Equities

Dear Client, I am delighted to take charge of the US Equity Strategy publication upon Anastasios Avgeriou’s departure. By way of introduction, I have been an investor for nearly 20 years, with my career spanning both the buy and sell side, bottom-up stock selection and top-down asset allocation, and fundamental and quantitative approaches to investing. I have invested through two business cycles (starting on the third one now), watched the internet stock bubble burst, and seen grown men shedding tears on Bloomberg keyboards in the summer of 2008 – the market has a way of humbling us, mere mortals. As a result of these diverse professional experiences, I became an agnostic and don’t believe there is one correct way to invest as long as a thesis is well thought through and backed up by numbers and in-depth analysis. I believe that different approaches to investing, fundamental and quant, bottom up and top down, should complement each other leading to “best of all worlds” results. I also rely on an investment framework which is disciplined enough to offer a structure to fall back on to minimize behavioral biases, and yet is flexible to rapidly accommodate both “black swan” and “grey rhino” themes into investment decision-making. The following are the guiding principles of this investment framework. I hope this week’s publication will provide insights into my approach to investing and the nature of the US Equity Strategy product under my stewardship. I look forward to your feedback and suggestions. Kind Regards, Irene Tunkel Chief Strategist, US Equity Strategy Principle 1: The Business Cycle Matters The business cycle and macroeconomic conditions are the cornerstones of any investment decision as they underpin the fundamentals of most assets, and preordain the types of assets likely to outperform based on their level of risk and sensitivity to economic growth. Analyzing the stages of the business cycle is a succinct way to summarize a wide range of economic data, such as capacity utilization, growth, policy, credit conditions and valuation. Each business cycle is different, yet on average across all cycles, the stages have the following characteristics (Table 1). Table 1Business Cycle Is In Expansion Stage

Eight Principles Of Successful Equity Investing

Eight Principles Of Successful Equity Investing

Recovery: Policy is easy, and liquidity is plentiful, profits rebound but growth is scarce, inflation is low, risk aversion elevated, and stocks are still cheap. In this environment cyclicals, small caps and value outperform. Expansion: Policy is neutral, inflation is moderate, growth is abundant, risk aversion is low. During this phase it is cyclicals and small caps that shine. Slowdown: Inflation is higher, and policy is tightened, growth is rolling over, valuations are extended, and risk aversion is rising. In this environment of slowing growth, growth stocks, large caps, defensives and real assets outperform (Chart 1). Contraction: Deflation (or fears thereof) ensues, output is falling, growth is scarce and risk aversion is high. In this environment defensives, quality and highly profitable stocks rule the day. Chart 1Performance Of Equities In Different Stages Of Business Cycle

Eight Principles Of Successful Equity Investing

Eight Principles Of Successful Equity Investing

Although the pandemic is barely over, the markets have galloped through the recovery stage and have landed squarely in expansion territory. US equities exhibited exceptional earnings growth of 52.5% year-on-year in Q1-2021 on the back of economic reopening, fiscal and monetary stimulus, and pent-up demand. Monetary and fiscal policy remain easy. The only deviation from a textbook description of expansion is low capacity utilization and a high unemployment rate which persist as aftereffects of factors specific to the pandemic: School closures and elevated unemployment benefits. High unemployment whilst demand for labor is high triggered inflationary pressures. However, we believe that we are near the end of the expansion stage and are about to transition into a moderate slowdown. While growth is to remain robust, it is bound to slow modestly from its peak: The Manufacturing ISM PMI came down from 64.7 in April to 61.2 in June. According to Bloomberg consensus estimates GDP growth is to slow from 6.4% in 2021 to 4% in 2022. The Fed is starting to “talk about talking about tightening”, and with inflation elevated many expect somewhat hawkish rhetoric/intervention from the Fed sooner than the end of 2022. Valuations are rich. Now may be opportune time to reposition for a slowdown to be ahead of the game. To do well in a slowdown stage, which may last for months but by no means heralds the end of a bull market in equities, we recommend dusting off growth, large-cap and defensive stocks and taking profits in some of the recent cyclical outperformers. A barbell approach may do well at this point, with portfolio overweights in both cyclical sectors such as energy and industrials along with more defensive plays such as health care and technology Principle 2: Shocks And Transient Themes Trump Both Macro And Fundamentals Macro is important on the cyclical time horizon but, intra-cycle, it is transient themes and macro shocks that move markets. These themes, also known as “black swans” and “grey rhinos”, are exogenous shocks and developments that dominate investor psyche. Mostly, they are policy driven, like trade war or fiscal stimulus, but occasionally are force majeure events, like Covid-19. Transient themes may have a positive or negative effect on the market. These are news and developments that are not immediately priced by the market but are not to be ignored or dismissed: They dominate investment outcomes irrespective of the normal market order of things. Usually transient themes are short-lived and fade once macroeconomic and fundamental data have readjusted to the new reality: Economic and earnings growth estimates have been revised, and relevant stock and sector returns have absorbed the shock. Back in March 2020, neither fundamentals nor valuations mattered. Nor did macro. Stocks were first sledgehammered by a “corona” theme, and then soared on a “liquidity is abundant” theme. It took analysts three months to downgrade US GDP growth to contraction (Chart 2)! Over the past few months, the only theme that seemed to matter to market participants was inflation, and inflation alone. Implications? Fear of inflation and sooner-than-expected Fed tightening have triggered an energetic selloff in bonds and defensive/growth equities. However, there are early signs that this theme is beginning to fade with rates stabilizing and growth stocks rebounding (Chart 3). Chart 2Markets Take Time To Price In Shocks

Markets Take Time To Price In Shocks

Markets Take Time To Price In Shocks

Chart 3Inflation Fears Triggered Equity Rotation

Inflation Fears Triggered Equity Rotation

Inflation Fears Triggered Equity Rotation

Principle 3: Interplay Between Valuations And Fundamentals Once the macro backdrop and transient themes are well understood, we zoom in our analysis to the valuations and fundamentals of individual styles and sectors to select the most attractive opportunities. Ideally, we are looking for the reasonably priced sectors that have solid fundamentals and can deliver strong growth. Finding sectors like that is easier said than done: Rarely do good and cheap exist in the same incarnation. Hence, investors need to compromise: Buy cheap stocks with poor earnings growth and challenged fundamentals or pay a premium for solid growth. A classic value/growth dilemma. Our approach is as follows: Cheap Sectors: Relative valuations are very important: Most value investments are mean-reversion plays (Chart 4) We don’t attach much weight to fundamentals – we don’t expect a stellar balance sheet or earnings growth In order to screen out value traps, we are looking for a catalyst for mean reversion For cheap stocks valuations are more important than fundamentals. Expensive Sectors: Relative valuations are much less important than growth expectations and fundamentals. Are fundamentals continuing to improve or have they reached a peak? Is earnings growth about to accelerate or slow? If fundamentals, e.g. RoE or margins are improving, and a slowdown in growth is not expected, then the valuation premium is justified. Chart 4Value Is Mean Reverting

Eight Principles Of Successful Equity Investing

Eight Principles Of Successful Equity Investing

The software industry group is a case in point. Back in 2019-2020 valuations were eyewatering (more than two standard deviations above 10 years of history) but earnings growth was resilient, and profitability was in a multi-year upward trend. The valuation premium was justified. But late in 2020 RoE started deteriorating, and the industry group experienced a pullback. More recently, RoE has stabilized and turned. Returns are following (Chart 5). Chart 5Changes In Profitability Drive Valuations

Changes In Profitability Drive Valuations

Changes In Profitability Drive Valuations

Principle 4: Stock Markets Are Markets Of Stocks Understanding the behavior of individual stocks makes top-down sector and style selection much more informed and nuanced. After all, we are dealing not just with a stock market, but with a market of stocks. Those glued to Bloomberg screens in March 2020 may have noticed a rare green with companies like Zoom, Citrix and Amazon rallying amidst stock Armageddon. These were green shoots (no pun intended) of one the most vigorous stock market rallies in history. Paying attention to stock-level data also gave an early pointer that pandemic shutdowns, as awful as they were, would be a boon for selected technology and e-commerce sectors (Chart 6). At present, we notice that cyclicals have not outperformed defensives since March. We also notice over the past two-to-three weeks the comeback of hot technology stocks, many of which are former “Covid-19 winners”, beaten up by a “back-to-work rally”. These are fintech and e-commerce names such as PayPal, Pinterest and Peloton, some of which are more than 50% off from their February peak. Reversal in performance of growth stocks is a sign that rates have stabilized, inflation fears are overdone, and US economic growth is gradually slowing. Chart 6Covid-19 Winners Led S&P 500 Rebound

