Equities

On Wednesday, President Biden unveiled his second major economic program. The American Jobs Plan is a $2.4 trillion investment in the country’s infrastructure, designed to improve the quality of infrastructure, create jobs and “out-compete China”. The…

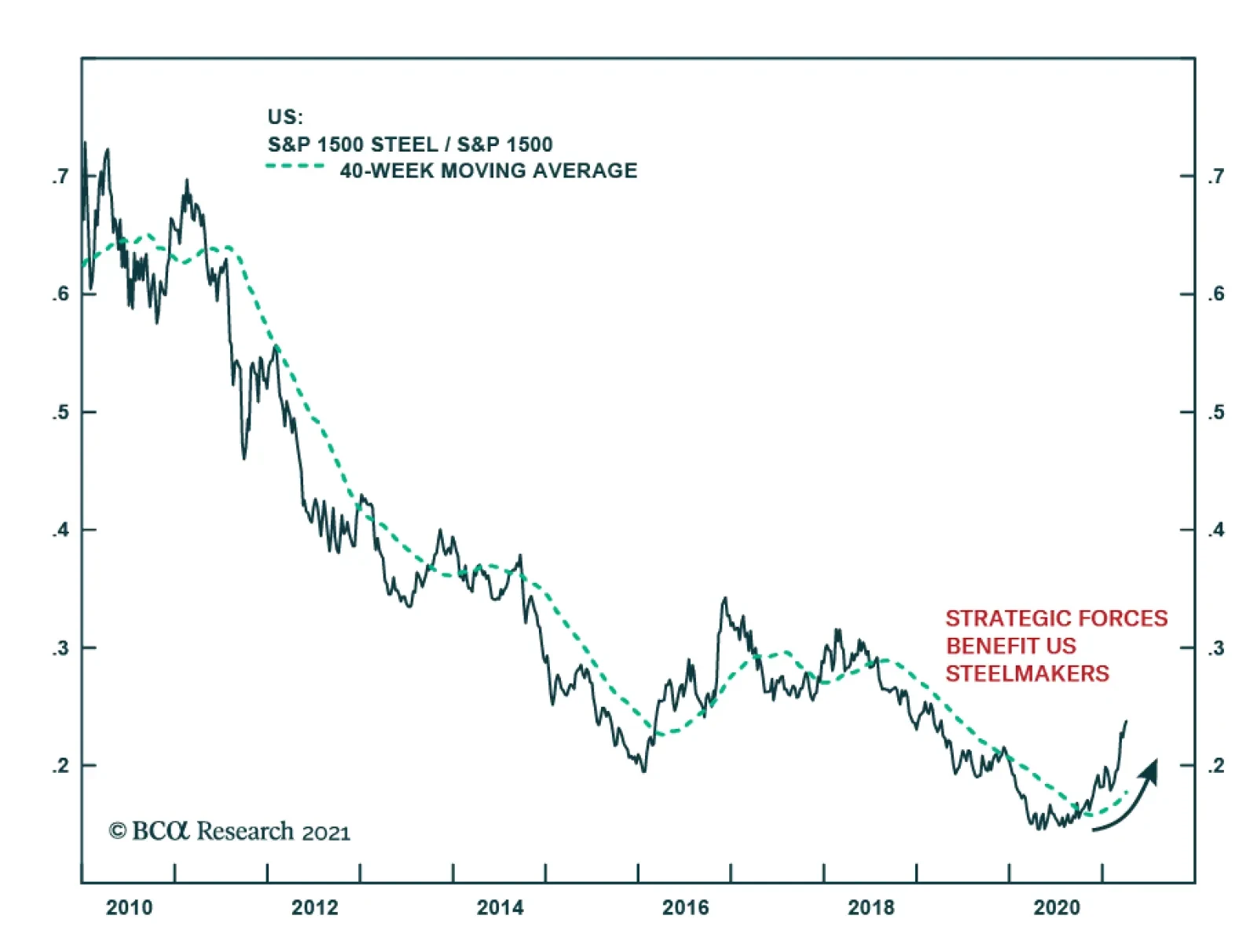

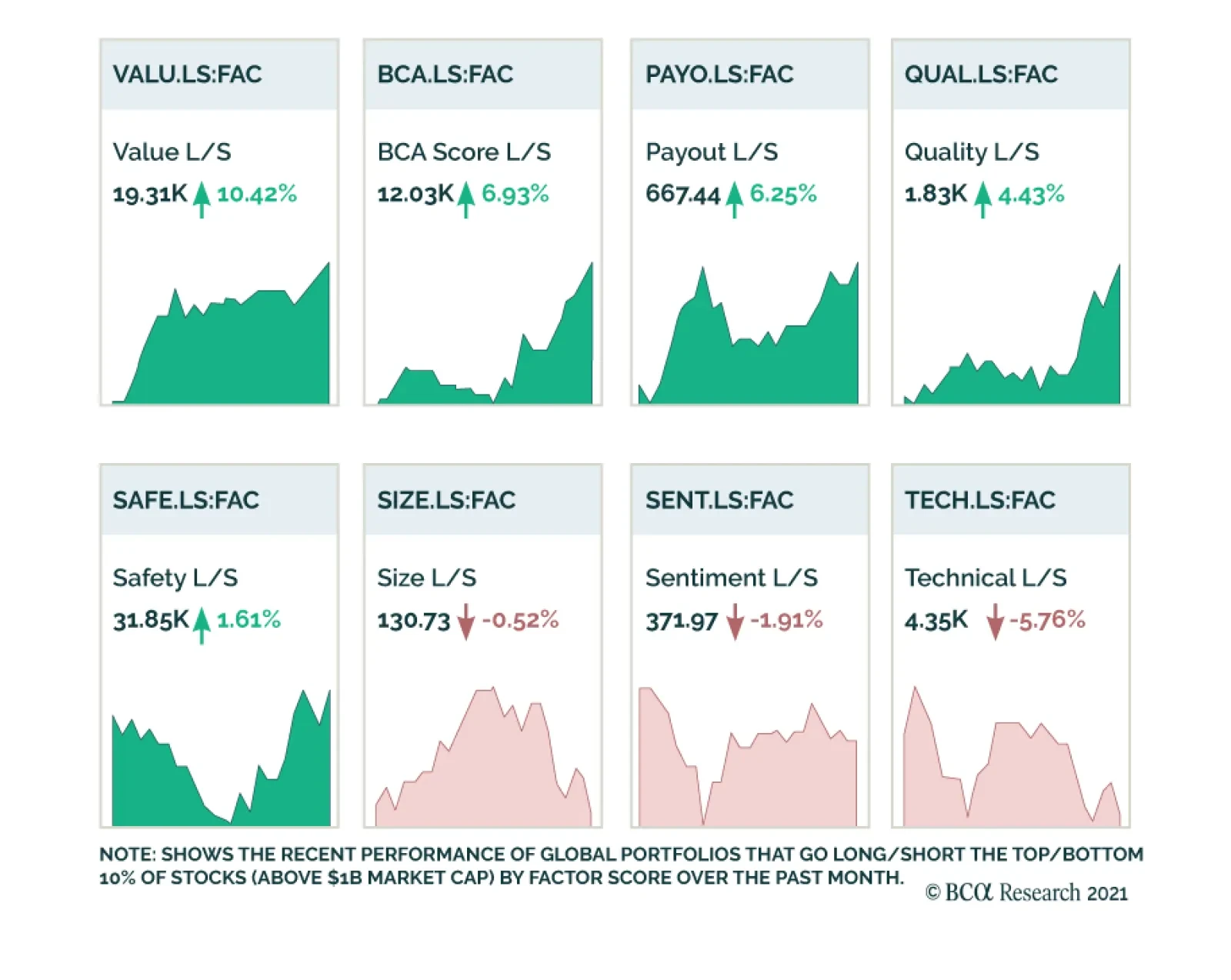

Size and Sentiment had been the dominant factors driving equity markets since the conclusion of the US Presidential Election and positive vaccine news in early November 2020. Other key factors such as Quality and Safety had been lagging. This phenomenon was…

In the latest Special Report we attempted to answer the question of whether this coming rebound in CPI is a paradigm shift that will push the US into a new era of consistently high (i.e. above 3%/annum) core CPI inflation, or is it a merely counter trend inflationary spike within the broader deflationary megatrend? We took a deep dive into six structural forces behind inflation that we identified. Four of those forces were pro-inflationary, while the remaining two were anti-inflationary (Table 1). We also assigned a value on our subjective strength scale for each force. Each value incorporates how quickly a particular force will come to fruition, and how strong it will be over the next 5-to-10 year period. Based on our analysis, we concluded that there are rising odds that the deflationary megatrend has run its course and has reached an inflection point of turning inflationary. Bottom Line: On a structural basis (10-years), it is likely that the deflationary trend is turning. For more details please refer to this Monday’s Special Report.

