Euro Area

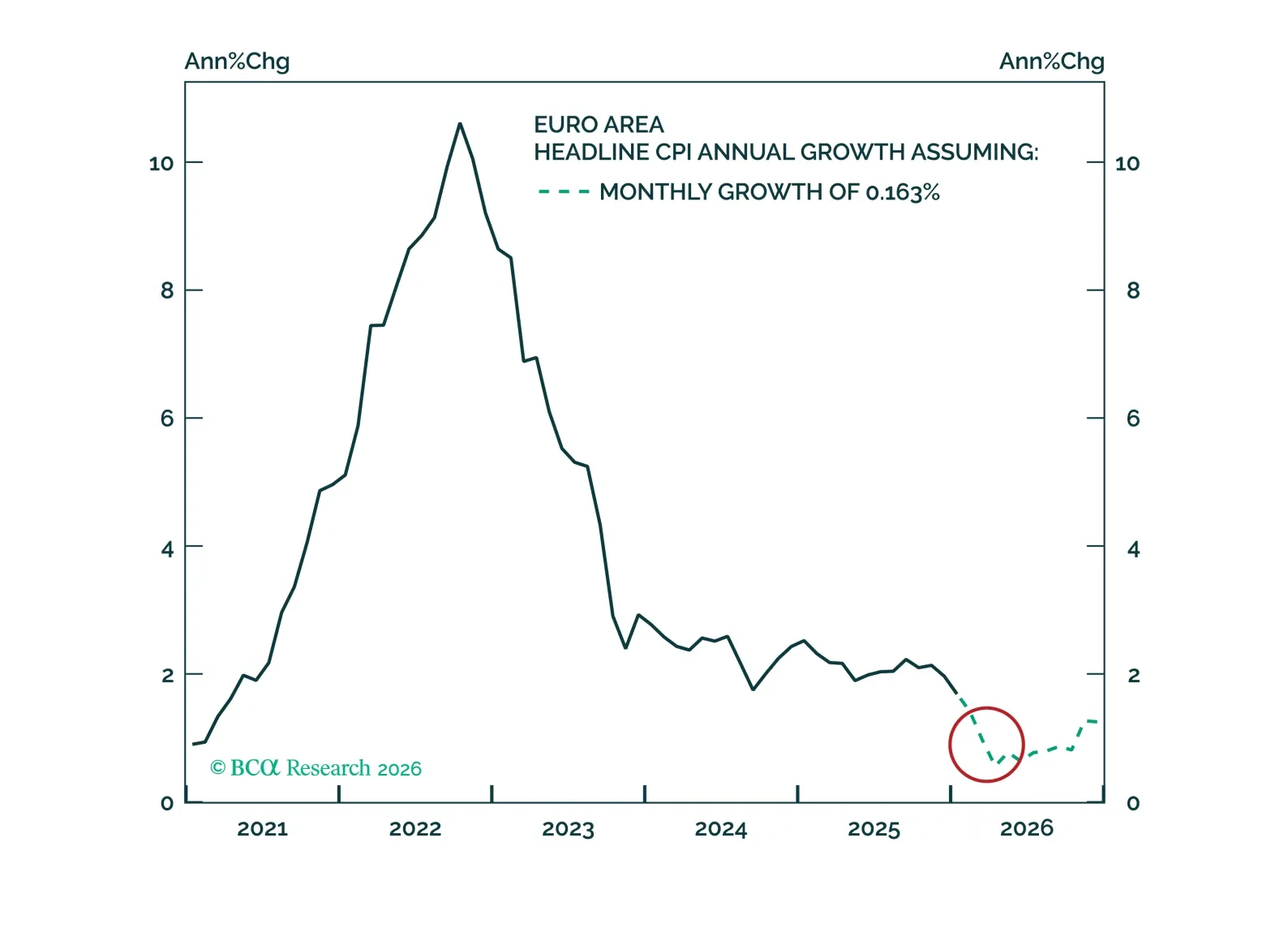

The ECB is about to make its first policy mistake in the current cycle by being complacent about the downside risks to inflation. The confluence of base effects, a stronger euro, food and energy deflation, and rapid services disinflation will push headline inflation closer to 1% in the first half of the year. This significant undershoot will force the ECB to deliver reflationary cuts. Go long the September 2026 3-month Euribor futures and tactically reduce exposure to inflation-linked bonds in the Eurozone.

