Equities

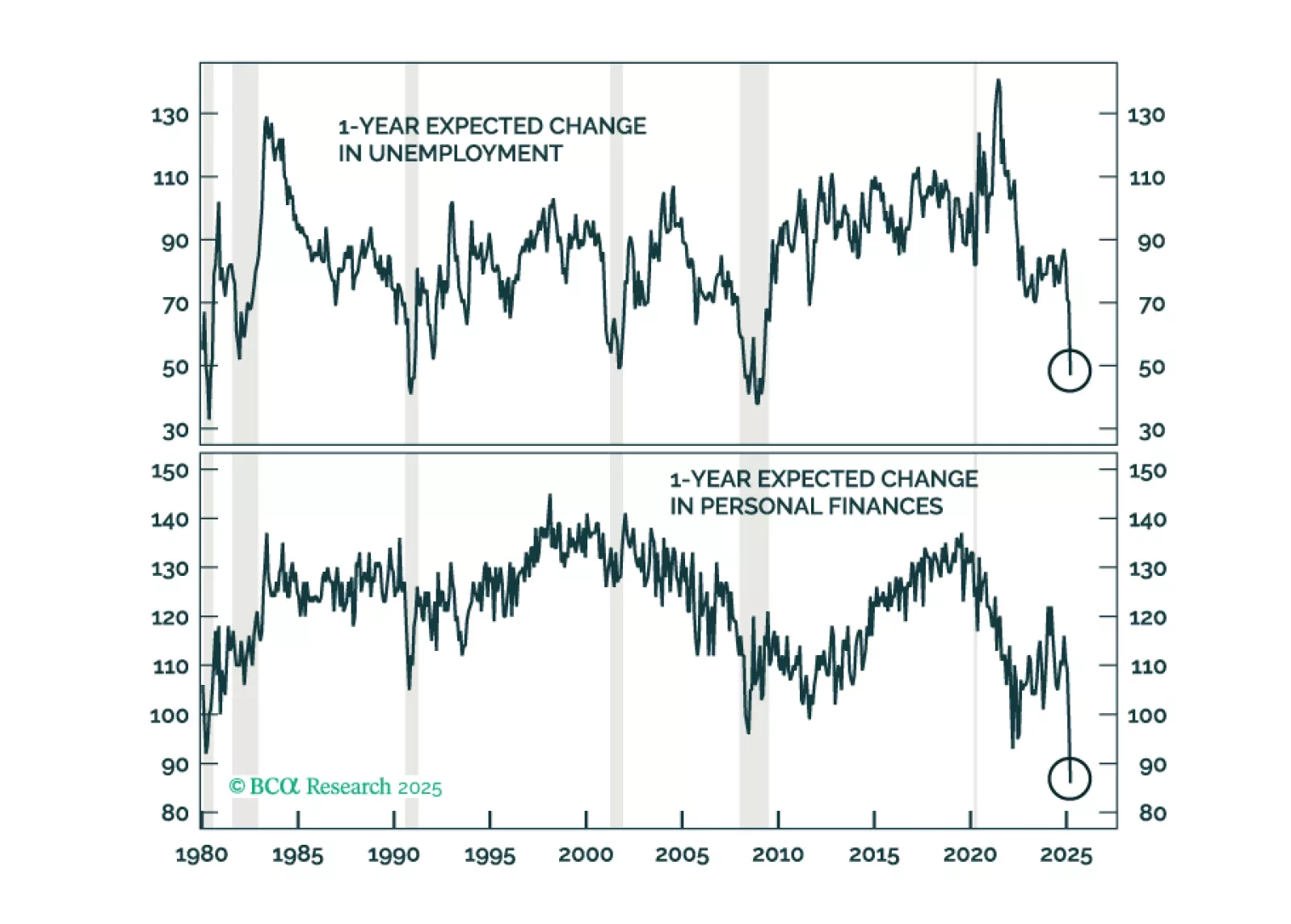

President Trump imposed tariffs on the world in his first 100 days, as we expected. Tariffs may have catalyzed a recession in the US, given the weakness in consumer sentiment and demand. Trump will soon backpedal and grant exemptions to countries that are negotiating, which he will showcase as proofs of his successful trade policy. While he may backpedal on his tariffs on other countries, China is not likely to receive the same treatment due to the US-China strategic competition.

