Equities

Highlights The equity risk premium has turned negative for the first time since 2002. It follows that any significant rise in bond yields will cause risk-asset prices to collapse, quickly flipping any incipient inflationary shock into a deflationary shock. Shorting bonds yielding 2 percent is a ‘widow maker’ trade, as anybody who has tried this with a long list of government bonds has learned to their cost, the most recent being UK gilts. Hence, the next on the list for the ‘widow maker’ is shorting the US 30-year T-bond which is now yielding 2 percent. In fact, the US 30-year T-bond is a must-own structural investment. Fractal analysis: Medical equipment versus healthcare services. Feature Chart of the WeekThe Equity Risk Premium Turns Negative For The First Time Since 2002

The Equity Risk Premium Turns Negative For The First Time Since 2002

The Equity Risk Premium Turns Negative For The First Time Since 2002

Mainstream investments are now priced to deliver negative, zero, or at best, feeble long-term investment returns. Mainstream investments are now priced to deliver negative, zero, or at best, feeble long-term investment returns. For example, the US 10-year Treasury Inflation Protected Security (TIPS) and the UK 10-year index linked gilt are yielding -1.3 percent and -2.8 percent respectively. Meaning that anybody who buys and holds these bonds to redemption is guaranteed a deeply negative 10-year real return. Meanwhile, in nominal yield space, 10-year government bonds yield -0.35 percent in Germany and Switzerland, 0.7 percent in the UK, and 1.3 percent in the US. What about equities? Unlike a bond’s redemption yield, equities do not offer a guaranteed long-term return for buy-and-hold investors. So, some analysts assume that the equity market’s earnings yield is the proxy for this long-term return. According to these analysts, the US equity market’s earnings yield of 4.4 percent means that it will deliver a prospective long-term real return of 4.4 percent per annum. Compared to the 10-year TIPS real yield of -1.3 percent, they argue that this offers an excess return or ‘equity risk premium’ of a comfortable +5.7 percent. Therefore, claim these analysts, equities are reasonably valued, relative to bonds, and in absolute terms. But as we will now demonstrate, this analysis is deeply flawed. The Equity Risk Premium Has Turned Negative The equity market’s earnings yield is a valuation metric, so clearly there is some connection between it and the prospective return delivered by the equity market. Nevertheless, the crucial point to grasp is that: The equity market’s earnings yield does not equal its prospective return. Charts I-2 - I-3 should make this point crystal clear. As you can see, the earnings yield rarely equals the delivered prospective 10-year return, either real or nominal. When the earnings yield is elevated, the prospective return turns out higher. Conversely, when the earnings yield is depressed, as now, the prospective return turns out to be much lower. Chart I-2The Equity Market's Earnings Yield Does NOT Equal Its Prospective Return, Either In Real Terms...

The Equity Market's Earnings Yield Does NOT Equal Its Prospective Return, Either In Real Terms...

The Equity Market's Earnings Yield Does NOT Equal Its Prospective Return, Either In Real Terms...

Chart I-3...Or In Nominal ##br##Terms

...Or In Nominal Terms

...Or In Nominal Terms

Therefore, to take the current earnings yield of 4.4 percent and subtract the real bond yield of -1.3 percent to derive an equity risk premium of +5.7 percent is analytically flawed, just as it is analytically flawed to subtract apples from oranges. To derive the equity risk premium, the correct approach is first to translate the earnings yield into a prospective 10-year return based on the established mathematical relationship between these variables. Chart I-4 does this and shows that, based on a very tight mathematical relationship through the past thirty five years, an earnings yield of 4.4 percent translates into a prospective 10-year nominal return of just 1 percent. Chart I-4We Must Mathematically Map The Earnings Yield Into A Prospective Return...

We Must Mathematically Map The Earnings Yield Into A Prospective Return...

We Must Mathematically Map The Earnings Yield Into A Prospective Return...

Having translated the earnings yield into a prospective 10-year nominal return of 1 percent, we can now make an apples-for-apples comparison with the 10-year T-bond yield of 1.3 percent (Chart I-5). Chart I-5...And Only Then Subtract The Bond Yield

...And Only Then Subtract The Bond Yield

...And Only Then Subtract The Bond Yield

Derived correctly therefore, the equity risk premium has turned negative for the first time since 2002 (Chart of the Week). We deduce that the equity market is very richly valued both in absolute terms and relative to bonds. And crucially, that this rich valuation is contingent on bond yields remaining ultra-low, or going even lower. Shorting Bonds Yielding 2 Percent Is A ‘Widow Maker’ All of which brings us to one of the most pressing questions we get from clients. When a bond is offering a feeble yield, what is the point in owning it? Maybe the best people to answer are the casualties of the now infamous ‘widow maker’ trades. The original widow maker trade was the idea that the yield on the Japanese Government Bond (JGB), at 2 percent, was so feeble that there was no point in owning it. Furthermore, with massive Japanese fiscal stimulus coming down the pike, the ‘no-brainer’ investment strategy was not just to disown the JGBs, but to take an outright short position, as it seemed that the only direction that JGB yields could go was up. In fact, JGB yields did not go up, they continued to trend down. As feeble yields became even feebler, the owners of the short positions got carried out of their careers, feet first. Meanwhile, those investors who owned 30-year JGBs yielding a ‘feeble’ 2 percent in 2013 reaped returns of 75 percent, and even now, are sitting on handsome profits of 55 percent. Some people protest that Japan is an exceptional and isolated case, rather than a template for economies which will not repeat their putative policy-errors. Such protests have always struck us as factually wrong, blinkered, and even prejudiced. Nevertheless, let’s indulge these prejudices with a simple rejoinder – forget Japan, what about Switzerland, or the UK? (Chart I-6) Chart I-6Shorting Bonds Yielding 2 Percent Is A 'Widow Maker'

Shorting Bonds Yielding 2 Percent Is A 'Widow Maker'

Shorting Bonds Yielding 2 Percent Is A 'Widow Maker'

Just like the JGB widow maker, anybody who shorted UK gilts yielding 2 percent is nursing heavy losses. Meanwhile, those investors who owned 30-year UK gilts yielding a ‘feeble’ 2 percent in 2018 reaped returns of 40 percent, and even now are sitting on tidy profits of 30 percent. Just like the JGB widow maker, anybody who shorted UK gilts yielding 2 percent is nursing heavy losses. Bear in mind that a 30-year bond yielding a feeble 2 percent will deliver a cumulative return of more than 80 percent to redemption. And that if the feeble yield becomes even feebler, this return will get front-end loaded, creating widow makers for the short positions and spectacular gains for the long positions, as witnessed in JGBs and UK gilts. The 30-Year T-Bond Is A Must-Own Structural Investment The next candidate for the widow maker is shorting the US 30-year T-bond, which is yielding, you guessed it, 2 percent. Remember that while Japan may not be a great template for the US, the UK certainly is – because the US and UK have very similar economic, financial, political, social, and cultural structures. Until recently therefore, bond yields in the US and UK were moving in near-perfect lockstep (Chart I-7). Chart I-7The Difference Between US And UK Bond Yields Is Just That The UK Has Had One More Deflationary Shock

The Difference Between US And UK Bond Yields Is Just That The UK Has Had One More Deflationary Shock

The Difference Between US And UK Bond Yields Is Just That The UK Has Had One More Deflationary Shock

So, what happened? The one word answer is: Brexit. The recent difference between US and UK bond yields is simply that the UK has had one more deflationary shock than the US. Put the other way around, the US is just one deflationary shock away from a UK level of bond yields – meaning the 30-year yield not at 2 percent, but at 1 percent. But why can’t the next shock be an inflationary shock resulting in much higher yields? The simple answer is that the equity risk premium has turned negative for the first time since 2002. Moreover, as we pointed out in The Road To Inflation Ends At Deflation the extremely rich valuation of $300 trillion of global real estate is also highly contingent on ultra-low bond yields. It follows that any significant rise in bond yields will collapse the value of $500 trillion of risk-assets. In a $90 trillion global economy, this will quickly flip any incipient inflationary shock into a deflationary shock. Any significant rise in bond yields will collapse the value of $500 trillion of risk-assets. We conclude that the US 30-year T-bond is a must-own structural investment. Fractal Analysis Update As hospitals have rushed to clear their backlog of non-pandemic treatments and procedures, medical equipment stock prices have surged. This is particularly true for US medical equipment (ticker IHI) which, since June, is up by 25 percent versus US healthcare services (Iqvia, Veeva, or loosely proxied by ticker XHS). Given that the backlog of treatments will eventually clear, and that the intense rally is now extremely fragile on its 65-day fractal structure (Chart I-8), a recommended countertrend trade is to short US medical equipment versus healthcare services. Set the profit target and symmetrical stop-loss at 8.5 percent. Chart I-8The Intense Rally In Medical Equipment Stocks Has Become Fragile

The Intense Rally In Medical Equipment Stocks Has Become Fragile

The Intense Rally In Medical Equipment Stocks Has Become Fragile

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Fractal Trading System Fractal Trades 6-Month Recommendations Structural Recommendations Closed Fractal Trades Closed Trades Asset Performance Equity Market Performance Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields ##br##- Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields ##br##- Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields ##br##- Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields ##br##- Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

