Equities

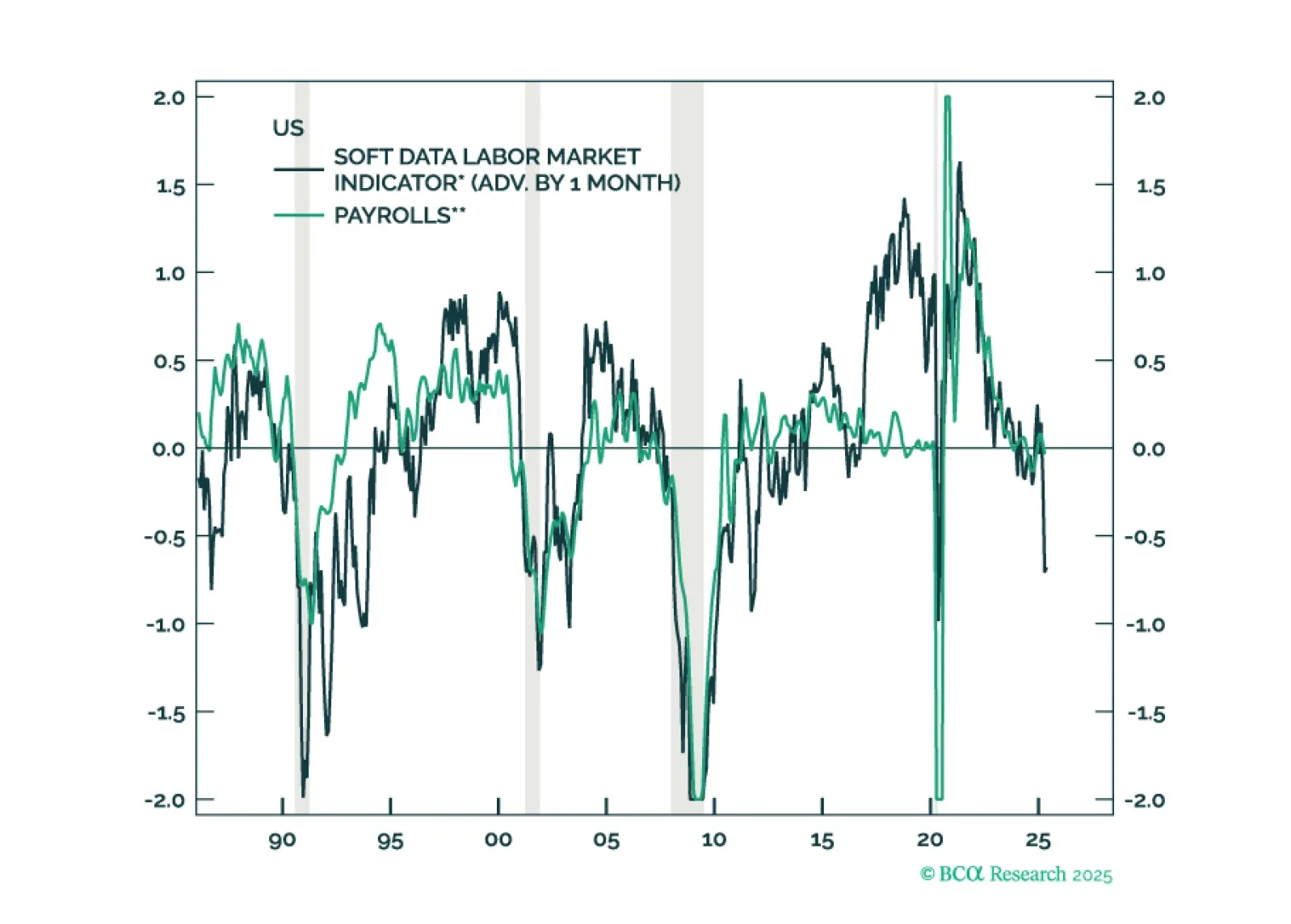

It may take several months for the tariff shock and policy uncertainty to filter through the real economy, but survey-based data are already sending a warning. Equities have priced in a lot of good news, and investors are too sanguine about the risk of a US recession.

