Euro Area

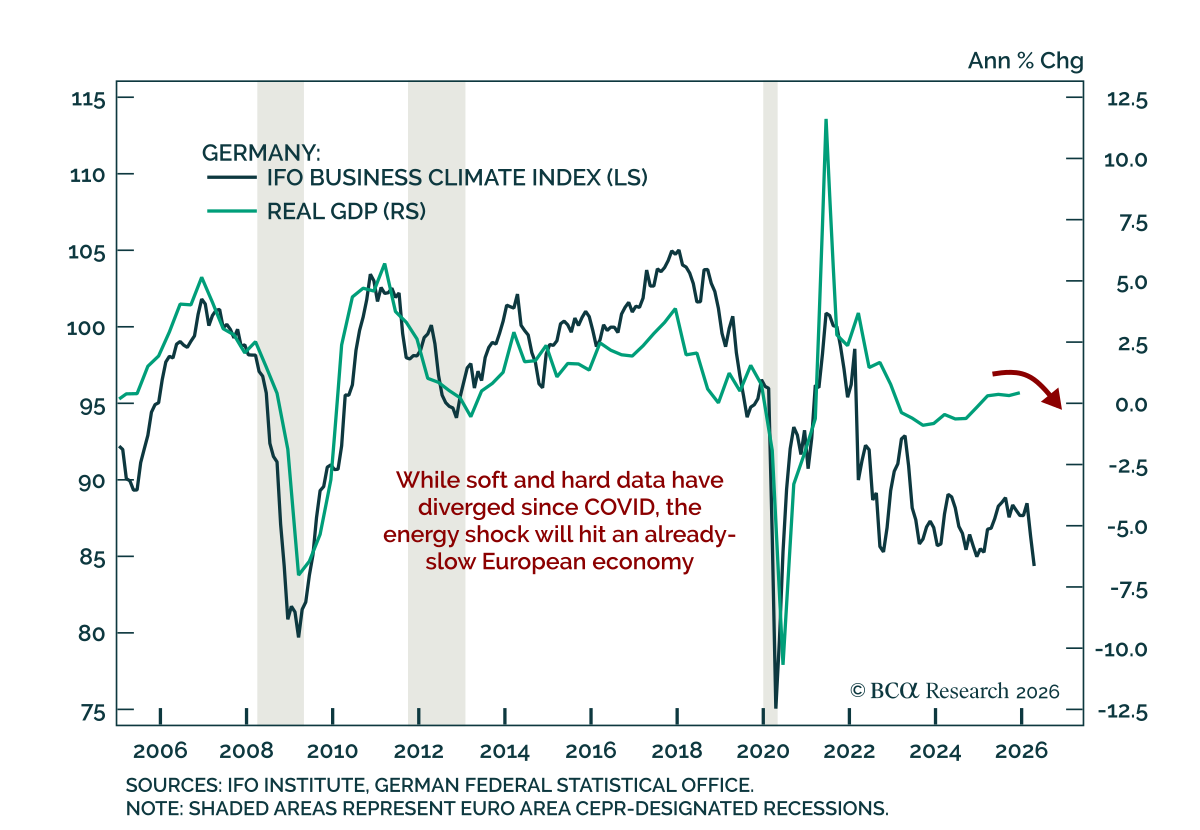

German data continue to deteriorate, reinforcing Europe’s vulnerability to a prolonged energy shock. The May GfK German Consumer Climate indicator fell to -33.3 from -28.1, a level not seen since the 2022 energy shock and near all-time lows for the series.…