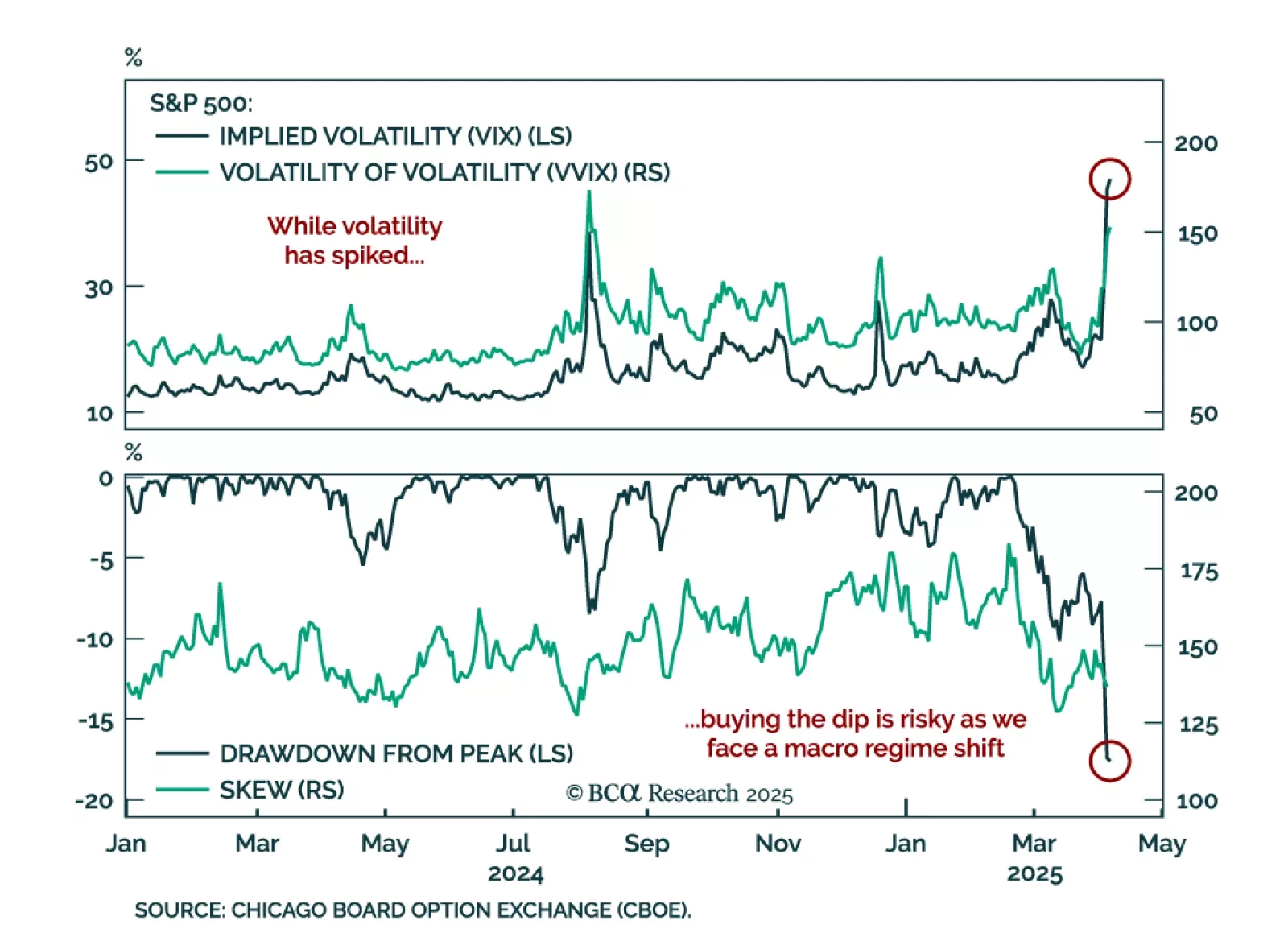

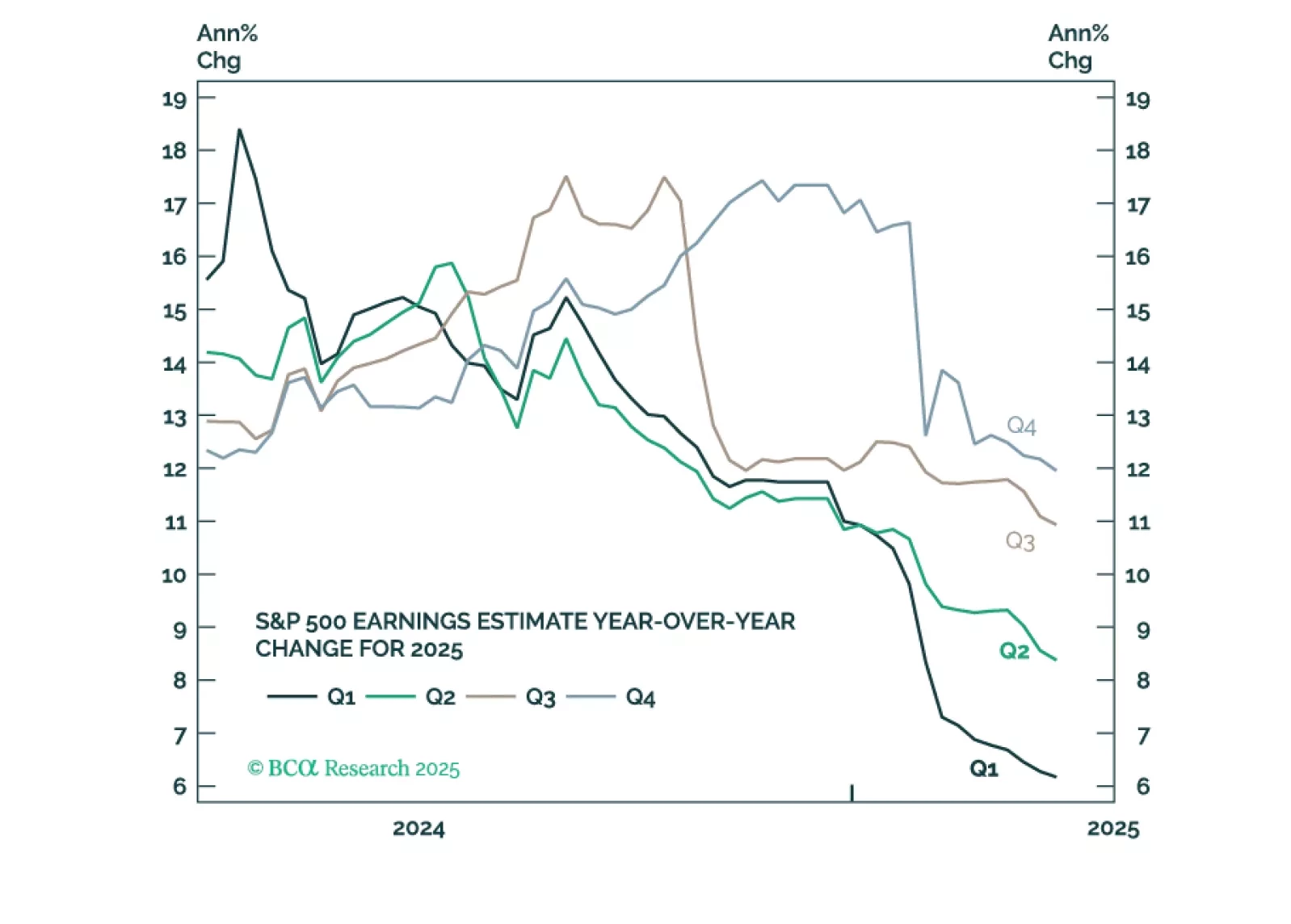

Equities will find a bottom when the full effects of tariffs on earnings and economic growth are priced in. The bottom of the market appears a long way away, and the S&P 500 may end up as low as 4,300, barring any reversals in trade policy that could undo the damage.

The stimulus measures driving the post-COVID expansion were beginning to wane after five years and pointing the economy in the direction of an organically occurring recession. Now that DOGE and the multi-front trade war have sped up the timetable, we reiterate our risk-off recommendations.

