Equities

Highlights Economy – The inevitable deceleration has arrived, but the economy is still growing far faster than trend and will continue to do so through 2022: A wide range of data series shows that US growth has likely peaked but deceleration from way, way above the long-run potential growth rate to way above it is not cause for concern. Markets – Growth worries pulled equities lower for one day last week before investors rushed back in to buy the dip: Stock volatility made a brief return at the beginning of the week before the S&P 500 snapped back to resume taking aim at new highs. Fundamentals supported the reversal as earnings are on a path to blow away expectations for the fifth consecutive quarter. Strategy – Investors should stay the course by overweighting risk assets in multi-asset portfolios: As long as the spread of the Delta variant does not lead to punishing new restrictions, the economy will continue to grow at an extremely rapid clip and the strong-growth, easy-policy backdrop will continue to support equities and credit. Feature The S&P 500 had its worst one-day performance since early April last Monday, shedding 1.6% and sending the VIX above 20 for only the ninth time since it broke into the teens in March (Chart 1). We do not read too much into day-to-day moves in financial markets, but the tumult seems to have resulted from equities’ delayed reaction to investor unease about decelerating growth. It makes intuitive sense that forward-looking markets often assign greater importance to the direction of a key data series than its level. In Wayne Gretzky terms, the level is largely an indication of where conditions have been, while the direction offers more insight into where they are headed. Direction does not always trump level, however, and investors should bear in mind that the current pace of growth is extremely elevated. The Bloomberg consensus of economists is calling for 6.6% real GDP growth in 2021 and 4.2% in 2022. Those figures project a tapering, especially from quarter to quarter (Table 1), but they still represent red-hot growth for an economy with an annual long-term potential growth rate in the range of 1.75% to 2%. They also reflect a gentle tapering, with growth expected to remain comfortably above trend through 2023. Chart 1Lower Highs, Lower Lows

Lower Highs, Lower Lows

Lower Highs, Lower Lows

Table 12% Is So Last Decade

Thrill Ride

Thrill Ride

We are far less concerned about deceleration from high single-digit growth than we would be about sub-trend readings. Falling below trend was the persistent fear in the aftermath of the Global Financial Crisis when economists and investors alike worried that the economy would not be able to stay above stall speed. Growth likely peaked in the second quarter, and supply bottlenecks and wavering confidence in the face of the spread of COVID-19’s Delta variant have brought the economic surprise index back down to earth (Chart 2). To take one example of a series that recently generated a negative surprise, however, we think the month-over-month decline in the ISM non-manufacturing index has less to say about the economy than its fourth straight reading in the 60s, a level it had reached just eight times in the previous 23 years (Chart 3). Chart 2The Economy Is Cooling Off, ...

The Economy Is Cooling Off, ...

The Economy Is Cooling Off, ...

Chart 3... But It's Still Quite Hot

Thrill Ride

Thrill Ride

Is The Bond Market Trying To Warn Us? Chart 4Inflation Fears Have Ebbed

Inflation Fears Have Ebbed

Inflation Fears Have Ebbed

We did not foresee the steep decline in 10-year Treasury yields that has played out since mid-June and it has led us to ask if underlying economic conditions are weaker than we perceived. Based on the available data, we do not think so. It seems like the rally in long-dated Treasuries can be attributed to an unwinding of inflation fears, concerns about slowing growth and the reversal of a Treasury sell-off that had gone too far too fast. We remain constructive on the economy, assuming vaccine-resistant COVID-19 variants do not emerge, and we still expect the 10-year Treasury yield will end the year north of 1.75%. Inflation fears have cooled considerably, with 10-year TIPS breakevens having retreated to the lower end of the Fed’s desired range, while the 5-year-on-5-year series (the 5-year breakeven five years from now) has dropped out of it (Chart 4). Though we do not expect inflation to become a problem for the economy for another couple of years, we do expect that it will re-emerge as a worry for investors once the primary impediments to labor supply disappear in September, especially if the year-over-year CPI readings continue to come in way above 2%. Our Global Fixed Income Strategy service stresses that investors should watch the mix of components driving inflation. If accelerated wage gains appear to be on their way to becoming entrenched or the rate of growth in rents inflects higher, the transitory inflation narrative might begin to weaken, leading the Fed to dial back accommodation sooner and/or faster than the bond market currently anticipates. Though we are not concerned about a widely anticipated peak in the rate of growth, a revival of COVID-19 after it seemed to have been defanged would throw a spanner into the works. A surge in new infections, even in countries like the UK and the US which have been ahead of the pack in terms of vaccinations, indicates that the Delta variant is especially transmissible. The spike in infections here (Chart 5, top panel) and abroad has apparently dampened economic optimism, helping to push Treasury and other developed world sovereign yields lower. The good news, however, is that the Delta variant does not appear to be particularly lethal (Chart 5, bottom panel) and the leading Pfizer and Moderna vaccines have acquitted themselves well against it. We are watching virus developments carefully, but we do not yet see evidence that suggests new rounds of activity restrictions are in store and we therefore expect virus variants will ultimately have little economic impact. Chart 5The Delta Variant Is More Contagious But Less Serious

The Delta Variant Is More Contagious But Less Serious

The Delta Variant Is More Contagious But Less Serious

Aside from the pendulum shifting from too-hot concerns to too-cold concerns, much of the Treasury rally appears to have been a reaction to the speed and extent of the backup in yields. Our Global Fixed Income Strategy colleagues point out that Treasuries became quite oversold in the first quarter. The 10-year yield got as far above its 200-day moving average as it did during the taper tantrum in 2013 (Chart 6, second panel), with both real-money investors (Chart 6, third panel) and speculators (Chart 6, bottom panel) shunning duration. Speculators have trimmed their short positions but the real money has yet to capitulate, suggesting that yields may be able to hang around current levels or edge even lower before returning to a level that better aligns with underlying economic strength, robust inflation readings and the future path of the fed funds rate. Earnings Continue To Crush Expectations Every equity investor is familiar with the earnings season dance. About halfway through the quarter, companies begin to guide analysts’ expectations lower. Analysts duly adjust their estimates down a few percentage points over the ensuing ten weeks before companies begin to report. Company earnings then come in about the level initially expected midway through the quarter and – voila! – three-quarters of S&P 500 constituents beat expectations and the overall index beats by around 3%. The typical pattern looks very much like it did across 2019 (Chart 7, top panel). Chart 6The Treasury Selloff Was Overdone

The Treasury Selloff Was Overdone

The Treasury Selloff Was Overdone

Chart 7Not The Same Old Song-And-Dance

Thrill Ride

Thrill Ride

Beginning with the second quarter of 2020, when the most stringent lockdown measures meant to stymie the spread of the pandemic were fully in force, the picture has been very different. S&P 500 constituents have barely guided down heading into earnings before proceeding to demolish estimates by close to 20% (Chart 7, bottom panel). The established practice of companies guiding analysts to position the bar at a height they think they can comfortably clear produced a narrow and consistent dispersion of earnings beats across the 32 quarters from 2012 to 2019, with a mean of 3.7% and a standard deviation of 1.4%, all clustered within a narrow 1-to-6% range (Chart 8). Chart 8Blasting Out Of The Old Range

Thrill Ride

Thrill Ride

Something else entirely has unfolded over the last four quarters, when earnings beat by an average of 19.5%, more than three times above the previous eight years’ peak and five times their mean. Even with the pandemic numbers pushing the mean higher and quadrupling the standard deviation, the four quarters’ beats have been 3.2, 2.2, 1.8 and 3.1 standard deviations above the mean, respectively. With a quarter of the S&P 500 having reported results through last Friday, the second quarter appears to be on a path to extend the blowout streak to five quarters (Chart 7, bottom panel). Investors, conditioned to the S&P 500 unfailingly beating earnings, don’t seem to be cognizant of how unusual the magnitude of the beats has been. Gigantic year-over-year earnings gains, which will peak this quarter, also seem to have obscured how low the bar has been set on a quarter-over-quarter basis. As our US Equity Sector Strategy colleagues have highlighted, year-over-year comparisons that span pandemic-distorted quarters are of limited use. To get a more relevant read, they compare 2021 results to 2019 results. (For the full year, 2021 earnings per share for the S&P 500 are projected to come in 18.2% above 2019, for 8.7% annualized growth). Table 2A Remarkably Low Bar

