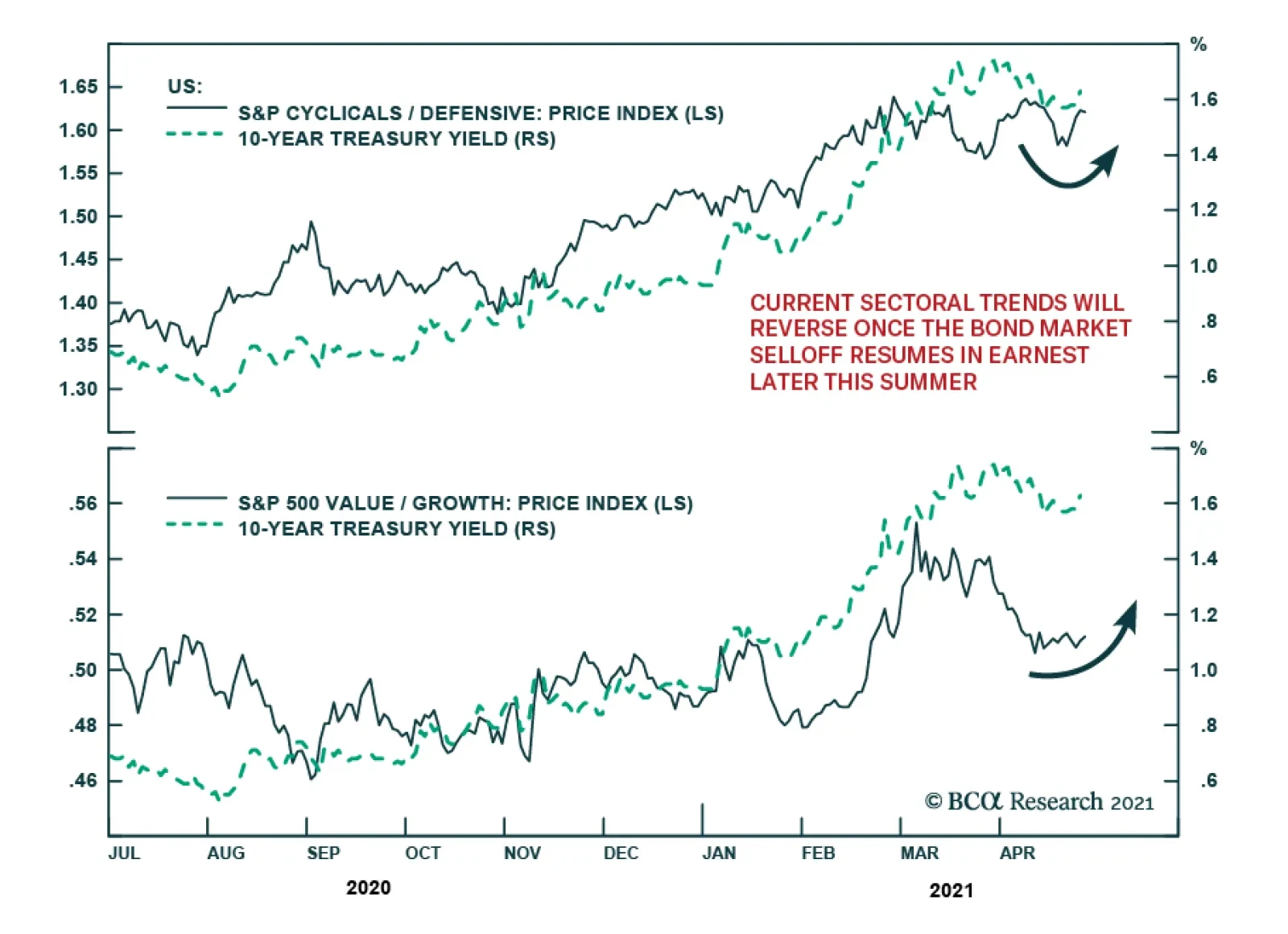

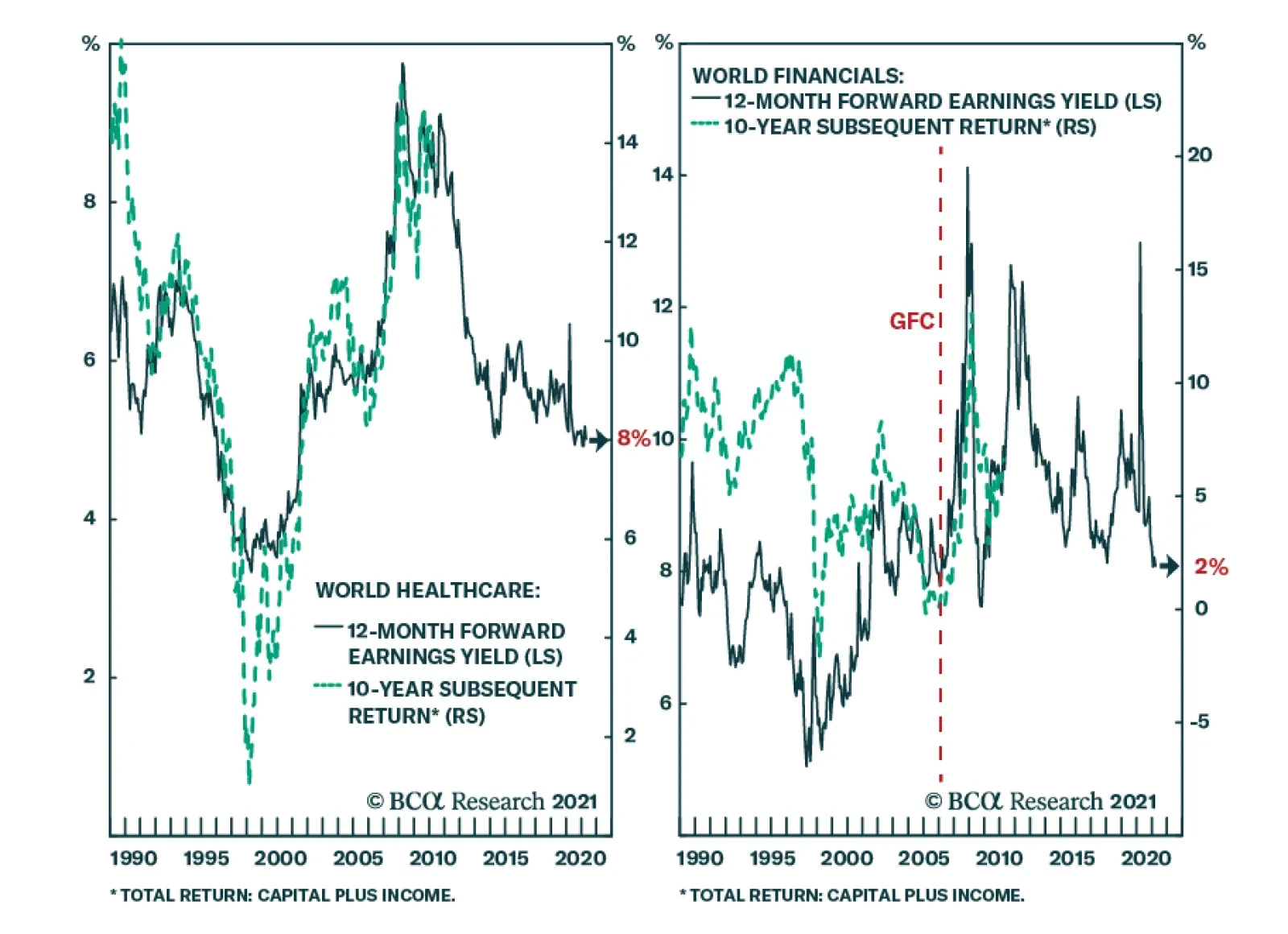

Equities

Highlights Sweden’s economic recovery is robust and will deepen. Policy is accommodative. Very few advanced economies will benefit as much from the global economic rebound. The labor market will tighten, capacity utilization will increase, and inflation will rise faster than the Riksbank forecasts. On a one- to two-year investment horizon, the SEK is a buy against both the USD and the EUR. Despite their pronounced outperformance, Swedish stocks possess significantly more upside against both Eurozone and US equities over the remainder of the cycle. Swedish industrials will beat their competitors in both these markets. Nonetheless, China’s policy tightening creates a meaningful tactical risk, which selling Norwegian stocks can hedge. Italy’s fiscal plan constitutes a new salvo in Europe’s efforts to avoid last decade’s mistakes. Feature Last week, the Swedish Riksbank did not follow in the footsteps of the Norges Bank. The Swedish central bank acknowledged that the economy is performing better than anticipated and that the housing market is gaining in strength; yet, it refrained from hinting at any forthcoming adjustment to its policy rate or the pace of its asset purchase program. The positive outlook for the Swedish economy will force the Riksbank to tighten policy significantly before the ECB. As a result, we expect the Swedish Krona to outperform the euro and the US dollar. Moreover, investors should continue to overweight Swedish equities due to their large exposure to industrials and financials, even if they have already significantly outperformed the Euro Area. Sweden’s Economic Outlook The Swedish economy will accelerate, which will put pressure on resource utilization and fan inflationary risk in the years ahead. The degree of stimulus supporting Sweden is consequential. Chart 1A Dual Labor Market

