Equities

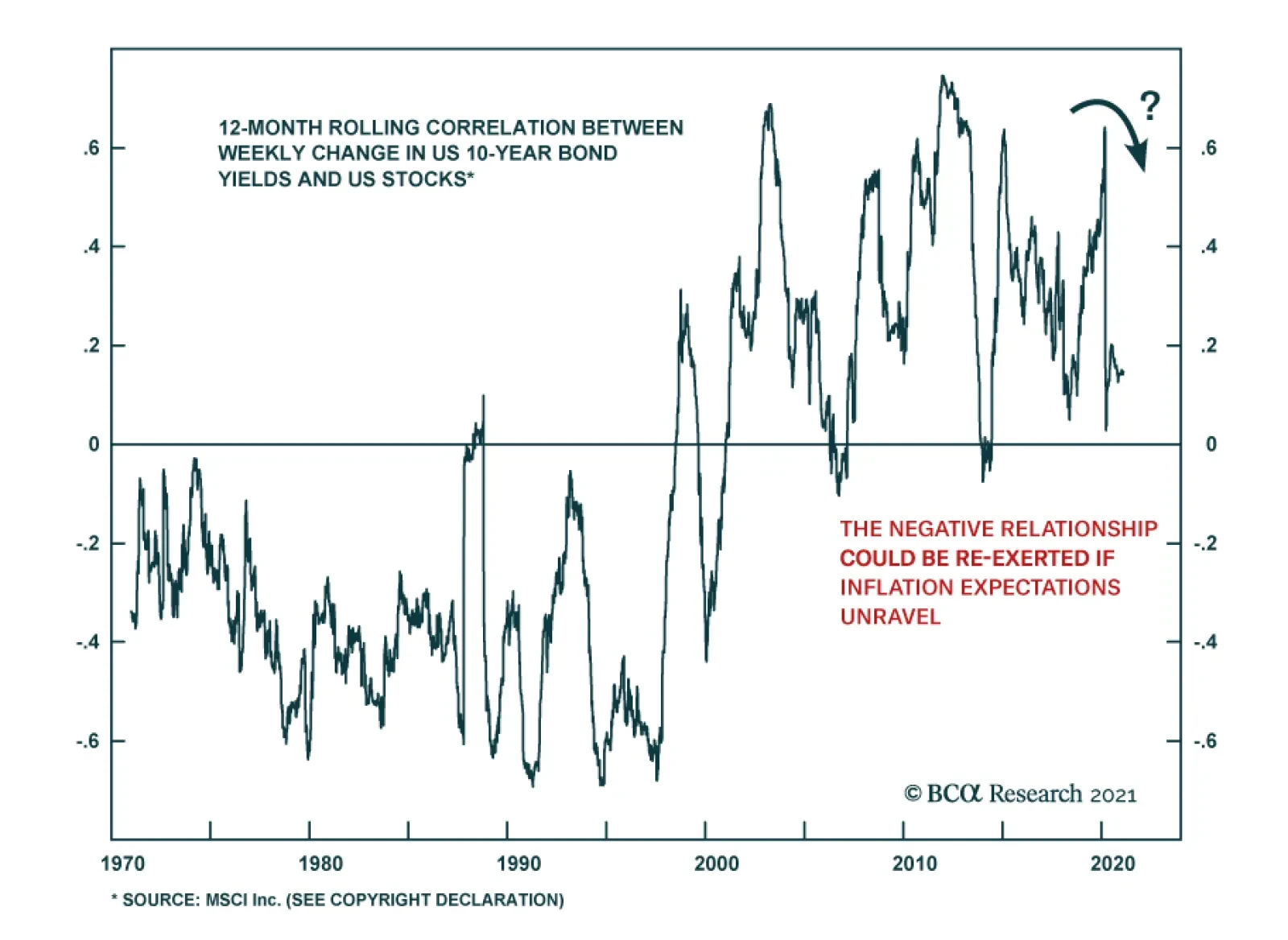

Global equity valuations are at a level where they are very sensitive to changes in the discount rate. Chart 1 shows that the cyclically-adjusted earnings yield on the S&P 500 is slightly below its 2000 low. Equity investors have thus far taken comfort from the fact that US bond yields have been depressed, and taking into consideration low bond yields the US equity market is not as bubbly as it was in the 2000s. Chart 1Rising US Bond Yields Threatens US Equity Valuations

Rising US Bond Yields Threatens US Equity Valuations

Rising US Bond Yields Threatens US Equity Valuations

However, the fact that the US equity market’s valuations after accounting for the level of interest rates are not as expensive as they were in 2000 does not mean share prices cannot experience a meaningful shakeout. Notably, there is a lot of speculation and euphoria among investors, reminiscent of the late 1990s (please refer to Charts 24-26 below). Critically, when equity multiples are very elevated and bond yields are extremely low, the sensitivity of multiples to interest rates is most pronounced. Hence, rising US Treasury yields could result in a setback in share prices. All in all, our themes for now are as follows: Chart 2A Full-Fledged Mania In Asian TMT Stocks

A Full-Fledged Mania In Asian TMT Stocks

A Full-Fledged Mania In Asian TMT Stocks

Enormous US fiscal and monetary stimulus, strong economic growth and supply bottlenecks will push up the US core inflation rate. As a result, the ongoing sell-off in long-term US bond yields will continue. EM and DM credit spreads are currently very tight and credit spreads might not be able to compress further to offset the rise in US Treasury yields. Hence, rising US Treasury yields will trigger higher corporate and EM sovereign bond yields. In brief, rising EM bond yields is the key risk to EM share prices. Charts 5 and 6 below illustrate these points. Given that the US trade-weighted dollar is extremely oversold, rising US Treasury yields will likely trigger a countertrend rally in the greenback. This will cause a shakeout in EM currencies, fixed-income markets and commodities prices. Historically, the greenback has not had a stable relationship with US Treasury yields – they were both positively and negatively correlated in different periods. In such an environment, DM growth stocks will underperform DM value stocks. We have less conviction in growth/value performance in the EM space. The reason lies in the speculative frenzy taking place in Chinese new economy stocks trading in Hong Kong as well as tech share prices in Korea and Taiwan. As Chart 2 reveals, the Hang Seng Tech index and EM TMT stocks have been rising exponentially. Visibility is very low. The timing of a reversal of this equity euphoria is impossible to predict. Outside these TMT stocks, the relative performance of EM equities has been rather underwhelming, as is illustrated in Charts 71-73. Notably, the economic recovery in EM ex-China, Korea and Taiwan has been much weaker than those in DM and North Asian economies (please refer to Charts 63 and 66). This will continue as many of these nations are lagging in vaccine rollouts and their fiscal and monetary support has been much smaller. In addition, peak stimulus in China means that the mainland’s construction and infrastructure investment will slow meaningfully in H2 2021. This is another risk to EM economies supplying to China. Weighing pros and cons, we continue to recommend a neutral allocation to EM in a global equity portfolio. The same is true for EM credit (sovereign and corporate) within a global credit portfolio. For local bonds, inflation in EM – including China – is still very low and will likely stay depressed. As a result, we continue recommending receiving 10-year swap rates in Mexico, Colombia, Russia, Malaysia, India and China. Investors should use a rebound in the US dollar to transition from receiving rates to being long on cash bonds. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Yellow Flags For Share Prices Rising US corporate bond yields pose a risk to the equity rally. Interestingly, New Zealand’s stock market has begun correcting. Often but not always, this development heralds a pullback in EM share prices (albeit for unknown reasons). Chart 3Yellow Flags For Share Prices

Yellow Flags For Share Prices

Yellow Flags For Share Prices

Chart 4Yellow Flags For Share Prices

Yellow Flags For Share Prices

Yellow Flags For Share Prices

Beware Of Potential Rise In EM Sovereign And Corporate USD Bond Yields Historically, rising EM corporate USD bond yields led to a selloff in EM share prices. If rising US Treasury yields begin pushing up EM sovereign and corporate bonds yields, which is quite likely, the EM equity rally will be jeopardized. Chart 5Beware Of Potential Rise In EM Sovereign And Corporate USD Bond Yields