Covid-19 Winners Led S&P 500 Rebound

Covid-19 Winners Led S&P 500 Rebound

Principle 5: Markets Are Forward Looking As Warren Buffet succinctly put it “buy risky assets when there is blood in the streets”, and “be fearful [i.e., sell], when others are greedy.” In other words, it is important to anticipate turning points, and be one step ahead of the market. Last year’s rally is a case in point, with the S&P 500 delivering the best return in history despite not having much to show for it in terms of earnings growth, with nearly 70% of S&P 500 returns coming from multiple expansion. Investors looked past shutdowns, rightly believing that the profit recession is transitory, companies are in sound financial health, valuations are at abysmal, once-in-a-lifetime, levels, and the V-shaped recovery will ensue once the pandemic is over (Chart 7). Chart 7Stocks Returns Lead Earnings

Stocks Returns Lead Earnings

Stocks Returns Lead Earnings

Conversely, the Q1-2021 earnings season was stellar, but many stocks, even those which exceeded expectations, have ceded gains: Stocks are priced to perfection, and investors concluded that, for some of them, the best days are behind, and growth is slowing (Chart 8). At present, trailing valuations of nearly all sectors and styles in the S&P 500 are at extreme levels, trading at 36x trailing earnings. However, forward PEs are on average 9 points lower, around 21x forward earnings. Hope is that the stock market will rerate and grow into its big shoes within the next 12 months with expected EPS growth of 23%. We think it will! Chart 8During Q1-2021 Earning Season, Beats Were Not Rewarded

During Q1-2021 Earning Season, Beats Were Not Rewarded

During Q1-2021 Earning Season, Beats Were Not Rewarded

Principle 6: Asset Prices Respond To The “Second Derivative” This principle is a corollary to “markets are forward looking”. Usually the rate of growth is already priced in, as markets are efficient and new information arrives as a change in expected growth, i.e. the impulse. Change in the growth outlook is absorbed by the markets and is a leading indicator of turning points in equity returns. Most often the impulse relates to change in economic or earnings growth expectations. For example, sales for the hotels industry group are still falling, but at a lower rate than before (the second derivative is improving). These “less bad” numbers are enough to send hotels returns soaring (Chart 9). Chart 9Hotels Are Rallying On “Less Bad” Sales

Hotels Are Rallying On “Less Bad” Sales

Hotels Are Rallying On “Less Bad” Sales

Principle 7: Thematic Investing: Channeling Cathie Woods Thematic investing is really “smart” momentum investing, but its appeal lies in being able to identify a theme/catalyst that unites stocks and makes them move in unison. Knowing a theme behind momentum helps one to understand its thematic drivers and anticipate turning points. Arguably, thematic investing is a nuisance for stock pickers, but a boon for top-down investors: Identifying a theme has a higher impact on portfolio returns than choosing the individual stocks to represent it. For example, identifying recovery in air travel and investing into the Jets ETF is a more important decision than choosing the right airline stock. Since February 2020, American Airlines is 94% and Delta is 98% correlated with Jets ETF (Chart 10). Knowing the drivers, we can brainstorm what can trigger a reversal of this theme, for example: An increase in the price of oil, a structural shift in business travel, falling consumer confidence, and a high household dissaving rate. Thematic investing is popular as it allows an investor to ride the momentum yet also be equipped to anticipate turning points. Chart 10Air Travel Stocks Are Highly Correlated

Air Travel Stocks Are Highly Correlated

Air Travel Stocks Are Highly Correlated

Thematic investing may be over a variety of investment horizons (stocks benefitting from retirement of baby boomers being an example of a structural theme versus stocks benefitting from post-corona supply-chain disruption being (hopefully) a short-lived theme). Further, themes can be high tech, such as autonomous driving or green energy, and low tech, such as the pandemic “puppy boom”. The most prominent and widely discussed themes in the recent months are “Covid-19 winners” vs “back to work”. Arguably, thematic investing is the “passive investing” of the future – a trend illustrated by the popularity of the ARK funds managed by Cathie Woods. Going forward, the US Equity service will be covering investment themes in a series of Special Reports. Principle 8: “No Country Is An Island” Lastly, while the focus of this publication is squarely on the US equity market, it is important to keep an eye on developments in the rest of the world. Companies in the S&P 500 derive 43% of sales from abroad. As a result, corporate earnings are highly sensitive to the direction of the trade-weighted dollar both due to the price of goods and to translation effects. Recent depreciation of the dollar will boost corporate earnings growth, especially for the technology (58% of earnings outside the US), materials (56%) and energy (50%) sectors. It takes roughly three to six months to fully absorb dollar moves into sales growth (Chart 11). Further, the economic growth rates of the major US trading partners, i.e., Europe, Mexico, Canada, and China, also have a profound effect on the US economy with transmission through the US trade balance, dollar movements and Treasury yields (Chart 12). Chart 11US Dollar Drives S&P 500 Sales

US Dollar Drives S&P 500 Sales

US Dollar Drives S&P 500 Sales

Chart 12Major US Trading Partners Affect US Economy

Major US Trading Partners Affect US Economy

Major US Trading Partners Affect US Economy

Bottom Line Markets are complex: Macro works until it does not, expensive stocks can be a good investment, and an equity rally may take off in the midst of an earnings recession. Yet, we believe that the eight principles of investing that we have outlined above will guide us through the noise and help successfully navigate equity markets. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com

The 10-year US Treasury yield has been range bound between 1.5% and 1.7% for the past three months despite fireworks in the US economic data, from CPI readings to unemployment beats. The fact that the bond market has refused to budge no matter how positive US data got, confirms our view that all the good news has already been priced in. Citigroup US economic surprise index (CESI) is hovering around zero, which corroborates the same message. Given a tight positive correlation (0.44) between CESI and UST10Y, and the fact that growth is peaking, it is unlikely that the bond market will enter another aggressive sell-off phase (see chart). The implication for equities is that long-duration growth equities, beaten down by rising yields, may stage a come back, especially once inflation data makes a clear ∩-turn on a year-over-year basis. Bottom Line: Bond market is likely to remain calm over the next three to six months, and it’s time to revisit beaten down growth names. Stay tuned for future research on the topic.

Time to Revisit Growth Names

Time to Revisit Growth Names

Highlights The Norwegian economy will continue to grow above trend for the next two years or so. Norwegian inflation will firm up. Among Advanced Economies, the Norges Bank will lead the way in terms of policy tightening; however, money markets already embed this view. Nonetheless, the Norwegian krone remains an appealing value play, a result of its pronounced pro-cyclicality. USD/NOK and EUR/NOK will depreciate over the next 24 months. Norwegian equities face structural headwinds, but they should outperform their US and Euro Area counterparts. However, Norwegian stocks will lag behind Swedish equities. Buy Norwegian stocks / sell Dutch ones. Feature Norway remains an example of how to handle the pandemic successfully. Since the onset of the COVID-19 crisis, Norway has registered the lowest rate of infections per capita, in part aided by its early decision to close its borders. Fiscal stimulus was prompt and finely tailored to the sectors most in need of emergency funds. Moreover, the Norges Bank cut interest rates to zero for the first time since its founding in 1816. As nations across the world coordinated monetary and fiscal accommodation during the pandemic, Nordic economies had already mastered this paradigm. Thus, counter-cyclical buffers worked like a charm in Norway. For example, the contraction in Norwegian GDP was the most subdued within the G10, and the recovery is also impressive. Today, Norwegian GDP is 2% above pre-pandemic levels, inflation is near the target rate of 2%, and the central bank will be among the first to lift interest rates. In this Special Report, we explore whether or not conditions remain ripe for strong performances by both Norwegian equities and the NOK. In our view, the global environment and the continued economic strength of Norway will create potent tailwind for Norwegian assets over the coming two years or so. A Robust Economic Outlook The Norwegian economy is set to continue growing at a robust above-trend pace and inflation will remain above the Norges Bank’s target. The Pandemic Norway has moved largely beyond the COVID-19 pandemic. The number of cases per 100 is a mere 2, which compares favorably to the US at 10, Germany at 4, France at 8, or its neighbor Sweden at 10. Norway closed its borders on March 12, 2020, to limit the entry of the virus on its territory, as health authorities opted for rapid containment measures. As a direct result of these policies, Norwegian consumers and workers gained greater peace of mind in their day-to-day dealings, and economic activity recovered rapidly. This process led to Norway’s GDP contracting by only 4.6% in Q2 2020, which compares favorably to contractions of 19.5% in the UK, 9.7% in Germany and 7.8% in Sweden. Norway’s vaccination campaign is also gaining momentum. At first, the country’s inoculation performance lagged. However, Norwegian procurement of vaccines has improved, and the pace of inoculation is accelerating (Chart 1, top panel). The result is that the share of the population that is fully vaccinated is inching toward 20% and accelerating. Authorities expect greater relaxation of containment measures this summer, which will allow mobility to improve (Chart 2). The local service sector will therefore receive a welcome fillip. Chart 1Norway's Vaccination Progress