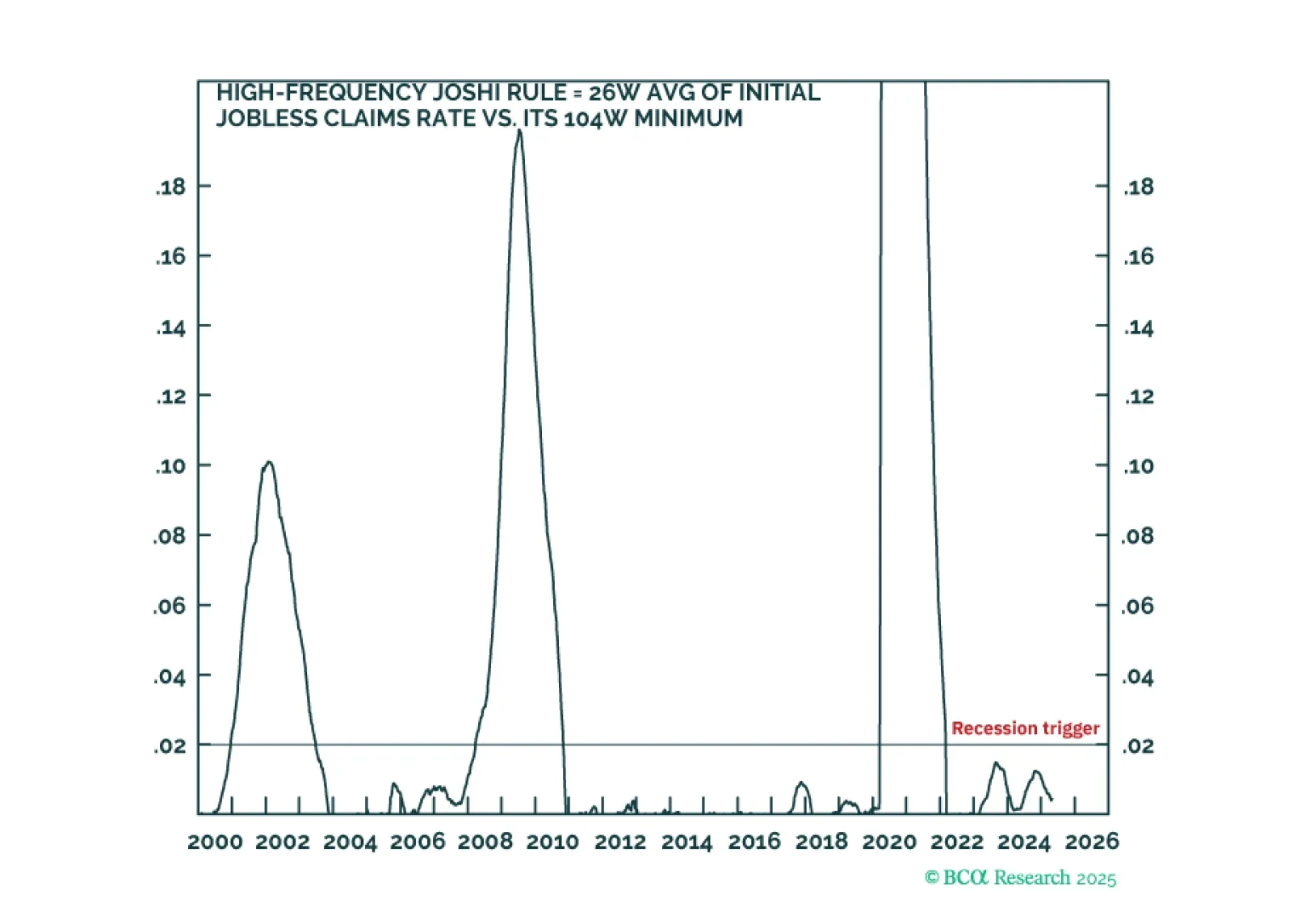

Today, we are introducing an additional ‘high-frequency Joshi rule’ which is updated weekly. The Joshi rules tell us that a US recession is not imminent. Until the Joshi rules are triggered, overweight non-US government bonds, and especially UK gilts, versus US T-bonds. And shift cyclical asset allocation from overweight to neutral-weight bonds. Plus: tactically long USD/GBP and tactically underweight global industrials (EXI).