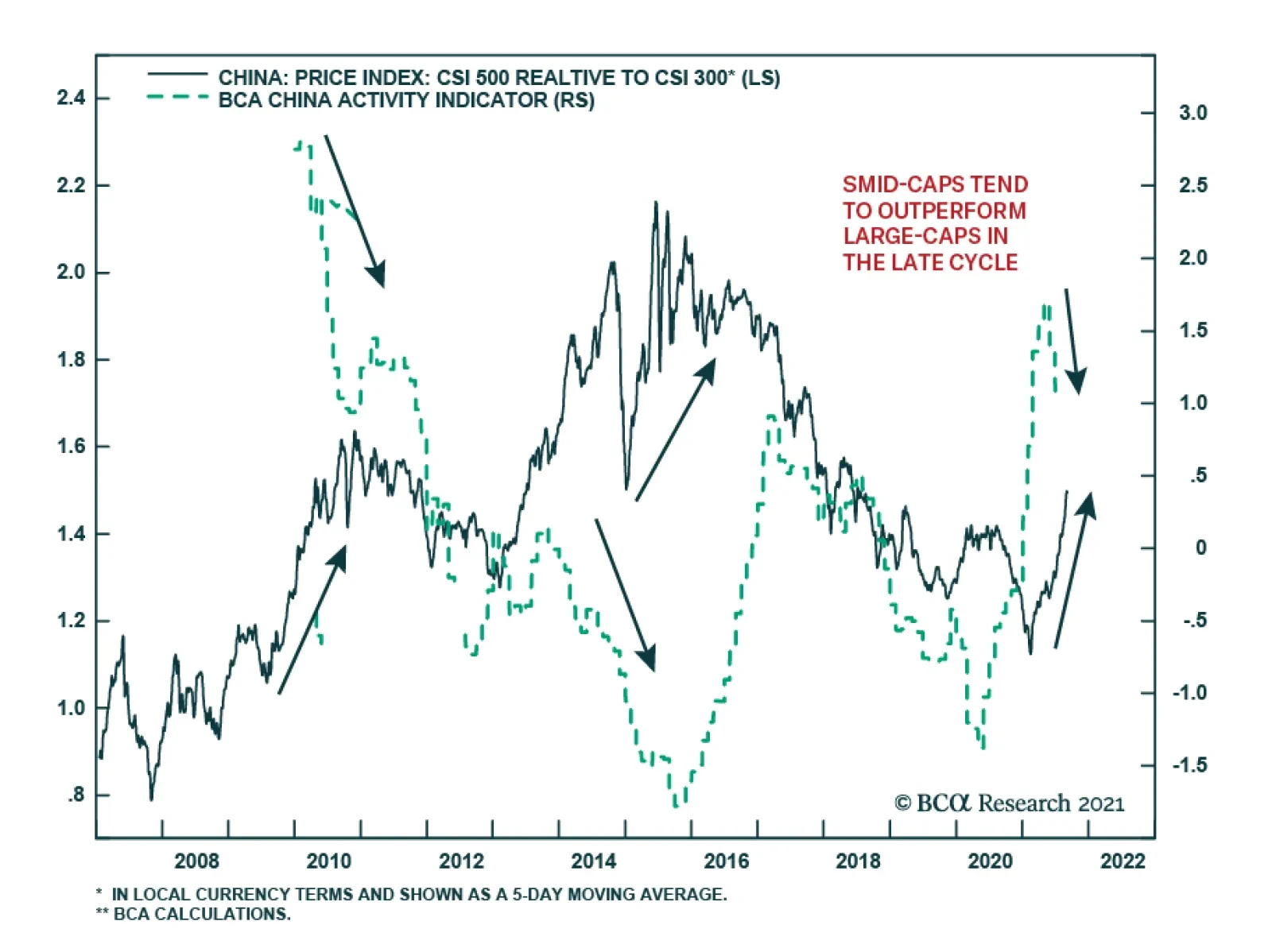

BCA Research's China Investment Strategy service concludes that small and medium caps will likely continue to outperform large-cap stocks this year. Chinese small and medium-cap (SMID-cap) stocks have outperformed large-caps since February and the recent…

Feature Chart 1Chinese Offshore Stocks Tumbled Amid Regulatory Crackdowns

Chinese Offshore Stocks Tumbled Amid Regulatory Crackdowns

Chinese Offshore Stocks Tumbled Amid Regulatory Crackdowns

Relative to the global equity index, onshore and offshore Chinese stocks have fallen by 18% and 32%, respectively, since their peaks in mid-February (Chart 1). The panic sell-off in the offshore market, which saw greater losses due to its high concentration in internet stocks, appears to be overdone and may technically rebound in the near term. However, any short-term bounce in Chinese stocks from oversold levels will likely be short-lived (Chart 2). The crackdown on new economy companies reflects socio-political and economic shifts in China, which raises the odds that the restrictions will continue with further actions focused on social welfare and healthcare. August’s official PMIs and economic data indicate a broad-based softening in China’s domestic demand and production. However, compared with 2018/19 when the US-China trade war exacerbated the deterioration in an already slowing economy, the economy now remains well supported by strong exports. Moreover, the magnitude of the slowdown has not exceeded policymakers’ pain thresholds (Chart 3). Chart 2Tactical Bounce Was Short-Lived In Previous Downturns

Tactical Bounce Was Short-Lived In Previous Downturns

Tactical Bounce Was Short-Lived In Previous Downturns

Chart 3China's Economic Recovery Losing Steam, But From An Elevated Level

China's Economic Recovery Losing Steam, But From An Elevated Level

China's Economic Recovery Losing Steam, But From An Elevated Level

In 2018/19, stimulus was measured and the authorities did not meaningfully relax limits on bank lending standards and shadow banking. Furthermore, China recently reiterated its cross-cycle macro policy setting, which means that policymakers will not use significant stimulus to achieve high and short-term economic growth. Given financial stability measures that aim to contain risks associated with the housing market and hidden local government debt, any monetary and fiscal easing will likely help to stabilize credit growth instead of substantially boosting it this year. For the time being, China’s financial assets continue to face downside risks stemming from a confluence of a weakening business cycle and ongoing regulatory tightening. Thus, we recommend investors maintain an underweight allocation to Chinese equities within a global equity portfolio. Qingyun Xu, CFA Associate Editor qingyunx@bcaresearch.com A Shining Moment For Chinese Small And Medium Caps Small and medium-cap (SMID-cap) stocks have outperformed large-caps since February and the recent regulatory restrictions have intensified the situation. The CSI500 index, which comprises 500 SMID-cap companies, has outperformed the large-cap CSI300 by 34% since mid-February (Chart 4, top panel). Uncertainties surrounding the pandemic and corporate earnings growth have fueled extreme dislocations between large-cap and SMID-cap stocks last year. Large-cap stocks were the main contributors to China’s stock rallies in the second half of last year, while the valuation premia in small cap stocks was compressed to near decade lows (Chart 4, bottom panel). Chart 4A Low Valuation Premia And More Policy Support May Further Lift Prices Of SMID-Caps

A Low Valuation Premia And More Policy Support May Further Lift Prices Of SMID-Caps

A Low Valuation Premia And More Policy Support May Further Lift Prices Of SMID-Caps

Chart 5SMID-Caps Tend To Outperform Large-Caps In Late Business Cycle

SMID-Caps Tend To Outperform Large-Caps In Late Business Cycle

SMID-Caps Tend To Outperform Large-Caps In Late Business Cycle

Historically, SMID-caps tend to outperform large-caps in the late cycle of an economic recovery (Chart 5). The spate of regulatory changes aimed at monopolistic behaviors in various sectors has curbed investors’ appetite for the industry leaders. In addition, the government’s increasing efforts to support small and medium corporates (SMEs) will help to shore up confidence in those companies. Therefore, small and medium caps will likely continue to outperform large-cap stocks this year. Fiscal Support: How Much Room In 2H? The July Politburo meeting pledged more fiscal support for the economy later in 2021 and into 2022. We expect local government bond (LGB) issuance to accelerate: a 4.47 trillion RMB new local government bond issuance quota was approved for 2021, including 820 billion in general bonds and 3.65 trillion in special purpose bonds (SPBs). By end-August, 2.37 trillion new local government bonds had been issued, which was only 53% of the entire year’s goal. However, there are some constraints that will likely reduce the reflationary effects on the economy. First, the quota for LGB issuance approved by the National People’s Congress is 16% lower than last year, but the amount of LGBs maturing this year is 30% higher. Therefore, even though this year’s gross LGB issuance has kept pace with that of last year, more than half of the LGBs issued from January to August was used for debt repayment (Chart 6). The move by local governments to use a large portion of their bond issuance quota to pay off existing debt resembles the situation in 2018 when a financial de-risking campaign encouraged local governments to reduce the stockpile of their leverage. As noted in last week’s report, infrastructure investment and the economy did not rebound in 2H2018, even though LGB issuance picked up (Chart 7). Chart 6More Than Half Of LGBs Issued This Year Has Been Used For Debt Repayment

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chart 7Improvement In Infrastructure Investment Was Short-Lived In 2019

Improvement In Infrastructure Investment Was Short-Lived In 2019

Improvement In Infrastructure Investment Was Short-Lived In 2019

Even if we assume that local governments will use all of their remaining bond quota by year end, the gross monthly average in local government bond issuance will be around 580 billion, only slightly higher than in 2H 2020. Secondly, infrastructure investment is discouraged by stringent regulations to approve projects (including project assessment and debt repayment ability) and the accountability of local officials for project failures. Approvals for infrastructure projects remain at the lowest level since March last year (Chart 8). Finally, SPBs made up only about 15% of overall infrastructure spending in the past three years, while the majority came from public-private partnerships (PPP) financing, revenues from government-managed funds, government budgets and bank loans. Falling proceeds from land transfers have dragged down government-managed funds (Chart 9). In addition, government expenditures show no signs of a material increase (Chart 9, bottom panel). Chart 8Infrastructure Investment Will Remain Subdued

