Equities

While the Middle East conflict’s inflationary impact is likely to persist, US recession risk is contained whereas non-US recession risk is more elevated. We discuss what this means for investment strategy. Plus, a new tactical trade is to underweight Utilities.

MacroQuant recommends a strong underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, has become neutral-to-slightly positive on the US dollar, has downgraded gold to neutral and copper to a strong underweight, and is bullish on oil.

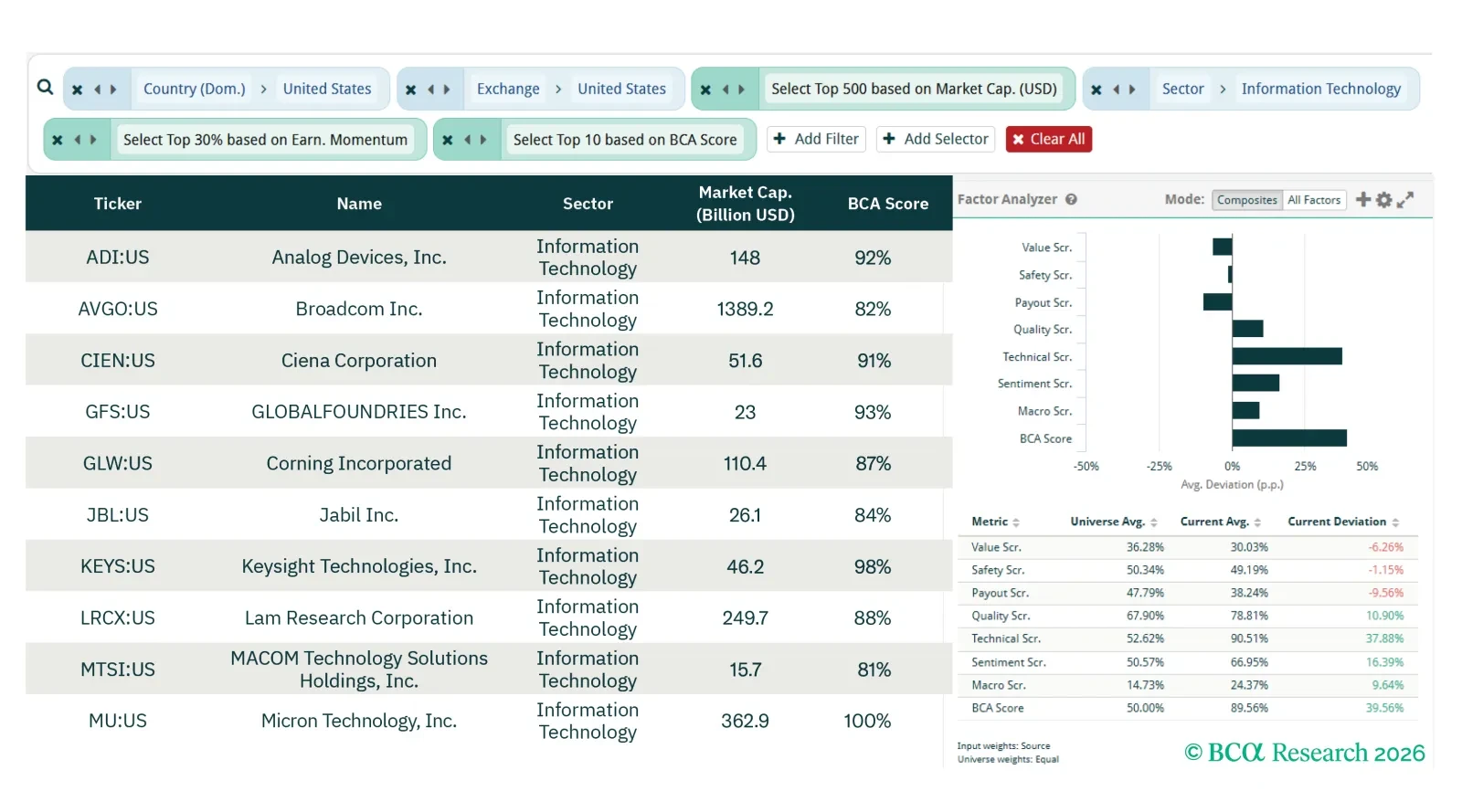

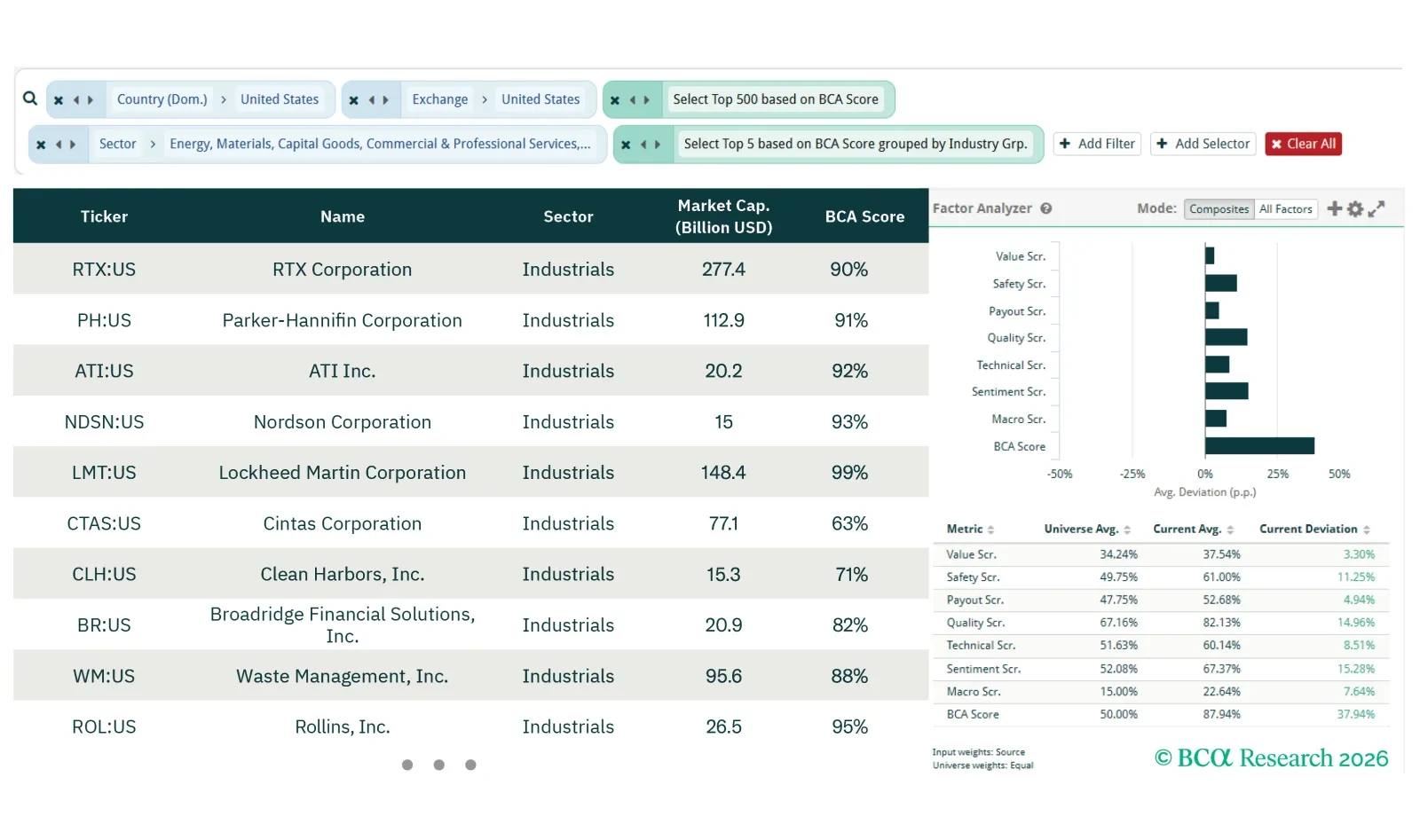

This screener report builds on the US Equity Strategy team's sector view published on 30 March 2026, where the team overweights Information Technology, Industrials, and Materials on a 3- to 12-month horizon. Here we utilize our screening tools to layer bottom-up stock selection onto their top-down sector views.