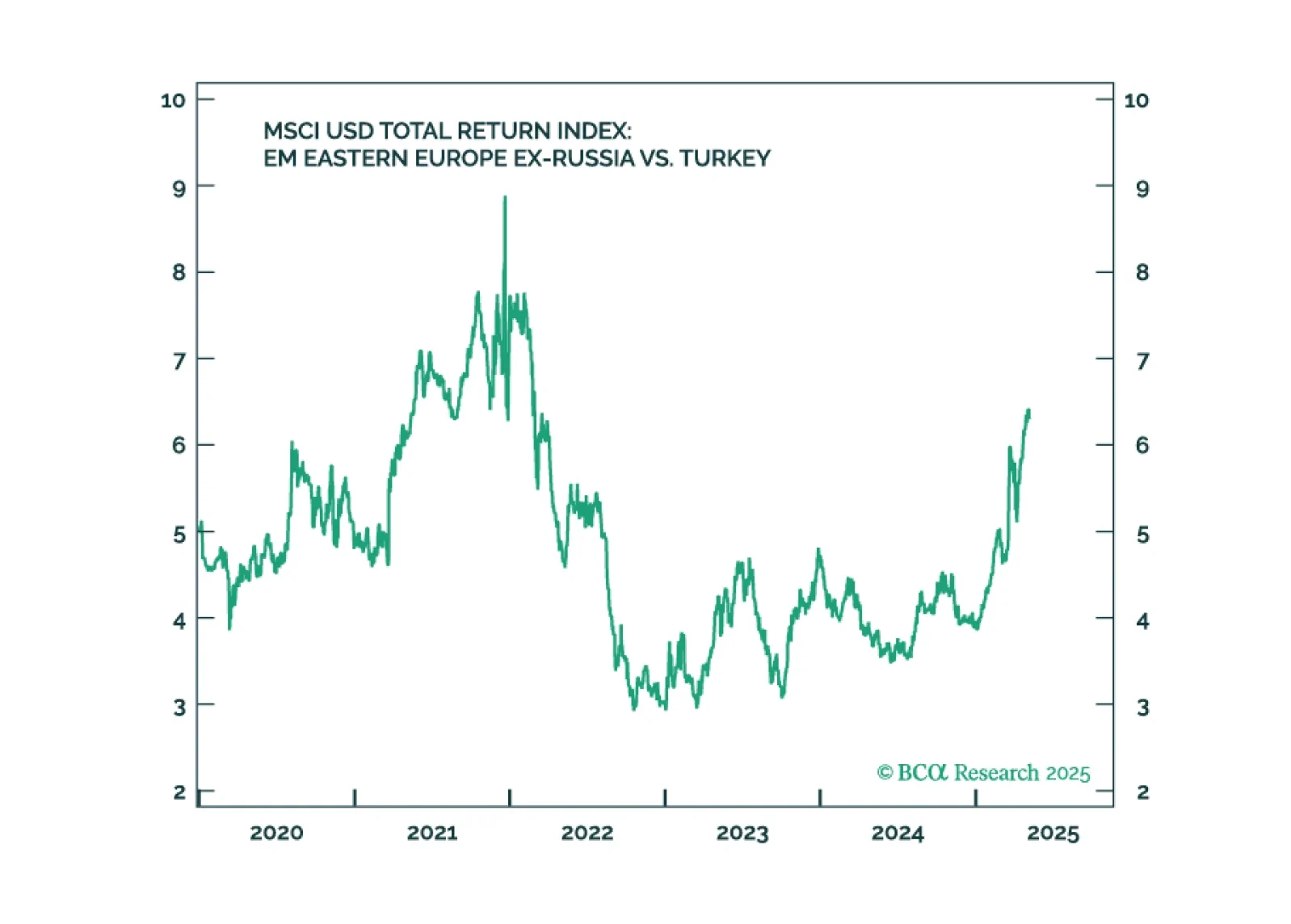

Erdogan's rule continues to decline. Social unrest will persist, governance will erode, and the macro backdrop will deteriorate further. We recommend underweighting Turkish assets.

