Equities

Trump’s immigration policies are protecting the US economy from a sharp rise in unemployment but steering it into a ‘mini stagflation’. Plus: a new tactical trade is to underweight global technology (IXN).

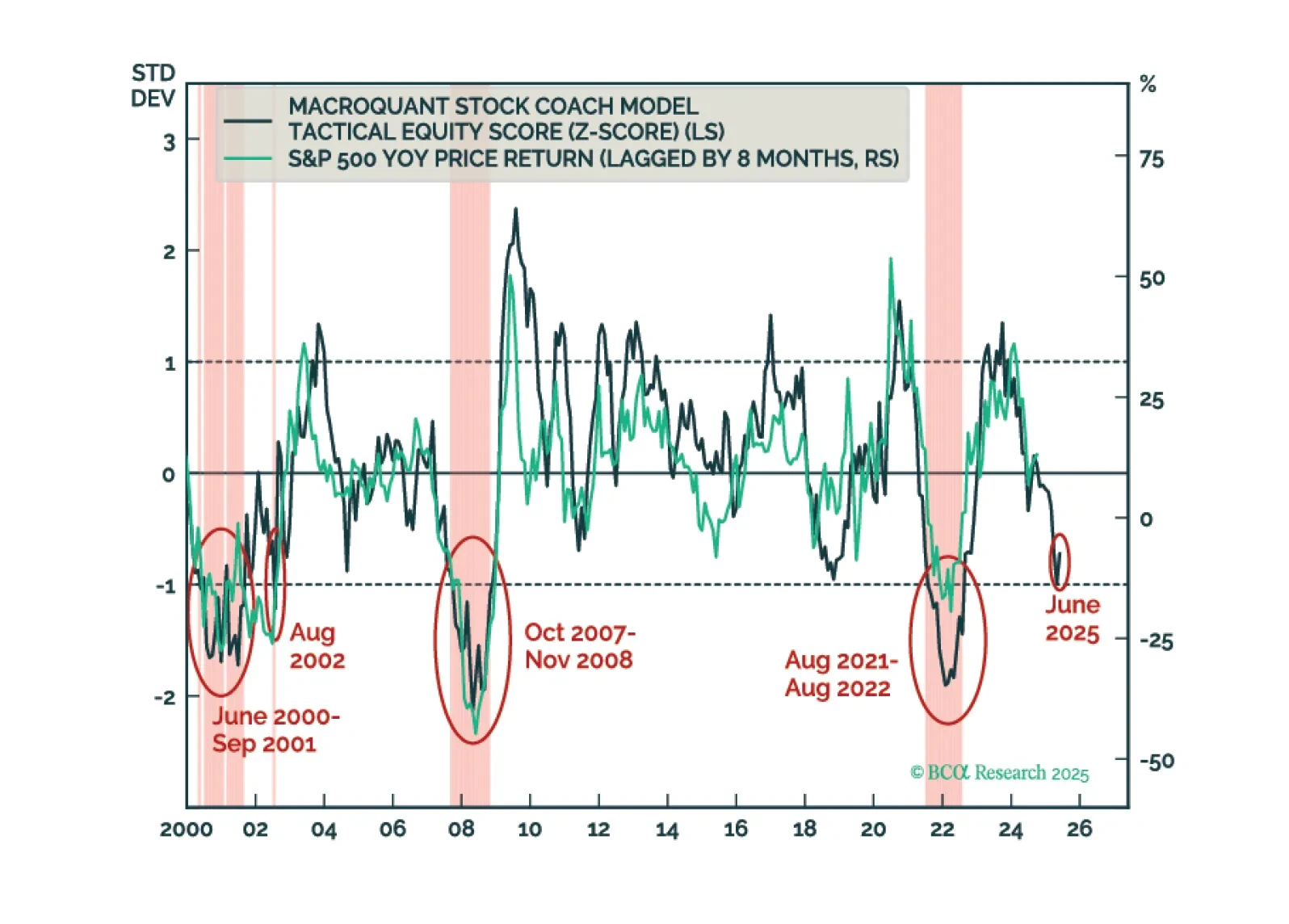

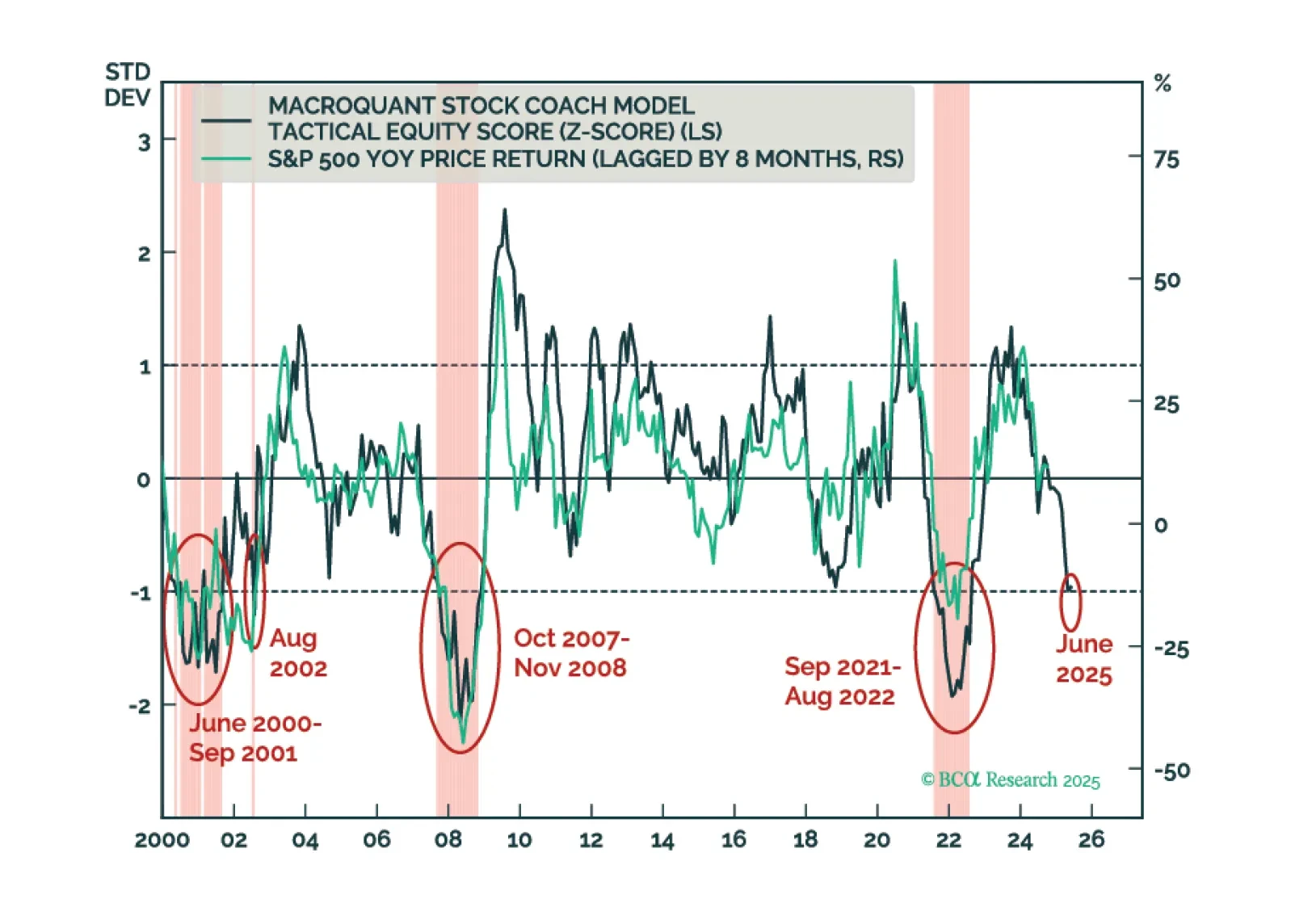

MacroQuant’s US equity z-score is dangerously close to the -1 threshold. Moves below that threshold have reliably coincided with equity bear markets in the past. As such, MacroQuant recommends an underweight on stocks, offset by an overweight on bonds and cash.