Beware Of Potential Rise In EM Sovereign And Corporate USD Bond Yields

Beware Of Potential Rise In EM Sovereign And Corporate USD Bond Yields

Chart 6Beware Of Potential Rise In EM Sovereign And Corporate USD Bond Yields

Beware Of Potential Rise In EM Sovereign And Corporate USD Bond Yields

Beware Of Potential Rise In EM Sovereign And Corporate USD Bond Yields

EM Equities Are Ignoring Many Warning Signs Due To Profit Recovery So far, the EM equity index has snubbed the rollover in China’s credit impulse and plummeting gold prices in non-US dollar currencies. The ongoing EM corporate earnings recovery has justified the rally in of share prices. However, much of the good news has already been priced in. Chart 7EM Equities Are Ignoring Many Warning Signs Due To Profit Recovery

EM Equities Are Ignoring Many Warning Signs Due To Profit Recovery

EM Equities Are Ignoring Many Warning Signs Due To Profit Recovery

Chart 8EM Equities Are Ignoring Many Warning Signs Due To Profit Recovery

EM Equities Are Ignoring Many Warning Signs Due To Profit Recovery

EM Equities Are Ignoring Many Warning Signs Due To Profit Recovery

Chart 9EM Equities Are Ignoring Many Warning Signs Due To Profit Recovery

EM Equities Are Ignoring Many Warning Signs Due To Profit Recovery

EM Equities Are Ignoring Many Warning Signs Due To Profit Recovery

Investors Are Super Bullish European investors are very bullish on EM equities and European growth. From a contrarian perspective, this does not always herald a bear market but suggests that odds of a meaningful shakeout are non-trivial. Chart 10Investors Are Super Bullish

Investors Are Super Bullish

Investors Are Super Bullish

Chart 11Investors Are Super Bullish

Investors Are Super Bullish

Investors Are Super Bullish

Investor Growth Expectations Are Super High Our proxy for global growth expectations as well as EM net EPS revisions are elevated. Similarly, analysts’ EM 12-month forward EPS growth differential vs. US are the widest since 2001. Chart 12Investor Growth Expectations Are Super High

Investor Growth Expectations Are Super High

Investor Growth Expectations Are Super High

Chart 13Investor Growth Expectations Are Super High

Investor Growth Expectations Are Super High

Investor Growth Expectations Are Super High

US Inflation And Rates US core goods inflation has been rising due to strong US household demand and supply bottlenecks. When the economy fully reopens, US core service inflation will rise as pent-up demand for services is unleashed. This will push up US bond yields regardless of the Fed’s rhetoric. Chart 14US Inflation And Rates

US Inflation And Rates

US Inflation And Rates

Chart 15US Inflation And Rates

US Inflation And Rates

US Inflation And Rates

Chart 16US Inflation And Rates

US Inflation And Rates

US Inflation And Rates

Look Out For Cracks In EM High-Yield Bond Space A rise in US TIPS and nominal yields will likely send shockwaves through EM risk assets and commodities that have greatly benefited from the plunge in TIPS yields. Watch out for cracks in the EM high-yield bond space. Chart 17Look Out For Cracks In EM High-Yield Bond Space

Look Out For Cracks In EM High-Yield Bond Space

Look Out For Cracks In EM High-Yield Bond Space

Chart 18Look Out For Cracks In EM High-Yield Bond Space

Look Out For Cracks In EM High-Yield Bond Space

Look Out For Cracks In EM High-Yield Bond Space

Chart 19Look Out For Cracks In EM High-Yield Bond Space

Look Out For Cracks In EM High-Yield Bond Space

Look Out For Cracks In EM High-Yield Bond Space

Chart 20Look Out For Cracks In EM High-Yield Bond Space

Look Out For Cracks In EM High-Yield Bond Space

Look Out For Cracks In EM High-Yield Bond Space

EM Currencies Are Not Yet Expensive But Are Overbought Although cyclically and for some countries structurally speaking EM currencies have more upside and their appreciation path will not be without major setbacks. In fact, several key currencies like MXN and ZAR are facing an important technical resistance. Investors should not chase them higher but accumulate them on a relapse. Chart 21EM Currencies Are Not Yet Expensive But Are Overbought

EM Currencies Are Not Yet Expensive But Are Overbought

EM Currencies Are Not Yet Expensive But Are Overbought

Chart 23EM Currencies Are Not Yet Expensive But Are Overbought

EM Currencies Are Not Yet Expensive But Are Overbought

EM Currencies Are Not Yet Expensive But Are Overbought

Chart 22EM Currencies Are Not Yet Expensive But Are Overbought

EM Currencies Are Not Yet Expensive But Are Overbought

EM Currencies Are Not Yet Expensive But Are Overbought

Equity Market Euphoria Is Running Wild Certain measures of stock market activity – like the call-put ratio, trading volumes and margin loans – reveal engulfing speculative behavior not only in the US but also in other markets like Korea. Chart 24Equity Market Euphoria Is Running Wild

Equity Market Euphoria Is Running Wild

Equity Market Euphoria Is Running Wild

Chart 25Equity Market Euphoria Is Running Wild

Equity Market Euphoria Is Running Wild

Equity Market Euphoria Is Running Wild

Chart 26Equity Market Euphoria Is Running Wild

Equity Market Euphoria Is Running Wild

Equity Market Euphoria Is Running Wild

A Mania Can Run Further And Longer Than Rational Analysis Can Envision The IPO boom is not as expansive as it was at its 2000 and 2007 peaks and there is some US dollar cash left to be put to work. Visibility is very low. Chart 27A Mania Can Run Further And Longer Than Rational Analysis Can Envision

A Mania Can Run Further And Longer Than Rational Analysis Can Envision

A Mania Can Run Further And Longer Than Rational Analysis Can Envision

Chart 28A Mania Can Run Further And Longer Than Rational Analysis Can Envision

A Mania Can Run Further And Longer Than Rational Analysis Can Envision

A Mania Can Run Further And Longer Than Rational Analysis Can Envision

Chart 29A Mania Can Run Further And Longer Than Rational Analysis Can Envision

A Mania Can Run Further And Longer Than Rational Analysis Can Envision

A Mania Can Run Further And Longer Than Rational Analysis Can Envision

Steep Equity Volatility Curves A steep equity volatility curve heralds a correction. Chart 30Steep Equity Volatility Curves

Steep Equity Volatility Curves

Steep Equity Volatility Curves

Chart 31Steep Equity Volatility Curves

Steep Equity Volatility Curves

Steep Equity Volatility Curves

Chart 32Steep Equity Volatility Curves

Steep Equity Volatility Curves

Steep Equity Volatility Curves

Chart 33Steep Equity Volatility Curves

Steep Equity Volatility Curves

Steep Equity Volatility Curves

Volatilities Across FX, Bonds And Commodities Oil volatility has been and remains in a bull market – making higher lows. Currency volatility remains elevated while US bond volatility is still very low and is bound to rise. Chart 34Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Chart 35Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Chart 36Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Chart 37Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Chart 38Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Chart 39Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Volatilities Across FX, Bonds and Commodities

Cyclicals Vs. Defensives And Growth Vs. Value Performance Global cyclical stocks’ relative performance versus defensive stocks might be due for a pause. Growth will underperform value in DM due to rising bond yields. We are less convinced about the growth/value performance in the EM equity space due to the mania occurring in EM TMT stocks. Chart 40Cyclicals Vs. Defensives And Growth Vs. Value Performance

Cyclicals Vs. Defensives And Growth Vs. Value Performance

Cyclicals Vs. Defensives And Growth Vs. Value Performance

Chart 41Cyclicals Vs. Defensives And Growth Vs. Value Performance

Cyclicals Vs. Defensives And Growth Vs. Value Performance

Cyclicals Vs. Defensives And Growth Vs. Value Performance

Chart 42Cyclicals Vs. Defensives And Growth Vs. Value Performance

Cyclicals Vs. Defensives And Growth Vs. Value Performance

Cyclicals Vs. Defensives And Growth Vs. Value Performance

Chart 43Cyclicals Vs. Defensives And Growth Vs. Value Performance

Cyclicals Vs. Defensives And Growth Vs. Value Performance

Cyclicals Vs. Defensives And Growth Vs. Value Performance

Profiles Of Various Global Equity Indexes Many global equity indexes excluding US or TMT have either not broken out or have done so only marginally. Chart 44Profiles Of Various Global Equity Indexes

Profiles Of Various Global Equity Indexes

Profiles Of Various Global Equity Indexes

Chart 45Profiles Of Various Global Equity Indexes

Profiles Of Various Global Equity Indexes

Profiles Of Various Global Equity Indexes

Chart 46Profiles Of Various Global Equity Indexes

Profiles Of Various Global Equity Indexes

Profiles Of Various Global Equity Indexes

Chart 47Profiles Of Various Global Equity Indexes

Profiles Of Various Global Equity Indexes

Profiles Of Various Global Equity Indexes

EM ex-TMT Equity Performance Has Been Unimpressive Excluding TMT stocks, EM equity indexes have not broken above their previous highs. It has been a mania in TMT stocks that has boosted the EM overall equity index. Chart 48EM ex-TMT Equity Performance Has Been Unimpressive

