Equities

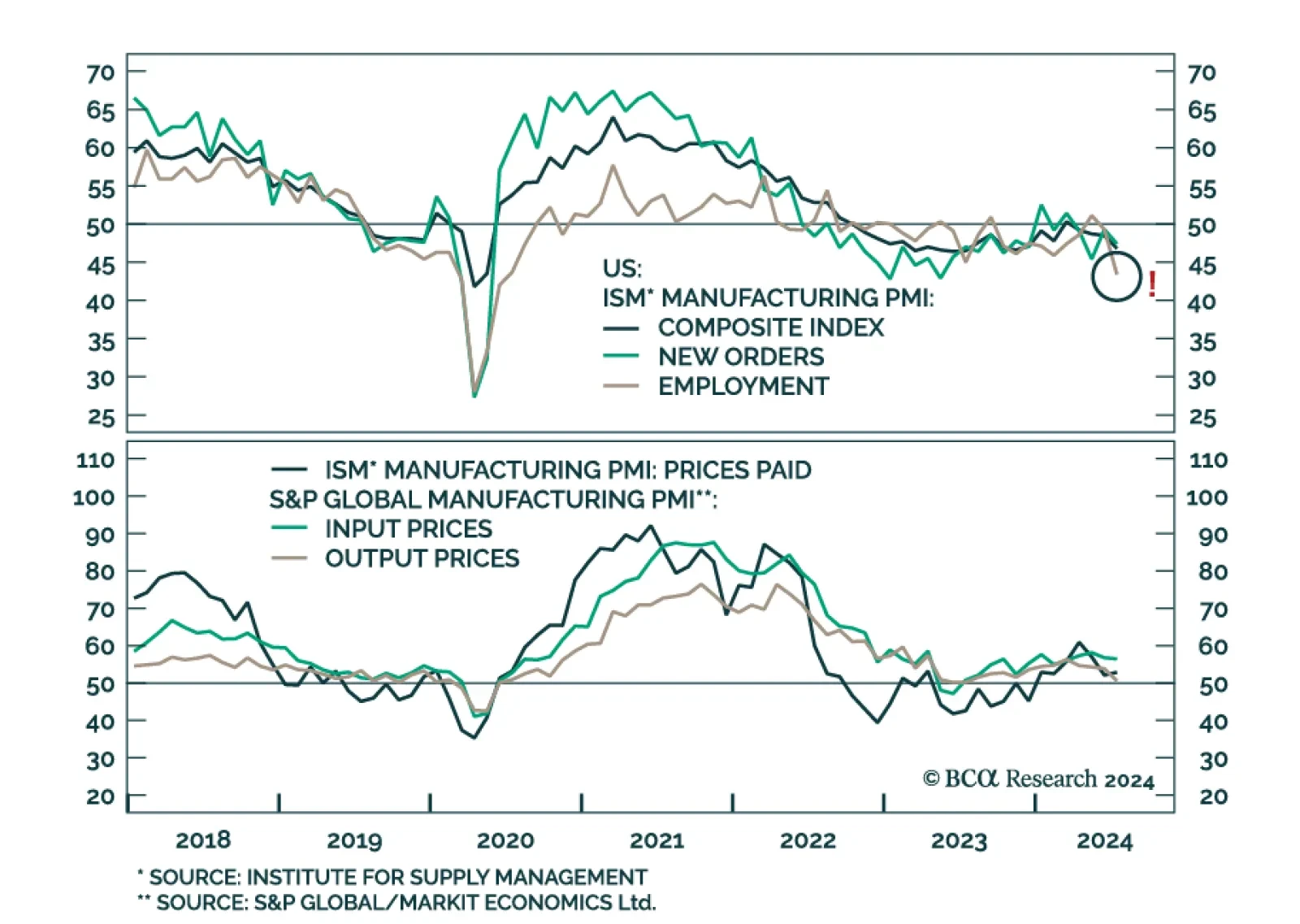

The ISM Manufacturing PMI disappointed in July. The headline index declined at a faster pace, from 48.5 to 46.8, disappointing expectations and extending a four-month contraction streak. Details were uninspiring. New orders dipped to 47.4 from 49.3,…

