Equities

Highlights Fiscal stimulus props up output when it’s injected into an economy, but is a consumption hangover just around the corner?: Fiscal drag is a very real phenomenon but we don’t think US investors have to worry about a consumption drag any time soon, given that consumption has yet to see a bounce. Is the housing market’s boom vulnerable to reversing?: Powered by an outward shift in the demand curve for single-family homes in the suburbs and beyond and helped along by a chronic supply deficit, it appears that the housing boom has at least another year or two to run. Is the Archegos implosion a sign of broader weaknesses?: Based on what we know now, we do not believe that one levered investor’s reported demise is a symptom of systemic problems in financial markets or the banking system. Feature BCA’s monthly editorial view meeting, held last week, underlined the unusual level of uncertainty confronting investors. Against a backdrop of enormous domestic fiscal stimulus and global monetary accommodation, an entire generation of market participants is ruminating about inflation for the very first time. The course of the pandemic remains a significant unknown; while the US has seemingly lined up all the vaccine doses it will need and has begun to hit its vaccination stride, infections are rising and Europe and Canada are still mired in shutdowns. It has been easy to tally up the excess pandemic savings as they’ve accumulated into what we expect will be a $2 trillion mass, but we can only guess how much of the hoard will be spent and when. It is unclear what elements of the infrastructure spending vision laid out by President Biden last week will make it through a Congress deeply riven by partisan conflict and fissures within the Democratic caucus and the fate of its associated tax hike proposals is therefore uncertain. Against this backdrop of unknowns, we highlight the questions that have come up the most in our recent discussions with clients. We continue to have a constructive view on risk assets and the economy but the situation is fluid and we will take our cue from the evidence as it emerges. A Stimulus Hangover? Q: I get that fiscal stimulus will produce a big GDP pop this year, but what happens after it’s gone? Is the US heading for a consumption/income hangover in 2022? It’s true that the US cannot keep pumping out transfer payments to households at its 2020 and 2021 rate. It’s also true, however, that fewer and fewer households are in need of them. Employee compensation surpassed its February 2020 pre-pandemic peak in both January and February (Chart 1) and it should continue to rise as more and more people go back to work. Conversely, unemployment assistance should naturally dwindle as vaccinations allow the private sector to take the baton from the federal government. Chart 1Aggregate Compensation Is Making New Highs

Aggregate Compensation Is Making New Highs

Aggregate Compensation Is Making New Highs

Chart 2The Big Surge Has Yet To Come

The Big Surge Has Yet To Come

The Big Surge Has Yet To Come

The end of the economic impact payments ($1,400 to adults earning $75,000 or less in the current round, following $1,200 and $600 rounds last spring and this January) will represent something of a fiscal cliff for vulnerable households. They have a high marginal propensity to consume and presumably have been depending on the transfers, as evidenced by the revised 7.6% month-over-month spike in January retail sales upon the distribution of the $600 round and its subsequent 3% decline in February (Chart 2). As people return to work, however, the number of vulnerable households should shrink. We nonetheless do not fear a near-term consumption hangover for the simple reason that there was no consumption sugar rush in 2020. Consumption growth has badly lagged increases in household net worth as the multitude of households who didn’t really need the economic impact payments used them to pad their savings, pay down debt or buy stocks. Once the $1,400 checks are fully disbursed, we estimate that excess household savings will top $2 trillion. Much of those excess pandemic savings have accumulated because households were unable to spend on things like restaurant meals, travel, movies, concerts and sporting events. We are confident that they will spend again once they recover their full menu of options, but much of the forgone services spending will simply be lost. Some of the unintended pandemic savings will remain savings and the consumption tailwind driven by pent-up demand will eventually dissipate. When that happens, consumption may indeed hit a bit of a wall and economic growth will likely decelerate. The key for our twelve-month market outlook is that the unfettered release of pent-up demand cannot begin until households recover their full range of consumption options. They won’t do so until the economy fully reopens, which means the inevitable slowdown clock has not yet begun to tick. One can’t be hungover without first getting drunk and the longer it takes for the consumption surge to arrive, the longer the slowdown will be delayed. In our most likely scenario, the hangover won’t arrive until 2023, beyond the time horizon of most institutional investors. How Vulnerable Is The Housing Market? Q: The US housing market has experienced a remarkable recovery. Is the real estate boom sustainable or is it vulnerable to a sudden reversal? We believe the real estate boom can be sustained over the next year and beyond. It is supported by strong demand, affordable financing and tight supplies. Against a backdrop of extended supply shortfalls, there is scope for prices to continue to rise even as new construction activity accelerates (Chart 3). Residential investment accounts for a modest amount of economic activity but housing is nonetheless likely to remain in a sweet spot in which rising prices boost household wealth at the margin and increasing activity boosts employment and income. Chart 3Falling Supply, Rising Prices

Falling Supply, Rising Prices

Falling Supply, Rising Prices

Chart 4A Seller's Market

A Seller's Market

A Seller's Market

The pandemic has acted to stoke demand for suburban single-family homes and it appears as if at least some of the migration from urban centers to suburban and exurban/rural communities will outlast the pandemic. Several businesses have already moved to lower their real estate expenses by shrinking their office footprints in high-cost central business districts (CBD). Working from home will be an option for many professionals going forward and a lot of them may choose to trade high-cost-per-square-foot city apartments for much cheaper space in the suburbs and beyond now that they are no longer tethered to their CBD offices five days a week. In addition to the work-from-home catalyst, the flow from cities may be persistent if urban living becomes less attractive in a post-pandemic world that features fewer bars and restaurants and lingering wariness about close interactions with crowds. The supply of houses is historically low when adjusted for the total number of US households (Chart 4) and the tight conditions are only partly related to the pandemic. The first pandemic feature is an unwillingness to have (potentially infected) prospective buyers trooping through one’s house to examine it. The second is an aversion among older people to sell their homes and move to the senior-living facilities that incubated infections in the pandemic’s initial waves. Both of these factors are temporary and should ease quickly once widespread immunization stifles COVID’s spread. The longer-run supply factor is restrictive zoning laws that make it difficult to construct new homes. This is an intractable issue in many if not most of the more desirable locations across the country and it will not be solved quickly or easily (Chart 5). Demand was poised to exceed supply in many of the nation’s housing markets even before work from home unshackled skilled professionals from their offices. That dynamic should help keep prices firm while supporting residential investment and construction employment. Chart 5New Home Construction Has Lagged Since The GFC

New Home Construction Has Lagged Since The GFC

New Home Construction Has Lagged Since The GFC

Chart 6Homes Are Still Affordable

Homes Are Still Affordable

Homes Are Still Affordable

Finally, houses remain quite affordable (Chart 6, top panel). Despite a backup of 40-50 basis points from the 2.8% bottom, the rates on 30-year fixed-rate mortgages are still extremely low relative to history (Chart 6, third panel). Buying is an appealing alternative to renting despite the rise in home prices over the last year (Chart 6, bottom panel). The rate of price appreciation is likely to slow once the pandemic supply impediments fade, but US home construction has not kept pace with long-run household formation growth and we expect the housing market will remain robust for at least the next year or two. Have Termites Gotten Into The Beams? Q: Retail investors nearly brought down a hedge fund with a large short position in GameStop (GME). Now a family office that looked a lot like a hedge fund has blown up after its prime brokers allowed it to amplify long equity exposures with ridiculous amounts of leverage. We all know there’s never just one cockroach. Do you think there’s a deeper rot in this market after 12 years of gains disconnected from the fundamentals? The details of the reported fire sales of margin collateral that may have wiped out the multi-billion-dollar Archegos portfolio have not been made public. No one but the parties involved have definitive knowledge of what occurred but it’s always worth thinking about what could go wrong, especially twelve years into a bull market. We can state with full confidence, however, that the S&P 500’s extended run has not been disconnected from the fundamentals. Chart 7Earnings Growth Has Outpaced Multiple Expansion