From Deflation To Eventual Inflation

From Deflation To Eventual Inflation

In the decade following the global financial crisis, investor concerns that the Fed’s monetary policies have artificially boosted equity market valuation have been mostly overblown. But today, it is now true that US equities are increasingly dependent on persistently low bond yields, as stocks can only avoid near bubble-like relative pricing if yields remain below trend rates of economic growth. Macroeconomic theory and the historical record both support the notion that nominal interest rates are normally in equilibrium when they are roughly equal to the trend rate of nominal income growth. A gap between interest rates and trend rates of growth was indeed justified for a few years following the global financial crisis, but in the few years prior to the pandemic, it is altogether possible that the neutral rate of interest (or “r-star”) was in fact meaningfully higher than academic estimates suggested. In a scenario where the US output gap closes quickly, inflation rises above target, and where permanent damage to the labor market from the pandemic is relatively limited, we expect the narrative of secular stagnation to be challenged and for investor expectations for the neutral rate to move closer to trend rates of economic growth. That would imply that the 5-year/5-year forward Treasury yield could hypothetically rise above 3%, and possibly as high as 4% or more. Such a shift would push the US equity risk premium back to 2002 levels based on current stock market pricing. This is not necessarily negative for equities, but it is also not clear what equity risk premium investors will require to contend with the myriad risks to the economic outlook that did not exist in the early 2000s. A low ERP that is technically not as low as that of the tech bubble era could thus still threaten stock prices, as T.I.N.A., “There Is No Alternative,” may not prevail. Many investors have questioned what asset allocation strategy should be pursued in a scenario where stock prices and bond yields are no longer positively correlated. While they are not likely to be without cost, options exist for investors to potentially earn positive absolute returns in a scenario where a significant shift in the interest rate outlook threatens both stock and bond prices. Chart II-1Equity Valuation Concerns Have Persisted For The Past Decade...

Equity Valuation Concerns Have Persisted For The Past Decade...

Equity Valuation Concerns Have Persisted For The Past Decade...

For the better part of the last decade, many investors have argued that the Fed’s monetary policies have artificially boosted equity market valuation. Based on the cyclically-adjusted P/E ratio metric originated by Robert Shiller, stocks reached pre-global financial crisis (GFC) multiples in late 2014 and early 2015 (Chart II-1). Based on metrics such as the price-to-sales ratio, stocks rose to pre-GFC valuation in late 2013, and are now even more richly valued than they were at the height of the dotcom bubble. These concerns have mostly occurred in response to absolute changes in stock multiples, but equity valuation cannot be divorced from the prevailing level of interest rates. Relative to bond yields, stocks were extraordinarily cheap for many years following the GFC. Measured by one simple approach to calculating the equity risk premium, the spread between the 12-month forward earnings yield (the inverse of the forward P/E ratio) and the real 10-year Treasury yield, stocks were the cheapest following the GFC that they had been since the mid 1980s, and remain reasonably priced today (Chart II-2). Chart II-2...But Stocks Have Actually Been Cheap Versus Bonds

...But Stocks Have Actually Been Cheap Versus Bonds

...But Stocks Have Actually Been Cheap Versus Bonds

The fact that stocks have appeared to be expensive for several years but quite cheap (or reasonably priced) relative to bonds underscores the fact that longer-term bond yields have been extraordinarily low following the global financial crisis. Still, equities were not dependent on low bond yields prior to the pandemic, as illustrated in Chart II-3. The chart highlights the range of 10-year Treasury yields that would be consistent with the pre-GFC equity risk premium range (measured from 2002-2007), alongside the actual 10-year yield and trend nominal GDP growth. The chart shows that for years following the financial crisis, bond yields could have risen to levels well above trend rates of economic growth and stocks would still have been priced in line with pre-crisis norms. This “normal pricing” range for the 10-year declined as the expansion continued, but remained consistent with trend growth rates and above the actual 10-year yield up until the beginning of the pandemic. Chart II-3 also highlights, however, that the circumstances changed last year. The equity risk premium briefly rose at the onset of the pandemic as stocks initially sold off sharply, but then quickly fell as stock prices recovered in response to aggressive fiscal and monetary easing. Today, it is true that US equities are increasingly dependent on persistently low bond yields, as stocks can only avoid bubble-like relative pricing if yields remain below trend rates of economic growth. Chart II-3Now, Stocks Are Increasingly Dependent On Low Bond Yields

Now, Stocks Are Increasingly Dependent On Low Bond Yields

Now, Stocks Are Increasingly Dependent On Low Bond Yields

Prior to the pandemic, most fixed-income investors would have viewed the risk of bond yields rising to trend nominal GDP growth, let alone above it, as minimal. Global investors have come to accept the secular stagnation narrative as described by Larry Summers in November 2013, and have gravitated to academic estimates of the neutral rate of interest (“R-star”) that show a substantial gap between the natural rate and trend real growth (Chart II-4). This view has manifested itself in a decline in surveyed estimates of the long-run Fed funds rate, but at present the 5-year/5-year forward Treasury yield has pushed well above this survey-derived fair value range (Chart II-5). It is possible that the fiscal response to the pandemic will cause investor views about r-star to evolve even further over the coming 12-24 months, and in this report we explore the potential headwind that such an evolution could present to stock prices at some point – potentially as early as next year. Chart II-4Investors Have Accepted Secular Stagnation, And The View That R-star Is Well Below Trend Rates Of Growth

Investors Have Accepted Secular Stagnation, And The View That R-star Is Well Below Trend Rates Of Growth

Investors Have Accepted Secular Stagnation, And The View That R-star Is Well Below Trend Rates Of Growth

Chart II-5The Market's Views About R-star May Be Shifting

The Market's Views About R-star May Be Shifting

The Market's Views About R-star May Be Shifting

R-star: A Brief Primer Macroeconomic theory and the historical record both support the notion that nominal interest rates are normally in equilibrium when they are roughly equal to the trend rate of nominal income growth. From the perspective of macro theory, the neutral rate of interest is determined by the supply of and demand for savings. But in practical terms, this implies that the neutral rate should normally be closely linked to the trend rate of economic growth. For example, if interest rates – and thus the cost of capital – were persistently below aggregate income growth, then demand for capital (and thus credit and likely labor demand) should increase as firms seek to profit from the gap between the interest rate and the expected rate of return from real investment. As such, the trend rate of growth acts as a good proxy for the interest rate that will balance the supply and demand for credit during normal economic circumstances. Empirically, academic estimates of r-star closely followed estimates of trend real GDP growth prior to the global financial crisis, as shown in Chart II-4 above. In addition, we noted in our January report that the stance of monetary policy, as defined by the difference between nominal GDP growth and the 10-year Treasury yield, has generally done a good job of explaining the US output gap prior to 2000. This supports the notion that monetary policy is stimulative (restrictive) when bond yields are below (above) trend growth rates. However, in the years following the GFC, investors’ estimates of r-star collapsed, as evidenced by the sharp decline in 5-year / 5-year forward Treasury yields (Chart II-6). This was followed by a decline in primary dealer and FOMC expectations for the long-term Fed funds rate, which investors took as validating their view that the neutral rate of interest has permanently declined. Chart II-6Investors Led The Fed And Others In Expecting A Lower Nominal Neutral Rate

Investors Led The Fed And Others In Expecting A Lower Nominal Neutral Rate

Investors Led The Fed And Others In Expecting A Lower Nominal Neutral Rate

R-star And Trend Growth: Is A Gap Between The Two Really Justified? Chart II-7R-star Likely Did Decline Following The GFC (For A Time)

R-star Likely Did Decline Following The GFC (For A Time)

R-star Likely Did Decline Following The GFC (For A Time)

It seems clear that r-star did indeed decline for a time after the GFC. The US and select European economies suffered a balance sheet recession in 2008/2009 that impacted credit demand for an extended period of time (Chart II-7), and extraordinarily low interest rates for several years did not fuel major credit excesses (at least in the household sector). But as we detailed in a Special Report last year,1 we doubt that the decline in r-star was permanent, for several reasons. The first, and most important, is that there have been at least four deeply impactful non-monetary shocks to both the US and global economies since 2008 that magnified the impact of prolonged household deleveraging and help explain the disconnect between growth and interest rates during the last economic cycle: The euro area sovereign debt crisis Premature fiscal austerity in the US, the UK, and euro area from 2010 – 2012/2014 The US dollar / oil price shock of 2014 The Trump administration’s aggressive use of tariffs beginning in 2018, impacting China but also other developed market economies. Chart II-8Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low

Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low

Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low

Except for the oil price shock of 2014 (which was driven by technological developments and a price war among producers), all of these non-monetary shocks were caused or exacerbated by policymakers – often for political reasons or due to regulatory failures. Second, the trend in US private sector credit growth last cycle does not suggest that r-star fell permanently. Chart II-8 underscores two points: the first is that while US household sector credit contracted for several years following the global financial crisis, it started growing again in 2013 and had largely closed the gap with income growth prior to the pandemic. The second point is that the nonfinancial corporate sector clearly leveraged itself over the course of the last expansion, arguing that interest rates have not in any way been restrictive for businesses. Third, we disagree with a common view in the marketplace that the 2018-2019 period supported the validity of low academic estimates of the neutral rate. Chart II-9 highlights that monetary policy ceased to be stimulative in 2019 according to the Laubach & Williams r-star estimate, which some investors have argued explains the late 2018 equity market selloff, the 2019 slowdown in the US housing market, the inversion of the yield curve, and the global manufacturing recession. Chart II-9Monetary Policy Ceased To Be Stimulative In 2019, According To The LW R-star Estimate

Monetary Policy Ceased To Be Stimulative In 2019, According To The LW R-star Estimate

Monetary Policy Ceased To Be Stimulative In 2019, According To The LW R-star Estimate

But this narrative ignores other important factors that contributed to the slowdown. For example, Chart II-10 highlights that this period of economic weakness exactly coincided with the most intense phase of the Sino-US trade war, as well as a significant slowdown in Chinese credit growth. The chart highlights that the selloff in the US equity market began almost immediately after a surge in the effective tariff rates levied by the two countries against each other, and after the Chinese credit impulse fell three percentage points (from 30% to 27% of GDP). Chart II-10The 2018 Stock Market Selloff Occurred Once Sino-US Tariffs Exploded

The 2018 Stock Market Selloff Occurred Once Sino-US Tariffs Exploded

The 2018 Stock Market Selloff Occurred Once Sino-US Tariffs Exploded

Chart II-11 highlights that interest rates did likely impact the housing market, but that it was the speed at which rates rose that was damaging rather than their level. The chart shows that the rise in mortgage rates from late 2016 to late 2018 was among the largest 2-year increases that has occurred since the early 1980s, so it is unsurprising that the growth in home sales and real residential investment slowed for a time. Additionally, Chart II-12 highlights that the rise in mortgage rates during this period did not cause a downtrend in mortgage credit growth, which only occurred in Q4 2018 in response to the impact of the sharp selloff in the equity market on household net worth. Chart II-11Mortgage Rates Rose Very Significantly From Late 2016 To Late 2018

Mortgage Rates Rose Very Significantly From Late 2016 To Late 2018

Mortgage Rates Rose Very Significantly From Late 2016 To Late 2018

Chart II-12A Record Rise In Mortgage Rates Did Not Crack The Housing Market

A Record Rise In Mortgage Rates Did Not Crack The Housing Market

A Record Rise In Mortgage Rates Did Not Crack The Housing Market

In short, the late 2018 / 2019 period saw a major global aggregate demand shock occur following an already-established slowdown in Chinese credit growth and a rapid rise in interest rates in the DM world. It is these factors that were likely responsible for the 2019 slowdown in economic growth, not the fact that interest rates reached levels that restricted economic activity on their own. R-star In A Post-Pandemic World Charts II-7 – II-12 above suggest that a gap between interest rates and trend rates of growth was indeed justified for a few years following the global financial crisis, but that a decline in r-star only appeared to be permanent due to persistent, non-monetary policy shocks to aggregate demand. In the few years prior to the pandemic, it is altogether possible that r-star was in fact meaningfully higher than academic estimates suggested. But that is now a counterfactual assertion, as the pandemic has transformed the outlook for interest rates and bond yields in conflicting ways. A 10% decline in the level of real output was the most intensely negative non-monetary shock to aggregate demand since the 1930s (Chart II-13), and we agree that another depression would have occurred without extraordinary government assistance. The economic damage caused by the pandemic certainly does not work in favor of a higher neutral rate, and we highlighted in Section 1 of our report that the Fed expects there to be some lingering and persistent slack in the labor market even once the pandemic is over. Chart II-13Without Major Monetary And Fiscal Policy Support, The Pandemic Would Probably Have Caused A Depression

Without Major Monetary And Fiscal Policy Support, The Pandemic Would Probably Have Caused A Depression

Without Major Monetary And Fiscal Policy Support, The Pandemic Would Probably Have Caused A Depression

Chart II-14A Huge Increase In Government Transfers And Spending Is Underway

April 2021

April 2021

On the other hand, Larry Summers, the chief proponent of the theory of secular stagnation, has argued for several years that increased fiscal spending was warranted in order to address an imbalance between private sector savings and investment. Summers himself now characterizes US fiscal policy as the “least responsible” that he has seen over the past 40 years, because of too-large government spending that risks overheating the economy (Chart II-14). Summers’ critique rests in large part on the fact that new government spending has not occurred in the form of investment (to balance out the existence of excess savings), but is instead providing transfers to households that in many cases have already accumulated significant excess savings. But the key point for investors is that the pandemic has completely shifted the narrative about fiscal spending, from “arguably insufficient for several years following the global financial crisis” to now “risking a dramatic overheating of the economy.” Some elements of Summers’ criticism of the Biden administration’s fiscal policy are justified, particularly the policy of large direct transfer payments to workers who have suffered no loss in employment or income as a result of the pandemic. Despite this, as detailed in Section 1 of our report, we are more sanguine about the risks of aggressive overheating for three reasons: it does seem likely that some portion of the spending on services that has been “missing” over the past year will never return or will be slow to return, some of the excess savings that have accumulated will not be immediately (or ever) spent, and the rise in consumer inflation expectations that has occurred over the past year has happened from an extremely low starting point and has yet to even rise above its post-GFC range. The low odds that we assign to dangerously above-target inflation over the coming 12-24 months does not, however, mean that investors’ expectations for r-star will stay low. For right or for wrong, the US government has aggressively dis-saved over the past year, in an environment where low expectations for the neutral rate were anchored by a view of excessive private sector savings and insufficient demand from governments. In a scenario where the US output gap closes quickly, inflation rises modestly above target, and where permanent damage to the labor market from the pandemic is relatively limited, it seems reasonable to conclude that the narrative of secular stagnation will be challenged and that investor expectations for the neutral rate will converge towards trend rates of economic growth. That would imply that the 5-year/5-year forward Treasury yield could hypothetically rise above 3%, possibly as high as 4% or more. This is not our base case view, but it will be an important possibility to monitor as the decisive end to social distancing and other pandemic control measures draws nearer. Investment Conclusions A rise in the 5-year/5-year forward Treasury yield does not, in and of itself, suggest that 10-year Treasury yields will rise to levels that would threaten a significant decline in stock prices. The Fed does not control the long-end of the Treasury curve, but it does exert a very strong influence on the short-end. For example, were the Fed to follow the median current projection of FOMC participants and refrain from raising interest rates until sometime after 2023, it would limit how high current 10-year Treasury yields could rise. But it is not difficult to envision plausible scenarios where the 10-year Treasury yield rises above the range consistent with the pre-GFC US equity risk premium. Chart II-15 presents three hypothetical fair value paths for the 10-year yield assuming a mid-2022 liftoff date and a 4% terminal Fed funds rate for the following three scenarios: Chart II-1510-Year Yields Could Rise Meaningfully Further If Investors Shift Their Expectations For R-star

10-Year Yields Could Rise Meaningfully Further If Investors Shift Their Expectations For R-star

10-Year Yields Could Rise Meaningfully Further If Investors Shift Their Expectations For R-star

The Fed raises rates at a pace of 1% (4 hikes) per year, with a term premium of 10 basis points The Fed raises rates at a pace of 1% (4 hikes) per year, with a term premium of 50 basis points The Fed raises rates at a pace of 1.5% (6 hikes) per year, with a term premium of 50 basis points In the first scenario, based on the current US 12-month forward P/E ratio, the fair value of the 10-year Treasury yield would rise above the range consistent with a reasonable ERP in the middle of 2022, the liftoff point assumed in all three scenarios. In the second and third scenarios, the US equity ERP would already be quite low. When using the late 1999 / early 2000 bubble period as a reference point, even the scenarios shown in Chart II-15 are not very threatening to stock prices. Given current equity market pricing, the third scenario would take the US equity risk premium back to mid 2002 levels, which were still meaningfully higher than during the peak of the bubble. And that is assuming an earlier liftoff than the market currently expects, a faster pace of rate hikes than experienced during the last economic cycle, and a very meaningful increase in the market’s expectations for the neutral rate. But it is not clear what equity risk premium investors will require to contend with the myriad risks to the economic outlook that did not exist in the early 2000s. For example, equity investors are today faced with a riskier policy environment than existed 20 years ago in the US and in other developed economies that is at least partially driven by populist sentiment, potentially impacting earnings via lower operating margins or higher taxes. These or other risks existed at several points over the past decade and T.I.N.A. (“There Is No Alternative”) prevailed, but that occurred precisely because the equity risk premium was very elevated. A low ERP that is technically not as low as what prevailed during the tech bubble era could thus still threaten stock prices, raising the specter of negative absolute returns from stocks and nominal government bonds for a period of time, beginning potentially at or in the lead-up to the first Fed rate hike. Chart II-16There Are Alternatives To A Traditional 60/40 Portfolio In A Rising Rate Environment

