Equities

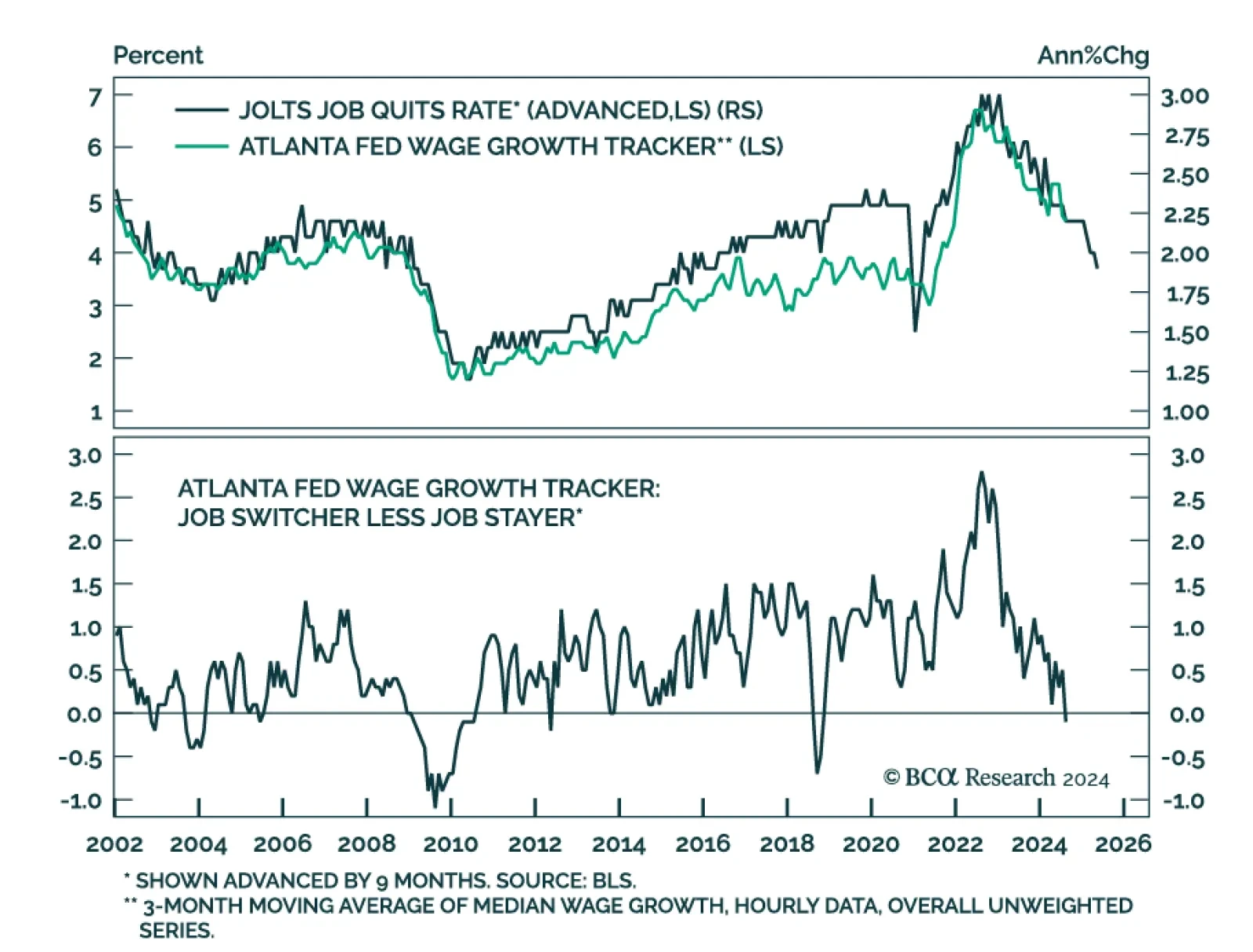

US job openings grew by a larger-than-expected 8.04 million jobs in August from 7.71 million. July’s openings were also revised 38 thousand higher. However, despite the upside surprise, the August hires rate fell to 3.3% and July’s hires were revised…