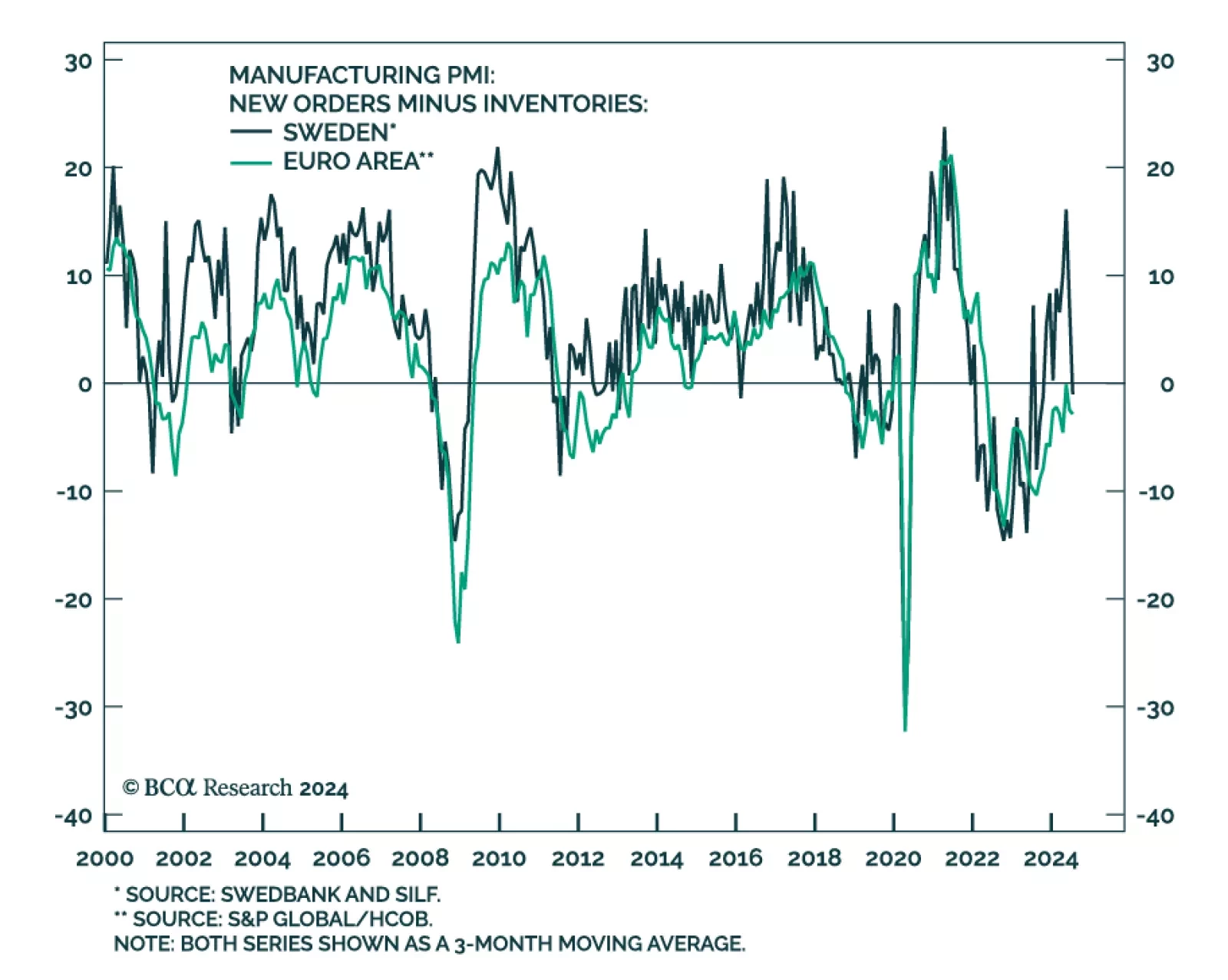

Sweden’s manufacturing PMI started contracting in July, plummeting from 53 to 49.2, falling far short of expectations that growth would broaden. Weakness was broad-based. Notably, new orders and new export orders plunged a whopping 15.1 and 8.7 points in…