A Dual Labor Market

A Dual Labor Market

On the fiscal front, the government support measures that have been announced since the beginning of the COVID-19 crisis currently amount to SEK420bn, or SEK197bn for 2020 (4% of GDP), and SEK223bn for 2021 (4.5% of GDP). Moreover, generous labor market protection and part-time employment schemes meant that the number of employees in permanent employment contracts remained stable during the pandemic (Chart 1). Thus, the bulk of the rise in Swedish unemployment came from workers on fixed-term contracts. Monetary policy remains very accommodative as well. The Riksbank left its repo rate unchanged at 0% through the crisis, but cut its lending rate from 0.75% to 0.1%. More importantly, the Swedish central bank is aggressively injecting liquidity into the economy. It set up a SEK500bn funding-for-lending facility in order to incentivize bank lending to the nonfinancial private sector, and started a SEK700bn QE program, which as of Q1 2021 had purchased SEK380bn securities and which will purchase another SEK120bn in Q2, with covered bonds issued by banks accounting for 70% of it. As a result, the amount of securities held on the Riksbank balance sheet will nearly triple by year end (Chart 2). Chart 2The Riksbank Is Open For Business

Take A Chance On Sweden

Take A Chance On Sweden

Beyond the monetary and fiscal stimulus, many factors point to greater economic strength for Sweden. Despite a slow start to the process, as of last week, nearly 30% of the Swedish population had received at least one vaccine dose, which is broadly in line with vaccination rates prevalent in France or Germany. Crucially, the pace of vaccination is accelerating at a rate of 13% per week. Even if this second derivative slows, more than 70% of the population will have received at least one dose by this summer. Thus, greater mobility is in the cards during the second quarter, which will boost household spending. Chart 3The Wealth Effect

The Wealth Effect

The Wealth Effect

The housing market also favors a pick-up in consumption. The HOX housing price index is growing at a 15% annual rate, its fastest expansion in over 5 years. As a result of the wealth effect, this rapid appreciation is consistent with a swift improvement in the growth rate of household expenditures (Chart 3). Moreover, spending on durable goods now stands 1.3% above its pre-pandemic levels, while spending on non-durables is back to pre-pandemic levels. This context suggests that increased mobility translates into greater spending. The industrial sector remains a particularly bright spot in the Swedish economy. Sweden is extremely sensitive to the global industrial and trade cycle, because exports represent 45% of GDP. Moreover, the highly cyclical intermediate and capital goods comprise 56% of the country’s foreign shipments, which accentuates the beta of the Swedish economy. BCA Research remains optimistic about the global industrial cycle. Sweden will reap a significant dividend. Already the Swedish PMI points to stronger industrial production, and the index’s exports component is roaring ahead (Chart 4). The potential for a greater uptake in consumption, capex, and durable goods spending in the rest of the EU (Sweden’s largest trading partner) bodes well for the Swedish manufacturing sector. Additionally, if the collapse in the US inventory-to-sales ratio is any indication for the rest of the world, a global restocking cycle is forthcoming, which will further boost Swedish industrial activity (Chart 4, bottom panels). Finally, global public infrastructure plans are on the rise, which will also help Sweden. Chart 4Sweden Is well Placed

Sweden Is well Placed

Sweden Is well Placed

Chart 5Brightening Labor Market Prospects

Brightening Labor Market Prospects

Brightening Labor Market Prospects

In this context, the Swedish labor market should tighten significantly in the approaching quarters. Already, job vacancies are rebounding, and redundancy notices have normalized, which matches both the GDP growth surprise in Q1 and the continued rise in the NIER Sweden Economic Tendency Indicator. Furthermore, the employment component of the PMIs stands at 58.9 and is consistent with a sharp improvement in job growth over the coming year (Chart 5). The expected labor market growth will contribute to an increase in capacity utilization, which will place upward pressure on wages and inflation. When the 12-month moving average of US and Eurozone imports rises, so does the Riksbank Resource Utilization Indicator, because global trade has such a pronounced effect on the Swedish economy (Chart 6). Meanwhile, greater resource utilization leads to accelerated inflation, greater labor shortages, and rising unit labor costs (Chart 7). Chart 6CAPU Will Rise

CAPU Will Rise

CAPU Will Rise

Chart 7The Coming Pressure Buildup

The Coming Pressure Buildup

The Coming Pressure Buildup

Bottom Line: As a result of generous stimulus and the global economic recovery, the Swedish economy is set to continue its rebound. Consequently, employment and capacity utilization will improve meaningfully, which will lead to a resurgence of inflation and wages in the coming 24 months. Investment Implications On a 12 to 24 months horizon, we remain positive on the Swedish krona and Swedish equities. Fixed Income And FX Chart 8Three Hikes By 2025

Three Hikes By 2025

Three Hikes By 2025

The backend of the Swedish OIS curve only discounts 75bps of hikes by 2025. This pricing is too modest (Chart 8). The Swedish economy will rebound further as the vaccination campaign advances, and rising house prices and household indebtedness will fan growing long-term risk to financial stability, both of which suggest that the Riksbank will have to change its tack in 2022. The great likelihood that the Fed will start tapering off its asset purchase toward the end this year, that the ECB will follow sometime in 2022, and that the Norges Bank will be increasing interest rates next year will give more leeway to the Swedish central bank. A wider Sweden/Germany 10-year government bond spread is not an appealing vehicle to play a more hawkish Riksbank down the road. This spread hit a 23-year high in March and now rests at 62bps or its 98th percentile since 2000. Moreover, the terminal rate proxy embedded in the German money market curve is currently so low that the spread between Sweden’s and the Eurozone’s terminal rate proxy stands near a record high. Hence, German yields already embed much more pessimism than Swedish ones. Nonetheless, BCA recommends a below benchmark duration exposure within the Swedish fixed-income space, as we do for other government bond markets around the world.1 A bullish bias toward the SEK is a bet on the Riksbank that offers a very appealing risk/reward ratio, according to BCA Research’s Foreign Exchange Strategy strategists.2 The krona is very cheap against both the euro and the US dollar, trading at 9% and 29% discounts to purchasing power parity, respectively. Moreover, the Swedish current account stands at 5.2% of GDP, compared to 2.3% and -3.1% for the Euro Area and the US, creating a natural underpinning under the SEK. Chart 9The SEK Loves Growth

The SEK Loves Growth

The SEK Loves Growth

Over the coming 12 to 24 months, cyclical forces favor selling EUR/SEK and USD/SEK on any strength. The SEK is one of the most cyclical G-10 currencies and has one of the strongest sensitivities to the US dollar. Hence, our positive global economic outlook and our FX strategists negative view on the greenback are synonymous with a weak USD/SEK. These same factors also mean that the krona will appreciate more than the euro, as the negative correlation between EUR/SEK and our Boom/Bust Indicator and global earnings growth illustrate (Chart 9). Equities We also like Swedish equities, but the state of the Swedish economy and the evolution of the Riksbank policy surprise have a limited impact on Swedish equities. The Swedish bourse is mostly about the evolution of the global business cycle. The Swedish benchmark heightened sensitivity to the global business cycle reflects its massive overweight in deep cyclicals, with industrials, financials, consumer discretionary, and materials accounting for 38.4%, 26.1%, 9.7% and 3.7% of the MSCI index respectively, or 78% altogether (Table 1). As a result, BCA’s preference for global cyclicals at the expense of defensives and this publication’s fondness for the recovery laggards like the industrial and financial sectors automatically translate into a favorable bias toward Sweden’s stocks.3 Table 1Mamma Mia! That’s A Lot Of Cyclicals

Take A Chance On Sweden

Take A Chance On Sweden

Valuations offer a more complex picture, but they do not diminish our predilection for Sweden. Swedish equities trade at a discount to US stocks but at a premium to Euro Area ones (Chart 10). However, Swedish stocks offer higher RoEs and profit margins than both the US and the Euro Area, while also sporting lower leverage (Chart 11). Thus, their valuation premium to Euro Area stocks is warranted and their discount to US ones is excessive, especially when rising yields hurt the relative performance of the growth stocks that dominate US indexes. Chart 10Swedish Discounts And Premia