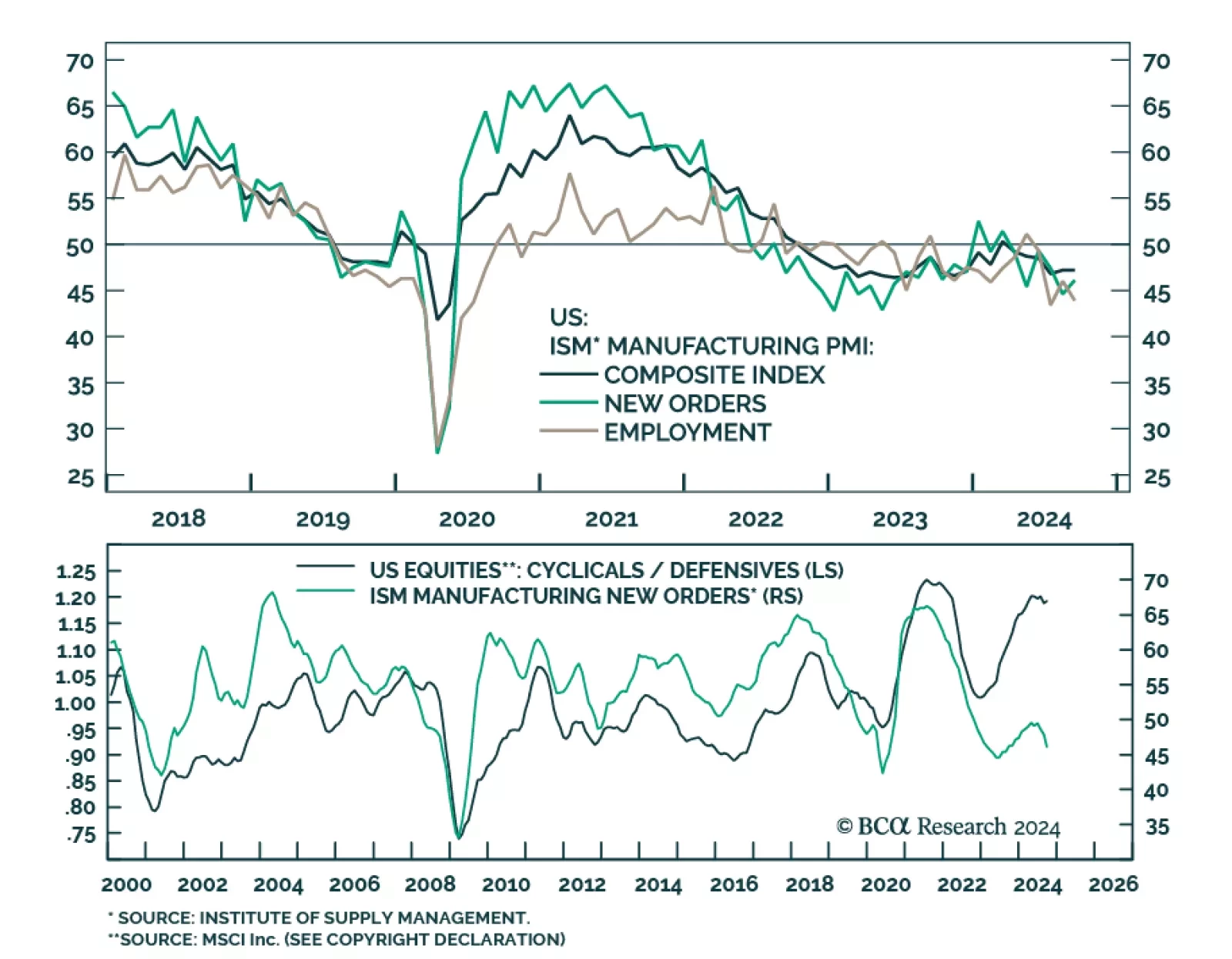

The ISM manufacturing PMI remained constant in September at 47.2, against expectations of a slower pace of decline and extending a six-month contraction streak. Measures of production and domestic demand decelerated at a notably slower pace while foreign…