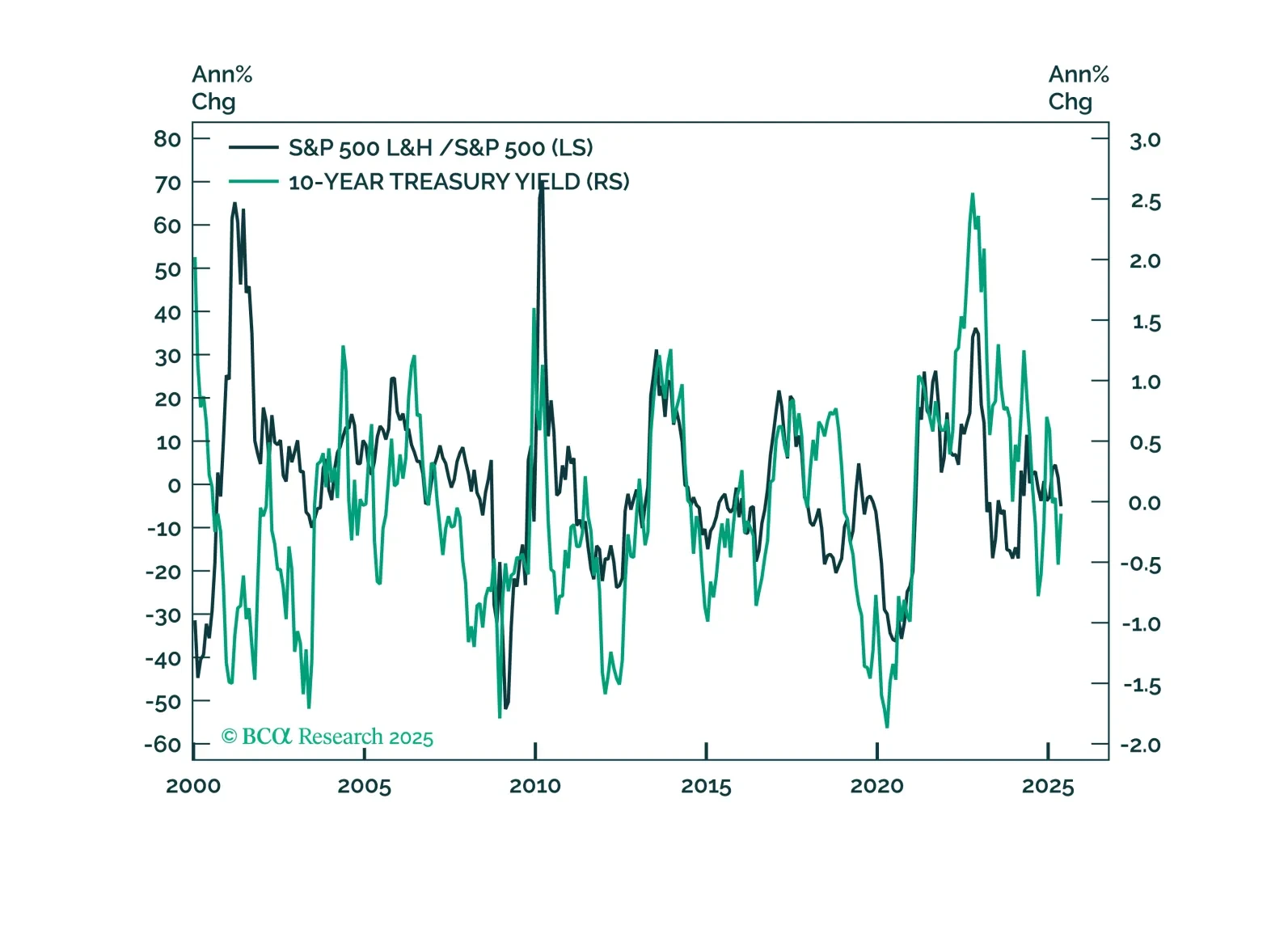

The Life and Health Insurance industry offers downside protection and portfolio diversification in the event of a market correction, surging inflation, or stubbornly high interest rates.

