Equities

Highlights We continue to believe that the distribution of Goldilocks economic and market outcomes is quite wide, … : Financial markets and the economy are in a good spot, supported by a combination of above-trend growth and easy monetary policy that will remain in place for at least the next year. … though an unwelcome COVID turn could put the US in the left-hand tail, … : Growth could fall short of expectations in the event of a negative pandemic surprise. As long as vaccinations occur at a pace that confers herd immunity by the end of September, the left-tail scenario is highly unlikely. … and a consumption tidal wave could bring the right tail into play: An explosive release of pent-up consumer demand could push US growth beyond the top of the sanguine consensus range. Too-strong growth would eventually become self-limiting because it would pull the Fed off the sidelines. Our recommendations are unchanged: Goldilocks is just right for risk assets, and we continue to favor equities over bonds and spread product over Treasuries. Feature The potential outcomes for financial markets and the US economy broadly align with Goldilocks’ porridge choices at the three bears’ house: one is too hot, one is too cold and one is just right. The just-right outcome is where we are positioned now: thanks to enormous infusions of emergency aid that have morphed into consumption pump-priming, above-trend growth appears to be assured. That would be plenty favorable for equities and credit on its own, but they also benefit from the Fed’s promise to maintain accommodative monetary policy longer than it previously would have. As our Chief Global Fixed Income Strategist Rob Robis puts it, emergency COVID monetary and fiscal policy will persist well beyond the COVID emergency. That’s an awfully good combination for risk assets and investors have taken note of it, driving equity multiples up and credit spreads down. It is entirely possible that they could spoil things by bidding prices too high, but so far the growth impacts – in the form of knockout earnings surprises and better-than-expected credit performance – have been able to keep the party going. It is our view that they will continue to do so this year, as the range of good-enough growth outcomes is so wide that a Goldilocks outcome is considerably more probable than not. Figure 1 doesn’t quite do it justice, because the area under the tails had to be large enough to accommodate lengthy words like “resurgent” and “consumption,” but we think the tails begin at least one standard deviation away from the middle of the distribution. Figure 1This One Is Just Right

Goldilocks And The Two Tails

Goldilocks And The Two Tails

How Did We Get Here? It is too soon for humanity to declare victory over COVID-19 but we do appear to have gained the upper hand as new case counts have plummeted from their January peaks in the US and the rest of the developed world (Chart 1). Much of Europe re-imposed stringent restrictions on activity for much of November and December, but US officials applied a loose patchwork of local measures, stepping in mostly when hospital capacity was strained (Chart 2). The good news going forward is that increased vigilance, and the cumulative infections that have already occurred, were apparently enough to slow the virus’ spread even during the northern hemisphere winter. The pandemic news can apparently be kept trending in the right direction without cutting off the economy’s oxygen. Chart 1The Tide Has Turned ...

The Tide Has Turned ...

The Tide Has Turned ...

Chart 2... Relieving Pressure On Local Health Care Systems

... Relieving Pressure On Local Health Care Systems

... Relieving Pressure On Local Health Care Systems

Lavish fiscal support has been the other critical element. The CARES Act swiftly rushed a great deal of aid to vulnerable households in two bursts spanning spring and early summer, with the first arriving mainly in April and May via economic impact payments of $1,200 per adult and $500 per child (Chart 3, top panel). The second burst came in the form of a weekly $600 federal unemployment insurance (UI) benefit supplement available through the end of July (though processing delays spread some of the flows into August) (Chart 3, middle panel). The transfers boosted aggregate household income above its pre-pandemic level despite a drop in compensation (Chart 3, bottom panel). Chart 3As Fiscal Transfers Wax And Wane, ...

Goldilocks And The Two Tails

Goldilocks And The Two Tails

Chart 4... So Does The Economy

... So Does The Economy

... So Does The Economy

By the end of the third quarter, however, the transfer flow had slowed to a trickle, with only the pandemic unemployment assistance (PUA) program, which expanded UI benefits to several categories of otherwise ineligible workers, still operating. President Trump’s executive order reallocating some FEMA funds briefly revived supplemental federal UI benefits, but the maximum $400 weekly bump only lasted for a handful of weeks in September and October. Once the fiscal transfers faded, signs of fraying rapidly emerged, with hiring flat-lining and retail sales falling sequentially in all three months of the fourth quarter (Chart 4). A New Paradigm No sooner had the economy begun to show signs of wear than the second round of economic impact payments, provided for in December’s compromise spending bill, arrived in two-thirds1 of American households and the federal government resumed topping up UI benefits. Both the direct payments ($600 per qualifying adult and $600 per child) and the supplemental UI benefits ($300 per week) were smaller than in the spring but we take the snapback in January retail sales as evidence that high marginal-propensity-to-consume households immediately put them to work. Households’ ability to satisfy their obligations to creditors (Chart 5) and landlords slipped as the year wore on as well. We expect that February rent collections and leading 30-day consumer delinquency rates will also show improvement (Chart 6), albeit not as dramatically as the retail series. Chart 560-Day Delinquency Rates Have Stopped Falling …

Goldilocks And The Two Tails

Goldilocks And The Two Tails

Chart 6... And Leading 30-Day Delinquencies Had Been Ticking Higher

Goldilocks And The Two Tails

Goldilocks And The Two Tails

With another, larger round of stimulus coming down the pike, the US economy will cease fraying around the edges. The immediate catalyst for the passage of the $1.9 trillion American Rescue Act was Georgia’s Senate run-off elections, but there were two longer-term developments at play. First, the mainstream economic consensus has come full circle since the global financial crisis and a chorus of expert voices is now warning governments of the perils of cutting off aid too quickly. Fed Chair Powell and Treasury Secretary Yellen have avidly taken up this theme, along with their central bank and finance ministry peers around the world. Second, and more lastingly and influentially, US voters have lost their taste for fiscal austerity. As we wrote with our US Political Strategy colleagues in last week’s Special Report, Democrats are actively renouncing Reaganite budget discipline and Republicans have quietly retired it. Now that the Fed has determined that Volcker-era inflation vigilance is no longer relevant, the stage is being set for a reversal of the investment-friendly inflation and interest rate trends that have been in place for four decades. That will weigh on financial market returns over the long run, but it should prop them up in the near term. Staying Out Of The Left Tail Central bankers are as prone as generals to fight the last war. Corrosively high inflation was every Fed official’s bête noire since the seventies, but a decade of missed inflation targets and tepid, plodding recoveries around the world has shifted central bankers’ focus to hysteresis and the specter of secular stagnation. Once the pandemic arrived, threatening self-reinforcing waves of defaults and bankruptcies, the Fed effectively declared that providing too much accommodation was a lesser evil than prematurely tightening to counter inflation fears that may prove to be unfounded. With fiscal policy makers also at pains to err on the side of doing too much, the near-term growth picture looks awfully good. Chart 7The Vaccination Effort Is Picking Up Steam

The Vaccination Effort Is Picking Up Steam

The Vaccination Effort Is Picking Up Steam

Against that policy backdrop, it will be hard for the US economy to slide into the left-hand tail of the distribution in the absence of a negative virus surprise. We cannot rule out the possibility of virus-resistant mutations or new rounds of outbreaks among a weary populace that lets its guard down, but a failure to vaccinate at a pace consistent with achieving herd immunity by the end of September looks to be the most likely route to disappointment. To that end, we are monitoring vaccination progress against the pace required to get enough of the population inoculated to effect herd immunity by the end of the third quarter (Chart 7). The US got off to a slow start, but we are confident that it will catch up by early spring under an administration that has made crushing the virus its top priority and a Congress that is providing the resources to enable local health authorities to get the job done. Overheating Is Not Inevitable The case for an upside near-term surprise stems from the notion that Congress has provided households with considerably more aid than they need. As we have previously noted, the number of households receiving economic impact payments is multiples of the number of households that have had to grapple with unemployment. Thanks to the first two rounds of fiscal transfers, we estimate that aggregate household income from March through January was nearly $600 billion greater than it would have been in the absence of COVID-19 (Table 1). The looming third round of direct payments could put incremental pandemic income in the neighborhood of $1 trillion. Table 1Households' Excess Pandemic Savings Keep Growing