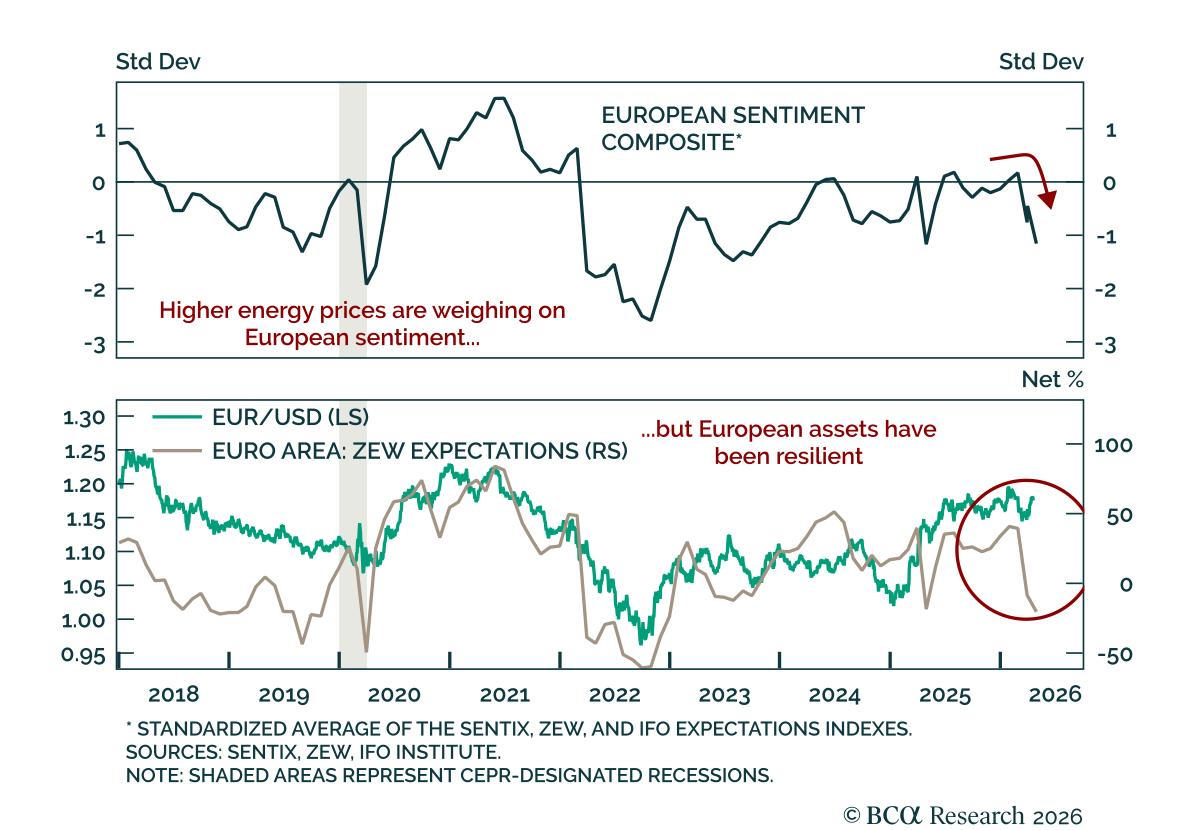

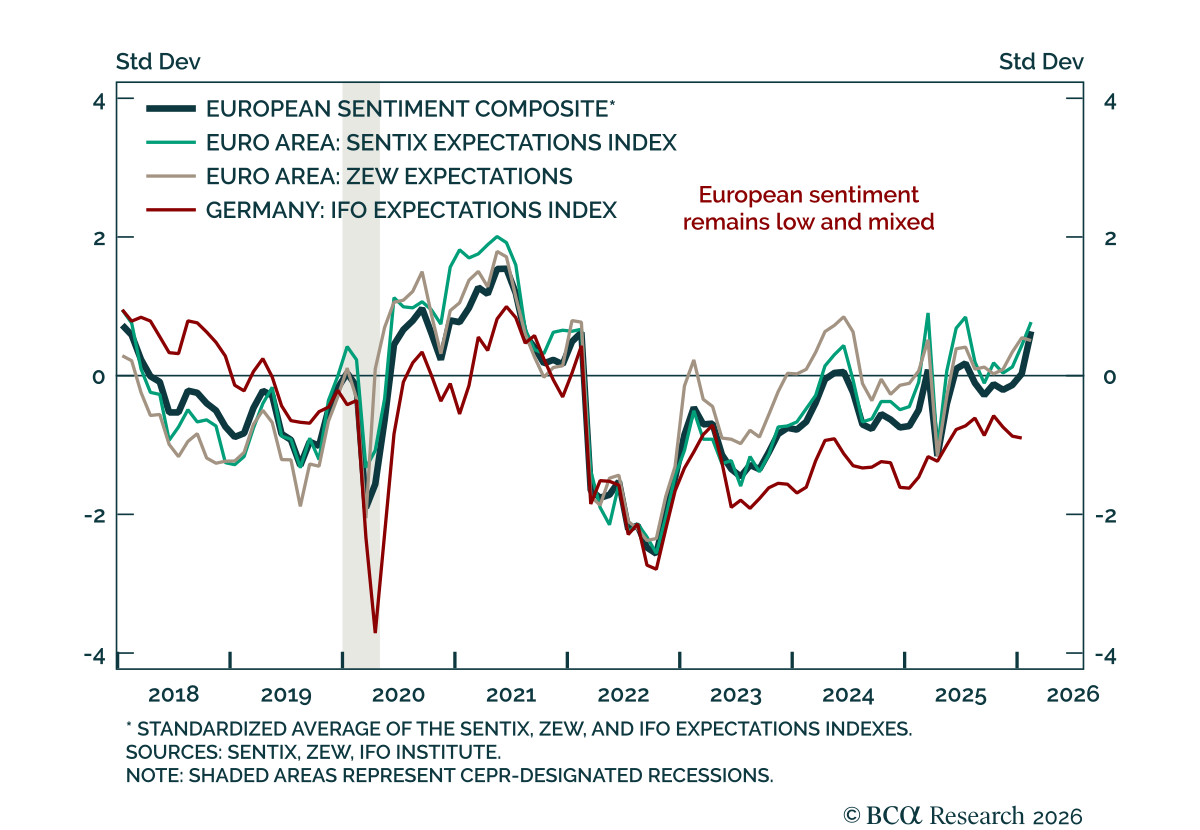

The April ZEW showed continued deterioration in European sentiment, with no sign yet of a rebound. Germany’s expectations component missed estimates and fell to -17.2 from -0.5, while the eurozone measure fell to -20.4 from -8.5. Current conditions in Germany…