Earnings Growth Has Outpaced Multiple Expansion

Earnings Growth Has Outpaced Multiple Expansion

Treating the pandemic sell-off as a vicious correction instead of a full-fledged bear market that ushered in a brand-new bull market, the current bull market began in March 2009 and has lasted for twelve years and one month (Chart 7, top panel). When it began, four-quarter forward consensus earnings estimates for the S&P 500 were $65. As of March 26th, forward four-quarter earnings were $180. Over the duration of the bull market, S&P 500 earnings estimates have nearly tripled, growing at an 8.75% annualized rate (Chart 7, middle panel). The index’s forward multiple has nearly doubled, from 11.25 to 21.5, rising at a 5.5% annualized rate (Chart 7, bottom panel). Earnings growth has accounted for the majority (about 61%) of the index’s 14.75% annualized gain. Through last January, ahead of the pandemic, when the forward multiple was 18.3, earnings growth accounted for two-thirds of the gain. The pandemic leg has been a re-rating phenomenon, but it slanders the overall advance to say that it has been disconnected from fundamentals. Earnings growth has been solid for an extended period of time and is poised to accelerate to 9.2% by the end of the year if today’s consensus expectations for calendar 2022 hold up. As for the issues raised by the news reports of Archegos’ demise, it is well understood that long bull markets breed excesses. It may be disheartening that a sizable pool of institutional capital found a way to use bespoke derivative instruments to game the system and evade regulatory attention but it’s certainly not surprising. When money, elections, university admissions, Olympic laurels, the World Series or the Tour de France are at stake, many people will do nearly anything to get an edge. Post-GFC measures like Basel III and the Volcker rule have made the regulated banking system more stable, but markets will never be completely shock-proof as long as humans are involved with them. We enjoy reading exposés as much as anyone else but we try to keep in mind that not every item the media sink their teeth into is evidence of systemic rot. There is a lot that is still not known about the Archegos saga beyond the apparent outlines of a highly leveraged investor who got into trouble when its underlying positions went the wrong way. It is striking to see broker-dealers challenging the three major ETF sponsors for ownership primacy in individual equities, as they do in DISCA, GSX, IQ, TME and VIAC – all stocks in which Archegos reportedly amassed large synthetic exposures. Credit Suisse and Nomura, which were singed the worst by Archegos exposures, have sizable holdings in several other companies, as do other broker-dealers. The presence of those other holdings might lead one to conclude that Archegos was not the only investor to discover that total-return swaps/contracts for difference offered a way to ramp up exposures. One might also conclude that the broker-dealers, finding households and non-financial businesses had little appetite for loans, were only too happy to provide leverage to investors via their prime brokerage arms. The two conclusions do not mean that a collapse is imminent, however. We continue to recommend that investors maintain risk-friendly portfolio positioning, albeit with added vigilance and a bias to shorten holding periods given the uncertain and potentially volatile backdrop. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com

Weekly Performance Update For the week ending Thu Apr 01, 2021 The Market Monitor displays the trailing 1-quarter performance of strategies based around the BCA Score. For each region, we construct an equal-weighted, monthly rebalanced portfolio consisting of the top 3 stocks per sector and compare it with the regional benchmark. For each portfolio, we show the weekly performance of individual holdings in the Top Contributors/Detractors table. In addition, the Top Prospects table shows the holdings that currently have the highest BCA Score within the portfolio. For more details, click the region headers below to be redirected to the full historical backtest for the strategy. BCA US Portfolio

Market Monitor (Apr 01, 2021)

Market Monitor (Apr 01, 2021)

Total Weekly Return BCA US Portfolio S&P500 TRI 2.30% 2.84% Top Contributors UTHR:US TX:US QFIN:US WES:US VICI:US Weekly Return 43 bps 26 bps 18 bps 18 bps 17 bps Top Detractors VIPS:US ESGR:US ARD:US UGI:US ACHC:US Weekly Return -17 bps -8 bps -4 bps -4 bps -3 bps Top Prospects ESGR:US TX:US QFIN:US VIPS:US SCCO:US BCA Score 99.76% 99.39% 97.20% 96.28% 95.00% BCA Canada Portfolio

Market Monitor (Apr 01, 2021)

Market Monitor (Apr 01, 2021)

Total Weekly Return BCA Canada Portfolio S&P/TSX TRI 2.75% 1.95% Top Contributors IFP:CA PXT:CA CFP:CA VII:CA TOU:CA Weekly Return 47 bps 35 bps 33 bps 33 bps 25 bps Top Detractors QBR.A:CA RCI.B:CA T:CA LNF:CA WEED:CA Weekly Return -11 bps -11 bps -10 bps -8 bps -7 bps Top Prospects LNF:CA IFP:CA LNR:CA CFP:CA LIF:CA BCA Score 98.91% 97.52% 97.24% 97.01% 96.13% BCA UK Portfolio

Market Monitor (Apr 01, 2021)

Market Monitor (Apr 01, 2021)

Total Weekly Return BCA UK Portfolio FTSE 100 TRI 1.94% 0.96% Top Contributors OXIG:GB NLMK:GB SVST:GB TM17:GB IPO:GB Weekly Return 36 bps 25 bps 22 bps 20 bps 17 bps Top Detractors DRX:GB XPP:GB ROSN:GB CNE:GB TYMN:GB Weekly Return -15 bps -8 bps -6 bps -6 bps -4 bps Top Prospects NLMK:GB GLTR:GB SVST:GB FXPO:GB BPCR:GB BCA Score 98.61% 97.92% 97.85% 96.33% 95.79% BCA Eurozone Portfolio

Market Monitor (Apr 01, 2021)

Market Monitor (Apr 01, 2021)

Total Weekly Return BCA EMU Portfolio MSCI EMU TRI 2.54% 2.74% Top Contributors SOL:IT PAH3:DE TEN:IT VGP:BE MOL:IT Weekly Return 29 bps 20 bps 16 bps 15 bps 15 bps Top Detractors SES:IT PHH2:DE HDG:NL MMT:FR GCO:ES Weekly Return -6 bps -5 bps -5 bps -4 bps -0 bps Top Prospects PHH2:DE SOLV:BE BEKB:BE SOL:IT SES:IT BCA Score 99.57% 99.23% 97.72% 97.51% 95.53% BCA Japan Portfolio

Market Monitor (Apr 01, 2021)

Market Monitor (Apr 01, 2021)

Total Weekly Return BCA Japan Portfolio TOPIX TRI -0.72% 0.97% Top Contributors 2362:JP 4980:JP 8595:JP 8966:JP 3132:JP Weekly Return 27 bps 14 bps 11 bps 10 bps 7 bps Top Detractors 9506:JP 9503:JP 2692:JP 5943:JP 7942:JP Weekly Return -16 bps -16 bps -15 bps -12 bps -11 bps Top Prospects 9436:JP 5451:JP 4008:JP 7279:JP 7942:JP BCA Score 99.17% 98.88% 98.73% 98.65% 98.57% BCA Hong Kong Portfolio

Image

Total Weekly Return BCA Hong Kong Portfolio Hang Seng TRI 3.97% 3.72% Top Contributors 148:HK 1888:HK 1088:HK 990:HK 856:HK Weekly Return 48 bps 45 bps 34 bps 34 bps 27 bps Top Detractors 41:HK 3306:HK 3369:HK 737:HK 991:HK Weekly Return -13 bps -4 bps -4 bps -3 bps 0 bps Top Prospects 990:HK 1378:HK 86:HK 737:HK 3306:HK BCA Score 99.89% 99.32% 98.84% 98.79% 98.51% BCA Australia Portfolio

Market Monitor (Apr 01, 2021)

Market Monitor (Apr 01, 2021)

Total Weekly Return BCA Australia Portfolio S&P/ASX All Ord. TRI 1.30% 0.63% Top Contributors ZIM:AU PDN:AU GRR:AU AQZ:AU BSE:AU Weekly Return 72 bps 25 bps 24 bps 15 bps 10 bps Top Detractors AGL:AU BLX:AU WPP:AU ADH:AU SOL:AU Weekly Return -19 bps -14 bps -13 bps -11 bps -6 bps Top Prospects GRR:AU BSE:AU ZIM:AU BLX:AU WPP:AU BCA Score 99.50% 99.47% 99.43% 98.58% 96.21%

Highlights Global manufacturing activity will soon peak due to growing costs and China’s policy tightening. This process will allow the dollar’s rebound to continue. EUR/USD’s correction will run further. This pullback in the euro is creating an attractive buying opportunity for investors with a 12- to 24-month investment horizon. Eurozone banks will continue to trade in unison with the euro. Feature The correction in the euro has further to run. The dollar currently benefits from widening real interest differentials, but a growing list of headwinds will cause a temporary setback for the global manufacturing sector, which will fuel the greenback rally further. Nonetheless, EUR/USD will stabilize between 1.15 and 1.12, after which it will begin a new major up-leg. Consequently, investors with a 12- to 24-month investment horizon should use the current softness to allocate more funds to the common currency. A Hiccup In Global Industrial Activity Global manufacturing activity is set to decelerate on a sequential basis and the Global Manufacturing PMI will soon peak. The first problem for the global manufacturing sector is the emergence of financial headwinds. The sharp rebound in growth in the second half of 2020 and the optimism created by last year’s vaccine breakthrough as well as the rising tide of US fiscal stimulus have pushed US bond yields and oil prices up sharply. These financial market moves are creating a “growth tax” that will bite soon. Mounting US interest rates have lifted global borrowing costs while the doubling in Brent prices has increased the costs of production and created a small squeeze on oil consumers. Thus, even if the dollar remains well below its March 2020 peak, our Growth Tax Indicator (which incorporates yields, oil prices and the US dollar) warns of an imminent top in the US ISM Manufacturing and the Global Manufacturing PMI (Chart 1). Already, the BCA Global Leading Economic Indicator diffusion index has dipped below the 50% line, which usually ushers in downshifts in global growth. A deceleration in China’s economy constitutes another problem for the global manufacturing cycle. Last year’s reflation-fueled rebound in Chinese economic activity was an important catalyst to the global trade and manufacturing recovery. However, according to BCA Research’s Emerging Market Strategy service, Beijing is now tightening policy, concerned by a build-up in debt and excesses in the real estate sector. Already, the PBoC’s liquidity withdrawals are resulting in a decline of commercial bank excess reserves, which foreshadows a slowing of China’s credit impulse (Chart 2). Chart 1The Global Growth Tax Will Bite