Infrastructure Investment Will Remain Subdued

Infrastructure Investment Will Remain Subdued

Chart 9Government Expenditures Remain Muted

Government Expenditures Remain Muted

Government Expenditures Remain Muted

As discussed in previous reports, local government bonds issuance only accounts for 12% of total social financing. As such, without a sizeable acceleration in bank loans, enhanced LGB issuance would not be enough to prompt a substantial increase in infrastructure investment growth. Our argument is underscored by the structural downshift in infrastructure investment since 2017 (Chart 7, top panel). Therefore, additional local government bond issuance this year will help to stabilize but not boost credit growth. August PMIs Confirm Slowing Economic Activity China's official PMIs eased further in August. The non-manufacturing index fell to contractionary territory of 47.5, below the expectation of a more muted 1.3-point decline to 52.0. Similarly, the manufacturing PMI eased by 0.3 points to 50.1, which is a hair above the 50 boom-bust line. Together, weakness in both sectors pushed down the composite index to 48.9 (Chart 10). Stringent restrictions designed to halt rising rates in COVID-19 infections explain much of the deterioration in China’s service-sector activity. The sector will likely rebound in September with the easing in infection levels (Chart 11). Chart 10PMIs Show Slowing Economic Activity

PMIs Show Slowing Economic Activity

PMIs Show Slowing Economic Activity

Chart 11Lingering COVID Effects Curb Service-Sector Recovery In 2H21

Lingering COVID Effects Curb Service-Sector Recovery In 2H21

Lingering COVID Effects Curb Service-Sector Recovery In 2H21

Meanwhile, the construction PMI surprisedly rebounded sharply in August (Chart 10, bottom panel). However, investors should be cautious not to read too much into the idiosyncratic month-on-month moves suggested by the construction PMI. Instead, construction activity has moderated significantly and is set to slow further, hinting at plunged excavator sales and real estate investment in construction (Chart 12). Chart 12Construction Activity Is Unlikely To Pick Up Meaningfully This Year

Construction Activity Is Unlikely To Pick Up Meaningfully This Year

Construction Activity Is Unlikely To Pick Up Meaningfully This Year

It is clear that China’s economy is losing momentum, but greater economic weakness will be needed for policymakers to stimulate meaningfully. Export Sector Remains A Bright Spot China’s exports remain robust. Export growth picked up in August from July on a year-over-year basis. Although the improvement in August reflects a base effect, exports in level reached a new high (Chart 13). Both skyrocketed exports container freight index and strong Korean exports suggest that global demand for Chinese manufacturing goods remains resilient (Chart 14). Even though manufacturing PMIs from developed markets have rolled over, they remain elevated and should continue to support China’s exports (Chart 15). Chart 13Chinese August Exports In Level Reached A New High

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chart 14Exports Will Remain Robust In The Rest Of The Year...

Exports Will Remain Robust In The Rest Of The Year...

Exports Will Remain Robust In The Rest Of The Year...

In contrast to resilient exports, China’s official PMI export new orders subindex has declined for five consecutive months. Even though falling PMI new export orders subindex heralds a slowing in exports growth, a reading of below the 50 boom-bust threshold in the former does not suggest a contraction in the growth rate of the latter. Furthermore, the month-over-month nature of PMI new export orders subindex tends to overstate the volatility in exports. The divergence between the PMI new export orders subindex and real export growth also occurred in 2018/19 during the height of the US-China trade war when export orders were volatile (Chart 16). Chart 15...And Will Continue To Benefit From Strong Global Demand

...And Will Continue To Benefit From Strong Global Demand

...And Will Continue To Benefit From Strong Global Demand

Chart 16A Divergence Between PMI New Export Orders And Export Growth

A Divergence Between PMI New Export Orders And Export Growth

A Divergence Between PMI New Export Orders And Export Growth

Regulatory Tightening In Real Estate Sector Stringent regulations in housing since the beginning of the year have started to cool the sector (Chart 17). However, home prices inflation in tier-one cities is still elevated (Chart 18). Thus, we expect the controls on housing and among property developers will remain in place for the next 6 to 12 months. Chart 17Housing Sector Is Cooling...

Housing Sector Is Cooling...

Housing Sector Is Cooling...

Chart 18...But Housing Prices In First-Tier Cities Keep Rising At A Faster Rate

...But Housing Prices In First-Tier Cities Keep Rising At A Faster Rate

...But Housing Prices In First-Tier Cities Keep Rising At A Faster Rate

Industrial Profits: Rising Prices, Falling Production China’s industrial profit growth remained solid in July despite the waning low base effect. Manufacturing producer prices continued to rise, offsetting weaker production growth (Chart 19). In addition, a low interest-rate environment helped to lift profits in the manufacturing sector by reducing debt servicing costs. While we expect weakening domestic demand and peaking producer prices to weigh on corporate profits in the rest of this year, profit growth is rolling over from a lofty height and will not likely drop sharply in the coming months (Chart 20). In addition, producer prices will likely remain at a historically high level in the next six months given robust global demand for raw materials and persistent global supply shortages. Chart 19Rising Prices And Low Interest Rates Helped To Offset Falling Industrial Production

Rising Prices And Low Interest Rates Helped To Offset Falling Industrial Production

Rising Prices And Low Interest Rates Helped To Offset Falling Industrial Production

Chart 20Peaking Producer Prices Will Weigh On Corporate Profits

Peaking Producer Prices Will Weigh On Corporate Profits

Peaking Producer Prices Will Weigh On Corporate Profits

Meanwhile, there is a large gap between the prices for producer goods and consumer goods, suggesting that manufacturers in mid-to-downstream industries have not been able to fully pass on rising input costs to domestic consumers (Chart 21). Profit growth continues to be disproportionally stronger in the upstream industrial producers than in the downstream industries, while the profit margin in the manufacturing sector remains much more muted (Chart 22). Chart 21Inflation Passthrough From Manufacturers To Domestic Consumers Remains Limited

Inflation Passthrough From Manufacturers To Domestic Consumers Remains Limited

Inflation Passthrough From Manufacturers To Domestic Consumers Remains Limited

Chart 22Profit Growth In Upstream Industries Still Outpaces Manufacturing Sector

Profit Growth In Upstream Industries Still Outpaces Manufacturing Sector

Profit Growth In Upstream Industries Still Outpaces Manufacturing Sector

Table 1

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chinese Small And Medium Caps Are Finding Their Shining Moment

Table 2

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chinese Small And Medium Caps Are Finding Their Shining Moment

Footnotes Market/Sector Recommendations Cyclical Investment Stance

Highlights Economic policy uncertainty is rising in the US and will generate volatility this fall. But by the end of the year the result should be more fiscal reflation. Biden’s approval rating is now “underwater” – net negative – but this was expected. Unless he suffers another black eye, he can still shepherd his two big bills through Congress by year’s end. Public support for Biden’s tax hikes is weak. Some tax hikes are likely but aggressive hikes are now off the table. The midterm elections were already likely to produce a Republican win in the House. History supports this consensus. But the Senate is still an open game. The presidential election outlook is only marginally affected, at most, by the messy Afghanistan pullout. Value stocks are re-testing their low point against growth stocks. We do not expect them to break down when Congress is about to pass historic new spending increases. Feature Economic policy uncertainty is reviving in the US and set to increase this fall. This is true in absolute terms and relative to global uncertainty, even at a time when China’s sweeping regulatory crackdown is generating a lot of global uncertainty (Chart 1). Chart 1US Relative Policy Uncertainty Reviving

US Relative Policy Uncertainty Reviving

US Relative Policy Uncertainty Reviving

Chart 2Policy Uncertainty Breakdown

Policy Uncertainty Breakdown

Policy Uncertainty Breakdown

The latest increase in the policy uncertainty index is largely driven by rising uncertainty over future government spending (Chart 2, panel 2) and expiring tax provisions (Chart 2, panel 3), more so than by public sentiment reflected in the mainstream media or even the inflation debate. The looming budget battle this fall will have major implications for taxes and spending and will lift the uncertainty indicators regarding sentiment and consumer prices. Volatility will ensue in the coming months. But by the end of the year, Congress will have passed at least one, likely two, new laws that will increase government fiscal support for the economy and dispel deflationary tail risks. The lingering pandemic will if anything help concentrate lawmakers’ minds on passing more stimulus. Therefore we expect US equities and cyclical sectors to grind higher. The passage of these bills will mark the high point in policy reflation, after which clouds will loom on the horizon in 2022. Biden’s Net Negative Approval Rating President Biden’s job approval rating is now officially “underwater” – more people disapprove of his leadership than approve (Table 1). This is raising serious doubts about his ability to shepherd legislation through Congress this fall. However, these doubts are overrated. Table 1Biden’s Net Approval Is Officially Negative