Goldilocks And The Two Tails

Goldilocks And The Two Tails

Coupled with foregone consumption that already sums to $1.1 trillion, households’ excess pandemic savings is on course to top $2 trillion. That’s a lot of dry powder, even in a $21 trillion economy, and it underpins our view that the probability-adjusted distribution of Goldilocks outcomes is very wide. Without another major virus shock, it is hard to see a scenario where growth doesn’t comfortably exceed its 2% trend level. The question is whether or not enough of the savings will be spent in 2021 and 2022 to push the economy into the right-hand tail and potentially overheat. No one can say with much conviction, as the current backdrop is without precedent. Mount Rushmore-level economists David Ricardo and Milton Friedman would advise investors to temper their enthusiasm. Ricardian equivalence suggests that households will be reluctant to spend distributions they may be taxed to pay for later, and Friedman’s permanent income hypothesis posits that one-off windfalls have little effect on consumption decisions. The multiplier effect of the direct payments to households may not be all it’s cracked up to be, but the lion’s share of the savings stash has come from reduced consumption. How much of that reduced consumption was merely deferred rather than destroyed will determine how much growth can rise. Despite the vast household spending shortfall, consumption of goods has actually tracked above the level that would have been expected if the pandemic had not occurred; the spending gap has entirely been a function of diminished services spending, especially in pandemic-stricken categories like food service, recreation and transportation (Table 2). People surely have an appetite to resume that spending, and will flock to their favorite places once they can again enjoy them fully, but there’s a hitch. Last year’s forgone spending cannot be caught up by eating multiple restaurant dinners in a day, going back in time to attend last season’s sports and entertainment events, or flying on two planes2 and staying in two hotel rooms. Table 2The Spending Gap Is Almost Entirely On The Services Side

Goldilocks And The Two Tails

Goldilocks And The Two Tails

As a result, it seems that a fair amount of forgone services consumption is likely to turn into demand destroyed. Some demand for services could be diverted to demand for goods – one might build out a home theater instead of going to ballgames, movies and concerts; one might buy home exercise equipment in place of a gym membership – but much of that substitution has already taken place and may not persist going forward. The bottom line is that some goods demand appears to have been pulled forward by the pandemic while some services demand has likely been destroyed. There is surely pent-up consumer demand, but only some of the accumulated savings will be directed to satisfying it and we do not think they’ll push the economy to overheat. Investment Implications Our base case has the Goldilocks backdrop of solid growth and ample monetary accommodation remaining in place for at least the rest of the year. Markets have fully discounted that scenario but earnings growth has surprised to the upside by a remarkable margin over the last three quarters (Chart 8) and we expect that the fundamental backdrop will support mid- to high-single-digit equity returns. That will allow stocks to easily surpass bonds and we continue to overweight the former and underweight the latter. If some of the excess savings fuels multiple expansion, equity returns could be even better. Chart 8Earnings Have Been Beating Expectations By A Remarkable Margin

Goldilocks And The Two Tails

Goldilocks And The Two Tails

Although we are not worried that inflation is about to break out to uncomfortably high levels, we do expect further yield curve steepening from the combination of accelerating growth and an inflation-tolerant Fed. We continue to recommend that fixed income investors keep duration below benchmark levels. We expect an ongoing rotation from COVID winners to COVID losers as the virus is increasingly contained and look for value to outperform growth. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 Every single adult taxpayer with adjusted gross income (AGI) of $75,000 or less (and every married filing jointly taxpayer with AGI of $150,000 or less) was eligible for the full payments. 2 Even GE’s CEO doesn’t have this option anymore.

BCA Research’s Global Investment Strategy service concludes that the recent increase in real yields could put further downward pressure on equity prices in the near term. Bond yields have jumped in recent weeks. After bottoming at 0.52% in August, the US…

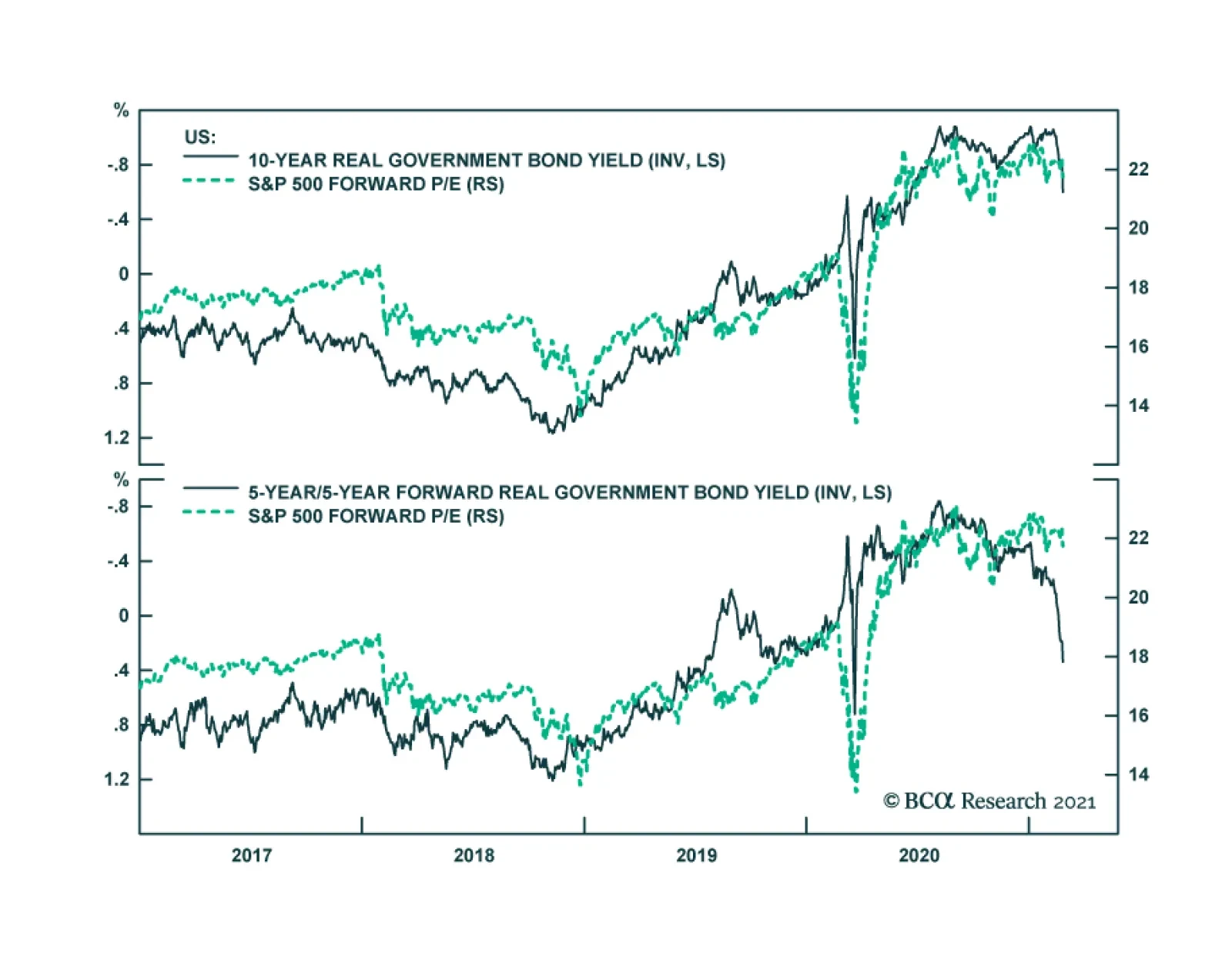

Dear Client, In addition to this week’s abbreviated report, we are sending you a Special Report on Bitcoin. I don’t recommend you buy it. Best regards, Peter Berezin Highlights Real government bond yields have increased in recent weeks, which could put further downward pressure on equity prices in the near term. Nevertheless, we continue to advocate overweighting equities over a 12-month horizon. Historically, rising real yields have been most toxic for stocks when yields have increased in response to hawkish central bank rhetoric. This is manifestly not the case today. The Fed’s accommodative stance should limit any near-term upward pressure on the US dollar. Investors should favor cyclical and value-oriented stocks over defensive and growth-geared plays. Higher Real Yields: A Near-Term Risk For Stocks Chart 1Government Bond Yields Have Increased Since Bottoming Last Year

