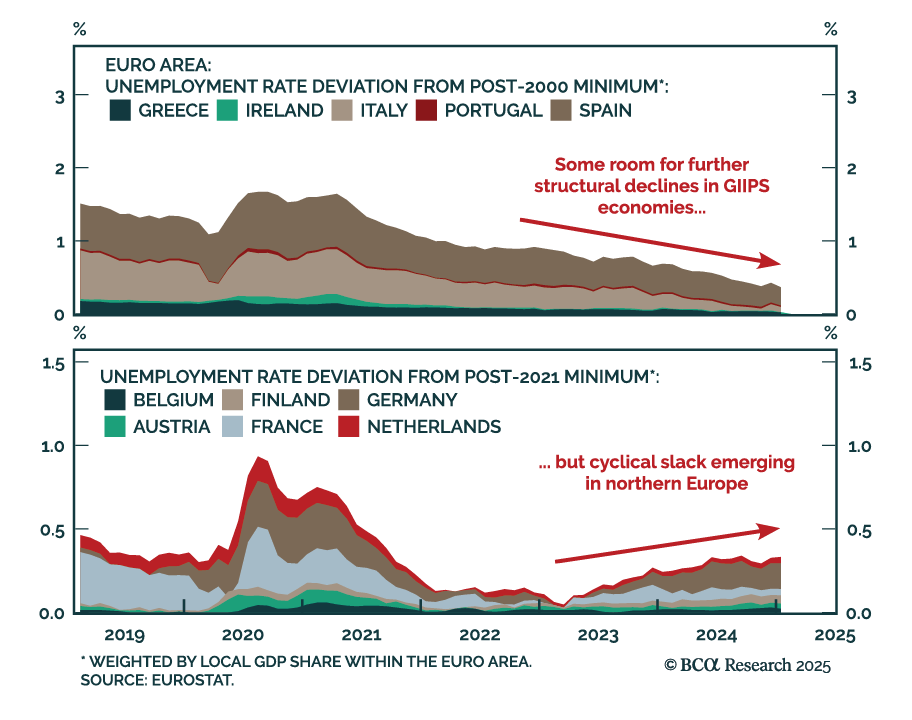

Euro Area

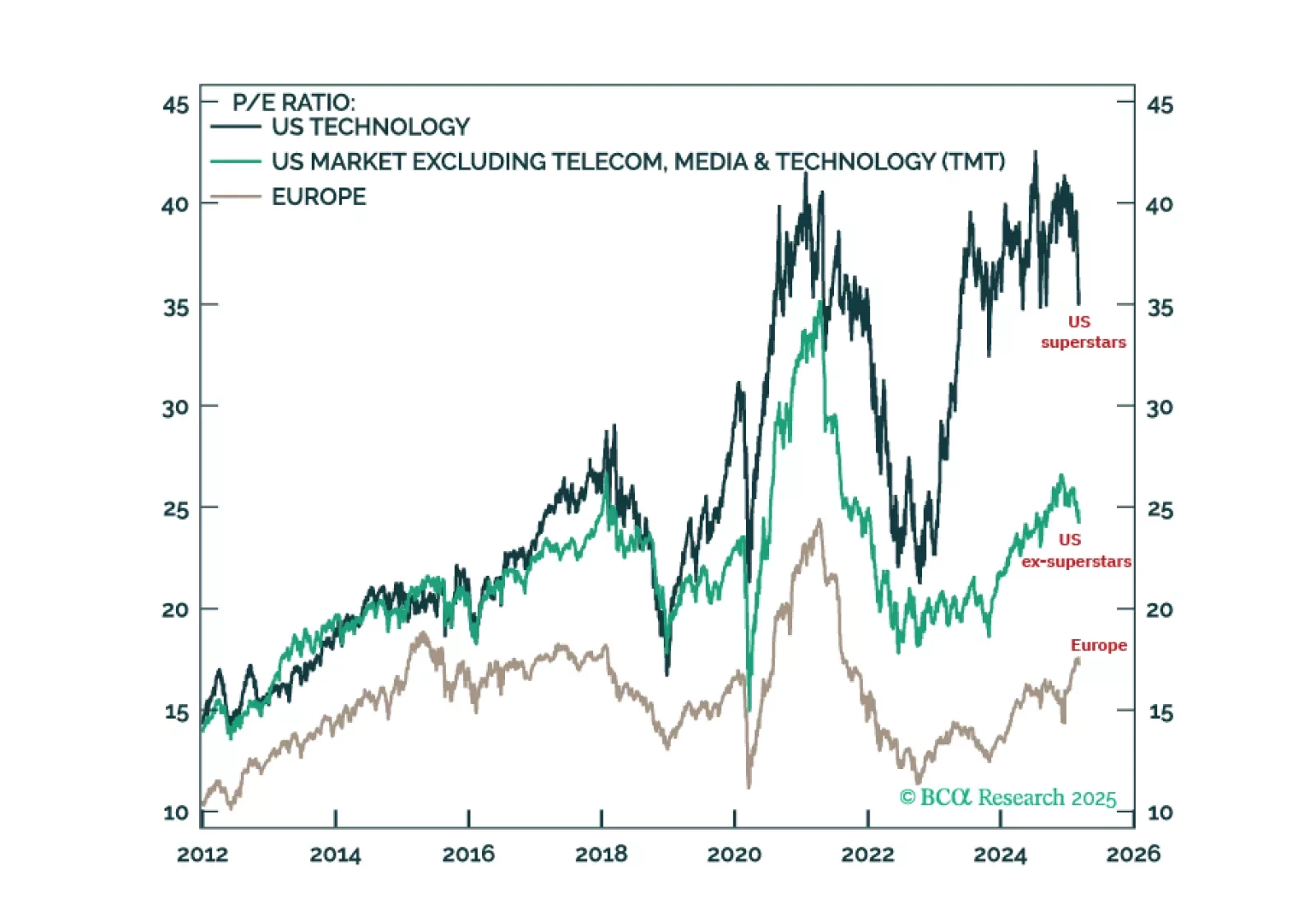

US stock market outperformance has been driven entirely by the 0.0002 percent of US superstar companies. But this superstar outperformance is based on two highly questionable assumptions: that all productivity gains from the generative-AI revolution will go into corporate profits; and specifically, into the profits of the Web 2.0 superstars which will morph into the generative-AI superstars. As these assumptions become undermined in the coming quarters, relative performance will reverse, starkly. On a structural horizon, stay maximum overweight Europe versus the US. Plus: time to go underweight global financials (IXG).