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Biden’s approval has mostly fallen due to his mishandling of the US military’s withdrawal from Afghanistan – which most Americans agree was necessary, however much they deplored the commander-in-chief’s handling of it. Therefore Biden’s approval rating will not fall much farther – at least not until he suffers another black eye. Until that happens, Biden’s approval will stabilize in the range of Obama’s and above Trump’s. The reason is that he retains a solid political base of support – and his political base is larger than President Trump’s, so his general approval will stay higher. Indeed his approval is still stronger than Obama’s among Democrats (Charts 3A and 3B). This is counterintuitive since Obama was a charismatic, young, and progressive Democrat. The reason is that Democrats are still very cognizant and fearful of the alternative: President Trump. This anti-Trump tailwind will help Biden for some time. Support among Democrats is critical for maintaining party discipline in passing the reconciliation bill this fall. It is also important for the midterm elections. Chart 3ABiden’s Job Approval Collapses

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart 3BBiden’s Approval Holding Up Among Democrats

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

On specific issues, Biden is weaker than Obama on foreign policy and than Trump on the economy (Charts 4A and 4B). The economy will remain the central concern, notwithstanding Afghanistan, and on this front Biden should stabilize or improve. However, other foreign policy issues could rise to the fore and hurt him at any time given today’s fraught geopolitical environment. Chart 4ABiden’s Falling Approval On Economy

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart 4BBiden’s Falling Approval On Foreign Policy

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

We say Biden’s score on the economy will improve because consumer confidence will rebound once the Delta variant of COVID-19 subsides (Chart 5). Both manufacturing and service sectors are performing better than when Biden was elected and employment is holding up in both sectors. The new orders-to-inventories measures suggest the service sector will continue to improve (Chart 6). The headline unemployment rate has dropped to 5.2%. Chart 5Consumer Confidence Should Support Biden

Consumer Confidence Should Support Biden

Consumer Confidence Should Support Biden

Chart 6PMIs Also Offer Some Support For Biden

PMIs Also Offer Some Support For Biden

PMIs Also Offer Some Support For Biden

Given the above, Biden still has enough clout to steer his signature legislation through Congress this fall, albeit with major modifications to his unwieldy $3.5 trillion American Families Plan. Moderate Democratic Senator Joe Manchin of West Virginia has called for a pause in new big spending legislation, but a close look at his words shows that he does not oppose the bill, he merely wants to water it down, which is not a change from his earlier position.1 He speaks for other moderates. The left-wing faction led by Senator Bernie Sanders of Vermont will make counter-threats yet ultimately has no choice other than to support the most progressive social legislation in recent memory. The bill will be watered down. Could this watering down process result in a total jettison of the Democrats’ proposed tax hikes? The Wall Street Journal reports that congressional support for tax hikes is losing steam.2 While aggressive tax hikes are off the table, we highly doubt that all tax hikes will be removed. Financial markets have not responded much to the threat of higher taxes. Small business owners, who are most sensitive to the risk of new taxes and regulation imposed by Democrats, have not shown much concern for either issue this year – they are much more worried about inflation (Chart 7). We assume the equity market would rally if tax hikes were dropped but we do not think this is likely to happen. Americans support higher taxes – but only Democrats are enthusiastic about across-the-board hikes on individuals, corporations, and capital gains. Polls show that 59% of independent voters, not to mention Democrats, support higher taxes on high-income earners, although the proposed 28% corporate is increasingly likely to be cut down (Chart 8). This is the fundamental reason for investors to expect Democrats to band together in the eleventh hour and include tax hikes in their reconciliation bill. If nothing else, a partial reversal of President Trump’s Tax Cut and Jobs Act will be necessary to give a veneer of affordability to Biden’s giant spending bill to get it past Senate moderates. Chart 7Business Will Worry About Tax Hikes When (If) They Pass

Business Will Worry About Tax Hikes When (If) They Pass

Business Will Worry About Tax Hikes When (If) They Pass

Chart 8Look Out: Americans Support Higher Taxes

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

The impact of Biden’s corporate tax hike is expected to be a 5%-8% one-off hit to corporate earnings, according to our Global Investment Strategy. The impact could be less than that but the combination of popular opinion and the Democratic Party’s need to finance their social agenda suggests that investors should plan for the worst, which in this case is not that bad – key tax rates will still be lower than they were under President Obama. The chief risk to Biden’s legislation is that passing the bipartisan infrastructure bill (80% subjective odds) consumes so much political capital that there is not enough left for Biden’s reconciliation bill (50%-65% subjective odds, depending on circumstances). This is possible. Congressional Democrat leaders want to tie these two bills together but most likely the quick success of infrastructure, which is more popular than social welfare, will lead Democrats to conclude that a bird in the hand is worth two in the bush. They will pass infrastructure on less-than-perfect assurances from Senate moderates that they will support reconciliation. Then a separate battle over reconciliation will ensue, in which Biden must cajole the left-wing and moderate factions of his party into a “yea” vote while Republicans obstruct. The second major risk to Biden’s legislation – and the macro backdrop – comes if he mismanages foreign policy more generally, such as with the looming crisis over Iran. A foreign policy failure beyond Afghanistan could cause permanent damage to his political capital. And yet Democrats would be even more desperate for a legislative victory then, as they would face a wipeout in the midterm elections if they had no legislative victories and two foreign policy humiliations. In other words, Biden is nowhere near so unpopular that moderate Democrats will abandon his signature legislative agenda and condemn their party and his administration to a heavy defeat in 2022. Bottom Line: Biden’s legislation will pass, including some tax hikes. The revised magnitude of tax hikes will not be known until later this fall when the Senate and House start producing legislative text. Policy uncertainty and equity volatility will trend upward this fall but the end-game is more reflationary policy, which should keep equities grinding higher at least through Christmas. Midterm Elections: The Best Case For Democrats Is Not Good Enough Are Republicans more likely to take Congress now that Biden’s approval is underwater? How would this impact the policy and macroeconomic outlook? While Republicans are highly likely to retake the House of Representatives, the Senate is still slightly tipped for the Democrats. Biden would have to fail to pass legislation or commit another major policy mistake to give Republicans full control of Congress, although this outcome is slightly favored in online betting markets. The House currently consists of 220 Democrats and 212 Republicans. There is always some fluctuation in the exact numbers. Three vacancies should be filled in November’s special elections, which could bring the count to 222 Democrats and 213 Republicans.3 With 218 votes needed to pass legislation on an absolute majority vote, Democrats can only afford to lose three votes at present. This is an extremely tight margin and shows that this fall’s reconciliation bill is at risk in the House as well as the Senate. In the midterm elections, Republicans only need to take five-to-six seats to regain the majority (218). This is easy on paper: the average seat gain for the opposition in midterm House elections is 35. Biden’s latest approval rating puts Democrats in line to lose 37 seats based on history. The opposition typically makes gains in the midterm because it is fired up whereas the presidential party is complacent. In addition Republicans are expected to gain two seats (possibly as many as four) via gerrymandering in 2022. True, Democrats have some underrated supports in 2022. In all probability the pandemic will be waning while the economy will be waxing. Biden will likely have passed at least a bipartisan infrastructure deal. The divisions within Republican ranks over Trumpism will also persist, which may or may not increase Democratic turnout and vote-switching from suburban Republicans. Hence it is reasonable to ask whether Democrats could surprise to the upside and retain the House. Online betting markets put the probability at 29%, and these odds make sense to us. The historical record helps to define what kind of events might alter the outlook for the midterms. Table 2 shows the midterm elections in which the presidential party performed best (the opposition party disappointed the historical norm). The following points are salient: Table 2Best-Case Outcomes For Presidential Party In Midterm Elections

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

There are only two cases in which the presidential party gained seats (Clinton 1998, Bush 2002) and three cases in which they only lost a few seats (Kennedy 1962, Reagan 1986, arguably Bush 1990). The Democratic victory of 1998 occurred at the top of an economic boom while the Republican victory of 2002 occurred one year after the 9/11 terrorist attacks. Neither is likely to be replicated for Democrats in 2022. Republicans’ mild losses in 1990 occurred just after Iraq invaded Kuwait. Republican’s mild losses in 1986 occurred despite a big legislative victory (tax reform). If either of the last two scenarios played out for Democrats in 2022, Democrats would likely lose the House by a whisker. Only if the Democrats’ 1962 scenario played out would Democrats retain the House in 2022, and only by a single seat. Yet the 1962 election occurred in the midst of the Cuban Missile Crisis! The takeaway is that a foreign policy crisis could help Democrats pare their losses in the midterms if Biden is deemed to have handled the crisis adroitly. But even then the ruling party would likely lose the House judging by history. Needless to say these are just historical examples. They also show that Democratic fortunes could turn around drastically between now and next fall (e.g. Kennedy went from a recession and the Bay of Pigs fiasco to gaining his party seats). The Senate outlook is less straightforward. Biden’s approval rating suggests a loss of four seats for Democrats based on the historical pattern. But the same pattern suggested Republicans would lose four seats in 2018 and instead they gained two. Our quantitative Senate election model, which we update every week in the Appendix, still tips the Democrats to gain one seat (a 51-49 majority) or at least retain their de facto one seat majority (50-50). Chart 9Presidential Vetoes In History

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

What are the macroeconomic implications? A Republican House and Democratic White House would play “constitutional hardball,” just as occurred from 2011-14, given that the country is still at historically peak levels of political polarization.4 There are likely to be critical differences between 2011 and 2023 – populism has fundamentally weakened support for fiscal austerity – but the most likely result is gridlock and deadlock. Republicans will not be able to slash spending or cut taxes as Biden will have the presidential veto, but Democrats will not be able to increase spending or hike taxes (Chart 9). The problem for Biden would be the need to avoid a national default when and if the Republicans insist on spending cuts to raise the debt ceiling. The looming debt ceiling showdown this fall will increase uncertainty and volatility but ultimately Democrats have the votes to avoid a default. That would not necessarily be the case if Republicans controlled the House. And this time around Republicans could be driven to impeach the president, for whatever reason, in retaliation for President Trump’s impeachment in 2019. This situation obviously cannot be ruled out, even though it would be virtually impossible for the Senate to convict. At the same time, some bipartisanship could occur, as it did under Trump following the 2018 midterms. Anti-trust legislation and immigration reform are the two most important policy areas to watch on this front. Republican gains in Congress would marginally weaken the Democrats’ hold on the White House in 2024, though we continue to believe that Democrats are favored. American voters are likely to be better off in November 2024 than they were in November 2020, amid a pandemic, recession, and nationwide social unrest. Our quantitative model tips Democrats with 308 electoral votes (Appendix). Professor Allan Lichtman’s “13 Keys” to the presidency – a nearly flawless prediction system since 1984 – currently suggest that the Democrats only have three keys turned against them. They would need to see six or more in order to lose the White House (Table 3). Obviously the long-term status of the economy will be a critical factor (Chart 10). Table 3Lichtman’s Keys To The Presidency (Updated Sept 2021)

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart 10Will Biden's Economy Grow Faster Than That Of His Two Predecessors?

