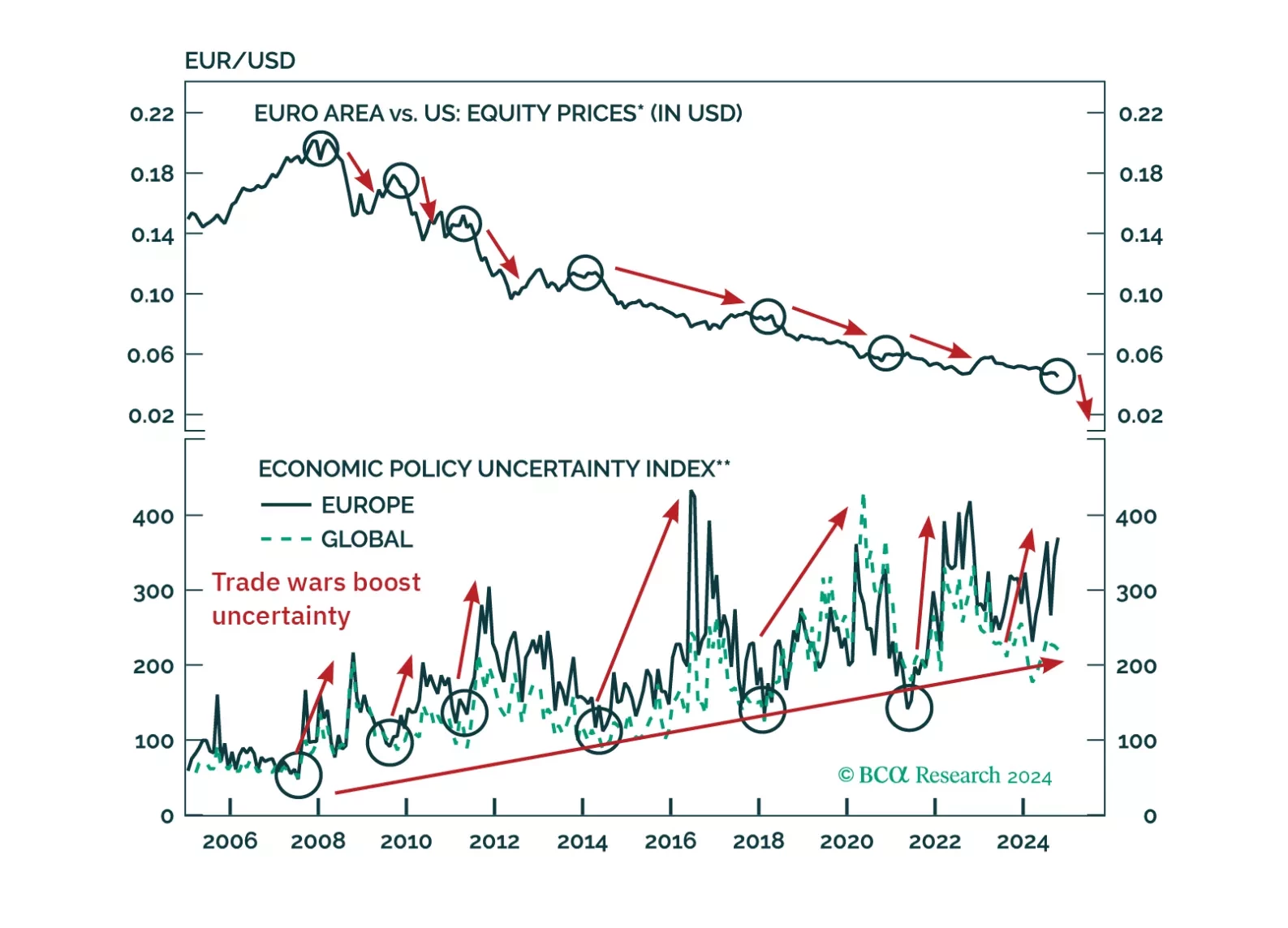

Euro

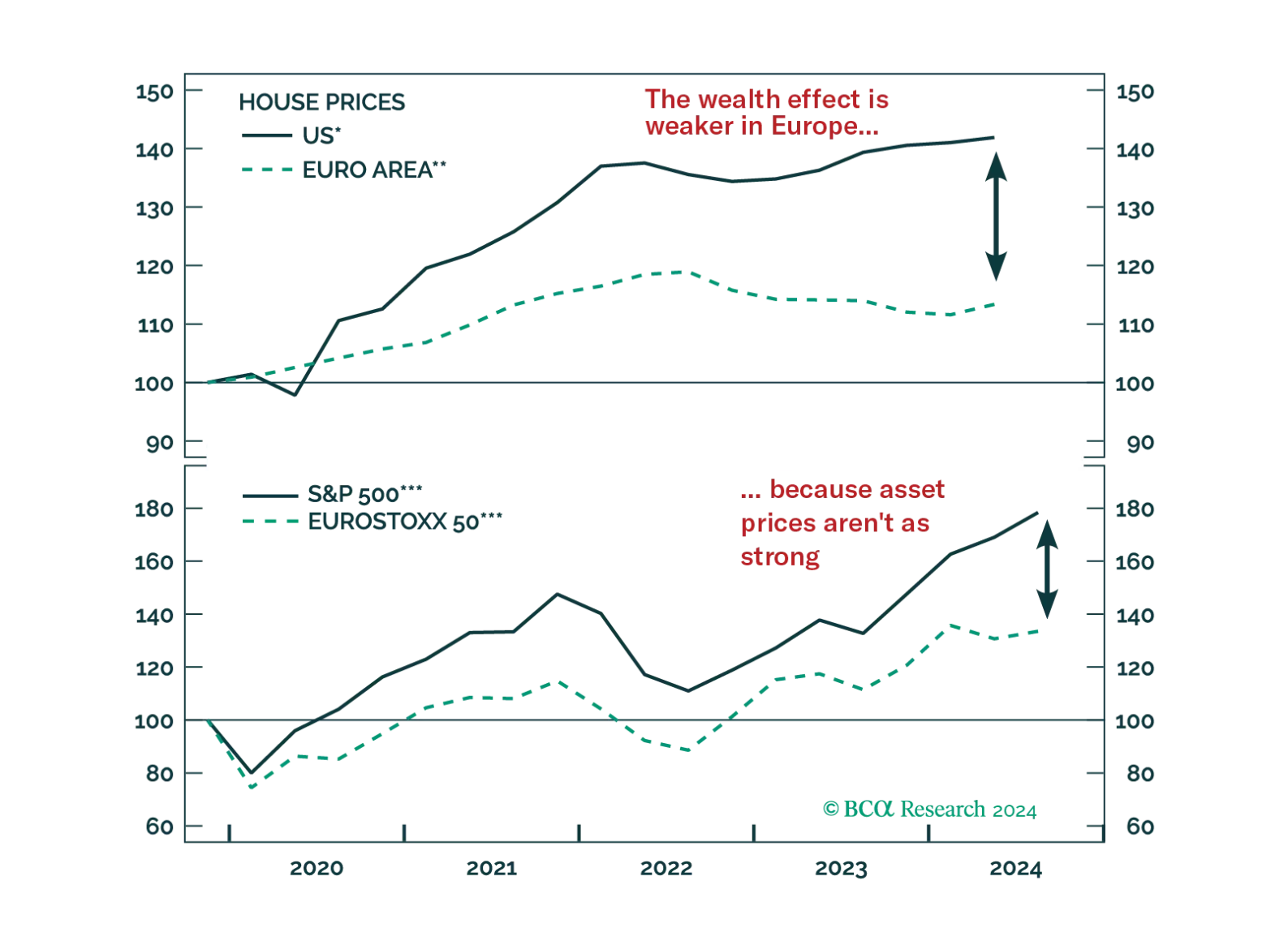

European assets and the euro have become oversold and are likely to rebound. Will this move be nothing more than a dead cat bounce leading to more weakness?