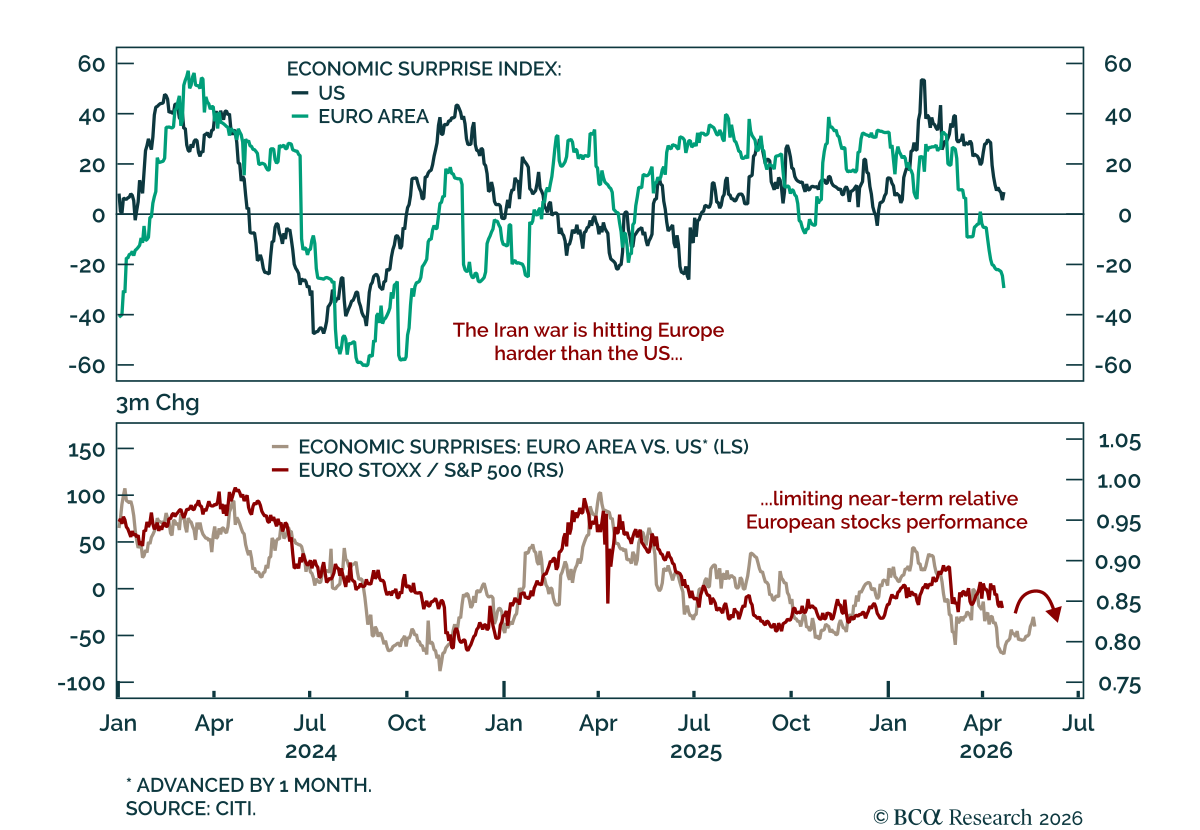

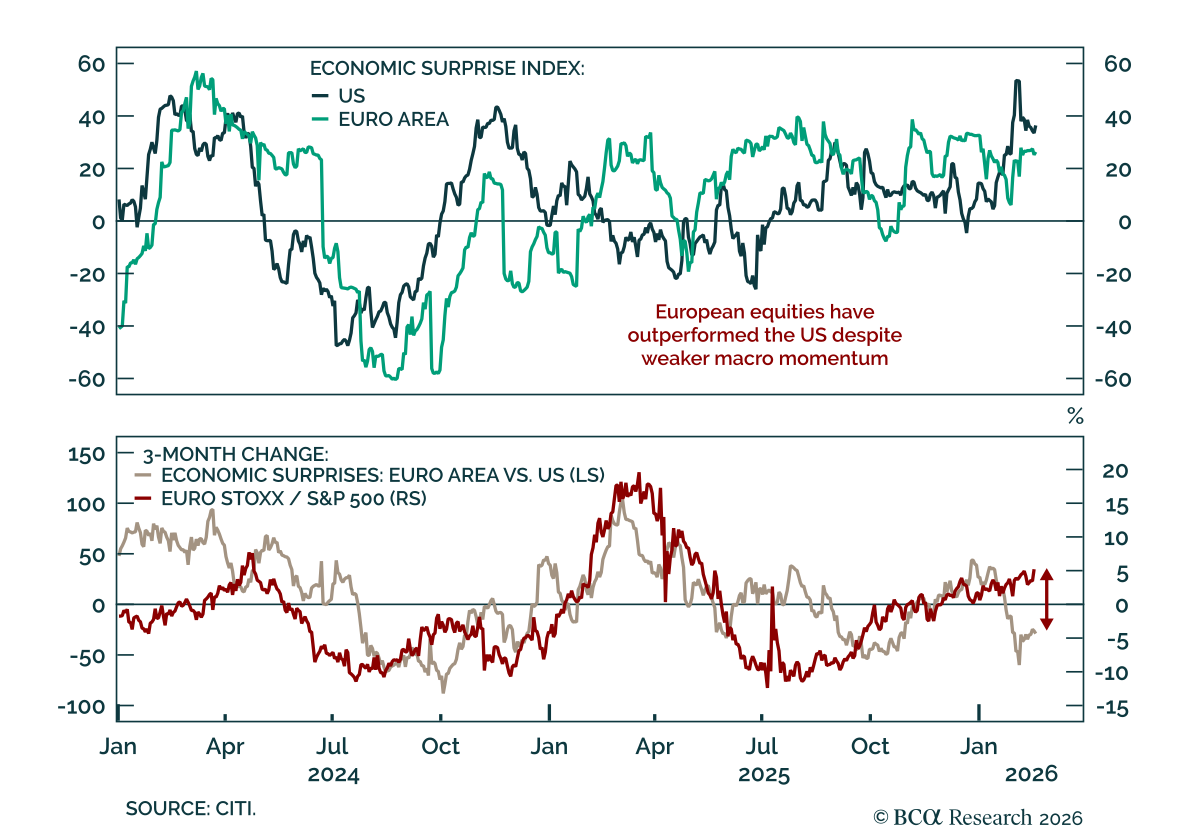

Relative momentum still favors the US over Europe despite the Hormuz shock. Our tactical framework rests on two ideas: The feedback loop between financial conditions and economic surprises, and macro momentum’s role in cross-asset returns. The Hormuz…