Will Biden's Economy Grow Faster Than That Of His Two Predecessors?

Will Biden's Economy Grow Faster Than That Of His Two Predecessors?

Bringing it all together, US fiscal policy has taken a more proactive turn but it is still likely to freeze after this fall. It will be hard to pass major budget bills in 2022 ahead of the election and gridlock is the likeliest outcome, making 2025 the next realistic chance for major fiscal changes. The immediate implication is that Biden and Democratic leaders will have to disconnect the bipartisan infrastructure bill from the partisan social welfare reconciliation bill this autumn. This will require a major concession from House Speaker Nancy Pelosi. Otherwise both bills could collapse and with them the Democratic Party’s fortunes. Biden and moderate Democrats that face competitive races in 2022 will demand a quick victory before moving onto the less popular part. Investment Takeaways Value stocks are re-testing their cycle lows against growth stocks (Chart 11). The Delta variant and global growth jitters continue to weigh on this trade. Chart 11S&P Value Re-Tests Lows Versus Growth

S&P Value Re-Tests Lows Versus Growth

S&P Value Re-Tests Lows Versus Growth

The S&P 500’s “Big Five” are rallying and outperforming the other 495 companies once again (Chart 12). Chart 12S&P 5 Recovery Versus 495

S&P 5 Recovery Versus 495

S&P 5 Recovery Versus 495

We expect politically induced volatility throughout the fall but we also expect it to be resolved in new and reflationary legislation. Signs that Biden’s legislation will pass should enable cyclical sectors and value stocks to recover, though the pandemic, global growth, and Chinese stability may prevent them from outperforming defensive sectors and growth stocks. A new set of hurdles will face markets if Republicans regain the House and halt fiscal easing from 2022-24. However, they will not be rewarded by voters if they create a fiscal or economic crisis, implying that the proactive fiscal turn in public opinion will prevail over the long run. If Biden’s legislation fails then it suggests that US fiscal policy is dysfunctional even under single-party control. This would heighten the deflationary tail risk and force us to reassess our macro and policy outlook. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Appendix Table A1USPS Trade Table

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A2Political Risk Matrix

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart A1Presidential Election Model

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart A2Senate Election Model

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A3Political Capital Index

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A4APolitical Capital: White House And Congress

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A4BPolitical Capital: Household And Business Sentiment

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A4CPolitical Capital: The Economy And Markets

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Footnotes 1 See Senator Joe Manchin, “Why I Won’t Support Spending Another $3.5 Trillion,” Wall Street Journal, September 2, 2021, wsj.com. 2 Richard Rubin, “Progressives’ Tax-The-Rich Dreams Fade As Democrats Struggle For Votes,” Wall Street Journal, September 5, 2021, wsj.com. 3 The three special House elections are: Florida’s 20th District, previously Democratic held; Ohio’s 11th District, previously Democratic held; Ohio’s 15th District, previously Republican held. 4 See Mark V. Tushnet, “Constitutional Hardball,” John Marshall Legal Review 37 (2004), pp. 523-53, scholarship.law.georgetown.edu.

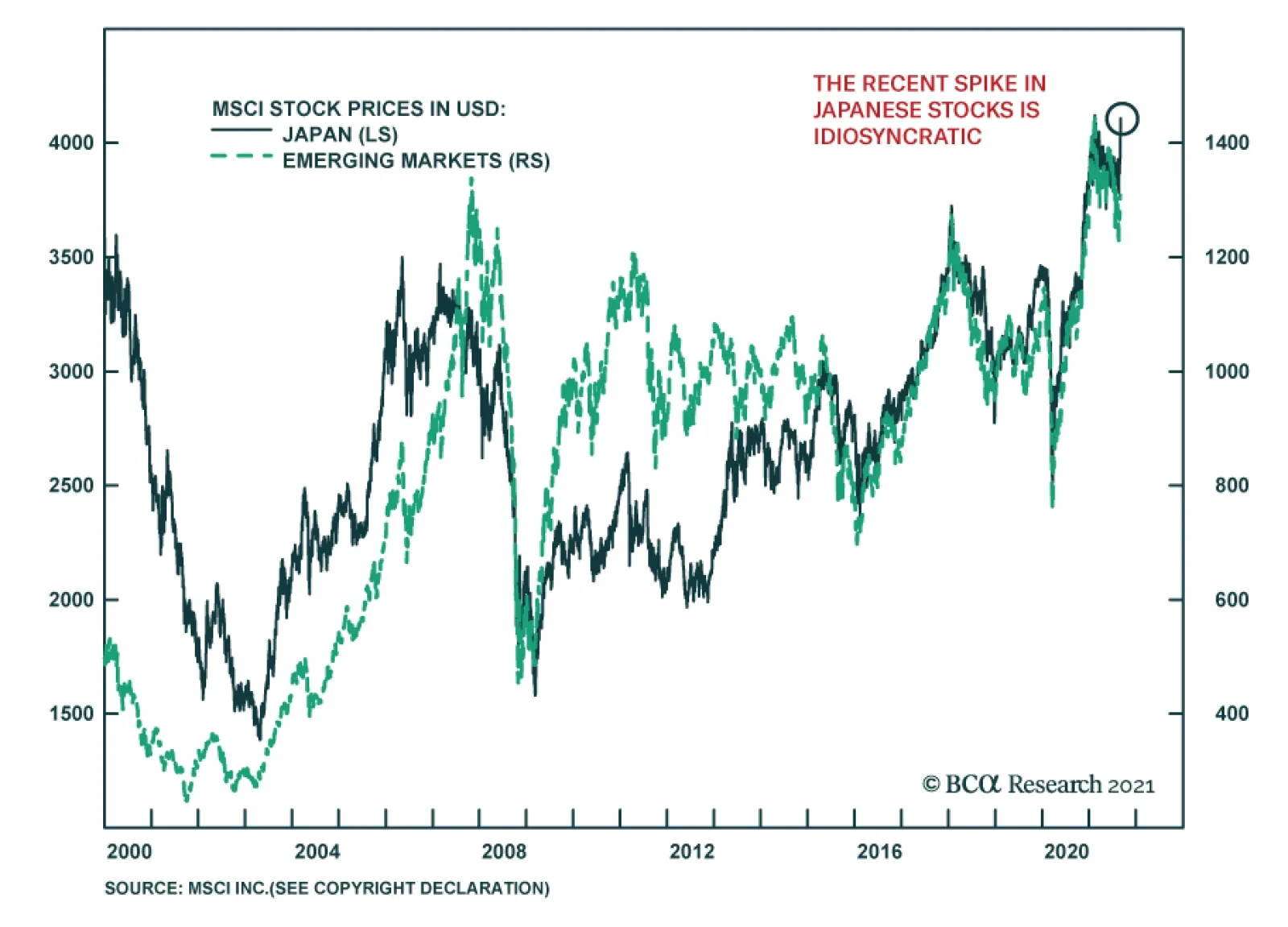

Japanese stocks have been enjoying a sharp rally in recent days with the MSCI Japan index up 6% in USD terms in just under a week and a half. The Japanese bourse is dominated by highly cyclical sectors with industrials, consumer discretionary, IT, financials,…

Foreword Today we are publishing a charts-only report focused on the S&P 500, Cyclicals/Defensives, Growth/Value, and Small/Large. Many of the charts are self-explanatory; to some we have added a short commentary. The charts cover macro, valuations, fundamentals, technicals, and the uses of cash. Our goal is to equip you with all the data you need to make investment decisions along these style dimensions. We also include performance, valuations, and earnings growth expectations tables for all styles, sectors, industry groups, and industries (GICS 1, 2 and 3). We hope you will find this publication useful. We alternate between Style and Sector chart packs updates on a bi-monthly basis. Overarching Investment Themes Macro Is bad news good news again? Investors are caught in crosscurrents of worries and deteriorating economic data. The Citigroup Economic Surprise index is in negative territory (Chart 1) – yet the US equity market defies gravity. The bad news is good news again, as it gives the Fed cover to keep a loose monetary policy for longer. Tapering: The Fed has broadcast its plans for tapering well in advance, and Fed Chair Jay Powell’s Jackson Hole speech, with its many caveats and uncertain timetable, produced a muted reaction from financial markets. However, investors exhaled with relief, when Powell explicitly separated the decision to taper from the timing of the first rate hike, conditioned on full employment, which is “a long way off”. Covid-19 Delta variant has caught investors off guard: "What does not kill us, mutates and tries again”. While a new wave of infections has dented consumer activity, there are early signs that it is cresting (Chart 2). Delta scare was a key reason for the underperformance of consumer services and cyclical stocks over the summer. Once fears of Delta subside, these groups will bounce back. Chart 1US Economic Data Disappoints