Government Bond Yields Have Increased Since Bottoming Last Year

Government Bond Yields Have Increased Since Bottoming Last Year

Bond yields have jumped in recent weeks. After bottoming at 0.52% in August, the US 10-year Treasury yield has climbed to 1.54%, up from 0.93% at the beginning of the year. Government bond yields in the other major economies have also risen (Chart 1). While inflation expectations have bounced, the most recent increase in yields has been concentrated in the real component of bond yields (Chart 2). Optimism about a vaccine-led global growth recovery, reinforced by continued fiscal stimulus – especially in the US – has prompted investors to move forward their expectations of how soon and how high policy rates will rise (Chart 3). Chart 2AThe Real Component Has Fueled The Most Recent Rise In Bond Yields (I)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (I)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (I)

Chart 2BThe Real Component Has Fueled The Most Recent Rise In Bond Yields (II)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (II)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (II)

How menacing is the increase in bond yields to stock market investors? Chart 4 shows that there has been a close correlation between real yields and the forward P/E ratio at which the S&P 500 trades. The 5-year/5-year forward real yield, in particular, has moved up sharply, which could put further downward pressure on stocks in the near term. Chart 3Path Of Expected Policy Rates Being Revised Upwards

Path Of Expected Policy Rates Being Revised Upwards

Path Of Expected Policy Rates Being Revised Upwards

Chart 4Rise In Real Rates Is A Headwind For Equity Valuations

Rise In Real Rates Is A Headwind For Equity Valuations

Rise In Real Rates Is A Headwind For Equity Valuations

Nevertheless, we continue to advocate overweighting equities over a 12-month horizon. As we pointed out two weeks ago, rising real yields have historically been most toxic for stocks when yields have increased in response to hawkish central bank rhetoric. This is manifestly not the case today. In his testimony to Congress this week, Jay Powell downplayed inflation risks, stressing that the US economy was “a long way” from the Fed’s goals. He pledged to tread “carefully and patiently” and give “a lot of advance warning” before beginning the process of normalizing monetary policy. We expect the 10-year Treasury yield to stabilize in the 1.6%-to-1.7% range, still well below the level that would threaten the health of the economy. Favor Cyclical And Value-Oriented Stocks In A Weaker Dollar Environment The Fed’s accommodative stance should limit any near-term upward pressure on the US dollar. Whereas stocks are most sensitive to absolute changes in long-term real bond yields, the dollar is more sensitive to changes in short-term real rate differentials with US trading partners (Chart 5). Since the Fed is unlikely to tighten monetary policy anytime soon, US short-term real rates could fall further as inflation rises. Chart 5The Dollar Is Sensitive To Changes In Short-Term Real Rate Differentials

The Dollar Is Sensitive To Changes In Short-Term Real Rate Differentials

The Dollar Is Sensitive To Changes In Short-Term Real Rate Differentials

Chart 6Cyclical Stocks Tend To Benefit The Most From Stronger Global Growth And A Weaker Dollar

Cyclical Stocks Tend To Benefit The Most From Stronger Global Growth And A Weaker Dollar

Cyclical Stocks Tend To Benefit The Most From Stronger Global Growth And A Weaker Dollar

Cyclical stocks, which are overrepresented outside the US, tend to benefit the most from strengthening global growth and a weakening dollar (Chart 6). Value stocks also generally do well in a weak dollar-strong growth environment (Chart 7). Moreover, bank shares – which are concentrated in value indices – typically outperform when long-term bond yields are rising (Chart 8). Chart 7AA Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (I)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (I)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (I)

Chart 7BA Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (II)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (II)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (II)

Chart 8Bank Shares Typically Excel When Long-Term Bond Yields Are Rising

Bank Shares Typically Excel When Long-Term Bond Yields Are Rising

Bank Shares Typically Excel When Long-Term Bond Yields Are Rising

In contrast, as relatively long-duration assets, growth stocks often struggle when bond yields go up. The same is true for more speculative plays such as cryptocurrencies. In this week’s Special Report, we discuss the fate of Bitcoin, arguing that investors should resist buying it. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Global Investment Strategy View Matrix

When Good News Is Bad News

When Good News Is Bad News

Special Trade Recommendations

When Good News Is Bad News

When Good News Is Bad News

Current MacroQuant Model Scores

When Good News Is Bad News

When Good News Is Bad News

Highlights Market-based geopolitical analysis is about identifying upside as well as downside risk. So far this year upside risks include vaccine efficacy, coordinated monetary and fiscal stimulus, China’s avoidance of over-tightening policy, and Europe’s stable political dynamics. Downside risks include vaccine rollout problems, excessive US stimulus, a Chinese policy mistake, and traditional geopolitical risks in the Taiwan Strait and Persian Gulf. Financial markets may see more turmoil in the near-term over rising bond yields and the dollar bounce. But the macro backdrop is still supportive for this year. We are initiating and reinitiating a handful of trades: EM currencies ex-Brazil/Turkey/Philippines, the BCA rare earth basket, DM-ex-US, and the Trans-Pacific Partnership markets, and global value plays. Feature Chart 1Bond Yield Spike Threatens Markets In Near Term

Bond Yield Spike Threatens Markets In Near Term

Bond Yield Spike Threatens Markets In Near Term

Investors hear a lot about geopolitical risk but the implication is always “downside risk.” What about upside risks? Where are politics and geopolitics creating buying opportunities? So far this year, on the positive side, the US fiscal stimulus is overshooting, China is likely to avoid overtightening policy, and Europe’s political dynamics are positive. However, global equity markets are euphoric and much of the good news is priced in. On the negative side, the US stimulus is probably too large. The output gap will be more than closed by the Biden administration’s $1.9 trillion American Rescue Plan yet the Democrats will likely pass a second major bill later this year with a similar amount of net spending, albeit over a longer period of time and including tax hikes. The countertrend bounce in the dollar and rising government bond yields threaten the US and global equity market with a near-term correction. The global stock-to-bond ratio has gone vertical (Chart 1). Meanwhile Biden faces immediate foreign policy tests in the Taiwan Strait and Persian Gulf. These two are traditional geopolitical risks that are once again underrated by investors. The near term is likely to be difficult for investors to navigate. Sentiment is ebullient and likely to suffer some disappointments. In this report we highlight a handful of geopolitical opportunities and offer some new investment recommendations to capitalize on them. Go Long Japan And Stay Long South Korea China’s stimulus and recovery matched by global stimulus and recovery have led to an explosive rise in industrial metals and other China-sensitive assets such as Swedish stocks and the Australian dollar that go into our “China Play Index” (Chart 2). Chart 2China Plays Looking Stretched (For Now)

China Plays Looking Stretched (For Now)

China Plays Looking Stretched (For Now)

While a near-term pullback in these assets looks likely, tight global supplies will keep prices well-bid. Moreover long-term strategic investment plans by China and the EU to accelerate the technology race and renewable energy are now being joined by American investment plans, a cornerstone of Joe Biden’s emerging national policy program. We are long silver and would buy metals on the dips. Chinese President Xi Jinping’s “new era” policies will be further entrenched at the March National People’s Congress with the fourteenth five-year plan for 2021-25 and Xi’s longer vision for 2035. These policies aim to guide the country through its economic transition from export-manufacturing to domestic demand. They fundamentally favor state-owned enterprises, which are an increasingly necessary tool for the state to control aggregate demand as potential GDP growth declines, while punishing large state-run commercial banks, which are required to serve quasi-fiscal functions and swallow the costs of the transition (Chart 3). Xi Jinping’s decision to promote “dual circulation,” which is fundamentally a turn away from Deng Xiaoping’s opening up and liberal reform to a more self-sufficient policy of import substitution and indigenous innovation, will clash with the Biden administration, which has already flagged China as the US’s “most serious competitor” and is simultaneously seeking to move its supply chains out of China for critical technological, defense, and health goods. Chart 3Xi Jinping Leans On The Banks To Save The SOEs