Swedish Discounts And Premia

Swedish Discounts And Premia

Chart 11Profitable Sweden

Profitable Sweden

Profitable Sweden

The outlook for Swedish earnings is appealing, both in absolute and relative terms. The Swedish market’s extreme sensitivity to global economic activity means that Sweden’s EPS increase and beat US profits when the Riksbank Resource Utilization Indicator expands (Chart 12). These relationships are artefacts of the Swedish economy’s pro-cyclicality, which causes capacity utilization to interweave tightly with the global business cycle (Chart 6). Chart 12The Winner Takes It All

The Winner Takes It All

The Winner Takes It All

Chart 13Better Capex Play Than You

Better Capex Play Than You

Better Capex Play Than You

Global capex and infrastructure spending favor Swedish equities compared to Euro Area ones. Over the past thirty years, Sweden’s stocks have outperformed those of the Eurozone when capital goods orders in the advanced economies have expanded (Chart 13). This reflects the Swedish benchmark’s large overweight in industrials, a sector that is the prime beneficiary of global capex. Capital goods orders are recovering well, and their growth rate can climb higher, especially as western multinationals announce capex plans and as governments from the US to Italy intend to ramp up infrastructure spending. Moreover, the large pent-up demand for durable goods in the Eurozone further enhances the potential of industrial firms, and thus, of Swedish equities.4 Chart 14Another Sign Of Pro-Cyclicality

Another Sign Of Pro-Cyclicality

Another Sign Of Pro-Cyclicality

BCA Research’s positive cyclical stance on commodities offers another reason to overweight Sweden’s market relative to that of the US and the Euro Area. Our Commodity and Energy Strategy sister service anticipates significant further upside for natural resources, especially base metals, over the remainder of the business cycle.5 Commodity prices still have room to rally, because demand will grow as the global economy continues to recover and because the supply of natural resources has been constrained by a decade of low investment. As a result, rising metal prices will symptomatize strong economic activity around the world and will incentivize capex in commodity extraction, both of which will boost the revenue of industrial firms. Furthermore, commodity price inflation often corresponds with rising yields, which boosts financials as well. These relationships explain the Swedish stocks’ outperformance of US and Eurozone stocks, when natural resource prices rally, despite the former’s low exposure to materials (Chart 14). At the sector level, the appeal of Swedish industrials relative to those of the Eurozone and the US completes the rationale to favor Swedish equities in a global portfolio. Swedish industrials are just as profitable as US ones and are more so than Euro Area ones, while having significantly lower leverage than either of them (Chart 15). Additionally, for the past two years, the EPS growth of Swedish industrials has bested that of US and Eurozone ones. Yet, their forward P/E ratio trades in line with the US and the Euro Area, while the sell-side’s long-term relative earnings growth estimate is too depressed (Chart 16). The same observations are valid when comparing Swedish industrials to French or German ones. Hence, in the context of a global business cycle upswing, buying Swedish industrials while selling their US and Euro Area competitors is an appealing pair trade, especially since it also involves short USD/SEK and short EUR/SEK bets. Chart 15Attractive Swedish Industrials...

Attractive Swedish Industrials...

Attractive Swedish Industrials...

Chart 16...And Not Expensive

...And Not Expensive

...And Not Expensive

Despite our optimism toward Swedish stocks on a 12 to 24 months basis, investors must hedge a near-term risk. Chinese authorities are aiming to contain financial excesses and trying to restrain credit growth. As we showed four weeks ago, China’s excess reserve ratio is contracting, which points toward a slowdown in the Chinese credit impulse.6 Historically, such a development can hurt global cyclicals, and thus, also Swedish equities. However, BCA Research’s China strategists believe that Beijing will not kill off the Chinese business cycle; thus, the recent disappointment in the Chinese PMI is transitory.7 Chart 17Industrials vs Materials: Europe vs China

Industrials vs Materials: Europe vs China

Industrials vs Materials: Europe vs China

Materials more than industrials will suffer the brunt of a China slowdown, as the re-opening trade and capex cycle among advanced economies will create a buffer for the latter. Indeed, the performance of global industrials relative to materials stocks correlates with the evolution of the spread between the Euro Area and Chinese PMI (Chart 17). Thus, we recommend selling Norwegian equities to hedge the tactical risk inherent in an overweight on Sweden. As Table 1 above shows, Norway overweighs materials and energy (two sectors greatly exposed to China), hence, a temporary pullback in commodity prices should hurt Norwegian stocks more than Swedish ones. Bottom Line: The SEK is an inexpensive and attractive vehicle to bet on both the global business cycle strength and the Swedish economic recovery. Thus, investors should use any rebound in EUR/SEK and USD/SEK to sell these pairs. Moreover, Swedish stocks greatly overweight cyclical sectors, particularly industrials and materials. This sectoral profile renders Swedish equities as attractive bets on the global economy. Additionally, Swedish shares display alluring operating metrics. As a result, we recommend investors go long Swedish industrials relative to those of the US and Euro Area. They should also overweight Swedish equities against the US and the Eurozone. Consequent to some China-related tactical risks, an underweight stance on Norwegian stocks constitutes an attractive hedge to this Swedish exposure. A Few Words On Italy’s National Recovery And Resilience Plan Mario Draghi’s plan to revive the Italian economy, announced last week, is an important marker of Europe’s changing relationship with fiscal policy. Last decade, excessive austerity contributed to subpar growth, ultimately firing up concerns about debt sustainability in many peripheral economies, and fueled risk premia in Italy and Spain. Under the cover of the current crisis, and in the face of the changing political winds in Brussel and Berlin where fiscal rectitude is not the mantra it once was, national European governments are beginning to propose ambitious fiscal stimulus plans. The National Recovery and Resilience program illustrates these dynamics. The EUR248bn plan is a testament to the importance of the NGEU recovery program as well as the REACT EU recovery fund. Through these facilities, the EU will contribute EUR191.5bn to the fiscal plan via grants and loans. Italy will contribute the remainder of the funds. While the total amount disbursed over the next six years corresponds to 14% of Italy’s 2019 GDP, the Draghi government estimates that the program will add 3.2 percentage points to GDP between 2024 and 2026. Importantly, markets are not rebelling. Despite expectations that Italy would continue to run an accommodative fiscal policy, the BTP/Bund spreads remain stable. We can expect this trend of greater stimulus to be mimicked around the EU. Spain is another large recipient of the NGEU program, and it too is likely to increase stimulus beyond what the EU will fund. France will hold an election in May 2022, and President Macron has all the incentives to stimulate the economy between now and then. If, as we wrote last week, Germany shifts to the left in September, then this outcome will be guaranteed. Bottom Line: The Draghi plan is the first salvo of greater fiscal stimulus in the EU. This trend will help Eurozone growth improve relative to the US over the coming few years. Despite a loose fiscal policy, BTPs and other peripheral bonds will continue to outperform on the back of declining risk premia. Mathieu Savary, Chief European Investment Strategist Mathieu@bcaresearch.com Footnotes 1Please see Global Fixed Income Strategy “GFIS Model Bond Portfolio Q1/2021 Performance Review & Current Allocations: Grand Reopening,” dated April 6, 2021, available at gfis.bcaresearch.com 2Please see Foreign Exchange Strategy “2021 Key Views: Tradeable Themes,” dated December 4, 2020, available at fes.bcaresearch.com 3Please see European Investment Strategy “Summer Of ‘21,” dated March 22, 2021, available at eis.bcaresearch.com 4Please see European Investment Strategy “Winds Of Change: Germany Goes Green,” dated April 23, 2021, available at eis.bcaresearch.com 5Please see Commodity & Energy Strategy “Industrial Commodities Super-Cycle Or Bull Market?” dated March 4, 2021, available at ces.bcaresearch.com 6Please see European Investment Strategy “The Euro Dance: One Step Back, Two Steps Forward,” dated March 29, 2021, available at eis.bcaresearch.com 7Please see China Investment Strategy “National People’s Congress Sets Tone For 2021 Growth,” dated March 17, 2021, available at cis.bcaresearch.com Cyclical Recommendations Structural Recommendations Currency Performance