Thrill Ride

Thrill Ride

We have been tracking quarter-over-quarter changes and were surprised to see that forward four-quarter earnings were expected to decline 2% from their first-quarter run rate ($196.52, annualized) when the reporting season began, with the second quarter declining by 8% (Table 2). Given manifold signs of economic revival, an 8% sequential contraction strikes us as highly improbable. With real GDP expected to grow by 9% on an annualized quarter-over-quarter basis, or better than 12% in nominal terms, 2% growth seems reasonable, so we see $50 as a more realistic and easily attainable ballpark estimate, which would have earnings beat by 11%. Regardless of where earnings end up, the bar has been set extremely low – the analyst consensus has not forecasted contraction in any forward four-quarter period since 1980 (Chart 9). Our takeaway is that earnings estimates have scope to move higher, taking the S&P 500 with them if multiples don’t contract, or giving valuations a chance to cool if the index moves sideways or turns lower. Chart 9An Odd Time To Call For The First Contraction In 40 Years

An Odd Time To Call For The First Contraction In 40 Years

An Odd Time To Call For The First Contraction In 40 Years

Investment Implications Our investment strategy recommendations follow from our ongoing analysis of the business cycle, the credit cycle, the monetary policy cycle and (when applicable) the sentiment cycle. Although the consistency of our risk-friendly asset allocation recommendations may have begun to seem boring, nothing in our cycle analysis calls for a change in our views. There is no reason to expect a recession when households are sitting on $2.4 trillion of excess savings, household net worth has advanced at the fastest rate on record, retail inventories have been depleted to record-low levels and payrolls are set to continue expanding at a furious rate over the next year-plus. The credit cycle is set to continue its charmed path, as rising incomes, cash-stuffed households and businesses, and zero interest rate policy suppress borrower distress and keep lenders eager to make loans. Monetary policy may get incrementally less accommodative as asset purchases shrink, but a rate hike is more than a year away. One can make a reasonable argument that the Fed will be unable to lift the fed funds rate to a truly restrictive level in the next policy tightening cycle once it begins to hike rates, even if it’s not our base case. We are certain that monetary policy settings will remain extremely easy well beyond our one-year investment timeframe. Sentiment is generally buoyant, but it is not at extreme levels that would warrant factoring it into our strategy as a contrarian indicator. We will therefore stay the course, while monitoring pandemic developments and keeping a sharp lookout for signs that we’re wrong about inflation or growth. If we are correct that the threat from COVID-19 will remain contained, we expect that earnings revisions will ensure that the next catalyst for equities will be a positive one. The consensus expectation for a decline in the earnings run rate is simply incompatible with observed conditions on the ground. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com

Dear Client, I will be on vacation next week. In lieu of our regular report, we will be sending you a Special Report written by my colleague Arthur Budaghyan, BCA Research’s Chief Emerging Markets Strategist. Arthur’s report will discuss the long-term outlook for industrial companies. He argues that the US is entering an industrial boom prompted by infrastructure stimulus and onshoring. This will benefit US industrial equities, or ones selling into the US on a multi-year horizon. I trust you will find it insightful. Best regards, Peter Berezin, Chief Global Strategist Highlights Investors keep asking whether the recent increase in US inflation is transitory. However, this is the wrong question to ask. Annualized core CPI inflation reached 10.6% in the second quarter. There is little doubt that inflation will fall from such elevated levels. The key question that investors should be asking is whether inflation will decline more or less than what the market is discounting. The widely watched 5-year/5-year forward TIPS inflation breakeven rate has sunk to 2.11%, below the Fed’s “comfort zone” of 2.3%-to-2.5%. Thus, the market already expects a substantial decline in inflation. Our sense is that US inflation will come down fast enough to allow the Fed to maintain a highly dovish policy stance, but not as fast as market expectations currently imply. As inflation surprises on the upside, long-term bond yields will rise. This should revive bank shares and other reflationary plays. The combination of a weaker US dollar, faster sequential Chinese growth, increased vaccine supplies, and favorable valuations should all help EM stocks later this year. Go long the Vanguard FTSE Emerging Markets ETF (VWO) versus the Vanguard S&P 500 ETF (VOO). The Right Question About Inflation Chart 1After A Spike In Q2, US Inflation Will Decelerate

After A Spike In Q2, US Inflation Will Decelerate

After A Spike In Q2, US Inflation Will Decelerate

Investors remain focused on whether the recent bout of US inflation is transitory. However, this is not the correct question to be asking at the present juncture. The US core CPI rose by 10.6% at an annualized pace in Q2 relative to the first quarter (Chart 1). It is almost inevitable that inflation will come down from such high levels. The key question investors should be asking is whether inflation will decline more or less than what is already baked into market expectations. As Chart 2 shows, investors expect US inflation to come down rapidly over the next two years. The 5-year/5-year forward TIPS breakeven inflation rate – a good proxy for where investors expect inflation to be over the long haul – has sunk to 2.11% (Chart 3). This is below the Fed’s comfort zone of 2.3%-to-2.5%.1 Globally, long-term inflation expectations remain subdued (Chart 4). Chart 2Inflation Is Expected To Moderate Over The Coming Years

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

Chart 3Inflation Expectations Have Fallen Back Below The Fed's Target Zone

Inflation Expectations Have Fallen Back Below The Fed's Target Zone

Inflation Expectations Have Fallen Back Below The Fed's Target Zone

Chart 4Long-Term Inflation Expectations Remain Subdued

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

Inflation Will Fall, But… Our sense is that US inflation will come down fast enough to allow the Fed to maintain a highly dovish policy stance, but not as fast as market expectations currently imply. Broad-based inflationary pressures would make the Fed nervous. However, that is not what we are seeing. Wages have accelerated markedly in only a few relatively low-skilled sectors such as retail trade and leisure and hospitality (Chart 5). For the economy as a whole, wage growth is broadly stable (Chart 6). The expiration of extended unemployment benefits, the reopening of schools, and increased immigration should also boost labor supply in the fall. Chart 5Faster Wage Growth Has Been Confined To A Few Low-Wage Sectors

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

Chart 6No Sign Of A Wage-Price Spiral... For Now

No Sign Of A Wage-Price Spiral... For Now

No Sign Of A Wage-Price Spiral... For Now

On the price front, more than two-thirds of the increase in the core CPI in June stemmed from pandemic-afflicted sectors (Chart 7). The price of the median item within the CPI index rose by just 2.2% year-over-year in June, somewhat below the pre-pandemic pace of inflation (Chart 8). Chart 7Most Of The Recent Increase In Inflation Is Pandemic-Related

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

Chart 8The Median Price In The CPI Basket Is Up Only 2.2%

The Median Price In The CPI Basket Is Up Only 2.2%

The Median Price In The CPI Basket Is Up Only 2.2%

… Not As Fast As The Market Expects While inflation will fall as pandemic effects recede, investors are overestimating how fast this will happen. US growth has undoubtedly peaked, but at a very high level. Economists surveyed by Bloomberg estimate that US GDP rose by 9.0% in Q2. Growth is expected to slow to 7.1% in Q3 and 5.1% in Q4, while averaging 4.2% in 2022 (Table 1). By any standard, these are very strong, above-trend growth rates. Table 1Growth Is Peaking, But At A Very High Level

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

Chart 9Nearly 90% Of US Seniors Have Had At Least One Shot

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

The current Delta-variant wave is unlikely to slow US growth by very much. Although vaccination rates among younger people are at middling levels, they are quite high for the elderly who are most at risk of serious illness. Close to 89% of Americans above the age of 65 have received at least one shot, and nearly 80% are fully vaccinated (Chart 9). The 65+ age group accounts for four-fifths of all Covid deaths in the United States. Widespread vaccination coverage for older Americans will take pressure off the hospital system, allowing the economy to remain open. Fiscal Support In The US And Abroad As we noted last week, Senate Democrats are likely to use the reconciliation process to both raise the debt ceiling and pass President Biden’s $3.5 trillion American Jobs and Families Plan. They are also likely to move forward on Biden’s proposed $600 billion in infrastructure spending, with or without Republican support. Meanwhile, much of the fiscal stimulus that has already been undertaken has yet to make its way through to the economy. US households are sitting on about $2.5 trillion in excess savings, about half of which stems from increased government transfers (Chart 10). Chart 10A Lot Of Excess Savings

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

Chart 11Inventories Are At Low Levels

Inventories Are At Low Levels

Inventories Are At Low Levels

Satiating that demand has not been easy for many companies. Retail sector inventories are at record lows (Chart 11). The number of homes that have been authorized for construction but where building has yet to begin has increased by 62% since the start of the pandemic (Chart 12). By limiting production, supply-chain bottlenecks will push some spending towards the future. This will keep growth from decelerating more than it otherwise would. Outside the US, fiscal policy will remain supportive. All 27 EU countries ratified the €750 billion Next Generation fund on May 28th. The allocations from the fund for southern European countries are relatively large (Chart 13). Most of the money will be spent on public investment projects with high fiscal multipliers. Chart 12Growing Backlog Of New Home Construction Projects

Growing Backlog Of New Home Construction Projects

Growing Backlog Of New Home Construction Projects

Chart 13EU Fiscal Policy: Allocations To Southern European Countries Are Relatively Large