Norway's Vaccination Progress

Norway's Vaccination Progress

Chart 2Mobility Will Pick Up

Mobility Will Pick Up

Mobility Will Pick Up

Fiscal Policy Fiscal policy remains an important complement to national health directives. During the crisis, the fiscal deficit reached 3.4% of GDP, which generated a fiscal thrust of 6% of GDP. Moreover, the drawdown from the Norwegian Oil Fund amounted to 12.5% of GDP. These provided targeted supports to industries, such as tourism and transport, while a furlough scheme protected household income. Thus, these programs effectively alleviated the pain on the sectors of the economy most affected by the pandemic. Going forward, Norway will also suffer from one of the smallest fiscal drag in the G10 for the remainder of 2021 and 2022 (Chart 3). Chart 3Norway's Advantageous Fiscal Backdrop

Norway's Advantageous Fiscal Backdrop

Norway's Advantageous Fiscal Backdrop

The Banking System The credit channel in Norway remains open and fluid, as a resilient banking system withstood the economic fallout from the pandemic. According to the Norges Bank, credit losses have been limited; they peaked at 1% of lending and are already declining. Additionally, banks have restricted exposure to the sectors hardest hit by the pandemic, such as travel and tourism, personal services, and transport (Chart 4). Moreover, the profitability of the banking system decreased, as global yields fell last year, but RoE remains around 10% and net interest margins hover near 2.5% and 1.5% for non-financial corporate loans and households lending, respectively. Crucially, the Norwegian banking system sports a regulatory Tier-1 capital-to-risk weighted-assets ratio of 20%, well above Basel III criteria or that of the Eurozone banks (Chart 4, bottom panel). Chart 4Norwegian Banks Are Faring Well

The Norwegian Method

The Norwegian Method

Household Consumption Household consumption will remain a source of strength over the coming quarters. Household net worth is growing robustly as a result of the rapid appreciation of house prices across the country (Chart 5, top panel). Moreover, the share of debt held by households with a high debt-to-income ratio or a low debt-servicing capacity remains low, which suggests household balance sheets are firming (Chart 5, middle panel). Employment is also recovering well. After peaking at 9.5% in March 2020, the headline unemployment rate fell to 3.3% last month (Chart 5, bottom panel). Meanwhile, the number of employed workers bottomed in July 2020 and has been steadily recovering ever since. The only blemish is that, as of Q4 2020, the rate of underemployment among the prime-age population remains at 3.5%, which is somewhat elevated by national standards. This balance sheet and employment backdrop confirms the Norges Bank’s projection: the household savings rate will decline significantly over the coming two years (Chart 6, top panel). Hence, the marked pick-up in consumer confidence should translate into a major recovery in real consumption growth (Chart 6, bottom panel). Nonetheless, the service sector will likely be the main beneficiary of this improvement, as real retail sales are already well above their historical trend Chart 5Positive Household Fundamentals

Positive Household Fundamentals

Positive Household Fundamentals

Chart 6Consumption Will Improve Further

Consumption Will Improve Further

Consumption Will Improve Further

Net Exports Chart 7Years Of Underinvestment In Oil & Gas

The Norwegian Method

The Norwegian Method

The external sector will create another tailwind for the Norwegian economy. Prior to the pandemic, 71% of Norway’s exports flowed to Europe. Moreover, oil and gas represented 53% of shipments, and cyclically sensitive exports amounted to 74% of total or 24% of GDP. Thus, even if China’s economy slows, Europe’s economic re-opening will raise the Norwegian trade balance, which sits near a multi-decade low.1 Moreover, greater mobility in Europe and around the world will elevate demand for petroleum. In light of the tepid pace of investment in global oil and gas extraction over the past five years, our commodity strategists forecast further oil and gas price appreciation2 (Chart 7), which will boost Norway’s terms of trade. The national income will therefore expand smartly, especially because oil and gas shipments will increase thanks to growing production from the new Johan Sverdrup field. Capital Spending This context suggests that capital spending, which accounts for 26% of Norway’s output (Chart 8), will constitute an important tailwind to domestic activity. Capex is even more important to the Norwegian economy than it is for other Nordic economies or even Germany (Chart 9). Chart 8Capital Spending Is Important For Norway

Capital Spending Is Important For Norway

Capital Spending Is Important For Norway

Chart 9The Capex Share Of GDP Is Higher In Norway

The Capex Share Of GDP Is Higher In Norway

The Capex Share Of GDP Is Higher In Norway

Norwegian capex is highly cyclical. Capital formation tracks our BCA Global Nowcast indicator (a combination of high-frequency economic and financial variables that proxy the global industrial cycle), as well as the domestic manufacturing PMI. These indicators suggest that capex should increase by 10-15% in the coming quarters (Chart 10). A Norges Bank survey of capex intentions, which are firming, corroborates this view. Chart 10Capex Will Recover Strongly Capex Will Recover

Capex Will Recover Strongly Capex Will Recover

Capex Will Recover Strongly Capex Will Recover

On the energy front, the new Johan Sverdrup oil and gas discovery marks a major turnaround in capital spending for Norway. According to the Norges Bank, real petroleum investment will increase from approximately NOK 175bn in 2021 to NOK 198bn by 2024 (Chart 11). Moreover, years of global underinvestment in oil extraction suggests Norway will gain market share in exports as production accelerates. Total petroleum production is slated to increase by 10% over the next 4 years. More importantly, by 2025, over 50% of production from Norwegian oil fields will be natural gas and associated liquids (Chart 12). Demand for natural gas and NGLs will be more inelastic than demand for crude because the latter is threatened by the rising electrification of vehicles, while the former faces more sustainable demand as China, among others, moves to replace its coal polluting plants with cleaner alternatives. Chart 11Real Petroleum Investment Will Increase By 13% In 2024

The Norwegian Method

The Norwegian Method

Chart 12Gas Production Is Rising In Importance

The Norwegian Method

The Norwegian Method

Inflation This positive economic outlook suggests that Norwegian inflation will remain above the central bank’s target of 2%. Already, headline CPI stands at 3%. Meanwhile, core inflation is at 2%, but it is decelerating. However, this slowdown should be temporary. According to a Norges Bank survey, both long-term and near-term inflation expectations among economists, business leaders, and households are rising, which indicates that a deflationary mentality has not taken root in Norway. Moreover, wage expectations have quickly normalized following the trauma of 2020 (Chart 13). Capacity constraints further reinforce the notion that inflation has upside. The Norges Bank Regional Network survey shows that capacity and labor supply constraints are tighter than they were in the 2014 to 2017 period, when inflation averaged 2.3% and the policy rate fell to 0.5% (Chart 14). Moreover, according to the same survey, selling prices are also stronger than they were during the 2016 oil collapse (Chart 14, bottom panel) Chart 13No Signs Of A Deflation Mentality

No Signs Of A Deflation Mentality

No Signs Of A Deflation Mentality

Chart 14Capacity Doesn’t Point To Falling Inflation

The Norwegian Method

The Norwegian Method

Bottom Line: The Norwegian economy will continue to grow above its trend rate of 1.5%, at least through to 2022. The acceleration in vaccination numbers will allow a reopening of the economy, while the fiscal drag will be limited and the banking system remains resilient. The outlook for households remains positive and employment is firming, which will lead to stronger consumption. Meanwhile, exports and capex have significant upside ahead. As a result, we anticipate Norwegian inflation will remain above target for the foreseeable future. The Norges Bank Will Lead The Pack The Norges Bank’s response to the pandemic was swift and all encompassing: It cut interest rates in the spring of 2020 from 1.5% to zero, the lowest level since the formation of the bank in 1816. It set up extraordinary F-loans at very generous interest rates, to provide ample liquidity to commercial banks. The longest maturity loan of 12 months had a prevailing interest rate of just 30 basis points. It also relaxed collateral requirements for these loans. It introduced swap lines with the Federal Reserve to provide US dollar funding to Norwegian firms. Since then, our Norges Bank monitor has rebounded powerfully from very depressed levels, which suggests that emergency policy settings have become unnecessary. Moreover, the Norwegian Central Bank Monitor towers above that of other G10 countries, which indicates that the Norges Bank should lead the pack in normalizing policy rates (Chart 15). Chart 15The Norges Bank Should Lead The Tightening Cycle

The Norges Bank Should Lead The Tightening Cycle

The Norges Bank Should Lead The Tightening Cycle

Chart 16The Growth Component Of Our Monitor Has Exploded Higher

The Growth Component Of Our Monitor Has Exploded Higher The Growth Component Of Our Monitor Has Exploded Higher

The Growth Component Of Our Monitor Has Exploded Higher The Growth Component Of Our Monitor Has Exploded Higher