We continue to expect the S&P 500 to gain ground in 2026, driven by revenue growth, with limited scope for margin or multiple expansion. With cyclical upside tilted toward the investment side of the economy, we favor sectors with high-quality, revenue-driven earnings growth, leverage capex, and valuations that leave room for catch-up.

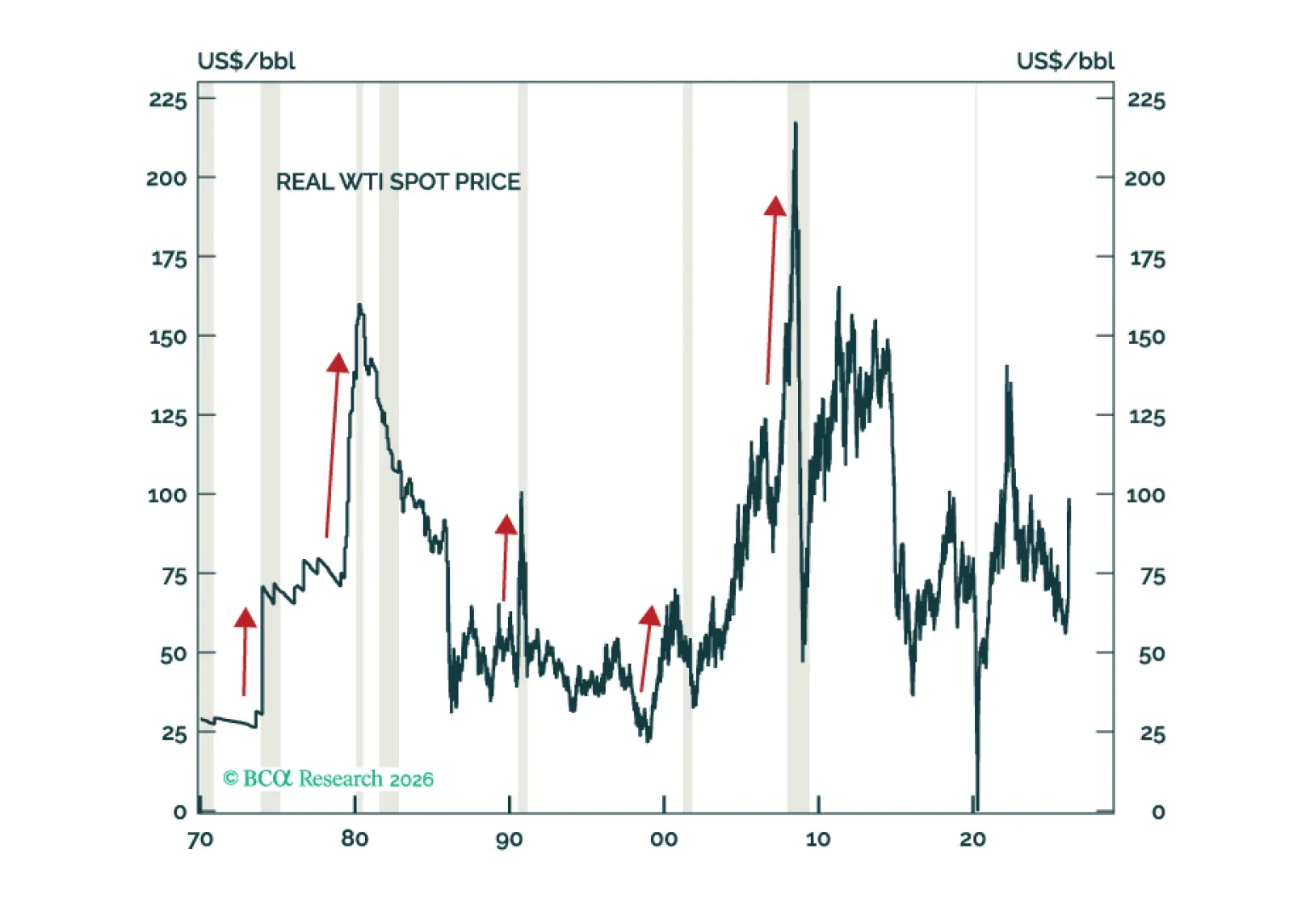

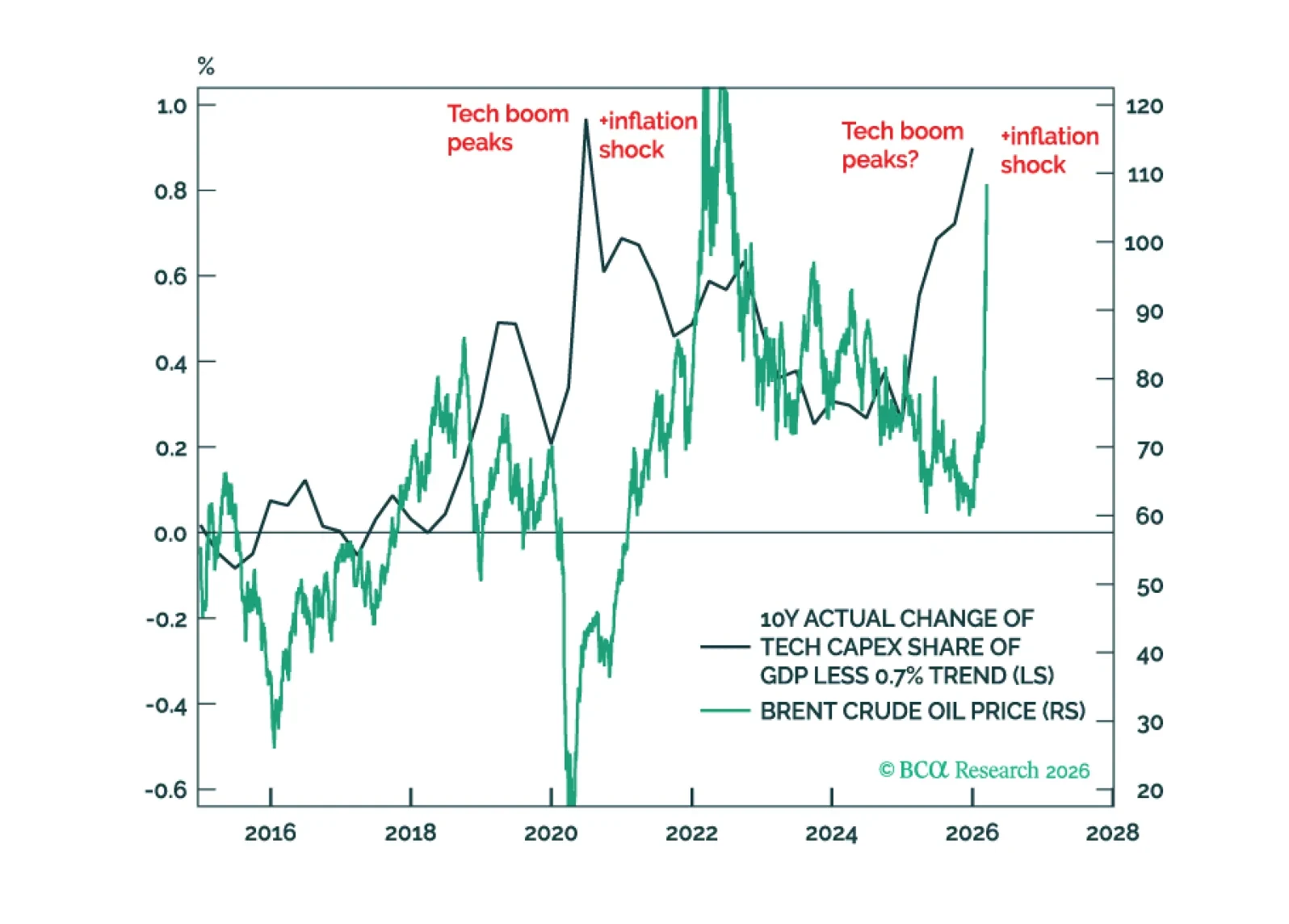

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