EU Fiscal Policy: Allocations To Southern European Countries Are Relatively Large

EU Fiscal Policy: Allocations To Southern European Countries Are Relatively Large

Chart 14Economic Growth In China Was Slow In H1

Economic Growth In China Was Slow In H1

Economic Growth In China Was Slow In H1

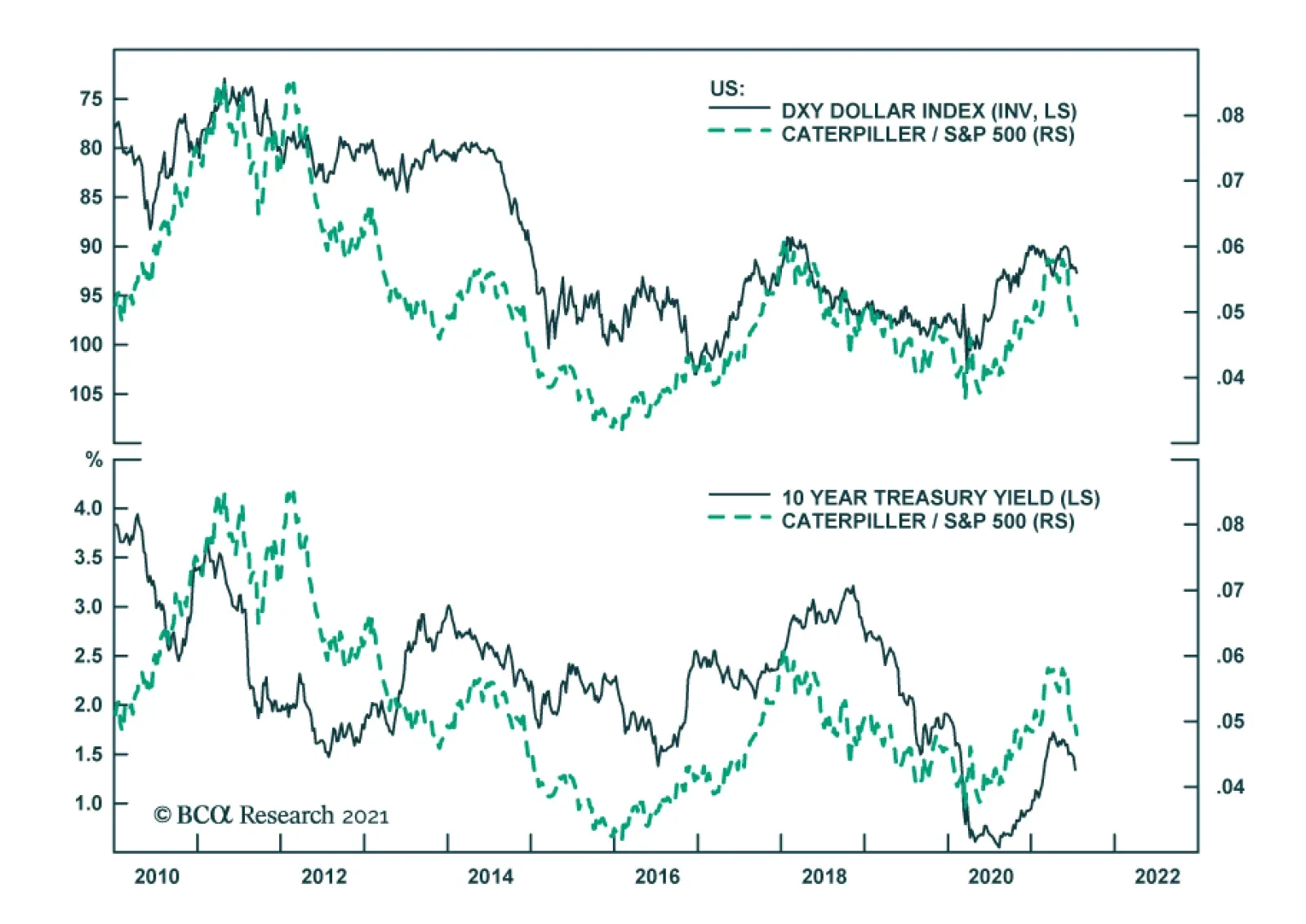

The Japanese government is contemplating sending stimulus checks to low-income citizens in advance of the general election due by October 22nd. It is an understandable move. Covid cases are rising again. As a result, the authorities have declared a state of emergency in Tokyo and barred spectators from attending the Olympic games in and around the city. Fortunately, the Japanese vaccination campaign has accelerated after a slow start. A third of the population has now received at least one shot. The government intends to vaccinate all eligible people by November. Looking at quarter-over-quarter growth rates, Chinese growth averaged just 3.8% on an annualized basis in the first half of 2021 (Chart 14). Growth should pick up in the second half of the year thanks in part to increased fiscal spending. As of June, local governments had used only 28% of their annual bond issuance quotas, compared with 61% over the same period last year and 65% in 2019. Most of the proceeds from local government bond sales will likely flow into infrastructure projects. Resumption Of The Dollar Bear Market Will Keep Inflation From Falling Too Far As a countercyclical currency, the US dollar usually weakens when global growth is strong (Chart 15). Short-term real interest rate differentials have moved sharply against the dollar, a trend that is unlikely to change anytime soon given the Fed’s dovish bias (Chart 16). While inflation in the US is not as sensitive to currency fluctuations as in most other countries, a weaker dollar will still lift tradeable goods prices (Chart 17). Chart 15The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Chart 16Rate Differentials Are A Headwind For The Dollar

Rate Differentials Are A Headwind For The Dollar

Rate Differentials Are A Headwind For The Dollar

Chart 17The Dollar And Inflation

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

Structural Forces Turning More Inflationary Not only are cyclical forces likely to turn out to be less disinflationary than investors believe, but many of the structural factors that have suppressed inflation over the past 40 years are reversing direction: Chart 18Globalization Plateaued More Than A Decade Ago

Globalization Plateaued More Than A Decade Ago

Globalization Plateaued More Than A Decade Ago

Globalization is in retreat: The ratio of global trade-to-manufacturing output has been flat for over a decade (Chart 18). Looking out, the ratio could even decline as more companies shift production back home in order to gain greater control over supply chains of essential goods. Baby boomers are leaving the labor force en masse. As a group, baby boomers hold more than half of US household wealth (Chart 19). They will continue to run down their wealth once they retire. However, since they will no longer be working, they will no longer contribute to national output. Continued spending against a backdrop of diminished production could be inflationary. Despite a pandemic-induced bounce, underlying productivity growth remains anemic (Chart 20). Slow productivity growth could cause aggregate supply to fall short of aggregate demand. Social stability is in peril, as exemplified by the recent dramatic increase in the US homicide rate. In the past, social instability and higher inflation have gone hand in hand (Chart 21). Perhaps most importantly, policymakers are deliberately aiming to run the economy hot. A tight labor market will eventually lift wage growth to a greater degree than what we have seen so far (Chart 22). Not only could higher wage growth push up inflation through the usual “cost-push” channel, but by boosting labor’s share of income, a tight labor market could spur aggregate demand. Chart 19Baby Boomers Have Accumulated A Lot Of Wealth

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

Chart 20Trend Productivity Growth Has Been Disappointing

Trend Productivity Growth Has Been Disappointing

Trend Productivity Growth Has Been Disappointing

Chart 21Historically, Social Unrest And Higher Inflation Move In Lock-Step

Historically, Social Unrest And Higher Inflation Move In Lock-Step

Historically, Social Unrest And Higher Inflation Move In Lock-Step

Chart 22A Tight Labor Market Eventually Bolsters Wages

A Tight Labor Market Eventually Bolsters Wages

A Tight Labor Market Eventually Bolsters Wages

Investment Implications Chart 23Positive Earnings Revisions Are At High Levels

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

The path to higher rates is lined with lower rates. The longer central banks keep interest rates below their neutral level, the more economies will overheat, and the more rates will eventually need to rise to bring inflation back down. For now, we are still in the warm-up phase to higher inflation. With long-term inflation expectations below target, central banks will be able to maintain accommodative monetary policies. This is good news for stocks, at least in the short-to-medium term. The recent wobble in equity markets has occurred despite a strong second quarter earnings season. According to the latest available data from I/B/E/S, 90% of S&P 500 companies have reported earnings above analyst expectations. Earnings have surprised on the upside by an average of 19.2%, compared to a historical average of 3.9%. Positive earnings revisions are at record high levels (Chart 23). Full year 2021 S&P 500 EPS estimates have risen 16% since the start of the year. Analysts have also raised their estimates for 2022 and 2023 (Chart 24). We continue to recommend that asset allocators favor stocks over bonds over a 12-month horizon. Chart 24Analysts Have Been Revising Up Earnings Estimates This Year