The Global Growth Tax Will Bite

The Global Growth Tax Will Bite

Chart 2Chinese Credit Will Slow

Chinese Credit Will Slow

Chinese Credit Will Slow

In addition to liquidity withdrawals, Chinese policymakers are also tightening the regulatory environment to tackle excessive debt buildups and real estate speculation. The crackdown on property developers and house purchases will cause construction activity to shrink in the second half of 2021. Meanwhile, tougher rules for both non-bank lenders and the asset management divisions of banks will further harm credit creation. BCA’s Chief EM strategist, Arthur Budaghyan, notes that consumer credit is already slowing. Chinese fiscal policy is unlikely to create a counterweight to the deteriorating credit impulse. China’s fiscal impulse will be slightly negative next year. Chinese financial markets are factoring in these headwinds, and on-shore small cap equities are trying to break down while Chinese equities are significantly underperforming global benchmarks. Chart 3Deteriorating Surprises

Deteriorating Surprises

Deteriorating Surprises

Bottom Line: The combined assault from the rising “growth tax” and China’s policy tightening is leaving its mark. Economic surprises in the US, the Eurozone, EM and China have all decelerated markedly (Chart 3), which the currency market echoes. Some of the most pro-cyclical currencies in the G-10 are suffering, with the SEK falling relative to the EUR and the NZD and AUD both experiencing varying degrees of weakness. The Euro Correction Will Run Further… Until now, the euro’s decline mostly reflects the rise in US interest rate differentials; however, the coming hiccup in the global manufacturing cycle is causing a second down leg for the euro. First, the global economic environment remains consistent with more near-term dollar upside, due to: Chart 4Commodities Are Vulnerable

Commodities Are Vulnerable

Commodities Are Vulnerable

A commodity correction that will feed the dollar’s rebound. Aggregate speculator positioning and our Composite Technical Indicator show that commodity prices are technically overextended (Chart 4). With this backdrop, the coming deceleration in Chinese economic activity is likely to catalyze a significant pullback in natural resources, which will hurt rates of returns outside the US and therefore, flatter the dollar. The dollar’s counter-cyclicality. The expected pullback in the Global Manufacturing PMI is consistent with a stronger greenback (Chart 5). The dollar’s momentum behavior. Among G-10 FX, the dollar responds most strongly to the momentum factor (Chart 6). Thus, the likelihood is high that the dollar’s recent rebound will persist, especially because our FX team’s Dollar Capitulation Index has only recovered to neutral from oversold levels and normally peaks in overbought territory. Chart 5The Greenback's Counter-Cyclicality

The Greenback's Counter-Cyclicality

The Greenback's Counter-Cyclicality

Chart 6The Dollar Is A High Momentum Currency

The Euro Dance: One Step Back, Two Steps Forward

The Euro Dance: One Step Back, Two Steps Forward

Second, the euro’s specific dynamics remain negative for now. Based on our short-term valuation model, the fair value of EUR/USD has downshifted back to 1.1, which leaves the euro 7% overvalued (Chart 7). Until now, real interest rate differentials and the steepening of the US yield curve relative to Germany’s have driven the decline in the fair value estimate. However, the deceleration in global growth also hurts the euro’s fair value because the US is less exposed than the Eurozone to the global manufacturing cycle. Chart 7The Euro's Short-Term Fair Value Is At 1.1

The Euro's Short-Term Fair Value Is At 1.1

The Euro's Short-Term Fair Value Is At 1.1

Chart 8Speculators Have Not Capitulated

Speculators Have Not Capitulated

Speculators Have Not Capitulated

The euro is also technically vulnerable, similar to commodities. Speculators are still massively net long EUR/USD and the large pool of long bets in the euro suggests that a capitulation has yet to take place (Chart 8). The euro responds very negatively to a weak Chinese economy. The Eurozone has deeper economic ties with China than the US. Exports to China account for 1.7% of the euro area’s GDP, and 2.8% of Germany’s compared to US exports to China at 0.5% of GDP. Indirect financial links are also larger. Credit to EM accounts for 45% of the Eurozone’s GDP compared to 5% for the US. Thus, the negative impact of a Chinese slowdown on EM growth has greater spillovers on European than on US ones rates of returns. A weak CNY and sagging Chinese capital markets harm the euro. The euro’s rebound from 1.064 on March 23 2020 to 1.178 did not reflect sudden inflows into European fixed-income markets. Instead, the money that previously sought higher interest rates in the US left that country for EM bonds and China’s on-shore fixed-income markets, the last major economies with attractive yields. These outflows from the US to China and EM pushed the dollar down, which arithmetically helped the euro. Thus, the recent EUR/USD correlates closely with Sino/US interest rate and with the yuan because the euro’s strength reflects the dollar demise (Chart 9). Consequently, a decelerating Chinese economy will also hurt EUR/USD via fixed-income market linkages. Finally, the euro will depreciate further if global cyclical stocks correct relative to defensive equities. Deep cyclicals (financials, consumer discretionary, energy, materials and industrials) represent 59% of the Eurozone MSCI benchmark versus 36% of the US index. Cyclical equities are exceptionally overbought and expensive relative to defensive names. They are also very levered to the global business cycle and Chinese imports. In this context, the expected deterioration in both China’s economic activity and the Global Manufacturing PMI could cause a temporary but meaningful pullback in the cyclicals-to-defensives ratio and precipitate equity outflows from Europe into the US (Chart 10). Chart 9EUR/USD And Chinese Rates

EUR/USD And Chinese Rates

EUR/USD And Chinese Rates

Chart 10EUR/USD Will Follow Cyclicals/Defensives

EUR/USD Will Follow Cyclicals/Defensives

EUR/USD Will Follow Cyclicals/Defensives

Bottom Line: A peak in the global manufacturing PMI will hurt the euro, especially because China will meaningfully contribute to this deceleration in global industrial activity. Thus, the euro’s pullback has further to run. An important resistance stands at 1.15. A failure to hold will invite a rapid decline to EUR/USD 1.12. Nonetheless, the euro’s depreciation constitutes nothing more than a temporary pullback. … But The Long-Term Bull Market Is Intact We recommend buying EUR/USD on its current dip because the underpinnings of its cyclical bull market are intact. Chart 11Investors Structurally Underweight Europe

Investors Structurally Underweight Europe

Investors Structurally Underweight Europe

First, investors are positioned for a long-term economic underperformance of the euro area relative to the US. The depressed level of portfolio inflows into Europe relative to the US indicates that investors already underweight European assets (Chart 11). This pre-existing positioning limits the negative impact on the euro of the current decrease in European growth expectations (Chart 11, bottom panel). Second, as we wrote last week, European growth is set to accelerate significantly this summer. Considering the absence of ebullient investor expectations toward the euro, this process can easily create upside economic surprises later this year, especially when compared to the US. Moreover, the deceleration in Chinese and global growth will most likely be temporary, which will limit the duration of their negative impact on Europe. Third, the US stimulus measure will create negative distortions for the US dollar. The addition of another long-term stimulus package of $2 trillion to $4 trillion to the $7 trillion already spent by Washington during the crisis implies that the US government deficit will not narrow as quickly as US private savings will decline. Therefore, the US current account deficit will widen from its current level of 3.5% of GDP. As a corollary, the US twin deficit will remain large. Meanwhile, the Fed is unlikely to increase real interest rates meaningfully in the coming two years because it believes any surge in inflation this year will be temporary. Furthermore, the FOMC aims to achieve inclusive growth (i.e. an overheated labor market). This policy combination forcefully points toward greater dollar weakness. The US policy mix looks particularly dollar bearish when compared to that of the Eurozone. To begin with, the balance of payment dynamics make the euro more resilient. The euro area benefits from the underpinning of a current account surplus of 1.9% of GDP. Moreover, the European basic balance of payments stands at 1.5% of GDP compared to a 3.6% deficit for the US. Additionally, FDI into Europe are rising relative to the US. The divergence in the FDI trends will continue due to the high probability that the Biden administration will soon increase corporate taxes. Chart 12The DEM In The 70s

The DEM In The 70s

The DEM In The 70s

The combination of faster vaccine penetration and much larger fiscal stimulus means that the US economy will overheat faster than Europe’s. Because the Fed seems willing to tolerate higher inflation readings, US CPI will rise relative to the Eurozone. In the 1970s, too-easy policy in Washington meant that the gap between US and German inflation rose. Despite the widening of interest rate and growth differentials in favor of the USD or the rise in German relative unemployment, the higher US inflation dominated currency fluctuations and the deutschemark appreciated (Chart 12). A similar scenario is afoot in the coming years, especially in light of the euro bullish relative balance of payments. Fourth, valuations constitute an additional buttress behind the long-term performance of the euro. Our FX strategy team Purchasing Power Parity model adjusts for the different composition of price indices in the US and the euro area. Based on this metric, the euro is trading at a significant 13% discount from its long-term fair value, with the latter being on an upward trend (Chart 13). Furthermore, BCA’s Behavioral Exchange Rate Model for the trade-weighted euro is also pointing up, which historically augurs well for the common currency. Lastly, even if the ECB’s broad trade-weighted index stands near an all-time high, European financial conditions remain very easy. This bifurcation suggests that the euro is not yet a major hurdle for the continent and can enjoy more upside (Chart 14). Chart 13EUR/USD Trades Well Below Long-Term Fair Value

EUR/USD Trades Well Below Long-Term Fair Value

EUR/USD Trades Well Below Long-Term Fair Value

Chart 14Easy European Financial ##br##Conditions

Easy European Financial Conditions

Easy European Financial Conditions

Chart 15Make Room For the Euro!