Xi Jinping Leans On The Banks To Save The SOEs

Xi Jinping Leans On The Banks To Save The SOEs

Chinese political and geopolitical risks are almost entirely priced out of the market, according to our GeoRisk Indicator, leaving Chinese equities exposed to further downside (Chart 4). Hong Kong equities have traded in line with GeoRisk Indicator for China, which suggests that they also have downside as the market prices in a rising risk premium due to the US’s attempt to galvanize its allies in a great circumvention of China’s economy in the name of democracy versus autocracy. Chart 4China/HK Political Risk Priced Out Of Market

China/HK Political Risk Priced Out Of Market

China/HK Political Risk Priced Out Of Market

China has hinted that it will curtail rare earth element exports to the US if the US goes forward with a technological blockade. Biden’s approach, however, is more defensive rather than offensive – focusing on building up domestic and allied semiconductor and supply chain capacity rather than de-sourcing China. President Trump’s restrictions can be rolled back for US designed or manufactured tech goods that are outdated or strictly commercial. Biden will draw the line against American parts going into the People’s Liberation Army. Biden has a chance in March to ease the Commerce Department’s rules implementing Trump’s strictures on Chinese software apps in US markets as a gesture of engagement. Supply constraints and shortages cannot be solved quickly in either semiconductors or rare earths. But both China and the US can circumvent export controls by importing through third parties. The problem for China is that it is easier for the US to start pulling rare earths from the ground than it is for China to make a great leap forward in semiconductor production. Given the US’s reawakening to the need for a domestic industrial policy, strategic public investments, and secure supply chains, we are reinitiating our long rare earth trade, using the BCA rare earth basket, which features producers based outside of China (Chart 5). The renminbi is starting to rolling over, having reached near to the ceiling that it touched in 2017 after Trump’s arrival. There are various factors that drive the currency and there are good macro reasons for the currency to have appreciated in 2016-17 and 2020-21 due to strong government fiscal and monetary reflation. Nevertheless the People’s Bank allowed the currency to appreciate extensively at the beginning of both Trump’s and Biden’s terms and the currency’s momentum is slowing as it nears the 2017 ceiling. We are reluctant to believe the renminbi will go higher as China will not want to overtighten domestic policy but will want to build some leverage against Biden for the forthcoming strategic and economic dialogues. For mainland-dedicated investors we recommend holding Chinese bonds but for international investors we would highlight the likelihood that the renminbi has peaked and geopolitical risk will escalate. There is no substantial change on geopolitical risk in the Taiwan Strait since we wrote about it recently. A full-scale war is a low-probability risk. Much more likely is a diplomatic crisis – a showdown between the US and China over Taiwan’s ability to export tech to the mainland and the level of American support for Taiwan – and potentially a testing of Biden’s will on the cybersecurity, economic security, or maritime security of Taiwan. While it would make sense to stay long emerging markets excluding Taiwan, there is not an attractive profile for staying long emerging markets excluding all of Greater China. Therefore investors who are forced to choose should overweight China relative to Taiwan (Chart 6). Chart 5Rare Earth Miners Outside China Can Go Higher

Rare Earth Miners Outside China Can Go Higher

Rare Earth Miners Outside China Can Go Higher

Market forces have only begun to register the fact that Taiwan is the epicenter of geopolitical risk in the twenty-first century. The bottleneck for semiconductors and Taiwan’s role as middleman in the trade war have supported Taiwanese stocks. It will take a long time for China, the US, and Europe to develop alternative suppliers for chips. But geopolitical pressures will occasionally spike and when they do Taiwanese equities will plunge (Chart 7). Chart 6EM Investors Need Either China Or Taiwan ... Taiwan Most At Risk

EM Investors Need Either China Or Taiwan ... Taiwan Most At Risk

EM Investors Need Either China Or Taiwan ... Taiwan Most At Risk

South Korean geopolitical risk is also beneath the radar, though stocks have corrected recently and emerging market investors should generally favor Korea, especially over Taiwan. The first risk to Korea is that the US will apply more pressure on Seoul to join allied supply chains and exclude shipments of sensitive goods to China. The second risk is that North Korea – which Biden is deliberately ignoring in his opening speeches – will demand America’s attention through a new series of provocations that will have to be rebuked with credible threats of military force. Chart 7Markets Starting To Price Taiwan Strait Geopolitical Risk

Markets Starting To Price Taiwan Strait Geopolitical Risk

Markets Starting To Price Taiwan Strait Geopolitical Risk

Chart 8South Korea Favored In EM But Still Faces Risks Over Chips, The North

South Korea Favored In EM But Still Faces Risks Over Chips, The North

South Korea Favored In EM But Still Faces Risks Over Chips, The North

Chart 9Don't Worry About Japan's Revolving Door

Don't Worry About Japan's Revolving Door

Don't Worry About Japan's Revolving Door

The North Korean risk is usually very fleeting for financial markets. The tech risk is more serious but the Biden administration is not seeking to force South Korea to stop trading with China, at least not yet. The US would need to launch a robust, multi-year diplomatic effort to strong-arm its allies and partners into enforcing a chip and tech ban on China. Such an effort would generate a lot of light and heat – shuttle diplomacy, leaks to the press, and public disagreements and posturing. Until this starts to occur, US export controls will be a concern but not an existential threat to South Korea (Chart 8). Japan is the geopolitical winner in Asia Pacific. Japan is militarily secure, has a mutual defense treaty with the US, and stands to benefit from the recovery in global trade and growth. Japan is a beneficiary of a US-driven tech shift away from excess dependency on China and is heavily invested in Southeast Asia, which stands to pick up manufacturing share. Higher bond yields and inflation expectations will detract from growth stocks more than value stocks, and value stocks have a larger market-cap weight in European and Japanese equity markets. Japanese politics are not a significant risk despite a looming election. While Prime Minister Yoshihide Suga is unpopular and likely to revive the long tradition of a “revolving door” of short-lived prime ministers, and while the Liberal Democratic Party will lose the super-majorities it held under Shinzo Abe, nevertheless the party remains dominant and the national policy consensus is behind Abe’s platform of pro-growth reforms, coordinated dovish monetary and fiscal policy, and greater openness to trade and immigration (Chart 9). Favor EU And UK Over Russia And Eastern Europe Russian geopolitical risk appears to be rolling over according to our indicator but we disagree with the market’s assessment and expect it to escalate again soon (Chart 10). Not only will Russian social unrest continue to escalate but also the Biden administration will put greater pressure on Russia that will keep foreign investors wary. Chart 10Russia Geopolitical Risk Will Not Roll Over

Russia Geopolitical Risk Will Not Roll Over

Russia Geopolitical Risk Will Not Roll Over

While geopolitics thus poses a risk to Russian equities – which are fairly well correlated (inversely) with our GeoRisk indicator – nevertheless they are already cheap and stand to benefit from the rise in global commodity prices and liquidity. Russia is also easing fiscal policy to try to quiet domestic unrest. The pound and the euro today are higher against the ruble than at any time since the invasion of Ukraine. It is possible that Russia will opt for outward aggressiveness amidst domestic discontent, a weak and relapsing approval rating for Vladimir Putin and his government, and the Biden administration’s avowed intention to prioritize democracy promotion, including in Ukraine and Belarus (Chart 11). The ruble will fall on US punitive actions but ultimately there is limited downside, at least as long as the commodity upcycle continues. Chart 11Ruble Can Fall But Probably Not Far