Negotiations on trade, Iran, and Ukraine will prove critical this month. Markets will remain volatile because positive data surprises enable the White House to press its hawkish tariff hikes, while negative surprises force the White House to backpedal.

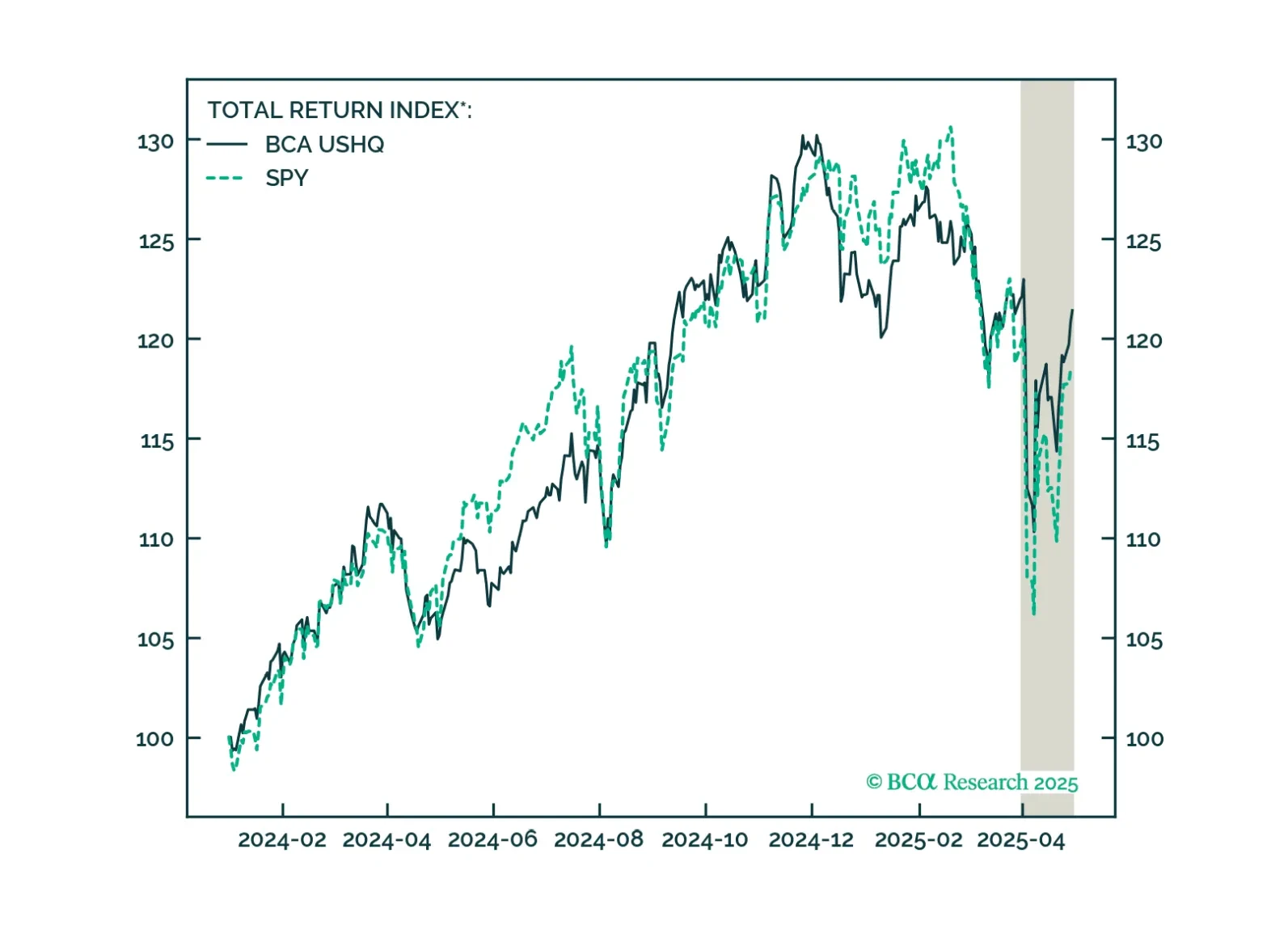

The US High Quality (USHQ) portfolio outperformed on the margin through April, returning -0.6%, whilst its SPY benchmark returned -1.2%. On a trailing three-month basis, performance remains robust vs. benchmark, with USHQ generating +230bps of excess return. Volatility and drawdown are lower too.