US Economic Data Disappoints

US Economic Data Disappoints

Chart 2Delta Infections Are Cresting

Delta Infections Are Cresting

Delta Infections Are Cresting

Supply chain disruptions are still rampant: Shipping costs have soared again in recent months: After falling below 10 this summer, the number of anchored containers ships waiting to offload in the West Coast ports has spiked again to 40, a level last seen in January 2021. Container freight costs have increased nearly five-fold from pre-pandemic levels (Chart 3). There are also significant backlogs of goods (Chart 4), and inventories have been drawn down to all-time low. It will take time for supply chains to normalize, with most industry participants expecting the situation to improve only in 2022. Chart 3Transportation Costs Have Surged

Transportation Costs Have Surged

Transportation Costs Have Surged

Chart 4Supply Chain Bottlenecks Are Not Abating

Supply Chain Bottlenecks Are Not Abating

Supply Chain Bottlenecks Are Not Abating

Labor shortages: : Companies are still struggling to fill job openings: There are 10 million job openings to slightly over eight million job seekers (Chart 5). That puts upward pressure on wages and increases companies’ costs. Disappointing jobs report: It is confounding, given strong demand for workers, that August payroll grew only by 235,000 jobs. While this low number may have resulted from the Delta hit to service industries, jobs data is volatile, and revisions are common. Next month's report will be a decisive data point for the Fed’s tapering timing decision. Chart 5Plenty Of Job Openings To Fill

Plenty of Job Openings To Fill

Plenty of Job Openings To Fill

Chart 6Inflation Is Broadening

Inflation Is Broadening

Inflation Is Broadening

Companies continue rising prices: Good news for corporate America is that its pricing power remains high, with 45% of companies planning on passing surging labor and supply costs on to consumers. This leads to a broadening of inflation across categories, with even trimmed means significantly overshooting 2% (Chart 6). While pricing power protects against significant margin compression, former peak margins are elusive. Consumer mood has soured: Consumers are well-aware of rising prices and expect inflation to exceed 6.5% within 12 months - high inflation is becoming embedded into consumer behavior and may become a self-fulfilling prophecy. The consumer confidence reading has slumped to a six-month low of 114 from 125 a month earlier. Many consumers have also postponed durable goods and house purchases discouraged by soaring prices and low inventories (Chart 7). Quality balance sheets outperformed: The wall of worries has resulted in strong balance sheet equities outperforming weak ones. This is also consistent with the classical performance of assets during the slowdown stage of the business cycle (Chart 8). Chart 7Consumer Are Discouraged By Prices And Shortages Of Inventory

Consumer Are Discouraged By Prices And Shortages Of Inventory

Consumer Are Discouraged By Prices And Shortages Of Inventory

Chart 8Strong Balance Sheet Companies Outperformed During The Slowdown

Strong Balance Sheet Companies Outperformed During The Slowdown

Strong Balance Sheet Companies Outperformed During The Slowdown

Valuations and Profitability Q2-2021 earnings season was remarkable both in terms of growth delivered (96% yoy%), and earnings surprise (88%). Earnings have grown at a 14% compound rate since 2019: Chart 9Earnings Growth Is Returning To Trend

US Equity Chart Pack

US Equity Chart Pack

Now earnings have returned to trend, and we expect normalization of growth. Analysts expect flat QoQ growth for the next three quarters. These are timid expectations; barring a black swan event, earnings growth is likely to surprise on the upside (Chart 9). Earnings growth will provide the necessary impetus for the US equity markets to move higher, with the driver of returns shifting from multiple expansion to earnings growth and cash disbursements to shareholders. Valuations remain elevated with the S&P 500 trading at 21x forward earnings. However, this level of valuations is more of a speed limit for future gains as opposed to a harbinger of a bear market. Sentiment Buy the dip investor mentality prevails. The S&P 500 has not had a 10% correction for nearly a year. This can be explained by FOMO (fear of missing out), and $2 trillion in excess savings in the US: cash that many retail investors aim to park in US equities. Retail flows into domestic equities have been exceptionally strong (Chart 10). Uses of Cash Share buybacks and other shareholder-friendly activities are on the rise again and are expected to gain steam this year and next. S&P 500 buybacks have increased from $120B reported two months ago to nearly $180B – impressive. This is another driver of returns in addition to earnings growth (Chart 11). Chart 10Retail Investors Buy On Dips

Retail Investors Buy On Dips

Retail Investors Buy On Dips

Chart 11Buybacks Are A Driver Of Returns

Buybacks Are A Driver Of Returns

Buybacks Are A Driver Of Returns

Investment Implications Low for longer: Fed’s dovish stance, Delta scare, and deteriorating economic growth data suggest that rates are likely to remain “low for longer”, and tapering may be postponed till January 2022. S&P 500: We expect US equities to perform well into the balance of the year on the back of an easy fiscal and monetary policy and steady earnings growth. Growth vs Value: Economic growth continues to slow, the Delta variant is still at the forefront of investor worries, and the Fed is dovish: Interest-rate sensitive stocks, such as Growth and Technology sector will continue outperforming. Cyclicals vs Defensives: We expect consumer cyclicals to start performing again once the onset of Delta dissipates, and more people are willing to travel and eat out. We believe that this is imminent and we are watching Delta stats closely. We also believe that parts of the Industrial sector most exposed to restocking of inventories, infrastructure, and construction will perform strongly. Small vs Large: Small is an “out of the gate” asset class, which tends to surge at the first whiff of recovery. Recently, Small started outperforming on the news that the number of new Delta cases is rolling over. Small is cheap relative to Large, and most of the earnings downgrades are already in the price. We are getting more constructive on this asset class. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com S&P 500 Chart 12Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 13Profitability

Profitability

Profitability

Chart 14Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Chart 15Uses Of Cash

Uses Of Cash

Uses Of Cash

Cyclicals Vs Defensives Chart 16Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 17Profitability

Profitability

Profitability

Chart 18Valuation And Technicals

Valuation And Technicals

Valuation And Technicals

Chart 19Uses Of Cash

Uses Of Cash

Uses Of Cash

Growth Vs Value Chart 20Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 21Profitability