EM ex-TMT Equity Performance Has Been Unimpressive

EM ex-TMT Equity Performance Has Been Unimpressive

Chart 49EM ex-TMT Equity Performance Has Been Unimpressive

EM ex-TMT Equity Performance Has Been Unimpressive

EM ex-TMT Equity Performance Has Been Unimpressive

Chart 50EM ex-TMT Equity Performance Has Been Unimpressive

EM ex-TMT Equity Performance Has Been Unimpressive

EM ex-TMT Equity Performance Has Been Unimpressive

Chart 51EM ex-TMT Equity Performance Has Been Unimpressive

EM ex-TMT Equity Performance Has Been Unimpressive

EM ex-TMT Equity Performance Has Been Unimpressive

A Mania In Chinese Stocks, Especially In TMT Stocks Chinese offshore stocks ex-TMT and onshore equal-weighted and small caps have done rather poorly. The latest euphoria in Hong Kong-listed Chinese stocks has been due to an increased quota for mainland investors to buy offshore stocks. This has led to massive southbound outflows and has propelled Chinese stock trading in Hong Kong. Chart 52A Mania In Chinese Stocks, Especially In TMT Stocks

A Mania In Chinese Stocks, Especially In TMT Stocks

A Mania In Chinese Stocks, Especially In TMT Stocks

Chart 53A Mania In Chinese Stocks, Especially In TMT Stocks

A Mania In Chinese Stocks, Especially In TMT Stocks

A Mania In Chinese Stocks, Especially In TMT Stocks

Chart 54A Mania In Chinese Stocks, Especially In TMT Stocks

A Mania In Chinese Stocks, Especially In TMT Stocks

A Mania In Chinese Stocks, Especially In TMT Stocks

The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021 Rollover in credit and fiscal stimulus in Q4 2020 entails weak growth in H2 2021 in segments leveraged to stimulus. Chart 55The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

Chart 56The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

Chart 57The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

Chart 58The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

The Chinese Economy: Peak Stimulus = Weak Growth In H2 2021

Commodity Prices The end of commodities restocking in China, weaker demand from mainland construction in H2 and elevated investor net long positions in commodities constitute the basis for a setback in commodities prices this year. Nevertheless, such a pullback will occur only if the USD rebounds and global equity prices sell off. Chart 59Commodity Prices

Commodity Prices

Commodity Prices

Chart 60Commodity Prices

Commodity Prices

Commodity Prices

Chart 61Commodity Prices

Commodity Prices

Commodity Prices

Chart 62Commodity Prices

Commodity Prices

Commodity Prices

The Recovery In EM ex-North Asia Has Been Very Subdued The economic recovery in EM ex-China, Korea and Taiwan has been much weaker than those in DM and North Asian economies. Chart 63The Recovery In EM ex-North Asia Has Been Very Subdued

The Recovery In EM ex-North Asia Has Been Very Subdued

The Recovery In EM ex-North Asia Has Been Very Subdued

Chart 64The Recovery In EM ex-North Asia Has Been Very Subdued

The Recovery In EM ex-North Asia Has Been Very Subdued

The Recovery In EM ex-North Asia Has Been Very Subdued

Chart 65The Recovery In EM ex-North Asia Has Been Very Subdued

The Recovery In EM ex-North Asia Has Been Very Subdued

The Recovery In EM ex-North Asia Has Been Very Subdued

Chart 66The Recovery In EM ex-North Asia Has Been Very Subdued

The Recovery In EM ex-North Asia Has Been Very Subdued

The Recovery In EM ex-North Asia Has Been Very Subdued

The Recovery In EM ex-North Asia Will Continue To Lag EM ex-North Asia’s economic underperformance will continue as many of these nations are lagging in vaccine rollouts and their fiscal and monetary support has been much smaller. Besides, their banks are reluctant to lend due to high NPLs. Chart 67The Recovery In EM ex-North Asia Will Continue To Lag

The Recovery In EM ex-North Asia Will Continue To Lag

The Recovery In EM ex-North Asia Will Continue To Lag

Chart 68The Recovery In EM ex-North Asia Will Continue To Lag

The Recovery In EM ex-North Asia Will Continue To Lag

The Recovery In EM ex-North Asia Will Continue To Lag

Chart 69The Recovery In EM ex-North Asia Will Continue To Lag

The Recovery In EM ex-North Asia Will Continue To Lag

The Recovery In EM ex-North Asia Will Continue To Lag

Chart 70The Recovery In EM ex-North Asia Will Continue To Lag

The Recovery In EM ex-North Asia Will Continue To Lag

The Recovery In EM ex-North Asia Will Continue To Lag

EM ex-TMT Equity Performance Has Been Underwhelming A slow recovery in EM ex-TMT industries explains why EM equity performance outside TMT stocks has been underwhelming. Chart 71EM ex-TMT Equity Performance Has Been Underwhelming

EM ex-TMT Equity Performance Has Been Underwhelming

EM ex-TMT Equity Performance Has Been Underwhelming

Chart 72EM ex-TMT Equity Performance Has Been Underwhelming

EM ex-TMT Equity Performance Has Been Underwhelming

EM ex-TMT Equity Performance Has Been Underwhelming

Chart 73EM ex-TMT Equity Performance Has Been Underwhelming

EM ex-TMT Equity Performance Has Been Underwhelming

EM ex-TMT Equity Performance Has Been Underwhelming

Footnotes

Highlights The post-2008 boom in stocks, corporate bonds, and real estate is a ‘rational bubble’, because the relationship between risk-asset valuations and falling bond yields is exponential. But the ‘rational bubble’ is turning into an ‘irrational bubble’. Stay tactically neutral to stocks for the next few weeks to see whether valuation can revert to rationality. This means keep existing investments in the market, but hold fire on new deployments of cash. If valuation reverts to rationality, then investors can safely deploy new cash into the market. But if valuation moves into irrationality, then it will require a completely different investment mindset, in which fractal analysis will become crucial in identifying the bursting of the bubble, just as it did in 2000. Fractal trade: the Chinese stock market is vulnerable to correction. Feature Chart of the WeekA 'Rational Bubble' And An 'Irrational Bubble'

A 'Rational Bubble' And An 'Irrational Bubble'

A 'Rational Bubble' And An 'Irrational Bubble'

Regular readers will know that we have characterised the post-2008 boom in stocks, corporate bonds, and real estate as a ‘rational bubble’. Rational, because the nosebleed valuations are justified by a fundamental driver. And not just any fundamental driver, but the most fundamental driver of all – the bond yield. However, the ‘rational bubble’ is turning into an ‘irrational bubble’, akin to the dot com mania in which valuations became totally disconnected from fundamentals (Chart of the Week). What should investors do? The Relationship Between Bond Yields And Risk-Asset Valuation Is Exponential Everyone realises that a lower bond yield justifies a lower prospective return from competing investments, such as stocks, corporate bonds, and real estate. As valuation is just the inverse of prospective return, a lower bond yield justifies a higher valuation for all risk-assets. (Chart I-2). Chart I-2House Prices have Decoupled From Rents Again (And It Didn't End Happily Last Time)

House Prices have Decoupled From Rents Again (And It Didn't End Happily Last Time)

House Prices have Decoupled From Rents Again (And It Didn't End Happily Last Time)

But few people realise that a lower bond yield justifies an exponentially higher valuation for risk-assets. To visualise this exponential relationship, look again at the Chart of the Week. The bond yield is plotted on a logarithmic (and inverted) left scale, while the stock market forward price-to-earnings is plotted on a linear right scale. The inverted log versus linear scales demonstrate that, in the ‘rational bubble’, the lower the bond yield, the greater the impact of a given decline in the bond yield on stock market valuation. Few people realise that a lower bond yield justifies an exponentially higher valuation for risk-assets. Chart I-3 and Chart I-4 also demonstrate the exponential relationship using the earnings yield as a proxy for the prospective return on stocks. A 1.5 percent decline in the bond yield had a smaller impact on the earnings yield when the bond yield started at 4 percent in 2014 than when the bond yield started at 3 percent in 2019. At the higher bond yield, the prospective return on stocks fell by 1 percent, but at the lower bond yield, the prospective return on stocks plunged by 2.5 percent. Chart I-3A 1.5 Percent Decline In The Bond Yield Had A Smaller Impact On The Earnings Yield When The Bond Yield Started At 4 Percent...

