Equities

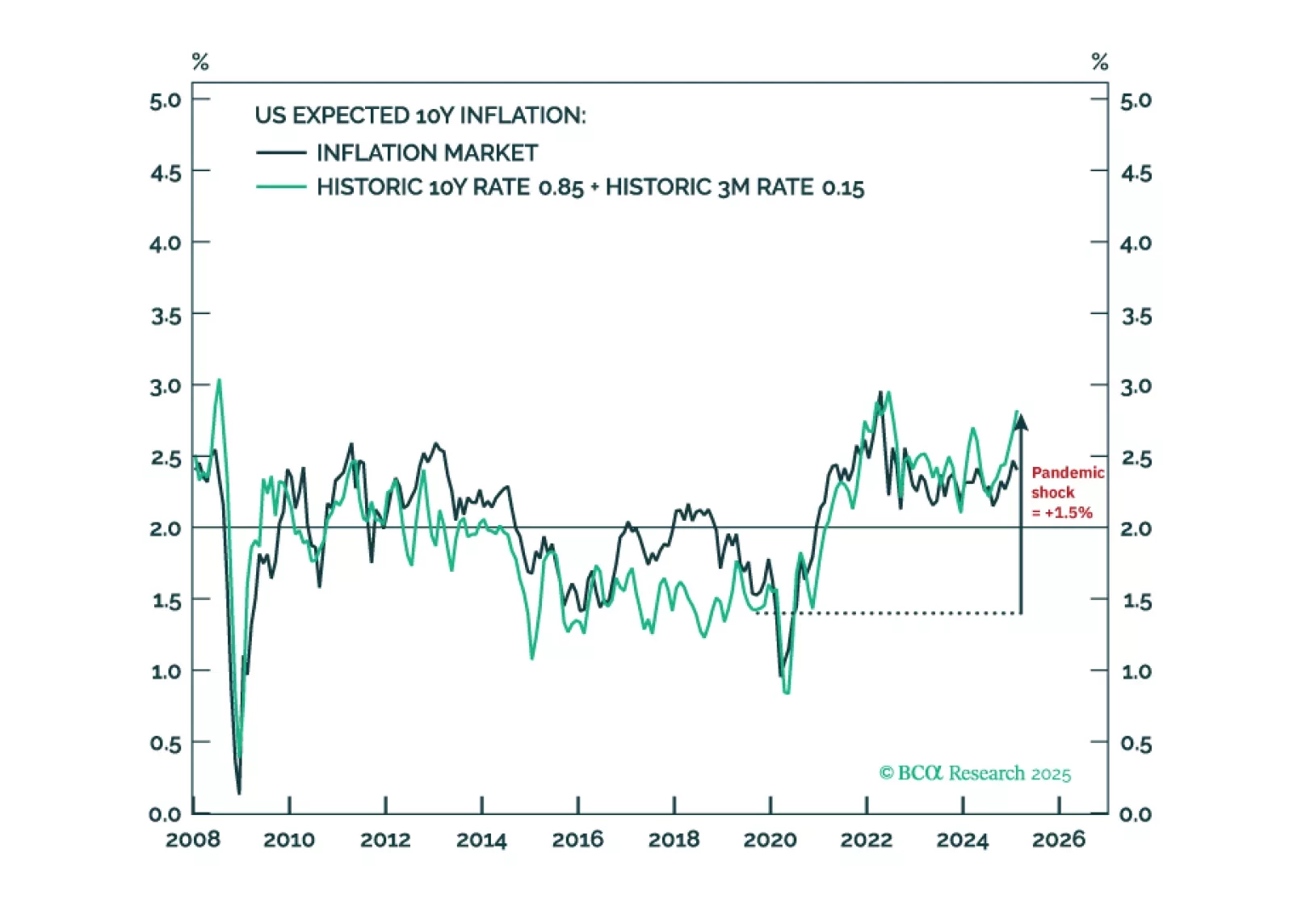

Tariffs will make a difficult job almost impossible. Hitting and sustaining a precise 2 percent inflation target is more about luck than judgement. It requires both the starting point for inflation expectations and any inflation/deflation shock to combine perfectly to 2 percent. While structural inflation expectations in the euro area and Japan could be close to 2 percent, those in the US and the UK will be stuck uncomfortably above 2 percent. We discuss the investment implications for rates and FX. Plus: gold is vulnerable to a tactical reversal.