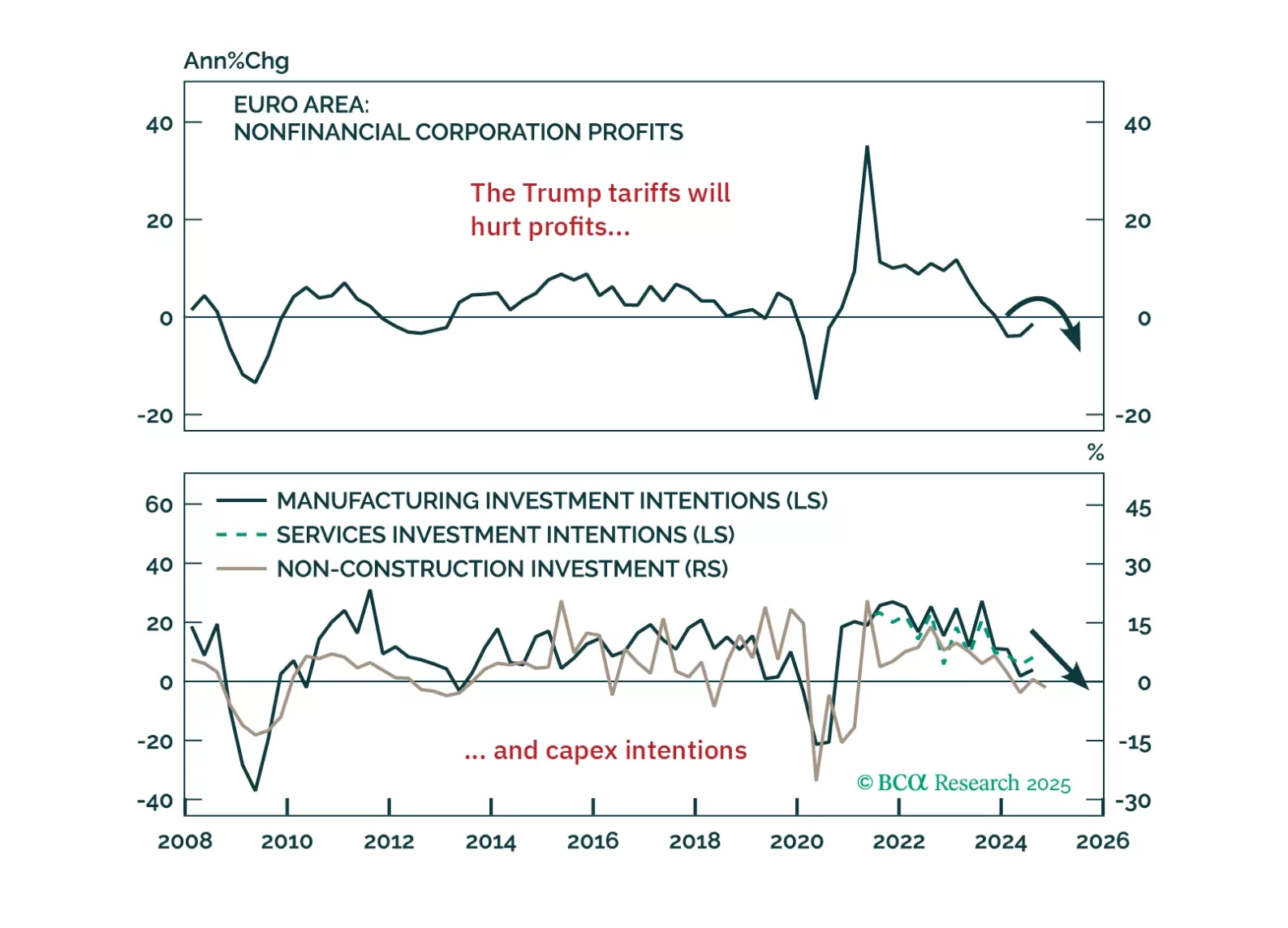

Trump’s tariff shock will push Europe into recession — but it’s also triggering a powerful integration response. In this report, we lay out the tactical case for staying defensive and the structural case for going long European assets when the dust settles.