Profitability

Profitability

Chart 22Valuations And Technicals

Valuations And Technicals

Valuations And Technicals

Small Vs Large Chart 23Macroeconomic Backdrop

Macroeconomic Backdrop

Macroeconomic Backdrop

Chart 24Profitability

Profitability

Profitability

Chart 25Valuations And Technicals

Valuations and Technicals

Valuations and Technicals

Chart 26Uses Of Cash

Uses Of Cash

Uses Of Cash

Recommended Allocation . Footnotes

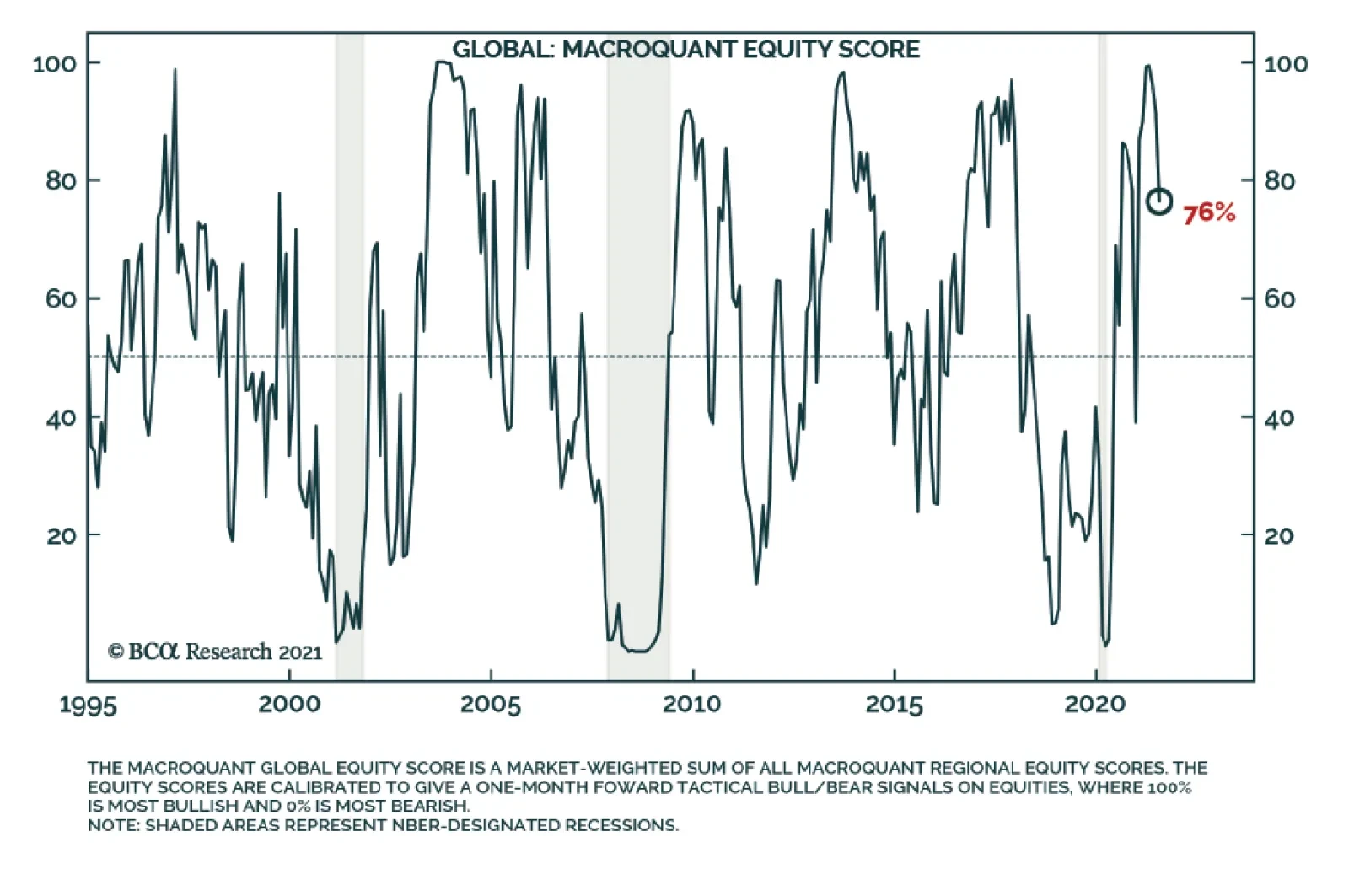

Our colleagues at BCA Research's Equity Analyzer team recently updated their MacroQuant model for equity investors. The model uses macroeconomic data to provide tactical investment recommendations and is calibrated to assist asset allocators in their decision…

Highlights A decline in the marginal propensity to spend out of both income and wealth over the past few decades generated a flood of excess savings. Facing a chronic shortfall of aggregate demand, central banks had no choice but to cut interest rates. This inflated asset prices. Looking out, the marginal propensity to spend should rise as household deleveraging pressures abate, retiring baby boomers shift from being savers to dissavers, and labor’s share of income increases. While rising bond yields will be a headwind to equities, continued above-trend global growth, upward earnings revisions, forthcoming Chinese fiscal stimulus, and a cresting in the number of new Delta variant cases all justify overweighting stocks on a 12-month horizon. A more cautious stance towards equities will be appropriate in two years’ time once stagflationary forces begin to assert themselves. The Keynesian Cross The “Keynesian Cross” is one of the first diagrams that students encounter in introductory macroeconomic courses (Chart 1). It simply plots Aggregate Expenditure (AE) versus output (Y). Chart 1The Keynesian Cross

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

Aggregate expenditure consists of personal consumption, capital investment, government expenditure, and net exports: (1)

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

If spending exceeds output, inventories will decline, causing firms to raise production. In contrast, if output exceeds spending, inventories will increase, prompting companies to cut production. Hence, the economy gravitates towards a level of output where inventories are stable; that is, where AE is equal to Y. Importantly, this level of production may or may not correspond to full employment. Introducing Asset Prices The Keynesian Cross model does not explicitly include asset prices. However, this can be easily rectified by postulating that spending depends on both income and wealth. For example, let us express consumption as: (2)

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

In this equation, α is the marginal propensity to consume out of wealth (i.e., how much consumption rises for every dollar increase in wealth, W) while β is the marginal propensity to consume out of income, Y.1 An increase in asset prices will boost wealth, leading to more consumption. A Simple But Illuminating Identity Consider the case where inventories are stable. Substituting equation (2) into equation (1) and then dividing by Y yields: (3)

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

The equation above is an identity. It does not say that a change in one term must lead to a change in another term in any causal sense of the word. All it says is that the terms on the right-hand side of the equation must add up to one. Suppose, for example, that α or β were to decline. If that were to happen, consumption would fall, leading to lower output. In order to restore output to its original level, either wealth would need to rise or some combination of investment, government spending, and net exports would need to increase. Upward Pressure On Savings There are at least three reasons to think that α and β have declined since the early 1980s: Chart 2US Household Debt Burdens Have Eased Significantly Over The Past Decade

US Household Debt Burdens Have Eased Significantly Over The Past Decade

US Household Debt Burdens Have Eased Significantly Over The Past Decade

Deleveraging: The need for households in economies such as the US to repair their balance sheets in the aftermath of the Global Financial Crisis put upward pressure on desired savings, leading to a decrease in β. The inability to use the equity in one’s home to finance consumption also lowered α. To this day, outstanding home equity line of credit (HELOC) balances in the US are a shadow of their former selves (Chart 2). Demographics: Savings vary over the life cycle. In general, savings are highest between the ages of 35 and 60 (Chart 3). The percentage of households in developed economies in their peak savings years began to increase in the late 1970s. While the trend has reversed in recent years, the ratio of workers-to-consumers in most countries (the so-called “support ratio”) remains elevated (Chart 4). Inequality: Higher income households save a greater share of their incomes than lower income households. As Atif Mian, Ludwig Straub, and Amir Sufi documented at last week’s Jackson Hole symposium, the rise in income inequality since 1980 has pushed up desired savings, thus lowering β in the process (Chart 5). Likewise, there is evidence that wealthier households tend to spend less of every additional dollar of wealth than poorer households.2 To the extent that wealth inequality has also increased since 1980, α has declined. Chart 3ASavings Peak Around Middle Age (I)

Savings Peak Around Middle Age (I)

Savings Peak Around Middle Age (I)

Chart 3BSavings Peak Around Middle Age (II)

Savings Peak Around Middle Age (II)

Savings Peak Around Middle Age (II)

Chart 4AIncreased Desired Savings Corresponded To A Rise In Support Ratios (I)

Increased Desired Savings Corresponded To A Rise In Support Ratios (I)

Increased Desired Savings Corresponded To A Rise In Support Ratios (I)

Chart 4BIncreased Desired Savings Corresponded To A Rise In Support Ratios (II)

Increased Desired Savings Corresponded To A Rise In Support Ratios (II)

Increased Desired Savings Corresponded To A Rise In Support Ratios (II)

Chart 5Income Inequality Has Skewed The Composition Of Savings

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

The Need For Policy Support The decline in α and β over the past few decades could have been offset by an increase in investment or net exports. Unfortunately, at least in the US, that never happened (Chart 6). The US trade deficit in goods and services stood at 3.9% of GDP in Q2 of 2021, the highest in 12 years. The non-petroleum trade deficit is at a record high. Investment spending also remains below the levels reached in the pre-GFC period. The shortfall in aggregate demand put pressure on policymakers to spur the economy. The results were somewhat mixed. Looking at the US, government spending on goods and services rose substantially during the Great Recession. However, spending then proceeded to fall to multi-decade lows as a share of GDP by 2019 (Chart 7). Transfer payments were also broadly stable as a share of GDP in the decade leading up to the pandemic. The Trump tax cuts reduced government revenue by around 1.7% of GDP. However, as we have noted in the past, the impact of the tax cuts on aggregate demand was fairly small. Chart 6US Private Sector Investment Remains Below Its Pre-GFC Peak While The Non-Petroleum Trade Deficit Is At A Record High

US Private Sector Investment Remains Below Its Pre-GFC Peak While The Non-Petroleum Trade Deficit Is At A Record High

US Private Sector Investment Remains Below Its Pre-GFC Peak While The Non-Petroleum Trade Deficit Is At A Record High

Chart 7Fiscal Policy Has Been More Reactive Than Proactive In The US

Fiscal Policy Has Been More Reactive Than Proactive In The US

Fiscal Policy Has Been More Reactive Than Proactive In The US

After surging during the pandemic, both direct government expenditure and transfer payments have come off their highs. Tax rates are also likely to rise for upper income earners and corporations. Nevertheless, with Congress set to pass a $550 billion infrastructure bill and a $3.5 trillion budget reconciliation bill, US fiscal policy will remain more stimulative over the next few years than it was in the pre-pandemic period. The same is likely to be true outside the US (Chart 8). Chart 8Fiscal Policy: Tighter But Not Tight

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

Central Banks To The Rescue This brings us to monetary policy. In the post-GFC period, lower interest rates helped keep capital investment from falling more than it would have otherwise. In addition, lower rates discouraged savings, thus supporting consumption. And, with other central banks also cutting rates, the decision by the Fed to maintain low rates prevented the dollar from strengthening excessively. Beyond the direct benefits to the economy, lower rates increased the prices of long-duration assets such as equities and homes. This raised W in the equations above. The resulting “wealth effect” stoked consumer spending, while also encouraging new investment (particularly in real estate). Excess Savings Should Diminish Looking out, there are a few reasons to think that α and β will begin trending higher, leading to more spending and less need for ultra-accommodative monetary policies: Chart 9Wealth Accumulation Through The Ages

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

Deleveraging pressures have abated. In the US, the ratio of household debt-to-disposable income has returned to pre-housing bubble levels. Debt-servicing costs are at a multi-decade low. Baby boomers are leaving the labor force. They hold over half of US household wealth, considerably more than younger generations (Chart 9). As baby boomers transition from being net savers to net dissavers, national savings will fall. Chart 10A Tight Labor Market Eventually Bolsters Wages