Make Room For the Euro!

Make Room For the Euro!

Finally, the euro will remain a beneficiary from reserve diversification away from the USD. The dollar’s status as the premier reserve currency is unchallenged. However, its share of global reserves has scope to decline while the euro’s proportion could move back to the levels enjoyed by legacy European currencies in the early 1990s (Chart 15). Large reserve holders will continue to move away from the dollar. BCA Research’s Geopolitical Strategy team argues that US tensions with China transcend the Trump presidency. Meanwhile, the current administration’s relationship with Russia and Saudi Arabia will be cold. For now, their main alternative to the dollar is the euro because of its liquidity. Moreover, the NGEU stimulus program creates an embryonic mechanism to share fiscal risk within the euro area. The Eurozone is therefore finally trying to evolve away from a monetary union bereft of a fiscal union. This process points toward a lower probability of a break up, which makes the euro more attractive to reserve managers. Bottom Line: Despite potent near-term headwinds, the euro’s long-term outlook remains bright. Global investors already underweight European assets, yet balance of payment and policy dynamics point toward a higher euro. Moreover, valuations and geopolitical developments reinforce the cyclical tailwinds behind EUR/USD. Thus, investors with a 12- to 24-month investment horizon should use the current euro correction to gain exposure to the European currencies. Any move in EUR/USD below 1.15 will generate a strong buy signal. Sector Focus: European Banks And The Istanbul Shake The recent decline in euro area bank stocks coincides with the 14% increase in USD/TRY and the 17% decline in the TUR Turkish equities ETF following the sacking of Naci Ağbal, the CBRT governor. President Erdogan is prioritizing growth over economic stability because his AKP party is polling poorly ahead of the 2023 election. The Turkish economy is already overheating, and the lack of independence of the CBRT under the leadership of Şahap Kavcıoğlu promises a substantial increase in Turkish inflation, which already stands at 16%. Hence, foreign investors will flee this market, creating further downward pressures on the lira and Turkish assets. European banks have a meaningful exposure to Turkey. Turkish assets account for 3% of Spanish bank assets or 28% of Tier-1 capital. For France, this exposure amounts to 0.7% and 5% respectively, and for the UK, it reaches 0.3% and 2%. As a comparison, claims on Turkey only represent 0.3% and 0.5% of the assets and Tier-1 capital of US banks. Unsurprisingly, fluctuations in the Turkish lira have had a significant impact one the share prices of European banks in recent years, even after controlling for EPS and domestic yield fluctuations (Table 1). Table 1TRY Is Important To European Banks…

The Euro Dance: One Step Back, Two Steps Forward

The Euro Dance: One Step Back, Two Steps Forward

Nonetheless, today’s TRY fluctuations are unlikely to have the same lasting impact on European banks share prices as they did from 2017 to 2019 because European banks have already shed significant amounts of Turkish assets (Chart 16). This does not mean that European banks are out of the woods yet. The level of European yields remains a key determinant of the profitability of Eurozone’s banks, and thus, of their share prices (Chart 17, top panel). Moreover, the euro still tightly correlates with European bank stocks as well (Chart 17, bottom panel). As a result, our view that the global manufacturing cycle will experience a temporary downshift and the consequent downside in EUR/USD both warn of further underperformance of European banks. Chart 16… But Less Than It ##br##Once Was

The Euro Dance: One Step Back, Two Steps Forward

The Euro Dance: One Step Back, Two Steps Forward

Chart 17Higher Yields And A stronger Euro, These Are Few Of My Favorite Things

Higher Yields And A stronger Euro, These Are Few Of My Favorite Things

Higher Yields And A stronger Euro, These Are Few Of My Favorite Things

These same views also suggest that this decline in bank prices is creating a buying opportunity. Ultimately, we remain cyclically bullish on the euro and the transitory nature of the manufacturing slowdown implies that global yields will resume their ascent. The cheap valuations of European banks, which trade at 0.6-times book value, make them option-like vehicles to bet on these trends, even if the banking sectors long-term prospects are murky. Moreover, they are a play on Europe’s domestic recovery this summer. We will explore banks in greater detail in future reports. Mathieu Savary, Chief European Investment Strategist Mathieu@bcaresearch.com

Highlights The Biden administration is combining Trumpian nationalism with a renewed push for US innovation in a major infrastructure bill that is highly likely to become law. Populism and Great Power struggle with China and Russia are structural forces that give enormous momentum to this effort. Don’t bet against it. President Biden’s $2.4 trillion infrastructure and green energy plan has a subjective 80% chance of passing into law by the end of the year, as infrastructure is popular and Democrats control Congress. The net deficit increase will range from $700 billion to $1.3 trillion depending on the size of corporate tax hikes in the final bill. The second part of Biden’s plan, the roughly $2 trillion American Families Plan, has a much lower chance of passage – at best 50/50 – as the 2022 midterm elections will loom and fiscal fatigue will set in. While the US infrastructure package is a positive cyclical catalyst, it was largely expected, and the Biden administration still faces early stress-tests on China/Taiwan, Russia, Iran, and even North Korea. Game theory helps explain why financial markets cannot ignore the 60% chance of a crisis in the Taiwan Strait. A full-fledged war is still low-probability but Taiwan remains the world’s preeminent geopolitical risk. In emerging markets, stay short Russian and Brazilian currency and assets – and continue favoring Indian stocks over Chinese. Feature The “arsenal of democracy” is a phrase that President Franklin Delano Roosevelt used to describe the full might of US government, industry, and labor in assisting the western allies in World War II. The US is reviving this combination of productive forces today, with President Joe Biden’s $4 trillion-plus American Jobs and Families Plan unveiled in Pittsburgh on March 31. The context is once again a global struggle among the Great Powers, albeit not world war (at least not yet … more on that below). The US is reviving its post-WWII pursuit of global liberal hegemony – symbolized by its role, growing once again, as the world’s chief consumer and chief warrior (Chart 1). Biden promoted his plan to build up the US’s infrastructure and social safety net explicitly as a historic and strategic investment – “in 50 years, people are going to look back and say this was the moment that American won the future.”1 It is critical for investors to realize that they are not witnessing another round of COVID-19 fiscal relief. That task is already completed with the Republican spending of 2020 and Biden’s own $1.9 trillion American Rescue Plan Act (ARPA), which together with the vaccine rollout are delivering a jolt to growth (Chart 2). Chart 1America Pursues Hegemony Anew

America Pursues Hegemony Anew

America Pursues Hegemony Anew

Chart 2Consensus Expects 6.5% US GDP Growth After American Rescue Plan

Consensus Expects 6.5% US GDP Growth After American Rescue Plan

Consensus Expects 6.5% US GDP Growth After American Rescue Plan

Our own back-of-the-envelope estimates of growth suggest that there is considerable upside risk even under current law (Chart 3). The output gap is also guesstimated here, and it will tighten faster than expected, especially as the service sector revives on economic reopening. Chart 3Back-Of-Envelope: US GDP And Output Gap Show Upside Risk After American Rescue Plan Act (ARPA)

The Arsenal Of Democracy

The Arsenal Of Democracy

A growth overshoot is even more likely considering that the first part of Biden’s proposal, the $2.4 trillion American Jobs Plan consisting mostly of infrastructure and green energy, is highly likely to pass Congress (by July at earliest and December at latest, most likely late fall). Our revised estimates for the US budget deficit show that this bill will add considerably to the deficit in the coming years, peaking in three or four years, thus averting the “fiscal cliff” in 2022-23 and adding to aggregate demand in the years after the short-term COVID-era cash handouts dry up (Chart 4). The net deficit increase will be $700 billion if Biden gets all of his tax hikes and $1.3 trillion if he only gets half of them, according to our sister US Political Strategy. Chart 4US Budget Deficit Will Remain Fat In Coming Years