The biggest improvement in our Norges Bank Monitor comes from its growth component, which has surged to its highest levels in over two decades. This improvement surpasses those that followed the global financial crisis and the burst of the dot-com bubble (Chart 16). In essence, the growth component of the Monitor signals that the Norwegian economy has achieved escape velocity. Norway’s robust economic turnover is increasing the velocity of money, which points to the need for higher interest rates. Money velocity can be regarded as the equilibrating mechanism between money supply and nominal output, from the classical Fisher equation MV=PQ (where M is the money supply, P is prices, Q is real output, and V is money velocity). Thus, rising money velocity (when PQ expands faster than M) signifies that the economy needs higher interest rates to encourage savings. In Norway’s case, the velocity of money is surging through 2021, which confirms that the Norges Bank may depart from its current emergency policy setting (Chart 17). Chart 17Money Velocity Is Rising In Norway

Money Velocity Is Rising In Norway

Money Velocity Is Rising In Norway

The OIS curve already reflects this reality. At the last central bank meeting in March, Governor Øystein Olsen stated that interest rates would increase in the second half of this year. Already, the central bank’s balance sheet has been expanding more slowly than that of its peers (Chart 18). In response to this messaging, investors now expect the Norges Bank to lead the Fed, ECB, Riksbank, and BoE in lifting interest rates (Chart 19). Chart 18The Norges Bank's Balance Sheet Impulse Has Rolled Over

The Norges Bank's Balance Sheet Impulse Has Rolled Over

The Norges Bank's Balance Sheet Impulse Has Rolled Over

Chart 19Money Markets Already Expect The Norges Bank To Tighten First

Money Markets Already Expect The Norges Bank To Tighten First

Money Markets Already Expect The Norges Bank To Tighten First

The Norges Bank must nonetheless manage a tough balancing act. Lifting rates too soon or too fast could torpedo the recovery, if the currency and bond yields increase too rapidly and tighten financial conditions in a disruptive fashion. However, not removing accommodation fast enough could lead to economic overheating. Bottom Line: The Norges Bank will be the first DM central bank to increase interest rates, most likely as soon as this September. The OIS curve already reflects this outlook; it prices in over 6 hikes by the end of 2023, more than any other DM money market curve. This pricing seems appropriate; thus, Norwegian money markets offer no compelling investment opportunity. Norway’s Problem: Sagging Productivity Both the OECD and the IMF view weak productivity growth as Norway’s biggest long-term hurdle. Despite the bright economic outlook for the next two years or so, we agree. Since 2004-2005, Norwegian productivity has sharply decelerated. At the turn of the millennium, the Norwegian’s mainland labor productivity was growing at 2.5%, or a percentage point above the average of the OECD. Today, labor productivity growth is a paltry 0.5%, placing Norway last among Nordic economies (Chart 20, left panel). Total factor productivity tells a similar story. After recording the fastest productivity expansion among G10 nation from 1990 to 2005, Norway’s TFP declined 11% and is now situated at the same level as it was in 1995. This deterioration is comparable to Italy’s TFP (Chart 20, left panel). Chart 20From Best To Last

The Norwegian Method

The Norwegian Method

According to the most recent OECD country report, one of the roots of Norway’s productivity problem is an absence of low-hanging fruit. Norway sports one of the highest GDP per hours worked in the world. This nation essentially sits near the global productivity frontier. Its product market regulations are generally not onerous (Chart 21, top panel). Likewise, more than 60% of both the service sector and the manufacturing sector’s workforce use ICT tools, which is at the highest level among OECD countries. Additionally, the jobs at risk of a negative impact from automation or technological changes represent a significantly smaller share of total employment than in most OECD nations (Chart 21, bottom panel). Chart 21Doing Things Right

The Norwegian Method

The Norwegian Method

The Dutch Disease, the hollowing out of the manufacturing sector due to a capital hungry resource sector, is the second root of Norway’s productivity problem. Historically and across countries, manufacturing is the sector that records the greatest productivity gains. However, since 1979, the oil and gas and the housing sectors have experienced the largest capital investments expansion in Norway. Meanwhile, the share of capex generated by the manufacturing sector has declined to a paltry 5% (Chart 22). Moreover, oil and gas represents a larger share of capex than the contribution of its gross value added to GDP. The same holds true for housing, whose share of capex doubled over the past 27 years. Meanwhile, manufacturing’s share of capex has consistently lagged its representation in GDP, which has steadily declined (Chart 23). These are the typical symptoms of the Dutch Disease; as long as oil prices remain in a secular decline, any cyclical improvement in productivity will prove to be transitory. Chart 22The Dutch Disease, Part I

The Dutch Disease, Part I

The Dutch Disease, Part I

Chart 23The Dutch Disease, Part II

The Dutch Disease, Part II

The Dutch Disease, Part II

Bottom Line: Despite an upbeat cyclical outlook, Norway’s deteriorating productivity trend constitutes a formidable structural headwind. There are no easy solutions, because Norway already sits near the global productivity frontier. Moreover, Norway suffers from a pronounced case of the Dutch Disease. For decades, the oil and gas sector has absorbed a share of capital that is greater than its role in the economy, starving the productivity-generating manufacturing sector from investments. With the oil sector entering a structural decline due to ESG concerns, this trend will not change without a significant change in the allocation of the Norwegian capital stock. Investment Implications The cyclical outlook (12 to 24 months) for the Norwegian currency and stock market remains appealing. The NOK’s Outlook Chart 24The Krone Is Undervalued On A PPP Basis

The Krone Is Undervalued On A PPP Basis

The Krone Is Undervalued On A PPP Basis

While money markets do not offer any compelling opportunities to play the Norges Bank’s hiking cycle, the krone remains attractive from a cyclical perspective. Over the next 12-18 months, the NOK should appreciate compared to both the US dollar and the euro on the back of four key pillars. On a purchasing power parity basis, the Norwegian krone is undervalued by 14%. This compares favorably with both the euro, which is undervalued by 12%, and the US dollar, which is overvalued by 12% (Chart 24). More importantly, our PPP model adjusts the consumption basket across countries, allowing for a more apples-to-apples comparison. The Norwegian krone is highly procyclical and will benefit from any improvement in the global backdrop. The performance of NOK/USD, NOK/EUR, and NOK/JPY moves in lockstep with global equities (Chart 25). Norwegian equities have greatly underperformed global bourses over the last decade, but, as we argue below, there is some room for mean reversion. Inflows into the Norwegian equity market should benefit the krone (Chart 26). Chart 25NOK Is A Procyclical ##br##Currency

NOK Is A Procyclical Currency

NOK Is A Procyclical Currency

Chart 26NOK Moves With A Rerating In Norwegian Shares

NOK Moves With A Rerating In Norwegian Shares

NOK Moves With A Rerating In Norwegian Shares

From a more fundamental perspective, the krone will benefit from positive income flows, given Norway’s large net international investment position (NIIP). In fact, ever since the first Norwegian oil fields began producing light sweet crude in the North Sea in the 1970s, Norway has maintained a structural trade surplus with most of its trading partners. This has allowed the country to build one of the biggest NIIP in the world (Chart 27), trailing only behind Hong Kong and Singapore. This large NIIP generates large income receipts that skew heavily toward equity dividends. This characteristic of the Norwegian balance of payment strengthens the bond between the NOK and global equities. Over the next few years, Norway’s trade balance should also get a boost, not only from rising oil and gas production, but also from an improvement in terms of trade, as we argued above. The trade balance has historically been the biggest driver of cross-border inflows into Norway, and that should remain positive for the basic balance and the NOK (Chart 28) Chart 28Norway's Basic Balance Should Improve Norway Balance Of Payments

Norway's Basic Balance Should Improve Norway Balance Of Payments

Norway's Basic Balance Should Improve Norway Balance Of Payments

Chart 27Norway Has A Large Net International Investment Position

Norway Has A Large Net International Investment Position

Norway Has A Large Net International Investment Position

On a structural basis, however, the Norwegian krone faces challenges. Declining productivity suggests that economic growth in Norway will be more inflationary. This will lower the fair value of the real exchange rate. Therefore, while we are positive on the NOK over the next 18 to 24 months, we will be cognizant not to overstay our welcome. Finally, as for NOK/SEK, the pair should rise as both oil and gas prices remain firm in the near term, but any structural challenges to both oil and/or Norwegian productivity will favor the SEK over the longer term (Chart 29). Chart 29NOK/SEK Will Track Crude Prices

NOK/SEK Will Track Crude Prices

NOK/SEK Will Track Crude Prices

The Equity Market Outlook Norwegian equities remain challenged as long-term holdings, but they are attractive on a cyclical basis. The poor profitability of Norwegian equities is their main long-term problem. Unlike Swedish stocks, Norwegian shares sport a return on equity in line with that of the Eurozone, not that of the US. Norway’s profit margins are weak and its asset turnover rivals that of the Euro Area (Chart 30). Additionally, the country’s poor productivity performance argues against a sudden reversal in RoEs. Chart 30Norway Is More Like The Eurozone Than Swden