Ruble Can Fall But Probably Not Far

Ruble Can Fall But Probably Not Far

Biden stated in his second major foreign policy speech, “we will not hesitate to raise the cost on Russia.” There are two areas where the Biden administration could surprise financial markets: pipelines and Russian bonds. Biden could suddenly adopt a hard line on the Nordstream 2 pipeline between Russia and Germany, preventing it from completion. This would require Biden to ask the Germans to put their money where their mouths are when it comes to trans-Atlantic solidarity. Biden is keen to restore relations with Germany, and is halting the withdrawal of US troops from there, but pressuring Germany on Russia is possible given that it lies in the US interest and Biden has vowed to push back against Russia’s aggressive regional actions and interference in American affairs. The US imposed sanctions on Russian “Eurobonds” under the Chemical and Biological Weapons Control and Warfare Elimination Act of 1991 (CBW Act) in the wake of Russia’s poisoning of secret agent Sergei Skripal in the UK in 2018. Non-ruble bank loans and non-ruble-denominated Russian bonds in primary markets were penalized, which at the time accounted for about 23% of Russian sovereign bonds. This left ruble-denominated sovereign bonds to be sold along with non-ruble bonds in secondary markets. The Biden administration views Russia’s poisoning of opposition leader Alexei Navalny as a similar infraction and will likely retaliate. The Defending American Security from Kremlin Aggression Act is not yet law but passed through a Senate committee vote in 2019 and proposed to halt most purchases of Russian sovereign debt and broaden sanctions on energy projects and Kremlin officials. Biden is also eager to retaliate for the large SolarWinds hack that Russia is accused of conducting throughout 2020. Cybersecurity stocks are an obvious geopolitical trade in contemporary times. Authoritarian nations have benefited from the use of cyber attacks, disinformation, and other asymmetric warfare tactics. The US has shown that it does not have the appetite to fight small wars, like over Ukraine or the South China Sea, whereas the US remains untested on the question of major wars. This incentivize incremental aggression and actions with plausible deniability like cyber. Therefore the huge run-up in cyber stocks is well-supported and will continue. The world’s growing dependency on technology during the pandemic lockdowns heightened the need for cybersecurity measures but the COVID winners are giving way to COVID losers as the pandemic subsides and normal economic activity resumes. Traditional defense stocks stand to benefit relative to cyber stocks as the secular trend of struggle among the Great Powers continues (Chart 12). Specifically a new cycle of territorial competition will revive military tensions as commodity prices rise. Chart 12Back To Work' Trade: Long Defense Versus Cyber

Back To Work' Trade: Long Defense Versus Cyber

Back To Work' Trade: Long Defense Versus Cyber

By contrast with Russia, western Europe is a prime beneficiary of the current environment. Like Japan, Europe is an industrial, trade-surplus economy that benefits from global trade and growth. It benefits as the geopolitical middleman between the US and its rivals, China and Russia, especially as long as the Biden administration pursues consultation and multilateralism and hesitates to force the Europeans into confrontational postures against these powers. Chart 13Political Risk Still Subsiding In Continental Europe

Political Risk Still Subsiding In Continental Europe

Political Risk Still Subsiding In Continental Europe

Meanwhile Russia and especially China need to court Europe now that the Biden administration is using diplomacy to try to galvanize a western bloc. China looks to substitute European goods for American goods and open up its market to European investors to reduce European complaints of protectionism. European domestic politics will become more interesting over the coming year, with German and French elections, but the risks are low. The rise of a centrist coalition in Italy under Mario Draghi highlights how overstated European political risk really is. In the Netherlands, Mark Rutte’s center-right party is expected to remain in power in March elections based on opinion polling, despite serious corruption scandals and COVID blowback. In Germany, Angela Merkel’s center-right party is also favored, and yet an upset would energize financial markets because it would result in a more fiscally accommodative and pro-EU policy (Chart 13). The takeaway is that there is limit to how far emerging European countries can outperform developed Europe, given the immediate geopolitical risk emanating from Russia that can spill over into eastern Europe (Chart 14). Developed European stocks are at peak levels, comparable to the period of Ukraine’s election, but Ukraine is about to heat up again as a battleground between Russia and the West, as will other peripheral states. Chart 14Favor DM Europe Over EM Europe

Favor DM Europe Over EM Europe

Favor DM Europe Over EM Europe

Chart 15GBP: Watch For Scottish Risk Revival In May

GBP: Watch For Scottish Risk Revival In May

GBP: Watch For Scottish Risk Revival In May

Finally, in the UK, the pound continues to surge in the wake of the settlement of a post-Brexit trade deal, notwithstanding lingering disagreements over vaccines, financial services, and other technicalities. British equities are a value play that can make up lost ground from the tumultuous Brexit years. There is potentially one more episode of instability, however, arising from the unfinished business in Scotland, where the Scottish National Party wants to convert any victory in parliamentary elections in May into a second push for a referendum on national independence. At the moment public opinion polls suggest that Prime Minister Boris Johnson’s achievement of an EU trade deal has taken the wind out of the sails of the independence movement but only the election will tell whether this political risk will continue to fall in the near term (Chart 15). Hence the pound’s rally could be curtailed in the near term but unless Scottish opinion changes direction the pound and UK domestic-oriented stocks will perform well. Short EM Strongmen Throughout the emerging world the rise of the “Misery Index” – unemployment combined with inflation – poses a persistent danger of social and political instability that will rise, not fall, in the coming years. The aftermath of the COVID crisis will be rocky once stimulus measures wane. South Africa, Turkey, and Brazil look the worst on these measures but India and Russia are also vulnerable (Chart 16). Brazilian geopolitical risk under the turbulent administration of President Jair Bolsonaro has returned to the 2015-16 peaks witnessed during the impeachment of President Dilma Rousseff amid the harsh recession of the middle of the last decade. Brazilian equities are nearing a triple bottom, which could present a buying opportunity but not before the current political crisis over fiscal policy exacts a toll on the currency and stock market (Chart 17). Chart 16EM Political Risk Will Bring Bad Surprises

EM Political Risk Will Bring Bad Surprises

EM Political Risk Will Bring Bad Surprises

Chart 17Brazil Risk Hits Impeachment Peaks On Bolso Fiscal Populism

Brazil Risk Hits Impeachment Peaks On Bolso Fiscal Populism

Brazil Risk Hits Impeachment Peaks On Bolso Fiscal Populism

Bolsonaro’s signature pension reform was an unpopular measure whose benefits were devastated by the pandemic. The return to fiscal largesse in the face of the crisis boosted Bolsonaro’s support and convinced him to abandon the pretense of austere reformer in favor of traditional Brazilian fiscal populist as the 2022 election approaches. His attempt to violate the country’s fiscal rule – a constitutional provision passed in December 2016 that imposes a 20-year cap on public spending growth – that limits budget deficits is precipitating a shakeup within the ruling coalition. Our Emerging Market Strategists believe the Central Bank of Brazil will hike interest rates to offset the inflationary impact of breaking the fiscal cap but that the hikes will likely fall short, prompting a bond selloff and renewed fears of a public debt crisis. The country’s political crisis will escalate in the lead up to elections, not unlike what occurred in the US, raising the odds of other negative political surprises. Chart 18Reinitiate Long Mexico / Short Brazil

Reinitiate Long Mexico / Short Brazil

Reinitiate Long Mexico / Short Brazil

While Latin America as a whole is a shambles, the global cyclical upturn and shift in American policy creates investment opportunities – particularly for Mexico, at least within the region. Investors should continue to prefer Mexican equities over Brazilian given Mexico’s fundamentally more stable economic policy backdrop and its proximity to the American economy, which will be supercharged with stimulus and eager to find ways to use its new trade deal with Mexico to diversify its manufacturing suppliers away from China (Chart 18). In addition to Brazil, Turkey and the Philippines are also markets where “strongman leaders” and populism have undercut economic orthodoxy and currency stability. A basket of emerging market currencies that excludes these three witnessed a major bottom in 2014-16, when Turkish and Brazilian political instability erupted and when President Rodrigo Duterte stormed the stage in the Philippines. These three currencies look to continue underperforming given that political dynamics will worsen ahead of elections in 2022 (possibly 2023 for Turkey) (Chart 19). Chart 19Keep Shorting The Strongmen