A 1.5 Percent Decline In The Bond Yield Had A Smaller Impact On The Earnings Yield When The Bond Yield Started At 4 percent...

A 1.5 Percent Decline In The Bond Yield Had A Smaller Impact On The Earnings Yield When The Bond Yield Started At 4 percent...

Chart I-4…Than When The Bond Yield Started ##br##At 3 Percent

...Than When The Bond Yield Started At 3 Percent

...Than When The Bond Yield Started At 3 Percent

To repeat, the lower the bond yield, the greater the impact of a given move in the bond yield on the prospective return from stocks. The intriguing question is, why? To answer this question, we must venture into a branch of behavioural psychology developed by Nobel Laureate Daniel Kahneman and Amos Tversky, called Prospect Theory. Prospect Theory Explains The ‘Rational Bubble’ Prospect Theory’s key finding is that we consistently overvalue the prospect of a tail-event, both positive and negative. For example, if there is a one in a million chance of winning a million pounds, then the expected value of this prospect is one pound. Yet we will consistently pay more than one pound for this positive tail-event. This willingness to overpay for a positive tail-event is the foundation of the multi-billion pound gambling and lottery industry. Now consider an ‘inverse lottery’, in which there is a one in a million chance of losing a million pounds. In theory, we should take on the risky prospect for one pound. Yet in practice, we will consistently demand more than one pound to take on this negative tail-event. In other words, we will demand a substantial ‘risk premium’. Prospect Theory explains that we overvalue tail-events because we are bad at comprehending small probabilities. Hence, the prospect of winning a million pounds, while in practice a negligible possibility, generates excessive optimism which results in overpayment for the bet. Likewise, the possibility of losing a million pounds, while in practice a negligible possibility, generates excessive pessimism, for which we demand payment of a ‘risk premium’. In the financial markets, stock markets tend to ‘gap down’ much more than they ‘gap up’. Hence, the risk of owning stocks is like the discomfort of the inverse lottery. This explains why investors normally demand a risk premium – an excess prospective return – to own stocks versus bonds. However, the risk relationship between stocks and bonds changes when bond yields approach their lower bound. Now, as bond yields have less scope to move down versus up, bond prices can gap down much more than they can gap up. The upshot is that the risk of owning bonds becomes no different to the risk of owning stocks, and the risk premium to own stocks versus bonds disappears. At ultra-low bond yields, the bond yield and the equity risk premium move up and down in tandem. Given that the prospective return on stocks equals the bond yield plus the risk premium, we can now answer our intriguing question. At ultra-low bond yields, the prospective return on stocks moves by more than the move in the bond yield, because the bond yield and the risk premium are moving up and down in tandem. The result is an exponential relationship between the bond yield and risk-asset valuations. And this explains how the post-2008 collapse in bond yields to unprecedented lows has generated a ‘rational bubble’ in stocks, corporate bonds, and real estate (Chart I-5 and Chart I-6). Chart I-5A Rational Bubble In Risk-Assets...

A Rational Bubble In Risk-Assets...

A Rational Bubble In Risk-Assets...

Chart I-6...Everywhere

...Everywhere

...Everywhere

The Rational Bubble Is Turning Irrational The post-2008 boom in risk-asset valuations is rational given the exponential relationship with a collapsed bond yield. But the rational valuation is turning irrational. Over the past few months, the stock market’s forward price-to-earnings multiple has continued to increase despite a backup in the bond yield. Note that this multiple is calculated on the next 12 months of earnings, so it already incorporates a strong post-pandemic earnings rebound (Chart I-7). Chart I-7The Rational Bubble Is Turning Irrational

The Rational Bubble Is Turning Irrational

The Rational Bubble Is Turning Irrational

Furthermore, since 2009, the bond yield (plus a fixed constant) has defined a reliable lower limit for the technology sector earnings yield, meaning a well-defined upper limit for the technology sector’s valuation. Since 2009, this valuation limit has effectively defined the limit of the rational bubble and hasn’t been breached. That is, until now. The recent breach of the post-2008 valuation limit means that the rational bubble is turning irrational (Chart I-8). Chart I-8The Post-2008 Rational Valuation Limit Has Been Breached

The Post-2008 Rational Valuation Limit Has Been Breached

The Post-2008 Rational Valuation Limit Has Been Breached

There are three ways that an irrational valuation can revert to rationality: Stock prices decline. Bond yields decline. Stock prices and bond yields drift sideways while (forward) earnings gradually rise to improve stock valuations. The Investment Decision The decision to be invested in the stock market is probably the most important decision for all investors, including those in Europe. Furthermore, the direction of the stock market is a global rather than a local phenomenon. Our current recommendation is to stay tactically neutral for the next few weeks to see whether risk-asset valuations can revert to rationality. This means keep existing investments in the market, but hold fire on new deployments of cash. Hold fire on new deployments of cash. If valuation reverts to rationality in any of the three ways listed above, then investors can safely deploy new cash into the market. But if valuation turns into irrationality, then it will require a completely different investment mindset. After all, you cannot analyse an irrational market using rational tools! In this case, technical analysis becomes much more important, and front and centre of these techniques is fractal analysis. Specifically, as investors with longer and longer time horizons join the irrational bubble, there will be well-defined moments of heightened fragility, at which correction risk increases. This is what burst the irrational bubble in 2000 (Chart I-9), and will burst any new irrational bubble. Stay tuned. Chart I-9The Dotcom Bubble Burst When All Investment Time Horizons Had Joined It

The Dotcom Bubble Burst When All Investment Time Horizons Had Joined It

The Dotcom Bubble Burst When All Investment Time Horizons Had Joined It

Fractal Trading System* The recent strong rally and outperformance of the Chinese stock market is fragile on all three fractal structures: 65-day, 130-day, and 260-day. A good trade is to underweight China versus New Zealand (MSCI indexes), setting a profit target and symmetrical stop-loss at 9 percent. In other trades, the continued momentum of reflation plays has weighed on some recent positions as well as stopping out short MSCI World versus the 30-year T-bond. Nevertheless, the rolling 12-month win ratio stands at 54 percent. Chart I-10MSCI: China Vs. New Zealand

MSCI: China Vs. New Zealand

MSCI: China Vs. New Zealand

When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Health care remains a top priority of the Democratic Party even though it is flying under the radar at the moment. Health care embodies the shift from small government to big government. While the 2021 budget reconciliation will hit Big Pharma and expand Medicaid, the 2022 reconciliation will seek a public health insurance option and Medicare role in price negotiations. If forced to choose between health care and climate change priorities, Democrats will choose health care. It is a bigger vote-winner. Stay short managed health care relative to the S&P 500. Go long health care facilities and equipment relative to the rest of the health sector. Feature The US Senate acquitted former President Donald Trump on a vote of 57-43 on February 13. No one was hanged.1 The trial was not economically or financially significant except insofar as it underscored peak US political polarization, US distraction from the global stage, and the extent of divisions within the Republican Party. Equity market volatility melted away as stocks surged higher on the generally positive backdrop of COVID vaccines and stimulus. Seven Republicans joined Democrats in voting to convict the former president of “incitement to insurrection.” Trump’s performance was worse than Bill Clinton’s but better than Andrew Johnson’s, though neither Clinton nor Johnson saw defections from their own party (Chart 1). The Republicans’ internal differences are serious enough to hobble them in the 2022 or 2024 elections but it is too soon to draw any hard conclusions. The Democratic agenda is also capable of bringing Republicans back together. Meanwhile the maximum of seven Republican defectors shows that it will be extremely difficult for Democrats to get 10 Republicans to join them in passing any controversial legislation in the Senate (Table 1). Hence the filibuster will remain in jeopardy over the long run if not in the short run. Also, in 2022, the Democrats have a chance to pick up seats in Pennsylvania and North Carolina. Chart 1Trump’s Acquittal And Historic Impeachment Results

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Table 1The Seven Senate Republicans Who Defected From Trump