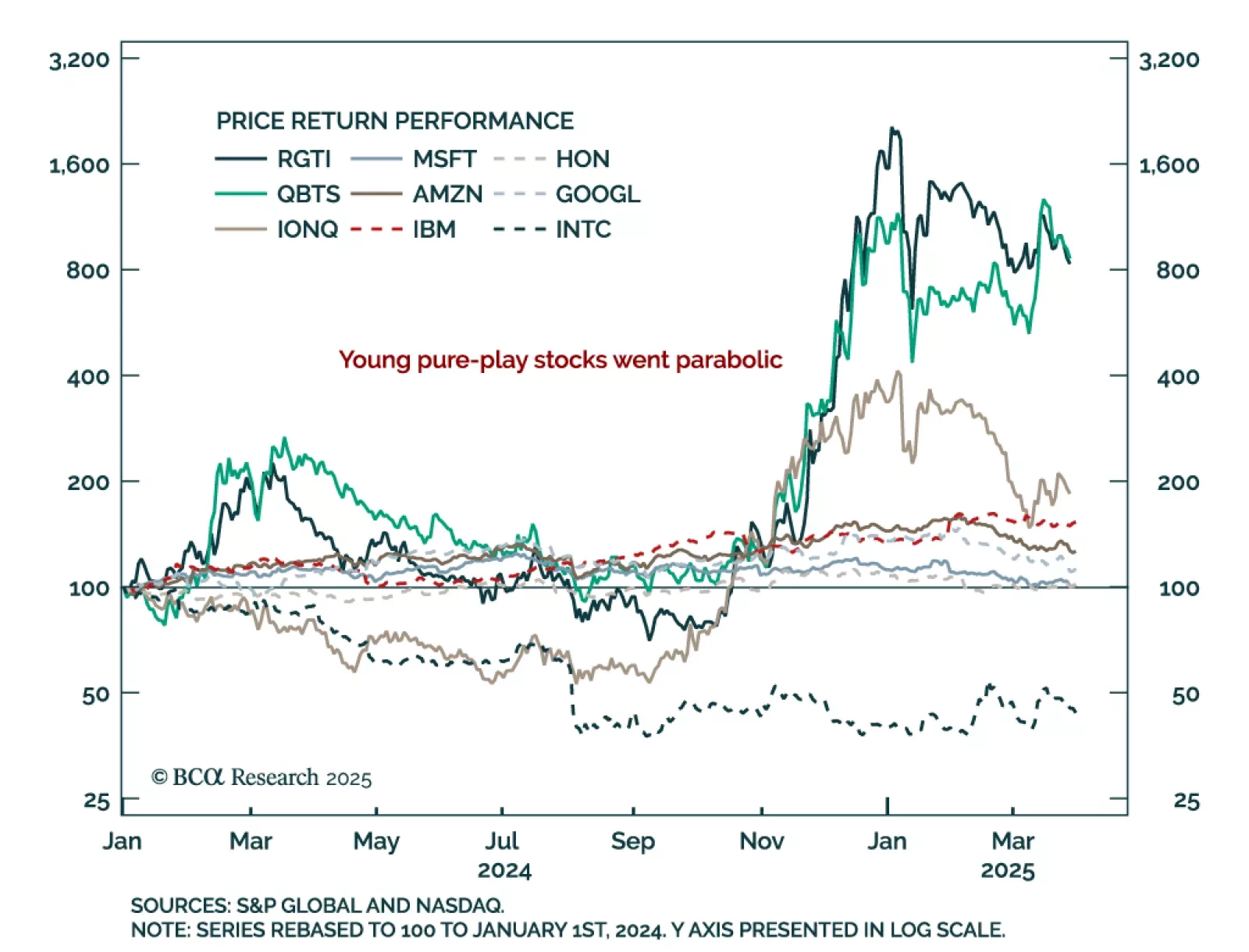

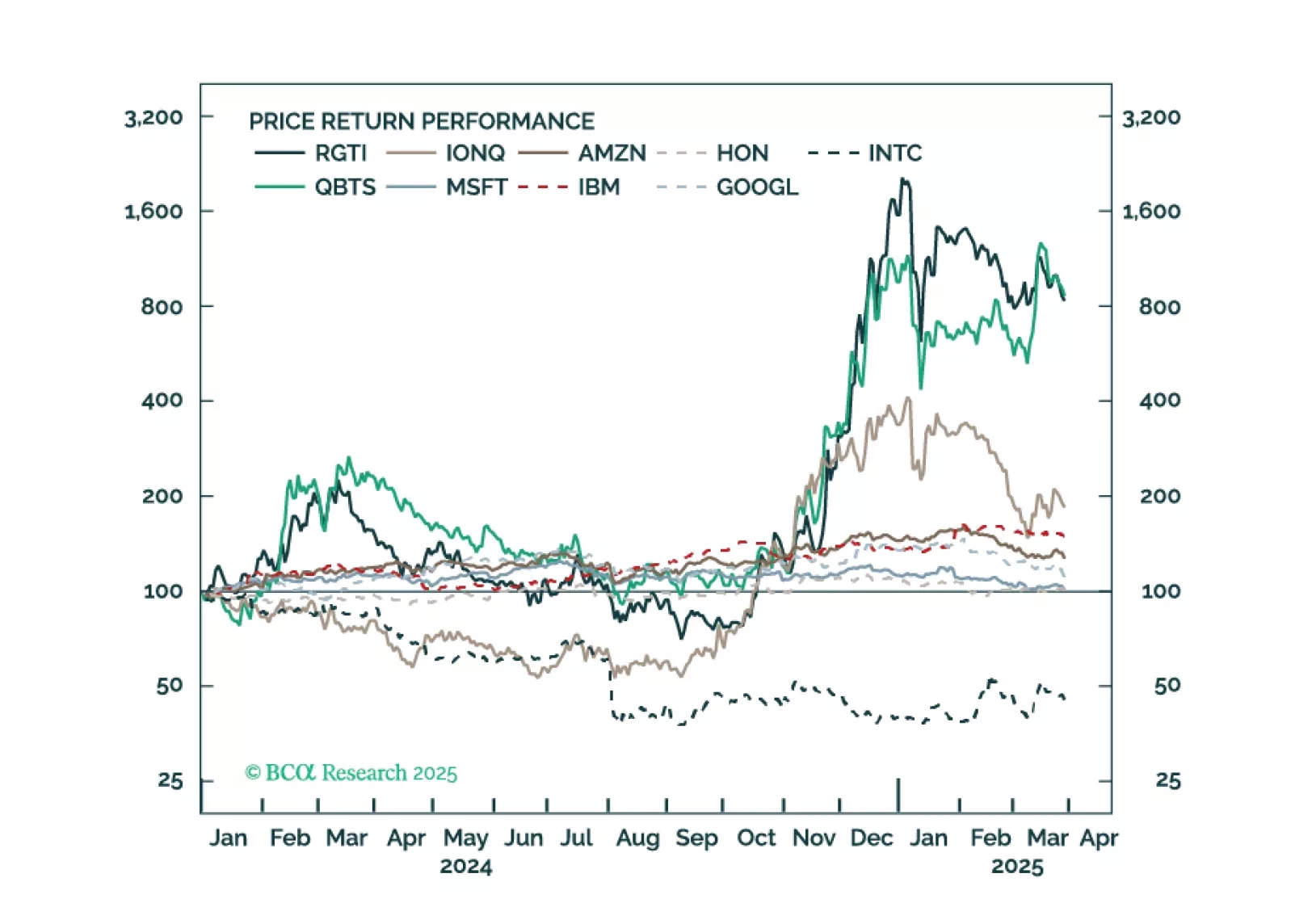

QC is on the verge of exciting technological breakthroughs and will eventually present multiple sound investment opportunities. However, the industry is still in its early innings, and buying pure-play QC stocks is akin to buying lottery tickets. Big Tech may end up dominating the space. We recommend a cautious stance.