The Arsenal Of Democracy

The Arsenal Of Democracy

We give Biden’s $2.4 trillion American Jobs Plan an 80% chance of passing through Congress by the end of the year. Infrastructure is broadly popular – as President Trump’s own $2 trillion infrastructure campaign proposal revealed – and Democrats have just enough votes to push it through the Senate via budget reconciliation, which requires zero votes from Republicans. Biden’s political capital is still strong given that his approval rating will stay above 50% as long as Trump is the obvious alternative and the Republicans are deeply divided over their own future (Chart 5).2 The second part of his plan, the $1.95 trillion American Families Plan, is much less likely to pass before the 2022 midterm elections – we would say 50/50 odds at best, if the infrastructure deal passes quickly. Chart 5Biden’s Political Capital Is Sufficient To Pass Another Major Law

The Arsenal Of Democracy

The Arsenal Of Democracy

Of course there are very important differences between Biden’s $2.4 trillion infrastructure plan and the similarly sized proposal that Trump would have unveiled this month had he been re-elected: Biden’s proposal is probably heavier on innovation and research and development, and certainly heavier on unionization and labor regulation, than Trump’s would have been. Biden’s plan integrates infrastructure with sustainability, renewable energy, and climate change initiatives that will help the US catch up with Europe and China on the green front. The plan will consist of direct government spending – rather than government seed money to promote private investment. It will be partially offset by repealing the corporate tax cuts in Trump’s signature Tax Cuts and Jobs Act. Most importantly – from a geopolitical point of view – Biden is making a bid for the US to resume its post-WWII quest for global liberal hegemony. He argued that the US stands at the crossroads of a global choice between “democracies and autocracies” and that rebuilding US infrastructure is ultimately about proving that democracies can create consensus and “deliver for their people.” Autocratic regimes, fairly or not, routinely call attention to the divisiveness of modern party politics in the West and the resulting policy gridlock which produces bad outcomes for many citizens, resulting in greater domestic dysfunction and “chaos.” It is important to note that this bid for hegemony will be more, not less, destabilizing for global politics as it will make the US economy more self-sufficient and insulated from the world. It will intensify the US-China and US-Russia strategic competition while making it more difficult for Biden to conduct bilateral diplomacy with these states given their differences in moral values and frequent human rights violations. What is happening now is the culmination of political shifts that pre-date the pandemic, but were galvanized by the pandemic, and it is of global, geopolitical significance for the coming decade and beyond.3 Biden and the establishment Democrats – embattled by populism on their right and left flanks – are shamelessly coopting President Trump’s “Make America Great Again” nationalism with a larger-than-life, infrastructure-and-manufacturing initiative that emphasizes productivity as well as “Buy American” protectionism. Biden explicitly argued that Americans need to boost innovation to “put us in a position to win the global competition with China in the upcoming years.” At Biden’s first press conference on March 25, he made a similar point about China: So I see stiff competition with China. China has an overall goal, and I don’t criticize them for the goal, but they have an overall goal to become the leading country in the world, the wealthiest country in the world, and the most powerful country in the world. That’s not going to happen on my watch because the United States are going to continue to grow and expand.4 The US trade deficit is set to widen a lot further under this massive domestic buildout. It aims to be the largest government investment program since Dwight Eisenhower’s building of the highways or the Kennedy-Johnson-Nixon space race. But it explicitly aims to diminish China’s role as a supplier of US goods and materials and the US trade deficit already shows evidence of economic divorce (Chart 6). The US is bound to have a larger trade deficit due to its own savings-and-investment imbalances but it has a powerful interest in redistributing this trade deficit to its allies and reducing over-dependency on China, which is itself pursuing strategic self-sufficiency and military modernization in anticipation of an ongoing rivalry this century. Chart 6Biden's Coopts Trump's Trade And Manufacturing Agenda

Biden's Coopts Trump's Trade And Manufacturing Agenda

Biden's Coopts Trump's Trade And Manufacturing Agenda

Bottom Line: Biden’s $2.4 trillion American Jobs Plan has an 80% chance of passing Congress later this year with a net increase to the fiscal thrust of between $700 billion and $1.3 trillion, depending on how many and how high the corporate tax hikes. The other $2 trillion social spending part of Biden’s plan has only a 50/50 chance of passage. The infrastructure and green energy rebuild should be understood as a return of Big Government motivated by populism and Great Power competition – it is a geopolitical theme with enormous momentum. The result will be faster US growth and higher inflation expectations, with the upside risk of a productivity boom (or boomlet) from the combination of public and private sector innovation. Investors should not bet against the cyclical bull market even though any increase in long-term potential GDP is speculative. A Fourth Taiwan Strait Crisis And The Cuban Missile Crisis Biden’s American Jobs Plan reserves $50 billion for US semiconductor manufacturing, a vast sum, larger than expectations and far larger than the relatively small public investments that helped revolutionize the US chip industry in the 1980s. But it will take a long time for these investments to pay off in the form of secure and redundant supply chains, while a semiconductor shortage is raging today that is already entangled with the US-China rivalry and tensions over the Taiwan Strait. The risk of a diplomatic or military incident is urgent because the chip shortage exacerbates China’s vulnerabilities at a time when the Biden administration is about to make critical decisions regarding the tightness of new export controls that cut off China’s access to US semiconductor chips, equipment, and parts. If the Biden administration appears to pursue a full-fledged tech blockade, as the Trump administration seemed bent on doing, then China will retaliate economically or militarily. Before going further we should point out that there are still areas of potential US-China cooperation under the Biden administration that could reduce tensions this year (though not over the long run). Biden and Xi Jinping might meet virtually as early as this month to discuss carbon emission reduction targets. Meanwhile China is positioning itself to serve as power-broker on two major foreign policy challenges – Iran and North Korea. Biden expressly seeks Chinese and Russian assistance based on the mutual interest in nuclear non-proliferation. Notably, Beijing’s renewed strategic dealings with Iran over the past month highlight its confidence that Biden does not have the appetite to stick with Trump’s “maximum pressure” but rather will seek to reduce sanctions and restore the 2015 nuclear deal. Hence China will seek to parlay influence over Tehran in exchange for reduced US pressure on its trade and economy (Chart 7). Beijing is making a similar offer on North Korea. Chart 7China Holds The Key To Iran, As With North Korea?

China Holds The Key To Iran, As With North Korea?

China Holds The Key To Iran, As With North Korea?

Ironically both Iranian and North Korean geopolitical tensions should skyrocket in the short term since high-stakes negotiations are beginning, even though they are ultimately more manageable risks than the mega-risk of US-China conflict over Taiwan. China cannot gain the advanced technology it needs to achieve a strategic breakthrough if the US should impose a total tech blockade, e.g. draconian export controls enforced on US allies. Yet it is highly unlikely to gain the tech by seizing Taiwan, since war would likely destroy the computer chip fabrication plants and provoke global sanctions that would crush its economy. The result is that China is launching a massive campaign of domestic production and indigenous innovation while circumventing US restrictions through cyber and other means. Still, a dangerous strategic asymmetry is looming because the US will retain access to the most advanced computer chips via its alliances and on-shoring, whereas China will remain vulnerable to a tech blockade via Taiwan. This brings us to our chief global geopolitical risk: a US-China showdown in the Taiwan Strait. Highlighting the urgency of the risk, Admiral John Aquilino, the nominee for Commander of the US Indo-Pacific Command, told the Senate Armed Services Committee that China might not wait six years to attack Taiwan: “My opinion is that this problem is much closer to us than most think and we have to take this on.”5 To illustrate the calculus of such a showdown – and our reasons for maintaining an alarmist tone and building up market hedges and safe-haven investments – we turn to game theory. Game theory is not a substitute for empirical analysis but a tool to formalize complex international systems with multiple decision-makers. An obvious yet fair analogy to a US-China-Taiwan crisis is the Cuban missile crisis of 1962.6 The standard construction of the Cuban missile crisis in game theory goes as follows: if the US maintains a blockade and the Soviets withdraw their missiles a compromise is achieved and war is averted; if the US conducts air strikes and the Soviets maintain or use their missiles then war ensues. The payouts to each player are shown in the matrix in Diagram 1. Diagram 1Cuban Missile Crisis, 1962

The Arsenal Of Democracy

The Arsenal Of Democracy

One concern about this construction is that the payouts may underestimate the costs of war since nuclear arms could be used. We insert a comment into the diagram highlighting that the payouts could be altered to account for nuclear war. Note that this alteration does not change the final outcome: the equilibrium scenario is still US blockade and Soviet withdrawal, which is what happened in reality. If we model a US-China-Taiwan conflict along similar lines, the US takes the role of the Soviet Union while China stands where the US stood in 1962 (Diagram 2). This is a theoretical scenario in which the US offers Taiwan a decisive improvement in its security or offensive military capabilities. However, because of the unique circumstances of the Chinese civil war, in which the victors established the People’s Republic of China in Beijing in 1949 and the defeated forces retreated to Taiwan, China’s regime legitimacy is at stake in any showdown over Taiwan. If Beijing suffered a defeat that secured Taiwan’s independence while degrading Beijing’s regime legitimacy and security, the Chinese regime might not survive the domestic blowback.7 Diagram 2Fourth Taiwan Strait Crisis – What Happens If The US Offers Game-Changing Military Support To Taiwan?

