Euro Area

Preliminary estimates suggest that Eurozone headline and core CPI inflation decelerated from 2.2% to 1.8% y/y and from 2.8% to 2.7%, respectively, in September. The inflation data from individual Euro Area countries earlier last week had already prompted…

Our expectation that a looming US recession will morph into a global recession remains intact. US monetary easing will only take effect with a lag and current deteriorating economic conditions are the product of past easing. Meanwhile, China’s…

France’s and Spain’s preliminary September CPI readings declined on a month-on-month basis, clocking in at 1.5% and 1.7% y/y respectively, and undershooting consensus expectations. Germany’s and Italy’s updates are due on Monday and the Eurozone CPI will be…

According to BCA Research’s European Investment Strategy service, the surprise fiscal announcement from China’s Politburo is a very different animal from previous stimulus attempts. Although the details are still vague, it adopts a much more pragmatic tone…

Preliminary estimates suggest that activity continued to slow across DM economies in September. Manufacturing PMIs contracted at a faster pace in the US, Eurozone, Germany, France and Australia, and grew at a slower pace in the UK. Services PMIs continued…

The European Central Bank (ECB) cut rates by 25 bps in September. It did not signal consecutive rate cuts and we highlighted that the short inter-meeting timeframe between September and October provides little scope for ongoing data releases to move the…

German equities have outperformed their Euro Area peers on a year-to-date basis, with the gap widening since May. The MSCI Germany Index returned nearly 4.5 percentage points more than the MSCI Eurozone index over the latter period. Since the beginning of the…

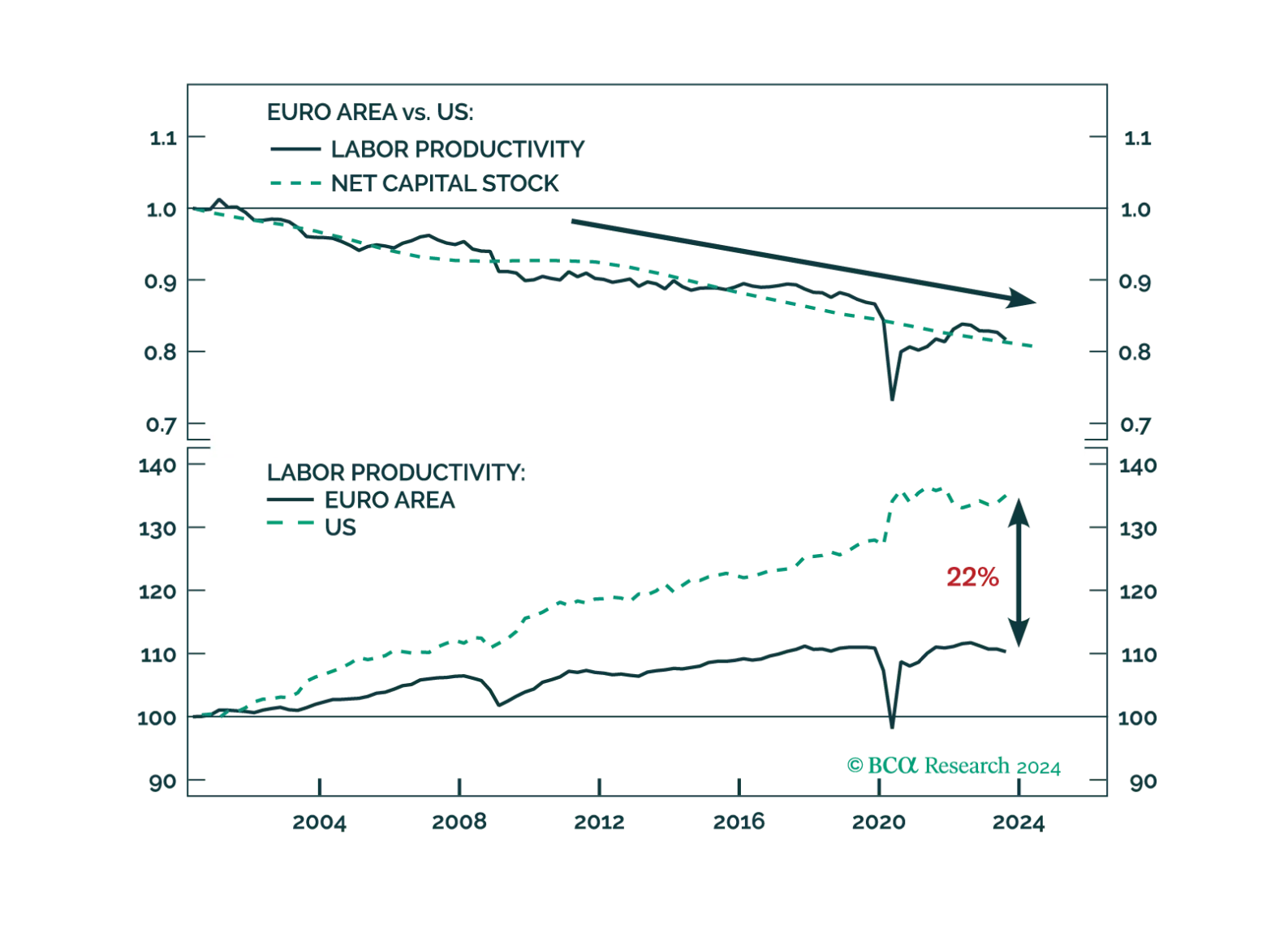

The Draghi report highlights sensible reforms that would address many of Europe’s productivity shortcomings. Whether European capitals heed Mario Draghi’s advices remains to be seen.

Volkswagen’s CEO has been making the point that the market for European carmakers has been deteriorating. Earlier last week, he went on to make a rather pointed reference at Chinese EV manufacturers. He was quoted saying that, "The pie has become…

The US suffers from enough imbalances to produce a mild recession. Unfortunately, such a recession could lead to a significant bear market in stocks, just as it did during the very mild 2001 recession.