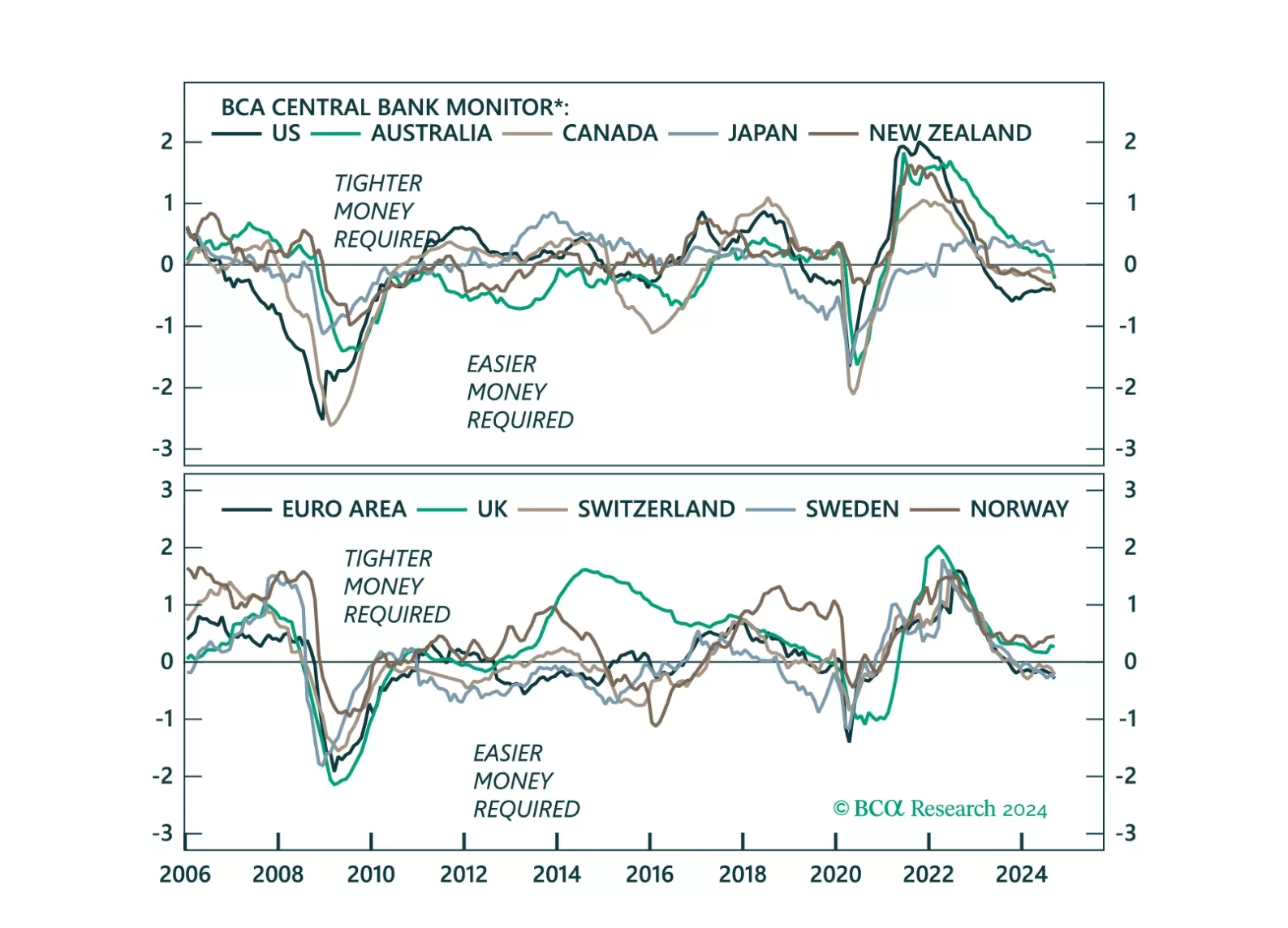

This week, we update our Central Bank Monitors (CBMs), that help us calibrate how monetary policy should be adjusted in developed-market economies. Our conclusion is that while overall, easier monetary settings are required, there a few trade ideas that arise from the divergences in signals amongst G10 countries.