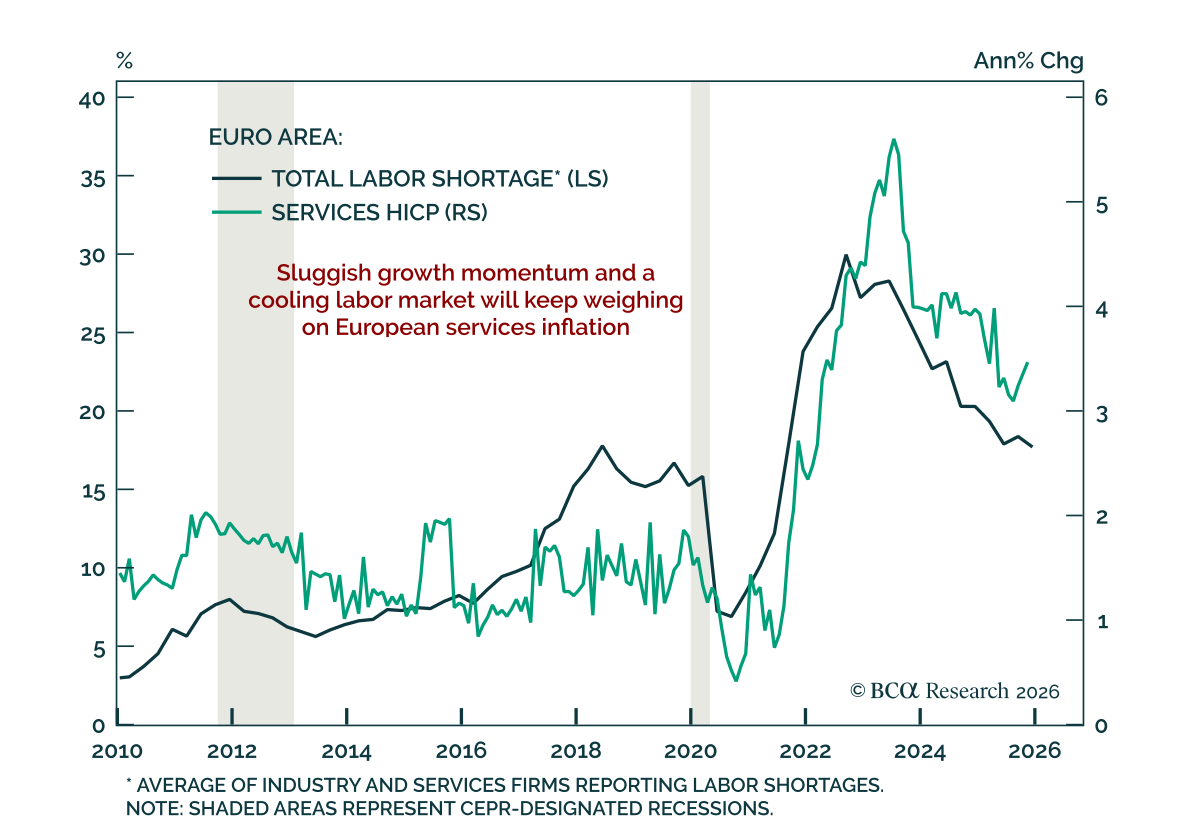

Euro area January flash HICP inflation cooled in line with expectations; mixed sentiment and limited growth momentum leave scope for insurance cuts by the ECB later this year. Euro area January flash HICP inflation was roughly in line with estimates and…