Take A Chance On Sweden

Take A Chance On Sweden

Fixed Income Performance Government Bonds

Take A Chance On Sweden

Take A Chance On Sweden

Corporate Bonds

Take A Chance On Sweden

Take A Chance On Sweden

Equity Performance Major Stock Indices

Take A Chance On Sweden

Take A Chance On Sweden

Geographic Performance

Take A Chance On Sweden

Take A Chance On Sweden

Sector Performance

Take A Chance On Sweden

Take A Chance On Sweden

Closed Trades

Highlights Last week featured a lot of good news for financial markets and the economy … : US GDP grew at 6.4% in the first quarter, powered by 10.7% growth in consumption; the six largest companies in the S&P 500 reported first quarter earnings that exceeded expectations by an average of 41%; and the Fed remained resolutely dovish. … and we continue to believe that they are likely to remain in our “just-right” base-case scenario over the next twelve months … : Our Goldilocks base-case scenario is underpinned by strong growth and accommodative monetary policy. Strong growth is assured as long as the virus doesn’t come roaring back, and the Fed still isn’t even talking about talking about tapering its asset purchases, much less hiking the fed funds rate. … so our risk-friendly asset allocation recommendations remain unchanged: There are no signs yet that equities and credit will not continue to generate significant excess returns over Treasuries and cash over the next twelve months. Feature We will be holding a webcast next Monday, May 10th at 10:00 a.m. Eastern time in lieu of publishing a Weekly Report. Please join us with your questions to make it a fully interactive event. We will resume our regular publication schedule on the 17th. Some say the world will end in fire, Some say in ice. – Robert Frost, “Fire and Ice” We continue to view financial markets and the economy through the lens of our stylized Goldilocks-and-the-Two-Tails distribution (Figure 1). Though the figure gives short shrift to our subjective probability that the Goldilocks base-case scenario will unfold over the next twelve months (≈ 70-75%), and overstates the likelihood of a too-cold outcome (≈ 5-10%), the size of the too-hot right tail (≈ 20-25%) is roughly in line with our expectations. Last week’s spate of economic data, company earnings releases and Fed guidance supported our view and shored up our conviction in it. The twin pillars of well-above-trend growth and extremely accommodative monetary policy remain firmly in place. Figure 1Goldilocks And The Two Tails

Fire, Not Ice

Fire, Not Ice

Last week’s data were especially strong. Sticking to the highlights, and skipping the uncertain impacts of the measures President Biden floated before a joint session of Congress, the following items suggest that the just-right scenario is considerably more probable than not. The Conference Board’s consumer confidence index surged higher (Chart 1, top panel) and given the way it tends to track the jobs plentiful sub-index (Chart 1, bottom panel), the road ahead looks good, provided that job openings rise as businesses still operating at limited capacity ramp up their operations. We have not found that consumer confidence is a robust predictor of key economic series, but the advance supports the notion that several elements are falling into place. Chart 1Consumer Confidence Is Surging ...

Consumer Confidence Is Surging ...

Consumer Confidence Is Surging ...

Initial jobless claims for the week ended April 23rd made their third straight post-pandemic low and the four-week moving average extended its recent descent (Chart 2). The four-week moving average is poised to take another step lower next week once the 742,000 April 2nd reading falls out of the calculation (the last three weeks have averaged 568,000). Headline first-quarter GDP growth of 6.4% was strong, albeit just shy of consensus expectations, but the underlying details were better. Adjusting for the 2.6-percentage-point drag from inventory destocking, which will turn into a boost when inventories are replenished in the future, and backing out the 0.9-percentage-point trade deficit, real final domestic demand surged at an annualized rate of 9.9%. Chart 2... And Layoffs Are Steadily Falling

... And Layoffs Are Steadily Falling

... And Layoffs Are Steadily Falling

On the corporate earnings front, the six largest S&P 500 constituents, Apple, Microsoft, Amazon, Google, Facebook and Tesla, all reported earnings that easily surpassed consensus expectations (Table 1). Those six companies account for 23% of aggregate index market cap and their beats drove projected per-share first-quarter earnings more than 7% higher, from $42.69 to $45.83. Even if the reports were not necessarily greeted by share-price gains, they have the index poised to deliver a fourth consecutive earnings beat of outsized proportions (Chart 3). Although the biggest companies’ successes in the calendar first quarter cannot blindly be extrapolated into the future, they suggest that S&P 500 earnings over the next four quarters will be greater than the market expected before last week. The beat goes on. Table 1Lifting All Boats

Fire, Not Ice

Fire, Not Ice

Chart 3Four Straight Quarters Of Eye-Popping Beats

Fire, Not Ice

Fire, Not Ice

The Fed Maintains Its Poker Face While the FOMC acknowledged that the economy has strengthened since its mid-March meeting, it showed no inclination to accelerate its timetable for dialing back accommodation. Though all four of the tweaks to its mid-March statement amounted to a marginal upgrade of its assessment of the economy’s current state and/or prospects, Chair Powell held fast to his messaging and the committee stayed the course on asset purchases. We continue to take the Fed at its word that it will not hike rates until the economy passes its “three tests” and it will not begin to taper asset purchases until it judges that the economy has made "substantial progress" toward meeting them. The picture has surely improved, but the inflation and employment criteria are not yet within reach. To recap, the Fed’s three preconditions for hiking the fed funds rate are as follows: 12-month PCE inflation must be 2% or higher. Labor market conditions must have reached levels consistent with maximum employment. 12-month PCE inflation must be on track to moderately exceed 2% for some time. Whether or not the economy has made substantial progress toward meeting those criteria is a squishier concept and the Fed has already given itself pre-emptive discretion on the first and most objective criterion by saying it will look through any transitory factors that push measured inflation higher. Powell called out base effects from last year’s pandemic wipeout that will disappear by June. He also cited supply-chain bottlenecks, and while he conceded that it is much harder to predict when they will be resolved, the committee is certain that they will prove to be a temporary phenomenon as well. “Full employment” is also a subjective metric, but the quarterly Summary of Economic Projections, released after every other FOMC meeting, provides a ready proxy. Our US Bond Strategy colleagues have calculated the average monthly net payroll gains required to reach the low end, the midpoint and the high end of the range of the participants’ long-run unemployment rate estimates, which currently span 3.5% to 4.5%, under various labor force participation rate assumptions (Tables 2A, 2B and 2C). We are focused on the top row of each iteration of the table because only a return to the pre-pandemic labor force participation rate of 63.3% would seem to satisfy the Fed’s stated commitment to achieving broad-based employment gains. While a return to the 3.5% pre-pandemic unemployment rate would also be consonant with spreading the gains from the expansion most broadly, it is useful to consider the full range of plausible outcomes given the Fed’s desire to retain some decision-making flexibility. Table 2AAverage Monthly Nonfarm Payroll Growth Required For The Unemployment Rate To Reach 4.5% By The Given Date

Fire, Not Ice

Fire, Not Ice

Table 2BAverage Monthly Nonfarm Payroll Growth Required For The Unemployment Rate To Reach 4% By The Given Date

Fire, Not Ice

Fire, Not Ice

Table 2CAverage Monthly Nonfarm Payroll Growth Required For The Unemployment Rate To Reach 3.5% By The Given Date

Fire, Not Ice

Fire, Not Ice

Per our colleagues’ simple assumptions, it would require an average of anywhere from 701,000 to 833,000 monthly net payroll additions to hit full employment by the end of the year, 534,000 to 631,000 by the middle of 2022, and 410,000 to 487,000 by the end of 2022. The year-end 2021 targets are probably too ambitious, but we think the economy can return to full employment at some point next year, given that labor demand will likely rise sharply upon the release of pent-up consumption demand. As a back-of-the-envelope check on the tables’ conclusions, we take a return to pre-pandemic employment as the goal for a return to full employment. Through March, 8.3 million fewer people were employed than at the pre-pandemic peak in December 20191 (Chart 4). It would take fourteen months (May 2022) to regain full employment at an average monthly pace of 600,000 net hires or seventeen months (August 2022) to achieve that goal at a 500,000-per-month clip. Chart 4More Than 8 Million Workers Still Don't Have A Job