Analysts Have Been Revising Up Earnings Estimates This Year

Analysts Have Been Revising Up Earnings Estimates This Year

Chart 25The Gains Of Recent Winners Have Not Been Fully Mirrored In Relative Earnings Growth

The Gains Of Recent Winners Have Not Been Fully Mirrored In Relative Earnings Growth

The Gains Of Recent Winners Have Not Been Fully Mirrored In Relative Earnings Growth

Chart 26Bank Shares Thrive In A Rising Yield Environment

Bank Shares Thrive In A Rising Yield Environment

Bank Shares Thrive In A Rising Yield Environment

Tech stocks have outperformed the broader market over the past seven weeks. However, unlike during the pandemic, 12-month forward EPS estimates for tech have not risen in relation to other sectors (Chart 25). As long-term bond yields move back up, tech shares will underperform. In contrast, banks will benefit from higher yields (Chart 26). Along the same lines, US stocks have outpaced other stock markets by more than one would have expected based on relative EPS trends. Notably, EM earnings have moved sideways versus the US since mid-2019. Yet, US stocks have outperformed EM by 17% over this period. Today, the forward P/E ratio for EM stands at 13.8, compared to 22.1 for the US (Chart 27). The combination of a weaker US dollar, faster sequential Chinese growth, increased vaccine supplies, and favorable valuations should all help EM stocks later this year. Go long the Vanguard FTSE Emerging Markets ETF (VWO) versus the Vanguard S&P 500 ETF (VOO). Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Chart 27Wide Valuation Gap Between US And Non-US Markets

Wide Valuation Gap Between US And Non-US Markets

Wide Valuation Gap Between US And Non-US Markets

Footnotes 1 The Federal Reserve targets an average inflation rate of 2% for the personal consumption expenditures (PCE) index. The TIPS breakeven is based on the CPI index. Due to compositional differences between the two indices, CPI inflation has historically averaged 30-to-50 basis points higher than PCE inflation. This is why the Fed effectively targets a CPI inflation rate of about 2.3%-to-2.5%. Global Investment Strategy View Matrix

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

Special Trade Recommendations

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

Current MacroQuant Model Scores

Investors Are Asking The Wrong Question About Inflation

Investors Are Asking The Wrong Question About Inflation

Highlights The Delta variant will continue causing jitters but there is much greater evidence today than there was in early 2020 that humanity can curb the virus, both with vaccines and government stimulus. Delta jitters will reinforce the Fed’s dovishness and will, if anything, increase the odds that President Biden passes his mammoth spending package this fall. The very near term could easily see more volatility but by the end of the year the reflationary cast of global policy will have won the day. Tax hikes and rate hikes lurk beyond 2021. There is still no stabilization in US-China policy and the US and its allies have called out China for cyber aggression, signaling a new front of open competition. A cyber event is one of the leading contenders for the next negative shock to the global economy. Structural factors strongly support rising concerns among the global elite about cyber insecurity. Stick to this year’s key themes and views: long gold, long value over growth, long international stocks, long Mexico, long aerospace and defense, and short emerging market “strongmen” regimes. Feature Global equities sank and rose over the past week as investors struggled with “peak growth” in the US and China, the prospect of monetary policy normalization, and other risks on the horizon, including immediate concerns over the Delta variant of COVID-19. The rapid rebound, including for cyclicals like European stocks, suggested that investors are still buying the dip given a very supportive macro and policy backdrop (Chart 1). The BCA House View consists of accommodative policy, economic recovery, a weakening dollar, and the outperformance of cyclical risk assets. We largely agree, with the caveat that there will be “No Return To Normalcy” in the geopolitical realm. Meaning that over the medium and long term the US dollar will remain firmer than expected and cyclical economies and sectors will face headwinds. Chart 1Equity Market Hits Wall Of Worry

Equity Market Hits Wall Of Worry

Equity Market Hits Wall Of Worry

The pandemic will have unforeseen consequences, such as social unrest and regime failures, while China’s secular slowdown and the Great Power competition between the US and its rivals will intensify. Not only is China slowing but also President Joe Biden has been confirmed as a China hawk, coopting President Trump’s aggressive stance and courting US allies to pile the pressure on Beijing. For most of this year the “normalcy” narrative has prevailed. Now investors are becoming fearful of the “abnormalcy” narrative. The US dollar has surprised its doubters on the basis of relative growth and interest rate differentials (Chart 2). Chart 2Dollar Remains Firm, Reflation Indicator Abates

Dollar Remains Firm, Reflation Indicator Abates

Dollar Remains Firm, Reflation Indicator Abates

Over the next six months, the key point is that until these geopolitical risks boil over and explode, they reinforce the bullish macro view, since government spending will surge to address national challenges. The rich democracies have awoken to the threat posed by malaise at home and autocracy abroad. They have reactivated fiscal policy to rebuild their states and expand the social safety net. They are increasing investments in infrastructure, renewables, and defense. This trend is especially positive for US allied economies, global manufacturers ex-China, commodity prices, and commodity producing emerging markets, at least until the next shock erupts. We discuss the risk of a cyber shock as well as the points above in this report. Policy Responses To The Delta Variant The Delta variant began in India and has now swept the world. So far the variants respond to COVID vaccines, which are being rolled out globally. National and local political leaders will promote vaccination campaigns first – only if hospital systems are clogged will they resort to social restrictions. New infections have risen much faster than hospitalizations and deaths, although the latter are lagging indicators and will eventually follow cases (Chart 3). But financial markets will largely look past the scare, as they looked past the various waves of the original virus over the past 15 months. Today investors have greater evidence of humanity’s ability to curb the virus and can expect government spending to tide over the economy if new restrictions are necessary. New social restrictions should not be ruled out. They are not politically impossible. Public opinion in the developed countries shows that about 77% of people believe restrictions were about right or should have been tighter, while only 23% believe there should have been fewer restrictions (Chart 4). About 40% of Germans oppose the lifting of restrictions even for the vaccinated! Chart 3Delta Variant: A Limited Risk Unless Hospitals Clog

Delta Variant: A Limited Risk Unless Hospitals Clog

Delta Variant: A Limited Risk Unless Hospitals Clog

Chart 4ANew Lockdowns Not Impossible

Stay The Course (But Gird For Cyber War)

Stay The Course (But Gird For Cyber War)

Chart 4BNew Lockdowns Not Impossible

Stay The Course (But Gird For Cyber War)

Stay The Course (But Gird For Cyber War)

Any financial or economic distress from virus variants will reinforce ultra-accommodative monetary policy. The European Central Bank adopted a symmetric inflation target of 2% as it completed its strategic review, up from a previous goal which simply aimed at inflation just under 2%. It is likely to expand rather than taper asset purchases (Chart 5). At the Fed, the balance of power between hawks and doves on the Federal Open Market Committee reflects the political and geopolitical trends of the day. In the wake of the Great Recession, the doves overwhelmed the hawks (Chart 6). The institution has fully transitioned today – it now aims to generate an inflation overshoot – and it will not jeopardize its new average inflation targeting regime by tightening policy too soon this year or next. Chart 5Central Banks Will Delay Normalization If COVID Crisis Persists

Central Banks Will Delay Normalization If COVID Crisis Persists

Central Banks Will Delay Normalization If COVID Crisis Persists

Chart 6Doves Firmly In Ascendancy At Federal Reserve

Stay The Course (But Gird For Cyber War)

Stay The Course (But Gird For Cyber War)

The Delta variant makes it more likely that governments will increase fiscal support. The European Union’s Recovery Fund has a modest impact but the EU Commission is not patrolling budget deficits anymore, in the event that new social restrictions set back the recovery. The Democratic Party will pass President Biden’s $3.5-$4.1 trillion American Jobs and Families Plan through Congress by Christmas (with a net deficit increase of $1.3-$2.5 trillion over eight years). Support rates among independents and Democrats suggest Biden will come up with the votes (Chart 7). A renewed sense of crisis will compel any straggling senators. Chart 7ADelta Variant Makes Biden Stimulus Even More Likely To Pass

Stay The Course (But Gird For Cyber War)

Stay The Course (But Gird For Cyber War)

Chart 7BDelta Variant Makes Biden Stimulus Even More Likely To Pass

Stay The Course (But Gird For Cyber War)

Stay The Course (But Gird For Cyber War)

Markets will cheer more government spending as they have done throughout the vast surge in budget deficits across the world, not least in the developed markets, where austerity stunted the recovery in the wake of the Great Recession (Chart 8). Beyond Delta jitters and reactive stimulus, there are clouds forming on the horizon over the medium and long term. Budget deficits will start contracting, central banks will start hiking rates, and taxes will go up (and not only in the US). Geopolitical risks that are suppressed today will erupt later. Bottom Line: The very near term could easily see more volatility but by the end of the year the reflationary cast of global economic policy will have won the day. The bigger problems come clearly into review after the ink dries on the last installment of the great Biden budget blowout. Chart 8Market Will Cheer Another Round Of Government Spending