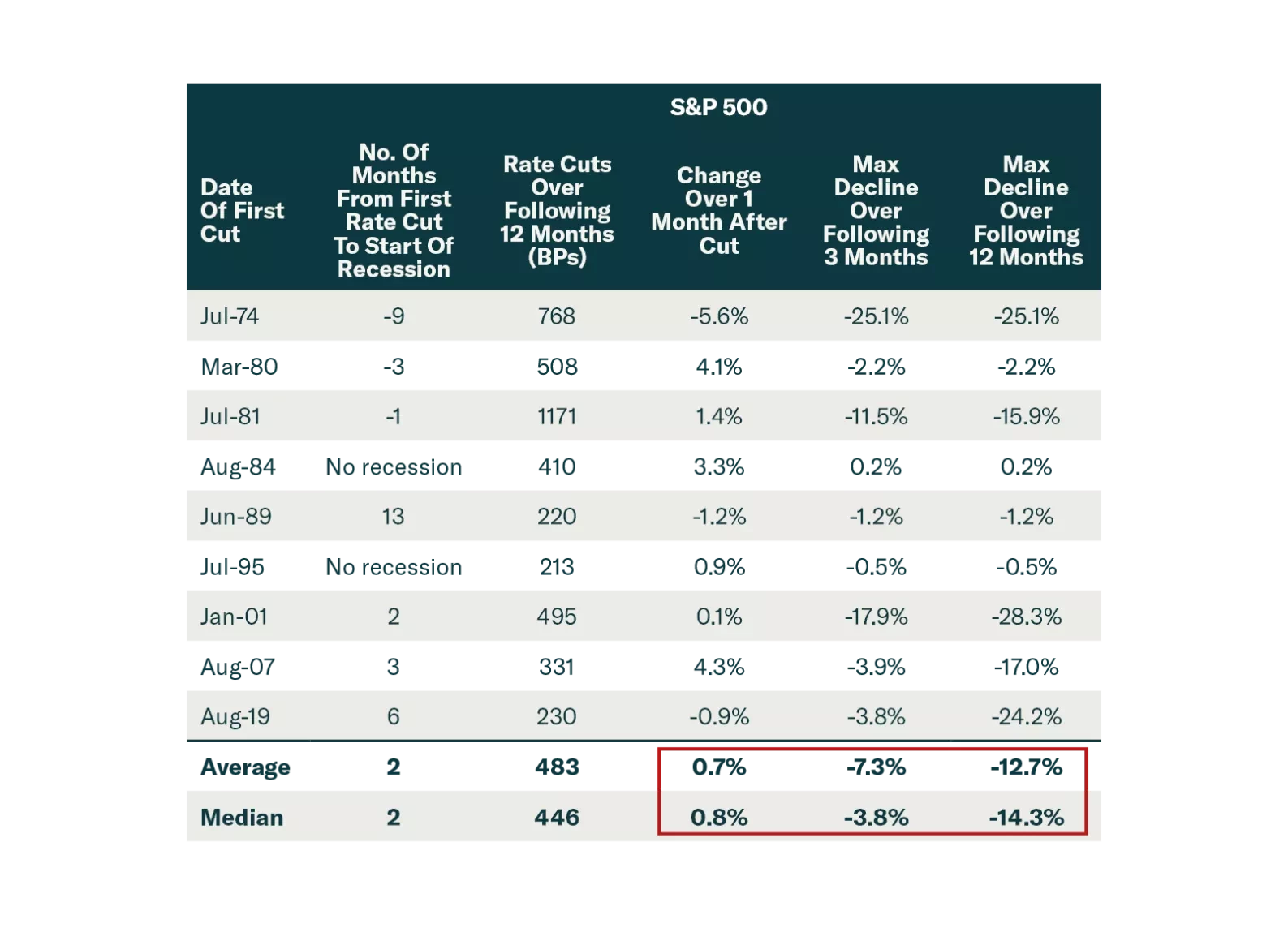

The market got excited by the 50 bps Fed cut and China stimulus. But these are a recognition that economies are slowing significantly. Stocks often rally after the first Fed cut, before falling sharply. Investors should stay defensive.