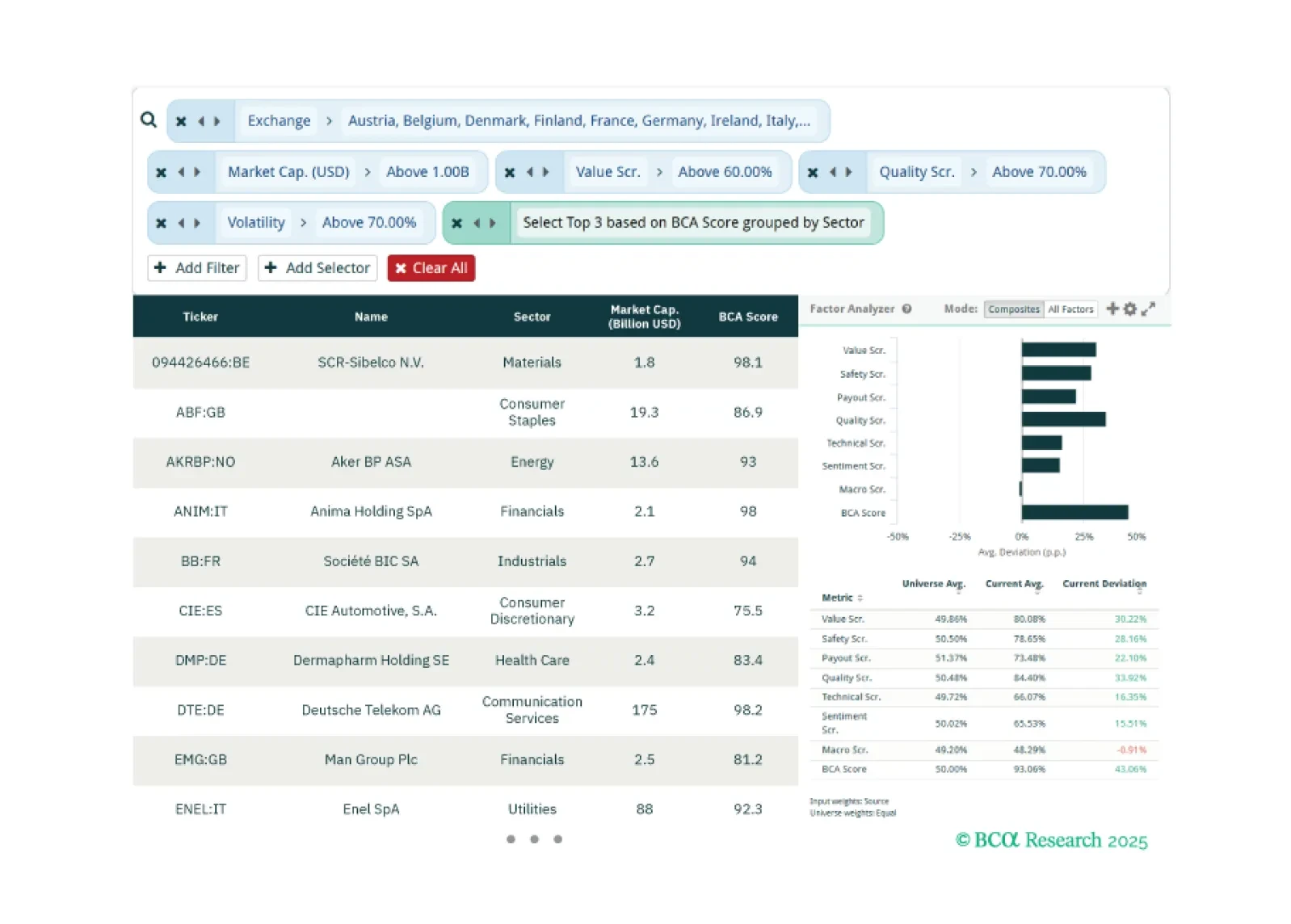

This week, our three screeners cover: Favoring European equities over US equities, cybersecurity stocks, and large caps with large moves in their BCA Score.