More Than 8 Million Workers Still Don't Have A Job

More Than 8 Million Workers Still Don't Have A Job

A 500,000-to-600,000 range seems doable to us if herd immunity can be achieved before the end of the summer and we expect that the economy will return to full employment somewhere around the middle of next year. That will position the Fed to hike rates for the first time in 2022, in line with the market’s December 2022 lift-off projection, and announce the start of tapering at the end of 2021 or the beginning of 2022. Those Fed views support our recommendations to maintain below-benchmark duration within fixed income portfolios and underweight Treasuries. Press Conference Highlights Jay Powell stayed on message at the post-meeting press conference, resisting every attempt to goad him into revealing more about the tapering timetable or expressing concern about the pickup in inflation and inflation expectations or the economy’s potential to overheat following unprecedentedly large fiscal stimulus. On Tapering Direct questions about tapering bookended the press conference and Powell batted them away directly and concisely. Opening question: Is it time to start talking about talking about tapering yet? A: No, it is not time yet. We’ll give the public plenty of notice when it is. Final question: What are we getting for $120 billion [of Treasury and agency purchases each month] that we couldn’t get for less? A: There will come a time to talk about talking about tapering. That time is not now. On Inflation (And Armchair Quarterbacks) The combination of strong fiscal support and the reversal of a synchronized (and unprecedented) global economic shutdown has the economy beginning to move ahead with potent momentum. The re-opening is likely to produce increases in inflation but we are fully cognizant that they are likely to be temporary. While we are not going to adjust monetary policy unnecessarily in response to temporary inflation pressures, we do not want inflation expectations “materially above” 2% and we will use our tools to bring them down if they were to reach those levels. Our commitment to our price stability mandate is the key difference between now and the late sixties and seventies and we’re well aware of the history of that period. On Transitory Inflation Factors Base effects are going to add about one percentage point to headline and 70 basis points to core inflation in April and May. They will disappear and “carry no implications for the rate of inflation in later periods.” Bottlenecks are a temporary blockage or restriction in the supply chain that slows down the process of delivering a good or bringing it to market. We think of them as things that will naturally be resolved as businesses and individuals adapt. They therefore do not call for a change in monetary policy even if it’s difficult to predict when they will disappear. For the bottlenecks, it’s “a matter of when they will pass through, not whether they will pass through.” What’s happening to prices now is a function of the re-opening of the economy. Demand, spurred by fiscal transfers and people going back to work, has come back much more quickly while the supply side will take a little bit of time to adapt. On Overheating/Bubbles The overall financial stability picture is mixed, but we view it as manageable on balance. There’s some froth in capital markets and strong home price appreciation is not an “unalloyed good,” but the housing market is much more stable than it was before the crisis. Leverage in the financial system is not a problem, the large banks are very well capitalized and don’t have any funding issues and households are in very good shape. Investment Implications Although our conviction levels are lower against a backdrop of unprecedented fiscal stimulus and the inherent uncertainty surrounding a global pandemic, we continue to hold to our view that overheating is unlikely in the near term. The output gap has still not closed and while households have an enormous amount of dry powder in the form of what we estimate to be $2.1 trillion of excess savings, some of 2020’s foregone services demand has been lost forever. The share of foregone demand that has been deferred rather than destroyed will not be released immediately and may well be spread out over a broad range of price points where there is available capacity (think flying business instead of coach, sitting in the best seats at the stadium or the theater, or ordering more expensive bottles of wine). Most importantly on the inflation front, broad wage pressures have not yet emerged. As Chair Powell noted, if the labor market really were tightening, one would expect wages to be rising. We expect that idled workers will return to the labor force as vaccinations proceed, schools reopen and the pandemic becomes less of an impediment to working. We are skeptical that the $300 weekly federal unemployment insurance benefit supplement is having a material effect on labor force participation, but the program will cease in September in any event. Chart 5Neither TIPS Inflation Break-Evens ...

Neither TIPS Inflation Break-Evens ...

Neither TIPS Inflation Break-Evens ...

Chart 6... Nor CPI Swap Inflation Break-Evens Are Sounding The Alarm

... Nor CPI Swap Inflation Break-Evens Are Sounding The Alarm

... Nor CPI Swap Inflation Break-Evens Are Sounding The Alarm

Our biggest inflation concern revolves around long-term inflation expectations. As long as economic actors like workers and businesses do not believe the long-run trajectory of consumer prices has changed, they have no reason to change their behavior to demand wage and price increases to keep pace with an upward inflection in the CPI. The slope of the two-to-five-year and five-to-ten-year segments of the inflation expectations curve remain negative (Charts 5 and 6), suggesting that the inflation mindset necessary to support an upward price spiral has not taken hold. We will not worry about the risk-asset bull market’s fiery demise until the 2-year/5-year and 5-year/10-year break-even slopes start to test the top of their post-GFC range, implying that investors believe a new inflation era has arrived. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 Per the household survey. The monthly employment situation report also includes the establishment survey of employers. We use the household survey here because it is used to calculate the unemployment rate though the establishment survey’s 8.4-million employment shortfall is nearly equivalent to the household survey's.

What Does Our S&P 500 Dividend Discount Model Say?

What Does Our S&P 500 Dividend Discount Model Say?

Since 2017, we have been updating our SPX dividend discount model (DDM) every April when the previous year’s annual S&P 500 dividend payment is finalized from the Standard & Poor’s. Table 1 below summarizes the results of our analysis. Our dividend growth estimates in the DDM result in an SPX 4,047 fair value target. As a reminder, we have been and remain very conservative in our other DDM assumptions. In more detail, we assume that no buybacks will occur, a long-held assumption of ours, i.e. we pencil in a steady divisor in the coming five-year time frame. 2026 is our terminal year when dividend growth settles at 6.6%, 60bps below the long-term average (bottom panel). Our 8.2% discount rate also mirrors the corporate junk bond yield historical average (please click here if you would like to receive our DDM and insert your own assumptions, along with our EPS/multiple sensitivity and ERP analyses that can also be found in the following Strategy Report). Bottom Line: Our DDM corroborates the message that the SPX is fully priced and points to 4,047 as the fair value price.

What Does Our S&P 500 Dividend Discount Model Say?

What Does Our S&P 500 Dividend Discount Model Say?

Weekly Performance Update For the week ending Thu Apr 29, 2021 The Market Monitor displays the trailing 1-quarter performance of strategies based around the BCA Score. For each region, we construct an equal-weighted, monthly rebalanced portfolio consisting of the top 3 stocks per sector and compare it with the regional benchmark. For each portfolio, we show the weekly performance of individual holdings in the Top Contributors/Detractors table. In addition, the Top Prospects table shows the holdings that currently have the highest BCA Score within the portfolio. For more details, click the region headers below to be redirected to the full historical backtest for the strategy. BCA US Portfolio

Market Monitor (Apr 29, 2021)

Market Monitor (Apr 29, 2021)

Total Weekly Return BCA US Portfolio S&P500 TRI 1.69% 1.86% Top Contributors DCP:US WES:US LPX:US MPLX:US SCCO:US Weekly Return 26 bps 24 bps 22 bps 15 bps 13 bps Top Detractors TGNA:US TRTN:US UTHR:US NRG:US NWSA:US Weekly Return -10 bps -9 bps -9 bps -6 bps -4 bps Top Prospects TX:US SCCO:US ESGR:US UHAL:US BRK.A:US BCA Score 99.58% 97.15% 97.12% 95.81% 94.73% BCA Canada Portfolio

Market Monitor (Apr 29, 2021)

Market Monitor (Apr 29, 2021)

Total Weekly Return BCA Canada Portfolio S&P/TSX TRI 0.83% 1.19% Top Contributors TOU:CA APHA:CA PXT:CA LIF:CA TOY:CA Weekly Return 38 bps 25 bps 24 bps 16 bps 13 bps Top Detractors QBR.A:CA AUP:CA H:CA L:CA EMP.A:CA Weekly Return -22 bps -18 bps -12 bps -9 bps -8 bps Top Prospects CFP:CA IFP:CA LNF:CA NWC:CA RUS:CA BCA Score 99.22% 98.92% 98.69% 92.61% 88.52% BCA UK Portfolio

Market Monitor (Apr 29, 2021)

Market Monitor (Apr 29, 2021)

Total Weekly Return BCA UK Portfolio FTSE 100 TRI 0.61% 0.38% Top Contributors TUNE:GB HSBK:GB DGOC:GB FXPO:GB CNE:GB Weekly Return 36 bps 33 bps 21 bps 15 bps 12 bps Top Detractors AO.:GB SSE:GB SVST:GB LSRG:GB DRX:GB Weekly Return -14 bps -11 bps -9 bps -8 bps -8 bps Top Prospects SVST:GB NLMK:GB TUNE:GB BPCR:GB GLTR:GB BCA Score 99.79% 99.27% 98.05% 97.39% 96.74% BCA Eurozone Portfolio

Market Monitor (Apr 29, 2021)

Market Monitor (Apr 29, 2021)

Total Weekly Return BCA EMU Portfolio MSCI EMU TRI 0.48% 0.01% Top Contributors AOF:DE IPS:FR SOLV:BE EVN:AT PHH2:DE Weekly Return 24 bps 16 bps 9 bps 8 bps 7 bps Top Detractors CNV:FR VIS:ES VIRP:FR MOL:IT TEN:IT Weekly Return -20 bps -12 bps -9 bps -9 bps -7 bps Top Prospects CNV:FR PHH2:DE SOL:IT SOLV:BE ROTH:FR BCA Score 99.51% 99.12% 98.75% 97.97% 96.58% BCA Japan Portfolio