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Biden’s Agenda After The American Rescue Plan Democrats are plowing forward with the first of two budget reconciliation bills, which enables them to pass legislation with a simple majority in the Senate. They hope to pass President Biden’s $1.9 trillion American Rescue Plan by mid-March, when unemployment benefits expire under the Consolidated Appropriations Act of 2020. The final sum might be a bit less than this headline number. The second budget reconciliation bill, for fiscal year 2022, will be passed in the autumn or next spring and will contain anywhere from $4 trillion to $8 trillion worth of additional spending on health care, child care, infrastructure, and green projects over a ten-year period (Chart 2). This number will be watered down in negotiation as the pandemic subsides and the aura of crisis dies down, reducing the willingness of moderate Democrats to vote for anything controversial. But investors should not doubt Biden’s agenda at this stage. If there is anything we know about the reconciliation process it is that the ruling party will get what it wants. Investors should plan accordingly: the output gap will be closed sooner than expected and inflationary pressures will build faster than expected, even though it will take a while for the labor market to heal. Chart 2Biden’s Agenda AFTER The American Rescue Plan

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

This policy combination of “loose fiscal, loose monetary” policy continues to drive stocks higher (and the dollar lower) despite the misgivings we noted about underrated geopolitical risks (Chart 3). A critical question is when the Fed will normalize monetary policy. This is not an apolitical question. Fed chair Jerome Powell’s term ends in February of 2022. He may contemplate tapering asset purchases prior to that date, causing troubles in the equity market, but actual tapering is more likely to occur in 2022, in the view of our US Bond Strategist Ryan Swift. Powell would only taper in 2022 if he is forced to do so by an ironclad policy consensus precipitated by robust inflation and possibly financial instability concerns. This timing gives President Biden an opportunity to nominate an ultra-dovish Fed chair. Rate hikes are entirely possible in 2022 but our political bias implies they are unlikely before 2023 (unless an ironclad consensus develops that they are necessary). Even in 2023, an ultra-dove will be reluctant to hike, depending on the context. And rate hikes are virtually off limits in 2024, at least until after the November election. This political timeline reinforces the view that the Fed will not be hiking anytime soon and investors should prepare for inflation risks to surprise to the upside over the coming years. Chart 3"Easy Fiscal, Easy Monetary" Policy Combination

"Easy Fiscal, Easy Monetary" Policy Combination

"Easy Fiscal, Easy Monetary" Policy Combination

The Senate parliamentarian has not yet ruled whether a federal minimum wage hike to $15 per hour can be included in the bill. Biden has accepted it may be cut but his party will push it through if possible. Last week we found that a higher minimum wage would not have a dramatic macroeconomic impact. Still, wages will rise in the coming years due to the cumulative effect of the Democratic Party’s policies. Higher wages, taxes, and regulatory hurdles will cut into corporate profits. But the passage of a higher minimum wage today would not in itself be a negative catalyst for equities. Rather, we would expect the rally to take a breather once the first reconciliation bill is finished (next week or in the coming weeks), since it will bring wage hikes, rate hikes, and tax hikes more clearly into view on the investment horizon. Unlike minimum wages, there is little controversy over whether budget reconciliation can be used to change the health care system. This was done in 2010 as the second critical part to President Barack Obama’s Affordable Care Act (Obamacare). Hence Biden is highly likely to get his health agenda passed, which is largely an agenda of entrenching and expanding Obamacare. That is, as long as he prioritizes health care above other structural reforms like climate change. We think he will. In the rest of this report we look at Biden’s health care policy and the implications for US financial markets. Biden’s Health Care Policy Health care has been a top priority of the Democrats since 1992 yet they have repeatedly lost control of the agenda due to surprise Republican victories in 2000 and 2016. Republicans expanded Medicare under Bush but then failed to repeal and replace Obamacare under Trump. Now Democrats have only the narrowest of majorities in the House and Senate and will push hard to solidify and build on Obamacare. There is a low chance that they will leave this issue unsettled under the Biden administration. If new obstacles arise, more political capital will be spent to secure health care reform at the expense of other policies on the agenda. COVID-19 reinforces the Democrats’ focus on health care. The US has seen around 1,500 deaths per million people, making it one of the worst performers amid the crisis, comparable to the UK and Italy (Chart 4). Yet COVID is only the latest in a line of US public health failings and it is important to put COVID into perspective. For example, among US adults aged 25-44 years old, all-cause excess mortality from March to July last year was about 11,899 more than expected. By contrast, during the same period in 2018, there were 10,347 unintentional deaths due to opioids (Chart 5).2 In other words, the COVID crisis last year was comparable to the opioid crisis in magnitude, at least for middle-aged people. Obviously COVID has taken a terrible toll and is a more deadly disease for the old and the sick. The point is that the public’s wrath over poor public health and the US government’s ineffectiveness is well established. A pandemic was foreseeable, and foreseen, yet not prepared for, and it came on top of the opioid crisis and the debate about 30 million Americans who lack health insurance. The Biden administration has the intention and the capability to address these issues. Chart 4US Handling Of COVID-19 Left Much To Be Desired

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Chart 5Opioid Crisis Versus COVID Crisis

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

The structural problem is well-known: The US spends more than other countries on health care but achieves worse results (Charts 6A & 6B). When workers get fired they lose health care, as insurance is tied to employment. Those whose employers do not provide health care or who are unemployed count among the ranks of the roughly 30 million uninsured. This number has fallen from its peak at 47 million in 2010 when Obamacare was enacted but has crept upward again since Trump’s attempt to dismantle that law and the lockdowns of 2020 (Chart 7). This is a driver of popular discontent that has proven again and again to generate votes, including in key swing states. Chart 6AThe US Spends More On Health Care …

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Chart 6B… But Sees Worse Avoidable Mortality

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Chart 7Rising Number Of Uninsured Even Pre-COVID

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

A range of public opinion polling over many years shows that health care is a close second or third to the economy and jobs in voter priorities. Voters care more about COVID and health care than they do about climate change and the environment (Chart 8, first panel). Chart 8Public Opinion On Biden’s Priorities: Jobs, Health, Then Climate

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Another important takeaway from this opinion polling is that voters could not care less about budget deficits. Big spending solutions are all the rage (Chart 8, second panel). The Biden administration is prioritizing economic recovery and the pandemic response but will also pursue its health care reforms. If this policy requires a tradeoff with infrastructure and renewables, we would expect health care to get the greater attention. Over the long run Obamacare can be replaced but not repealed. The law is getting more popular over time and entitlements get harder to repeal over time. Slightly more than half of voters have a favorable view of the law and only 34% have an unfavorable view. Only 29%of voters want to repeal or scale back the law while about 62% want to build on it or keep it as it is (Chart 9). Underscoring this polling is the fact that the law was modeled on a Republican plan and even Trump adopted several of the most popular provisions: requiring insurance coverage for patients with preexisting conditions and slapping caps on pharmaceutical prices through import and pricing schemes. The Supreme Court has ruled Obamacare constitutional and is not expected to change that ruling this spring. It could object to the individual mandate – the most controversial part of Obamacare that required each person to pay a tax penalty if they did not purchase health insurance. But if parts of the law are stricken, Democrats have the votes to patch it up or provide an alternative. Chart 9Obamacare Has Grown On American Public

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Biden simultaneously shows that Democrats rejected the most popular alternative to Obamacare – “Medicare for All,” or single-payer government-provided health care – at least for the current presidential cycle. Medicare for All was co-sponsored by Vice President Kamala Harris and is still a long-term goal of the progressive wing of the Democratic Party. However, voters do not like the proposal when asked about its practical consequences (Chart 10). In the Democratic primary, only Senators Bernie Sanders and Elizabeth Warren argued for wholesale revolution in US health care that would see private insurance cease to exist and 176 million voters moved onto a public health system. Sanders’s plan would have cost an estimated $31 trillion, increasing the budget deficit by $13 trillion over 10 years, and would have encouraged the overuse of medical services due to the absence of a co-pay or fixed cost. This idea will not vanish but the Biden administration’s likely success in expanding Obamacare will lead the party to focus on other things (e.g. climate change). Chart 10Insufficient Public Demand For Government-Provided Health Care (For Now)

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Biden’s big proposal is to add a public insurance option that would exist alongside current private insurance options. This idea was originally part of Obamacare but was removed during negotiations – precisely because the Democrats eschewed the use of budget reconciliation (again, not a constraint this time).3 The Biden plan is estimated to cost $2.25 trillion over 10 years and includes larger subsidies, the ability of workers to choose whether they want their employer-provided plan or the public option, automatic enrollment, a lower age of eligibility for Medicare (from 65 to 60), drug price caps, and various other provisions (Table 2). Table 2Biden’s Health Care Plan