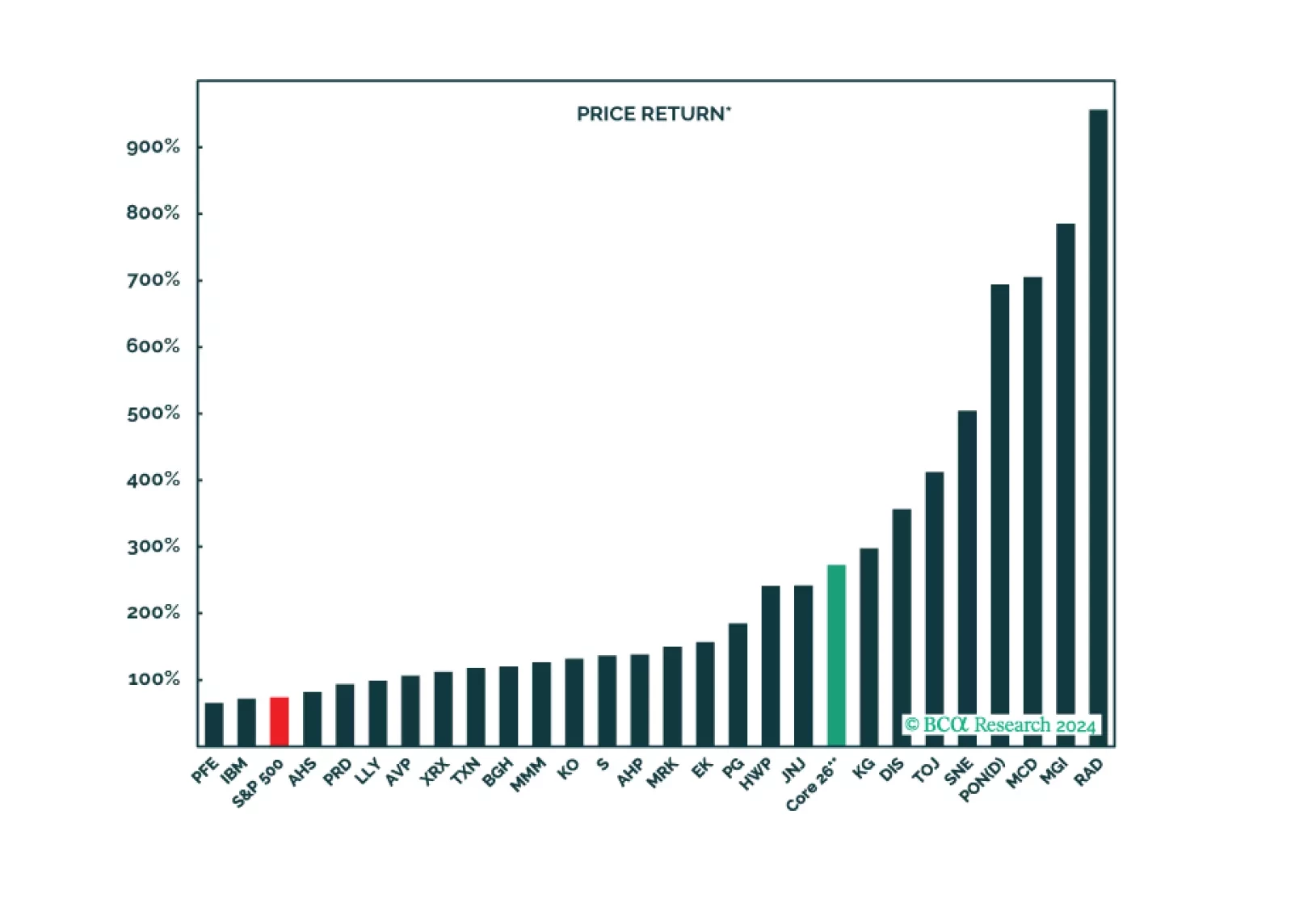

The Nifty Fifty bull market of the early seventies was a mania in which investors got carried away chasing after a subset of prized growth stocks. While we do not think the Magnificent Seven stocks are in a bubble, they do have some parallels with the growth stars of 50 years ago.

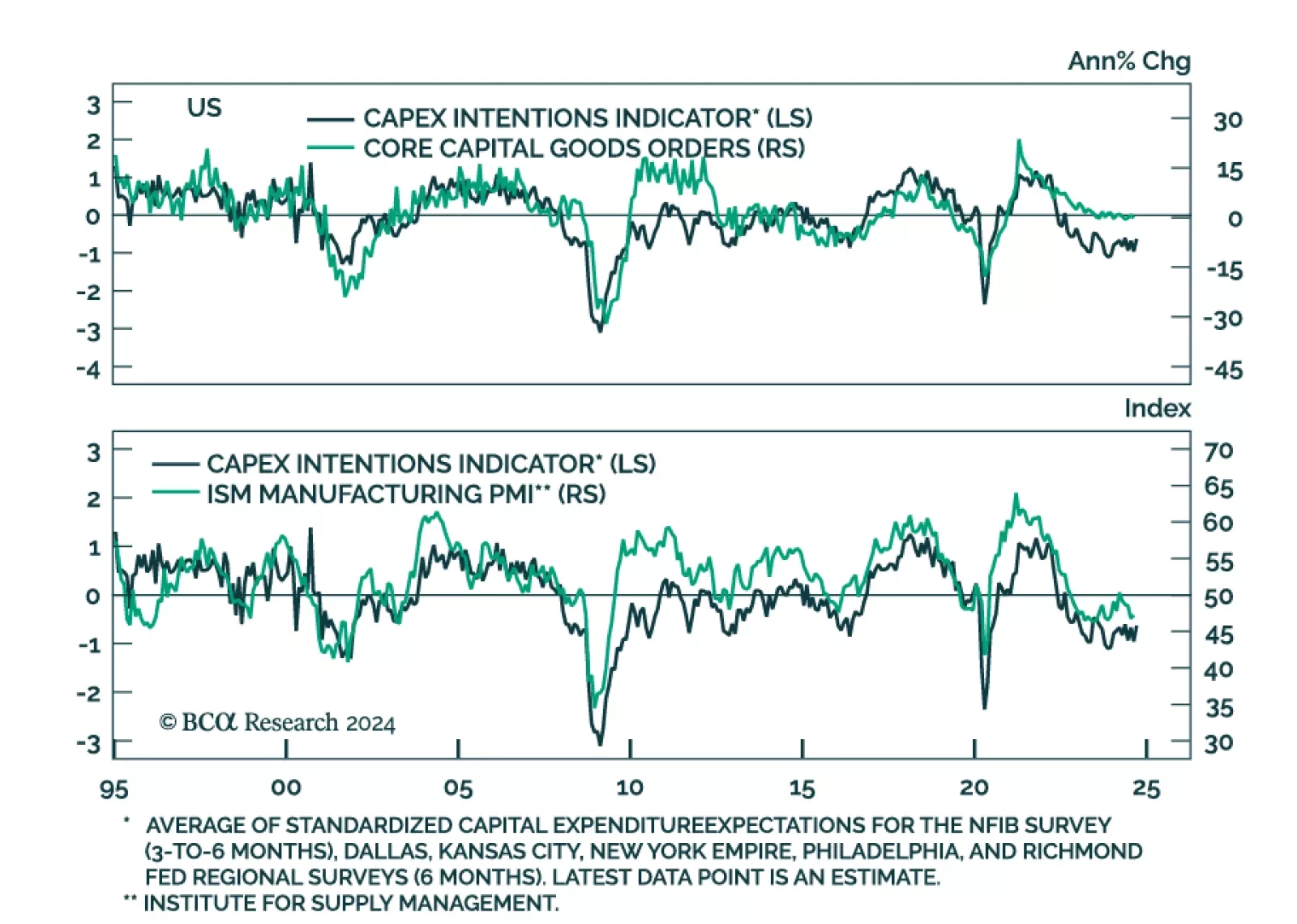

Preliminary estimates suggested that US durable goods orders stagnated in August after having surged 9.9% m/m in July, and beating expectations they would decline. Excluding the volatile transportation component, however, durable goods grew a robust 0.5%. …