Norway Is More Like The Eurozone Than Swden

Norway Is More Like The Eurozone Than Swden

Sectoral composition creates another structural handicap for the Norwegian market. Oslo overweighs Energy and Financials (Table 1). Energy stocks can experience periodic rallies, but their long-term outlook is bleak in a world moving away from carbon-based power. Meanwhile, financials are also likely to remain structural laggards. The regulatory legacy of the Great Financial Crisis has curtailed leverage, which is depressing the RoE of the banking sector. Greater competition and the emergence of the fintech industry are further undermining fee income. None of these factors will change anytime soon. Table 1Sectoral Breakdown

The Norwegian Method

The Norwegian Method

That being said, Norwegian equities remain a compelling opportunity for the next two years or so, despite their long-term problems. Norwegian stocks have an extremely negative beta to the US dollar. The historical sensitivity of the NOK to the USD in part explains this attribute, the other part being their elevated cyclicality. The dollar is one of the most counter-cyclical currencies in the world; thus, its weakness correlates with strong Norwegian forward earnings, which are heavily influenced by commodity prices and the global industrial cycle. This process also lifts Norwegian stock prices (Chart 31). Hence, BCA’s positive outlook on the global business cycle, as well as our negative stance on the dollar, points to significantly stronger Norwegian share prices.3 The slowdown in China’s economy is one risk that could cause some near-term tremors in Norwegian assets, which investors should use to build positions. In response to Beijing’s efforts to limit systemic risk, the Chinese credit impulse has slowed from 1.1% of GDP to 0.3%, and could flirt with the zero line. The ensuing investment slowdown will weigh on the global industrial sector and cause a temporary pullback in commodity prices. As Chart 32 illustrates, this will be negative for Norwegian equities; historically, following declines in Chinese yields, Norwegian forward earnings and stock prices weaken. However, global energy demand will remain robust even as China slows; therefore, correcting Norwegian equities create a buying opportunity. Chart 31Norwegian Stocks Are A Dollar-Bearish Bet

Norwegian Stocks Are A Dollar-Bearish Bet

Norwegian Stocks Are A Dollar-Bearish Bet

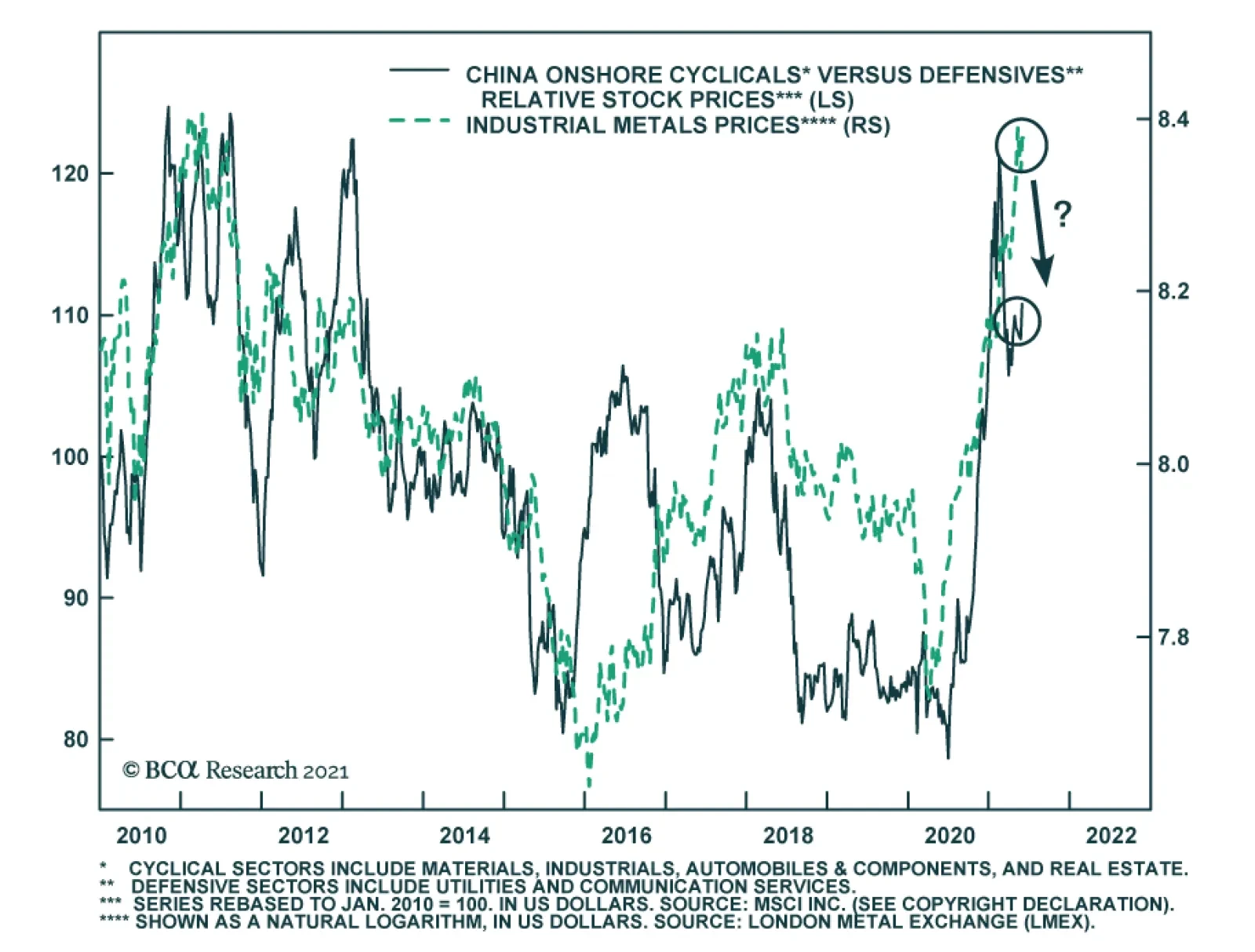

Chart 32A Chinese Slowdown Is A Risk

A Chinese Slowdown Is A Risk

A Chinese Slowdown Is A Risk

Norwegian stocks should also outperform US and Eurozone equities. Nonetheless, Norwegian equities enjoy their greatest appeal against the US benchmark. Norwegian stocks trade at valuation discounts ranging from 38% to 54% compared to their US counterparts. Meanwhile, Norway’s net earnings revisions remain depressed compared to the US. Most importantly, Norwegian stocks are more pro-cyclical and sensitive to EM and global financial conditions than US shares are. Consequently, Oslo outperforms New York when the broad trade-weighted dollar depreciates, EM currencies appreciate, and the global yield curve slope steepens (Chart 33). We expect these trends to intensify over the remainder of the business cycle. Chart 33Oslo Beats New York

Oslo Beats New York

Oslo Beats New York

Norwegian equities are also more responsive than Eurozone equities to global business-cycle oscillations. Norwegian equities outperform those of the Eurozone when the dollar depreciates (Chart 34). Additionally, a simple modelling exercise reveals that rising oil prices and global yields result in higher relative share prices in favor of Norway (Chart 35). Chart 34Norway Outperforms The Eurozone When The Dollar Weakens

Norway Outperforms The Eurozone When The Dollar Weakens

Norway Outperforms The Eurozone When The Dollar Weakens

Chart 35Favor Norway Over ##br##The Euro Area

Favor Norway Over The Euro Area

Favor Norway Over The Euro Area

Sweden is the one market that maintains a hedge over Norway.4 Swedish stocks not only sport a RoE nine percentage point above that of Norway, they are also sensitive to the global business cycle. However, the main advantage of Swedish equities is their sectoral breakdown. Sweden has an enormous overweight in industrials (38% of the benchmark), while Norway greatly overweighs materials. In an environment in which China is likely to decelerate, but global capex and infrastructure spending will remain firm, Sweden’s industrials’ weighting gives it a powerful advantage over its neighbor’s stock market. Finally, we recommend the following high-octane trade: Long Norwegian / short Dutch stocks. The Amsterdam bourse has a 47% allocation to tech stocks and a greater “growth” bias than the S&P 500. This means that the relative performance of Norwegian stocks compared to Dutch equities is even more sensitive to the global business cycle, oil prices, and bond yields. As a result, our simple model incorporating both Brent prices and yields currently sends a strong buy signal in favor of Norway (Chart 36). Chart 36Time To Buy Norway And Sell The Netherlands

Time To Buy Norway And Sell The Netherlands

Time To Buy Norway And Sell The Netherlands

Bottom Line: The NOK will perform strongly against both the USD and the EUR over the coming 18 to 24 months. Norwegian equities are not an appealing long-term bet; however, they will experience significant upside over the coming two years, both in absolute terms and relative to the US and Euro Area stocks. While Oslo is unlikely to outperform Stockholm over this period, we recommend buying Norwegian stocks and selling the Dutch index. Mathieu Savary Chief European Investment Strategist Mathieu@bcaresearch.com Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see European Investment Strategy Report, "A Surprising Dance," dated May 10, 2021. 2 Please see Commodity & Energy Strategy Report, "OPEC’s 2.0 Production Strategy In Focus," dated May 20, 2021. 3 Please see Foreign Exchange Strategy Report, "Explaining Recent Weakness In The US Dollar," dated May 14, 2021. 4 Please see European Investment Strategy Report, "Take A Chance On Sweden," dated May 03, 2021.