Market Monitor (Apr 29, 2021)

Market Monitor (Apr 29, 2021)

Total Weekly Return BCA Japan Portfolio TOPIX TRI -1.08% -0.70% Top Contributors 8595:JP 4980:JP 8966:JP 6960:JP 9503:JP Weekly Return 17 bps 14 bps 11 bps 10 bps 9 bps Top Detractors 8255:JP 4534:JP 5451:JP 5943:JP 1766:JP Weekly Return -20 bps -17 bps -17 bps -16 bps -13 bps Top Prospects 1766:JP 9436:JP 4008:JP 8595:JP 8133:JP BCA Score 99.43% 99.07% 98.55% 98.00% 97.78% BCA Hong Kong Portfolio

Image

Total Weekly Return BCA Hong Kong Portfolio Hang Seng TRI 1.14% 1.91% Top Contributors 1888:HK 148:HK 1898:HK 867:HK 373:HK Weekly Return 33 bps 25 bps 24 bps 15 bps 14 bps Top Detractors 990:HK 1117:HK 315:HK 1883:HK 719:HK Weekly Return -14 bps -11 bps -8 bps -6 bps -5 bps Top Prospects 990:HK 2232:HK 811:HK 3306:HK 86:HK BCA Score 99.91% 98.78% 97.55% 97.11% 96.98% BCA Australia Portfolio

Market Monitor (Apr 29, 2021)

Market Monitor (Apr 29, 2021)

Total Weekly Return BCA Australia Portfolio S&P/ASX All Ord. TRI -0.14% 0.47% Top Contributors STX:AU 360:AU SGF:AU PDN:AU CAJ:AU Weekly Return 40 bps 34 bps 19 bps 16 bps 9 bps Top Detractors API:AU HVN:AU ADH:AU HT1:AU DDR:AU Weekly Return -34 bps -26 bps -22 bps -16 bps -16 bps Top Prospects BSE:AU GRR:AU PSQ:AU BLX:AU BFG:AU BCA Score 99.83% 99.32% 98.75% 97.77% 96.89%

Highlights Biden’s first 100 days are characterized by a liberal spend-and-tax agenda unseen since the 1960s. It is not a “bait and switch,” however. Voters do not care about deficits and debt. At least not for now. The apparent outcome of the populist surge in the US and UK in 2016 is blowout fiscal spending. Yet the US and UK also invented and distributed vaccines faster than others. US growth and equities have outperformed while the US dollar experienced a countertrend bounce. While growth will rotate to other regions, China’s stimulus is on the wane. Of Biden’s three initial geopolitical risks, two are showing signs of subsiding: Russia and Iran. US-China tensions persist, however, and Biden has been hawkish so far. Our new Australia Geopolitical Risk Indicator confirms our other indicators in signaling that China risk, writ large, remains elevated. Cyclically we are optimistic about the Aussie and Australian stocks. Mexico’s midterm elections are likely to curb the ruling party’s majority but only marginally. The macro and geopolitical backdrop is favorable for Mexico. Feature US President Joe Biden gave his first address to the US Congress on April 28. Biden’s first hundred days are significant for his extravagant spending proposals, which will rank alongside those of Lyndon B. Johnson’s Great Society, if not Franklin Delano Roosevelt’s New Deal, in their impact on US history, for better and worse. Chart 1Biden's First 100 Days - The Market's Appraisal

Biden's First 100 Days - The Market's Appraisal

Biden's First 100 Days - The Market's Appraisal

The global financial market appraisal is that Biden’s proposals will turn out for the better. The market has responded to the US’s stimulus overshoot, successful vaccine rollout, and growth outperformance – notably in the pandemic-struck service sector – by bidding up US equities and the dollar (Chart 1). From a macro perspective we share the BCA House View in leaning against both of these trends, preferring international equities and commodity currencies. However, our geopolitical method has made it difficult for us to bet directly against the dollar and US equities. Geopolitics is about not only wars and trade but also the interaction of different countries’ domestic politics. America’s populist spending blowout is occurring alongside a sharp drop in China’s combined credit-and-fiscal impulse, which will eventually weigh on the global economy. This is true even though the rest of the world is beginning to catch up in vaccinations and economic normalization. As for traditional geopolitical risk – wars and alliances – Biden has not yet leaped over the three initial foreign policy hurdles that we have highlighted: China, Russia, and Iran. In this report we will update the view on all three, as there is tentative improvement on the Russian and Iranian fronts. In addition, we will introduce our newest geopolitical risk indicator – for Australia – and update our view on Mexico ahead of its June 6 midterm elections. Biden’s Fiscal Blowout From a macro point of view, Biden’s $1.9 trillion American Rescue Plan Act (ARPA) was much larger than what Republicans would have passed if President Trump had won a second term. His proposed $2.3 trillion American Jobs Plan (AJP) is also larger, though both candidates were likely to pass an infrastructure package. The difference lies in the parts of these packages that relate to social spending and other programs, beyond COVID relief and roads and bridges. The Republican proposal for COVID relief was $618 billion while the Republicans’ current proposal on infrastructure is $568 billion – marking a $3 trillion difference from Biden. In reality Republicans would have proposed larger spending if Trump had remained president – but not enough to close this gap. And Biden is also proposing a $1.8 trillion American Families Plan (AFP). Biden’s praise for handling the vaccinations must be qualified by the Trump administration’s successful preparations, which have been unfairly denigrated. Similarly, Biden’s blame for the migrant surge at the southern border must be qualified by the fact that the surge began last year.1 A comparison with the UK will put Biden’s administration into perspective. The only country comparable to the US in terms of the size of fiscal stimulus over 2019-21 so far – excluding Biden’s AJP and AFP, which are not yet law – is the United Kingdom. Thus the consequence of the flare-up of populism in the Anglo-Saxon world since 2016 is a budget deficit blowout as these countries strive to suppress domestic socio-political conflict by means of government largesse, particularly in industrial and social programs. However, populist dysfunction was also overrated. Both the US and UK retain their advantages in terms of innovation and dynamism, as revealed by the vaccine and its rollout (Chart 2). Chart 2Dysfunctional Anglo-Saxon Populism?

Dysfunctional Anglo-Saxon Populism?

Dysfunctional Anglo-Saxon Populism?

No sharp leftward turn occurred in the UK, where Prime Minister Boris Johnson and his Conservatives had the benefit of a pre-COVID election in December 2019, which they won. By contrast, in the US, President Trump and the Republicans contended an election after the pandemic and recession had virtually doomed them to failure. There a sharp leftward turn is taking place. Going forward the US will reclaim the top rank in terms of fiscal stimulus, as Biden is likely to get his infrastructure plan (AJP) passed. Our updated US budget deficit projections appear in Chart 3. Our sister US Political Strategy gives the AJP an 80% chance of passing in some form and the AFP only a 50% chance of passing, depending on how quickly the AJP is passed. This means the blue dashed line is more likely to occur than the red dashed line. The difference is slight despite the mind-boggling headline numbers of the plans because the spending is spread out over eight-to-ten years and tax hikes over 15 years will partially offset the expenditures. Much will depend on whether Congress is willing to pay for the new spending. In Chart 3 we assume that Biden will get half of the proposed corporate tax hikes in the AJP scenario (and half of the individual tax hikes in the AFP scenario). If spending is watered down, and/or tax hikes surprise to the upside, both of which are possible, then the deficit scenarios will obviously tighten, assuming the economic recovery continues robustly as expected. But in the current political environment it is safest to plan for the most expansive budget deficit scenarios, as populism is the overriding force. Chart 3Biden’s Blowout Spending

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s campaign plan was even more visionary, so it is not true that Biden pulled a “bait and switch” on voters. Rather, the median voter is comfortable with greater deficits and a larger government role in American life. Bottom Line: The implication of Biden’s spending blowout is reflationary for the global economy, cyclically negative for the US dollar, and positive for global equities. But on a tactical time frame the rotation to other equities and currencies will also depend on China’s fiscal-and-credit deceleration and whether geopolitical risk continues to fall. Russia: Some Improvement But Coast Not Yet Clear US-Russia tensions appeared to fizzle over the past week but the coast is not yet clear. We remain short Russian currency and risk assets as well as European emerging market equities. Tensions fell after President Putin’s State of the Nation address on April 21 in which he warned the West against crossing Russia’s “red lines.” Biden’s sanctions on Russia were underwhelming – he did not insist on halting the final stages of the Nord Stream II pipeline to Germany. Russia declared it would withdraw its roughly 100,000 troops from the Ukrainian border by May 1. Russian dissident Alexei Navalny ended his hunger strike. Putin attended Biden’s Earth Day summit and the two are working on a bilateral summit in June. Chart 4Russia's Domestic Instability Will Continue