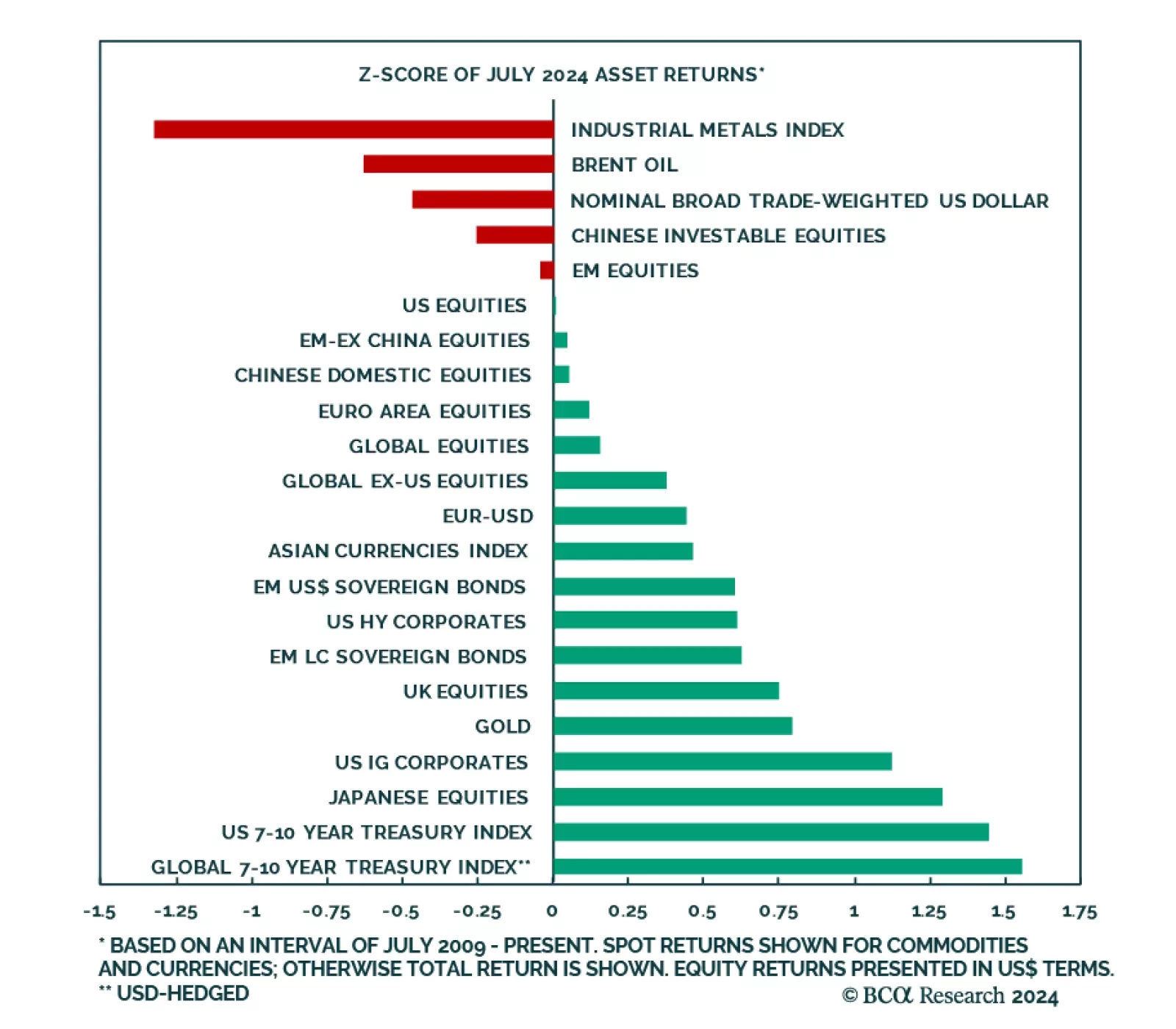

No clear risk-on/risk-off pattern emerged from July’s market performance data. On the one hand, consistent with a risk-off environment, US bonds ranked highest in the monthly return distribution, while pro-cyclical industrial metals and oil lagged.…