Keep Shorting The Strongmen

Keep Shorting The Strongmen

Investment Takeaways We closed out some “risk-on” trades at the end of January – admittedly too soon – and since then have hedged our pro-cyclical strategic portfolio with safe-haven assets, while continuing to add risk-on trades where appropriate. The Biden administration still faces one or more major foreign policy tests that can prove disruptive, particularly to Taiwanese, Chinese, Russian, and Saudi stocks. Biden’s foreign policy doctrine will be established in the crucible of experience but his preferences are known to favor diplomacy, democracy over autocracy, and to pursue alliances as a means of diversifying supply chains away from China. We will therefore look favorably upon the members of the Comprehensive and Progressive Trans-Pacific Partnership (CPTPP) and recommend investors reinitiate the long CPTPP equities basket. These countries, which include emerging markets with decent governance as well as Japan, Australia, New Zealand, and Canada all stand to benefit from the global upswing and US foreign policy (Chart 20). Chart 20Reinitiate Long Trans-Pacific Partnership

Reinitiate Long Trans-Pacific Partnership

Reinitiate Long Trans-Pacific Partnership

Chart 21Reinitiate Long Global Value Over Growth

Reinitiate Long Global Value Over Growth

Reinitiate Long Global Value Over Growth

The Biden administration will likely try to rejoin the CPTPP but even if it fails to do so it will privilege relations with these countries as it strives to counter China and Russia. The UK, South Korea, Thailand and others could join the CPTPP over time – though an attempt to recruit Taiwan would exacerbate the geopolitical risks highlighted above centered on Taiwan. The dollar is perking up, adding a near-term headwind to global equities, but the cyclical trend for the dollar is still down due to extreme monetary and fiscal dovishness. Tactically, go long Mexican equities over Brazilian equities. From a strategic point of view we still favor value stocks over growth stocks and recommend investors reinitiate this global trade (Chart 21). Strategically, wait to overweight UK stocks in a global portfolio until the result of the May local elections is known and the risk of Scottish independence can be reassessed. Strategically, favor developed Europe over emerging Europe stocks as a result of Russian geopolitical risks that are set to escalate. Strategically go long global defense stocks versus cyber security stocks as a geopolitical “back to work” trade for a time when economic activity resumes and resource-oriented territorial, kinetic, military risks reawaken. Strategically, favor EM currencies other than Brazil, Turkey, and the Philippines to minimize exposure to economic populism, poor macro fundamentals, and election risk. Strategically, go long the BCA Rare Earths Basket to capture persistent US-China tensions under Biden and the search for alternatives to China. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com We Read (And Liked) … Supply-Side Structural Reform Supply-Side Structural Reform, a compilation of Chinese economic and policy research, discusses several aspects of Chinese economic reform as it is practiced under the Xi Jinping administration, spanning the meaning and importance of supply-side structural reform in China as well as five major tasks.1 The book consists of contributions by Chinese scholars, financial analysts, and opinion makers in 2015, so we have learned a lot since it was published, even as it sheds light on Beijing’s interpretation of reform. 2015 was a year of financial turmoil that saw a dramatic setback for China’s 2013 liberal reform blueprint. It also saw the launch of a new round of reforms under the thirteenth Five Year Plan (2016-20), which aimed to push China further down the transition from export-manufacturing to domestic and consumer-led growth. Beijing’s renewed reform push in 2017, which included a now infamous “deleveraging campaign,” ultimately led to a global slowdown in 2018-19 that was fatefully exacerbated by the trade war with the United States – only to be eclipsed by the COVID-19 pandemic in 2020. Built on fundamental economic theory and the social background of China, the book’s authors examine the impact of supply-side reform on the Chinese financial sector, industrial sector, and macroeconomic development. The comprehensive analysis covers short-term, mid-term and long-term effects. From the perspective of economic theory, there is consensus that China's supply-side structural reform framework did not forsake government support for the demand side of the economy, nor was it synonymous with traditional, liberal supply-side economics in the Western world. In contrast to Say’s Law, Reaganomics, and the UK’s Thatcherite privatization reforms, China's supply-side reform was concentrated on five tasks specific to its contemporary situation: cutting excessive industrial capacity, de-stocking, deleveraging, cutting corporate costs, and improving various structural “weaknesses.” The motives behind the new framework were to enhance the mobility and efficiency of productive factors, eliminate excess capacity, and balance effective supply with effective demand. Basically, if China cannot improve efficiencies, capital will be misallocated, corporations will operate at a loss, and the economy’s potential will worsen over the long run. The debt buildup will accelerate and productivity will suffer. Regarding implementation, the book sets forth several related policies, including deepening the reform of land use and the household registration (hukou) system, and accelerating urbanization, which are effective measures to increase the liquidity of productive factors. Others promote the transformation from a factor-driven economy to efficiency and innovation-driven economy, including improving the property rights system, transferring corporate and local government debt to the central government, and encouraging investment in human capital and in technological innovation. The book also analyzes and predicts the potential costs of reform on the economy in the short and long term. In the short run, authors generally anticipated that deleveraging and cutting excessive industrial capacity would put more pressure on the government’s fiscal budget. The rise in the unemployment rate, cases of bankruptcy, and the negative sentiment of investors would slow China’s economic growth. In the medium and long run, this structural reform was seen as necessary for a sustainable medium-speed economic growth, leading to more positive expectations for households and corporates. The improved efficiency in capital allocation would provide investors with more confidence in the Chinese economy and asset market. Authors argued that overall credit risk was still controllable in near-term, as the corresponding policies such as tax reduction and urbanization would boost private investment and consumption in the short run. These policies increased demand in the labor market and created working positions to counteract adverse impacts. Employment in industries where excessive capacity was most severe only accounted for about 3% of total urban employment in 2013. Regarding the rise in credit risk during de-capacity, the asset quality of banks had improved since the 1990s and the level of bad debt was said to be within a controllable range, given government support. Moreover, in the long run, the merger and reorganization of enterprises would increase the efficient supply and have a positive effect on economic innovation-driven transformation. We know from experience that much of the optimism about reform would confront harsh realities in the 2016-21 period. The reforms proceeded in a halting fashion as the US trade war interrupted their implementation, prompting the government to resort to traditional stimulus measures in mid-2018, only to be followed by another massive fiscal-and-credit splurge in 2020 in the face of the pandemic. Yet investors could be surprised to find that the Politburo meeting on April 17, 2020 proclaimed that China would continue to focus on supply-side structural reform even amid efforts to normalize the economy and maintain epidemic prevention and control. Leaders also pledged to maintain the supply-side reform while emphasizing demand-side management during annual Central Economic Work Conference in December 2020. In other words, Xi administration’s policy preferences remain set, and compromises forced by exogenous events will soon give way to renewed reform initiatives. This is a risk to the global reflation trade in 2021-22. There has not been a total abandonment of supply-side reform. The main idea of demand-side reform – shifts in the way China’s government stimulates the economy – is to fully tap the potential of the domestic market and call for an expansion of consumption and effective investment. Combined with the new concept of “dual circulation,” which emphasizes domestic production and supply chains (effectively import substitution), the current demand-side reforms fall in line with the supply-side goal of building a more independent and controllable supply chain and produce higher technology products. These combined efforts will provide “New China” sectors with more policy support, less regulatory constraint, and lead to better economic and financial market performance. Despite the fluctuations in domestic growth and the pressure from external demand, China will maintain the focus on reform in its long-term planning. The fundamental motivation is to enhance efficiency and innovation that is essential for China’s productivity and competitiveness in the future. Thus, investors should not become complacent over the vast wave of fiscal and credit stimulus that is peaking today as we go to press. Instead they should recognize that China’s leaders are committed to restructuring. This means that the economic upside of stimulus has a cap on it– a cap that will eventually be put in place by policymakers, if not by China’s lower capacity for debt itself. It would be a colossal policy mistake for China to overtighten monetary and fiscal policy in 2021 but any government attempts to tighten, the financial market will become vulnerable. A final thought: it is unclear whether there is potential for an improvement in China’s foreign relations contained in this conclusion. What the western world is demanding is for China to rebalance its economy, open up its markets, cut back on the pace of technological acquisition, reduce government subsidies for state-owned companies, and conform better to US and EU trade rules. There is zero chance that China will provide all of these things. But its own reform program calls for greater intellectual property protections, greater competition in non-strategic sectors (which the US and EU should be able to access under recent trade deals), and targeted stimulus for sustainable energy, where the US and EU see trade and investment opportunities. Thus there is a basis for an improvement in cooperation. What remains to be seen is how protectionist dual circulation will be in practice and how aggressively the US will pursue international enforcement of technological restrictions on China under the Biden administration. Jingnan Liu Research Associate JingnanL@bcaresearch.com Footnotes 1 Yifu L, et al. Supply-Side Structural Reform (Beijing: Democracy & Construction Publishing House, 2016). 351 pages. Appendix: GeoRisk Indicator China