This week our three screeners explore: UK stocks that are cheap and offer a geopolitical hedge; French stocks that are sensitive to China; and US Value and dividend paying stocks.

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

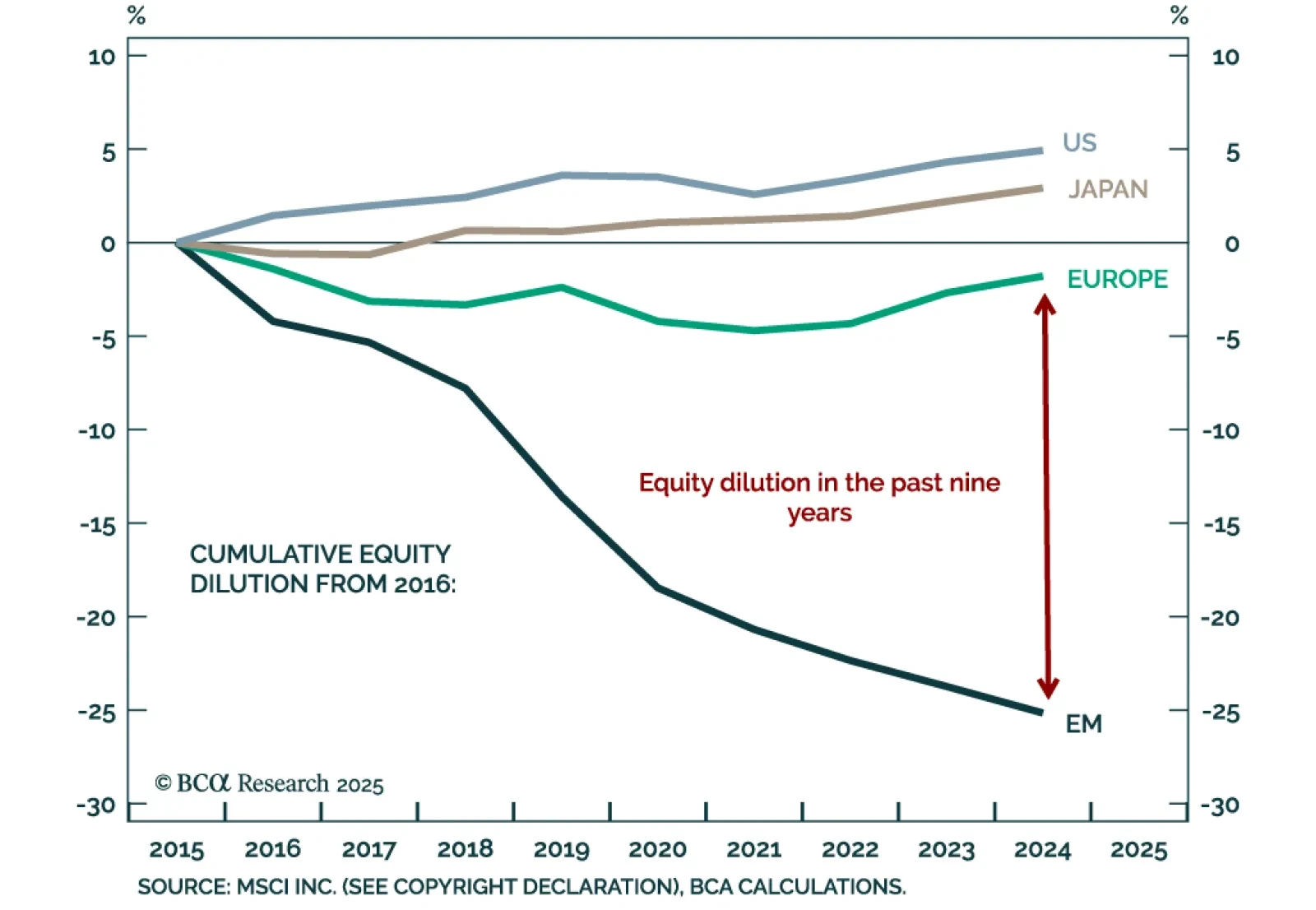

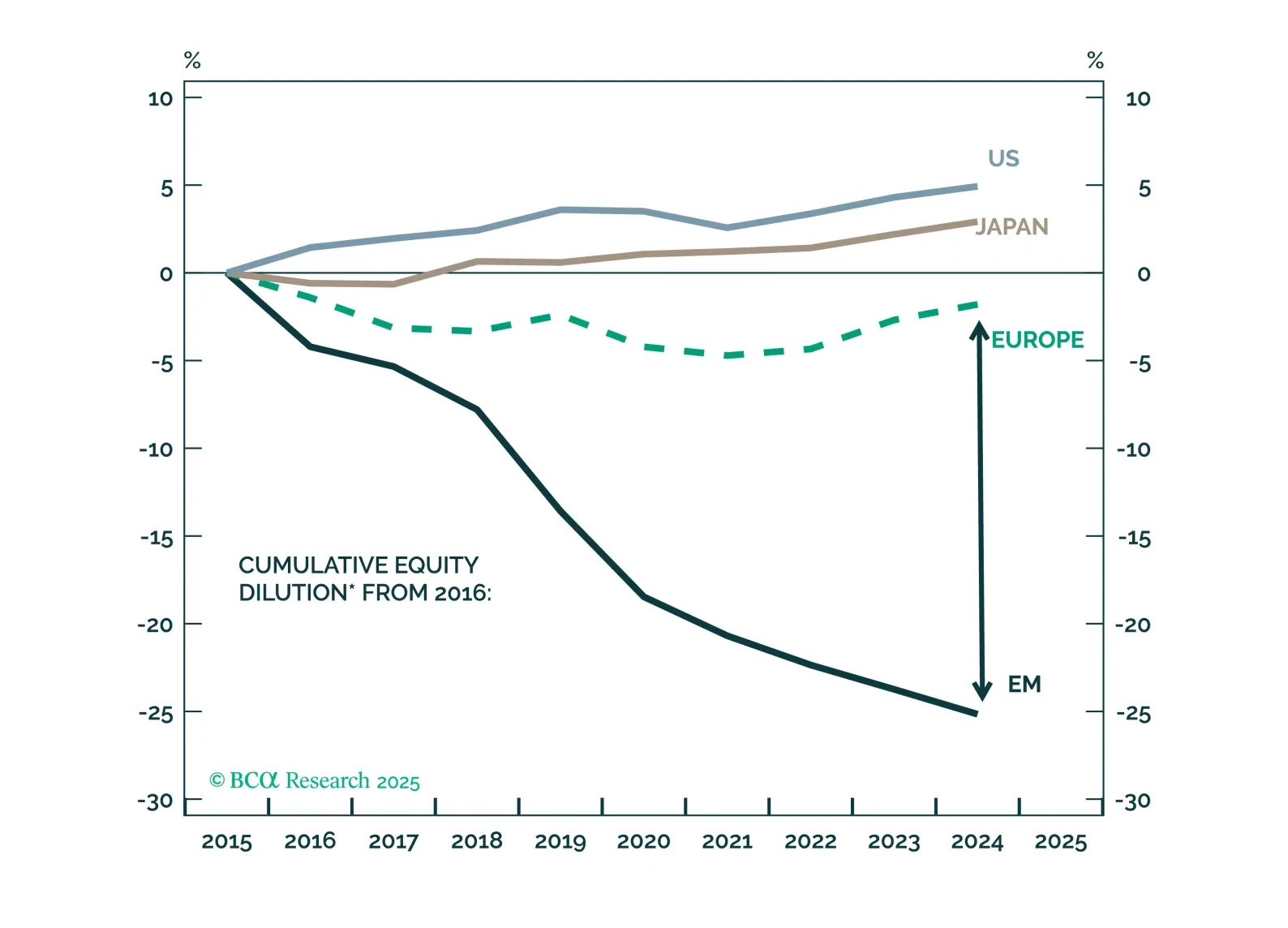

Dilution is one of the two main reasons why EM EPS has been much weaker than EM GDP and EM non-diluted profits. We calculate “pure” dilution – adjusted for companies’ inclusion and exclusion from the stock index – for various bourses around the world. To our knowledge, this is the first time this analysis has been conducted.