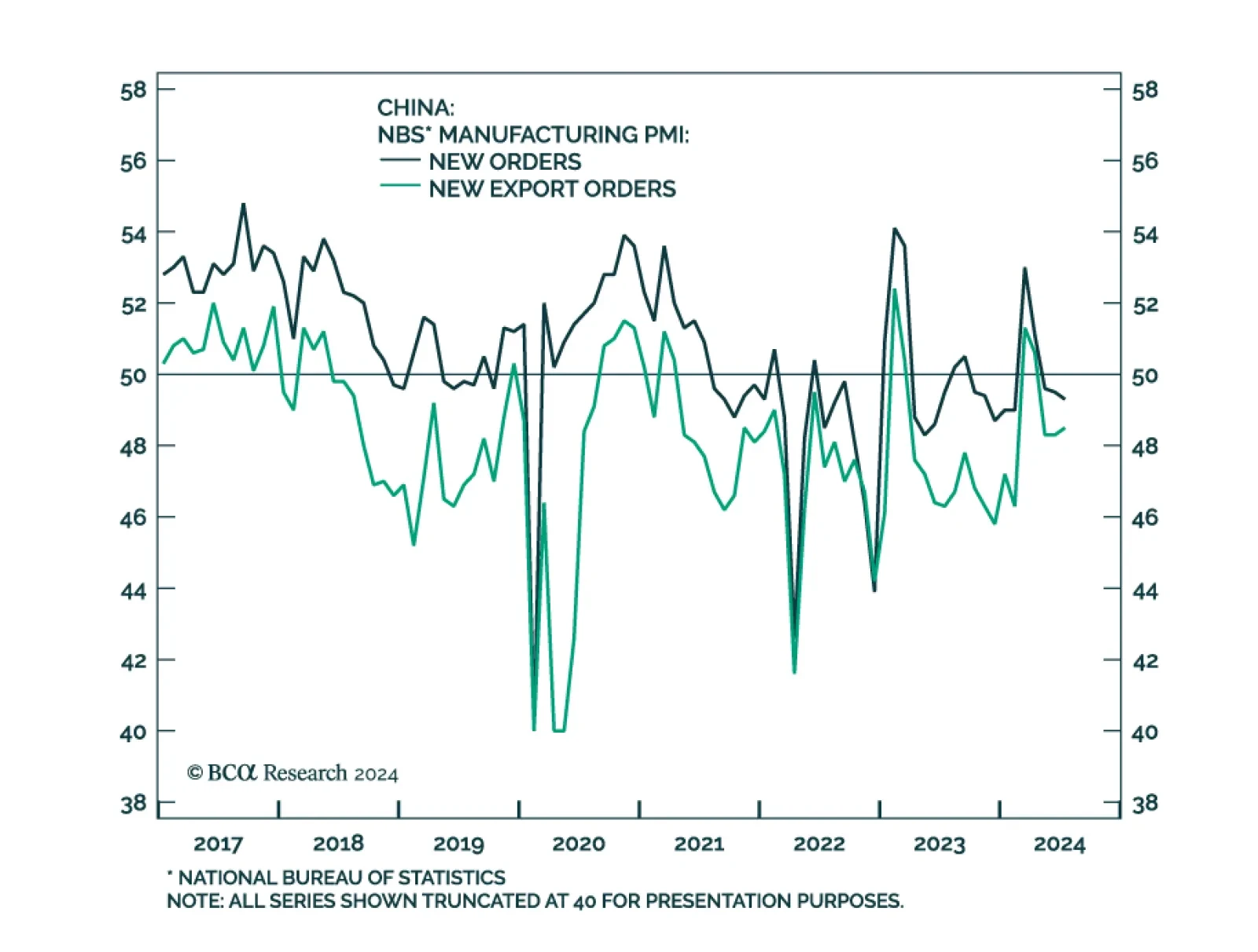

China’s NBS manufacturing PMI declined further in July, from 49.5 to 49.4, marking a third consecutive month of contraction. New orders and new export orders underscored continued weakness in both domestic and foreign demand conditions. Meanwhile, the NBS…