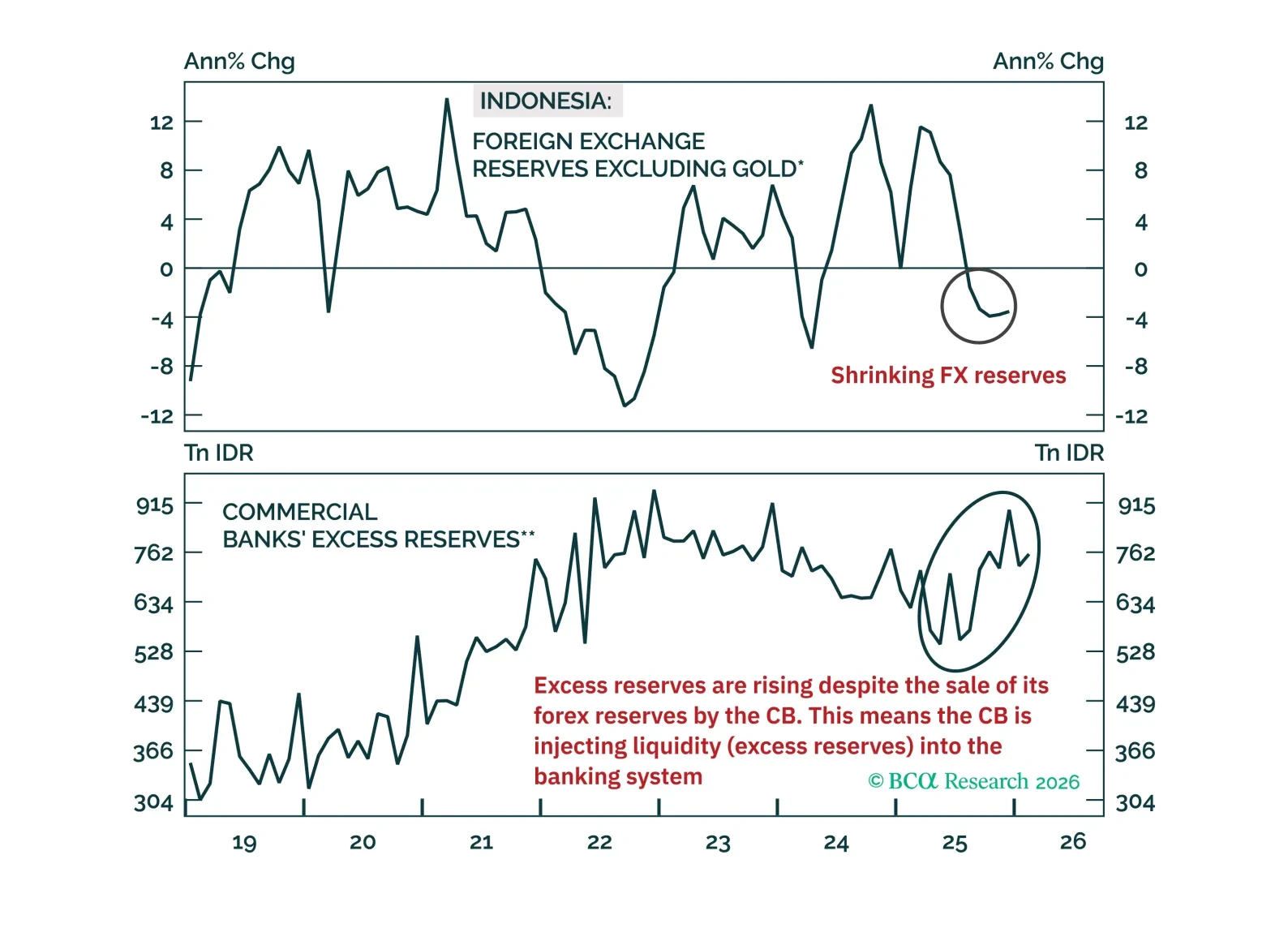

Indonesian rupiah will continue to plunge, and its local-currency bond yields will rise materially. Investors should short domestic bonds, currency unhedged.