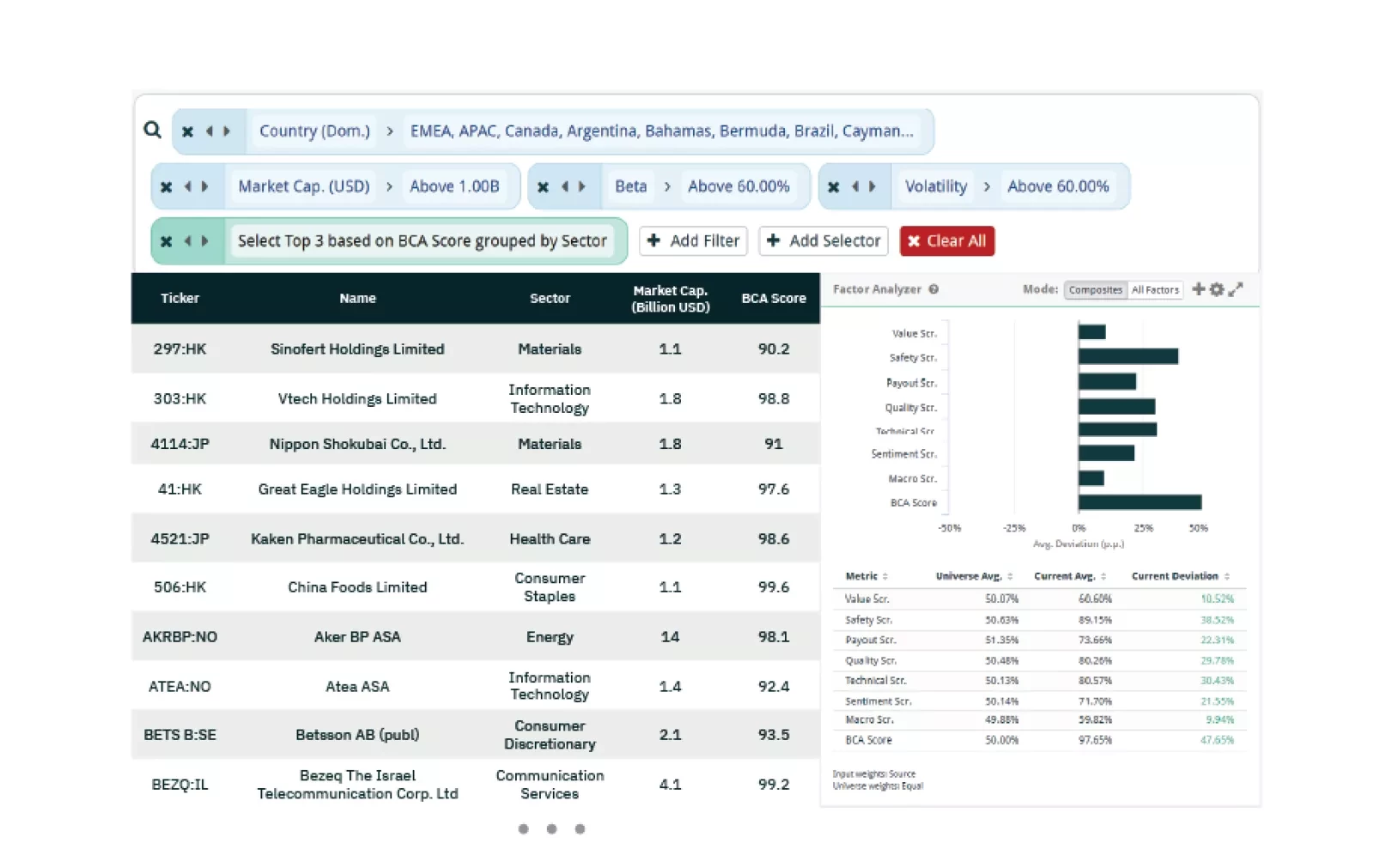

This week, our three screeners cover: Equity plays in Low Vol & Low Beta outside the US; Chinese stocks; and stocks that are buys according to the PEG ratio.

