Euro Area

European assets are selling off as investors panic about the upcoming French election. Is this panic justified, and if so, for how long?

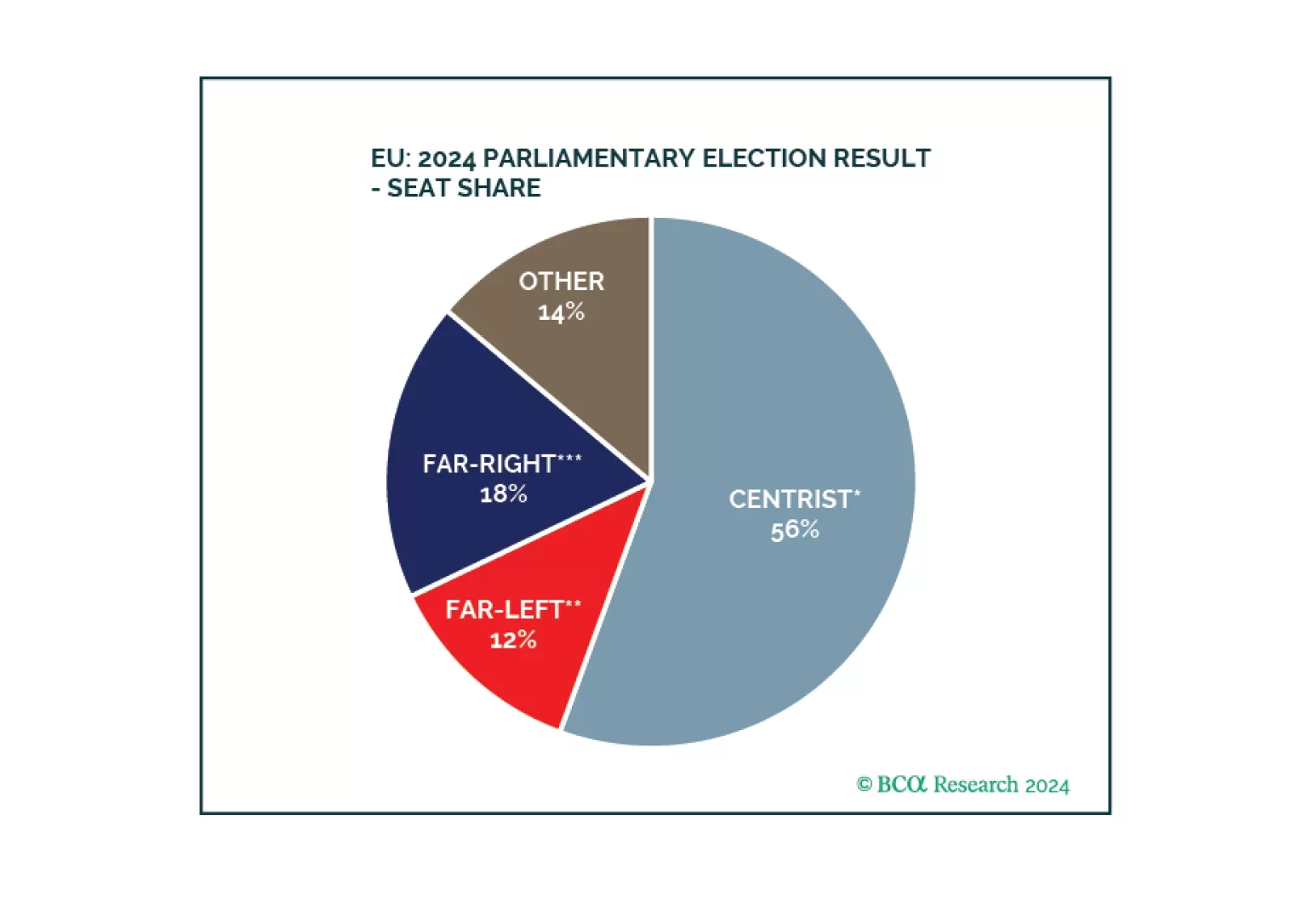

Europe did not witness a major policy reversal. Inflationary pressures are coming down, enabling the ECB to cut rates and European states to maintain soft budgets. Geopolitical challenges ensure that European parties continue to cooperate on national defense, economic security, and energy security.