A Tight Labor Market Eventually Bolsters Wages

A Tight Labor Market Eventually Bolsters Wages

Governments are working to mitigate income inequality. Not only are redistributionist policies increasingly in vogue, but policymakers are trying to run economies hot. Historically, a tight labor market has curbed income inequality, while driving up workers’ share of overall income (Chart 10). Upside For Bond Yields, Both Near And Far Bond yields in the major economies likely hit a generational low last summer. Yields should rise over the coming years, first as slack diminishes, and later as structural forces reduce the amount of excess savings sloshing around the global economy. In the near term, a cresting of the Delta variant wave will prop up Treasury yields. While the number of new cases in the US continues to rise, the second derivative has turned for the better. A heat map shows that the weekly growth in new cases has slowed substantially in most US states (Chart 11). Chart 11The Delta Variant Wave Is Fading In The US

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

Globally, the Delta variant wave is abating (Chart 12). The transmission rate has clearly peaked within the G7 (Chart 13). The number of cases has begun to fall in recent hot spots such as Indonesia and Thailand. And, after rising above 100, the 7-day average of new cases in China has fallen back to 30. Chart 12The Delta Wave Is Cresting

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

Chart 13The Covid Transmission Rate Is Falling Again

The Covid Transmission Rate Is Falling Again

The Covid Transmission Rate Is Falling Again

The tapering of bond purchases by the major central banks should also lift yields. Canada began tapering this past April. BCA’s fixed-income experts expect the Fed to start paring back purchases by the end of this year, with the ECB and BoE following suit in early 2022. We do not expect bond markets to become unhinged. Central banks would strongly push back against an excessive rise in yields. Nevertheless, a move in the US 10-year Treasury yield to 1.8% by early next year seems reasonable. Stocks Can Withstand Rising Bond Yields… For Now Chart 14Equity Valuations and Real Bond Yields Have Tended To Move In Tandem

Equity Valuations and Real Bond Yields Have Tended To Move In Tandem

Equity Valuations and Real Bond Yields Have Tended To Move In Tandem

Equity valuations have broadly tracked real bond yields over the past few years (Chart 14). While higher yields will weigh on equity prices, there are a number of remaining tailwinds for stocks: Growth will remain above trend in the foreseeable future: Bloomberg consensus estimates foresee the global economy growing at an above-trend pace well into next year (Table 1). We agree with this assessment, and in fact, see upside risks to consensus growth forecasts. In particular, Chinese growth is likely to accelerate later this year as credit growth rebounds and fiscal spending increases. Local governments used less than 40% of their annual debt issuance quotas as of the end of July. Typically by that time of the year, they have used 70% of their quotas. Table 1Global Growth Will Remain Above Trend Well Into Next Year

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

Forward earnings estimates will continue to drift higher: Analysts are usually too optimistic. As a result, they normally have to cut estimates over the course of the calendar year. This year has been different (Chart 15). In early July, analysts expected S&P 500 companies to generate about $45 in EPS in Q2. In the end, they generated about $53. Earnings are projected to decline in absolute terms in Q3 and remain below Q2 levels until the second quarter of next year, when they are anticipated to grow by a meagre 3.5% year-over-year (Table 2). As earnings estimates move up, stock prices will rise, even if P/E multiples move sideways. Chart 15Unusually, Analysts Have Been Revising Earnings Estimates Higher This Year

Unusually, Analysts Have Been Revising Earnings Estimates Higher This Year

Unusually, Analysts Have Been Revising Earnings Estimates Higher This Year

Table 2US Earnings Estimates Have Upside

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

Rising inflation expectations will lift nominal bond yields more than real yields: Investors expect inflation to come down rapidly over the coming months (Chart 16). The 5-year/5-year forward TIPS breakeven inflation rate is below the Fed’s comfort zone of 2.3%-to-2.5% (Chart 17).3 We think that US inflation will fall fast enough over the next few quarters to allow the Federal Reserve to maintain a fairly accommodative monetary stance, but not as fast as markets are discounting. Chart 16Investors Expect Inflation To Fall Rapidly From Current Levels

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

The global equity risk premium remains elevated: We measure the equity risk premium (ERP) by subtracting the real 10-year bond yield from the forward earnings yield.4 Based on this measure, the global ERP stands at 634 bps (Chart 18). At the peak of the stock market boom in 2000, the global ERP was barely positive. Even in the US, where valuations are more stretched than abroad, the ERP stands at 574 bps. Remarkably, this is almost exactly where the ERP was in May 2008. An increase in the US 10-year Treasury yield to 1.8% by early next year – representing roughly a 50 basis-point increase from current levels in nominal terms and even less in real terms – would still leave US stocks attractively priced relative to bonds. Chart 17Below The Fed's Comfort Zone

Below The Fed's Comfort Zone

Below The Fed's Comfort Zone

In summary, investors should remain overweight global equities on a 12-month horizon. A more cautious stance towards stocks will be appropriate in two years’ time once stagflationary forces begin to assert themselves. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Chart 18The Global Equity Risk Premium Remains Elevated

The Global Equity Risk Premium Remains Elevated

The Global Equity Risk Premium Remains Elevated

Footnotes 1 Note that Gross Domestic Product should theoretically equal Gross Domestic Income. Thus, Y can denote either income or output. 2 For example, in a sample of five euro area economies, the European Central Bank found that the marginal propensity to consume out of wealth is higher for households at the lower end of the wealth distribution. 3 The Federal Reserve targets an average inflation rate of 2% for the personal consumption expenditures (PCE) index. The TIPS breakeven is based on the CPI index. Due to compositional differences between the two indices, CPI inflation has historically averaged 30-to-50 basis points higher than PCE inflation. This is why the Fed effectively targets a CPI inflation rate of about 2.3%-to-2.5%. 4 It is necessary to subtract the real bond yield, rather than the nominal bond yield, from the earnings yield because the earnings yield provides an estimate of the real total expected return to shareholders. For further discussion on this, please see Appendix A of the Global Investment Strategy Special Report, “TINA To The Rescue?” dated August 23, 2019. Global Investment Strategy View Matrix

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

Special Trade Recommendations

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

Current MacroQuant Model Scores

Financial Markets Face The Keynesian Cross

Financial Markets Face The Keynesian Cross

Weekly Performance Update For the week ending Thu Sep 02, 2021 The Market Monitor displays the trailing 1-quarter performance of strategies based around the BCA Score. For each region, we construct an equal-weighted, monthly rebalanced portfolio consisting of the top 3 stocks per sector and compare it with the regional benchmark. For each portfolio, we show the weekly performance of individual holdings in the Top Contributors/Detractors table. In addition, the Top Prospects table shows the holdings that currently have the highest BCA Score within the portfolio. For more details, click the region headers below to be redirected to the full historical backtest for the strategy. BCA US Portfolio

Market Monitor (Sep 2, 2021)

Market Monitor (Sep 2, 2021)

Total Weekly Return BCA US Portfolio S&P500 TRI 1.49% 1.54% Top Contributors AMN:US MPLX:US CQP:US PSA:US CBRE:US Weekly Return 21 bps 17 bps 17 bps 14 bps 14 bps Top Detractors GOLF:US ESGR:US NUE:US AN:US TGT:US Weekly Return -9 bps -8 bps -7 bps -7 bps -4 bps Top Prospects ESGR:US TX:US SC:US BRK.A:US PFE:US BCA Score 98.20% 97.97% 97.36% 96.72% 96.04% BCA Canada Portfolio

Market Monitor (Sep 2, 2021)

Market Monitor (Sep 2, 2021)

Total Weekly Return BCA Canada Portfolio S&P/TSX TRI 1.76% 1.48% Top Contributors CTS:CA PXT:CA CS:CA GIB.A:CA TOU:CA Weekly Return 44 bps 41 bps 22 bps 20 bps 19 bps Top Detractors RUS:CA AND:CA TOY:CA NWC:CA WIR.UN:CA Weekly Return -17 bps -13 bps -9 bps -8 bps -4 bps Top Prospects RUS:CA WIR.UN:CA LNF:CA HCG:CA PXT:CA BCA Score 99.37% 96.68% 95.39% 94.62% 94.14% BCA UK Portfolio

Market Monitor (Sep 2, 2021)

Market Monitor (Sep 2, 2021)

Total Weekly Return BCA UK Portfolio FTSE 100 TRI 3.18% 0.74% Top Contributors MXCT:GB NVTK:GB NFC:GB INDV:GB ROSN:GB Weekly Return 59 bps 36 bps 23 bps 19 bps 18 bps Top Detractors VTC:GB EMIS:GB BPCR:GB AAF:GB POLR:GB Weekly Return -10 bps -2 bps -1 bps -1 bps 1 bps Top Prospects SVST:GB CKN:GB FXPO:GB ROSN:GB VVO:GB BCA Score 99.31% 98.34% 96.50% 96.41% 96.39% BCA Eurozone Portfolio

Market Monitor (Sep 2, 2021)

Market Monitor (Sep 2, 2021)

Total Weekly Return BCA EMU Portfolio MSCI EMU TRI 1.18% 1.30% Top Contributors ALTA:FR FSKRS:FI BSL:DE FDJ:FR CDI:FR Weekly Return 25 bps 21 bps 18 bps 17 bps 15 bps Top Detractors STO3:DE FLUX:BE LEG:DE TL5:ES SOLV:BE Weekly Return -23 bps -11 bps -8 bps -7 bps -6 bps Top Prospects HLAG:DE LOG:ES STR:AT ALB:ES SOLV:BE BCA Score 99.13% 98.84% 97.66% 96.37% 95.01% BCA Japan Portfolio

Market Monitor (Sep 2, 2021)

Market Monitor (Sep 2, 2021)