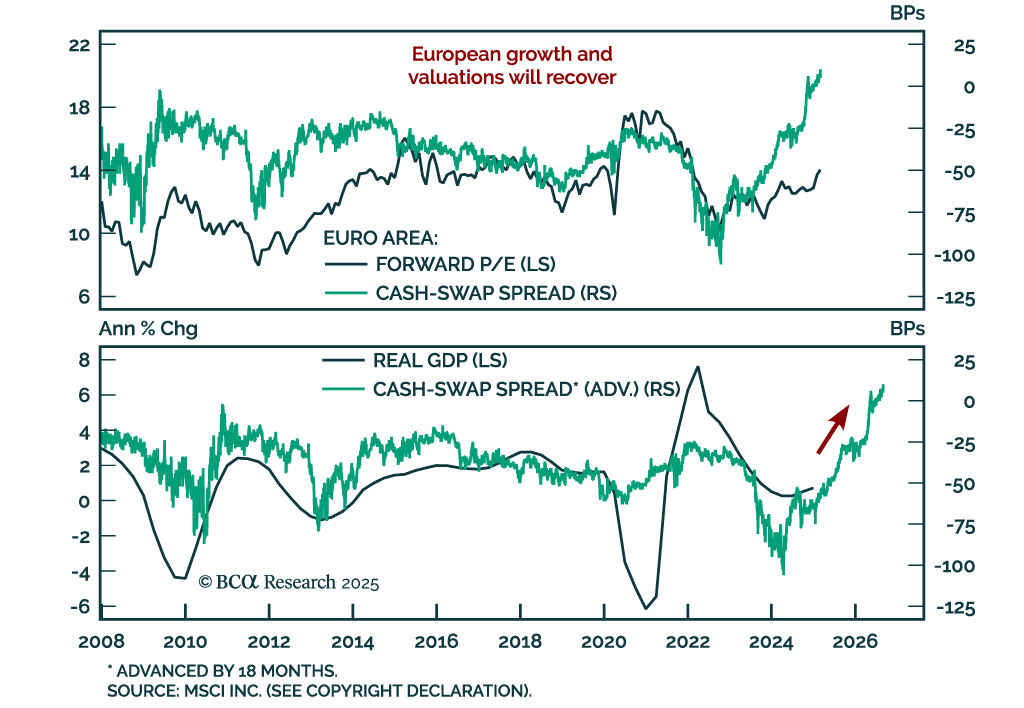

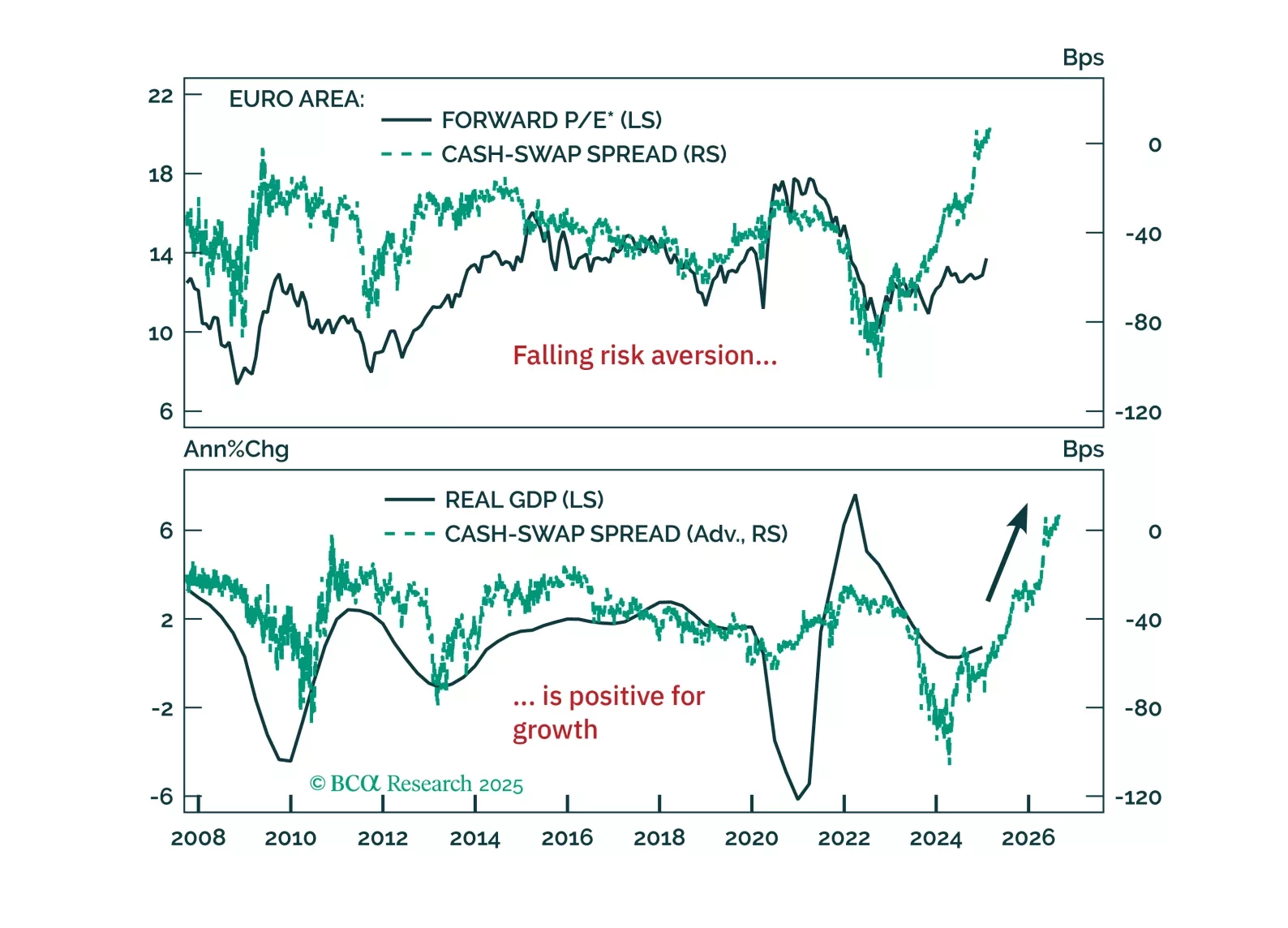

Europe’s resilience to global liquidity deterioration isn’t a fluke—it signals a structural shift. Our latest report explains why the decline in precautionary money demand marks the end of Europe’s liquidity trap and what it means for investors.