The Arsenal Of Democracy

The Arsenal Of Democracy

Thus we reduce the Chinese payout in the case of American victory. In the top right cell of Diagram 2, the row player’s payout falls from two points (2ppt) in the first diagram to one point (1ppt) in this diagram. This seemingly slight change entirely alters the outcome of the game. Beijing now faces equally bad outcomes in the event of defeat, whereas victory remains preferable to a tie. Therefore as long as China believes that the US will not resort to nuclear weapons to defend Taiwan (a reasonable assessment) then it may make the mistake of opting for military force to ensure victory. Fortunately for global investors the US is not providing Taiwan with game-changing military capabilities, although it is ultimately up to China to decide what threatens its security and the US is in the process of upgrading Taiwan’s defense in an effort to deter Beijing from forceful reunification. Thus the exercise demonstrates why we do not expect immediate war – no game-changer yet – but at the same time it shows why war is much likelier than the consensus holds if the military or political status quo changes in a way that China deems strategically unacceptable. A lower-degree Taiwan crisis should be expected – i.e. one in which the US maintains tech restrictions, offers arms sales or military training that do not upend the military balance, or signs free trade agreements or other significant upgrades to the US-Taiwan relationship.8 We would give a 60% probability to some kind of crisis over the next 12-24 months. The global equity market could at least suffer a 10% correction in a standard geopolitical crisis and it could easily fall 20% if US-China war appears more likely. What would trigger a full-fledged Taiwan war? We would grow even more alarmed if we saw one of three major developments: Chinese internal instability giving rise to a still more aggressive regime; the US providing Taiwan with offensive military capabilities; or Taiwan seeking formal political independence. The first is fairly likely, the second lends itself to miscalculation, and the third is unlikely. But it would only take one or two of these to increase the war risk dramatically. Bottom Line: The Taiwan Strait is still the critical geopolitical risk and Biden’s policy on China is still unclear. Iranian and North Korean tensions will escalate in the short run but the fundamental crisis lies in Taiwan. Since some kind of showdown is likely and war cannot be ruled out we advise clients to accumulate safe-haven assets like the Japanese yen and otherwise not to bet headlong against the US dollar until it loses momentum. Emerging Markets Round-Up In this section we will briefly update some important emerging market themes and views: Chart 8Favor USMCA Over Putin's Russia

Favor USMCA Over Putin's Russia

Favor USMCA Over Putin's Russia

Russia: US-Russia tensions are escalating in the face of Biden’s reassertion of the US bid for liberal hegemony, which poses a direct threat to Russia’s influence in eastern Europe and the former Soviet Union. Ukraine is expected to see a renewed conflict this spring. The top US and Russian military commanders spoke on the phone for the second time this year after Ukrainian military reports indicated that Russia is amassing forces on the border. We also assign a 50/50 chance that the US will use sanctions to prevent the completion of the NordStream II pipeline from Russia to Germany, an event that would shake up the German election as well as provoke a Russian backlash. The Russian ruble has suffered a long slide since Putin’s invasion of Georgia in 2008 and Crimea in 2014 and the country’s currency and equities have not staged much of a comeback amid the global cyclical upswing and commodity price rally post-COVID. We recommend investors favor the Canadian dollar and Mexican peso as oil plays in the context of American stimulus and persistent Russian geopolitical risk (Chart 8). We also favor developed market European stocks over emerging Europe, which will suffer from renewed US-Russia tensions. Brazil: Brazilian President Jair Bolsonaro’s domestic political troubles are metastasizing as expected – the rally-around-the-flag effect in the face of COVID-19 has faded and his popular approval rating now looks dangerously like President Trump’s did, relative to previous presidents, which is an ominous warning for the “Trump of the South,” who faces an election in October 2022 (Chart 9). The COVID-19 deaths are skyrocketing, with intensive care units reaching critical levels across the country. The president has reshuffling his cabinet, including all three heads of the military in an unprecedented disruption that compounds fears about his willingness to politicize the military.9 Meanwhile the judicial system looks likely (but not certain) to clear former President Luiz Inácio Lula da Silva to run against Bolsonaro for the presidency, a potent threat (Chart 10). Bolsonaro’s three pillars of political viability have cracked under the pandemic: the country remains disorderly, the systemic corruption and the “Car Wash” scandal under the former ruling party are no longer at the center of public focus, and fiscal stimulus has replaced structural reform. Chart 9Brazil: Will ‘Trump Of The South’ Face Trump’s Fate?

The Arsenal Of Democracy

The Arsenal Of Democracy

Our Brazilian GeoRisk Indicator has reached a peak with Bolsonaro’s crisis – and likely breaking of the fiscal spending growth cap put in place at the height of the political crisis in 2016 – while Brazilian equities relative to emerging markets have hit a triple bottom (Chart 11). It is too soon for investors to buy into Brazil given that the political upheaval can get worse before it gets better and a Lula administration is no cure for Brazil’s public debt crisis, though a short-term technical rally is at hand. Chart 10Brazil’s Lula Looks To Be A Contender In 2022?

The Arsenal Of Democracy

The Arsenal Of Democracy

Chart 11Brazil: Policy Risk Peaks, Equities Hit Triple-Bottom Versus EM

Brazil: Policy Risk Peaks, Equities Hit Triple-Bottom Versus EM

Brazil: Policy Risk Peaks, Equities Hit Triple-Bottom Versus EM

India: A lot has happened since we last updated our views on India, South Asia, and the broader Indian Ocean basin. Farmer protests broke out in India, forcing Prime Minister Narendra Modi to temporarily suspend his much-needed structural reforms to the agricultural sector, while China-backed military coup broke out in Myanmar, and the US election set up a return to negotiations with Iran and the Taliban in Afghanistan. Perhaps the biggest surprise was the Indo-Pakistani ceasefire, despite boiling tensions over India’s decision to make Jammu and Kashmir a federal union territory. The ceasefire is temporary but it does highlight a changing geopolitical dynamic in the region. India and Pakistan ceased fire along the Line of Control where they have fought many times. The ceasefire does not resolve core problems – Pakistan will not stop supporting militant proxies and India will not grant Kashmir autonomy – but it does show their continued ability to manage the intensity of disputes while dealing with the global pandemic. An earlier sign of coordination occurred after the exchange of air strikes in early 2019, which preceded the Indian election and suggested that India and Pakistan had the ability to control their military encounters. India’s move to revoke the autonomy of Jammu and Kashmir in August 2019, along with various militant operations, created the basis for another major conflict this year. After all, the Kargil war in 1999 followed nuclear weaponization, while the 2008 conflict followed the Mumbai attack. But instead India and Pakistan have agreed to a temporary truce. A major India-Pakistan conflict would be a “black swan” as nobody is expecting it at this point. Not coincidentally, India and China also reduced tensions after the flare-up in their Himalayan territorial disputes in 2020. China may be reducing tensions now that it no longer has to distract its population from Trump and the US election. China is shifting its focus to the Myanmar coup, another area where it hopes to parlay its influence with a Biden administration preoccupied with democracy and human rights. Sino-Indian tensions will resume later, especially as China continues its infrastructure construction at the farthest reaches of its territory for the sake of economic stimulus, internal control, and military logistics. The Biden administration is adopting the Trump administration’s efforts to draw India into a democratic alliance. But more urgently it is trying to withdraw from Afghanistan and cut a deal with Iran, which means it will need Indian and Pakistani cooperation and will want India to play a supportive role. Typically India eschews alliances and it will disapprove of Biden’s paternalism. For both China and Pakistan, making a temporary truce with India discourages it from synching up relations with the US immediately. Still, we expect India to cooperate more closely with the US over time, both on economic and security matters. This includes a beefed up “Quad” (Quadrilateral Security Dialogue) with Japan and Australia, which already have strong economic ties with India. Biden’s attempt to frame US foreign policy as a global restoration of democracy and liberalism will not go very far if he alienates the largest democracy in the world and in Asia. Nor will his attempt to diversify the US economy away from China or counter China’s regional assertiveness. Therefore Biden will have to take a supportive role on US-India ties. We are sticking with our contrarian long India / short China equity trade (Chart 12). India cannot achieve its geopolitical goals without reforming its economy and for that very reason it will redouble its structural reform drive, which is supported by changing voting patterns in favor of accelerating nationwide economic development. India will also receive a tailwind from the US and its allies as they seek to diversify production sources and reduce supply chain dependency on China, at least for health, defense, and tech. Meanwhile China’s government is pursing import substitution, deleveraging, and conflict with its neighbors and the United States. While Chinese equities are much cheaper than Indian equities on a P/E basis, they are not as pricey on a P/B and P/S basis (Chart 13) – and valuation trends can continue under the current macro and geopolitical backdrop. Indian equities are more volatile but from a long-term and geopolitical point of view, India’s moment has arrived. Chart 12Contrarian Trade: Stick To Long India / Short China

Contrarian Trade: Stick To Long India / Short China

Contrarian Trade: Stick To Long India / Short China

Bottom Line: Stay long Indian equities relative to Chinese and stay short Russian and Brazilian currencies and assets. These views are based on political and geopolitical themes that will remain relevant over the long run but are also seeing short-term confirmation. Chart 13Indian Stocks Not As Over-Priced On Price-To-Book, Price-To-Sales