China: GeoRisk Indicator

China: GeoRisk Indicator

Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

UK

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Canada

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Taiwan

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Section III: Geopolitical Calendar

BCA Research’s Emerging Markets Strategy service concludes that there are many similarities between the current US macro picture and the late 1960s. In the late 1960s, US inflation was subdued, and interest rates were very low in the preceding two-three…

Global government bond markets are selling off in unison on greater optimism about the economic outlook, with yields at the long end of the curve increasing faster than yields on the short end. This bear steepening suggests that while investors are taking…

Looking To Re-establish Small Cap Bias

Looking To Re-establish Small Cap Bias

Upgrade Alert Small cap indexes regained their footing late last year and recovered two years of losses relative to the SPX in a mere quarter. During that uprising in mid-January we monetized sizable gains both on a cyclical and tactical (high-conviction) time horizon, and subsequently added the small cap bias back to our upgrade watch list. Following a drubbing in absolute and relative valuations, small caps have regained their luster and are now trading at a near 15% premium on a 10-year Cyclically Adjusted P/E (CAPE) basis. Given BCA’s view that the sell-off in the bond market has staying power, we are monitoring this ratio closely for a better entry point. Bottom Line: Small cap stock indexes remain on our upgrade alert list, awaiting a more compelling level to re-establish a small cap size portfolio bias.

Highlights The multiple paid for oil sector profits is collapsing because the market fears that the profits slump will not be short-lived. The fear is not just of a lasting hit to aviation and a slower recovery in road mobility, but an existential fear for fossil-fuelled road transportation in the post-pandemic world. Stay structurally underweight oil and gas. Within the cyclical and value segments of the equity market, overweight metals and miners versus oil and gas. Structurally underweight the stock markets of Norway and the UK which are oil and gas heavy. Structurally overweight the stock markets of Germany, Switzerland, and Denmark which have zero exposure to oil and gas or basic resources. Fractal trade: tin’s near-vertical rally is at high risk of correction. Feature Chart of the WeekOil Production Has Gone Nowhere

Oil Production Has Gone Nowhere

Oil Production Has Gone Nowhere

The Brent crude oil price recently hit $65, not far below its pre-pandemic level of $69. Yet in the stock market, oil and gas equities remain the dogs, languishing 32 percent below their pre-pandemic price level. Relative to the market, the oil and gas sector has underperformed by 42 percent, and the underperformance has been almost a straight line down. Moreover, since last June when the crude oil price has risen by 50 percent, oil and gas equity prices have gone nowhere. This massive divergence of a surging crude oil price from slumping oil and gas equities raises the obvious question, what can explain this dichotomy? (Chart I-2 and Chart I-3) Chart I-2Oil And Gas Equities Have Slumped In Absolute Terms...

Oil And Gas Equities Have Slumped In Absolute Terms...

Oil And Gas Equities Have Slumped In Absolute Terms...

Chart I-3...And In Relative ##br##Terms

...And In Relative Terms

...And In Relative Terms

One apparent puzzle is that the oil sector’s profits have underperformed their established relationship with the crude oil price. In fact, there is no puzzle. The oil sector’s profits might appear to track the oil price, but the reality is that profits track the value of oil production, meaning the product of oil production and the oil price. Clearly though, if output is flat, then profits will appear to track the oil price. But as it took a massive cut in oil output to support the oil price, the value of oil production and therefore, the oil sector’s profits, have significantly underperformed the oil price. Put another way, if you need to cut output to boost the commodity price it might help the commodity price, but it doesn’t much help the equity sector’s profits! (Chart I-4 and Chart I-5). Chart I-4Oil And Gas Profits Appear To Track The Oil Price

Oil And Gas Profits Appear To Track The Oil Price

Oil And Gas Profits Appear To Track The Oil Price

Chart I-5In Reality, Oil And Gas Profits Track The Value Of Oil Output

In Reality, Oil And Gas Profits Track The Value Of Oil Output

In Reality, Oil And Gas Profits Track The Value Of Oil Output

Will Fossil-Fuelled Road Transportation Be Driven To Extinction? We can now explain the 42 percent underperformance of oil equities, and perhaps more importantly, forecast what will happen next. When the pandemic took hold, and economic mobility ground to a halt, the oil sector’s 12-month forward profits slumped. Bear in mind that aviation accounts for 8 percent of oil consumption but, more crucially, road transportation accounts for half of all oil consumption. However, as the pandemic’s impact was expected to be short-lived, the multiple paid for those depressed 12-month forward profits rose. This partly compensated for the profit slump, but still left oil equity prices much lower. The multiple paid for oil sector profits is collapsing because the market fears that the profit slump will not be short-lived. When profits started to recover – albeit, as just discussed, by much less than the oil price rise – it should have boosted oil equity prices. The problem was that the multiple paid for those profits fell by much more than the recovery in profits, with the result that oil equities continued to underperform. Begging the question, why is the multiple paid for oil sector profits collapsing? (Chart I-6) Chart I-6Why Is The Multiple Paid For Oil Sector Profits Collapsing?

Why Is The Multiple Paid For Oil Sector Profits Collapsing?

Why Is The Multiple Paid For Oil Sector Profits Collapsing?

The multiple paid for oil sector profits is collapsing because the market fears that the profit slump will not be short-lived. The fear is not just of a lasting hit to aviation and a slower recovery in road mobility. The fear has become existential. Governments’ plans for pandemic stimulus and recovery have put green energy at front and centre stage. Thereby the recovery has fast-tracked the ultimate nemesis of the oil industry – the extinction of fossil-fuelled road transportation. Are the fears for oil consumption justified? Yes. Aviation is not likely to reach its pre-pandemic level of oil consumption for many years, and long-haul aviation may never get there. But the much bigger threat is fossil-fuelled road transportation. From October 2021, London will extend its Ultra Low Emission Zone (ULEZ) to an 8 mile radius from the city centre.1 The effect will be to banish from London all diesel-fuelled vehicles made before 2015 as well as some older petrol-fuelled vehicles. We expect other major cities to follow London’s example. In most cases, this initiative will happen regardless of the success (or not) of electric vehicles (EVs). Combined with other green initiatives around the world, policymakers’ unashamed aim is to drive fossil-fuelled road transportation to extinction. To repeat, road transportation accounts for half of all oil consumption. The upshot is that the structural downtrend in oil consumption will persist unless the shift away from fossil-fuelled road transportation hits a brick wall, or at least a bottleneck. We do not see such a brick wall or a bottleneck in the foreseeable future. We conclude that though the sector may offer occasional countertrend tactical buying opportunities, long-term equity investors should underweight oil and gas. Structurally Prefer Metals And Miners To Oil And Gas The preceding analysis of the oil sector can be extended to other commodity equities, like the metals and miners. To reiterate, it is the total value of commodity output – the product of commodity production and the commodity price – that drives the profits of commodity equities. On this basis, the long-term prospects for the metals and miners appear somewhat brighter than for oil and gas equities (Chart I-7). Chart I-7Commodity Sector Profits Track The Value Of Commodity Output