There Are Alternatives To A Traditional 60/40 Portfolio In A Rising Rate Environment

There Are Alternatives To A Traditional 60/40 Portfolio In A Rising Rate Environment

Many investors have questioned what asset allocation strategy should be pursued in a scenario where stock prices and bond yields are no longer positively correlated. Chart II-16 provides some perspective on the question, by comparing the total return of a 60/40 stock/bond portfolio to a strategy involving the opportunistic redeployment of cash into stocks. The strategy rule maintains a 50/50 stock/cash allocation during normal market conditions, but it then shifts the entire cash allocation into equities following a 15% selloff in the stock market. The portfolio is shifted back to a 50/50 allocation once stocks rise to a new rolling 1-year high. The chart highlights that 60/40 balanced portfolio-style returns may be achievable with cash as the diversifier without a significant reduction in the Sharpe ratio. In fact, the strategy has the effect of lowering average volatility due to prolonged periods of comparatively lower equity exposure, although this occurs at the cost of higher volatility during periods of high market stress (precisely when investors most want protection from volatility). But the bottom line for investors is that while they are not likely to be without cost, options exist for investors to potentially earn positive absolute returns in a scenario where a significant shift in the interest rate outlook threatens both stock and bond prices. As noted above, this remains a risk to our view rather than our expectation, but we will continue to monitor the potential threat posed to stock prices as the pandemic draws to a decisive close later this year. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Footnotes 1 2020-03-20 GIS SR “Revisiting The Neutral Rate Of Interest: A Contrarian View In A Time Of Crisis.”

Highlights Extremely accommodative fiscal policy and a rapid pace of vaccination puts the US on track to close its output gap by the end of the year. The situation is different in Europe, and the euro area economy will likely continue to underperform the US until at least the summer. Investors are now unusually more hawkish than the Fed, whose caution is driven by the expectation of some lingering and persistent slack in the labor market even once the pandemic is over. The Fed’s rate projections, coupled with the extraordinary size of the American Rescue Plan, have stoked investor concerns about a significant rise in inflation. For inflation to rise dangerously above the Fed’s target, the US would likely need to see a persistently strong and positive output gap, and/or a major upward shift in expectations among consumers and firms. We expect a meaningful recovery in inflation this year, perhaps to above-target levels even without factoring in transitory supply-chain effects, but probably not to levels that investors deem to be “out of control.” Over the coming 6 to 12 months, a comparatively sanguine perspective on inflation supports a bullish view on stocks and an overweight stance towards equities within a multi-asset portfolio. We recommend that investors maintain below-benchmark portfolio duration, and overweight US speculative over investment-grade corporate bonds. The fact that Europe may lag growth-wise for a few months could continue to impact regional equity performance as well as the trend in the dollar over the coming 0-3 months. But over a 6-12 month time horizon, we continue to favor global ex-US vs. US stocks, and expect the dollar to be lower than it is today. A Brighter Light At The End Of The Tunnel Chart I-1Even Better Than Some Optimists Would Have Predicted

Even Better Than Some Optimists Would Have Predicted

Even Better Than Some Optimists Would Have Predicted

Over the past 4-6 weeks, the US has continued to make incredible progress in vaccinating its population against COVID-19. Chart I-1 highlights that the pace of vaccination is now well within the range required for herd immunity to be in place by the end of the third quarter. If this pace continues at an average of 2.5 million doses per day, the US will have vaccinated 90% of its population by the end of September (if it is determined that the vaccine is safe to give to children). And these calculations assume the continuation of a two-dose regime, meaning that the eventual rollout of Johnson & Johnson's Janssen vaccine – which requires only one dose and has shown to be extremely effective at preventing severe illness and death – could shorten the time to herd immunity rates of vaccination among adults even further. The situation is clearly different in Europe. The vaccination progress in several European countries is woefully behind that of the US and the UK (Chart I-2), and per capita cases in the euro area have again risen significantly above that of the US (Chart I-3). This reality motivated last week’s news that the European Union is reportedly planning on banning exports of the AstraZeneca vaccine for a period of time, as European policymakers grow increasingly concerned about the potential economic consequences of lengthened or additional pandemic control measures over the coming few months. Chart I-2Europe Is Badly Lagging The Vaccine Race…

April 2021

April 2021

There was at least some positive economic news from Europe this month, as reflected by the flash manufacturing and services PMIs (Chart I-4). The euro area manufacturing PMI surpassed that of the US this month, reflecting that the prospects for goods-producing companies in Europe remain solidly linked to the strong global manufacturing cycle. Services, on the other hand, have been the weak spot in Europe, having remained below the boom/bust line since last summer (in contrast to the US). The March services PMI highlighted that this gap is now starting to narrow, although the euro area economy will likely continue to underperform the US until at least the summer. Chart I-3...And It Is Starting To Show

...And It Is Starting To Show

...And It Is Starting To Show

Chart I-4Some Closure Of The Services Gap, But Still A Ways To Go

Some Closure Of The Services Gap, But Still A Ways To Go

Some Closure Of The Services Gap, But Still A Ways To Go

The underperformance of the European services sector over the past nine months has been due in part to more severe pandemic control measures, but also a comparatively timid fiscal policy. The IMF’s October Fiscal Monitor highlighted that the US had provided roughly eight percentage points more of GDP in above-the-line fiscal measures versus the European Union as a whole, and that was before the US December 2020 relief bill and this month’s $1.9 trillion American Rescue Plan (ARP) act were passed. The CBO estimates that the ARP will result in about US$1 trillion in outlays in 2021, which is roughly 5% of nominal GDP. Consequently, Chart I-5 highlights that consensus expectations now suggest that the output gap will be marginally positive by the end of the year, with the Fed’s most recent forecast implying that real GDP will be more than 1% above the CBO’s estimate of potential output. Chart I-5The US Output Gap Will Likely Be Closed By The End Of This Year

The US Output Gap Will Likely Be Closed By The End Of This Year

The US Output Gap Will Likely Be Closed By The End Of This Year

The Fed Versus The Market Despite this, the Fed held pat during this month’s FOMC meeting and did not validate market expectations of rate hikes beginning in early 2023. Chart I-6 highlights the Fed funds rate path over the coming years as implied by the OIS curve, alongside the Fed’s median projection of the Fed funds rate. This means that investors are now more hawkish than the Fed, which is the opposite of what has typically prevailed since the global financial crisis. Chart I-6The Market Is Now, Unusually, More Hawkish Than The Fed

The Market Is Now, Unusually, More Hawkish Than The Fed

The Market Is Now, Unusually, More Hawkish Than The Fed

Fed Chair Jerome Powell implied during the March 17 press conference that some FOMC participants were unwilling to change their projections for the path of interest rates based purely on a forecast, which argues that the median dot in the Fed’s “dot plot” will shift higher in the second half of the year if participants’ growth and inflation forecasts come to fruition. But Charts I-7A and I-7B suggest that the Fed’s caution is also driven by the expectation of some lingering and persistent slack in the labor market even once the pandemic is over. Chart I-7AA Positive Output Gap Implies…

April 2021

April 2021

Chart I-7B…An Unemployment Rate Below NAIRU

April 2021

April 2021

The charts highlight the historical relationship between the output gap and the deviation of NAIRU from the unemployment rate, from 2000 and 2010. In both cases, the charts show that the unemployment rate would be below the CBO’s estimate of NAIRU at the end of this year (roughly 4.5%) given the CBO’s estimate for potential (i.e. full employment) GDP and the Fed's forecast for growth. However, the Fed is forecasting that the unemployment rate will essentially be at NAIRU, which is itself above the Fed’s longer-run unemployment rate projection of 4%. As such, the Fed does not see the unemployment rate falling to “full employment” levels this year, a precondition for the onset of rate normalization. Investors should note that the relationships shown in Charts I-7A and I-7B suggest that the unemployment rate will be closer to 3-3.5% at the end of this year if the Fed’s growth forecast is correct, which would constitute full employment based on the Fed’s 4% unemployment rate target. The difference between a 3-3.5% unemployment rate and the Fed’s estimate of 4.5% translates to a gap of roughly 1.5-2.5 million jobs at the end of this year, which underscores that the Fed expects either a significant shift in temporary to permanent unemployment or an influx of unemployed workers back into the labor force who don’t quickly find jobs once social distancing ends and pandemic restrictions are no longer required. Chart I-8The Full Employment Level Of GDP Has Not Been Significantly Revised