Market Will Cheer Another Round Of Government Spending

Market Will Cheer Another Round Of Government Spending

China Policy And Cyber War What might the next major negative shock be? A leading candidate is China, with its confluence of internal and external risks. China’s policymakers opened the floodgates of credit-and-fiscal stimulus to combat the global pandemic in 2020. They quickly shifted to tightening policy to prevent destabilizing asset bubbles. Now they are easing again. Stimulus and growth have both peaked. Authorities are on the verge of overtightening policy but tactical shifts in economic policy often occur in July. Right on cue the State Council ordered across-the-board cuts to bank reserve requirements on July 9. The Politburo’s July meeting on economic policy will bring an even more important policy signal. The concrete impact of the RRR cut should not be overstated. China has been lowering RRRs since late 2011 as its broad money growth has continually declined. The trend is indicative of China’s secular slowdown. A new series of RRR cuts is often attended by a global equity selloff (Chart 9). Chart 9China Blinked - But One RRR Cut Will Not Prevent A Global Selloff

China Blinked - But One RRR Cut Will Not Prevent A Global Selloff

China Blinked - But One RRR Cut Will Not Prevent A Global Selloff

Our China Investment Strategy highlights that policy remains restrictive in other areas. Local governments have been told not to borrow if they have hidden debts. Moreover the crackdown on China’s tech sector also continues apace. These regulatory crackdowns are characteristic of the Xi Jinping administration and can continue for a while as it further consolidates power in advance of the twentieth National Party Congress in fall 2022. The US-China conflict is getting worse. The Biden administration took several punitive actions over the past month. It warned businesses against investing in Hong Kong and Xinjiang. It rejected a restart of the strategic and economic dialogue. While a bilateral summit between Biden and Xi Jinping is possible on October 30-31, it is not yet scheduled and would only temporarily improve relations. One of Biden’s more significant recent moves was to orchestrate a joint statement with allies condemning China for aggressive behavior in cyber space.1 A massive cyber attack should be high up on any investor’s list of “gray rhino” events (high-probability, high-impact events). The world has suffered large shocks from global terrorism, financial crisis, and pandemic. Lightning rarely strikes the same place twice. Of course, nobody knows what will cause the next upset. But a devastating cyber event has been underrated in the investment community and that is changing (Table 1). Fed Chair Powell, asked by a reporter what was the chief risk to the global financial system, said “cyber risk.” To quote in full: So you would worry about a cyber event. That's something that many, many government agencies, including the Fed and all large private businesses and all large private financial companies in particular, monitor very carefully, invest heavily in. And that's really where the risk I would say is now, rather than something that looked like the global financial crisis.2 Table 1Cyber Event Underrated In Consensus View Of Global Risks

Stay The Course (But Gird For Cyber War)

Stay The Course (But Gird For Cyber War)

Here are six structural reasons that cyber risk will continue to escalate: Cyber space is one of the truly ungoverned spaces. The US is the preponderant power in cyber space, as elsewhere, but there is no regular order or code of conduct. The US cyber bureaucracy is decentralized and uncoordinated while its opponents are centrally commanded, aggressive, and sophisticated. Great power competition is escalating. The US is struggling with China, Russia, and Iran and all sides seek to intimidate enemies and gain allies. Cyber capabilities enhance essential tasks like spying, sabotage, and information warfare. The tech race is intensifying, with companies and governments investing heavily in innovation and industry, while US export controls exacerbate China’s frantic efforts to obtain advanced tech by any means. The pandemic boosted digital dependency across industry and commerce, creating a “perfect storm” for cyber attacks and hacking.3 The US and its allies are threatening to retaliate more actively against cyber attacks, which may initially lead to an increase in the total number of attacks. In addition, Israel will need to sabotage Iran’s nuclear program if it is not halted by diplomacy. The US is polarized and war-weary yet claiming greater commitment to its allies, a paradox that encourages foreign rivals to use cyber tools to foment US divisions; strike at regional opponents that lack US security guarantees; and test the US commitment to its allies. The current US-Russia negotiations toward a truce against cyber attacks on critical infrastructure are the sole example of a potential structural improvement. The US and Russia could conceivably lay down some rules of the road in cyber space. There may be a basis for an agreement in that already this year the US refrained from blocking the Nordstream II pipeline with Germany while Russia refrained from re-invading Ukraine. However, a Russo-American truce would not dispel the risk of a global cyber surprise. It could even increase the odds. Russia this year alone showed with the Colonial Pipeline hack and the JBS meat-packing hack that its proxies can disrupt critical US infrastructure. It would make sense to agree to a truce so that the US does not demonstrate the same capability against Russia. Even without a truce, Russia does not benefit from provoking massive US cyber attacks. The US is the world’s leading cyber power and has pledged that it will retaliate. Rather Russia will concentrate its efforts closer to home: suppressing dissent, intimidating the former Soviet Union, and testing the US’s willingness to defend its allies. It would be useful for Russia to use cyber attacks to undermine NATO unity and demonstrate that the US is reluctant to defend NATO members’ critical infrastructure. Remember the cyber strike against Estonia in 2007. Hence huge shocks could still emerge in Europe or elsewhere even if the US and Russia make a ceasefire regarding their own critical infrastructure. The same can be said for China, Iran, and North Korea. Attacks in their neighborhood are even more likely than direct provocations against the United States now that the US is threatening graver consequences. Beijing is concentrating its cyber power on technological acquisition. But it will also try to intimidate its neighbors into neutrality and test America’s commitment to its allies. This applies to markets like Taiwan, South Korea, the Philippines, and Vietnam. Not all cyber attacks would cause a global shock but the danger of Biden’s emphasis on alliances and multilateralism is that the US will be tested and its commitments will expand. Local cyber attacks could escalate if the US believes it must prove its resolve. Bottom Line: Cyber firms’ share prices have risen since we made our contrarian buy call back in March. True, fundamentals are poor despite the strong geopolitical tailwind. The BCA Equity Analyzer shows that valuations, debt, liquidity, and return on equity have deteriorated relative to the global large cap equity universe (Chart 10). Still, as long as liquidity is ample and geopolitical risk is high we expect cyber firms’ share prices to keep grinding upward. Chart 10Cyber Stocks: Poor Fundamentals But Geopolitics A Secular Driver

Stay The Course (But Gird For Cyber War)

Stay The Course (But Gird For Cyber War)

Investment Takeaways We are sticking with our key themes and views: long gold; long value over growth; long DM-ex-US stocks such as FTSE100 (Chart 11) and European industrials; long US neighbors Mexico and Canada; long defense and cyber stocks; and short the assets of emerging market “strongman” regimes from China and Russia to Brazil, Turkey, and the Philippines. Taking several of our trade recommendations alongside the copper-to-gold ratio, a key measure of global reflation, there could be more near-term downside (Chart 12). Nevertheless these are strategic trades designed to bear rewards over 12 months and beyond. Mainland Chinese investors should book gains on long Chinese 10-year government bonds. We would not rule out a bigger bond rally later given China’s risks at home and abroad, but RRR cuts often lead to a selloff and the signal is that the socialist policy “put” remains in place. Book gains on long Italian / short Spanish equities. This tactical trade is now hitting the top of its range and will likely mean revert. We are still optimistic on European stocks and the euro as a whole and view the German election as a positive catalyst almost regardless of outcome. Chart 11Stay The Course: Long Value Over Growth

Stay The Course: Long Value Over Growth

Stay The Course: Long Value Over Growth

Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Chart 12Stick To Cyclical Trades Over Near-Term Volatility

Stick To Cyclical Trades Over Near-Term Volatility

Stick To Cyclical Trades Over Near-Term Volatility

Footnotes 1 White House, “The United States, Joined by Allies and Partners, Attributes Malicious Cyber Activity and Irresponsible State Behavior to the People’s Republic of China,” July 19, 2021, whitehouse.gov. 2 “Jerome Powell: Full 2021 60 Minutes Interview Transcript,” CBS News, April 11, 2021, cbsnews.com. 3 Connor Fairman, “2020: Cybercrime’s Perfect Storm,” Council on Foreign Relations, January 20, 2021, cfr.org.