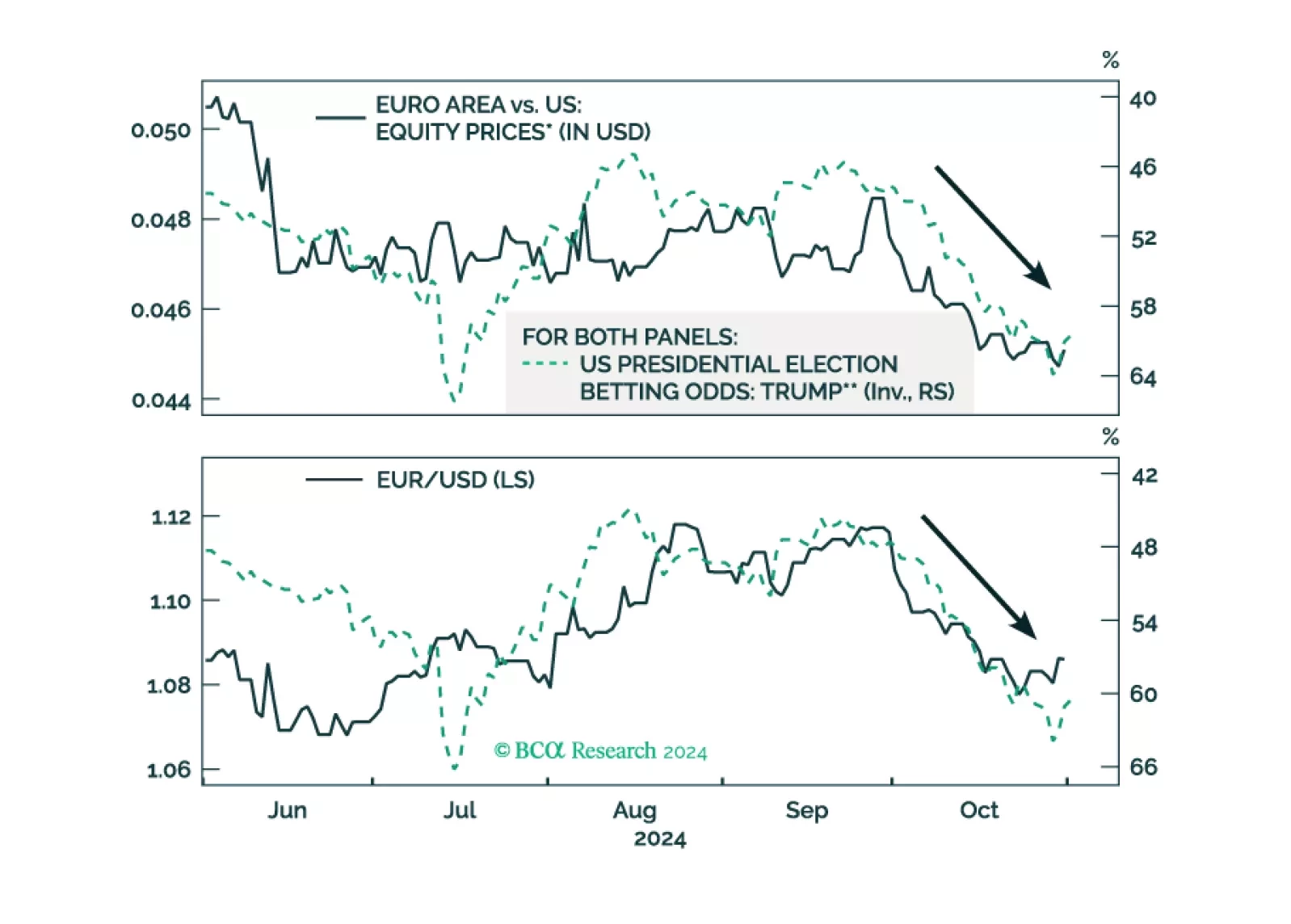

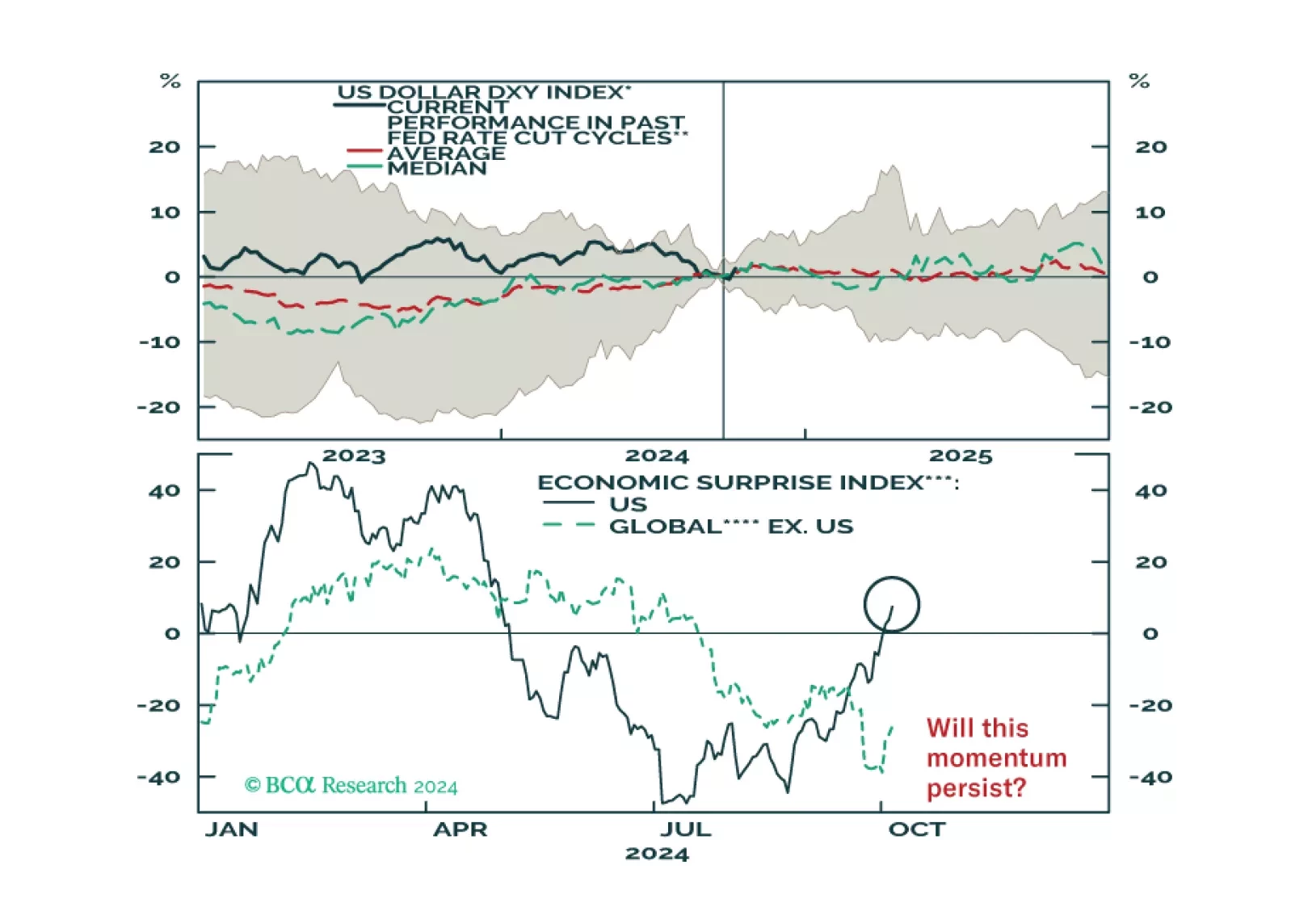

As the odds of a Trump victory rise, European assets underperform US ones. What would be the immediate impact of a Trump victory on European stocks?

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.