The Full Employment Level Of GDP Has Not Been Significantly Revised

The Full Employment Level Of GDP Has Not Been Significantly Revised

There are three possible circumstances that would resolve this seeming contradiction. The first is that the Fed’s estimate for growth this year is simply too high, and that the output gap will be close to zero at the end of the year (i.e., more in line with consensus market expectations). The second is that the CBO is understating the level of GDP that is consistent with full employment, namely that potential GDP is higher than what they currently project. But Chart I-8 shows that the CBO’s current estimate for potential output at the end of this year is only 0.4% below what it had estimated prior to the pandemic, which is smaller than the positive gap implied by the Fed’s growth estimate for this year (roughly 1.2%). The third possibility is that the Fed is overestimating the extent to which the pandemic will cause permanent damage to the labor market. As we noted in our February report, even once social distancing is no longer required, it does seem likely that some portion of the spending on services that has been “missing” over the past year will never return. While it seems reasonable to expect that the gap in spending on hospitality and travel will close quickly once the health situation allows, it also seems reasonable to expect that some service areas, particularly retail, will experience a permanent loss in demand owing to durable shifts in consumer behavior that occurred during the pandemic (greater familiarity and use of online shopping, a permanent reduction of some magnitude in commuting, etc). A gap of 1.5-2.5 million jobs accounts for roughly 10-15% of pre-pandemic employment in retail trade, or 4-7% of the sum of retail trade, leisure & hospitality, and other services. It is possible that permanent job losses or significantly deferred job recovery of this size will occur, but it is far from clear that it will. Were job losses / deferred jobs recovery of this magnitude to not materialize, it would suggest that the US will reach full employment earlier than the Fed is currently projecting, and would significantly increase the odds that the Fed will begin to taper its asset purchases and/or raise interest rates at some point next year – which is earlier than investors currently expect. For Now, Dangerously Above-Target Inflation Is Unlikely Fed projections of a 0% Fed funds rate for the next 2 1/2 years, coupled with the extraordinary size of the American Rescue Plan, have understandably stoked investor concerns about a significant rise in inflation. Larry Summers’ recent interview with Bloomberg was emblematic of the concern, during which he criticized the Biden administration’s fiscal policy as the “least responsible” that the US has experienced in four decades and warned of the potential inflationary consequences of overheating the economy.1 It is true that the Federal Reserve is explicitly aiming to generate a temporary overshoot of inflation relative to its target, the Biden administration’s fiscal plan is legitimately large, and there is a tremendous pool of excess savings that could be deployed later this year once the pandemic is essentially over. Clearly, the risks of overheating must be higher than they have been in the past. But from our perspective, out-of-control inflation over the coming 12-24 months would very likely necessitate one of two things to occur, and possibly both: US consumers decide to spend an overwhelmingly large amount of the excess savings that have been accumulated. Main street expectations for consumer prices rise sharply, prompted by a public discussion about the likelihood of a shifting inflation regime. Our view is rooted in the examination of the modern-day Phillips Curve that we presented in our January report, which considers both the impact of economic/labor market slack and inflation expectations as a driver of actual inflation. The modern-day Phillips Curve posits that expectations act as the trend for inflation, and slack in the economy determines whether actual inflation is above or below that baseline. Chart I-9 highlights that the output gap worked well prior to the global financial crisis at explaining the difference between actual and exponentially-smoothed inflation, the latter acting as a long-history proxy for expectations. Pre-GFC, the chart highlights that there have been only two exceptions to the relationship that concerned the magnitude rather than the direction of inflation. Post-GFC, the relationship deviated substantially, but in a way that implied that actual inflation was too strong during the last expansion, not too weak – particularly during the early phase of the economic recovery. This likely occurred because expectations initially stayed very well anchored due to the Fed’s strong record of maintaining low and stable inflation, but ultimately declined due to a persistently negative output gap as well as in response to the 2014 collapse in oil prices (Chart I-10). Chart I-9Pre-GFC, The Output Gap Generally Explained Inflation Surprises

Pre-GFC, The Output Gap Generally Explained Inflation Surprises

Pre-GFC, The Output Gap Generally Explained Inflation Surprises

Chart I-10Inflation Expectations Eventually Succumbed Post-GFC To Collapsing Energy Prices

Inflation Expectations Eventually Succumbed Post-GFC To Collapsing Energy Prices

Inflation Expectations Eventually Succumbed Post-GFC To Collapsing Energy Prices

Thus, for inflation to rise dangerously above the Fed’s target, the US would likely need to see a persistently strong and positive output gap, and/or a major upward shift in expectations among consumers and firms. Chart I-11 highlights that the amount of excess savings that have accumulated as a percentage of GDP does indeed significantly exceed the magnitude of the output gap, but some of those savings have been and will be invested in financial markets (boosting valuation), some will be used to pay down debt, some will eventually be spent on international travel (boosting services imports), and some will likely be permanently held as deposits in anticipation of future tax increases. And while long-term household expectations for prices have risen since the passing of the CARES act last year, the rise has merely unwound the decline that took place following the 2014 oil price collapse (Chart I-12). Chart I-11A Huge Pool Of Savings Exists, But Not All Of It Will Be Spent

A Huge Pool Of Savings Exists, But Not All Of It Will Be Spent

A Huge Pool Of Savings Exists, But Not All Of It Will Be Spent

Chart I-12Long-Term Consumer Inflation Expectations Have Risen From A Very Low Base

Long-Term Consumer Inflation Expectations Have Risen From A Very Low Base

Long-Term Consumer Inflation Expectations Have Risen From A Very Low Base

For now, this framework points to a meaningful recovery in inflation this year, perhaps to above-target levels even without factoring in transitory supply-chain effects, but probably not to levels that investors deem to be “out of control.” Investment Conclusions Over the coming 6 to 12 months, a comparatively sanguine perspective on inflation supports a bullish view on stocks and an overweight stance towards equities within a multi-asset portfolio. While the Fed is likely to shift in a hawkish direction compared with its current projections, it is highly unlikely to become meaningfully more hawkish than current market expectations unless economic growth and the recovery in the labor market is much stronger than the Fed or the market is projecting. In fact, even if the market’s expectations for the first Fed rate hike shift to mid-2022 over the coming several months, Chart I-13 highlights that the impact on the equity market is likely to be minimal unless investors shift up their expectations for the terminal Fed funds rate. The chart presents a fair value estimate for the 10-year Treasury yield based on the OIS-implied path of the Fed funds rate out to December 2024, and assumes that short rates ultimately rise to the Fed’s long-term Fed funds rate projection of 2.5%. The second fair value series assumes that the shape of the OIS curve stays the same, but shifts closer by 6 months. Chart I-13The Market’s Assumed Rate Hike Path And Terminal Rate Are Not Threatening For Stocks

April 2021

April 2021

The chart underscores that the 10-year yield will rise to at most between 2-2.2% by the end of the year based on these scenarios. A shift forward in the timing of Fed rate hikes will impact the short end of the curve, but the long end will remain relatively unchanged if terminal rate expectations stay constant and the term premium on long-term bonds remains near zero. These levels would in no way be economically damaging nor threatening to stock market valuation. It is possible, however, that investor expectations for the neutral rate of interest (“r-star”) will shift higher once the pandemic is over, and we explore this risk to stocks in Section 2 of our report. For now, this remains a risk to our view rather than our expectation, but it is likely to remain an important possibility to monitor as the decisive end to social distancing and other pandemic control measures draws nearer. Within fixed income, we recommend that investors maintain below-benchmark portfolio duration even though investors are already pricing in a more hawkish path for the Fed funds rate. First, Chart I-13 highlighted that yields at the long end of the curve are likely to continue to move modestly higher this year even if the projected path for the Fed funds rate remains relatively unchanged. But more importantly, barring a substantially negative development on the health or vaccine front that prolongs the pandemic, the risk appears to be clearly to the upside in terms of the timing of the first Fed rate hike and the terminal Fed funds rate. As such, from a risk-reward perspective, a long duration stance remains unattractive. We would also recommend overweighting US speculative over investment-grade corporate bonds, as spreads are not as historically depressed for the former than the latter (Chart I-14). Finally, in terms of the dimensions of equity market performance and the dollar, we recommend that investors overweight global ex-US equities vs. the US, overweight value vs. growth, overweight cyclicals vs. defensives, and overweight small vs. large caps. We are also bearish on the dollar on a 12-month time horizon. However, there are two caveats that investors should bear in mind. First, global cyclicals versus defensives (especially in equally-weighted terms) as well as small versus large caps have already mostly normalized not just the impact of the pandemic but as well that of the 2018-2019 Trump trade war (Chart I-15). We would expect, at best, modest further gains from both positions this year. Chart I-14Speculative-Grade Corporate Bonds Are Less Expensive Than Investment-Grade

Speculative-Grade Corporate Bonds Are Less Expensive Than Investment-Grade

Speculative-Grade Corporate Bonds Are Less Expensive Than Investment-Grade

Chart I-15Going Forward, Expect More Modest Gains From Cyclicals And Small Caps

Going Forward, Expect More Modest Gains From Cyclicals And Small Caps

Going Forward, Expect More Modest Gains From Cyclicals And Small Caps

Second, the fact that Europe may lag growth-wise for a few months could continue to impact regional equity performance as well as the trend in the dollar on a 0-3 month time horizon. The US dollar is typically a counter-cyclical currency, but there have been exceptions to that rule. And historically, exceptions have tended to revolve around periods when US growth has been quite strong, as is currently the case (Chart I-16). A continued counter-trend rally in the dollar is thus possible over the course of the next few months, but we would expect USD-EUR to be lower than current levels 12 months from now. Chart I-16A Short-Term Counter-Trend Dollar Move Is Possible