Highlights The Norwegian economy will continue to grow above trend for the next two years or so. Norwegian inflation will firm up. Among Advanced Economies, the Norges Bank will lead the way in terms of policy tightening; however, money markets already embed this view. Nonetheless, the Norwegian krone remains an appealing value play, a result of its pronounced pro-cyclicality. USD/NOK and EUR/NOK will depreciate over the next 24 months. Norwegian equities face structural headwinds, but they should outperform their US and Euro Area counterparts. However, Norwegian stocks will lag behind Swedish equities. Buy Norwegian stocks / sell Dutch ones. Feature Norway remains an example of how to handle the pandemic successfully. Since the onset of the COVID-19 crisis, Norway has registered the lowest rate of infections per capita, in part aided by its early decision to close its borders. Fiscal stimulus was prompt and finely tailored to the sectors most in need of emergency funds. Moreover, the Norges Bank cut interest rates to zero for the first time since its founding in 1816. As nations across the world coordinated monetary and fiscal accommodation during the pandemic, Nordic economies had already mastered this paradigm. Thus, counter-cyclical buffers worked like a charm in Norway. For example, the contraction in Norwegian GDP was the most subdued within the G10, and the recovery is also impressive. Today, Norwegian GDP is 2% above pre-pandemic levels, inflation is near the target rate of 2%, and the central bank will be among the first to lift interest rates. In this Special Report, we explore whether or not conditions remain ripe for strong performances by both Norwegian equities and the NOK. In our view, the global environment and the continued economic strength of Norway will create potent tailwind for Norwegian assets over the coming two years or so. A Robust Economic Outlook The Norwegian economy is set to continue growing at a robust above-trend pace and inflation will remain above the Norges Bank’s target. The Pandemic Norway has moved largely beyond the COVID-19 pandemic. The number of cases per 100 is a mere 2, which compares favorably to the US at 10, Germany at 4, France at 8, or its neighbor Sweden at 10. Norway closed its borders on March 12, 2020, to limit the entry of the virus on its territory, as health authorities opted for rapid containment measures. As a direct result of these policies, Norwegian consumers and workers gained greater peace of mind in their day-to-day dealings, and economic activity recovered rapidly. This process led to Norway’s GDP contracting by only 4.6% in Q2 2020, which compares favorably to contractions of 19.5% in the UK, 9.7% in Germany and 7.8% in Sweden. Norway’s vaccination campaign is also gaining momentum. At first, the country’s inoculation performance lagged. However, Norwegian procurement of vaccines has improved, and the pace of inoculation is accelerating (Chart 1, top panel). The result is that the share of the population that is fully vaccinated is inching toward 20% and accelerating. Authorities expect greater relaxation of containment measures this summer, which will allow mobility to improve (Chart 2). The local service sector will therefore receive a welcome fillip. Chart 1Norway's Vaccination Progress

Norway's Vaccination Progress

Norway's Vaccination Progress

Chart 2Mobility Will Pick Up

Mobility Will Pick Up

Mobility Will Pick Up

Fiscal Policy Fiscal policy remains an important complement to national health directives. During the crisis, the fiscal deficit reached 3.4% of GDP, which generated a fiscal thrust of 6% of GDP. Moreover, the drawdown from the Norwegian Oil Fund amounted to 12.5% of GDP. These provided targeted supports to industries, such as tourism and transport, while a furlough scheme protected household income. Thus, these programs effectively alleviated the pain on the sectors of the economy most affected by the pandemic. Going forward, Norway will also suffer from one of the smallest fiscal drag in the G10 for the remainder of 2021 and 2022 (Chart 3). Chart 3Norway's Advantageous Fiscal Backdrop

Norway's Advantageous Fiscal Backdrop

Norway's Advantageous Fiscal Backdrop

The Banking System The credit channel in Norway remains open and fluid, as a resilient banking system withstood the economic fallout from the pandemic. According to the Norges Bank, credit losses have been limited; they peaked at 1% of lending and are already declining. Additionally, banks have restricted exposure to the sectors hardest hit by the pandemic, such as travel and tourism, personal services, and transport (Chart 4). Moreover, the profitability of the banking system decreased, as global yields fell last year, but RoE remains around 10% and net interest margins hover near 2.5% and 1.5% for non-financial corporate loans and households lending, respectively. Crucially, the Norwegian banking system sports a regulatory Tier-1 capital-to-risk weighted-assets ratio of 20%, well above Basel III criteria or that of the Eurozone banks (Chart 4, bottom panel). Chart 4Norwegian Banks Are Faring Well

The Norwegian Method

The Norwegian Method

Household Consumption Household consumption will remain a source of strength over the coming quarters. Household net worth is growing robustly as a result of the rapid appreciation of house prices across the country (Chart 5, top panel). Moreover, the share of debt held by households with a high debt-to-income ratio or a low debt-servicing capacity remains low, which suggests household balance sheets are firming (Chart 5, middle panel). Employment is also recovering well. After peaking at 9.5% in March 2020, the headline unemployment rate fell to 3.3% last month (Chart 5, bottom panel). Meanwhile, the number of employed workers bottomed in July 2020 and has been steadily recovering ever since. The only blemish is that, as of Q4 2020, the rate of underemployment among the prime-age population remains at 3.5%, which is somewhat elevated by national standards. This balance sheet and employment backdrop confirms the Norges Bank’s projection: the household savings rate will decline significantly over the coming two years (Chart 6, top panel). Hence, the marked pick-up in consumer confidence should translate into a major recovery in real consumption growth (Chart 6, bottom panel). Nonetheless, the service sector will likely be the main beneficiary of this improvement, as real retail sales are already well above their historical trend Chart 5Positive Household Fundamentals

Positive Household Fundamentals

Positive Household Fundamentals

Chart 6Consumption Will Improve Further

Consumption Will Improve Further

Consumption Will Improve Further

Net Exports Chart 7Years Of Underinvestment In Oil & Gas

The Norwegian Method

The Norwegian Method

The external sector will create another tailwind for the Norwegian economy. Prior to the pandemic, 71% of Norway’s exports flowed to Europe. Moreover, oil and gas represented 53% of shipments, and cyclically sensitive exports amounted to 74% of total or 24% of GDP. Thus, even if China’s economy slows, Europe’s economic re-opening will raise the Norwegian trade balance, which sits near a multi-decade low.1 Moreover, greater mobility in Europe and around the world will elevate demand for petroleum. In light of the tepid pace of investment in global oil and gas extraction over the past five years, our commodity strategists forecast further oil and gas price appreciation2 (Chart 7), which will boost Norway’s terms of trade. The national income will therefore expand smartly, especially because oil and gas shipments will increase thanks to growing production from the new Johan Sverdrup field. Capital Spending This context suggests that capital spending, which accounts for 26% of Norway’s output (Chart 8), will constitute an important tailwind to domestic activity. Capex is even more important to the Norwegian economy than it is for other Nordic economies or even Germany (Chart 9). Chart 8Capital Spending Is Important For Norway

Capital Spending Is Important For Norway

Capital Spending Is Important For Norway

Chart 9The Capex Share Of GDP Is Higher In Norway

The Capex Share Of GDP Is Higher In Norway

The Capex Share Of GDP Is Higher In Norway

Norwegian capex is highly cyclical. Capital formation tracks our BCA Global Nowcast indicator (a combination of high-frequency economic and financial variables that proxy the global industrial cycle), as well as the domestic manufacturing PMI. These indicators suggest that capex should increase by 10-15% in the coming quarters (Chart 10). A Norges Bank survey of capex intentions, which are firming, corroborates this view. Chart 10Capex Will Recover Strongly Capex Will Recover

Capex Will Recover Strongly Capex Will Recover

Capex Will Recover Strongly Capex Will Recover

On the energy front, the new Johan Sverdrup oil and gas discovery marks a major turnaround in capital spending for Norway. According to the Norges Bank, real petroleum investment will increase from approximately NOK 175bn in 2021 to NOK 198bn by 2024 (Chart 11). Moreover, years of global underinvestment in oil extraction suggests Norway will gain market share in exports as production accelerates. Total petroleum production is slated to increase by 10% over the next 4 years. More importantly, by 2025, over 50% of production from Norwegian oil fields will be natural gas and associated liquids (Chart 12). Demand for natural gas and NGLs will be more inelastic than demand for crude because the latter is threatened by the rising electrification of vehicles, while the former faces more sustainable demand as China, among others, moves to replace its coal polluting plants with cleaner alternatives. Chart 11Real Petroleum Investment Will Increase By 13% In 2024