Weekly Performance Update For the week ending Thu Jul 22, 2021 The Market Monitor displays the trailing 1-quarter performance of strategies based around the BCA Score. For each region, we construct an equal-weighted, monthly rebalanced portfolio consisting of the top 3 stocks per sector and compare it with the regional benchmark. For each portfolio, we show the weekly performance of individual holdings in the Top Contributors/Detractors table. In addition, the Top Prospects table shows the holdings that currently have the highest BCA Score within the portfolio. For more details, click the region headers below to be redirected to the full historical backtest for the strategy. BCA US Portfolio

Market Monitor (Jul 22, 2021)

Market Monitor (Jul 22, 2021)

Total Weekly Return BCA US Portfolio S&P500 TRI 0.37% 0.18% Top Contributors AN:US IPG:US JLL:US DELL:US ESGR:US Weekly Return 42 bps 19 bps 12 bps 7 bps 6 bps Top Detractors SIG:US LPX:US FLO:US MTZ:US PEG:US Weekly Return -13 bps -9 bps -8 bps -6 bps -5 bps Top Prospects TX:US MPLX:US BRK.A:US ESGR:US ANAT:US BCA Score 97.25% 95.16% 95.13% 93.88% 91.26% BCA Canada Portfolio

Market Monitor (Jul 22, 2021)

Market Monitor (Jul 22, 2021)

Total Weekly Return BCA Canada Portfolio S&P/TSX TRI -0.95% -0.42% Top Contributors ONEX:CA RCH:CA QBR.A:CA SMU.UN:CA TCL.A:CA Weekly Return 13 bps 12 bps 6 bps 6 bps 3 bps Top Detractors IFP:CA CS:CA CFP:CA CRON:CA CNQ:CA Weekly Return -25 bps -21 bps -15 bps -13 bps -10 bps Top Prospects LNF:CA CS:CA IFP:CA CFP:CA ELF:CA BCA Score 98.98% 98.62% 98.50% 96.76% 93.76% BCA UK Portfolio

Market Monitor (Jul 22, 2021)

Market Monitor (Jul 22, 2021)

Total Weekly Return BCA UK Portfolio FTSE 100 TRI 0.73% -0.61% Top Contributors FDEV:GB FDM:GB HFD:GB SVST:GB GLTR:GB Weekly Return 42 bps 26 bps 12 bps 12 bps 10 bps Top Detractors SPI:GB RMG:GB TUNE:GB CMCX:GB MNOD:GB Weekly Return -18 bps -11 bps -10 bps -9 bps -8 bps Top Prospects SVST:GB ROSN:GB GROW:GB NLMK:GB RMG:GB BCA Score 99.11% 96.58% 95.14% 93.80% 93.56% BCA Eurozone Portfolio

Market Monitor (Jul 22, 2021)

Market Monitor (Jul 22, 2021)

Total Weekly Return BCA EMU Portfolio MSCI EMU TRI 0.22% 0.25% Top Contributors CNV:FR MONT:BE REY:IT PHA:FR ROVI:ES Weekly Return 20 bps 16 bps 10 bps 9 bps 8 bps Top Detractors ATS:AT RWAY:IT LOUP:FR PMAG:AT SON:PT Weekly Return -12 bps -11 bps -9 bps -7 bps -7 bps Top Prospects STR:AT TESB:BE SOLV:BE BB:FR FDJ:FR BCA Score 99.74% 97.33% 96.76% 96.66% 96.57% BCA Japan Portfolio

Market Monitor (Jul 22, 2021)

Market Monitor (Jul 22, 2021)

Total Weekly Return BCA Japan Portfolio TOPIX TRI -0.77% -1.81% Top Contributors 7593:JP 8117:JP 6960:JP 6413:JP 3459:JP Weekly Return 8 bps 7 bps 6 bps 4 bps 4 bps Top Detractors 5021:JP 5020:JP 3291:JP 7994:JP 6641:JP Weekly Return -19 bps -14 bps -13 bps -12 bps -12 bps Top Prospects 4966:JP 6960:JP 9436:JP 6641:JP 8117:JP BCA Score 99.72% 99.39% 99.01% 98.49% 98.41% BCA Hong Kong Portfolio

Image

Total Weekly Return BCA Hong Kong Portfolio Hang Seng TRI -0.77% -0.97% Top Contributors 215:HK 2380:HK 316:HK 990:HK 323:HK Weekly Return 30 bps 26 bps 14 bps 12 bps 11 bps Top Detractors 220:HK 3600:HK 468:HK 856:HK 2232:HK Weekly Return -29 bps -25 bps -24 bps -22 bps -19 bps Top Prospects 1277:HK 2232:HK 857:HK 1606:HK 990:HK BCA Score 99.81% 99.47% 99.25% 98.76% 98.51% BCA Australia Portfolio

Market Monitor (Jul 22, 2021)

Market Monitor (Jul 22, 2021)

Total Weekly Return BCA Australia Portfolio S&P/ASX All Ord. TRI 0.10% 0.56% Top Contributors NEC:AU RUL:AU JLG:AU SGF:AU GRR:AU Weekly Return 22 bps 17 bps 16 bps 15 bps 12 bps Top Detractors AGI:AU FLN:AU BLX:AU DDR:AU PSQ:AU Weekly Return -47 bps -12 bps -8 bps -8 bps -8 bps Top Prospects GRR:AU BFG:AU PIC:AU BLX:AU SOL:AU BCA Score 99.09% 98.31% 97.86% 97.46% 97.33%

BCA Research’s Counterpoint service observes that over the past three years the US dollar has almost perfectly tracked the performance of bonds versus equities, proving that the main driver for dollar demand is (defensive) portfolio flows. This is because,…

Feature June’s economic data and second-quarter GDP indicate that China’s economic recovery may have peaked. Slight improvements in some sectors, including manufacturing investment, exports and consumption, were offset by slowing in China’s old economy, such as infrastructure and real estate. A softening economy will weigh on Chinese corporate profits in 2H21. Inflation in Producer Price Index (PPI) has likely peaked, but it remains far above its historic average. Downstream industries may benefit from low interest rates and slightly less inflationary pressures on input prices, however, their profit growth has rolled over given weakening domestic demand and base effect. Industrial profits will shift downward in 2H21, meanwhile China’s macro policy will probably disappoint investors. Last week’s GDP’s numbers show that small-to-medium enterprises (SMEs) and private-sector businesses bore the brunt of rising global commodity prices and a slow recovery in domestic household consumption and services. The data, coupled with recent policy moves, support our view that China’s leadership is focused on helping vulnerable segments of the economy rather than boosting domestic demand by broadly easing policies (Chart 1). Nonetheless, the authorities may resort to easing policy later in 2021 if export growth weakens significantly in the second half of the year. A series of Reserve Requirement Ratio (RRR) and/or interest rate cuts, increased infrastructure project approvals, and/or looser real estate regulations, will signal that China’s ongoing policy tightening cycle has ended. In recent weeks both Chinese onshore and offshore stocks slipped further in absolute terms and relative to global benchmarks (Chart 2). We continue to recommend that investors remain cautious on Chinese stocks, at least through Q3. Chart 1No Broad Easing Yet

No Broad Easing Yet

No Broad Easing Yet

Chart 2Investors Still Cautious On China's Economy And Policy

Investors Still Cautious On China's Economy And Policy

Investors Still Cautious On China's Economy And Policy

Qingyun Xu, CFA Associate Editor qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com Q2 GDP: Recovering At A Slower Pace China’s official GDP growth, on a year-over-year basis, slowed to 7.9% in Q2 from 18.3% in Q1 (Chart 3, top panel). While Q2’s weaker reading reflects the base effect in the data, it was slightly below the market’s expectation of 8.0-8.5%. Moreover, on a sequential basis (quarter-over-quarter), Q2’s seasonally adjusted GDP growth was one of the slowest in the past decade (Chart 3, bottom panel). These figures and the underlying data highlight that China’s economic growth momentum, which historically lags the credit impulse by six to nine months, has peaked (Chart 4). However, in 1H21, China aggregate output still grew by a 5.5% average annual rate during the same period over the past two years, well within Chinese policymakers’ target of above 5% growth needed to maintain a stable economy. Meanwhile, the bifurcation in China’s economic recovery continues. While robust external demand for Chinese goods helped to underpin manufacturing output, the sector’s profit growth has lagged upstream industries. Moreover, state-owned enterprises (SOEs) are experiencing soaring profit growth whereas SMEs have struggled with rising global commodity prices and sluggish domestic consumption as discussed below. We expect that the pace in credit growth deceleration will moderate in 2H21 and interest rates will stay at historically low levels. However, the authorities are unlikely to loosen macro policies until more signs of economic weaknesses emerge. Chart 3Q2 GDP: Slowing From An Elevated Level

Q2 GDP: Slowing From An Elevated Level

Q2 GDP: Slowing From An Elevated Level

Chart 4Chinese Economic Growth Should Soften Further In 2H21

Chinese Economic Growth Should Soften Further In 2H21

Chinese Economic Growth Should Soften Further In 2H21

Robust Exports, Sluggish Manufacturing Investment Chart 5Subdued Manufacturing Investment Recovery Despite Robust Exports