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Medicare, a giant consumer, would be able to negotiate drug prices directly with companies to drive down the price. Tax hikes on high-income earners and capital gains would pay for Biden’s policy. With public backing and full Democratic control of Congress, there is little that can stop Biden from achieving this health care policy, other than a change in direction from his party, which we do not expect. The first budget reconciliation only contains small parts of the Biden agenda, such as incentives for states to expand Medicaid under Obamacare and a reduction in Medicaid rebates for drug manufacturers.4 The second budget reconciliation process will have to cover health care and tax hikes. But the consensus view is that the second reconciliation will focus on infrastructure and green energy. This is a conflict of priorities that will have to be resolved. The research above suggests it will be resolved in favor of health care. This would leave the regular budget process as the means to advance infrastructure and green projects. Macro Impact Of Biden’s Health Care Policy The great health care debate over the past decade reflected the broad post-Cold War debate in the US over the role of government in the economy. It centered on whether government involvement should increase to expand health insurance coverage. Although private US health care spending accounts for 31% of total health care spending, and is thus larger than either Medicare (21%) or Medicaid (16%), the government has control of 44% of spending when all of its functions are added together. This share is set to increase now that the debate has been decided in favor of Big Government (at least for now). Future administrations might carve out more space for private choice and competition in health care but a permanent step-up in government involvement and regulation has occurred given the above points about Obamacare’s irrevocability. What are the macro consequences of such a change? The imposition of Obamacare may have contributed to the sluggish economic recovery in the wake of the Great Recession but the case is hard to examine objectively because the tax penalties only took effect in 2015-16 and then a new administration ceased implementation in 2017. In 2015 the Congressional Budget Office estimated that repealing Obamacare would increase the budget deficit by $353 billion over a ten year period but that it would also increase GDP by an average of 0.7% per year during the latter end of full implementation, thus boosting revenues and producing a net $137 billion increase in the budget deficit over ten years.5 In other words, Obamacare marginally tightened fiscal policy and encouraged some workers to cut their hours or stop working due to expanded subsidies, tax credits, and Medicaid eligibility.6 Repealing it would have reduced the tax burden on corporations and reduced the subsidy benefits to households but possibly with a slight boost to growth (Chart 11). Going forward, Biden’s policies are adjustments rather than a total overhaul but they would ostensibly add $2.25 trillion in spending and $1.4 trillion in revenue, resulting in a negative impact on the budget deficit (fiscal loosening) of $850 billion. The implication is that Biden’s plan would increase rather than decrease aggregate demand, albeit marginally in an era of already gigantic deficits. It would also remove some labor supply and eventually drag on GDP growth. Yet the impact of these effects is still uncertain given the general context of loose fiscal and loose monetary policy, the reduction in the number of uninsured people, and the potentially positive second-order effects of this increase in the social safety net for low-income families with high marginal propensities to consume. The bottom line is that the macro effects of Biden’s health plan will not be known for many years but the headline effect in the short run is an incremental addition to an already extremely loose fiscal policy setting. Chart 11Macro Effects Of Obamacare Repeal

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

The negative effects will largely fall on high-income earners, capital gains earners, and corporations who will provide the revenue to pay for the plan. The private health insurance industry faced an existential threat from the Sanders plan but it still faces a loss of customers and earnings from the Biden plan. The major difference between Obamacare and Bidencare is that Obamacare forced insurance companies to provide a basic insurance option to the public but did not offer a public option to compete with them. Therefore their customer base increased albeit at a lower profit. Whereas Biden’s plan will create a public competitor that will siphon off customers from private insurance. Biden proposed giving workers this choice anytime but in the presidential debates suggested there would be limits. Either way private insurers stand to lose customers over time. This is not a major political constraint given that Big Insurance gets little sympathy from the public but it will have a negative impact on innovation and productivity in the health sector. Meanwhile Medicare would reimburse hospitals, clinics, and drug providers less for their services and goods. This would weigh on the profitability of small and private medical outfits and favor large and public providers that receive government subsidies and can stomach higher costs. It would also take a toll on Big Pharma and biotech sectors which have operated in a lucrative environment of low taxes, low regulation, and sizable pricing power. The US government has enormous negotiating power in the market, especially over home care, hospitals, nursing homes, and prescription drugs. Private and public investment are roughly evenly split, with public money dominating health care research and private money dominating structures and equipment. The government accounts for about 40% of total drug spending and both political parties believe this influence should be used to keep costs down, as public opinion is increasingly dissatisfied with high drug costs.7 There is a lot more to be said about the US health care system. A risk of Biden’s health reform is that it will increase the demand for health services without arranging for consummate increases in supply. In this sense it is inflationary. Investment Takeaways Health care stocks and each of the health care sub-sectors – pharmaceuticals, biotech, managed health care, facilities, and equipment – underperformed the S&P500 index amid the passage of Obamacare from March 23 to November 20, 2010. Within the sector, managed health care (health insurance) and biotech suffered most when the legislation first hit while facilities and equipment suffered most over the whole legislative episode. Once the law took full effect in 2014-15, equipment and managed health care outperformed, facilities were flat, and pharma and biotech underperformed. A look at the performance of the health care sector relative to the S&P 500 over the past 13 years shows that the sector rallied on President Obama’s victories in 2008, fell during the passage of Obamacare, staged a recovery that continued through the Supreme Court’s decision to uphold the new law in June of 2012, and then dropped off (Chart 12 A). Health stocks benefited from the global macro backdrop from 2011-15. After 2015, when Obamacare took full effect, the business cycle entered its later stage, and populism emerged (with Sanders threatening a government takeover and Trump firing up the cyclical economy), health care stocks underperformed the market. Chart 12AHealth Sector's Response To Obamacare Saga

Health Sector's Response To Obamacare Saga

Health Sector's Response To Obamacare Saga

Subsequent rallies have occurred, notably on the outbreak of COVID-19, but have not been sustainable. When Republicans failed to repeal Obamacare, when various crises gave defensive plays a tailwind, when Biden won the Democratic nomination over Sanders or Warren, and when the pandemic arose, the sector surged, often due to risk aversion in financial markets. In the end the negative trend reasserted itself as the combination of rising risk sentiment and policy headwinds outweighed the underlying demographic tailwind for earnings as society aged. Since the Democratic sweep of government in the 2020 elections the sector is testing new lows in relative performance. Pharmaceuticals charted a similar course to the overall health sector but never regained their pre-Obamacare peak in relative performance. They have underperformed again and again since the rise of Bernie Sanders and are today touching new lows (Chart 12B). Chart 12BBig Pharma's Response To Obamacare Saga

Big Pharma's Response To Obamacare Saga

Big Pharma's Response To Obamacare Saga

A closer look at the sector since the 2020 election and especially the Democratic victory in the Senate shows that it continues to underperform the broad market. Facilities are the most resilient, pharma and biotech are trying to find a bottom, and equipment and managed health care have sold off. Relative to the health care sector, equipment and facilities are the outperformers but, again, pharma and biotech are trying to bottom (Chart 13). These results make sense as Biden’s biggest policy impact will be to stimulate demand for health care facilities and equipment while constraining profits for Big Insurance and Big Pharma via the public insurance option and allowing Medicare to negotiate drug prices. Thus equipment and facilities benefit from the political environment, pharma and biotech should be monitored to see if they break down to new lows on the passage of legislation, and managed health care gets the short end of the stick. Our US Equity Strategy service is neutral on the sector as a whole, overweight equipment, and underweight pharma. Chart 13Health Care Sector Response To Biden's Democratic Sweep

Health Care Sector Response To Biden's Democratic Sweep

Health Care Sector Response To Biden's Democratic Sweep

Putting it all together, health care stocks are good candidates for a short-term, tactical bounce when the exuberant stock rally suffers a correction but they are not yet candidates for strategic investments. They are not likely to find a bottom until Biden’s policies are passed, or the pro-cyclical macro backdrop has changed. Biden’s policies are high priority for his party and face low legislative and political hurdles to passage, yet will have a huge impact on the relevant industries – undercutting the private health insurance customer base and capping the profits of America’s drug makers. These changes will have long-term ramifications so they are not likely to be fully discounted yet. Previously health care firms had huge pricing power – they could charge whatever they wanted while they did not face the full might of the government in setting prices – but going forward that will change. Biotech and pharma have large profit margins that are exposed to this policy shift so they are exposed to further downside – we would not be bottom-feeders. Moreover pharmaceuticals make up 28% of the health sector while biotech makes up 13%, so that these sectors will weigh down the whole sector. One would think that health care would outperform during a global pandemic – and most sectors did see a big bounce during the height of the COVID-19 outbreak. But the pandemic has created the impetus for a stimulus splurge that has fired up the cyclical parts of the economy. It has also underscored the industry’s public role and undercut its profit-making capabilities, not least by producing a Democratic sweep bent on improving US health outcomes – at the expense of US health industry profits. In sum, from a tactical point of view, health care stocks are well-positioned for a near-term rally in relative performance but from a strategic point of view they continue to face policy headwinds and should be underweighted relative to the broad S&P 500. Tactically, stay short the managed health care sub-sector relative to the S&P 500 (Chart 14). Strategically, go long health care facilities and equipment relative to the health care sector. Chart 14Health Stocks Outlook Under Biden Administration