The Norwegian Method

The Norwegian Method

Chart 12Gas Production Is Rising In Importance

The Norwegian Method

The Norwegian Method

Inflation This positive economic outlook suggests that Norwegian inflation will remain above the central bank’s target of 2%. Already, headline CPI stands at 3%. Meanwhile, core inflation is at 2%, but it is decelerating. However, this slowdown should be temporary. According to a Norges Bank survey, both long-term and near-term inflation expectations among economists, business leaders, and households are rising, which indicates that a deflationary mentality has not taken root in Norway. Moreover, wage expectations have quickly normalized following the trauma of 2020 (Chart 13). Capacity constraints further reinforce the notion that inflation has upside. The Norges Bank Regional Network survey shows that capacity and labor supply constraints are tighter than they were in the 2014 to 2017 period, when inflation averaged 2.3% and the policy rate fell to 0.5% (Chart 14). Moreover, according to the same survey, selling prices are also stronger than they were during the 2016 oil collapse (Chart 14, bottom panel) Chart 13No Signs Of A Deflation Mentality

No Signs Of A Deflation Mentality

No Signs Of A Deflation Mentality

Chart 14Capacity Doesn’t Point To Falling Inflation

The Norwegian Method

The Norwegian Method

Bottom Line: The Norwegian economy will continue to grow above its trend rate of 1.5%, at least through to 2022. The acceleration in vaccination numbers will allow a reopening of the economy, while the fiscal drag will be limited and the banking system remains resilient. The outlook for households remains positive and employment is firming, which will lead to stronger consumption. Meanwhile, exports and capex have significant upside ahead. As a result, we anticipate Norwegian inflation will remain above target for the foreseeable future. The Norges Bank Will Lead The Pack The Norges Bank’s response to the pandemic was swift and all encompassing: It cut interest rates in the spring of 2020 from 1.5% to zero, the lowest level since the formation of the bank in 1816. It set up extraordinary F-loans at very generous interest rates, to provide ample liquidity to commercial banks. The longest maturity loan of 12 months had a prevailing interest rate of just 30 basis points. It also relaxed collateral requirements for these loans. It introduced swap lines with the Federal Reserve to provide US dollar funding to Norwegian firms. Since then, our Norges Bank monitor has rebounded powerfully from very depressed levels, which suggests that emergency policy settings have become unnecessary. Moreover, the Norwegian Central Bank Monitor towers above that of other G10 countries, which indicates that the Norges Bank should lead the pack in normalizing policy rates (Chart 15). Chart 15The Norges Bank Should Lead The Tightening Cycle

The Norges Bank Should Lead The Tightening Cycle

The Norges Bank Should Lead The Tightening Cycle

Chart 16The Growth Component Of Our Monitor Has Exploded Higher

The Growth Component Of Our Monitor Has Exploded Higher The Growth Component Of Our Monitor Has Exploded Higher

The Growth Component Of Our Monitor Has Exploded Higher The Growth Component Of Our Monitor Has Exploded Higher

The biggest improvement in our Norges Bank Monitor comes from its growth component, which has surged to its highest levels in over two decades. This improvement surpasses those that followed the global financial crisis and the burst of the dot-com bubble (Chart 16). In essence, the growth component of the Monitor signals that the Norwegian economy has achieved escape velocity. Norway’s robust economic turnover is increasing the velocity of money, which points to the need for higher interest rates. Money velocity can be regarded as the equilibrating mechanism between money supply and nominal output, from the classical Fisher equation MV=PQ (where M is the money supply, P is prices, Q is real output, and V is money velocity). Thus, rising money velocity (when PQ expands faster than M) signifies that the economy needs higher interest rates to encourage savings. In Norway’s case, the velocity of money is surging through 2021, which confirms that the Norges Bank may depart from its current emergency policy setting (Chart 17). Chart 17Money Velocity Is Rising In Norway

Money Velocity Is Rising In Norway

Money Velocity Is Rising In Norway

The OIS curve already reflects this reality. At the last central bank meeting in March, Governor Øystein Olsen stated that interest rates would increase in the second half of this year. Already, the central bank’s balance sheet has been expanding more slowly than that of its peers (Chart 18). In response to this messaging, investors now expect the Norges Bank to lead the Fed, ECB, Riksbank, and BoE in lifting interest rates (Chart 19). Chart 18The Norges Bank's Balance Sheet Impulse Has Rolled Over

The Norges Bank's Balance Sheet Impulse Has Rolled Over

The Norges Bank's Balance Sheet Impulse Has Rolled Over

Chart 19Money Markets Already Expect The Norges Bank To Tighten First

Money Markets Already Expect The Norges Bank To Tighten First

Money Markets Already Expect The Norges Bank To Tighten First

The Norges Bank must nonetheless manage a tough balancing act. Lifting rates too soon or too fast could torpedo the recovery, if the currency and bond yields increase too rapidly and tighten financial conditions in a disruptive fashion. However, not removing accommodation fast enough could lead to economic overheating. Bottom Line: The Norges Bank will be the first DM central bank to increase interest rates, most likely as soon as this September. The OIS curve already reflects this outlook; it prices in over 6 hikes by the end of 2023, more than any other DM money market curve. This pricing seems appropriate; thus, Norwegian money markets offer no compelling investment opportunity. Norway’s Problem: Sagging Productivity Both the OECD and the IMF view weak productivity growth as Norway’s biggest long-term hurdle. Despite the bright economic outlook for the next two years or so, we agree. Since 2004-2005, Norwegian productivity has sharply decelerated. At the turn of the millennium, the Norwegian’s mainland labor productivity was growing at 2.5%, or a percentage point above the average of the OECD. Today, labor productivity growth is a paltry 0.5%, placing Norway last among Nordic economies (Chart 20, left panel). Total factor productivity tells a similar story. After recording the fastest productivity expansion among G10 nation from 1990 to 2005, Norway’s TFP declined 11% and is now situated at the same level as it was in 1995. This deterioration is comparable to Italy’s TFP (Chart 20, left panel). Chart 20From Best To Last

The Norwegian Method

The Norwegian Method

According to the most recent OECD country report, one of the roots of Norway’s productivity problem is an absence of low-hanging fruit. Norway sports one of the highest GDP per hours worked in the world. This nation essentially sits near the global productivity frontier. Its product market regulations are generally not onerous (Chart 21, top panel). Likewise, more than 60% of both the service sector and the manufacturing sector’s workforce use ICT tools, which is at the highest level among OECD countries. Additionally, the jobs at risk of a negative impact from automation or technological changes represent a significantly smaller share of total employment than in most OECD nations (Chart 21, bottom panel). Chart 21Doing Things Right

The Norwegian Method

The Norwegian Method

The Dutch Disease, the hollowing out of the manufacturing sector due to a capital hungry resource sector, is the second root of Norway’s productivity problem. Historically and across countries, manufacturing is the sector that records the greatest productivity gains. However, since 1979, the oil and gas and the housing sectors have experienced the largest capital investments expansion in Norway. Meanwhile, the share of capex generated by the manufacturing sector has declined to a paltry 5% (Chart 22). Moreover, oil and gas represents a larger share of capex than the contribution of its gross value added to GDP. The same holds true for housing, whose share of capex doubled over the past 27 years. Meanwhile, manufacturing’s share of capex has consistently lagged its representation in GDP, which has steadily declined (Chart 23). These are the typical symptoms of the Dutch Disease; as long as oil prices remain in a secular decline, any cyclical improvement in productivity will prove to be transitory. Chart 22The Dutch Disease, Part I

The Dutch Disease, Part I

The Dutch Disease, Part I

Chart 23The Dutch Disease, Part II

The Dutch Disease, Part II

The Dutch Disease, Part II

Bottom Line: Despite an upbeat cyclical outlook, Norway’s deteriorating productivity trend constitutes a formidable structural headwind. There are no easy solutions, because Norway already sits near the global productivity frontier. Moreover, Norway suffers from a pronounced case of the Dutch Disease. For decades, the oil and gas sector has absorbed a share of capital that is greater than its role in the economy, starving the productivity-generating manufacturing sector from investments. With the oil sector entering a structural decline due to ESG concerns, this trend will not change without a significant change in the allocation of the Norwegian capital stock. Investment Implications The cyclical outlook (12 to 24 months) for the Norwegian currency and stock market remains appealing. The NOK’s Outlook Chart 24The Krone Is Undervalued On A PPP Basis