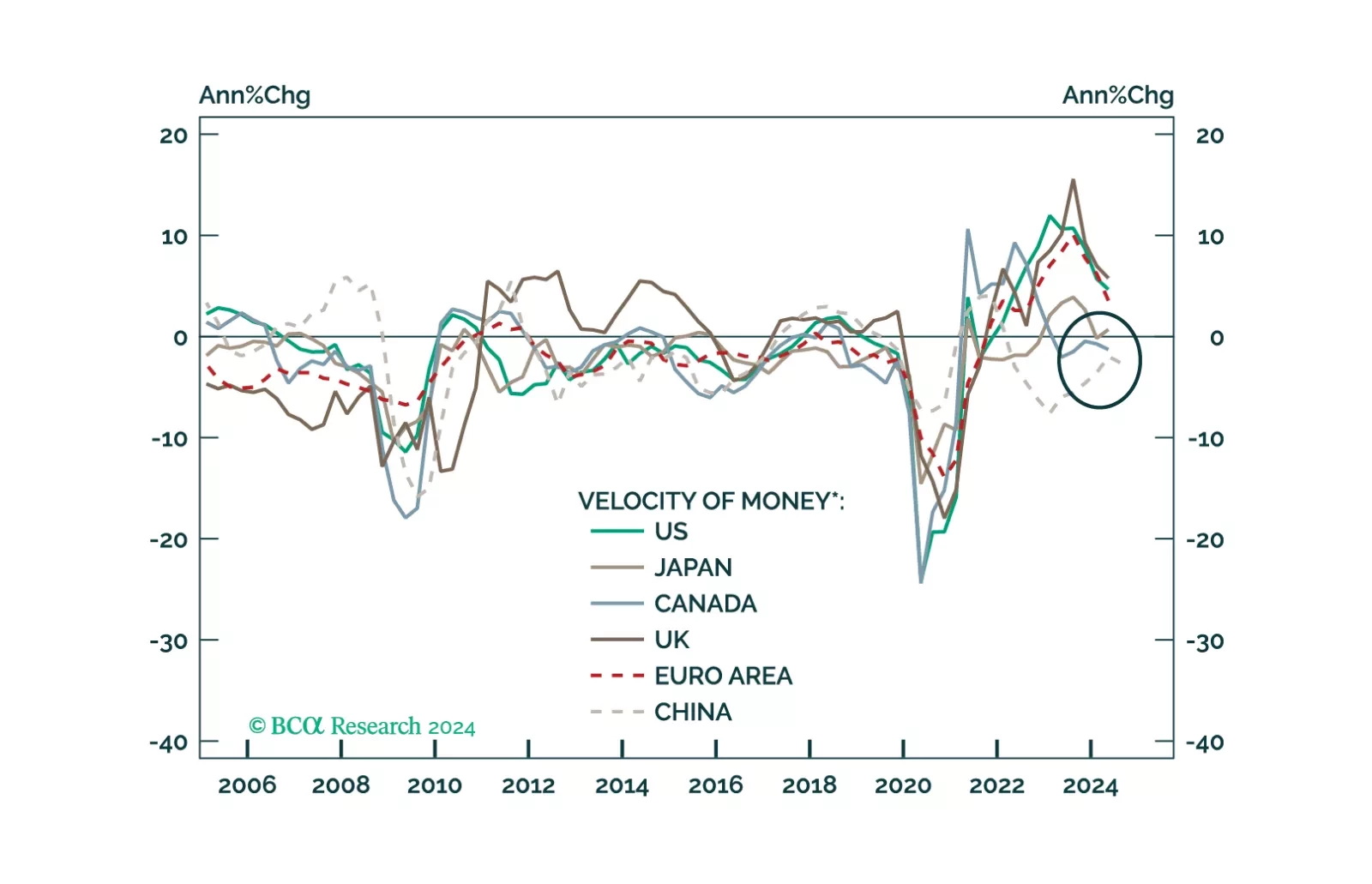

This Insight looks at the likely direction of bond yields and the dollar, from the lens of money velocity.