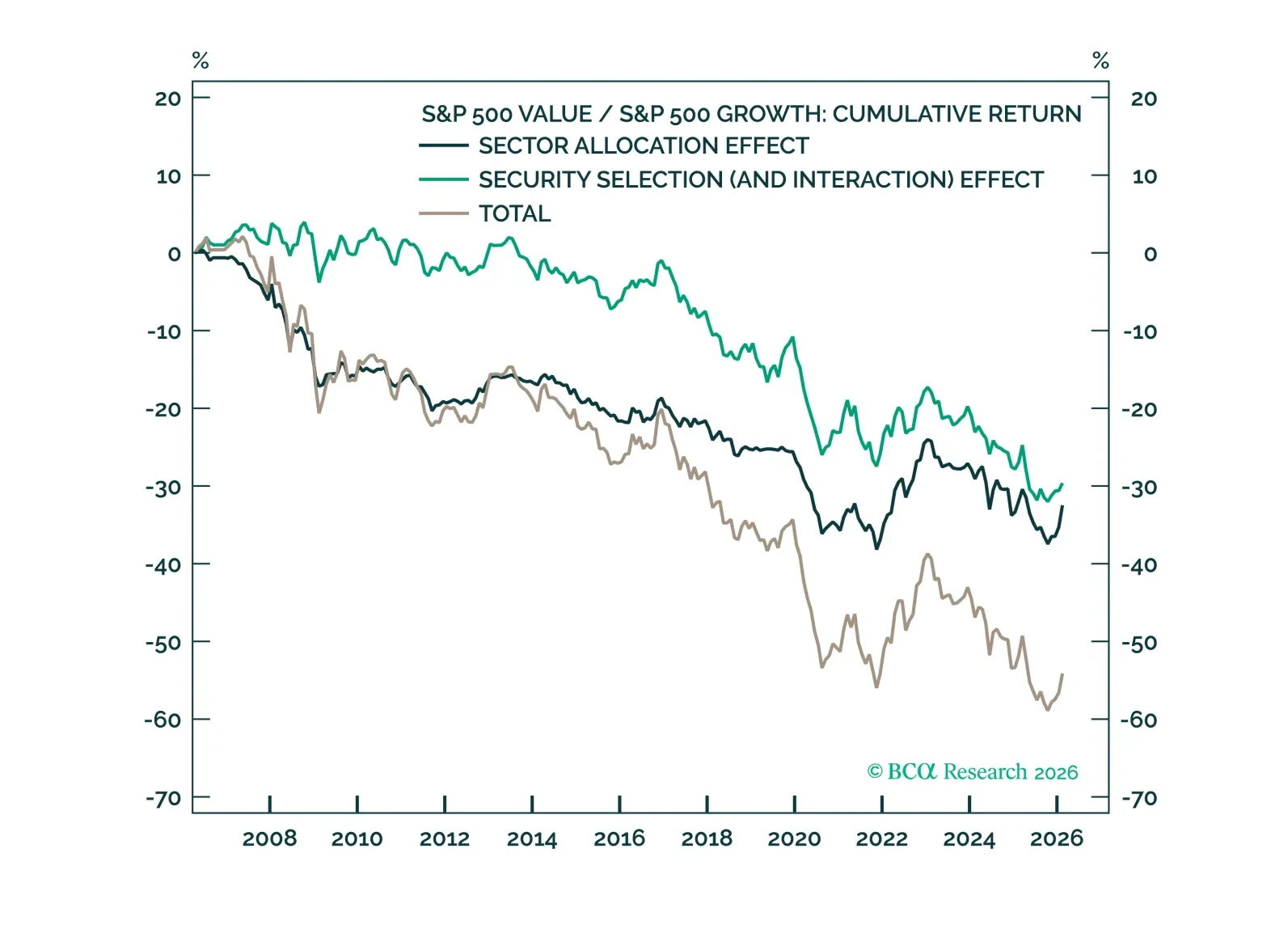

Although Value has had a meaningful run, the longer-run Growth trend likely remains intact. However, benchmark Growth indices are increasingly concentrated. Sector-neutral and within-sector implementations may allow investors to retain much of the same Growth/Value exposure while reducing dependence on technology and limiting concentration risk.

Forced to choose between growth and inflation, the Fed will save growth and the stock market rather than the 2 percent inflation target and the bond market.