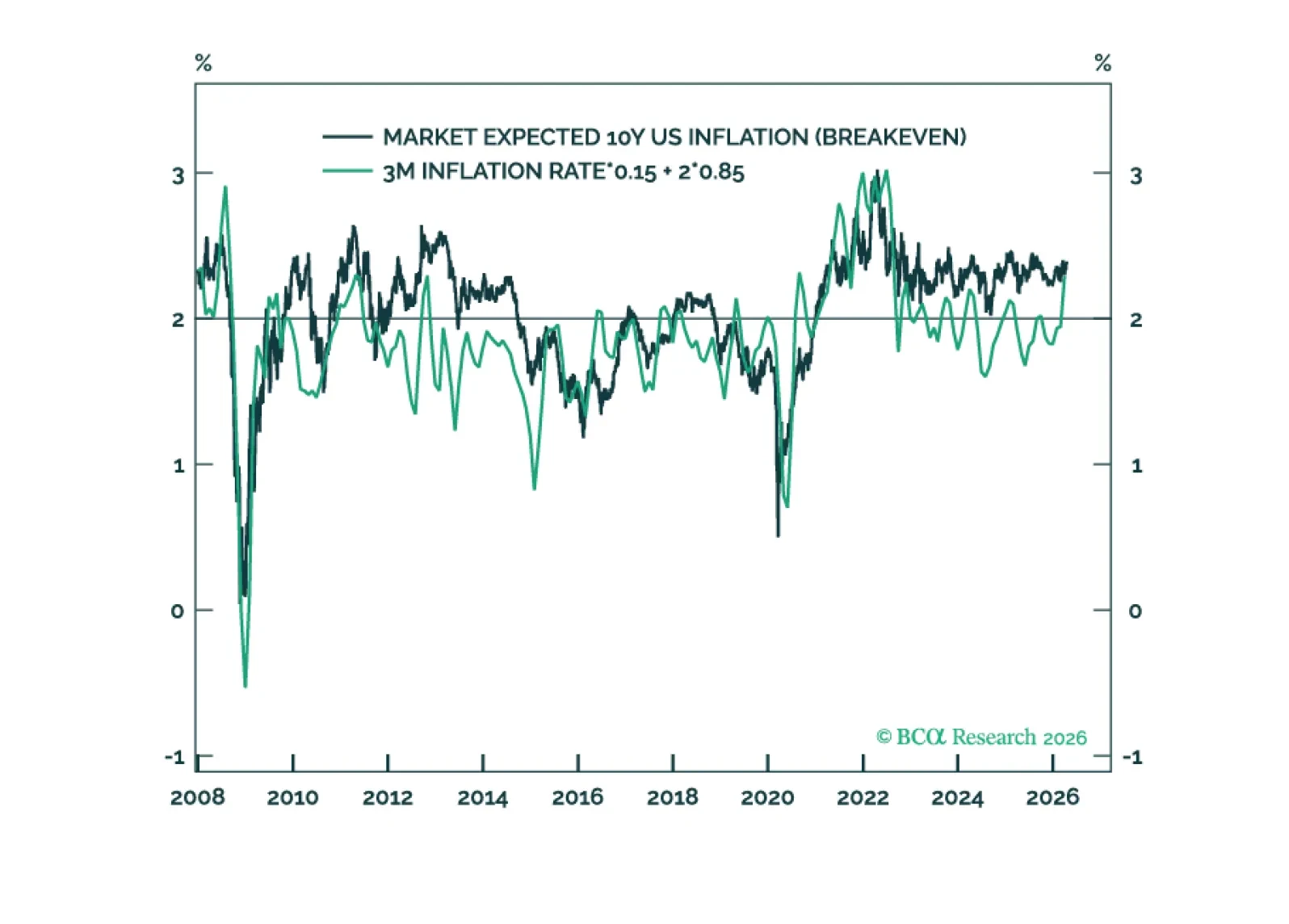

In this Special Report, we describe how inflation expectations are formed. We then demonstrate that steady state inflation expectations have un-anchored in the UK, are un-anchoring in Japan, and are at high risk of un-anchoring in the US. And we conclude with some implications for bond markets.