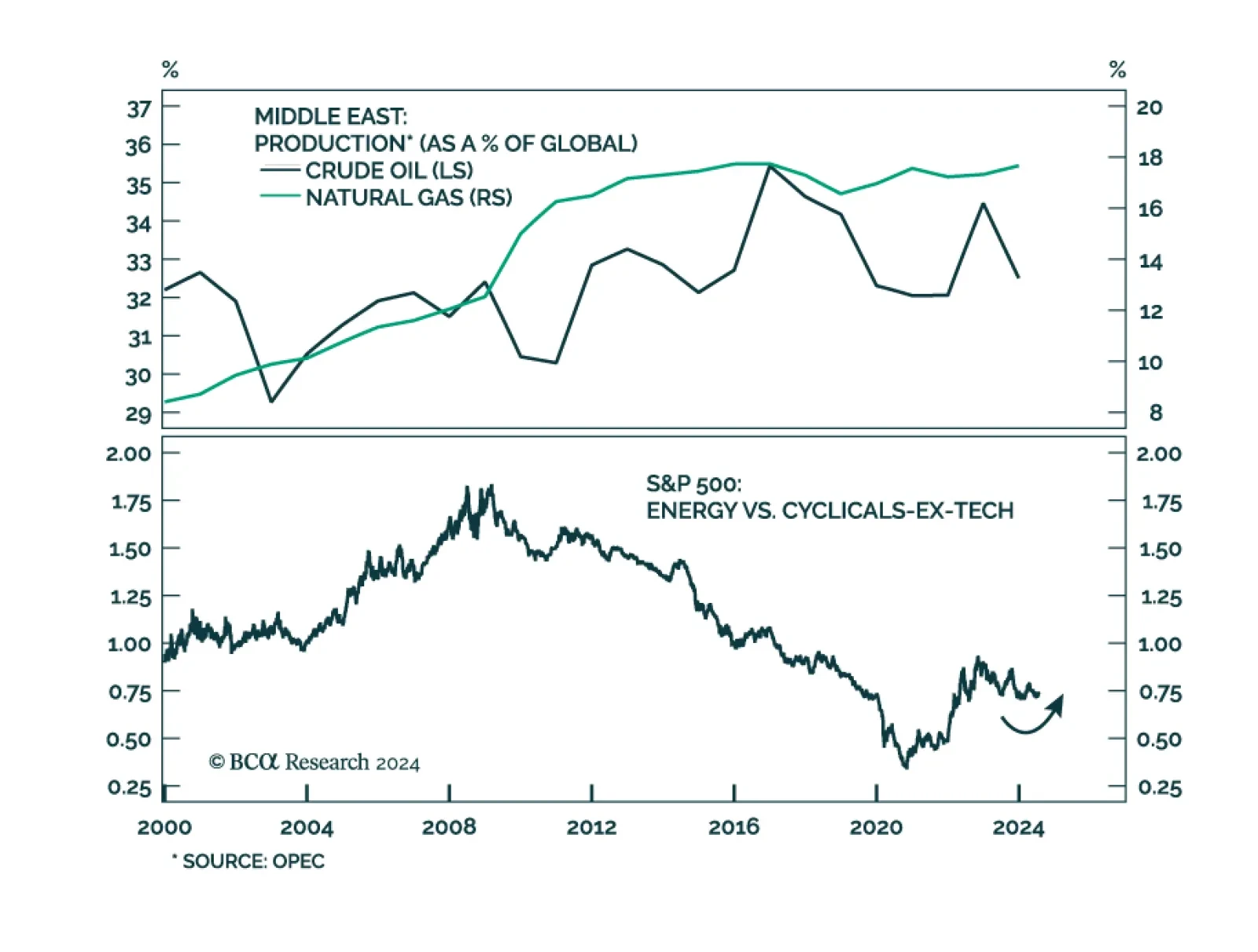

Following the recent escalation in the Middle East conflict, BCA Research’s Geopolitical Strategy service upgrades its subjective odds of a major oil supply shock to 37%. Volatility should spike again as investors contemplate the prospect of rising oil prices…

Historically, interest-rate sensitive sectors such as financials and real estate have tended to post the highest returns in the 3 months preceding the first Fed rate cut. Interestingly, industrials, typically a deep cyclical sector, have also tended to post…

