Euro Area

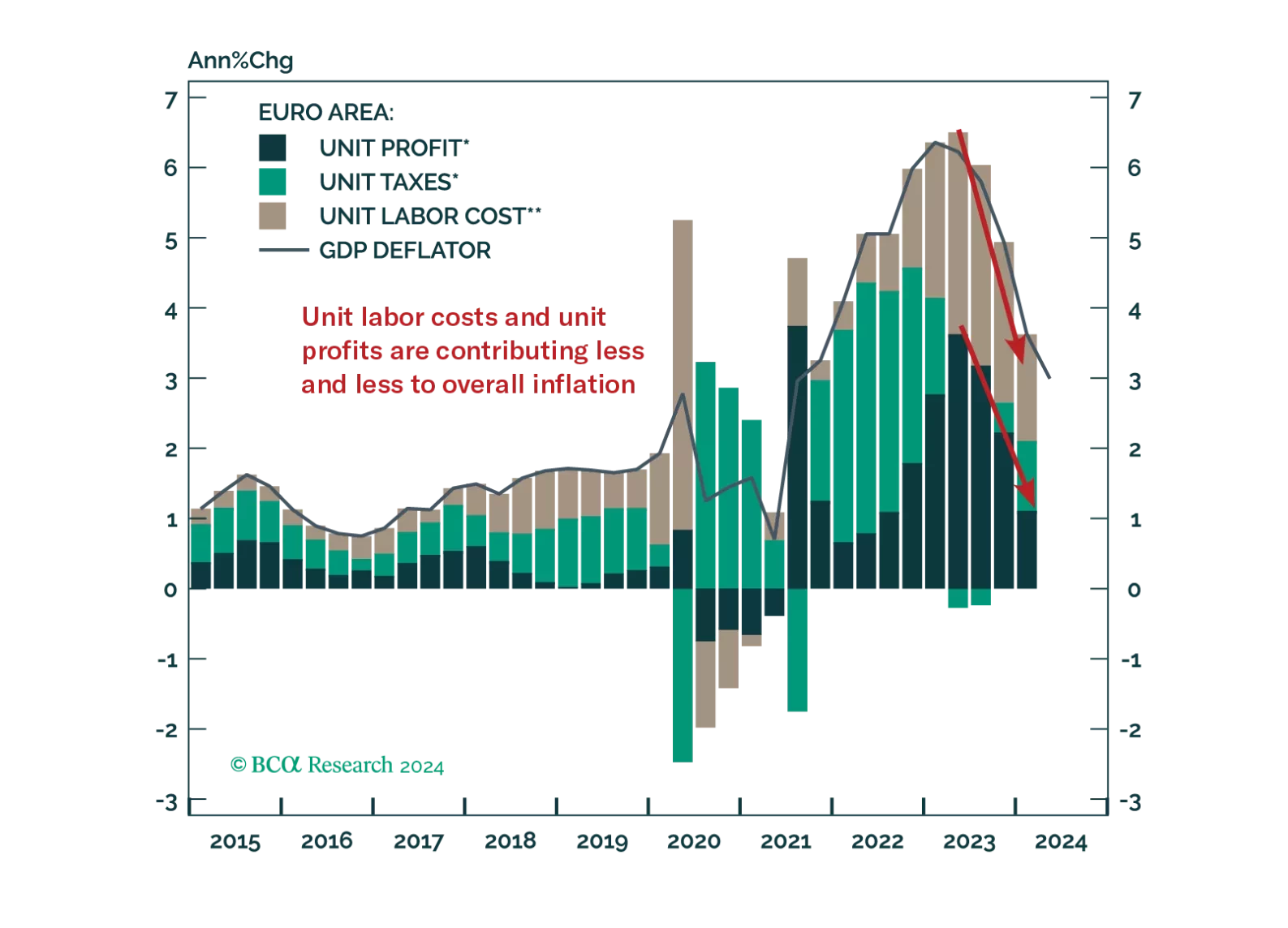

The ECB will cut rates once more this year; however, markets underprice how far it will ease next year.