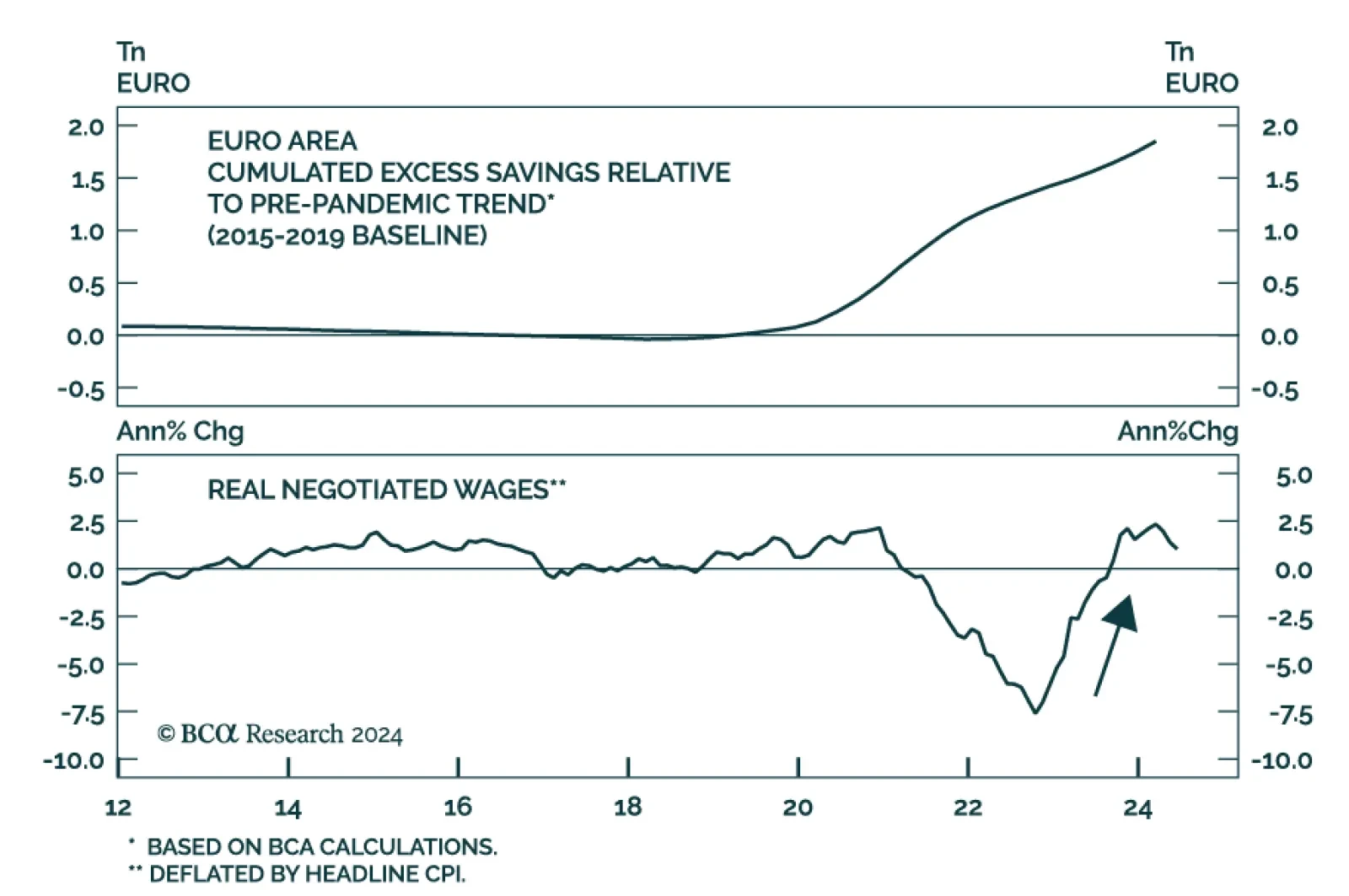

The Eurozone’s Bright Spots

…

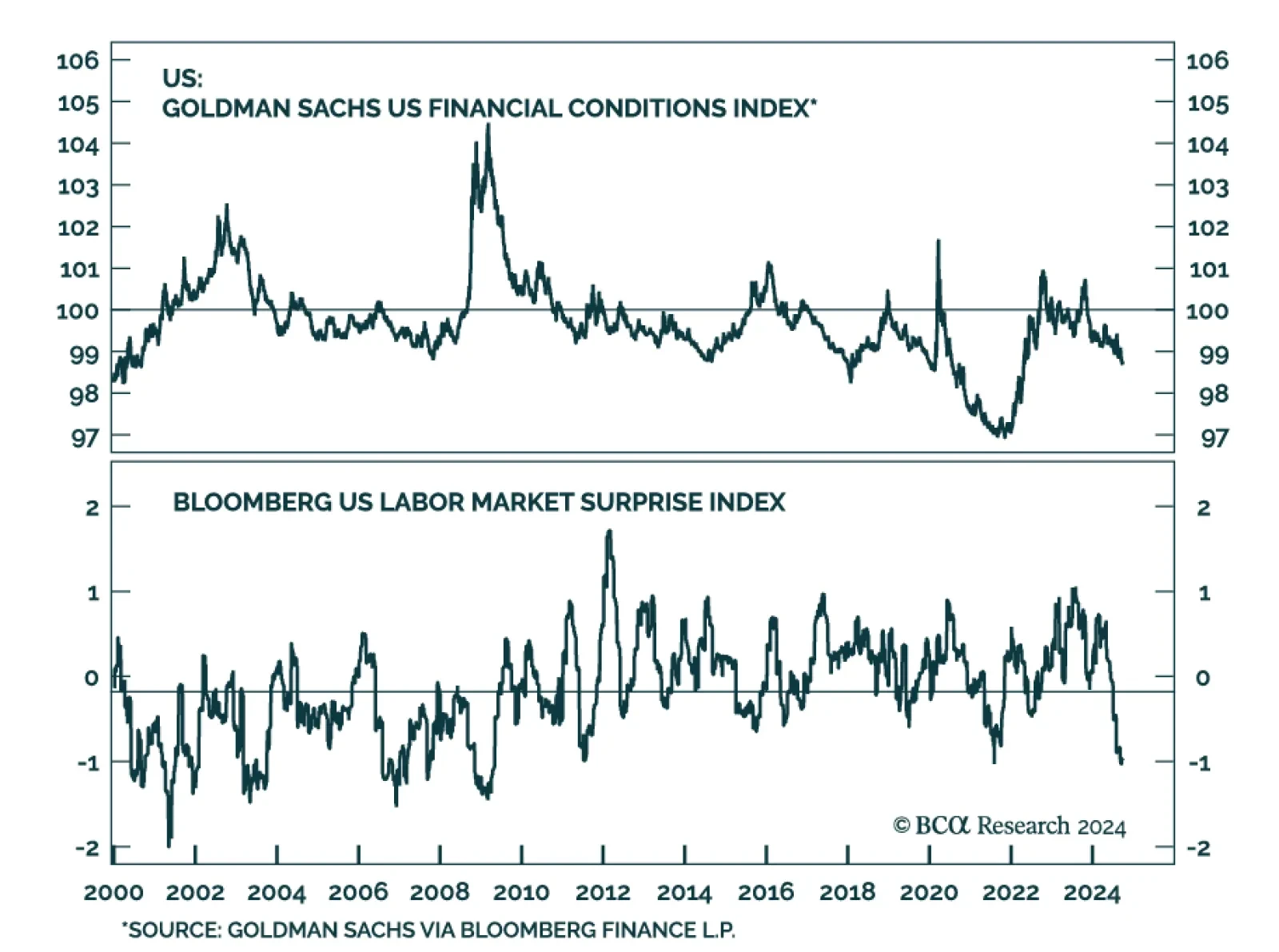

US financial conditions have become noticeably easier since August. The Fed has embarked on its easing cycle with a bang, sending equities higher and spreads lower, while the trade-weighted dollar gave back more than half of its year-to-date gains. The…