Subdued Manufacturing Investment Recovery Despite Robust Exports

Subdued Manufacturing Investment Recovery Despite Robust Exports

China’s export growth in June beat market expectations, despite shipping disruptions at major ports in Guangdong province due to a resurgence in COVID-19 cases. However, the recovery in manufacturing investment was muted through most of 1H21 even though export growth was resilient (Chart 5). There are several reasons for the sluggish recovery: the RMB’s rapid appreciation in the first five months of 2021, rising inflation and the limited pricing power that Chinese exporters gained in the first half of the year likely impeded their profits and curbed their propensity to invest (Chart 6). Total export values in USD significantly outpaced those in RMB terms, suggesting that the profit gains by Chinese exporters were offset by the strengthening local currency (Chart 7). Chart 6Rapid RMB Appreciation Will Weigh On Industrial Profits

Rapid RMB Appreciation Will Weigh On Industrial Profits

Rapid RMB Appreciation Will Weigh On Industrial Profits

Chart 7Divergence Between Exports In USD versus RMB

Divergence Between Exports In USD versus RMB

Divergence Between Exports In USD versus RMB

Furthermore, manufacturers in mid-to-downstream industries have been unable to fully pass on rising input costs to domestic consumers, which is evidenced in the faster growth of manufacturing output volume compared with price increases. It contrasts with the previous inflationary cycles, where surging prices for manufactured goods surpassed output volume (Chart 8A & 8B). Chart 8AChina's Manufacturing Recovery: Stronger Volume Than Prices

China's Manufacturing Recovery: Stronger Volume Than Prices

China's Manufacturing Recovery: Stronger Volume Than Prices

Chart 8BMuted Profit Margin Recovery In Manufacturing Compared With Mining

Muted Profit Margin Recovery In Manufacturing Compared With Mining

Muted Profit Margin Recovery In Manufacturing Compared With Mining

June’s improvement in manufacturing investment may not advance into 2H21 without added policy support. The nearly 2% depreciation in the RMB against the dollar in recent weeks will alleviate some pressure on exporters’ profit margins. However, export prices in USD also started to weaken (Chart 9). In addition, June’s manufacturing PMI and a Chinese business school survey,1 reported a deterioration in business conditions among smaller businesses. The weaker sentiment will depress manufacturing investments since China’s manufacturing sector is dominated by private and smaller businesses (Chart 10). Chart 9Chinese Export Prices In USD Are Rolling Over

Chinese Export Prices In USD Are Rolling Over

Chinese Export Prices In USD Are Rolling Over

Chart 10Deteriorating Business Sentiment Will Depress Manufacturing Investments

Deteriorating Business Sentiment Will Depress Manufacturing Investments

Deteriorating Business Sentiment Will Depress Manufacturing Investments

Recent policy measures to keep a low interest-rate environment will help the export and manufacturing sectors by reducing operating costs. The measures are also in keeping with China’s shift from boosting its service sector to maintaining a steady share of manufacturing output in its domestic economy (Chart 11). Chart 11Maintaining A Steady Share Of Manufacturing Output In China's Economy

Maintaining A Steady Share Of Manufacturing Output In China's Economy

Maintaining A Steady Share Of Manufacturing Output In China's Economy

Policy Tightening In The Old Economy Continues Chart 12Investments In Real Estate Have Lost Steam

Investments In Real Estate Have Lost Steam

Investments In Real Estate Have Lost Steam

Infrastructure investment growth slowed further in June. Investments in real estate, which drove China’s economic recovery in the second half of 2020, are also losing momentum (Chart 12). The slowdown, engineered by policymakers, will likely endure for the rest of the year. Bank loans to real estate developers tumbled to a cyclical low (Chart 13). In addition, deposit and advance payments, the main source of funds for real estate projects, nose-dived along with home sales (Chart 14). Chart 13No Signs Of Looser Financing Regulations In Property Sector

No Signs Of Looser Financing Regulations In Property Sector

No Signs Of Looser Financing Regulations In Property Sector

Chart 14Falling Home Sales Will Further Depress Real Estate Investments

Falling Home Sales Will Further Depress Real Estate Investments

Falling Home Sales Will Further Depress Real Estate Investments

Chart 15Sharp Pullback In New Infrastructure Project Approvals This Year

Sharp Pullback In New Infrastructure Project Approvals This Year

Sharp Pullback In New Infrastructure Project Approvals This Year

Infrastructure project approvals by the Ministry of Finance remain on a downward trend (Chart 15). Last week, China’s Banking and Insurance Regulatory Commission (CBIRC) announced a new rule to stop financial institutions from lending to local government financing vehicles (LGFV) that hold off-balance sheet government debt. LGFVs are largely used by provincial governments to borrow from banks to help fund infrastructure projects. Regulations targeting the real estate sector will further dampen real estate investments in the second half of this year. Land purchases and housing starts, both leading indicators for real estate investment, have declined since February. Excavator sales and investment in construction equipment also deteriorated sharply (Chart 16). Given that housing prices remain elevated, we do not expect real estate regulations to shift to an easier tone. The deceleration in China’s old economy is reflected in imports. While the value of imports remains strong, the volume has slowed, which suggests that the surge was due to soaring commodity prices (Chart 17, top panel). In particular, the growth in China’s imports of copper and steel, on a year-over-year basis and in volume terms, contracted in June (Chart 17, bottom panel). Chart 16Construction Activities Set To Slow Further

Construction Activities Set To Slow Further

Construction Activities Set To Slow Further

Chart 17Falling Import Volume

Falling Import Volume

Falling Import Volume

The Key To A Consumption Recovery Retail sales picked up slightly in June following two consecutive months of decline. However, retail sales remain below their pre-pandemic level (Chart 18). Labor market dynamics and household income growth, which stayed sluggish through 1H21, hold the key to the speed and magnitude of a recovery in consumption this year (Chart 19). Chart 18Sluggish Recovery In Household Consumption

Sluggish Recovery In Household Consumption

Sluggish Recovery In Household Consumption

Chart 19A Lackluster Consumption Recovery Due To Slow Recovery in Household Income

A Lackluster Consumption Recovery Due To Slow Recovery in Household Income

A Lackluster Consumption Recovery Due To Slow Recovery in Household Income

Household precautionary savings, which remain elevated compared with their historical norms, have depressed the propensity to spend (Chart 20). While the overall unemployment rate in China’s urban centers has steadily declined this year, the rate of jobless young graduates (ages 16-24) picked up and is nearly three percentage points higher than its historical mean (Chart 21). However, the high unemployment among graduates will not encourage policymakers to stimulate the economy. The number of new graduates in both 2020 and 2021 is larger than the historical average, while the growth in new job creation has nearly recovered to that of the pre-pandemic years (Chart 22). Chart 20Households' Propensity For Precautionary Savings Remains Elevated

Households' Propensity For Precautionary Savings Remains Elevated

Households' Propensity For Precautionary Savings Remains Elevated

Chart 21Rising Unemployment Rate Among Younger Workers

Rising Unemployment Rate Among Younger Workers

Rising Unemployment Rate Among Younger Workers

Moreover, labor market slack among young graduates seems to be concentrated in the services sector, and this sector’s improvement is dependent on China’s domestic pandemic situation and inoculation rates rather than on stimulus (Chart 23). Chart 22Urban Job Creation Growth Still On The Mend

Urban Job Creation Growth Still On The Mend

Urban Job Creation Growth Still On The Mend

Chart 23Interruptions In Service Sector Recovery Due To Lingering COVID Cases

Interruptions In Service Sector Recovery Due To Lingering COVID Cases

Interruptions In Service Sector Recovery Due To Lingering COVID Cases

Elevated Inflation, Downshifting Industrial Profits Chart 24China's PPI May Have Reached A Cyclical Peak...

China's PPI May Have Reached A Cyclical Peak...

China's PPI May Have Reached A Cyclical Peak...

