Equities

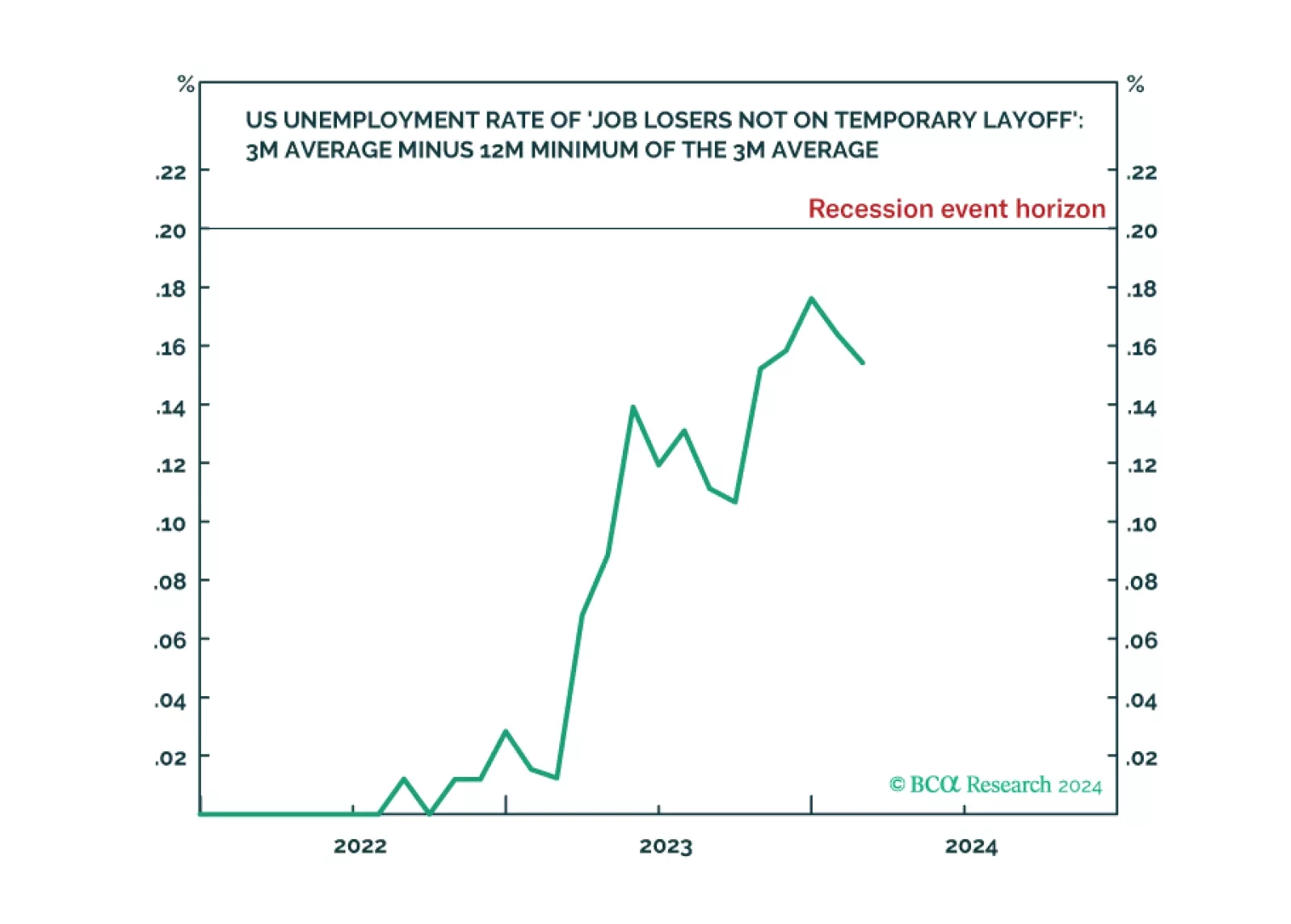

The Joshi rule real-time US recession indicator remains at an elevated 0.154 versus its recession event horizon of 0.200, indicating weakening US labour demand. With the last mile of US disinflation requiring labour demand to ‘catch down’ with labour supply, investors should watch the Joshi rule very closely to pre-empt a potential tipping-point. Plus: tactically long Portugal versus Europe, and wheat versus cotton; and tactically short USD/CLP, Qualcomm (QCOM), and Salesforce (CRM).

We are pushing back the anticipated start date for a Eurozone recession and assessing how it affects our equity stance.

Clients are increasingly more positive about the US economy, but there are no signs of exuberance. The rally could continue as the majority is not fully invested. Financial conditions have already eased, and the Fed is unlikely to surprise on the upside but will deliver a promised cut this summer. CRE is a still pain point of the US economy. We are not bearish, but after a fast and furious rally, markets are fragile.