Indian Stocks Not As Over-Priced On Price-To-Book, Price-To-Sales

Indian Stocks Not As Over-Priced On Price-To-Book, Price-To-Sales

Investment Takeaways To conclude we want to highlight two investment takeaways. First, while the market has rallied in expectation of the US stimulus package, Biden must now get the package passed. This roller coaster process, combined with the inevitable European recovery once the vaccine rollout gets on its feet (Chart 14), will power an additional rally in cyclicals, value stocks, and commodities. This is true as long as China does not tighten monetary and fiscal policy too abruptly, a risk we have highlighted in previous reports. Chart 14Europe's Vaccination Problem

Europe's Vaccination Problem

Europe's Vaccination Problem

While the US is pursuing “Buy American” provisions within its stimulus package, its growing trade deficit shows that it will be forced to import goods and services to meet its surging demand. This is beneficial for its nearest trade partners, Canada and Mexico, and Europe – as well as China substitutes further afield in some cases. Our European Investment Strategist Mathieu Savary has pointed out the opportunities lurking in Europe at a time when vaccine troubles and lockdowns are clouding the medium-term economic view, which is brightening. He recommends going long the “laggard” sectors and sub-sectors that have not benefited much relative to “leaders” that rallied sharply in the wake of last year’s stimulus, vaccine discovery, and defeat of President Trump (Chart 15). The laggard sectors are primed to outperform on rising US interest rates and decelerating Chinese economy as well (Chart 16). Therefore we recommend going long his basket of Euro Area laggards and short the leaders. Chart 15Europe’s Laggards And Leaders

The Arsenal Of Democracy

The Arsenal Of Democracy

Chart 16Macro Forces Favor The Laggards over the Leaders

Macro Forces Favor The Laggards over the Leaders

Macro Forces Favor The Laggards over the Leaders

Chart 17Will OPEC 2.0 Maintain Production Discipline To Keep Oil Supplies Tight?

Will OPEC 2.0 Maintain Production Discipline To Keep Oil Supplies Tight?

Will OPEC 2.0 Maintain Production Discipline To Keep Oil Supplies Tight?

Commodities – especially base metals – will continue to benefit from the global and European reopening as well as the US infrastructure buildout, assuming that China does not shoot its economy in the foot. Our Commodity & Energy Strategy highlights that global oil prices should remain in a $60-$80 per barrel range over the coming years on the back of tight supply/demand balances and ongoing OPEC 2.0 production management (Chart 17). We continue to see upside oil price risks in the first half of the year but downside risks in the second half. The US pursuit of a deal with Iran may trigger sparks initially – i.e. unplanned supply outages – but this will be followed by increased supply from Iran and/or OPEC 2.0 as a deal becomes evident. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 White House, "Remarks by President Biden on the American Jobs Plan," Pittsburgh, Pennsylvania, March 31, 2021, whitehouse.gov. 2 A bipartisan bill is conceivably, barely, since Republicans face pressure to join with such a popular bill, but they cannot accept the corporate tax hikes, unionization, or green boondoggles that will inevitably occur. 3 The pandemic and President Trump’s hands-off attitude toward it helped galvanize this revival of Big Government, but the revival was already well on its way prior to the pandemic. 4 White House, "Remarks by President Biden in Press Conference," March 25, 2021, whitehouse.gov. 5 Again, "the most dangerous concern is that of a military force against Taiwan," though he implied that Beijing would wait until after the February 2022 Winter Olympics before taking action. He requested that the US urgently increase regional military defense. See Senate Armed Services Committee, "Nomination – Aquilino," March 23, 2021, armed-services.senate.gov. 6 At that time the Soviet Union stationed nuclear missiles in Cuba that threatened the US homeland directly and sent a convoy to make the missile installation permanent. The US imposed a blockade. A showdown ensued, at great risk of war, until the Soviets withdrew and the Americans made some compromises regarding missiles in Turkey. 7 Note that this was not the case for the US in 1962: Cuba did not have special significance for the legitimacy of the American republic and the American regime would have survived a defeat in the showdown, although its security would have been greatly compromised. 8 Taiwan is proposing to buy a missile segment enhancement for its Patriot Advanced Capability-3 missile defense system for delivery in 2025, though this is not yet confirmed by the Biden administration. See for example Yimou Lee, "Taiwan To Buy New U.S. Air Defence Missiles To Guard Against China," Reuters, March 31, 2021, reuters.com. 9 See Monica Gugliano, "I Will Intervene! The Day Bolsonaro Decided To Send Troops To The Supreme Court," Folha de São Paulo, August 2020, piaui.folha.uol.com.br.

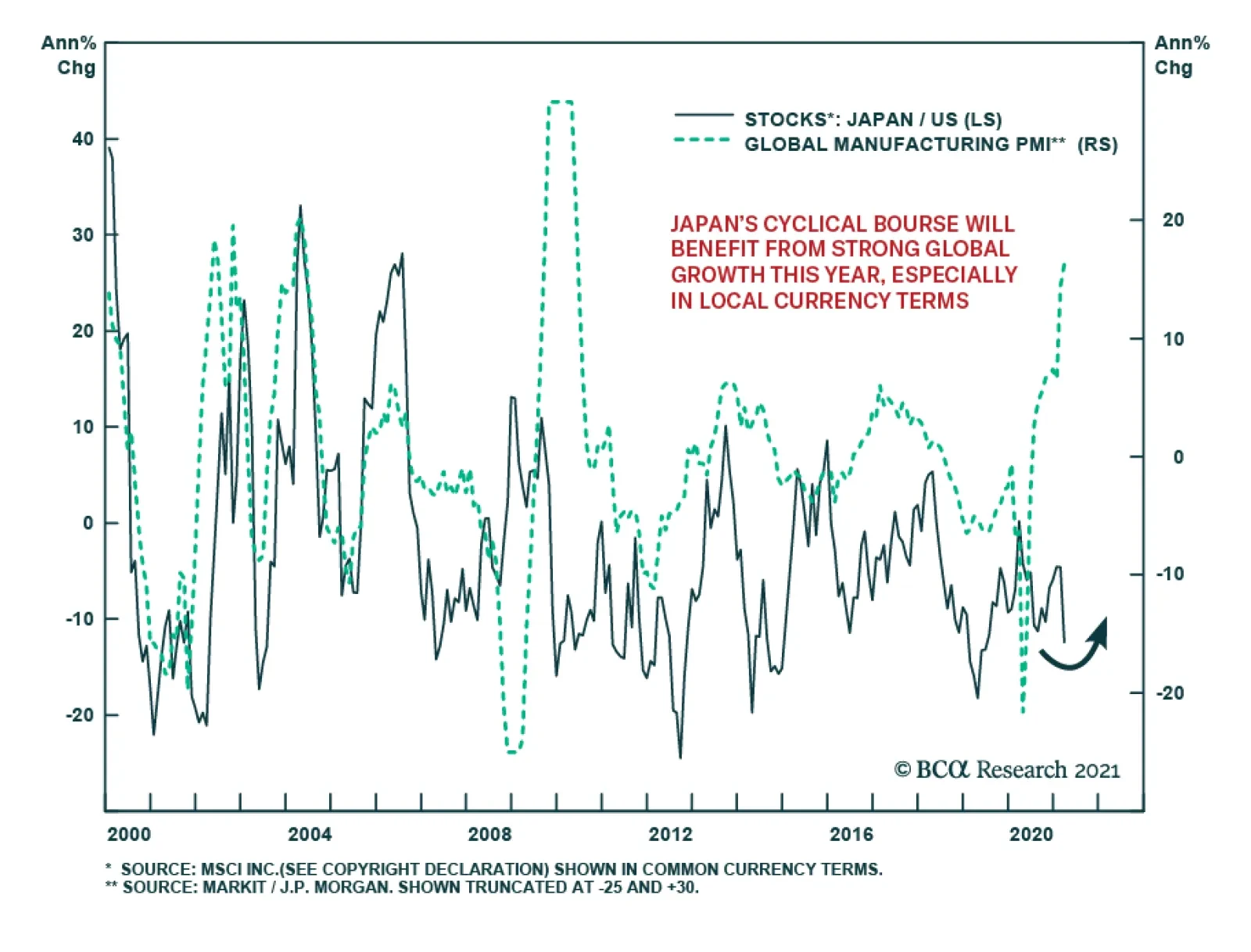

Japanese equities have stalled so far this year. The MSCI Japan index is up a negligible 0.8% in US dollar terms, underperforming the MSCI All-Country World index. Nonetheless, in local currency terms, Japanese equities outperformed, which fits with the…