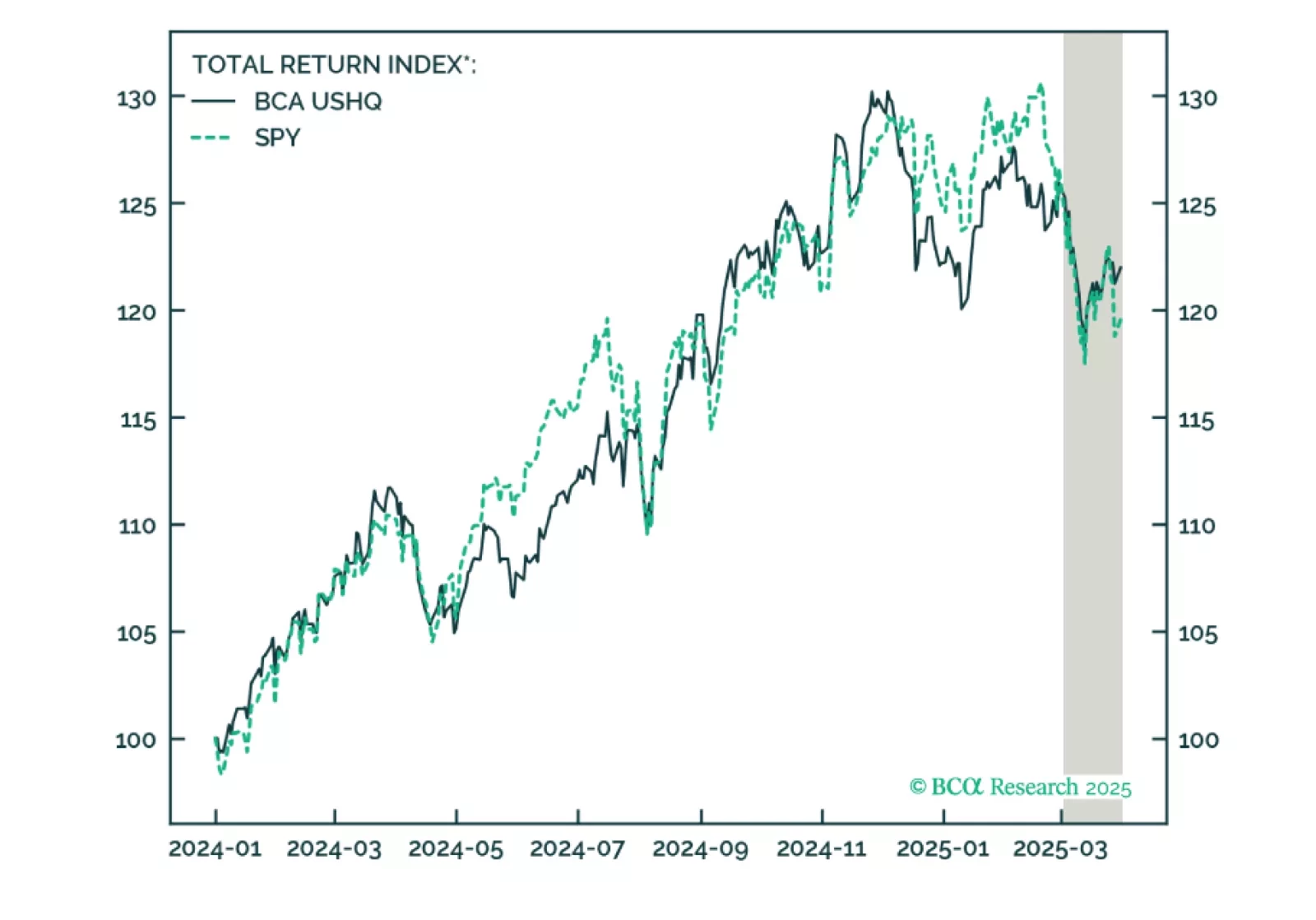

The US High Quality (USHQ) portfolio outperformed its benchmark in March, despite realizing a negative return. USHQ returned -2.6%, whilst its SPY benchmark returned -3.9%. Over a trailing-quarter basis, USHQ posted meaningful outperformance vs. benchmark, generating +230bps of excess return, while also exhibiting lower volatility and a smaller drawdown.