risen above 4%, a level that has not been reached since 1991 during the First Gulf War. In this report, we examine the risk of stagflation by comparing the current environment to that of the late 1960s and 1970s. We conclude that while investors cannot rule out the possibility of a stagflationary outcome, there are important differences that point toward a stagflation outcome over the coming 6-24 months as a risk, not a likely event. We conclude by highlighting assets that may produce absolute returns in a world in which long-maturity bond yields are rising and risks of stagflationary dynamics are present. Revisiting The 1960s And 70s Chart II-2The 1960s Laid The Groundwork For Elevated Inflation

The 1960s Laid The Groundwork For Elevated Inflation

The 1960s Laid The Groundwork For Elevated Inflation

The first step in judging the risk of a return to 1970s-style stagflation is to review, in a detailed way, what caused those conditions. Investors are well aware of the role that two separate energy price shocks played in raising prices and damaging output during this period, but they are less cognizant of the impact that a persistent period of above-trend output and significant labor market tightness had in setting up the conditions for sharply higher inflation. This focus of investors on energy prices partially reflects the fact that the Misery Index increased most visibly in the 1970s and that policymakers in the 1960s may not have realized how extensively economic output was running above its potential. With the benefit of hindsight, Chart II-2 illustrates the extent to which inflationary pressures built up in the 1960s, well before the first oil price shock in 1973. The chart shows that the unemployment rate was below NAIRU – the non-accelerating inflation rate of unemployment – for 70% of the time during the 1960s, and that inflation had already responded to this in the latter half of the decade. Annual headline PCE inflation was running just shy of 5% at the onset of the 1970 recession; it fell to 3% in the aftermath of the recession, but had already begun to reaccelerate in the first half of 1973. Following the 1973/1974 recession, inflation did decelerate significantly, falling from 11-12% to 5% in headline terms, and from 10% to 6% in core terms. But the pace of price appreciation did not fall below 5-6% in the second half of the 1970s, despite a significant and sustained rise in the unemployment rate above its natural rate. The 1975 to 1978 period is especially important for investors to understand, because it is arguably the clearest period of true stagflation in the 1970s. The fact that the Misery Index rose sharply during two major oil price shocks is not particularly surprising in and of itself, given the direct impact of energy prices on headline consumer prices; it is the fact that the index remained so elevated between these shocks, the result of persistently high inflation in the face of significant labor market slack, that is most relevant to investors. There are two reasons that both inflation and unemployment remained high during this period. First, labor market slack was sizeable during these years because the US economy was more energy-intensive in the 1970s than it is today. Chart II-3 highlights that goods-producing employment lagged overall employment growth from late 1973 to late 1977, underscoring that the rise in oil prices significantly impacted jobs growth in energy-intensive industries.

Chart II-3

Second, it is clear that the combination of demand-pull inflation in the late 1960s and the predominantly cost-push inflation of the 1970s led to expectations of persistent inflation among households and firms. The original Phillips Curve, as formulated by New Zealand economist William Phillips in the late 1950s, described a negative relationship between the unemployment rate and the pace of wage growth. Given the close correlation between wage and overall price growth at the time, the Phillips Curve was soon extended and generalized to describe an inverse relationship between labor market slack and overall price inflation. But the experience of the 1970s highlighted that inflation expectations are also an important determinant of inflation, a realization that gave birth to the expectations-augmented (i.e. “modern-day”) Phillips Curve (more on this below). The Stagflation Era Versus Today

Chart II-

Table II-1 presents a stagflation “threat matrix,” representing the Bank Credit Analyst service’s assessment of the various factors that could potentially contribute to a stagflationary environment today, relative to what occurred in the 1960s and 1970s. While we acknowledge that there are some similarities today to what occurred five decades ago, the most threatening factors have been present for a shorter period of time and appear to have a smaller magnitude than what occurred during the stagflationary era. In addition, key factors, such as the visibility available to policymakers and investors about household inflation expectations and the potential output of the economy, would appear to reduce significantly the risk of a stagflationary outcome today. We discuss each of the factors presented in Table II-1 below: Fiscal & Monetary Policy Chart II-4Government Spending Last Cycle Looked Nothing Like The 1960s