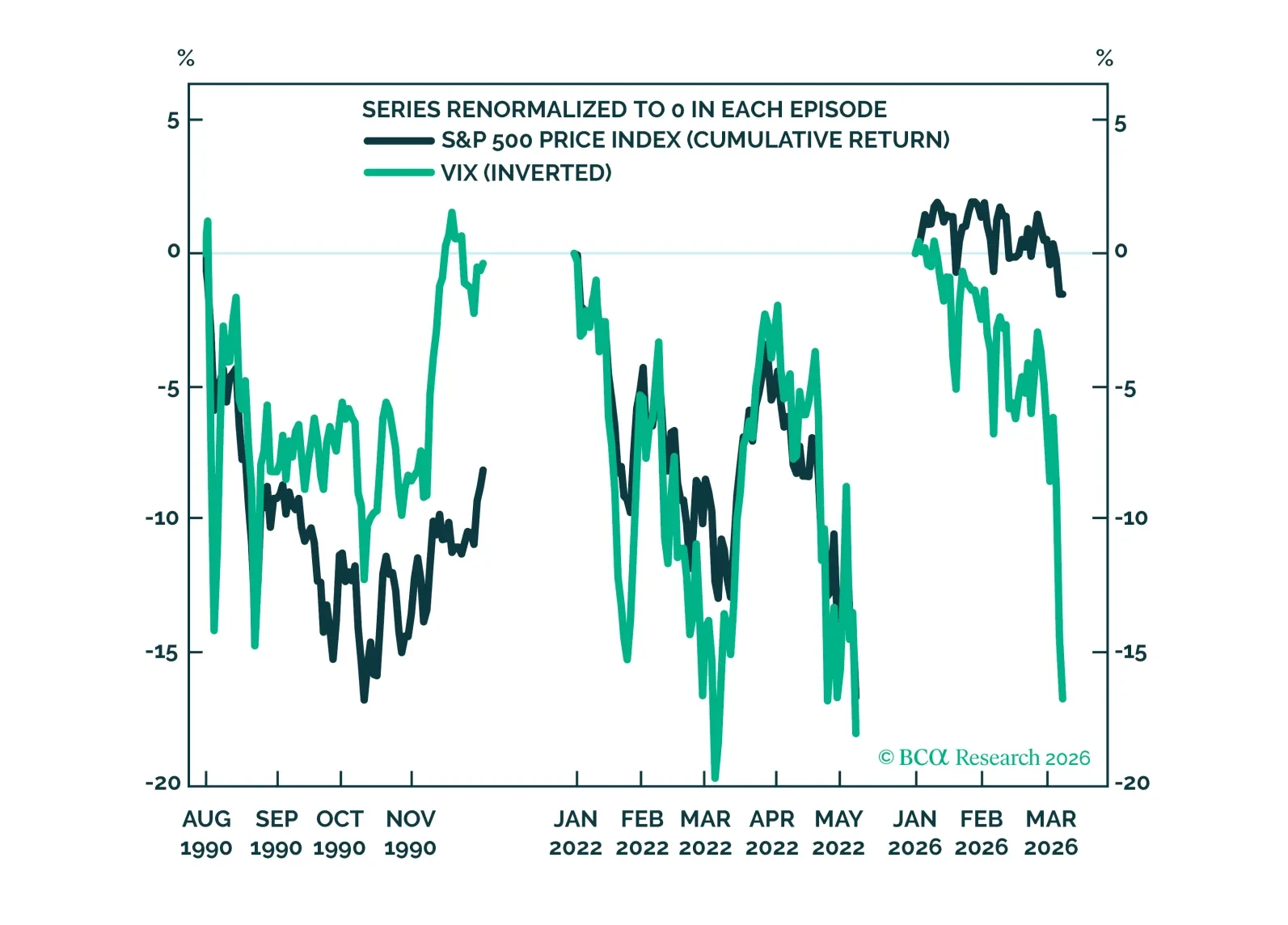

This screener report builds on the macro risk portfolio framework developed in the US Equity Strategy and Equity Analyzer collaboration published on 9 March 2026. Here, we apply the framework to analyze recent Middle East hostilities and identify how bottom-up equity positioning should adapt as the conflict evolves, which we analyzed in a US Equity Strategy report published on 16 March 2026.

Middle East tensions sparked a surge in volatility, yet the S&P 500 decline has been comparatively modest. Across asset classes, moves seem related to risk preferences and near-term inflation concerns. Within equities, some cyclicals are under pressure, but the equity market’s growth view has been resilient, while the inflation view has climbed.