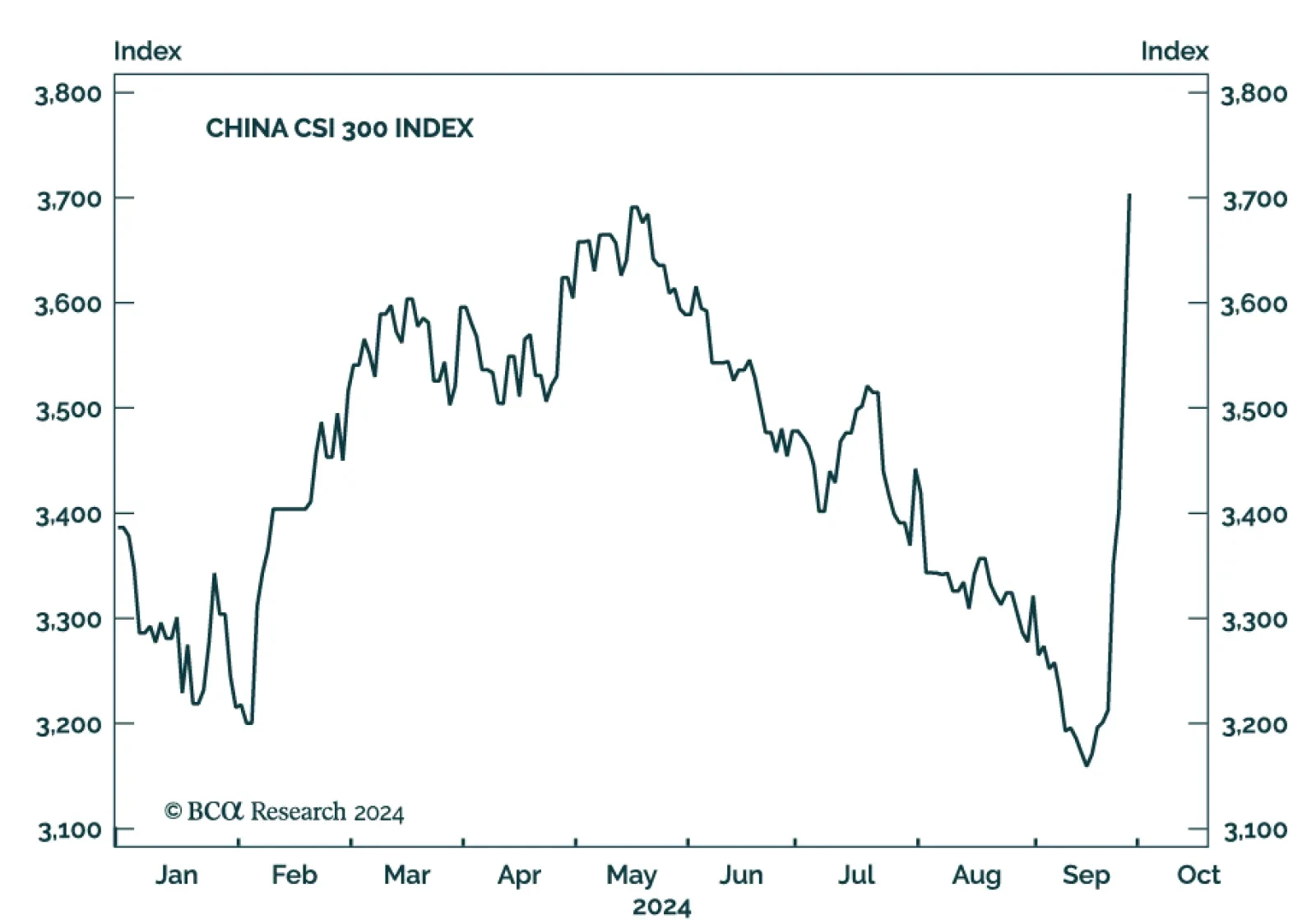

September’s Chinese PMIs were uninspiring. The Caixin manufacturing PMI dipped into contraction territory (50.4 to 49.3) despite expectations it would modestly improve. The alternative NBS manufacturing PMI improved from 49.1 to 49.8, above expectations,…