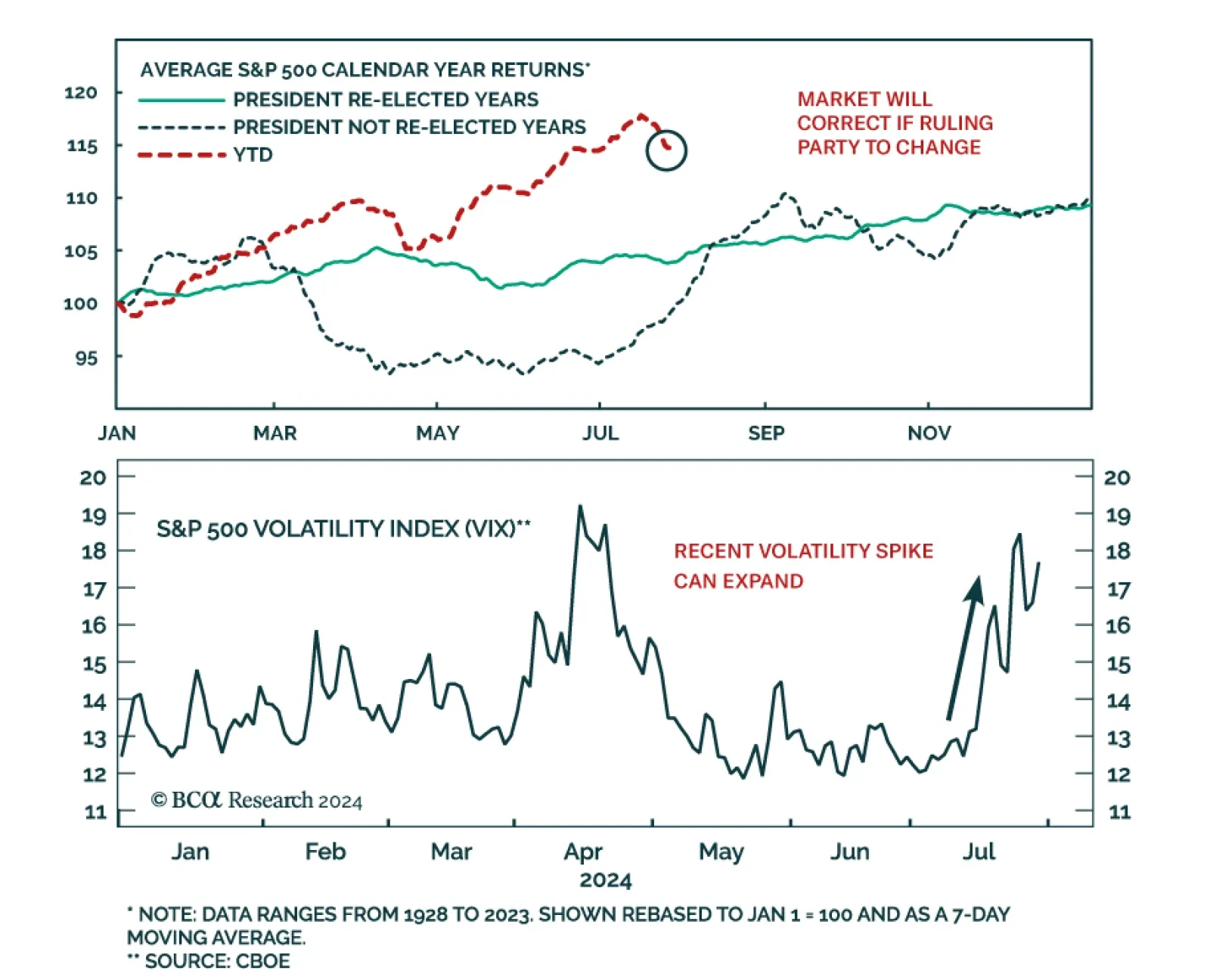

According to BCA Research’s US Equity Strategy service, the stock market outperformance in 2024 thus far is an unusual pattern in election years. The historical data imply that the market will suffer a spill if investors come to believe the incumbent party…

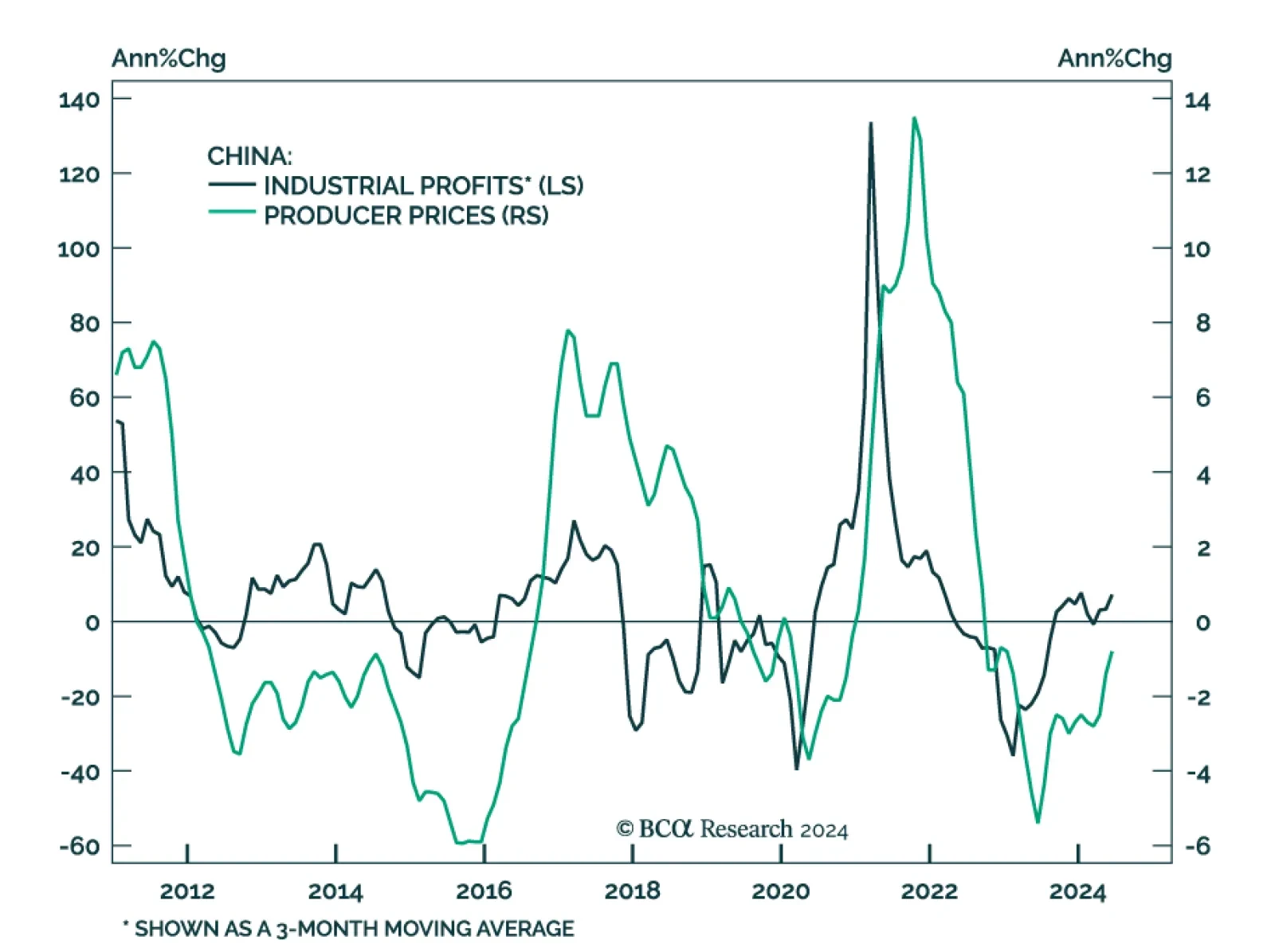

Chinese industrial profits growth accelerated in June, rising from 0.7% y/y to 3.6%. Profits expanded at 3.5% in the first half of 2024, compared to 3.4% in the first half of 2023, and suggest that China’s manufacturing sector remains resilient. A slower…

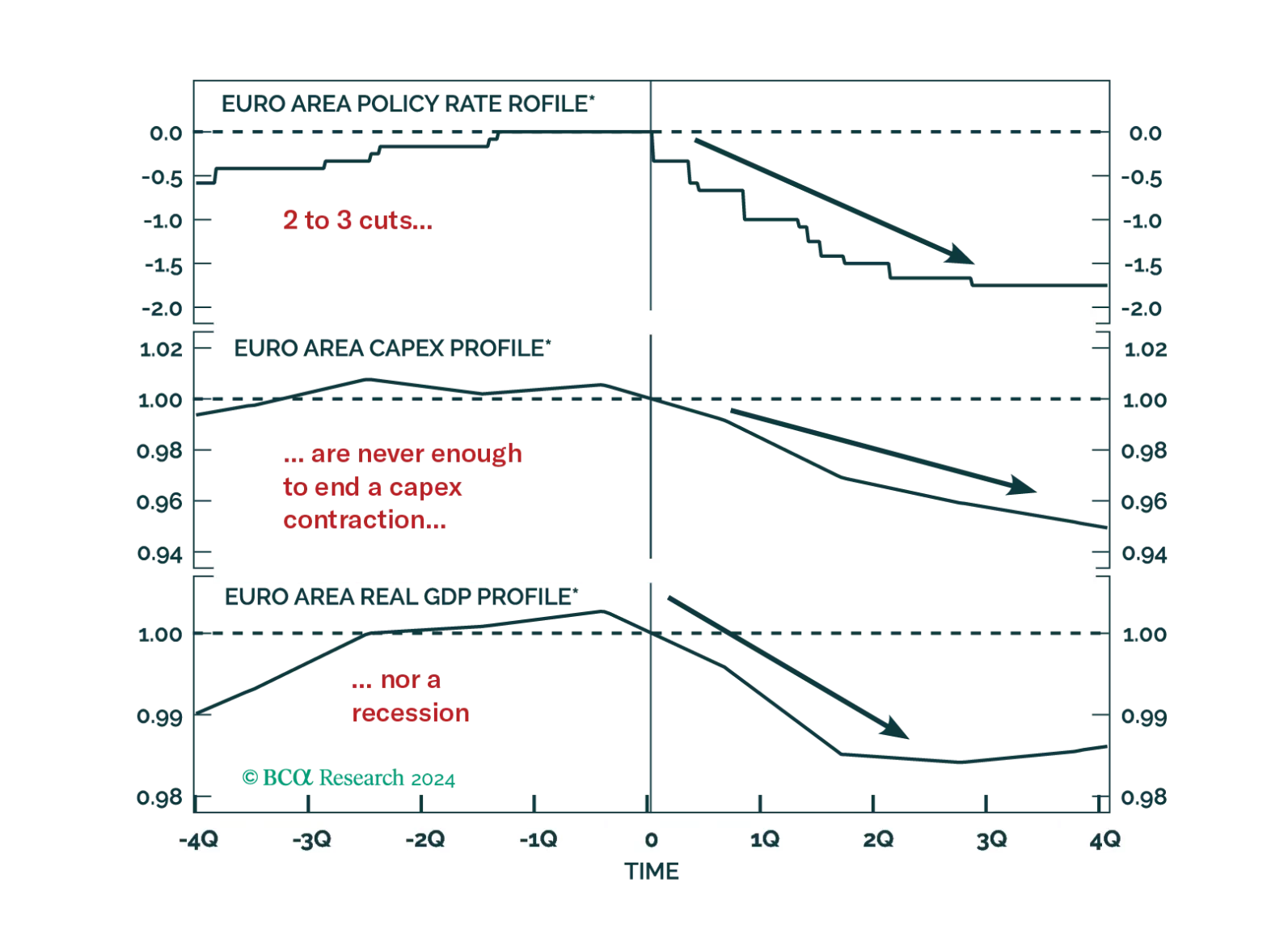

Investors hope that the ECB rate cuts priced into the curve will be sufficient to achieve a soft landing in Europe. History argues against this view, but will this time be different?