China’s domestic inflationary pressures eased slightly in June with a small decline in both consumer and producer prices. The input price component of the manufacturing PMI, which normally leads the PPI by about three months, dropped sharply last month, which indicates that the PPI may have reached its cyclical peak (Chart 24). However, producer price inflation will likely remain elevated in the second half of the year. Although global industrial metal prices have rolled over since May, they remain at their highest level since 2011 (Chart 25). A rapid deceleration in Chinese credit growth and weakening demand in 2H21 will remove some pressure in the sizzling hot commodity market, but global supply-side constraints will limit the downside in raw material prices, at least through the next six months. Therefore, diminishing inflationary pressures on the PPI will only slightly reduce input costs for China’s mid-to- downstream manufacturers, which have been unable to pass on rising commodity prices to domestic consumers (Chart 26). As discussed earlier, Chinese export prices in both USD and RMB terms have also rolled over. Chart 25...But Global Commodity Prices Are Still Elevated

...But Global Commodity Prices Are Still Elevated

...But Global Commodity Prices Are Still Elevated

Chart 26Absence Of Inflation Pass-Through

Absence Of Inflation Pass-Through

Absence Of Inflation Pass-Through

Given that price changes are more important to corporate profits than volume changes, Chinese mid-to-downstream industries will continue to face downward pressure on their profit margins. Profit growth in mid-to-downstream industries consistently lagged their upstream counterparts in the past 12 months (Chart 27). Moreover, state-holding enterprises, which dominate upstream industries, have seen a 150% jump in profit growth from a year ago, while the rate of profit gains among privately owned industrial companies tumbled this year (Chart 28). Chart 27A Faster Mean Reversal In Profit Growth Among Private Companies

Taking The Pulse Of China’s Slowing Economy

Taking The Pulse Of China’s Slowing Economy

Chart 28A Faster Mean Reversal In Profit Growth Among Private Companies

A Faster Mean Reversal In Profit Growth Among Private Companies

A Faster Mean Reversal In Profit Growth Among Private Companies

Chinese policymakers will probably focus on addressing imbalances in China’s industrial sector and economy by supporting SMEs and the private sector. Meanwhile, industrial profit growth will decline in 2H21 from its V-shaped recovery last year, given weakening domestic demand and the waning base effect. Table 1China Macro Data Summary

Taking The Pulse Of China’s Slowing Economy

Taking The Pulse Of China’s Slowing Economy

Table 2China Financial Market Performance Summary

Taking The Pulse Of China’s Slowing Economy

Taking The Pulse Of China’s Slowing Economy

Footnotes 1The CKGSB (Cheung Kong Graduate School Of Business) Business Conditions Index (BCI) comprises four sub-indices: corporate sales, corporate profits, corporate financing environment and inventory levels. Equity Sector Recommendations Cyclical Investment Stance

Highlights Metals prices are likely to suffer in the short term on the back of weakening Chinese demand and fading inflationary pressures. Accordingly, in our most recent Global Asset Allocation (GAA) Quarterly Outlook, we downgraded the AUD to underweight against the greenback. Bond yields, globally, are bound to rise moderately over the course of the coming 12 months. Australian yields, however, are likely to rise slower than those in the US. The RBA has been explicit in communicating what it would take to adjust its policy stance and is likely to lag behind other central banks in DM. We therefore recommend investors favor Australian government bonds in a global bond portfolio. Australian equities, now dominated by Financials rather than the Materials sector, would benefit from a rise in bond yields. However, a weaker AUD and declining metal prices warrant no more than a benchmark exposure to Australian equities within a global equity portfolio. Introduction Recently, clients have often been asking about Australia. The reasons seem clear. With a potential commodities “super-cycle” driven by a shift to renewable energy and electric vehicles (EVs), both the Australian economy and equities should be in a position to benefit. The reality, however, has been much less positive. Particularly the divergence between the core driver of the Australian market, industrial metals, and the performance of both equities and the currency over the past few years has been a concern (Chart 1). Over the past year and a half, Australian equities have underperformed the MSCI ACWI by 12.4% (Chart 2, panel 1). This underperformance was mainly due to the outperformance of the US. However, even against global markets excluding the US, Australian equities did not match the rise in commodity prices – particularly industrial metals (Chart 2, panel 2). Chart 1Despite The Rise In Metals Prices...

Despite The Rise In Metals Prices...

Despite The Rise In Metals Prices...

Chart 2...Australian Equities Have Not Outperformed

...Australian Equities Have Not Outperformed

...Australian Equities Have Not Outperformed

Chart 3Financials Dominate Australian Equities

Financials Dominate Australian Equities

Financials Dominate Australian Equities

The structure of the Australian market has changed over the past few years. The commodities boom and subsequent global liquidity boom over the past two decades have fueled a housing bubble in Australia and an unsustainable rise in household debt. As a result, Australian equities are no longer dominated by metals and mining stocks, but rather by banks (Chart 3). We structured this Special Report in a Q&A format, answering questions we think are most relevant for investors to assess both the short- and long-term outlook for Australia. We aim to provide an overview of the economy and draw some conclusions on how investors should be positioned. Our conclusions are as follows: Over the past year and a half, the Australian economy has shown how complementary actions between fiscal and monetary policy, as well as social restriction measures, can mitigate both economic and human damage. The Reserve Bank of Australia (RBA) will be in no rush to adjust its policy stance until wage growth is back to its 3% target. However, RBA officials risk running the economy hot in the meantime given that measures of employment are back to their pre-pandemic levels. The RBA is not likely to change its policy stance before reaching its wage growth and inflation targets and will probably lag behind other global central banks in tightening. In that case, investors should favor Australian government bonds in a global bond portfolio. Australian banks remain well-funded and in good health. But their excessive exposure to the housing sector puts them at grave risk if home prices collapse. Despite this, there seems to be a feedback loop where a decline in mortgage rates fuels further demand for loans, pushing up home prices. A slowdown in Chinese credit growth and economic activity will hamper commodity demand, weighing down on Australian equities. The longer-term outlook remains compelling for Australian equities and metals as we enter into a new commodities “supercycle” fueled by a transition to renewable and alternative energy. The Australian economy stands to benefit given that the country has high levels of both production and reserves of the minerals needed for this transition. Q: How Does The Economy Look In The Short-Term? A: Australia can be regarded as one of the few countries that successfully navigated the pandemic with a minimal amount of damage, both to its population and economy. With swift measures to limit travel and implement social restrictions, the spread of the outbreak was curtailed to slightly over 30,000 total cases, representing only 0.12% of its population (Chart 4). On the other hand, its vaccination campaign has been much slower (at 38 doses administered per 100 people) than in other DM economies such as the US, UK, France, or Germany with 100, 120, 90, and 102 doses per 100 people, respectively. In the short term, this might not seem particularly damaging to the economy. However, if vaccination rates do not pick up rapidly, Australia’s international travel restrictions (which cannot sustainably be kept in place) will hamper economic growth and become a major drag on the tourism and education sectors (Chart 5, panels 1 & 2). Chart 4Government Policies Contained The Pandemic Outbreak...

Government Policies Contained The Pandemic Outbreak...

Government Policies Contained The Pandemic Outbreak...

Chart 5...At The Expense Of Tourism

...At The Expense Of Tourism

...At The Expense Of Tourism

Ample fiscal support – in the form of wage subsidies and business support through the JobKeeper program – mitigated the shortfall in household incomes (Chart 6). This provided a boost to both consumers and businesses with Q1 GDP growth coming in at 1.8% quarter-on-quarter (7.4% annualized). GDP expectations for the remainder of this year and next show a resilient strong momentum for Australian growth and domestic demand (Chart 7). Chart 6Fiscal Stimulus Supported Employment...

A Deeper Dive Into The Land Down Under

A Deeper Dive Into The Land Down Under

Chart 7...And Overall Growth

...And Overall Growth

...And Overall Growth

Chart 8Labor Market Back To Pre-Pandemic Levels...

Labor Market Back To Pre-Pandemic Levels...

Labor Market Back To Pre-Pandemic Levels...

The labor market recovery has been an excellent example of how fiscal support and lockdown measures complement each other. Most employment indicators have almost recovered or surpassed their pre-pandemic levels: The unemployment rate stands at 4.90%, compared to 5.13%, the underemployment rate is at 7.44%, compared to 8.60%. The total number of those employed is now above its pre-pandemic level, albeit still below the 2018-2019 growth trend (Chart 8). Q: When Will The RBA Shift Its Policy Stance? A: The RBA has been explicit in communicating that changes in its policy stance hinge on Australian wage growth rising sustainably towards 3% – a level last reached in Q1 2013. Even with economic activity mostly restored, wage growth remains low at 1.49% (Chart 9). Our belief is that until that occurs, the RBA will probably maintain its accommodative stance. Our global fixed-income strategists, in a recent report, highlighted their belief that the RBA is likely to be less hawkish than markets currently expect – on both tapering and hiking rates. We agree with that assessment. Comments by RBA Governor Lowe earlier last month back our dovish belief: He stated that “The Board is committed to maintaining highly supportive monetary conditions to support a return to full employment in Australia and inflation consistent with the target…This is unlikely to be until 2024 at the earliest”. Market expectations nevertheless remain much more hawkish – pointing to a first rate hike by mid 2022 and almost 70 basis points of hikes by 2024 (Chart 10). Chart 9...However Wage Growth Remains Muted

...However Wage Growth Remains Muted

...However Wage Growth Remains Muted

Chart 10Market Expects A Hawkish RBA...

Market Expects A Hawkish RBA

Market Expects A Hawkish RBA

Chart 11...And Is Already Pricing That Down The Curve

...And Is Already Pricing That Down The Curve

...And Is Already Pricing That Down The Curve

Chart 12Inflation Remains Well-Below The RBA's Target

Inflation Remains Well-Below The RBA's Target

Inflation Remains Well-Below The RBA's Target