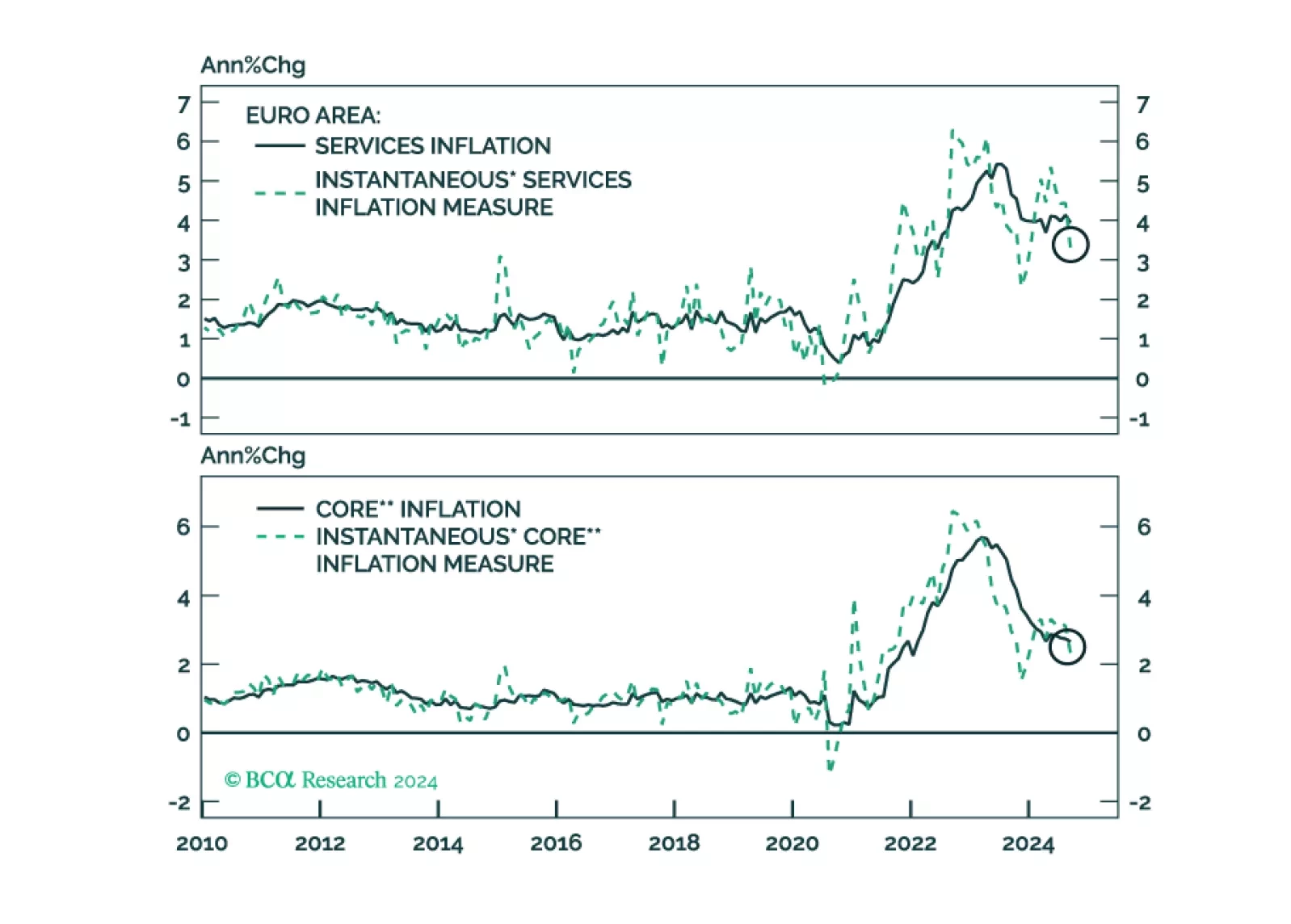

Yesterday, the ECB solidified its recent dovish tilt in response to weaker growth and decreasing inflationary pressures. It is now set to cut rates 25bps each meeting. How low will the ECB deposit rate ultimately go and what does this imply for yields and the euro?

This week, we cover the main questions we fielded during our latest client trip in Europe. Among the many topics broached are Europe’s recession odds, the impact of China’s stimulus, and the outlook for European markets.

This report looks at the likely path for the dollar and bond yields over the next 6-to-12 months.