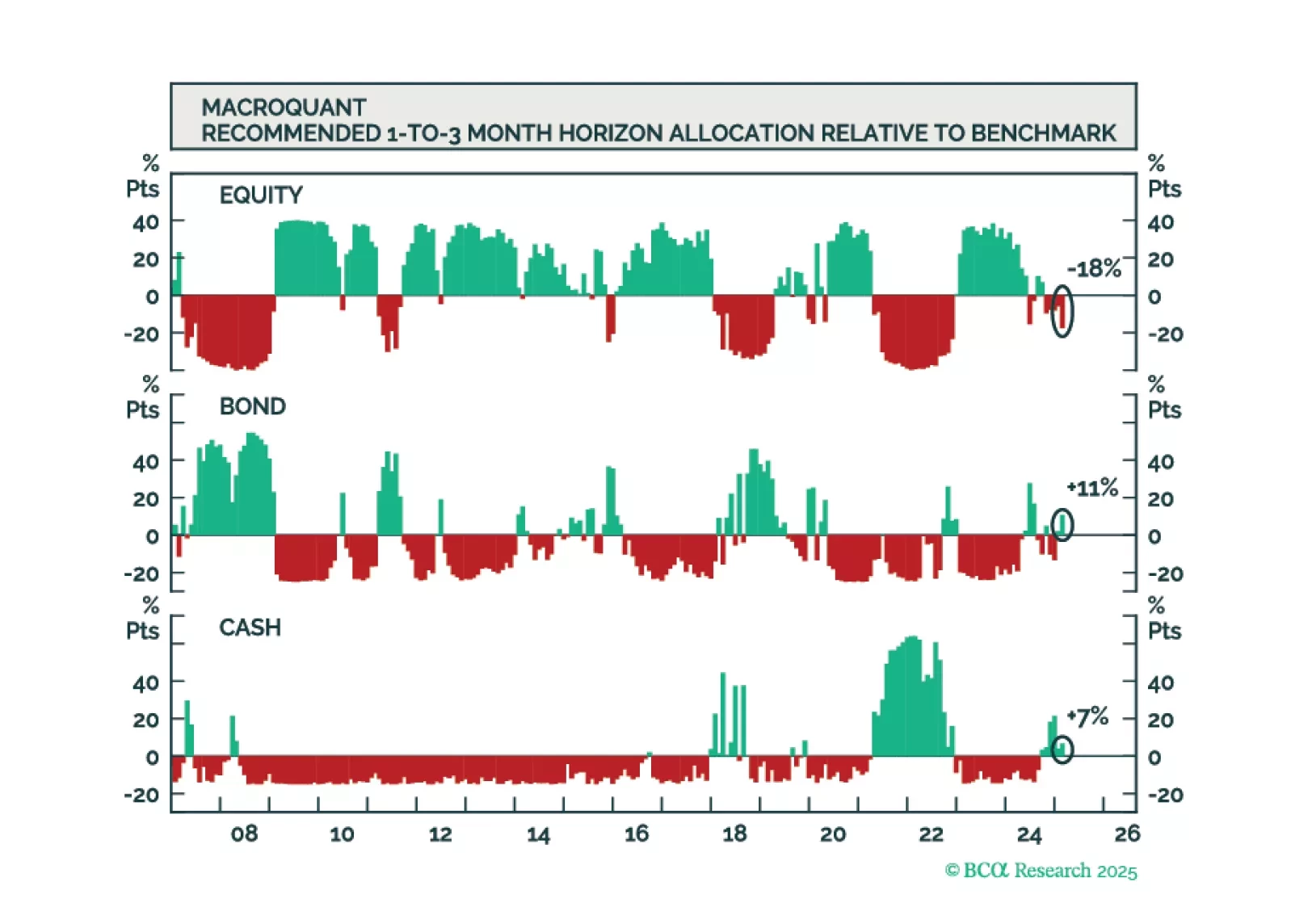

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

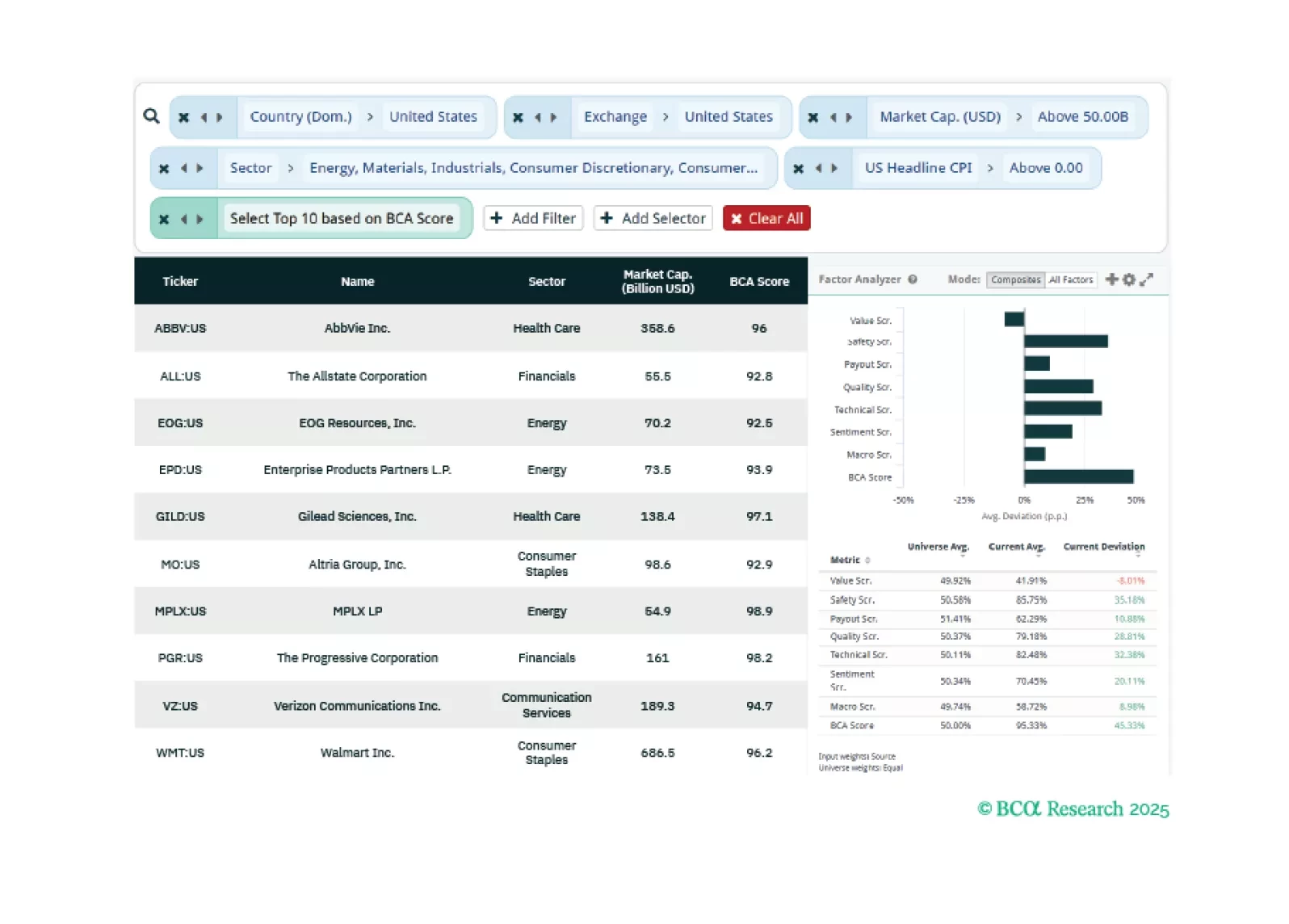

This week, our three screeners cover equity plays for if a US recession is not imminent, avoiding value traps, and which sectors exhibit the highest dividend payers.

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.