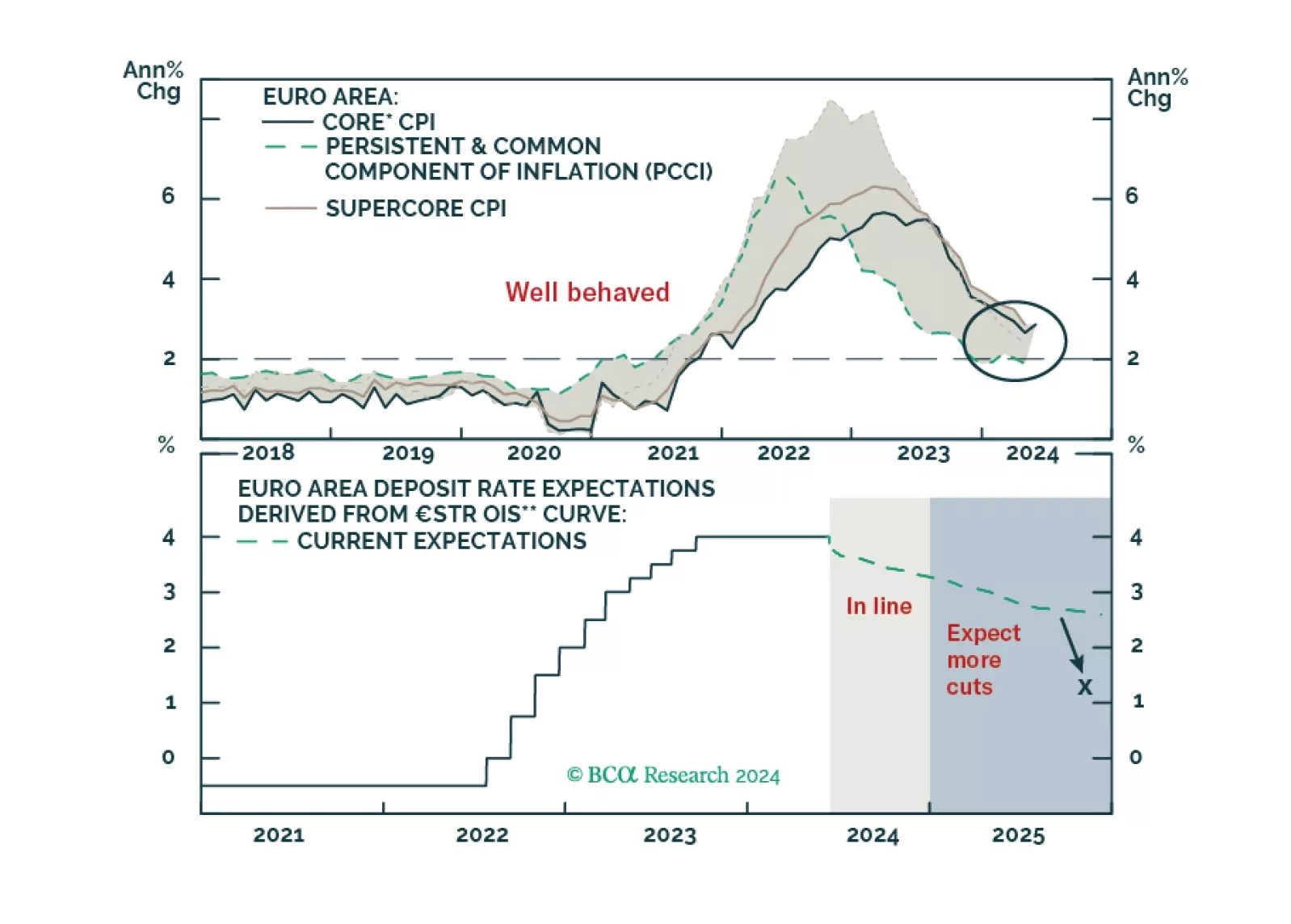

The ECB is now firmly in easing mode, even if it refuses to pre-commit to a specific rate path. What does this data dependency mean for the euro and European yields?

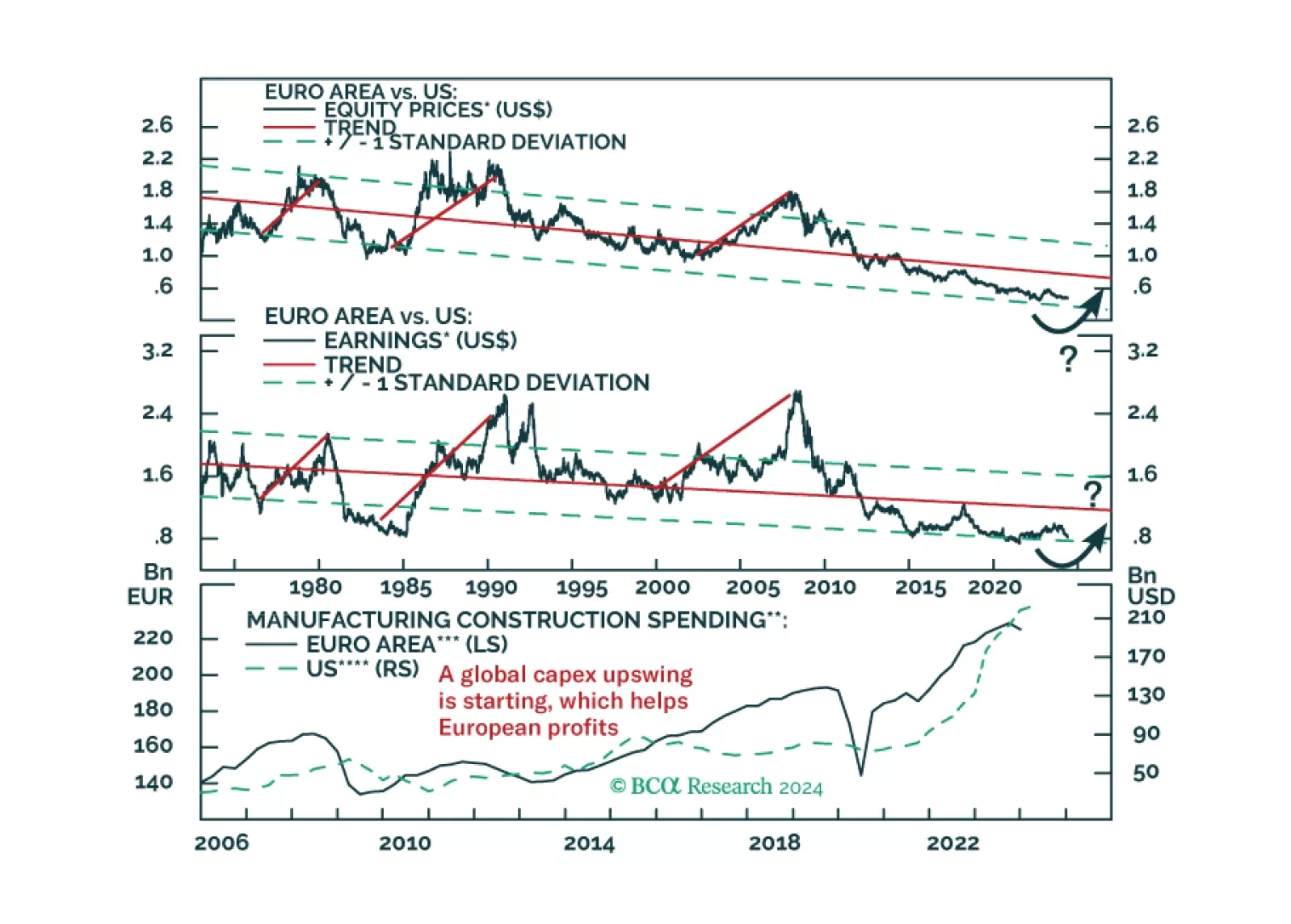

European stocks have massively underperformed US ones since the GFC. Demographics and productivity say this trend will continue, but is that really so?