EM equities remain vulnerable because share prices have run well ahead of underlying profits. Our Chart Of The Week comes from Arthur Budaghyan, Chief Emerging Markets/China Strategist. Since January 2023, the MSCI EM Equity Index has rallied 40% in USD…

March flash PMIs point to rising inflation pressures, with the US more resilient than its DM peers. Input costs rose and delivery times lengthened across developed markets. Manufacturing was resilient, but services PMIs declined. The US PMIs pointed to…

The ECB held rates but higher energy prices complicate the outlook for inflation and growth. The European Central Bank left rates at 2%, but revised its forecasts. December projections pointed to an inflation undershoot, but forecasts now see both headline…

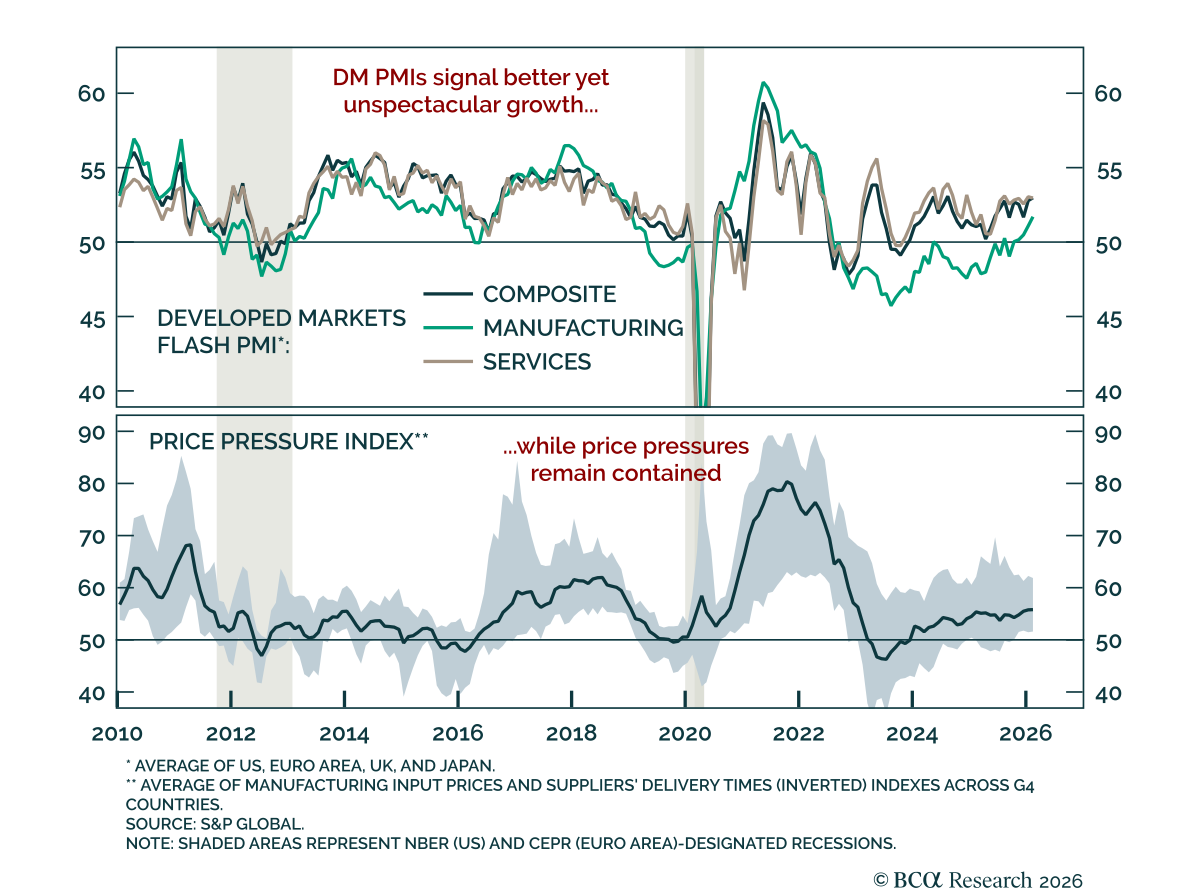

February flash PMIs edged higher, pointing to gradual improvement in global growth. After moving mostly sideways through 2025, developed markets PMIs are picking up. Manufacturing is showing decent momentum, rebounding after being weighed down by trade…

Relative macro momentum suggests scope for US tactical equity outperformance versus Europe. Just as macro momentum drives cross-asset returns, relative momentum helps explain cross-country equity performance. A simple measure is the difference in economic…

European sentiment has yet to reach escape velocity, with growth momentum still limited. The February ZEW showed expectations declining to 39.4 from 40.8 at the Euro Area level. In Germany, expectations fell to 58.3 from 59.6, missing expectations, while…