The Krone Is Undervalued On A PPP Basis

The Krone Is Undervalued On A PPP Basis

While money markets do not offer any compelling opportunities to play the Norges Bank’s hiking cycle, the krone remains attractive from a cyclical perspective. Over the next 12-18 months, the NOK should appreciate compared to both the US dollar and the euro on the back of four key pillars. On a purchasing power parity basis, the Norwegian krone is undervalued by 14%. This compares favorably with both the euro, which is undervalued by 12%, and the US dollar, which is overvalued by 12% (Chart 24). More importantly, our PPP model adjusts the consumption basket across countries, allowing for a more apples-to-apples comparison. The Norwegian krone is highly procyclical and will benefit from any improvement in the global backdrop. The performance of NOK/USD, NOK/EUR, and NOK/JPY moves in lockstep with global equities (Chart 25). Norwegian equities have greatly underperformed global bourses over the last decade, but, as we argue below, there is some room for mean reversion. Inflows into the Norwegian equity market should benefit the krone (Chart 26). Chart 25NOK Is A Procyclical ##br##Currency

NOK Is A Procyclical Currency

NOK Is A Procyclical Currency

Chart 26NOK Moves With A Rerating In Norwegian Shares

NOK Moves With A Rerating In Norwegian Shares

NOK Moves With A Rerating In Norwegian Shares

From a more fundamental perspective, the krone will benefit from positive income flows, given Norway’s large net international investment position (NIIP). In fact, ever since the first Norwegian oil fields began producing light sweet crude in the North Sea in the 1970s, Norway has maintained a structural trade surplus with most of its trading partners. This has allowed the country to build one of the biggest NIIP in the world (Chart 27), trailing only behind Hong Kong and Singapore. This large NIIP generates large income receipts that skew heavily toward equity dividends. This characteristic of the Norwegian balance of payment strengthens the bond between the NOK and global equities. Over the next few years, Norway’s trade balance should also get a boost, not only from rising oil and gas production, but also from an improvement in terms of trade, as we argued above. The trade balance has historically been the biggest driver of cross-border inflows into Norway, and that should remain positive for the basic balance and the NOK (Chart 28) Chart 28Norway's Basic Balance Should Improve Norway Balance Of Payments

Norway's Basic Balance Should Improve Norway Balance Of Payments

Norway's Basic Balance Should Improve Norway Balance Of Payments

Chart 27Norway Has A Large Net International Investment Position

Norway Has A Large Net International Investment Position

Norway Has A Large Net International Investment Position

On a structural basis, however, the Norwegian krone faces challenges. Declining productivity suggests that economic growth in Norway will be more inflationary. This will lower the fair value of the real exchange rate. Therefore, while we are positive on the NOK over the next 18 to 24 months, we will be cognizant not to overstay our welcome. Finally, as for NOK/SEK, the pair should rise as both oil and gas prices remain firm in the near term, but any structural challenges to both oil and/or Norwegian productivity will favor the SEK over the longer term (Chart 29). Chart 29NOK/SEK Will Track Crude Prices

NOK/SEK Will Track Crude Prices

NOK/SEK Will Track Crude Prices

The Equity Market Outlook Norwegian equities remain challenged as long-term holdings, but they are attractive on a cyclical basis. The poor profitability of Norwegian equities is their main long-term problem. Unlike Swedish stocks, Norwegian shares sport a return on equity in line with that of the Eurozone, not that of the US. Norway’s profit margins are weak and its asset turnover rivals that of the Euro Area (Chart 30). Additionally, the country’s poor productivity performance argues against a sudden reversal in RoEs. Chart 30Norway Is More Like The Eurozone Than Swden

Norway Is More Like The Eurozone Than Swden

Norway Is More Like The Eurozone Than Swden

Sectoral composition creates another structural handicap for the Norwegian market. Oslo overweighs Energy and Financials (Table 1). Energy stocks can experience periodic rallies, but their long-term outlook is bleak in a world moving away from carbon-based power. Meanwhile, financials are also likely to remain structural laggards. The regulatory legacy of the Great Financial Crisis has curtailed leverage, which is depressing the RoE of the banking sector. Greater competition and the emergence of the fintech industry are further undermining fee income. None of these factors will change anytime soon. Table 1Sectoral Breakdown

The Norwegian Method

The Norwegian Method

That being said, Norwegian equities remain a compelling opportunity for the next two years or so, despite their long-term problems. Norwegian stocks have an extremely negative beta to the US dollar. The historical sensitivity of the NOK to the USD in part explains this attribute, the other part being their elevated cyclicality. The dollar is one of the most counter-cyclical currencies in the world; thus, its weakness correlates with strong Norwegian forward earnings, which are heavily influenced by commodity prices and the global industrial cycle. This process also lifts Norwegian stock prices (Chart 31). Hence, BCA’s positive outlook on the global business cycle, as well as our negative stance on the dollar, points to significantly stronger Norwegian share prices.3 The slowdown in China’s economy is one risk that could cause some near-term tremors in Norwegian assets, which investors should use to build positions. In response to Beijing’s efforts to limit systemic risk, the Chinese credit impulse has slowed from 1.1% of GDP to 0.3%, and could flirt with the zero line. The ensuing investment slowdown will weigh on the global industrial sector and cause a temporary pullback in commodity prices. As Chart 32 illustrates, this will be negative for Norwegian equities; historically, following declines in Chinese yields, Norwegian forward earnings and stock prices weaken. However, global energy demand will remain robust even as China slows; therefore, correcting Norwegian equities create a buying opportunity. Chart 31Norwegian Stocks Are A Dollar-Bearish Bet

Norwegian Stocks Are A Dollar-Bearish Bet

Norwegian Stocks Are A Dollar-Bearish Bet

Chart 32A Chinese Slowdown Is A Risk

A Chinese Slowdown Is A Risk

A Chinese Slowdown Is A Risk

Norwegian stocks should also outperform US and Eurozone equities. Nonetheless, Norwegian equities enjoy their greatest appeal against the US benchmark. Norwegian stocks trade at valuation discounts ranging from 38% to 54% compared to their US counterparts. Meanwhile, Norway’s net earnings revisions remain depressed compared to the US. Most importantly, Norwegian stocks are more pro-cyclical and sensitive to EM and global financial conditions than US shares are. Consequently, Oslo outperforms New York when the broad trade-weighted dollar depreciates, EM currencies appreciate, and the global yield curve slope steepens (Chart 33). We expect these trends to intensify over the remainder of the business cycle. Chart 33Oslo Beats New York

Oslo Beats New York

Oslo Beats New York

Norwegian equities are also more responsive than Eurozone equities to global business-cycle oscillations. Norwegian equities outperform those of the Eurozone when the dollar depreciates (Chart 34). Additionally, a simple modelling exercise reveals that rising oil prices and global yields result in higher relative share prices in favor of Norway (Chart 35). Chart 34Norway Outperforms The Eurozone When The Dollar Weakens

Norway Outperforms The Eurozone When The Dollar Weakens

Norway Outperforms The Eurozone When The Dollar Weakens

Chart 35Favor Norway Over ##br##The Euro Area

Favor Norway Over The Euro Area

Favor Norway Over The Euro Area

Sweden is the one market that maintains a hedge over Norway.4 Swedish stocks not only sport a RoE nine percentage point above that of Norway, they are also sensitive to the global business cycle. However, the main advantage of Swedish equities is their sectoral breakdown. Sweden has an enormous overweight in industrials (38% of the benchmark), while Norway greatly overweighs materials. In an environment in which China is likely to decelerate, but global capex and infrastructure spending will remain firm, Sweden’s industrials’ weighting gives it a powerful advantage over its neighbor’s stock market. Finally, we recommend the following high-octane trade: Long Norwegian / short Dutch stocks. The Amsterdam bourse has a 47% allocation to tech stocks and a greater “growth” bias than the S&P 500. This means that the relative performance of Norwegian stocks compared to Dutch equities is even more sensitive to the global business cycle, oil prices, and bond yields. As a result, our simple model incorporating both Brent prices and yields currently sends a strong buy signal in favor of Norway (Chart 36). Chart 36Time To Buy Norway And Sell The Netherlands

Time To Buy Norway And Sell The Netherlands

Time To Buy Norway And Sell The Netherlands

Bottom Line: The NOK will perform strongly against both the USD and the EUR over the coming 18 to 24 months. Norwegian equities are not an appealing long-term bet; however, they will experience significant upside over the coming two years, both in absolute terms and relative to the US and Euro Area stocks. While Oslo is unlikely to outperform Stockholm over this period, we recommend buying Norwegian stocks and selling the Dutch index. Mathieu Savary Chief European Investment Strategist Mathieu@bcaresearch.com Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see European Investment Strategy Report, "A Surprising Dance," dated May 10, 2021. 2 Please see Commodity & Energy Strategy Report, "OPEC’s 2.0 Production Strategy In Focus," dated May 20, 2021. 3 Please see Foreign Exchange Strategy Report, "Explaining Recent Weakness In The US Dollar," dated May 14, 2021. 4 Please see European Investment Strategy Report, "Take A Chance On Sweden," dated May 03, 2021. Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades