Euro Area

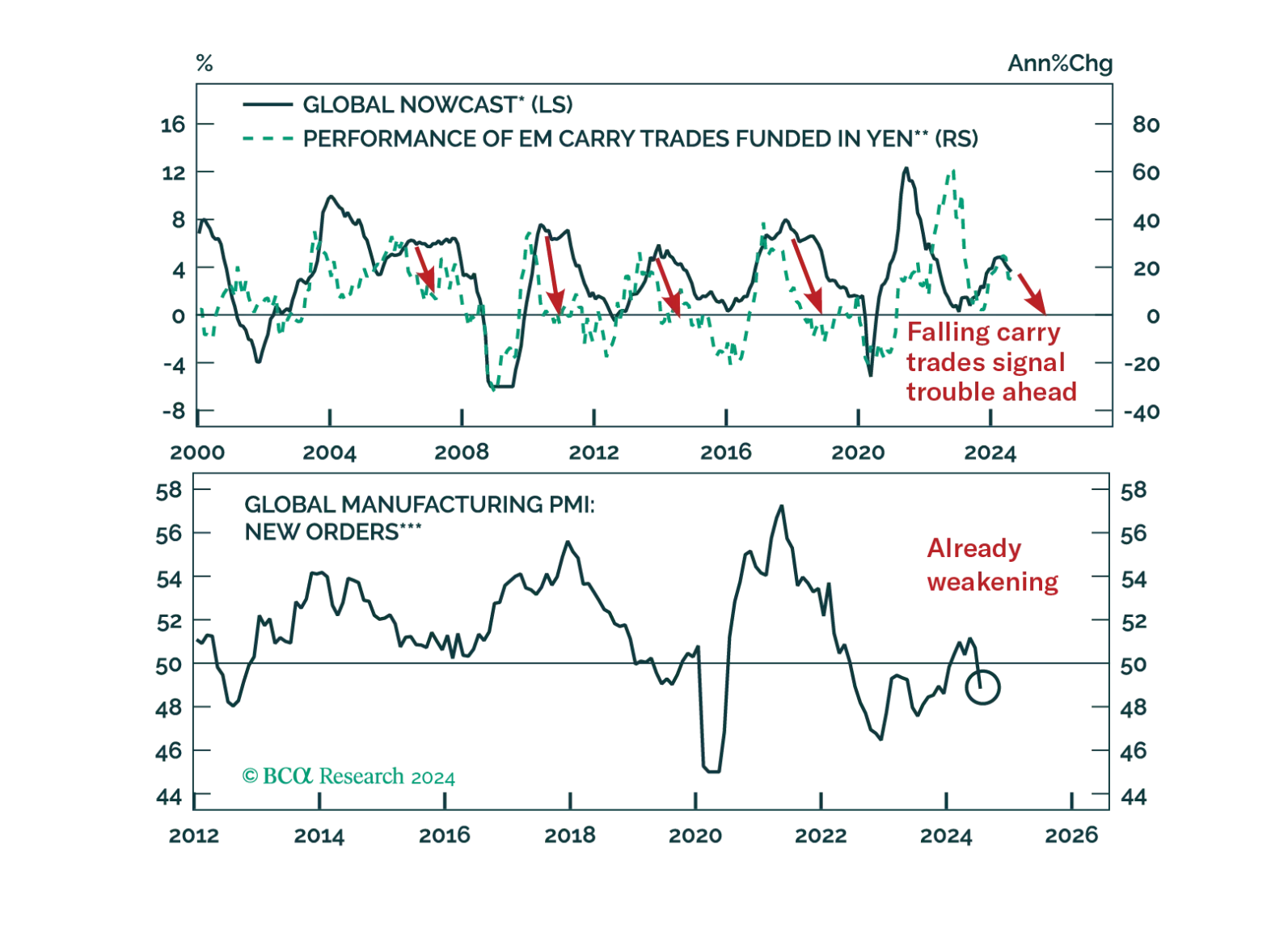

According to BCA Research’s European Investment Strategy service, investors should fade the rebound in European equities and bond yields as the euro is also at risk. Last week’s bounce in global equities is temporary. The pause in the carry trades unwound,…

The unwind of yen carry trades caused violent tremors across the globe. Was this shock a one-off event or the prelude to more troubles?

German Industrial production and factory orders continued their slump in June. The usual powerhouse of the Euro Area economy has been trailing its peers throughout 2024. While both industrial production and factory orders surprised to the upside in June,…

After briefly breaking a 27-month streak of negative sentiment back in June, the Eurozone Sentix Economic index disappointed in August. The overall index worsened from July’s negative reading to -13.9, below expectations of a milder deterioration. The…

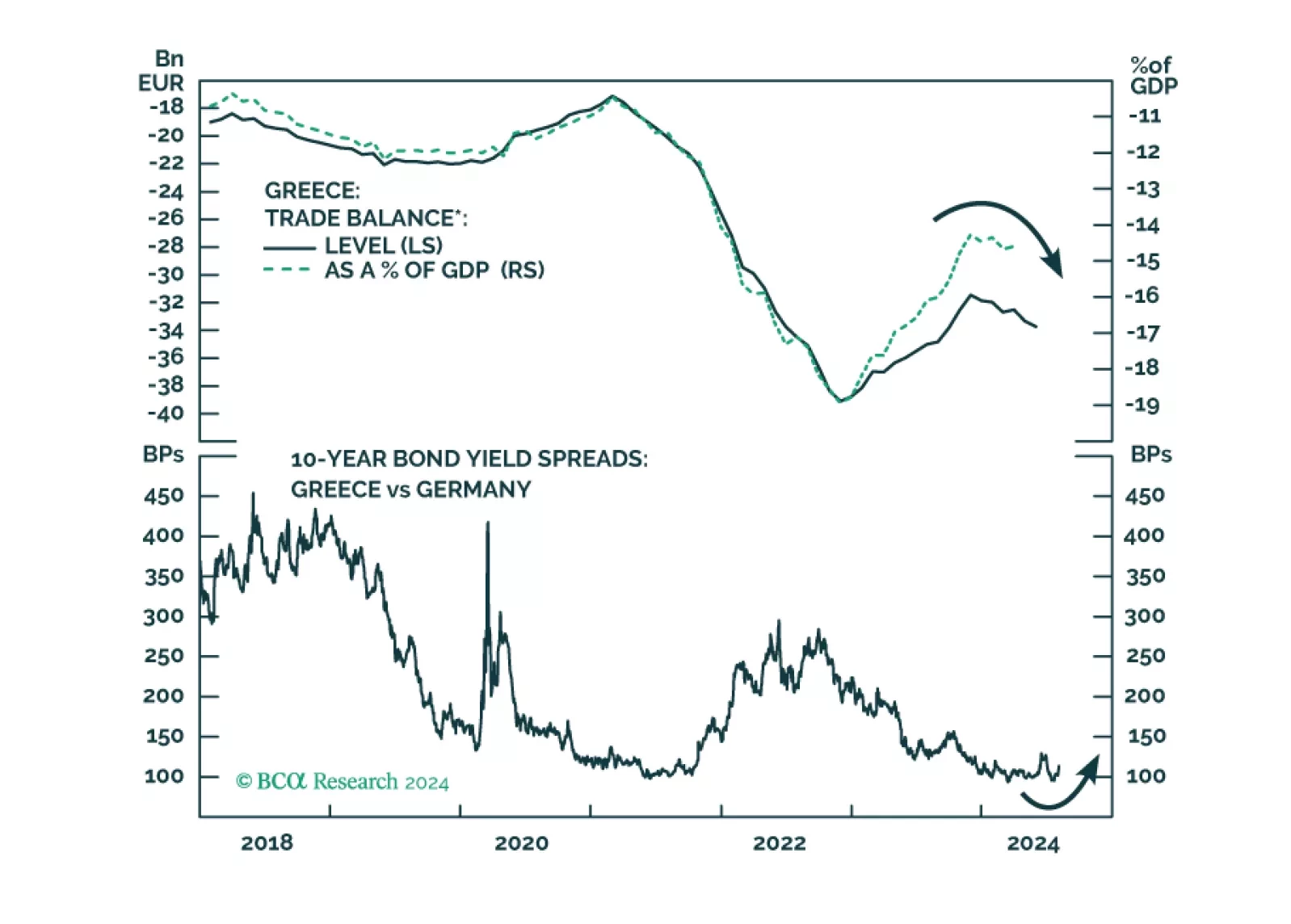

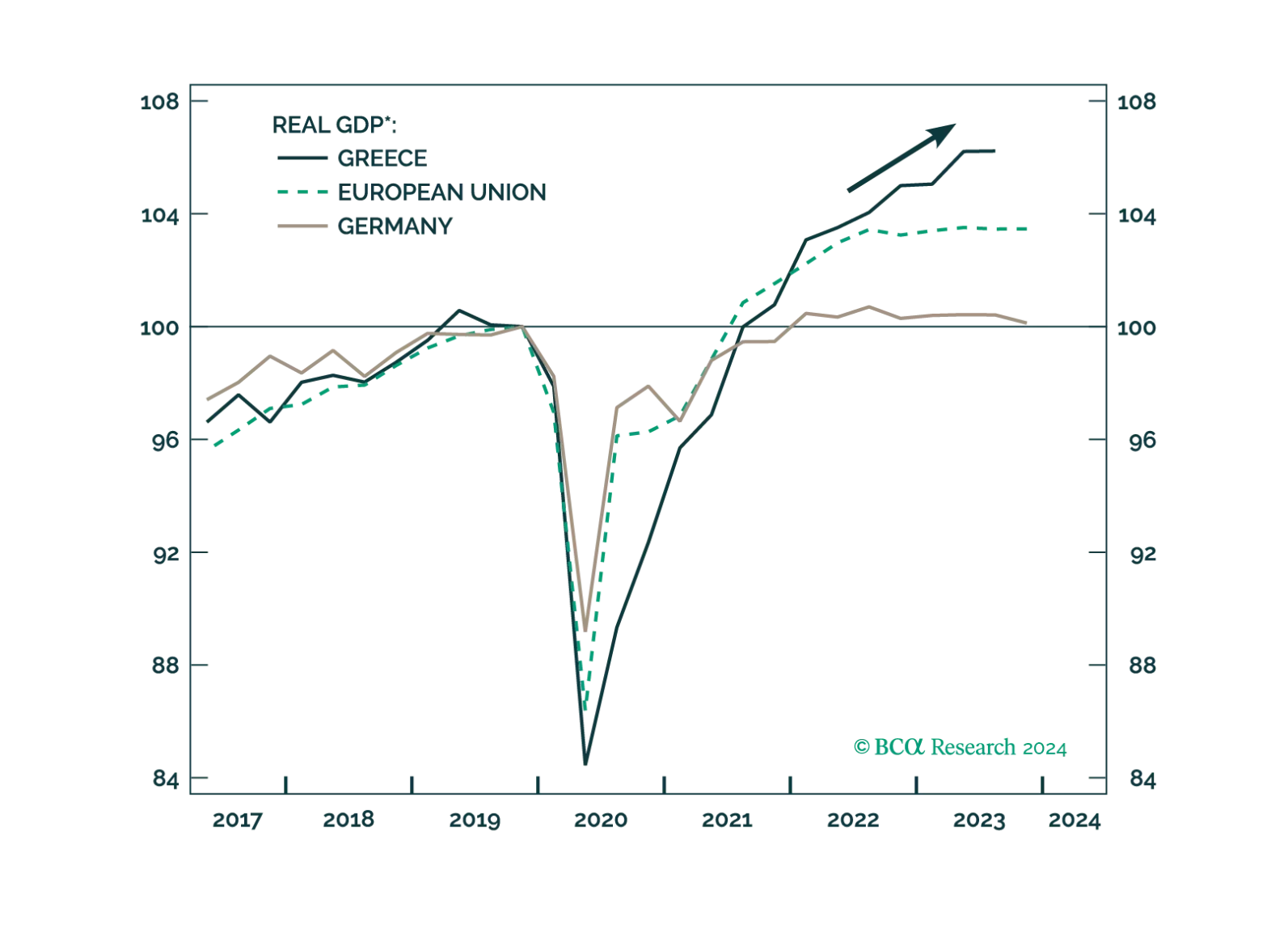

Absolute return investors should be tactically cautious on Greek assets. Dedicated EM equity portfolios, however, should overweight Greek stocks.

Greece has staged a surprising economic recovery in recent years. Greek risk assets are the best performers in Europe. Can it last?