Commodity Sector Profits Track The Value Of Commodity Output

Commodity Sector Profits Track The Value Of Commodity Output

Looking at the production of copper, it has increased by around 25 percent over the past decade, albeit this is just in line with world real GDP. By comparison, the production of oil has gone nowhere (Chart of the Week). It is the total value of commodity output that drives the profits of commodity equities. Turning to price, relative to the 2011 high the copper price is around 15 percent lower, whereas the oil price is 50 percent lower (Chart I-8). Chart I-8The Copper Price Has Outperformed The Oil Price

The Copper Price Has Outperformed The Oil Price

The Copper Price Has Outperformed The Oil Price

Hence, on the all-important value of output, copper has moved in a sideways channel over the past decade while oil has been in an unmistakeable structural downtrend, with lower highs and lower lows (Chart I-9). Chart I-9The Value Of Output Is Trending Sideways For Copper, But Downwards For Oil

The Value Of Output Is Trending Sideways For Copper, But Downwards For Oil

The Value Of Output Is Trending Sideways For Copper, But Downwards For Oil

This relative trend is likely to continue as the shift from fossil-fuelled road transportation to EVs will weigh on oil demand, while supporting copper (and other metal) demand. We do not recommend an outright overweight in metals and miners given that their profits are just moving in a sideways channel. However, within the cyclical and value segments of the equity market, a good structural position is to overweight metals and miners versus oil and gas. When Oil And Gas Underperforms, So Does Norway’s OBX And The UK’s FTSE 100 Regional and country equity market performances is driven by the dominant sectors within each stock market. In relative terms, it is also driven by the sectors that are missing. If the oil and gas sector is a structural underperformer, then oil and gas heavy stock markets such as Norway and the UK will be structural underperformers too. If the oil and gas sector is a structural underperformer, it inevitably means that oil and gas heavy stock markets such as Norway and the UK will be structural underperformers too (Chart I-10 and Chart I-11). Chart I-10When Oil And Gas Underperforms, Norway's OBX Underperforms...

When Oil And Gas Underperforms, Norway's OBX Underperforms...

When Oil And Gas Underperforms, Norway's OBX Underperforms...

Chart I-11...And The UK's FTSE 100 ##br##Underperforms

...And The UK's FTSE 100 Underperforms

...And The UK's FTSE 100 Underperforms

The corollary is that stock markets which are under-exposed to the structurally underperforming sector will be at a relative advantage. This supports our structural overweighting to the stock markets of Germany, Switzerland, and Denmark, which all have zero exposure to oil and gas and basic resources. Fractal Trading System* Tin’s near-vertical rally is at high risk of correction based on fragility on all three fractal structures: 65-day, 130-day, and 260-day. A good trade is to short tin versus lead, setting a profit target and symmetrical stop-loss at 13 percent. In other trades, the underweights to China and Korea surged, but short AUD/JPY and short copper/gold reached their stop-losses. The rolling 12-month win ratio stands at 57 percent. Chart I-12Tin Vs. Lead

Tin Vs. Lead

Tin Vs. Lead

When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 ULEZ will be the zone inside London’s North Circular and South Circular Roads. Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

For this month’s Special Report, we are sending you a collaboration between our US Investment Strategy and US Political Strategy teams. US Political Strategy is our newest strategy service and it extends the proprietary framework of our Geopolitical Strategy service to provide analysis of political developments that is relevant for US-focused investors. Please contact your relationship manager if you would like more information or to begin trialing the service. Highlights Ronald Reagan cast a long shadow over the elected officials who followed him … :The influence of the economic policies associated with Ronald Reagan held such persistent sway that even the Clinton and Obama administrations had to follow their broad outlines. … just as Paul Volcker did over central bankers at home and abroad … : The Volcker Fed’s uncompromising resistance to the 1970s’ runaway inflation established the Fed’s credibility and enshrined a new global central banking orthodoxy. … but it appears their enduring influence may have finally run its course … : The pandemic overrode everything else in real time, but investors may ultimately view 2020 as the year in which Democrats broke away from post-Reagan orthodoxy and the Fed decided Volcker’s vigilance was no longer relevant. … to investors’ potential chagrin: If inflation, big government and organized labor come back from the dead, globalization loses ground, regulation expands, anti-trust enforcement regains some bite and tax rates rise and become more progressive, then the four-decade investment golden age that Reagan and Volcker helped launch may be on its last legs. Feature The pandemic dominated everything in real time in 2020, as investors scrambled to keep up with its disruptions and the countermeasures policymakers deployed to shelter the economy from them. With some distance, however, investors may come to view it as a year of two critical policy inflection points: the end of the Reagan fiscal era and the end of the Volcker monetary era. The shifts could mark a watershed because Reagan’s and Volcker’s enduring influence helped power an investment golden age that has lasted for nearly 40 years. What comes next may not be so supportive for financial markets. Political history often unfolds in cycles even if their starting and ending dates are never as clear cut in real life as they are in dissertations. Broadly, the FDR administration kicked off the New Deal era, a 48-year period of increased government involvement in daily life via the introduction and steady expansion of the social safety net, broadened regulatory powers and sweeping worker protections. It was followed by the 40-year Reagan era, with a continuous soundtrack of limited government rhetoric made manifest in policies that sought to curtail the spread of social welfare programs, deregulate commercial activity, devolve power to state and local government units and the private sector and push back against unions. The Obama and Trump administrations challenged different aspects of Reaganism, but the 2020 election cycle finally toppled it. Ordinarily, that might only matter to historians and political scientists, but the Reagan era coincided with a fantastic run in financial markets. So, too, did the inflation vigilance that lasted long after Paul Volcker’s 1979-1987 tenure at the helm of the Federal Reserve, which drove an extended period of disinflation, falling interest rates and rising central bank credibility. Our focus here is on fiscal policy, and we touch on monetary policy only to note that last summer’s revision of the Fed’s statement of long-run monetary policy goals shut the door on the Volcker era. The end of both eras could mark an inflection point in the trajectory of asset returns. The Happy Warrior The nine most terrifying words in the English language are, “I’m from the government, and I’m here to help.”1 Chart II-1After The Recession, Reagan Was A Hit

After The Recession, Reagan Was A Hit

After The Recession, Reagan Was A Hit

Ronald Reagan held his conservative views with the zeal of the convert that he was.2 Those views were probably to the right of much of the electorate, but his personal appeal was strong enough to make them palatable to a sizable majority (Chart II-1). Substitute “left” for “right” and the sentiment just as easily sums up FDR’s ability to get the New Deal off the ground. Personal magnetism played a big role in each era’s rise, with both men radiating relatability and optimism that imbued their sagging fellow citizens with a sense of comfort and security that made them willing to try something very different. 1980 was hardly 1932 on the distress scale, but America was in a funk after the upheaval of the sixties, the humiliating end to Vietnam, Watergate, stagflation and a term and a half of uninspiring and ineffectual presidential leadership. Enter the Great Communicator, whose initial weekly radio address evoked the FDR of the Fireside Chats – jovial, resolute and confident, with palpable can-do energy – buffed to a shine by a professional actor and broadcaster whose vocal inflections hit every mark.3 The Gipper,4 with his avuncular bearing, physical robustness and ever-present twinkle in his eye, was just what the country needed to feel better about itself. Reaganomics 101 Government does not tax to get the money it needs; government always finds a need for the money it gets.5 President Reagan’s economic plan had three simple goals: cut taxes, tame government spending and reduce regulation. From the start of his entry into politics in the mid-sixties, Reagan cast himself as a defender of hard-working Americans’ right to keep more of the fruits of their labor from a grasping federal government seeking funding for wasteful, poorly designed programs. He harbored an intense animus for LBJ’s Great Society, which extended the reach of the federal government in ways that he characterized as a drag on initiative, accomplishment and freedom, no matter how well intentioned it may have been. That message hung a historic loss on Barry Goldwater in 1964 when inflation was somnolent but it proved to be far more persuasive after the runaway inflation of the seventies exposed the perils of excessive government (Chart II-2). Chart II-2Inflation Rises When The Labor Market Heats Up

Inflation Rises When The Labor Market Heats Up

Inflation Rises When The Labor Market Heats Up