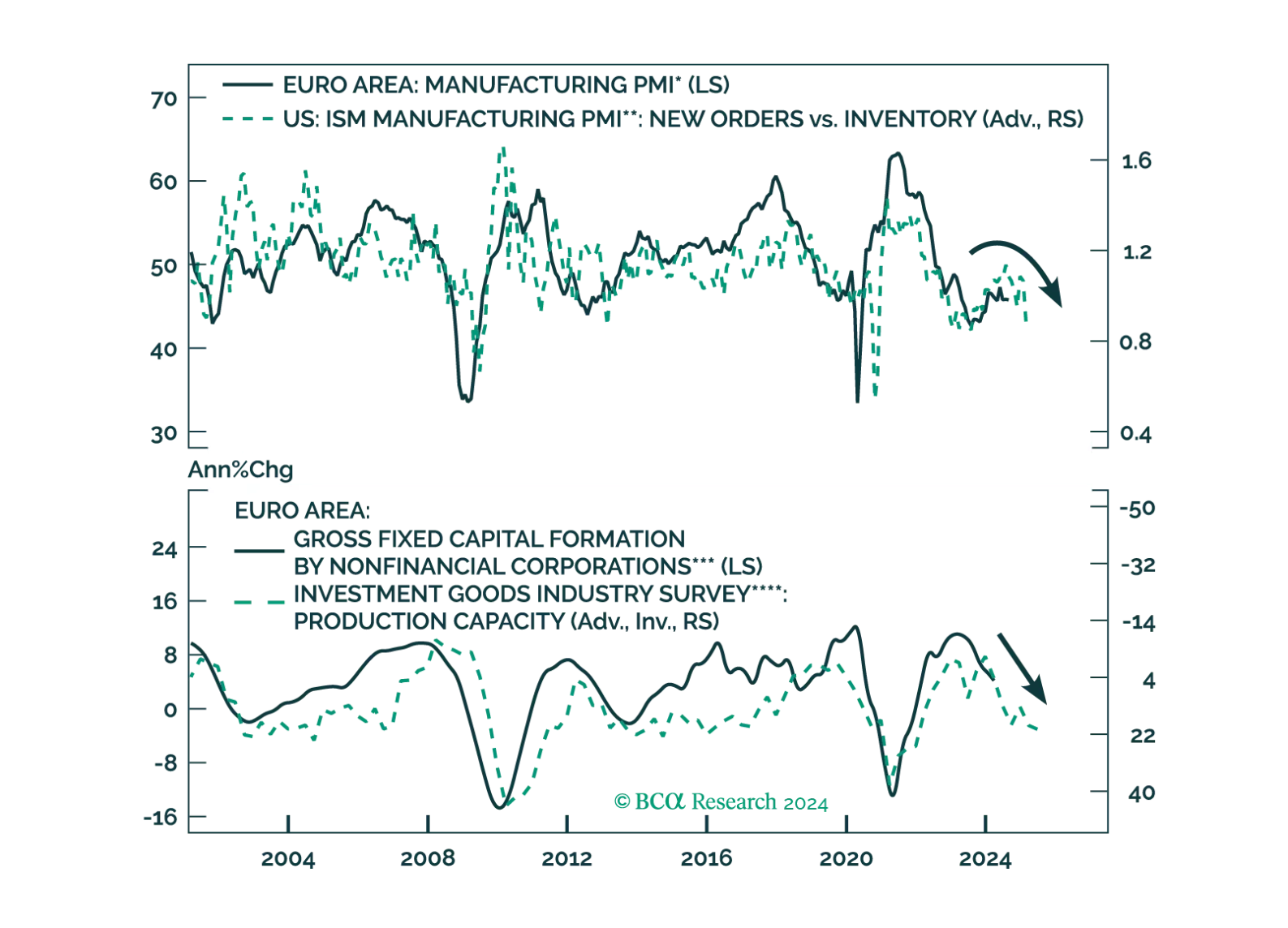

Crucial leading indicators of the global and European economies continue to deteriorate. How should investors position their European portfolios to benefit from these trends?