A Short-Term Counter-Trend Dollar Move Is Possible

A Short-Term Counter-Trend Dollar Move Is Possible

A counter-trend dollar move could also correspond with a period of US outperformance versus global ex-US, or at a minimum, a period of flat performance when global ex-US stocks would normally outperform. Our China strategists expect that the Chinese credit impulse will decelerate later this year (Chart I-17), which would weigh on EM stocks and heighten the importance of European equities in driving global ex-US outperformance. European equity outperformance, in turn, will likely necessitate the outperformance of euro area financials. Chart I-18 highlights that euro area equity underperformance versus the US last year was mostly a tech story, but today there is little difference between the relative performance of euro area stocks overall versus indexes that exclude the broadly-defined technology sector. In both cases, the euro area index is roughly 10% below its US counterpart relative to pre-pandemic levels, which exactly matches the extent to which euro area financials have underperformed. Chart I-17A Slowing Chinese Credit Impulse Means EM Equities Will Struggle To Outperform

A Slowing Chinese Credit Impulse Means EM Equities Will Struggle To Outperform

A Slowing Chinese Credit Impulse Means EM Equities Will Struggle To Outperform

Chart I-18Euro Area Financials Need To Outperform For Europe To Outperform

Euro Area Financials Need To Outperform For Europe To Outperform

Euro Area Financials Need To Outperform For Europe To Outperform

Euro area financials have demonstrated very poor fundamental performance over the past decade, but they are likely to outperform for some period once the European vaccination campaign gains enough traction to alter the disease’s transmission and hospitalization dynamics. Chart I-19 highlights that euro area bank 12-month forward earnings have further room to recover to pre-pandemic levels than for banks in the US, and Chart I-20 highlights that euro area banks trade at their deepest price-to-book discount versus their US peers since the euro area financial crisis. Chart I-19Euro Area Bank Earnings Have Catch-Up Potential

Euro Area Bank Earnings Have Catch-Up Potential

Euro Area Bank Earnings Have Catch-Up Potential

Chart I-20Euro Area Banks Are Extremely Cheap Versus The US

Euro Area Banks Are Extremely Cheap Versus The US

Euro Area Banks Are Extremely Cheap Versus The US

Thus, while euro area and global ex-US equities may not outperform on the back of rising global stock prices over the coming few months, investors focused on a 6-12 month time horizon should respond by increasing their allocation to European stocks and to further reduce dollar exposure. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst March 31, 2021 Next Report: April 29, 2021 II. R-star, And The Structural Risk To Stocks In the decade following the global financial crisis, investor concerns that the Fed’s monetary policies have artificially boosted equity market valuation have been mostly overblown. But today, it is now true that US equities are increasingly dependent on persistently low bond yields, as stocks can only avoid near bubble-like relative pricing if yields remain below trend rates of economic growth. Macroeconomic theory and the historical record both support the notion that nominal interest rates are normally in equilibrium when they are roughly equal to the trend rate of nominal income growth. A gap between interest rates and trend rates of growth was indeed justified for a few years following the global financial crisis, but in the few years prior to the pandemic, it is altogether possible that the neutral rate of interest (or “r-star”) was in fact meaningfully higher than academic estimates suggested. In a scenario where the US output gap closes quickly, inflation rises above target, and where permanent damage to the labor market from the pandemic is relatively limited, we expect the narrative of secular stagnation to be challenged and for investor expectations for the neutral rate to move closer to trend rates of economic growth. That would imply that the 5-year/5-year forward Treasury yield could hypothetically rise above 3%, and possibly as high as 4% or more. Such a shift would push the US equity risk premium back to 2002 levels based on current stock market pricing. This is not necessarily negative for equities, but it is also not clear what equity risk premium investors will require to contend with the myriad risks to the economic outlook that did not exist in the early 2000s. A low ERP that is technically not as low as that of the tech bubble era could thus still threaten stock prices, as T.I.N.A., “There Is No Alternative,” may not prevail. Many investors have questioned what asset allocation strategy should be pursued in a scenario where stock prices and bond yields are no longer positively correlated. While they are not likely to be without cost, options exist for investors to potentially earn positive absolute returns in a scenario where a significant shift in the interest rate outlook threatens both stock and bond prices. Chart II-1Equity Valuation Concerns Have Persisted For The Past Decade...

Equity Valuation Concerns Have Persisted For The Past Decade...

Equity Valuation Concerns Have Persisted For The Past Decade...

For the better part of the last decade, many investors have argued that the Fed’s monetary policies have artificially boosted equity market valuation. Based on the cyclically-adjusted P/E ratio metric originated by Robert Shiller, stocks reached pre-global financial crisis (GFC) multiples in late 2014 and early 2015 (Chart II-1). Based on metrics such as the price-to-sales ratio, stocks rose to pre-GFC valuation in late 2013, and are now even more richly valued than they were at the height of the dotcom bubble. These concerns have mostly occurred in response to absolute changes in stock multiples, but equity valuation cannot be divorced from the prevailing level of interest rates. Relative to bond yields, stocks were extraordinarily cheap for many years following the GFC. Measured by one simple approach to calculating the equity risk premium, the spread between the 12-month forward earnings yield (the inverse of the forward P/E ratio) and the real 10-year Treasury yield, stocks were the cheapest following the GFC that they had been since the mid 1980s, and remain reasonably priced today (Chart II-2). Chart II-2...But Stocks Have Actually Been Cheap Versus Bonds

...But Stocks Have Actually Been Cheap Versus Bonds

...But Stocks Have Actually Been Cheap Versus Bonds

The fact that stocks have appeared to be expensive for several years but quite cheap (or reasonably priced) relative to bonds underscores the fact that longer-term bond yields have been extraordinarily low following the global financial crisis. Still, equities were not dependent on low bond yields prior to the pandemic, as illustrated in Chart II-3. The chart highlights the range of 10-year Treasury yields that would be consistent with the pre-GFC equity risk premium range (measured from 2002-2007), alongside the actual 10-year yield and trend nominal GDP growth. The chart shows that for years following the financial crisis, bond yields could have risen to levels well above trend rates of economic growth and stocks would still have been priced in line with pre-crisis norms. This “normal pricing” range for the 10-year declined as the expansion continued, but remained consistent with trend growth rates and above the actual 10-year yield up until the beginning of the pandemic. Chart II-3 also highlights, however, that the circumstances changed last year. The equity risk premium briefly rose at the onset of the pandemic as stocks initially sold off sharply, but then quickly fell as stock prices recovered in response to aggressive fiscal and monetary easing. Today, it is true that US equities are increasingly dependent on persistently low bond yields, as stocks can only avoid bubble-like relative pricing if yields remain below trend rates of economic growth. Chart II-3Now, Stocks Are Increasingly Dependent On Low Bond Yields

Now, Stocks Are Increasingly Dependent On Low Bond Yields

Now, Stocks Are Increasingly Dependent On Low Bond Yields

Prior to the pandemic, most fixed-income investors would have viewed the risk of bond yields rising to trend nominal GDP growth, let alone above it, as minimal. Global investors have come to accept the secular stagnation narrative as described by Larry Summers in November 2013, and have gravitated to academic estimates of the neutral rate of interest (“R-star”) that show a substantial gap between the natural rate and trend real growth (Chart II-4). This view has manifested itself in a decline in surveyed estimates of the long-run Fed funds rate, but at present the 5-year/5-year forward Treasury yield has pushed well above this survey-derived fair value range (Chart II-5). It is possible that the fiscal response to the pandemic will cause investor views about r-star to evolve even further over the coming 12-24 months, and in this report we explore the potential headwind that such an evolution could present to stock prices at some point – potentially as early as next year. Chart II-4Investors Have Accepted Secular Stagnation, And The View That R-star Is Well Below Trend Rates Of Growth

Investors Have Accepted Secular Stagnation, And The View That R-star Is Well Below Trend Rates Of Growth

Investors Have Accepted Secular Stagnation, And The View That R-star Is Well Below Trend Rates Of Growth