Eurozone GDP surprised to the upside in Q2, growing by 0.3% q/q annualized against expectations of 0.2%. Stronger-than-expected expansions in France (0.3% q/q vs 0.2%) and Spain (0.8% q/q vs 0.5%), as well as steady growth in Italy (0.2% q/q), offset a…

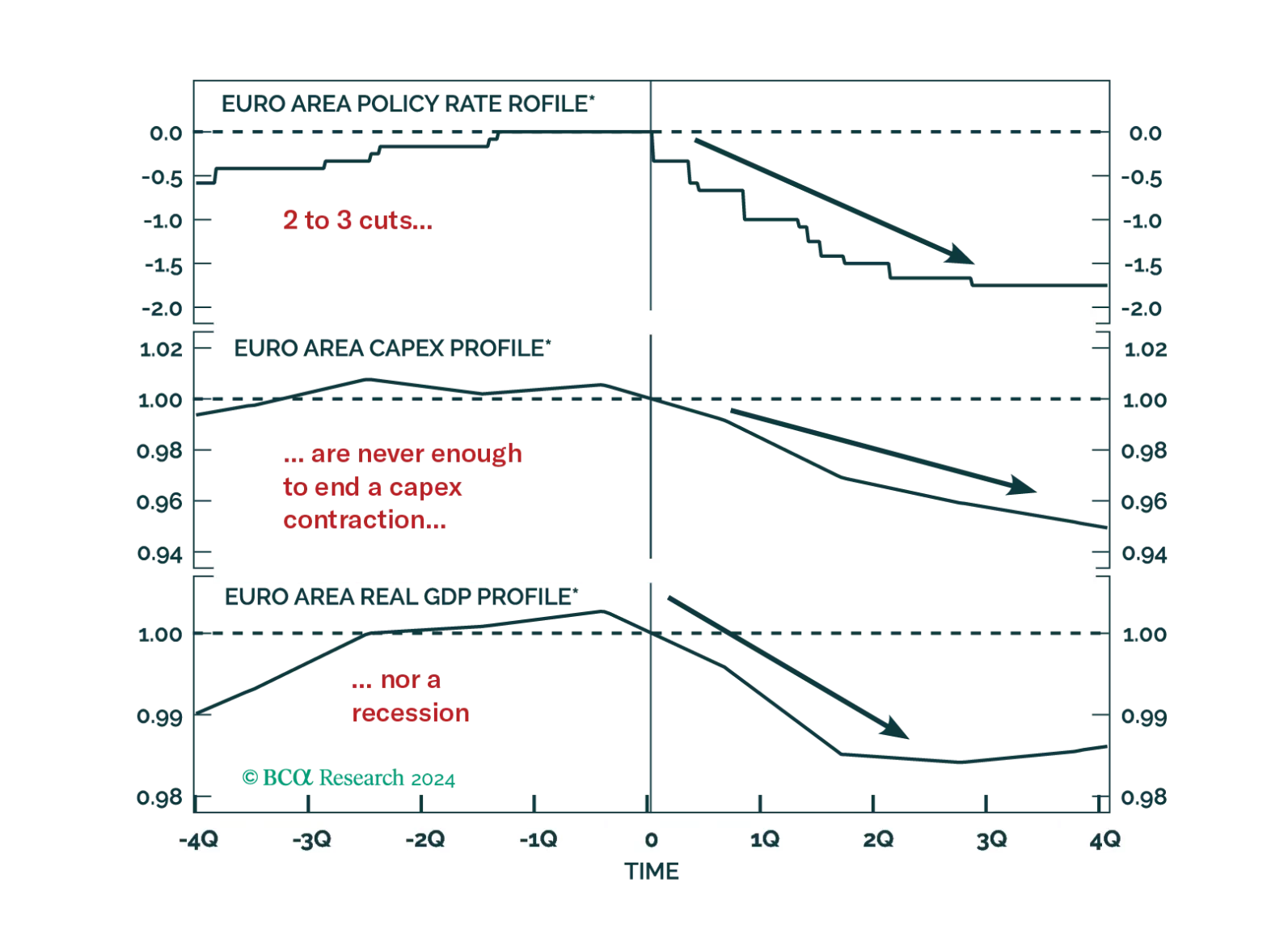

According to BCA Research’s European Investment Strategy service, a foreign shock is likely to tip the Eurozone economy into a recession because important vulnerabilities have emerged domestically. Policy is restrictive. Real interest rates stand 370bps…

Investors hope that the ECB rate cuts priced into the curve will be sufficient to achieve a soft landing in Europe. History argues against this view, but will this time be different?

We assign high odds that the US will tip into a recession by year-end or early 2025. Given it has been the largest driver of global demand in this cycle, a US recession will morph into a global downturn. The procyclical Eurozone economy is particularly…