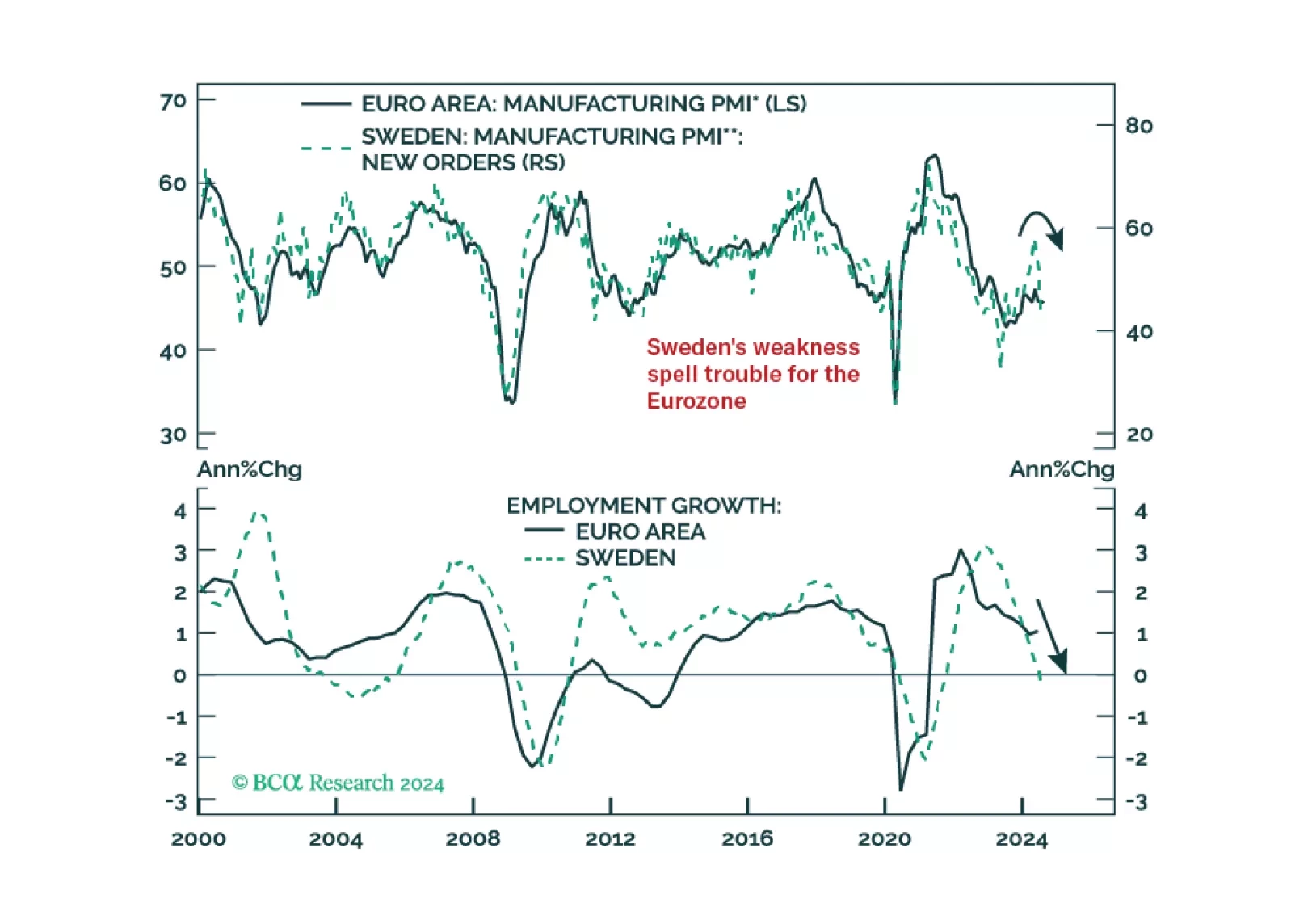

Our negative stance on European growth and assets is not devoid of risks. To gauge whether these risks warrant upgrading our growth outlook, we monitor Sweden closely. So, what is the current message from this Nordic economy?

In this Special Report, we assess the impact of monetary policy tightening on major economies. Interest rate sensitive GDP already slowed significantly in response to the aggressive rate hiking cycle. Despite the beginning of policy easing, our forward-looking indicators suggest monetary policy will continue to weigh on the economy.