Russia's Domestic Instability Will Continue

Russia's Domestic Instability Will Continue

De-escalation is not certain, however. First, some US officials have cast doubt on Russia’s withdrawal of troops and it is known that arms and equipment were left in place for a rapid mobilization and re-escalation if necessary. Second, Russian-backed Ukrainian separatists will be emboldened, which could increase fighting in Ukraine that could eventually provoke Russian intervention. Third, the US has until August or September to prevent Nord Stream from completion. Diplomacy between Russia and the US (and Russia and several eastern European states) has hit a low point on the withdrawal of ambassadors. Fourth, Russian domestic politics was always the chief reason to prepare for a worse geopolitical confrontation and it remains unsettled. Putin’s approval rating still lingers in the relatively low range of 65% and government approval at 49%. The economic recovery is weak and facing an increasingly negative fiscal thrust, along with Europe and China, Russia’s single-largest export destination (Chart 4). Putin’s handouts to households, in anticipation of the September Duma election, only amount to 0.2% of GDP. More measures will probably be announced but the lead-up to the election could still see an international adventure designed to distract the public from its socioeconomic woes. Russia’s geopolitical risk indicators ticked up as anticipated (Chart 5). They may subside if the military drawdown is confirmed and Biden and Putin lower the temperature. But we would not bet on it. Chart 5Russian Geopolitical Risk: Wait For 'All Clear' Signal

Russian Geopolitical Risk: Wait For 'All Clear' Signal

Russian Geopolitical Risk: Wait For 'All Clear' Signal

Bottom Line: It is possible that Biden has passed his first foreign policy test with Russia but it is too soon to sound the “all clear.” We remain short Russian ruble and short EM Europe until de-escalation is confirmed. The Russian (and German) elections in September will mark a time for reassessing this view. Iran: Diplomacy On Track (Hence Jitters Will Rise) While Russia may or may not truly de-escalate tensions in Ukraine, the spring and summer are sure to see an increase in focus on US-Iran nuclear negotiations. Geopolitical risks will remain high prior to the conclusion of a deal and will materialize in kinetic attacks of various kinds. This thesis is confirmed by the alleged Israeli sabotage of Iran’s Natanz nuclear facility this month. The US Navy also fired warning shots at Iranian vessels staging provocations. Sporadic attacks in other parts of the region also continue to flare, most recently with an Iranian tanker getting hit by a drone at a Syrian oil terminal.2 The US and Iran are making progress in the Vienna talks toward rejoining the 2015 nuclear deal from which the US withdrew in 2018. Iran pledged to enrich uranium up to 60% but also said this move was reversible – like all its tentative violations of the Joint Comprehensive Plan of Action (JCPA) so far (Table 1). Iran also offered a prisoner swap with the US. Saudi Arabia appears resigned to a resumption of the JCPA that it cannot prevent, with crown prince Mohammed bin Salman offering diplomatic overtures to both the US and Iran. Table 1Iran’s Nuclear Program And Compliance With JCPA 2015

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Still, the closer the US and Iran get to a deal the more its opponents will need to either take action or make preparations for the aftermath. The allegation that former US Secretary of State John Kerry’s shared Israeli military plans with Iranian Foreign Minister Javad Zarif is an example of the kind of political brouhaha that will occur as different elements try to support and oppose the normalization of US-Iran ties. More importantly Israel will underscore its red line against nuclear weaponization. Previously Iran was set to reach “breakout” capability of uranium enrichment – a point at which it has enough fissile material to produce a nuclear device – as early as May. Due to sabotage at the Natanz facility the breakout period may have been pushed back to July.3 This compounds the significance of this summer as a deadline for negotiating a reduction in tensions. While the US may be prepared to fudge on Iran’s breakout capabilities, Israel will not, which means a market-relevant showdown should occur this summer before Israel backs down for fear of alienating the United States. Tit-for-tat attacks in May and June could cause negative surprises for oil supply. Then there will be a mad dash by the negotiators to agree to deal before the de facto August deadline, when Iran inaugurates a new president and it becomes much harder to resolve outstanding issues. Chart 6Iran Deal Priced Into Oil Markets?

Iran Deal Priced Into Oil Markets?

Iran Deal Priced Into Oil Markets?

Hence our argument that geopolitics adds upside risk to oil prices in the first half of the year but downside risk in the second half. The market’s expectations seem already to account for this, based on the forward curve for Brent crude oil. The marginal impact of a reconstituted Iran nuclear deal on oil prices is slightly negative over the long run since a deal is more likely to be concluded than not and will open up Iran’s economy and oil exports to the world. However, our Commodity & Energy Strategy expects the Brent price to exceed expectations in the coming years, judging by supply and demand balances and global macro fundamentals (Chart 6). If an Iran deal becomes a fait accompli in July and August the Saudis could abandon their commitment to OPEC 2.0’s production discipline. The Russians and Saudis are not eager to return to a market share war after what happened in March 2020 but we cannot rule it out in the face of Iranian production. Thus we expect oil to be volatile. Oil producers also face the threat of green energy and US shale production which gives them more than one reason to keep up production and prevent prices from getting too lofty. Throughout the post-2015 geopolitical saga between the US and Iran, major incidents have caused an increase in the oil-to-gold ratio. The risk of oil supply disruption affected the price more than the flight to gold due to geopolitical or war risk. The trend generally corresponds with that of the copper-to-gold ratio, though copper-to-gold rose higher when growth boomed and oil outperformed when US-Iran tensions spiked in 2019. Today the copper-to-gold ratio is vastly outperforming the oil-to-gold on the back of the global recovery (Chart 7). This makes sense from the point of view of the likelihood of a US-Iran deal this year. But tensions prior to a deal will push up oil-to-gold in the near term. Chart 7Biden Passes Iran Test? Likely But Not A Done Deal

Biden Passes Iran Test? Likely But Not A Done Deal

Biden Passes Iran Test? Likely But Not A Done Deal

Bottom Line: The US-Iran diplomacy is on track. This means geopolitical risk will escalate in May and June before a short-term or interim deal is agreed in July or August. Geopolitical risk stemming from US-Iran relations will subside thereafter, unless the deadline is missed. The forward curve has largely priced in the oil price downside except for the risk that OPEC 2.0 becomes dysfunctional again. We expect upside price surprises in the near term. Biden, China, And Our Australia GeoRisk Indicator Ostensibly the US and Russia are avoiding a war over Ukraine and the US and Iran are negotiating a return to the 2015 nuclear deal. Only US-China relations utterly lack clarity, with military maneuvering in the Taiwan Strait and South China Sea and tensions simmering over the gamut of other disputes. Chart 8Biden Still Faces China Test

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

The latest data on global military spending show not only that the US and China continue to build up their militaries but also that all of the regional allies – including Japan! – are bulking up defense spending (Chart 8). This is a substantial confirmation of the secular growth of geopolitical risk, specifically in reaction to China’s rise and US-China competition. The first round of US-China talks under Biden went awry but since then a basis has been laid for cooperation on climate change, with President Xi Jinping attending Biden’s virtual climate change summit (albeit with no bilateral summit between the two). If John Kerry is removed as climate czar over his Iranian controversy it will not have an impact other than to undermine American negotiators’ reliability. The deeper point is that climate is a narrow basis for US-China cooperation and it cannot remotely salvage the relationship if a broader strategic de-escalation is not agreed. Carbon emissions are more likely to become a cudgel with which the US and West pressure China to reform its economy faster. The Department of Defense is not slated to finish its comprehensive review of China policy until June but most US government departments are undertaking their own reviews and some of the conclusions will trickle out in May, whether through Washington’s actions or leaks to the press. Beijing could also take actions that upend the Biden administration’s assessment, such as with the Microsoft hack exposed earlier this year. The Biden administration will soon reveal more about how it intends to handle export controls and sanctions on China. For example, by May 19 the administration is slated to release a licensing process for companies concerned about US export controls on tech trade with China due to the Commerce Department’s interim rule on info tech supply chains. The Biden administration looks to be generally hawkish on China, a view that is now consensus. Any loosening of punitive measures would be a positive surprise for Chinese stocks and financial markets in general. There are other indications that China’s relationship with the West is not about to improve substantially – namely Australia. Australia has become a bellwether of China’s relations with the world. While the US’s defense commitments might be questionable with regard to some of China’s neighbors – namely Taiwan (Province of China) but also possibly South Korea and the Philippines – there can be little doubt that Australia, like Japan, is the US’s red line in the Pacific. Australian politics have been roiled over the past several years by the revelation of Chinese influence operations, state- or military-linked investments in Australia, and propaganda campaigns. A trade war erupted last year when Australia called for an investigation into the origins of COVID-19 and China’s handling of it. Most recently, Victoria state severed ties with China’s Belt and Road Initiative. Despite the rise in Sino-Australian tensions, the economic relationship remains intact. China’s stimulus overweighed the impact of its punitive trade measures against Australia, both by bidding up commodity prices and keeping the bulk of Australia’s exports flowing (Chart 9). As much as China might wish to decouple from Australia, it cannot do so as long as it needs to maintain minimum growth rates for the sake of social stability and these growth rates require resources that Australia provides. For example, global iron ore production excluding Australia only makes up 80% of China’s total iron ore imports, which necessitates an ongoing dependency here (Chart 10). Brazil cannot make up the difference. Chart 9China-Australia Trade Amid Tensions