Health Stocks Outlook Under Biden Administration

Health Stocks Outlook Under Biden Administration

Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Jesse Anak Kuri Associate Editor jesse.Kuri@bcaresearch.com Appendix Table A1APolitical Capital: White House And Congress

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Table A1BPolitical Capital: Household And Business Sentiment

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Table A1CPolitical Capital: The Economy And Markets

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Table A2Political Risk Matrix

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Table A3Biden’s Cabinet Position Appointments

Don't Forget Biden's Health Care Policy

Don't Forget Biden's Health Care Policy

Footnotes 1 During the election crisis [of 1876], Kentucky Democrat Henry Watterson urged that “a hundred thousand petitioners” and “ten thousand unarmed Kentuckians” go to Washington to see that justice was done. Years later, when he was sitting next to [Ulysses S.] Grant at a dinner party, Watterson told him, “I have a bone to pick with you.” “Well, what is it?” asked Grant. “You remember in 1876,” said Watterson, “when it was said I was coming to Washington at the head of a regiment, and you said you would hang me if I came.” “Oh, no,” cried Grant, “I never said that.” “I am glad to hear it,” smiled Watterson. “I like you better than ever.” “But,” added Grant drily, “I would, if you had come.” See Paul F. Boller, Jr, Presidential Campaigns: From George Washington To George W. Bush (Oxford: Oxford University Press, 2004 [1984]), p. 141. 2 See Jeremy Samuel Faust, Harlan M. Krumholz, and Chengan Du, “All-Cause Excess Mortality and COVID-19-Related Mortality Among US Adults Aged 25-44 Years, March-July 2020,” Journal of the American Medical Association, December 16, 2020, jamanetwork.com. 3 The death of Senator Edward Kennedy forced the Democrats to use reconciliation for the second part of President Obama’s health care reform, the Healthcare and Education Reconciliation Act of 2010. 4 Currently the Medicaid rebate cap is set at 100% of the cost of making a drug. Other provisions would include a boost for rural health care services (a partial reallocation of headline COVID relief funds) and an expansion of Obamacare tax credits and subsidies for unemployed workers to keep their former employer-provided insurance. These are mainly COVID relief measures rather than aspects of Biden’s long-term health agenda. See Julie Rovner, “KHN’s ‘What the Health?’: All About Budget Reconciliation,” Kaiser Family Foundation, February 11, 2021, khn.org; see also Nick Hut, “A look at some of the healthcare-specific provisions in the pending COVID-19 relief legislation,” Healthcare Financial Management Association, February 10, 2021, hfma.org. 5 For the CBO’s original report on repeal, see “Budgetary and Economic Effects of Repealing the Affordable Care Act,” Congressional Budget Office, June 19, 2015, cbo.gov. More recently see Paul N. Van de Water, “Affordable Care Act Still Reduces Deficits, Despite Tax Repeals,” Center for Budget and Policy Priorities, January 9, 2020, cbpp.org. 6 See BCA Global Investment Strategy, “The Fed’s Dilemma,” May 12, 2017 and “Four Key Questions On The 2018 Global Growth Outlook,” January 5, 2018, bcaresearch.com. Regarding the debate around Obamacare, promoters highlight the recovery in US growth and jobs – including full-time jobs and small-business jobs – by 2015. Critics say the recovery would have been stronger if not for the law. See e.g. Casey B. Mulligan, “Has Obamacare Been Good for the Economy?” Manhattan Institute, Issues Brief, June 27, 2016, manhattan-institute.org; Cathy Schoen, “The Affordable Care Act and the U.S. Economy: A Five-Year Perspective,” Commonwealth Fund, February 2016, commonwealthfund.org. 7 Republican Senator Chuck Grassley co-sponsored a bill with his Democratic counterpart Ron Wyden of Oregon that would penalize drug companies that raised drug prices faster than inflation. In a separate bill with Senator Amy Klobuchar of Minnesota, he also proposed to prevent big name drug companies from paying generic drug-makers to delay the introduction of generics to the market. These bills were not debated on the main floor because then-Senate Majority Leader Mitch McConnell was unenthused about them but they exemplify the bipartisan consensus on government intervention to push down drug prices.

Last year we created two baskets of stocks to capture the economic reopening theme by constructing a long/short pair trade. This year, we crystallized 21.5% in gains from that pair trade and subsequently reopened it. Today, we take a new angle at the economic reopening theme and pit “Back-To-Work” laggards against leaders. First, we filtered for well-behaved cyclical industries among all the sectors and sub-sectors we cover. We define a well-behaved cyclical industry as one that trailed the SPX from February 19, 2020 to March 23, 2020; and then outpaced the broad market from March 23, 2020 to today (all computations are in relative to SPX terms). Chart 1

How To Play The Reopening Trade Now Using US Equity Baskets

How To Play The Reopening Trade Now Using US Equity Baskets

Such filtering excluded all of the defensive & cyclical industries that outperformed the market during the recession, and it also excluded those industries that were too damaged by the pandemic and could not recover above the March 23rd trough level (for example, airlines) always in relative terms. The appendix on page 4 has a stylized depiction of our analysis. In total 27 industries survived the filtering. We then computed what is the minimum percentage increase required in order for each group to recover to its February 19 level, and then calculated the difference between that required increase and the one that actually materialized. A positive value signifies that the sector climbed above its February 19 level, whereas a negative value means that the sector still has not recovered. Chart 1 displays the results. Our rationale is as follows: should the economic recovery and normalization themes continue unabated as we expect, then the risk/reward trade-off of owning the “laggards” is greater than the “overshooters”: the former have ample upside potential left, whereas the latter are already discounting a lot of good news. We deem there is an exploitable opportunity within the reopening theme and today we recommend investors institute a new long reopening industry “laggards”/short “overshooters” pair trade (excluding the GICS1 sectors). Chart 2

How To Play The Reopening Trade Now Using US Equity Baskets

How To Play The Reopening Trade Now Using US Equity Baskets

Chart 2 plots the ratio of the two baskets against the ISM manufacturing prices paid sub-component and the 10-year US Treasury yield and supports our rationale that the “laggards” have a long runway ahead versus the “overshooters”. Finally, as a proxy for this trade we also include tickers for the largest stock in each sub-sector (excluding GICS1). Laggards: V, BLK, HCA, MCD, HON, AXP, JPM, COP, PSX, MAR, SLB. Overshooters: EMR, BLL, LIN, NUE, UNP, HD, DHI, CAT, MS, J, TSLA, AMAT. We are aware of some minor conflicts between the “Overshooters” and the “Back-To-Work” basket and also versus our current recommendations table, but we still recommend investors put on this trade pair trade. Bottom Line: Institute a new long USES “Laggards” basket/short USES “Overshooters” basket pair trade. Appendix

How To Play The Reopening Trade Now Using US Equity Baskets

How To Play The Reopening Trade Now Using US Equity Baskets

A Positive For The Rally

A Positive For The Rally

In the last week’s Strategy Report we highlighted how the often-heavy-lifting tech sector’s profit growth contribution to calendar 2021 SPX earnings is giving way to other GICS1 industries. Historically, the tech sector commanded the lion’s share of profit explanation for the SPX, but not in 2021. In fact, the S&P IT sector is ranked 4th in terms of contribution to overall SPX profits, behind industrials, financials and consumer discretionary (see chart). Additionally, the tech sector no longer sports an earnings weight similar to its market cap weight as it has run ahead of itself. This is also the case because the rest of the sectors are playing catch up this year as the US economy is slated to reopen on the back of the herculean inoculation efforts (profit weight and mkt cap weight columns, Table 1). In fact, the metric of market cap weight minus the sector’s earnings weight is a rough valuation measure highlighting that tech stocks are 5x to 10x more expensive than their deep cyclical peers (industrials, materials and energy, last column, Table 1). Bottom Line: A broader-based participation in the equity rally is a healthy backdrop for the cyclical return prospects of the SPX. Table 1