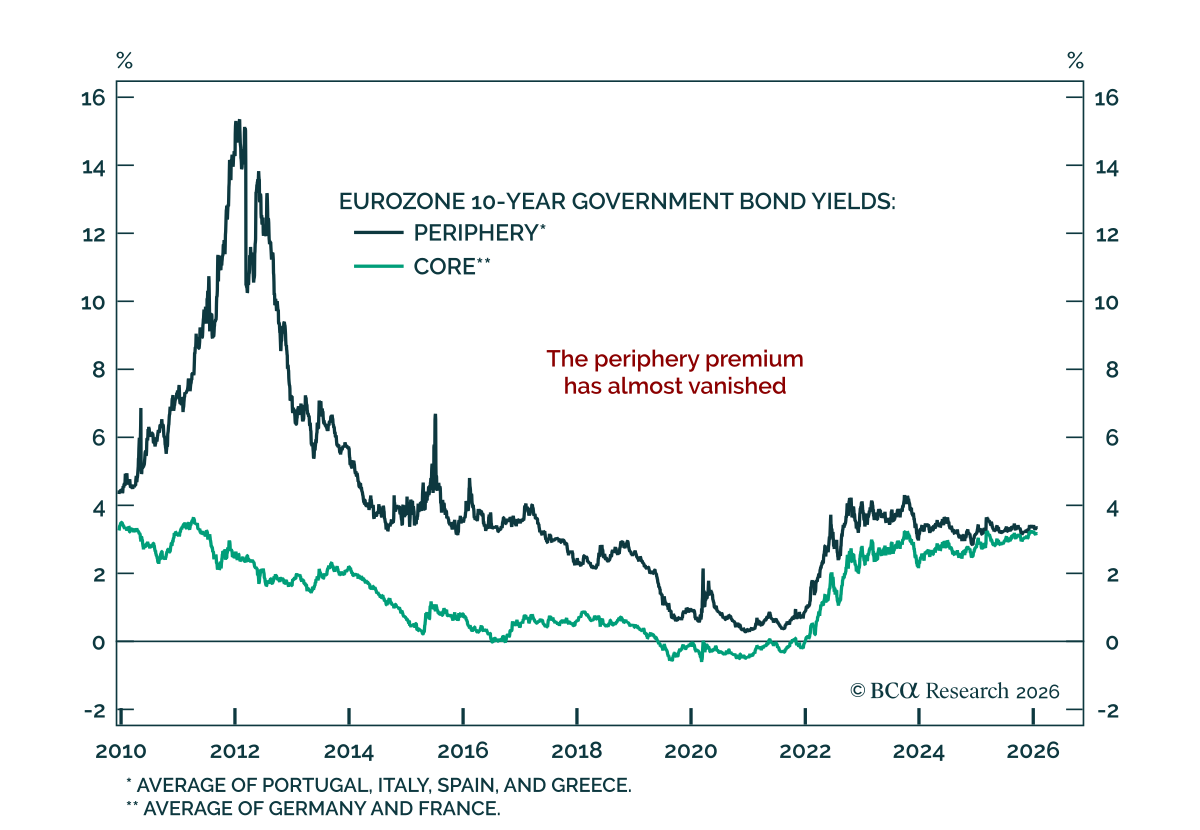

Peripheral Europe is driving the region’s resilience, and finally closing the gap with the core. Our Chart Of The Week comes from Jeremie Peloso, Chief European Investment Strategist. The resilience of the European economy and strong equity performance in…

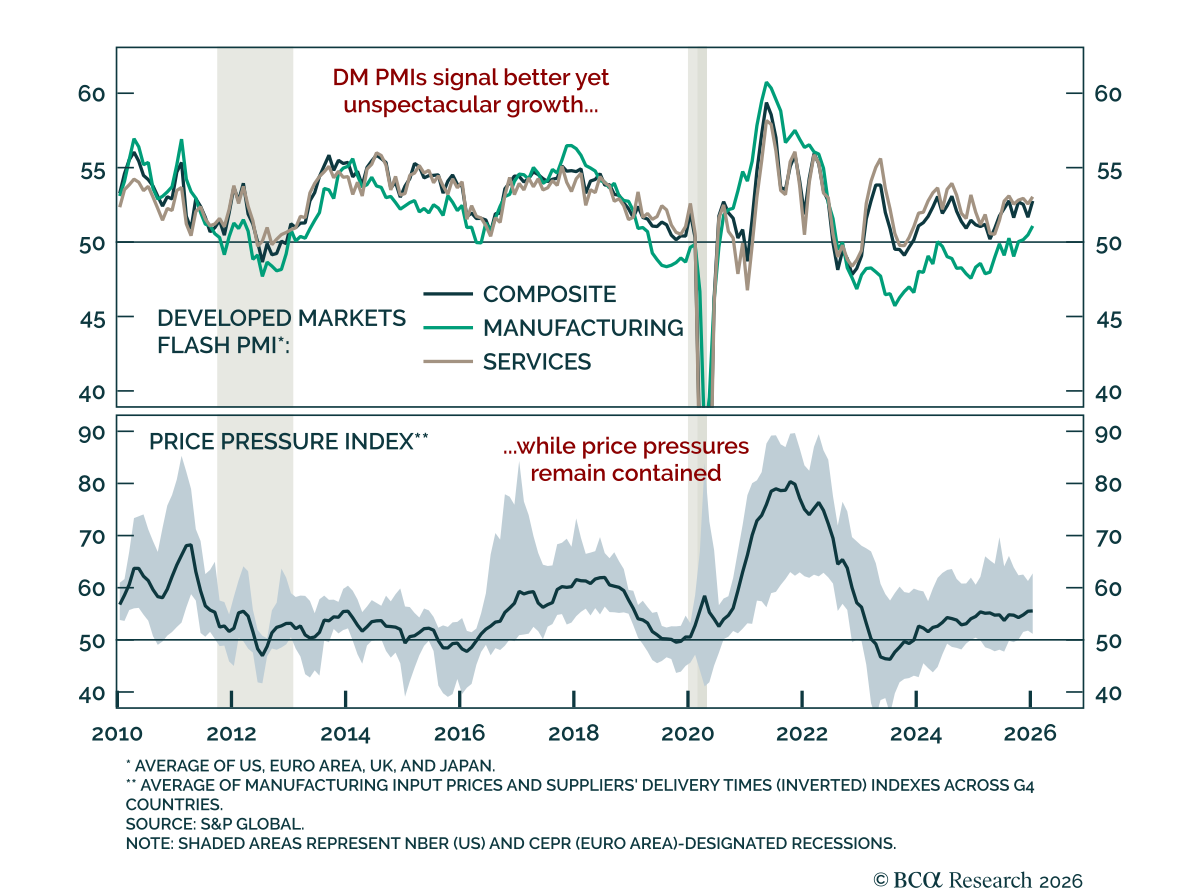

January flash PMIs point to better, though unspectacular, global growth momentum. Developed markets PMIs showed improvement in global growth momentum. PMIs have largely moved sideways through 2025, with manufacturing now recovering after trade uncertainty and…

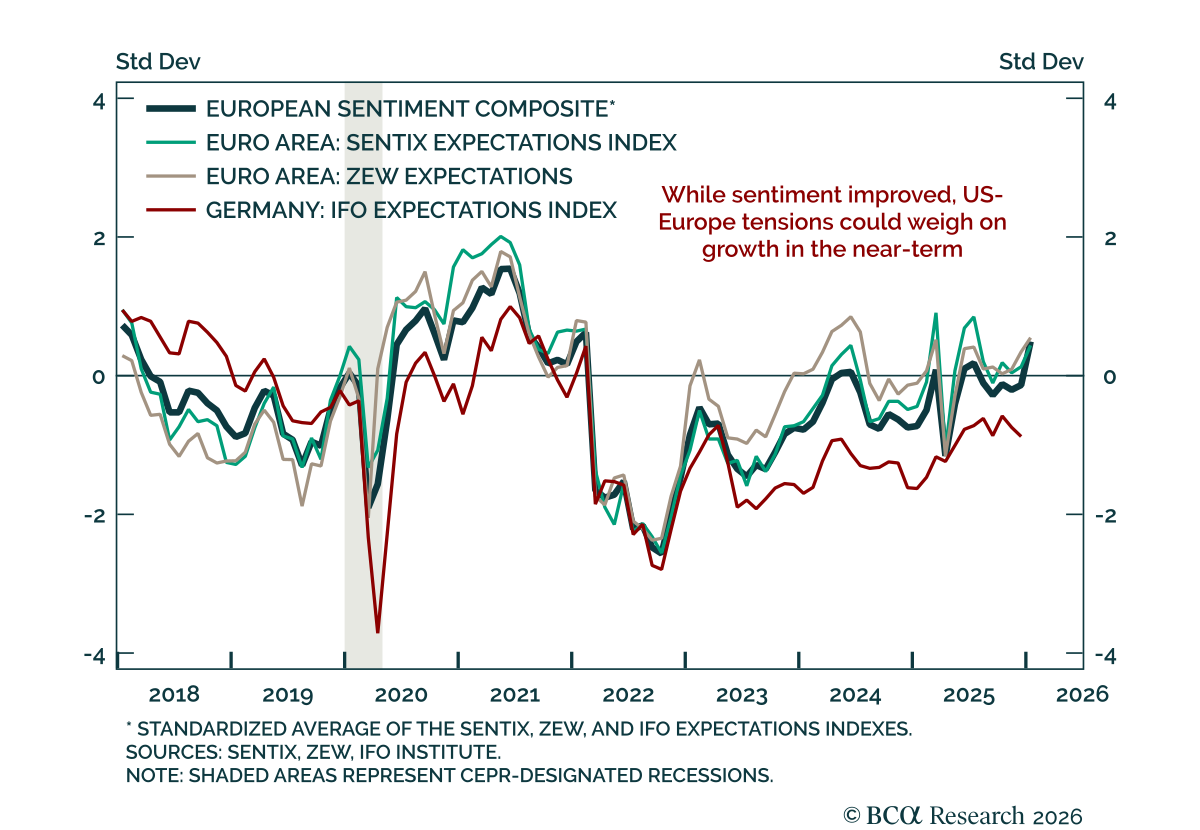

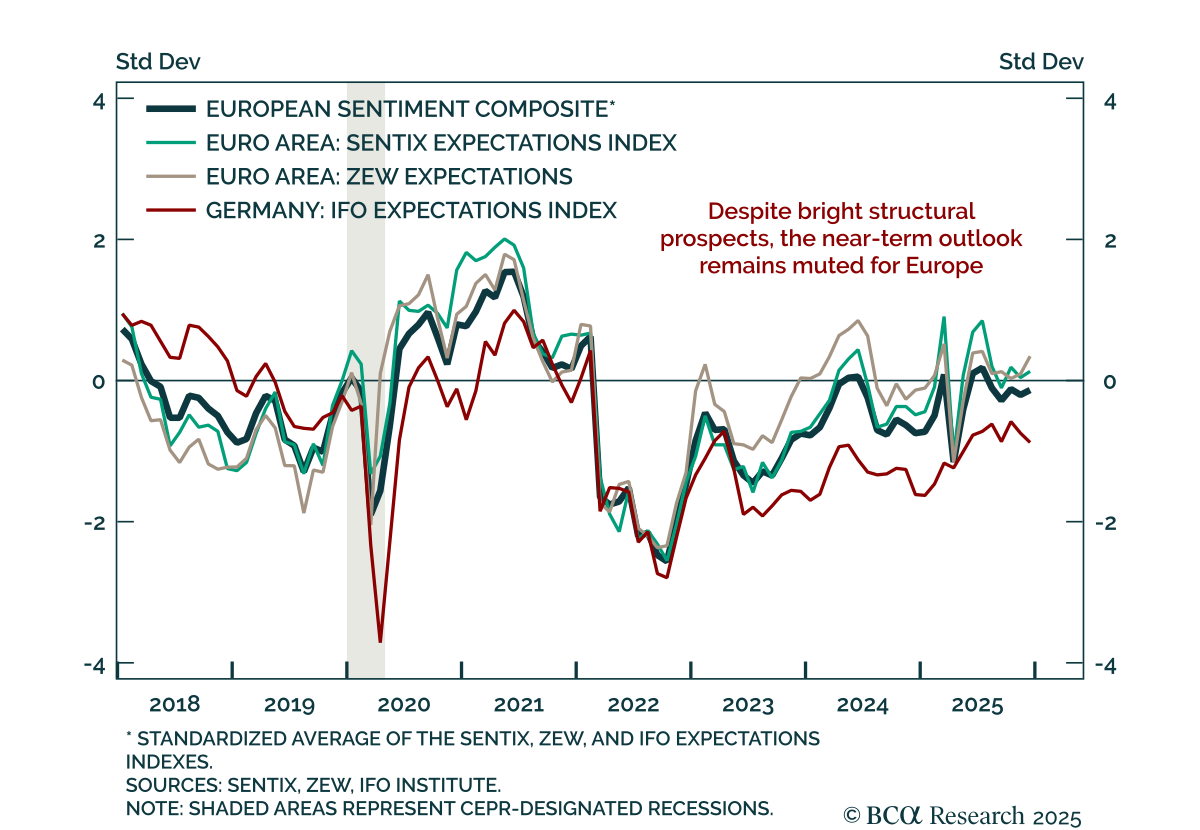

January Euro area sentiment improved, but growth momentum remains limited as tensions with the US rise and reflationary ECB cuts remain possible. January sentiment brightened in the Euro area. The ZEW survey beat expectations for Germany, with both current…