Government Spending Last Cycle Looked Nothing Like The 1960s

Government Spending Last Cycle Looked Nothing Like The 1960s

The persistently tight labor market that contributed to the inflationary buildup in the 1960s occurred as a result of easy fiscal and monetary policy. Chart II-4 highlights that the contribution to real GDP growth from government expenditure and investment was very elevated in the 1960s. Chart II-5 shows that a positive output gap in the late 1960s and the first half of the 1970s is well explained by the fact that 10-year US government bond yields were persistently below nominal GDP growth. The relationship between the stance of monetary policy and the output gap only meaningfully diverged in the latter half of the 1970s, during the true stagflationary era that we noted above. Chart II-5Easy Monetary Policy Juiced Aggregate Demand In The 60s And Early 70s

Easy Monetary Policy Juiced Aggregate Demand In The 60s And Early 70s

Easy Monetary Policy Juiced Aggregate Demand In The 60s And Early 70s

Chart II-6Monetary Policy Today Is Extremely Easy

Monetary Policy Today Is Extremely Easy

Monetary Policy Today Is Extremely Easy

Today, it is clear that the stance of fiscal policy has recently been extraordinarily easy, and 10-year US government bond yields have remained well below nominal GDP growth for the better part of the last decade. Relative to estimates of potential nominal GDP growth, 10-year Treasury yields are the lowest they have been since the 1970s (Chart II-6). Ostensibly, this supports concerns that policy might contribute to a stagflationary outcome. These concerns were raised by Larry Summers in March, when he described the Biden administration’s fiscal policy as the “least responsible” that the US has experienced in four decades and warned of the potential inflationary consequences of overheating the economy.3 But there are two important counterpoints to these concerns. First, easy fiscal policy this cycle has followed a period during the last economic cycle in which government spending contributed to the most sustained drag on economic activity since the 1950s. Unlike the 1960s, the unemployment rate has been below NAIRU for only a third of the time over the past decade. In addition, Chart II-7 highlights that fiscal thrust will turn to fiscal drag next year, underscoring the temporary nature of the massive burst in fiscal spending that has occurred in response to the pandemic. Under normal circumstances, the fiscal drag implied by Chart II-7 would substantially raise the risks of a recession next year, but we have noted in previous reports that a significant amount of excess savings remain to support spending and employment. The net impact of these two factors results in a reasonable expectation that the US economy will return to maximum employment next year, but this is a far cry from the 1960s when the unemployment rate was below its natural rate for 70% of the decade.

Chart II-7

Based on conventional measures, US monetary policy has been easy for a decade, but easy monetary policy did not begin to contribute positively to a rise in household sector credit growth last cycle until 2014/2015. This underscores that the natural rate of interest (“R-star”) did fall during the early phase of the last economic expansion. However, we argued in an April report that R-star was likely rising in the latter half of the last expansion,4 and we believe that the terminal Fed funds rate is likely higher than what the Fed is currently projecting, barring any additional negative policy shocks. Thus, while we do not believe that the duration of easy monetary policy over the past decade has laid the groundwork for a major rise in prices, it is now clearly positively contributing to aggregate demand and does risk a future overshoot in prices if long maturity bond yields remain well below the pace of economic growth for a sustained period of time. The Impact Of Shortages Chart II-8Gasoline Shortages Plagued The US Economy In The 1970s

Gasoline Shortages Plagued The US Economy In The 1970s

Gasoline Shortages Plagued The US Economy In The 1970s

Gasoline shortages occurred during the oil shocks of the 1970s and are a key similarity that some investors point toward when comparing the situation today with the stagflationary era. Chart II-8 highlights that the annual growth in real personal consumption expenditures on energy goods and services fell into negative territory on six occasions in the 1970s, although it was most pronounced during the two oil price shocks and their resulting recessions. Today, the impact of shortages appears to be broader than what occurred in the 1970s, but less impactful and not likely to be as long-lasting. Chart II-9 highlights that the OPEC oil embargo of 1973 raised the global oil bill by 2.4% of global GDP and permanently raised the price of oil. The global oil bill will only be fractionally above its pre-pandemic level in 2022, with oil prices at $80/bbl, and, while it is true that US gasoline prices have risen significantly, they are not higher than they were from 2011-2014 (Chart II-10). Chart II-9$80/bbl Oil Is Not Onerous

$80/bbl Oil Is Not Onerous

$80/bbl Oil Is Not Onerous

Chart II-10US Gasoline Prices Are High, But They Have Been Higher

US Gasoline Prices Are High, But They Have Been Higher

US Gasoline Prices Are High, But They Have Been Higher