Chart II-5The Market's Views About R-star May Be Shifting

The Market's Views About R-star May Be Shifting

The Market's Views About R-star May Be Shifting

R-star: A Brief Primer Macroeconomic theory and the historical record both support the notion that nominal interest rates are normally in equilibrium when they are roughly equal to the trend rate of nominal income growth. From the perspective of macro theory, the neutral rate of interest is determined by the supply of and demand for savings. But in practical terms, this implies that the neutral rate should normally be closely linked to the trend rate of economic growth. For example, if interest rates – and thus the cost of capital – were persistently below aggregate income growth, then demand for capital (and thus credit and likely labor demand) should increase as firms seek to profit from the gap between the interest rate and the expected rate of return from real investment. As such, the trend rate of growth acts as a good proxy for the interest rate that will balance the supply and demand for credit during normal economic circumstances. Empirically, academic estimates of r-star closely followed estimates of trend real GDP growth prior to the global financial crisis, as shown in Chart II-4 above. In addition, we noted in our January report that the stance of monetary policy, as defined by the difference between nominal GDP growth and the 10-year Treasury yield, has generally done a good job of explaining the US output gap prior to 2000. This supports the notion that monetary policy is stimulative (restrictive) when bond yields are below (above) trend growth rates. However, in the years following the GFC, investors’ estimates of r-star collapsed, as evidenced by the sharp decline in 5-year / 5-year forward Treasury yields (Chart II-6). This was followed by a decline in primary dealer and FOMC expectations for the long-term Fed funds rate, which investors took as validating their view that the neutral rate of interest has permanently declined. Chart II-6Investors Led The Fed And Others In Expecting A Lower Nominal Neutral Rate

Investors Led The Fed And Others In Expecting A Lower Nominal Neutral Rate

Investors Led The Fed And Others In Expecting A Lower Nominal Neutral Rate

R-star And Trend Growth: Is A Gap Between The Two Really Justified? Chart II-7R-star Likely Did Decline Following The GFC (For A Time)

R-star Likely Did Decline Following The GFC (For A Time)

R-star Likely Did Decline Following The GFC (For A Time)

It seems clear that r-star did indeed decline for a time after the GFC. The US and select European economies suffered a balance sheet recession in 2008/2009 that impacted credit demand for an extended period of time (Chart II-7), and extraordinarily low interest rates for several years did not fuel major credit excesses (at least in the household sector). But as we detailed in a Special Report last year,2 we doubt that the decline in r-star was permanent, for several reasons. The first, and most important, is that there have been at least four deeply impactful non-monetary shocks to both the US and global economies since 2008 that magnified the impact of prolonged household deleveraging and help explain the disconnect between growth and interest rates during the last economic cycle: The euro area sovereign debt crisis Premature fiscal austerity in the US, the UK, and euro area from 2010 – 2012/2014 The US dollar / oil price shock of 2014 The Trump administration’s aggressive use of tariffs beginning in 2018, impacting China but also other developed market economies. Chart II-8Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low

Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low

Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low

Except for the oil price shock of 2014 (which was driven by technological developments and a price war among producers), all of these non-monetary shocks were caused or exacerbated by policymakers – often for political reasons or due to regulatory failures. Second, the trend in US private sector credit growth last cycle does not suggest that r-star fell permanently. Chart II-8 underscores two points: the first is that while US household sector credit contracted for several years following the global financial crisis, it started growing again in 2013 and had largely closed the gap with income growth prior to the pandemic. The second point is that the nonfinancial corporate sector clearly leveraged itself over the course of the last expansion, arguing that interest rates have not in any way been restrictive for businesses. Third, we disagree with a common view in the marketplace that the 2018-2019 period supported the validity of low academic estimates of the neutral rate. Chart II-9 highlights that monetary policy ceased to be stimulative in 2019 according to the Laubach & Williams r-star estimate, which some investors have argued explains the late 2018 equity market selloff, the 2019 slowdown in the US housing market, the inversion of the yield curve, and the global manufacturing recession. Chart II-9Monetary Policy Ceased To Be Stimulative In 2019, According To The LW R-star Estimate

Monetary Policy Ceased To Be Stimulative In 2019, According To The LW R-star Estimate

Monetary Policy Ceased To Be Stimulative In 2019, According To The LW R-star Estimate

But this narrative ignores other important factors that contributed to the slowdown. For example, Chart II-10 highlights that this period of economic weakness exactly coincided with the most intense phase of the Sino-US trade war, as well as a significant slowdown in Chinese credit growth. The chart highlights that the selloff in the US equity market began almost immediately after a surge in the effective tariff rates levied by the two countries against each other, and after the Chinese credit impulse fell three percentage points (from 30% to 27% of GDP). Chart II-10The 2018 Stock Market Selloff Occurred Once Sino-US Tariffs Exploded

The 2018 Stock Market Selloff Occurred Once Sino-US Tariffs Exploded

The 2018 Stock Market Selloff Occurred Once Sino-US Tariffs Exploded

Chart II-11 highlights that interest rates did likely impact the housing market, but that it was the speed at which rates rose that was damaging rather than their level. The chart shows that the rise in mortgage rates from late 2016 to late 2018 was among the largest 2-year increases that has occurred since the early 1980s, so it is unsurprising that the growth in home sales and real residential investment slowed for a time. Additionally, Chart II-12 highlights that the rise in mortgage rates during this period did not cause a downtrend in mortgage credit growth, which only occurred in Q4 2018 in response to the impact of the sharp selloff in the equity market on household net worth. Chart II-11Mortgage Rates Rose Very Significantly From Late 2016 To Late 2018

Mortgage Rates Rose Very Significantly From Late 2016 To Late 2018

Mortgage Rates Rose Very Significantly From Late 2016 To Late 2018

Chart II-12A Record Rise In Mortgage Rates Did Not Crack The Housing Market

A Record Rise In Mortgage Rates Did Not Crack The Housing Market

A Record Rise In Mortgage Rates Did Not Crack The Housing Market

In short, the late 2018 / 2019 period saw a major global aggregate demand shock occur following an already-established slowdown in Chinese credit growth and a rapid rise in interest rates in the DM world. It is these factors that were likely responsible for the 2019 slowdown in economic growth, not the fact that interest rates reached levels that restricted economic activity on their own. R-star In A Post-Pandemic World Charts II-7 – II-12 above suggest that a gap between interest rates and trend rates of growth was indeed justified for a few years following the global financial crisis, but that a decline in r-star only appeared to be permanent due to persistent, non-monetary policy shocks to aggregate demand. In the few years prior to the pandemic, it is altogether possible that r-star was in fact meaningfully higher than academic estimates suggested. But that is now a counterfactual assertion, as the pandemic has transformed the outlook for interest rates and bond yields in conflicting ways. A 10% decline in the level of real output was the most intensely negative non-monetary shock to aggregate demand since the 1930s (Chart II-13), and we agree that another depression would have occurred without extraordinary government assistance. The economic damage caused by the pandemic certainly does not work in favor of a higher neutral rate, and we highlighted in Section 1 of our report that the Fed expects there to be some lingering and persistent slack in the labor market even once the pandemic is over. Chart II-13Without Major Monetary And Fiscal Policy Support, The Pandemic Would Probably Have Caused A Depression

Without Major Monetary And Fiscal Policy Support, The Pandemic Would Probably Have Caused A Depression

Without Major Monetary And Fiscal Policy Support, The Pandemic Would Probably Have Caused A Depression

Chart II-14A Huge Increase In Government Transfers And Spending Is Underway

April 2021

April 2021

On the other hand, Larry Summers, the chief proponent of the theory of secular stagnation, has argued for several years that increased fiscal spending was warranted in order to address an imbalance between private sector savings and investment. Summers himself now characterizes US fiscal policy as the “least responsible” that he has seen over the past 40 years, because of too-large government spending that risks overheating the economy (Chart II-14). Summers’ critique rests in large part on the fact that new government spending has not occurred in the form of investment (to balance out the existence of excess savings), but is instead providing transfers to households that in many cases have already accumulated significant excess savings. But the key point for investors is that the pandemic has completely shifted the narrative about fiscal spending, from “arguably insufficient for several years following the global financial crisis” to now “risking a dramatic overheating of the economy.” Some elements of Summers’ criticism of the Biden administration’s fiscal policy are justified, particularly the policy of large direct transfer payments to workers who have suffered no loss in employment or income as a result of the pandemic. Despite this, as detailed in Section 1 of our report, we are more sanguine about the risks of aggressive overheating for three reasons: it does seem likely that some portion of the spending on services that has been “missing” over the past year will never return or will be slow to return, some of the excess savings that have accumulated will not be immediately (or ever) spent, and the rise in consumer inflation expectations that has occurred over the past year has happened from an extremely low starting point and has yet to even rise above its post-GFC range. The low odds that we assign to dangerously above-target inflation over the coming 12-24 months does not, however, mean that investors’ expectations for r-star will stay low. For right or for wrong, the US government has aggressively dis-saved over the past year, in an environment where low expectations for the neutral rate were anchored by a view of excessive private sector savings and insufficient demand from governments. In a scenario where the US output gap closes quickly, inflation rises modestly above target, and where permanent damage to the labor market from the pandemic is relatively limited, it seems reasonable to conclude that the narrative of secular stagnation will be challenged and that investor expectations for the neutral rate will converge towards trend rates of economic growth. That would imply that the 5-year/5-year forward Treasury yield could hypothetically rise above 3%, possibly as high as 4% or more. This is not our base case view, but it will be an important possibility to monitor as the decisive end to social distancing and other pandemic control measures draws nearer. Investment Conclusions A rise in the 5-year/5-year forward Treasury yield does not, in and of itself, suggest that 10-year Treasury yields will rise to levels that would threaten a significant decline in stock prices. The Fed does not control the long-end of the Treasury curve, but it does exert a very strong influence on the short-end. For example, were the Fed to follow the median current projection of FOMC participants and refrain from raising interest rates until sometime after 2023, it would limit how high current 10-year Treasury yields could rise. But it is not difficult to envision plausible scenarios where the 10-year Treasury yield rises above the range consistent with the pre-GFC US equity risk premium. Chart II-15 presents three hypothetical fair value paths for the 10-year yield assuming a mid-2022 liftoff date and a 4% terminal Fed funds rate for the following three scenarios: Chart II-1510-Year Yields Could Rise Meaningfully Further If Investors Shift Their Expectations For R-star