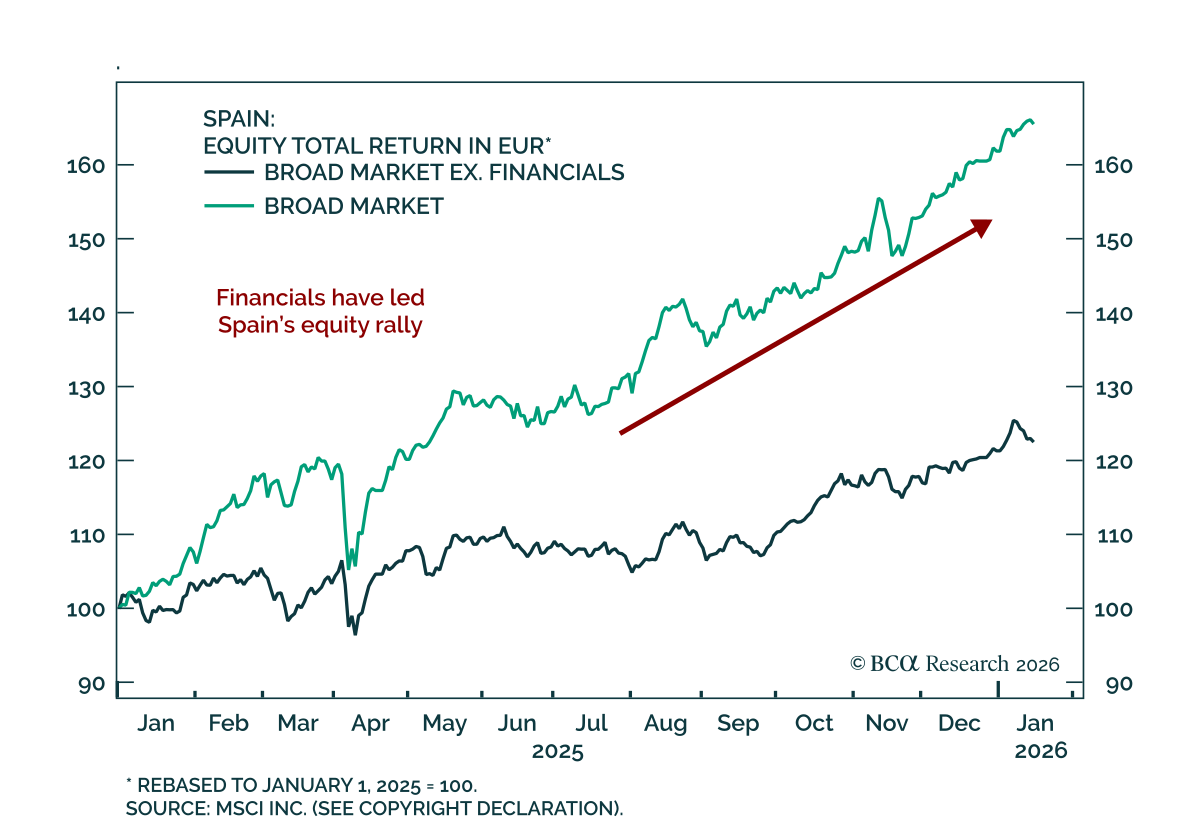

Our GeoMacro and European strategists highlight Spain’s equity and bond outperformance as fundamentally driven, supported by improving balance sheets, stronger profitability, and repeated earnings upgrades. Financials have led the equity rally, which reflects…