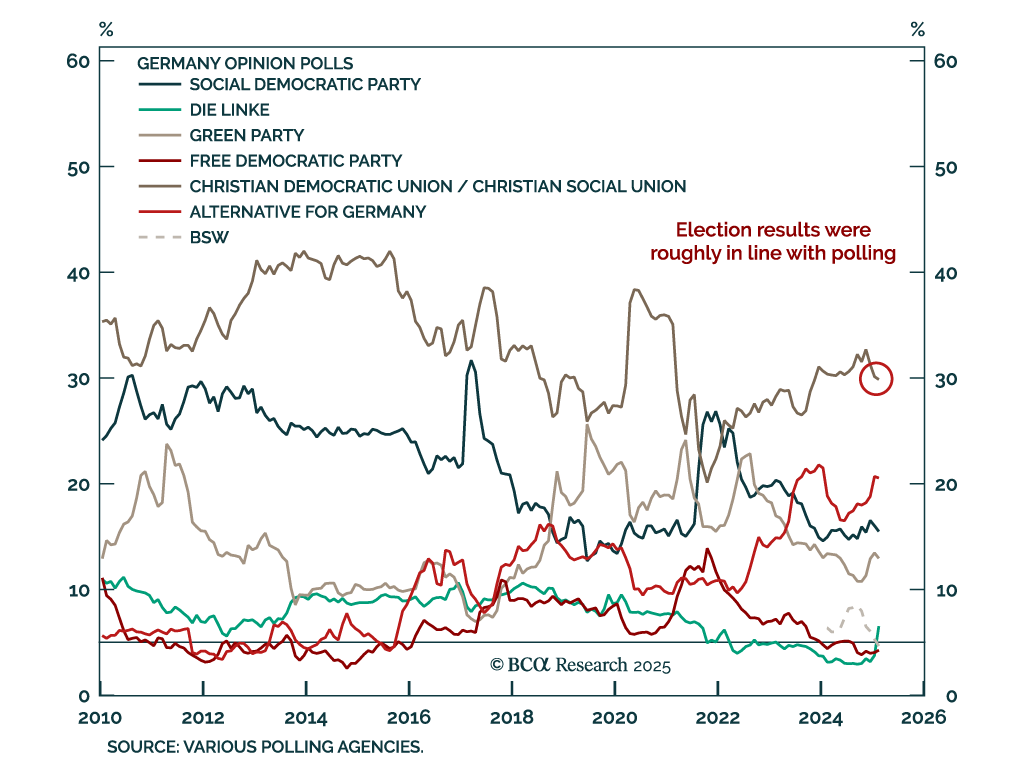

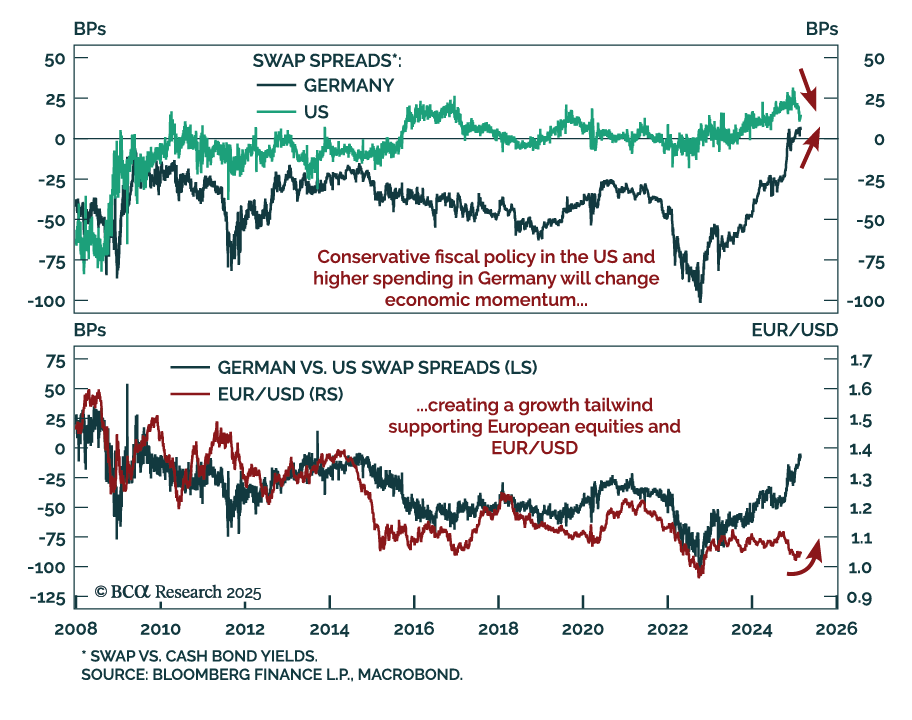

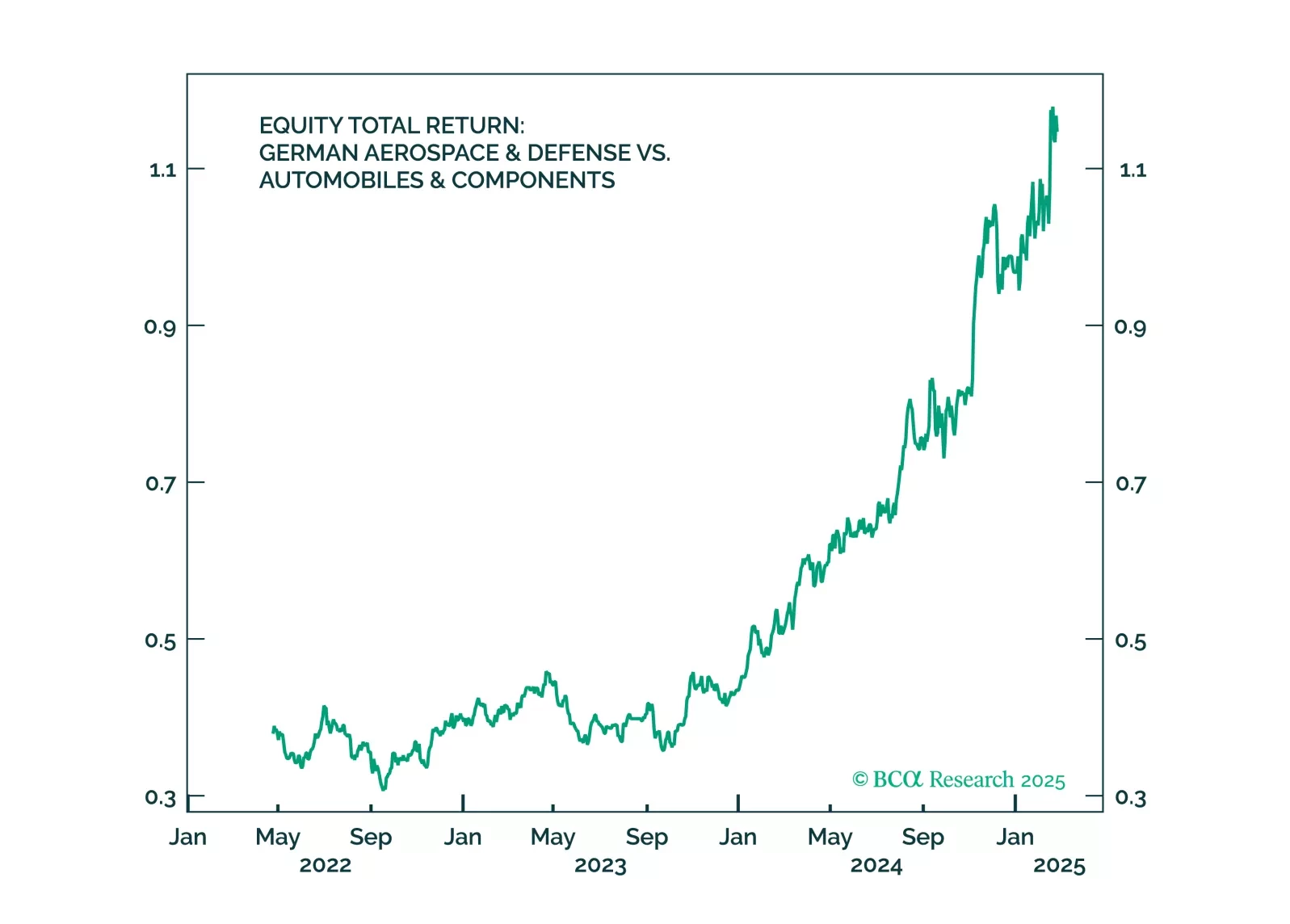

Trump’s ceasefire talks are positive for Germany – and so was the German election result. But Trump’s tariffs will hit Germany soon. Investors should use near-term volatility to increase exposure to Germany.