China-Australia Trade Amid Tensions

China-Australia Trade Amid Tensions

Chart 10China Cannot Replace Australia

China Cannot Replace Australia

China Cannot Replace Australia

This resource dependency does not necessarily reduce geopolitical tension, however, because it increases China’s supply insecurity and vulnerability to the US alliance. The US under Biden explicitly aims to restore its alliances and confront autocratic regimes. This puts Australia at the front lines of an open-ended global conflict. Chart 11Introducing: Australia GeoRisk Indicator (Smoothed)

Introducing: Australia GeoRisk Indicator (Smoothed)

Introducing: Australia GeoRisk Indicator (Smoothed)

Our newly devised Australia GeoRisk Indicator illustrates the point well, as it has continued surging since the trade war with China first broke out last year (Chart 11). This indicator is based on the Australian dollar and its deviation from underlying macro variables that should determine its course. These variables are described in Appendix 1. If the Aussie weakens relative to these variables, then an Australian-specific risk premium is apparent. We ascribe that premium to politics and geopolitics writ large. A close examination of the risk indicator’s performance shows that it tracks well with Australia’s recent political history (Chart 12). Previous peaks in risk occurred when President Trump rose to power and Australia, like Canada, found itself beset by negative pressures from both the US and China. In particular, Trump threatened tariffs and the Australian government banned China’s Huawei from its 5G network. Today the rise in geopolitical risk stems almost exclusively from China. There is potential for it to roll over if Biden negotiates a reduction in tensions but that is a risk to our view (an upside risk for Australian and global equities). Chart 12Australian GeoRisk Indicator (Unsmoothed)

Australian GeoRisk Indicator (Unsmoothed)

Australian GeoRisk Indicator (Unsmoothed)

What does this indicator portend for tradable Australian assets? As one would expect, Australian geopolitical risk moves inversely to the country’s equities, currency, and relative equity performance (Chart 13). Australian equities have risen on the back of global growth and the commodity boom despite the rise in geopolitical risk. But any further spike in risk could jeopardize this uptrend. Chart 13Australia Geopolitical Risk And Tradable Assets

Australia Geopolitical Risk And Tradable Assets

Australia Geopolitical Risk And Tradable Assets

An even clearer inverse relationship emerges with the AUD-JPY exchange rate, a standard measure of risk-on / risk-off sentiment in itself. If geopolitical risk rises any further it should cause a reversal in the currency pair. Finally, Australian equities have not outperformed other developed markets excluding the US, which may be due to this elevated risk premium. Bottom Line: China is the most important of Biden’s foreign policy hurdles and unlike Russia and Iran there is no sign of a reduction in tension yet. Our Australian GeoRisk Indicator supports the point that risk remains very elevated in the near term. Moreover China’s credit deceleration is also negative for Australia. Cyclically, however, assuming that China does not overtighten policy, we take a constructive view on the Aussie and Australian equities. Biden’s Border Troubles Distract From Bullish Mexico Story The biggest criticism of Biden’s first 100 days has been his reduction in a range of enforcement measures on the southern border which has encouraged an overflow of immigrants. Customs and Border Patrol have seen a spike in “encounters” from a low point of around 17,000 in 2020 to about 170,000 today. The trend started last year but accelerated sharply after the election and had surpassed the 2019 peak of 144,000. Vice President Kamala Harris has been put in charge of managing the border crisis, both with Mexico and Central American states. She does not have much experience with foreign policy so this is her opportunity to learn on the job. She will not be able to accomplish much given that the Biden administration is unwilling to use punitive measures or deterrence and will not have large fiscal resources available for subsidizing the nations to the south. With the US economy hyper-charged, especially relative to its southern neighbors, the pace of immigration is unlikely to slacken. From a macro point of view the relevance is that the US is not substantially curtailing immigration – quite the opposite – which means that labor force growth will not deviate from its trend. What about Mexico itself? It is not likely that Harris will be able to engage on a broader range of issues with Mexico beyond immigration. As usual Mexico is beset with corruption, lawlessness, and instability. To these can be added the difficulties of the pandemic and vaccine rollout. Tourism and remittances are yet to recover. Cooperation with US federal agents against the drug cartels is deteriorating. Cartels control an estimated 40% of Mexican territory.4 Nevertheless, despite Mexico’s perennial problems, we hold a positive view on Mexican currency and risk assets. The argument rests on five points: Strong macro fundamentals: With China’s fiscal-and-credit impulse slowing sharply, and US stimulus accelerating, Mexico stands to benefit. Mexico has also run orthodox monetary and fiscal policies. It has a demographic tailwind, low wages, and low public debt. The stars are beginning to align for the country’s economy, according to our Emerging Markets Strategy. US and Canadian stimulus: The US and Canada have the second- and third-largest fiscal stimulus of all the major countries over the 2019-21 period, at 9% and 8% of GDP respectively. Mexico, with the new USMCA free trade deal in hand, will benefit. US protectionism fizzled: Even Republican senators blocked President Trump’s attempted tariffs on Mexico. Trump’s aggression resulted in the USMCA, a revised NAFTA, which both US political parties endorsed. Mexico is inured to US protectionism, at least for the short and medium term. Diversification from China: Mexico suffered the greatest opportunity cost from China’s rise as an offshore manufacturer and entrance to the World Trade Organization. Now that the US and other western countries are diversifying away from China, amid geopolitical tensions, Mexico stands to benefit. The US cannot eliminate its trade deficit due to its internal savings/investment imbalance but it can redistribute that trade deficit to countries that cannot compete with it for global hegemony. AMLO faces constraints: A risk factor stemmed from politics where a sweeping left-wing victory in 2018 threatened to introduce anti-market policies. President Andrés Manuel López Obrador (known as AMLO) and his MORENA party gained a majority in both houses of the legislature. Their coalition has a two-thirds majority in the lower house (Chart 14). However, we pointed out that AMLO’s policies have not been radical and, more importantly, that the midterm election would likely constrain his power. Chart 14Mexico’s Midterm Election Looms

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

These are all solid points but the last item faces a test in the upcoming midterm election. AMLO’s approval rating is strong, at 63%, putting him above all of his predecessors except one (Chart 15). AMLO’s approval has if anything benefited from the COVID-19 crisis despite Mexico’s inability to handle the medical challenge. He has promised to hold a referendum on his leadership in early 2022, more than halfway through his six-year term, and he is currently in good shape for that referendum. For now his popularity is helpful for his party, although he is not on the ballot in 2021 and MORENA’s support is well beneath his own. Chart 15AMLO’s Approval Fairly Strong

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

MORENA’s support is holding at a 44% rate of popular support and its momentum has slightly improved since the pandemic began. However, MORENA’s lead over other parties is not nearly as strong as it was back in 2018 (Chart 16, top panel). The combined support of the two dominant center-right parties, the Institutional Revolutionary Party and the National Action Party, is almost equal to that of MORENA. And the two center-left parties, the Democratic Revolution Party and Citizen’s Movement, are part of the opposition coalition (Chart 16, bottom panel). The pandemic and economic crisis will motivate the opposition. Chart 16MORENA’s Support Holding Up Despite COVID

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Traditionally the president’s party loses seats in the midterm election (Table 2). Circumstances are different from the US, which also exhibits this trend, because Mexico has more political parties. A loss of seats from MORENA does not necessarily favor the establishment parties. Nevertheless opinion polling shows that about 45% of voters say they would rather see MORENA’s power “checked” compared to 41% who wish to see the party go on unopposed.5 Table 2Mexican President’s Party Tends To Lose Seats In Midterm Election

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)