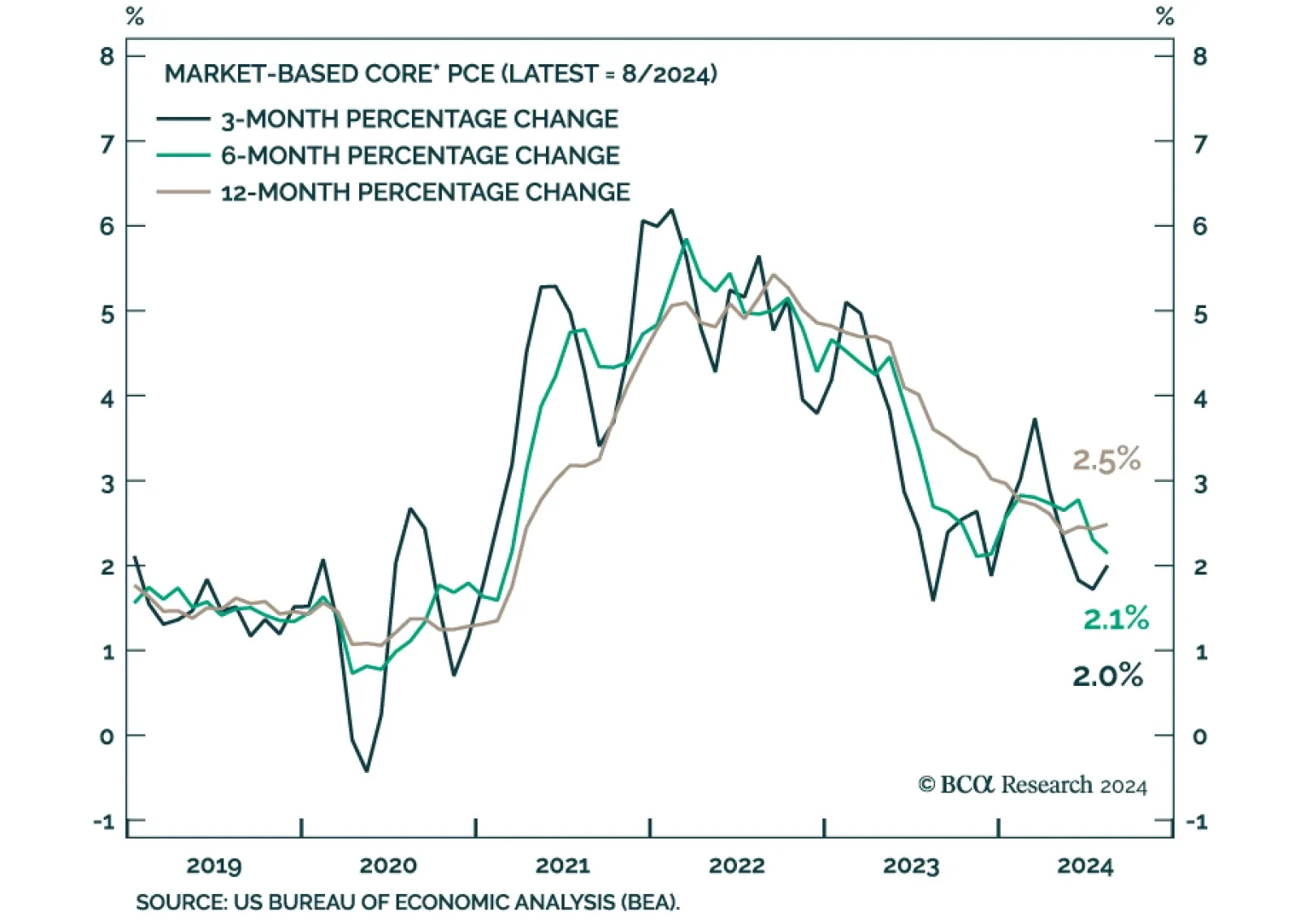

US nominal personal income growth decelerated to a 0.2% pace in August, from 0.3% in July, missing expectations that it would accelerate. Nominal personal spending also disappointed, growing at a slower 0.2% pace from 0.5%. In real terms, spending barely…

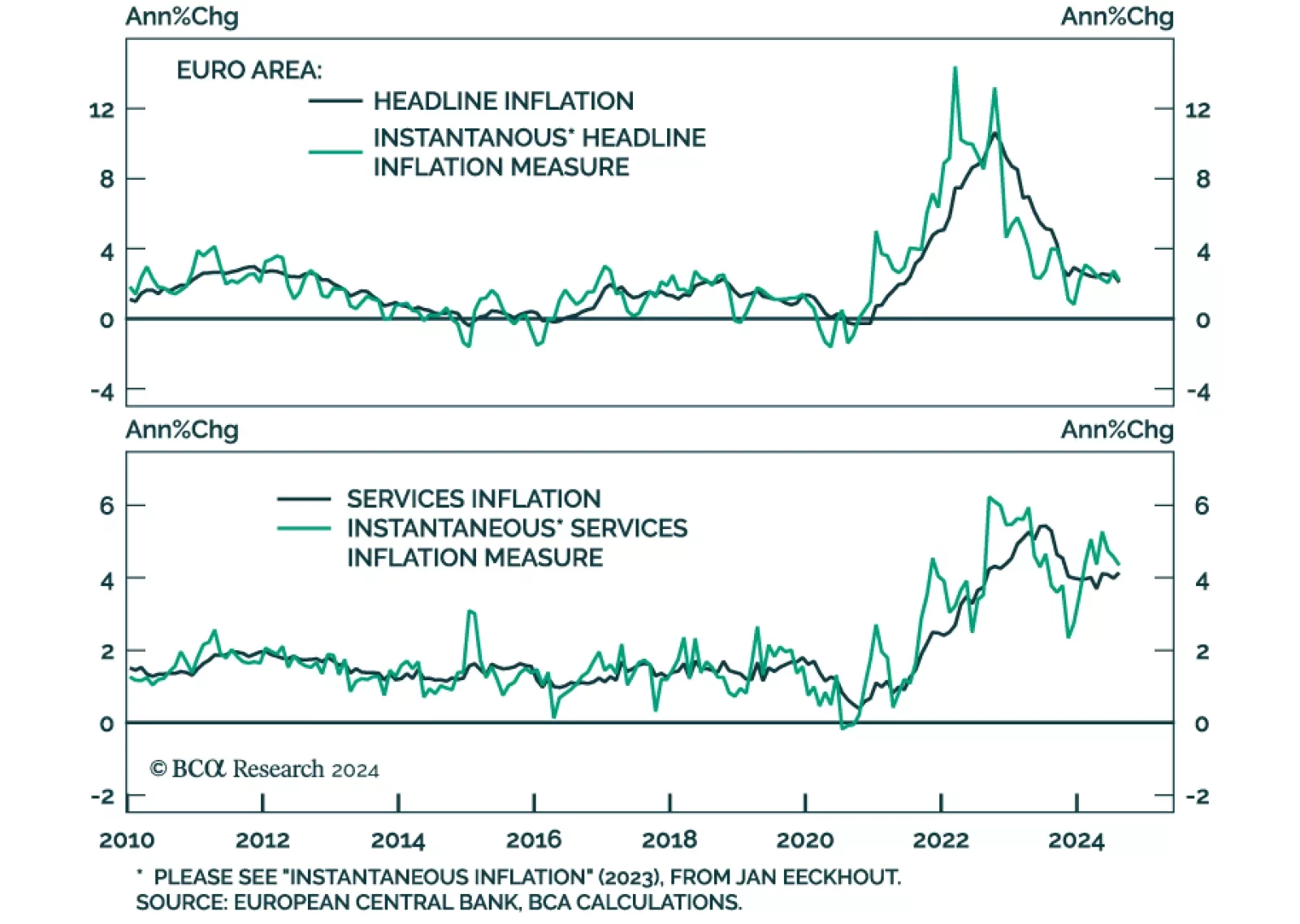

France’s and Spain’s preliminary September CPI readings declined on a month-on-month basis, clocking in at 1.5% and 1.7% y/y respectively, and undershooting consensus expectations. Germany’s and Italy’s updates are due on Monday and the Eurozone CPI will be…