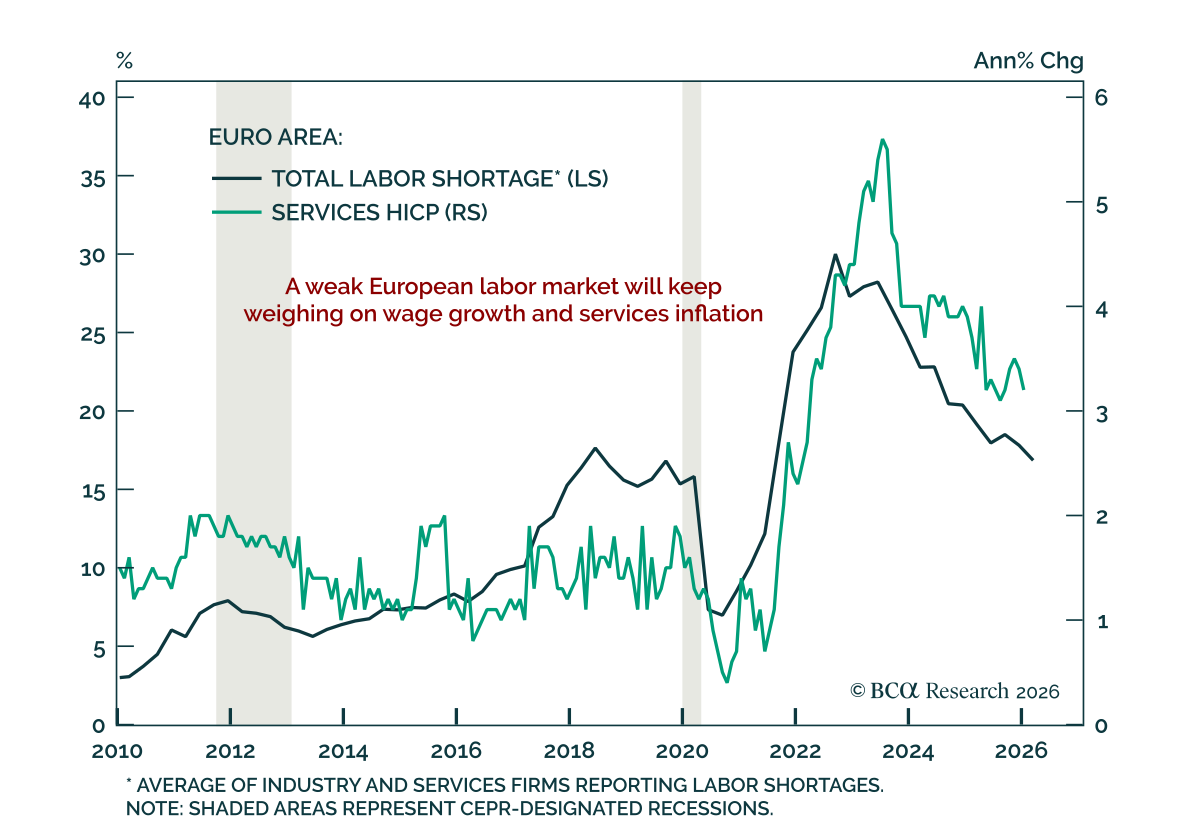

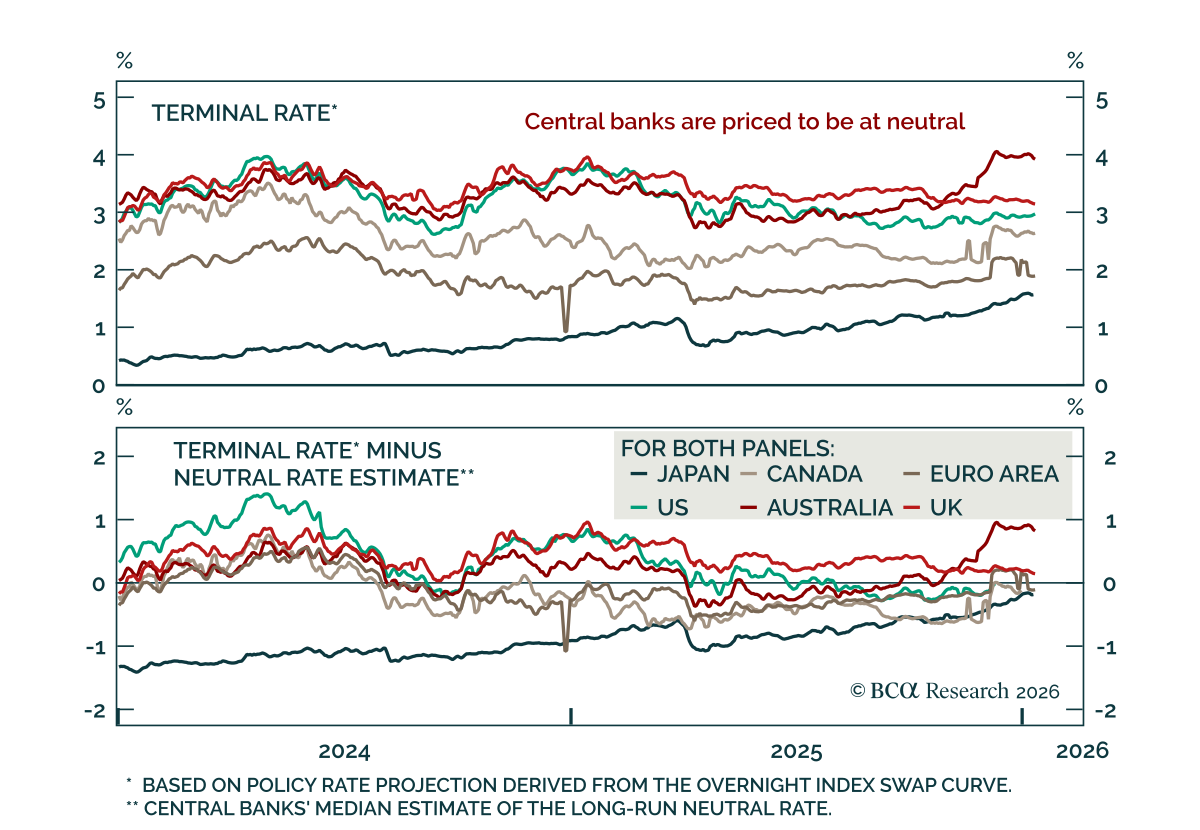

Our Global Fixed Income strategists maintain an above-benchmark duration stance as labor market risks continue to support downside yield potential, even as the global easing cycle winds down. With policy normalization largely complete, monetary policy is…