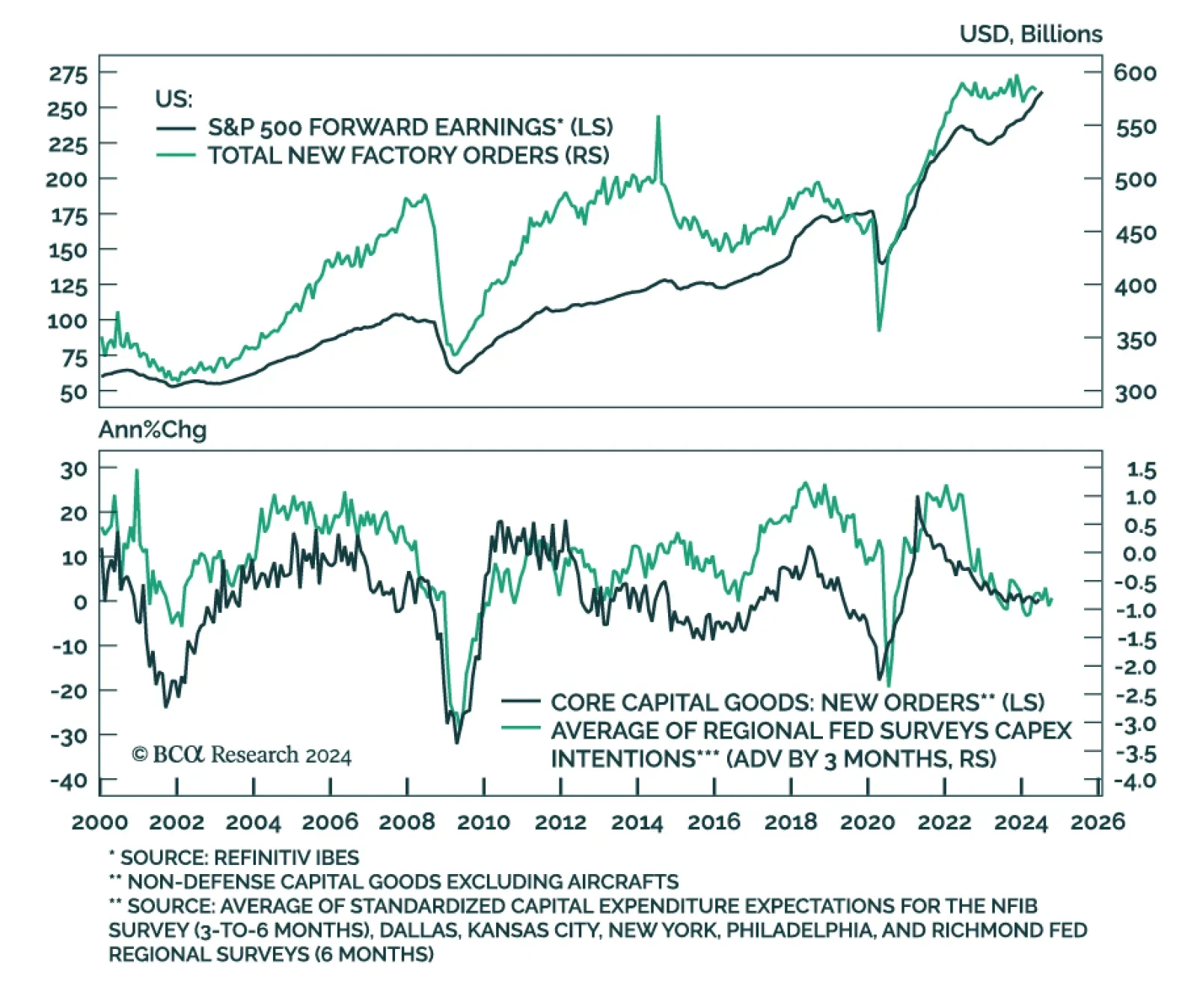

Preliminary estimates suggest that US durable goods orders plummeted in June. They contracted 6.6% m/m, largely disappointing expectations of a faster pace of growth. However, a whopping 127% monthly decrease in highly volatile commercial aircrafts orders…