A Positive For The Rally

A Positive For The Rally

Last week, we observed that evidence from the past decade suggests that higher yields are not always a risk to stock prices, as long as the yield increase reflects favorable economic conditions, which also push up the dividend growth rate. Evidence from a…

Semiconductor equities continue to defy gravity. Semiconductors are a high beta play on the global recovery and the strength of the technology sector. That has made them a prime beneficiary of the reflationary environment that has been crucial to the stocks…

European equities lagged US ones throughout the bulk of last year, and continue to do so in 2021. Several factors explain this mediocre performance. The euro’s strength tightened monetary conditions in the euro area and is weighing on corporate…

Prepare To Lock In Gains In The Cyclicals/ Defensives Portfolio Bent

Prepare To Lock In Gains In The Cyclicals/ Defensives Portfolio Bent

Chinese data is waving a red flag as we highlighted in this Monday’s Strategy Report where we also instituted a 2.5% rolling stop to the cyclicals vs. defensives ratio. Not only are the Chinese authorities trying to engineer a slowdown with the recent reverse repo operations, but also BCA’s China Monetary Indicator and the selloff in the Chinese sovereign bond market are all corroborating the economic deceleration signal (top & middle panels). Railway freight (and infrastructure spending) data also highlight that not everything is as rosy as it appears to the naked eye in the Middle Kingdom, giving us even more reasons to worry about the longevity of the US cyclical/defensive bull market run (bottom panel). Finally, the cyclical/defensive ratio is sitting 14% above its 200-day moving average confirming the dual stretched message that our valuation and technical indicators are emitting (not shown). Bottom Line: We put a 2.5% rolling stop on the cyclicals vs. defensives ratio in order to protect gains north of 17% since inception. Should it get triggered, we will downgrade the ratio from overweight to neutral via trimming the niche materials sector to a benchmark allocation. Stay tuned.

Highlights Volatility subsided but we still think geopolitical risk is underrated in the near term. The new Biden administration faces critical tests on China/Taiwan and Iran. The Biden-Xi phone call did not resolve anything. We recommend investors hedge geopolitical risk by adding a tactical long CHF-USD. The medium-to-long-term macro backdrop is shifting in favor of frontier markets – but it is too soon to dive in. African frontier markets have not yet benefited from the global economic recovery – and may face more pain in the near term. The Ethiopian crisis will further destabilize the Horn of Africa region. Kenya is the relative beneficiary in geopolitical terms, though Kenyan stocks are expensive relative to other frontier markets. Feature Volatility subsided over the past two weeks, global stocks rallied, and bond yields rose. The US dollar bounce lost some of its steam. From a macro point of view, we understand investor exuberance. But from a geopolitical point of view, risks are now understated. President Joe Biden faces imminent tests from China, Iran, and Russia. Table 1 provides a checklist of what we need to see to conclude that a new US-China modus vivendi has been established. The phone conversation between Presidents Biden and Xi Jinping on February 10 is marginally positive but, judging by history, the call shows that tensions remain high.1 Until these conditions are met the two sides are hurtling toward a diplomatic crisis over the Taiwan Strait sometime after China emerges from its annual National People’s Congress. Incidentally, China’s ongoing policy shift toward slower and more disciplined growth will be the takeaway from this year’s legislative session, which is not positive for global cyclicals or China plays beyond the near term. China’s credit impulse has decisively rolled over and the combined fiscal-and-credit impulse is peaking now (Chart 1). Table 1First Biden-Xi Call Did Not Resolve US-China Tensions

Frontier Markets And The Ethiopian Crisis

Frontier Markets And The Ethiopian Crisis

Chart 1China's Fiscal-And-Credit Stimulus Peaking Now

China's Fiscal-And-Credit Stimulus Peaking Now

China's Fiscal-And-Credit Stimulus Peaking Now

A crisis is also brewing in the Middle East. Iran is not going to abandon its quest for nuclear weapons over the long run but it is willing to negotiate a deal in the short run that reduces US sanctions. Especially if lame duck President Hassan Rouhani gets it done before he steps down in August. The next Iranian president will not want to make the same mistake Rouhani made and bet his future on the unreliable United States. This requires Biden to rejoin the existing 2015 nuclear deal with a vague commitment to negotiate a better deal later. However, this outcome is precisely what Israeli officials have called a “calamity.” 2 The Biden team gives Iran three-to-four months before it has enough highly enriched uranium to make a bomb – it wants to move quickly on negotiations. Israel gives it a year – it wants to convince the Democrats to stick with Trump’s maximum pressure. Either way the first half of this year is crunch time. Otherwise Iran’s new administration will require a much longer negotiation. Negotiations will be checkered with attacks to demonstrate credible threats and red lines. Ultimately, since we expect Biden to forge a US-Iran détente, and since the China/Taiwan risk is negative for energy prices, we no longer express our Iran view in the form of a long oil position. Brent crude is close to our Commodity & Energy Strategy’s $63 per barrel target for this year’s average. The Saudis could abandon their production discipline when Iranian oil gets closer to coming online. Investors should distinguish these immediate geopolitical risks from the general, long-running US-China and US-Iran conflicts. These will wax and wane while global risk assets grind upward over the long haul. If China avoids over-tightening policy and the Biden administration passes early hurdles we will be more bullish. For now we recommend investors hedge their bets by increasing exposure to safe-haven assets. We remain long gold and Japanese yen. Tactically we recommend going long the Swiss franc versus the dollar as well. Finally, in what follows, we take a sojourn from these headline geopolitical risks to offer a special report on the Ethiopian crisis and implications for Africa, Europe, and frontier markets. Now is not the right time to dive headlong into African frontier markets given the risks outlined above but we do see an opportunity on the horizon. Is The Ethiopian Crisis Investment Relevant? Ethiopia is now in its fourth month of crisis. The country is grappling with internal conflict brought upon by political and ethnic differences among the former and current ruling elite. Over the past week, Ethiopian Prime Minister Abiy Ahmed spoke with US Secretary of State Antony Blinken, French President Emmanuel Macron, and German Chancellor Angela Merkel about reports that Eritrean soldiers have entered the fray. East Africa will become increasingly unstable as conflict persists, threatening security, migration, and investment into the region. Investors looking to frontier markets in light of the global liquidity explosion should exercise caution. Peacemaking Abiy Goes On The Offensive Ethiopian government forces continue to battle a minority group, the Tigray People Liberation Front (TPLF), in the north of the country. Large-scale attacks, like those seen at the start of the conflict, have mostly diminished. However, both sides continue to maintain their offensive positions. With the recent entry of Eritrean forces into Ethiopia to support the government’s battle against the TPLF, conflict between government forces and the TPLF will continue at the very least. Tensions between the government of Prime Minister Abiy and the Tigray people have been in play for years. The Tigray largely dominated Ethiopia’s ruling coalition and security forces until the past decade. Public protests in 2015 were driven by frustration over laws that denied Ethiopians basic civil and political rights. In 2018, a popular uprising brought Abiy to power and he ushered in democratic reforms and an end to conflict with neighboring Eritrea. Abiy’s “reforms” are so far of limited relevance to investors. He released several high-profile political prisoners, lifted a draconian state of emergency, and planned to amend the constitution to institute term limits for prime ministers. Some civil liberties were restored. The investment-relevant aspect of the reforms were proposals to end government monopolies in key economic sectors, including telecommunications, energy, and air transport – but these have yet to happen. Abiy was most eager to dismantle Ethiopia's previous ruling party, the Ethiopian People's Revolutionary Democratic Front (EPRDF), which was dominated by the Tigray and had run the country for 28 years. Abiy supplanted the EPRDF with a single national Prosperity Party, which was not organized on ethnic lines. Having controlled all facets of state power prior to its ouster in 2018, the TPLF views Abiy’s democratic reforms and proposals for economic liberalization with anxiety. Abiy’s interest in reforming the federalist structure of the Ethiopian state - which divides Ethiopia into nine self-governing ethnic territories - threatens to undermine the order that has historically permitted the small Tigrayan ethnic group to wield a power disproportionate to its population (Chart 2). Chart 2Major Ethnic Groups In Ethiopia

Frontier Markets And The Ethiopian Crisis

Frontier Markets And The Ethiopian Crisis