Highlights President Biden’s $2.4 trillion “American Jobs Plan” is a major US public investment that will dispel any endogenous deflationary tail risk from the US economy this cycle, increase inflation expectations yet boost productivity, and hike corporate taxes. The proposal has an 80% chance of passage before the end of the year given that infrastructure is popular and Democrats can pass the bill via reconciliation with zero Republican votes. The $2.4 trillion infrastructure proposal will take effect over eight years and will be offset by corporate tax hikes that will take effect over 15 years. The increase in the budget deficit will be around $400 billion if all tax hikes pass and $1.4 trillion if only half the tax hikes pass. The American Families Plan will follow with another roughly $700 billion to $1.3 trillion increase to the budget deficit, depending on how much individual/household taxes go up. But this bill only has a 50/50 chance of passing before the 2022 midterm elections. Investors should maintain a bullish cyclical (12-month) bias and keep favoring value stocks, industrials, and materials over tech and health care. We also recommend going long consumer discretionary stocks and energy large caps versus small caps. Feature President Joe Biden spoke in Pittsburgh on Wednesday to unveil his economic vision and policy proposals going forward. Biden proposed a $2.4 trillion “American Jobs Plan” infrastructure and green energy package to be implemented over eight years, which will be part of a $4 trillion-plus “Build Back Better” legislative agenda that will be partially offset by an estimated $3 trillion in tax hikes to take effect over 15 years. The result will be a pro-cyclical boost to fiscal thrust, GDP growth, and inflation expectations; some potential for a productivity boom; a possible expansion of the social safety net; and tax reform that reduces US corporate profits. Pennsylvania is a Rust Belt state, Biden’s home state, and a critical swing state in the 2016 and 2020 elections, so the location makes sense. Biden aims to solidify the economic recovery and restore the Democratic Party’s leadership on infrastructure and manufacturing after Republican President Trump nearly stole their thunder. If he succeeds then his administration and party will improve their support substantially. The US economy is opening rapidly while the COVID-19 vaccination campaign continues apace. Chart 1 shows that household disposable income and net worth surged as a result of giant fiscal relief while consumer spending lags behind due to social distancing. The $1.7 trillion treasure chest of personal savings creates the basis for an increase in spending as consumers get vaccinated and regain their freedom. Economic policy uncertainty has collapsed, even relative to global uncertainty (Chart 2). There are no longer doubts about whether government will spend the country out of a slump. Even state and local governments have been bailed out despite having much stronger finances than predicted. However, there are doubts about how much more deficit spending the Biden administration will be able to push through, and that is what will now be debated in Congress following Biden’s Pittsburgh proposals. Chart 1Lower Spending And Higher Income Led To Mounting Excess Savings

Lower Spending And Higher Income Led To Mounting Excess Savings

Lower Spending And Higher Income Led To Mounting Excess Savings

Chart 2US Policy Uncertainty Soon To Revive

US Policy Uncertainty Soon To Revive

US Policy Uncertainty Soon To Revive

There will not be much of a deflationary tail risk to the new business cycle in the context of this expansive fiscal policy, as bullish investors are well aware. However, policy uncertainty will revive going forward as more spending will raise the risk of economic overheating, tax hikes will affect different sectors disproportionately, deficits and debt will balloon, and Biden’s challenges with immigration and foreign policy will intensify. There is an upside risk for the stock market that Congress delays tax hikes but this is not our base case. In this week’s report we revise and update our estimates for the impact of Biden administration’s legislative proposals – including his projected $4 trillion-plus in spending on infrastructure, health, and education – taking into consideration Biden’s Pittsburgh speech, his first press conference on March 25, and all the rumors and leaks that have come to light over the past two weeks. Back-Of-The-Envelope Estimates Of US Growth And Output Gap After ARPA First we need to revise our back-of-the-envelope estimates of the impact of the $1.9 trillion American Rescue Plan Act (ARPA). Chart 3 shows two scenarios for US GDP growth. The first is the “maximum” scenario, in which US real GDP grows by 10.7% because all of the money authorized under the new law is spent. The second scenario puts real growth at 6% by using only the Congressional Budget Office’s expected federal outlays (as opposed to budget authority) to estimate the government spending component of GDP. In both cases we assume that 33% of the fiscal relief is spent in FY2021 and the remainder in FY2022. These scenarios do not include Biden’s American Jobs and Families Plans because those bills have yet to be drafted, let alone pass Congress. Chart 3Revised US GDP Estimates With ARPA

Biden’s Pittsburgh Speech And Legislative Agenda

Biden’s Pittsburgh Speech And Legislative Agenda

Consensus estimates put real GDP growth at 5.7% and the Federal Reserve estimates that 2021 growth will clock in at 6.5%, as shown in Chart 4. Not all of the government spending will translate directly into aggregate demand because 37% of the ARPA consists of direct checks and unemployment benefits to households that may only spend one-third of the amount they receive (while paying down debt with a third of it and saving a third of it). Yet more government deficit spending is coming down the pike and consumers are sitting on a huge pile of savings, which implies that growth could surprise to the upside of consensus estimates. Chart 4Consensus Estimates Of US GDP PosT-ARPA

Consensus Estimates Of US GDP PosT-ARPA

Consensus Estimates Of US GDP PosT-ARPA

Chart 5 uses our same back-of-the-envelope calculation to estimate the impact of current law (including ARPA) on the US output gap. The output gap is the difference between actual GDP growth and potential GDP growth – during busts the country’s growth falls well beneath potential while during booms it rises above potential. The chart shows that if all of the government relief funds are spent then the output gap will be more than closed by the end of the year. By contrast, the CBO’s January projection shows the output gap persisting through 2025. While our estimates in Chart 5 may be too generous regarding federal cash handouts translating directly to consumer spending and higher demand, nevertheless the consensus estimate is entirely understated and out of date as a result of ARPA and the Biden administration’s additional fiscal spending that is coming. Chart 5Revised US Output Gap Estimates With ARPA

Biden’s Pittsburgh Speech And Legislative Agenda

Biden’s Pittsburgh Speech And Legislative Agenda

Chart 6Revised US Budget Deficit Projection Post-ARPA

Biden’s Pittsburgh Speech And Legislative Agenda

Biden’s Pittsburgh Speech And Legislative Agenda

Chart 6 updates our US budget deficit outlook using the CBO’s February budget baseline. The ARPA’s increase in government spending is added to create the new Democratic Party status quo scenario over the next ten years, with the budget normalizing by 2025. The Democratic low spending scenario assumes that Biden passes the $2.4tn infrastructure-plus plan announced in Pittsburgh (Table 1) using all the revenue from all the corporate tax hikes. Biden’s agenda will be broken into separate bills with varying probabilities of success. So in our budget deficit outlook we only include the infrastructure-and-corporate-tax-hikes component that is apparently being prioritized. Table 1Biden's 'American Jobs Plan'

Biden’s Pittsburgh Speech And Legislative Agenda

Biden’s Pittsburgh Speech And Legislative Agenda

Bottom Line: US growth will surprise to the upside of consensus estimates while the US output gap will be closed much sooner than expected. Financial markets are largely prepared for this outcome, although it reinforces that investors should maintain a cyclically bullish view and tactically should buy on the dips. Biden’s Pittsburgh Speech And ‘American Jobs Plan’ Budget Impacts Our view is that the Biden administration has a subjective 80% chance of passing a second major budget reconciliation bill (FY2022) and a 50% chance of passing a third budget reconciliation bill (FY2023). The question appears to be resolved that Democrats will prioritize infrastructure over social welfare. Whichever one they prioritize can be linked to tax hikes and yet will still be highly likely to pass given that no Republican votes are needed under budget reconciliation rules. Moderate Democrats may water down the tax provisions but they would be suicidal to oppose their entire party on the administration’s signature piece of legislation. The social spending bill, assuming it follows infrastructure, would have to be pursued via a third reconciliation bill for FY2023 but it is less likely to pass. By next year Biden will have spent a lot of his political capital, fiscal spending fatigue will be a real phenomenon, and the 2022 midterm elections will loom. What matters for investors is the impact on the budget deficit since that will determine how big of an impact will hit GDP and how long US fiscal policy remains accommodative. Table 2 shows the impact on the budget balance if Biden gets all of his spending and all revenue proposals (Baseline), if he gets all the spending but only half the tax hikes (Scenario 1), and if he gets half the spending and half the tax hikes (Scenario 2). Scenarios 3 and 4 treat the social spending plan with varying degrees of tax revenue from the proposed individual tax hikes, while Scenarios 5 and 6 treat the infrastructure plan with varying tax revenue from corporate tax hikes. Table 2Biden’s Forthcoming ‘American Jobs Plan’ Legislative Proposals

Biden’s Pittsburgh Speech And Legislative Agenda

Biden’s Pittsburgh Speech And Legislative Agenda

Table 3 shows the Biden campaign’s proposed tax hikes by line item along with the spending proposals. The range of net deficit spending runs from about $400 billion to about $3 trillion over ten years, which is a broad range and not very telling but which seems, subjectively, likely to settle in the $2 trillion range. Chart 7 shows the budget deficit’s deviation from the status quo trajectory in each of these scenarios, i.e. additional fiscal thrust. Table 3Biden’s Tax-And-Spend Proposals In Detail

Biden’s Pittsburgh Speech And Legislative Agenda