Remain tactically cautious on European assets as persistently weak sentiment keeps growth momentum subdued. European economic sentiment remains soft with little sign of acceleration. The European Commission’s Economic Sentiment Index missed expectations in…

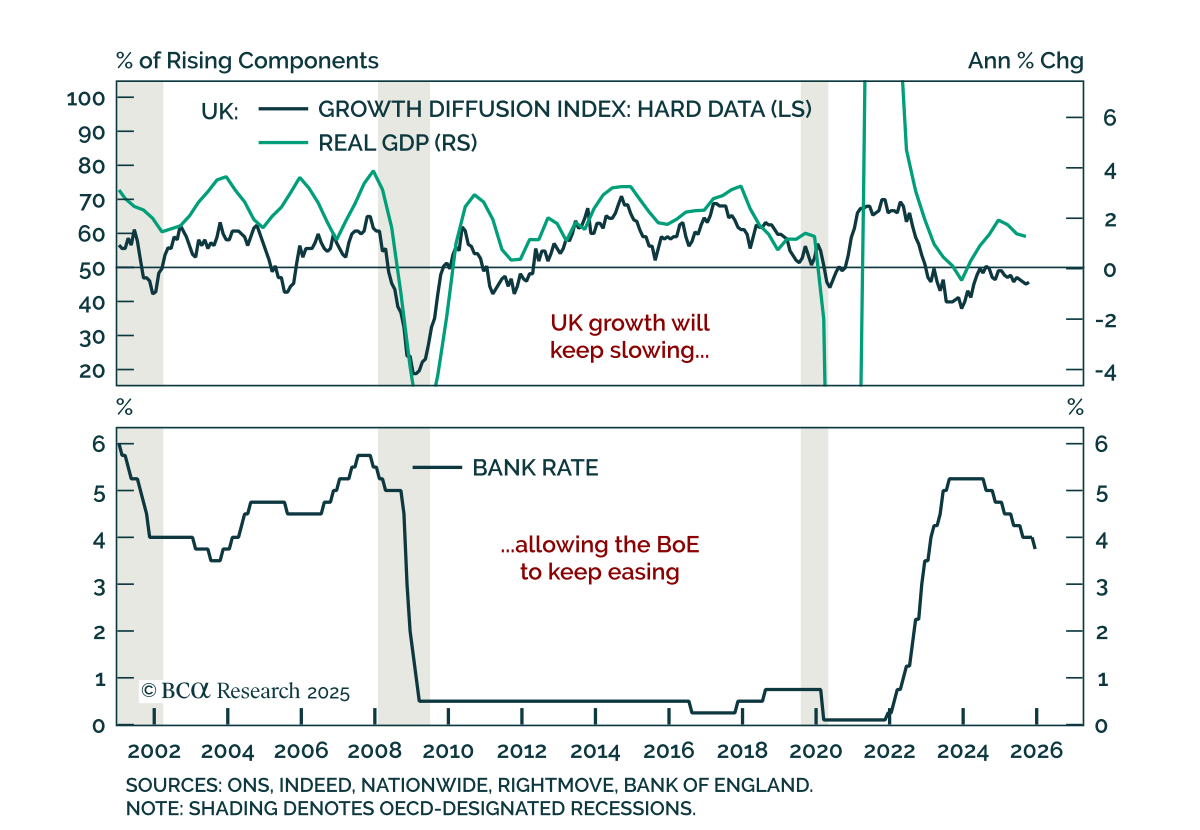

Stay long September 2026 Euribor futures and overweight UK gilts, as Europe could see reflationary cuts while the UK slowdown argues for deeper easing. The ECB left rates unchanged at 2% in a routine meeting and revised its growth and inflation forecasts…

Remain tactically cautious on European assets as sentiment stays mixed and leading indicators show no acceleration. Euro area sentiment data for December continued to send conflicting signals. The Sentix index slightly beat expectations, improving to -6.2…