10-Year Yields Could Rise Meaningfully Further If Investors Shift Their Expectations For R-star

10-Year Yields Could Rise Meaningfully Further If Investors Shift Their Expectations For R-star

The Fed raises rates at a pace of 1% (4 hikes) per year, with a term premium of 10 basis points The Fed raises rates at a pace of 1% (4 hikes) per year, with a term premium of 50 basis points The Fed raises rates at a pace of 1.5% (6 hikes) per year, with a term premium of 50 basis points In the first scenario, based on the current US 12-month forward P/E ratio, the fair value of the 10-year Treasury yield would rise above the range consistent with a reasonable ERP in the middle of 2022, the liftoff point assumed in all three scenarios. In the second and third scenarios, the US equity ERP would already be quite low. When using the late 1999 / early 2000 bubble period as a reference point, even the scenarios shown in Chart II-15 are not very threatening to stock prices. Given current equity market pricing, the third scenario would take the US equity risk premium back to mid 2002 levels, which were still meaningfully higher than during the peak of the bubble. And that is assuming an earlier liftoff than the market currently expects, a faster pace of rate hikes than experienced during the last economic cycle, and a very meaningful increase in the market’s expectations for the neutral rate. But it is not clear what equity risk premium investors will require to contend with the myriad risks to the economic outlook that did not exist in the early 2000s. For example, equity investors are today faced with a riskier policy environment than existed 20 years ago in the US and in other developed economies that is at least partially driven by populist sentiment, potentially impacting earnings via lower operating margins or higher taxes. These or other risks existed at several points over the past decade and T.I.N.A. (“There Is No Alternative”) prevailed, but that occurred precisely because the equity risk premium was very elevated. A low ERP that is technically not as low as what prevailed during the tech bubble era could thus still threaten stock prices, raising the specter of negative absolute returns from stocks and nominal government bonds for a period of time, beginning potentially at or in the lead-up to the first Fed rate hike. Chart II-16There Are Alternatives To A Traditional 60/40 Portfolio In A Rising Rate Environment

There Are Alternatives To A Traditional 60/40 Portfolio In A Rising Rate Environment

There Are Alternatives To A Traditional 60/40 Portfolio In A Rising Rate Environment

Many investors have questioned what asset allocation strategy should be pursued in a scenario where stock prices and bond yields are no longer positively correlated. Chart II-16 provides some perspective on the question, by comparing the total return of a 60/40 stock/bond portfolio to a strategy involving the opportunistic redeployment of cash into stocks. The strategy rule maintains a 50/50 stock/cash allocation during normal market conditions, but it then shifts the entire cash allocation into equities following a 15% selloff in the stock market. The portfolio is shifted back to a 50/50 allocation once stocks rise to a new rolling 1-year high. The chart highlights that 60/40 balanced portfolio-style returns may be achievable with cash as the diversifier without a significant reduction in the Sharpe ratio. In fact, the strategy has the effect of lowering average volatility due to prolonged periods of comparatively lower equity exposure, although this occurs at the cost of higher volatility during periods of high market stress (precisely when investors most want protection from volatility). But the bottom line for investors is that while they are not likely to be without cost, options exist for investors to potentially earn positive absolute returns in a scenario where a significant shift in the interest rate outlook threatens both stock and bond prices. As noted above, this remains a risk to our view rather than our expectation, but we will continue to monitor the potential threat posed to stock prices as the pandemic draws to a decisive close later this year. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst III. Indicators And Reference Charts BCA’s equity indicators highlight that the “easy” money from expectations of an eventual end to the pandemic have already been made. Our technical, valuation, and sentiment indicators are very extended, highlighting that investors should expect positive but more modest returns from stocks over the coming 6-12 months. Our monetary indicator has aggressively retreated from its high last year, reflecting a meaningful recovery in government bond yields. The indicator remains above the boom/bust line, however, highlighting that monetary policy remains supportive for risky asset prices. Forward equity earnings already price in a complete earnings recovery, but for now there is no meaningful sign of waning forward earnings momentum. Net revisions remain very strong, and positive earnings surprises have ticked slightly lower from their strongest levels on record. Within a global equity portfolio, US stocks have recently risen versus global ex-US, reflecting a countertrend rise in the US dollar and a lagging vaccination campaign in Europe. We expect a deceleration in the Chinese credit impulse later this year, which will weigh on EM stocks and heighten the importance of European equities in driving global ex-US outperformance. European equity outperformance, in turn, will likely necessitate the outperformance of euro area financials. The US 10-Year Treasury yield has risen well above its 200-day moving average. Long-dated yields are technically stretched to the upside, but our valuation index highlights that bonds are still extremely expensive and that yields could move higher over the cyclical investment horizon. The recent bounce in the US dollar has reflected improved relative US growth expectations, but also previously oversold levels. The dollar may continue to strengthen on a 0-3 month time horizon, but we expect it to be lower in 12 months’ time than it is today. Commodity prices have recovered not just back to pre-pandemic levels, but also back to 2014 levels. This underscores that many commodity prices are extended, and may be due for a breather once the Chinese credit impulse begins to decline. US and global LEIs remain in a solid uptrend, and global manufacturing PMIs are strong. This underscores that the global demand for goods is robust, and that output is below pre-pandemic levels in most economies because of very weak services spending. The latter will recover significantly later this year, as social distancing and other pandemic control measures disappear. EQUITIES: Chart III-1US Equity Indicators

US Equity Indicators

US Equity Indicators

Chart III-2Willingness To Pay For Risk

Willingness To Pay For Risk

Willingness To Pay For Risk

Chart III-3US Equity Sentiment Indicators

US Equity Sentiment Indicators

US Equity Sentiment Indicators

Chart III-4Revealed Preference Indicator

Revealed Preference Indicator

Revealed Preference Indicator

Chart III-5US Stock Market Valuation

US Stock Market Valuation

US Stock Market Valuation

Chart III-6US Earnings

US Earnings

US Earnings

Chart III-7Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Chart III-8Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

FIXED INCOME: Chart III-9US Treasurys And Valuations

US Treasurys And Valuations

US Treasurys And Valuations

Chart III-10Yield Curve Slopes

Yield Curve Slopes

Yield Curve Slopes

Chart III-11Selected US Bond Yields

Selected US Bond Yields

Selected US Bond Yields

Chart III-1210-Year Treasury Yield Components

10-Year Treasury Yield Components

10-Year Treasury Yield Components

Chart III-13US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

Chart III-14Global Bonds: Developed Markets

Global Bonds: Developed Markets

Global Bonds: Developed Markets

Chart III-15Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

CURRENCIES: Chart III-16US Dollar And PPP

US Dollar And PPP

US Dollar And PPP

Chart III-17US Dollar And Indicator

US Dollar And Indicator

US Dollar And Indicator

Chart III-18US Dollar Fundamentals

US Dollar Fundamentals

US Dollar Fundamentals

Chart III-19Japanese Yen Technicals

Japanese Yen Technicals

Japanese Yen Technicals

Chart III-20Euro Technicals

Euro Technicals

Euro Technicals

Chart III-21Euro/Yen Technicals

Euro/Yen Technicals

Euro/Yen Technicals

Chart III-22Euro/Pound Technicals

Euro/Pound Technicals

Euro/Pound Technicals

COMMODITIES: Chart III-23Broad Commodity Indicators

Broad Commodity Indicators

Broad Commodity Indicators

Chart III-24Commodity Prices

Commodity Prices

Commodity Prices

Chart III-25Commodity Prices

Commodity Prices

Commodity Prices

Chart III-26Commodity Sentiment

Commodity Sentiment

Commodity Sentiment

Chart III-27Speculative Positioning

Speculative Positioning

Speculative Positioning

ECONOMY: Chart III-28US And Global Macro Backdrop

US And Global Macro Backdrop

US And Global Macro Backdrop

Chart III-29US Macro Snapshot

US Macro Snapshot

US Macro Snapshot