Euro Area

In Section I, we argue that global investors have been lulled into a false sense of security concerning the resiliency of the US economy. Tight monetary policy means that something must change for a recession to be avoided, and developed market rates cuts will likely be too modest and come too late to save the day. Nimble investors or those highly sensitive to tracking error should not be underweight stocks over the coming 3-6 months. Over a 6-12 month time horizon, we continue to recommend that investors remain underweight global equities versus US$-hedged long-maturity developed market government bonds. Section II is a guest report written by Martin Barnes, BCA’s former Chief Economist. Martin revisits the idea of the Debt Supercycle and discusses how its true end may emerge in response to a fiscal crisis in the US over the coming few years.

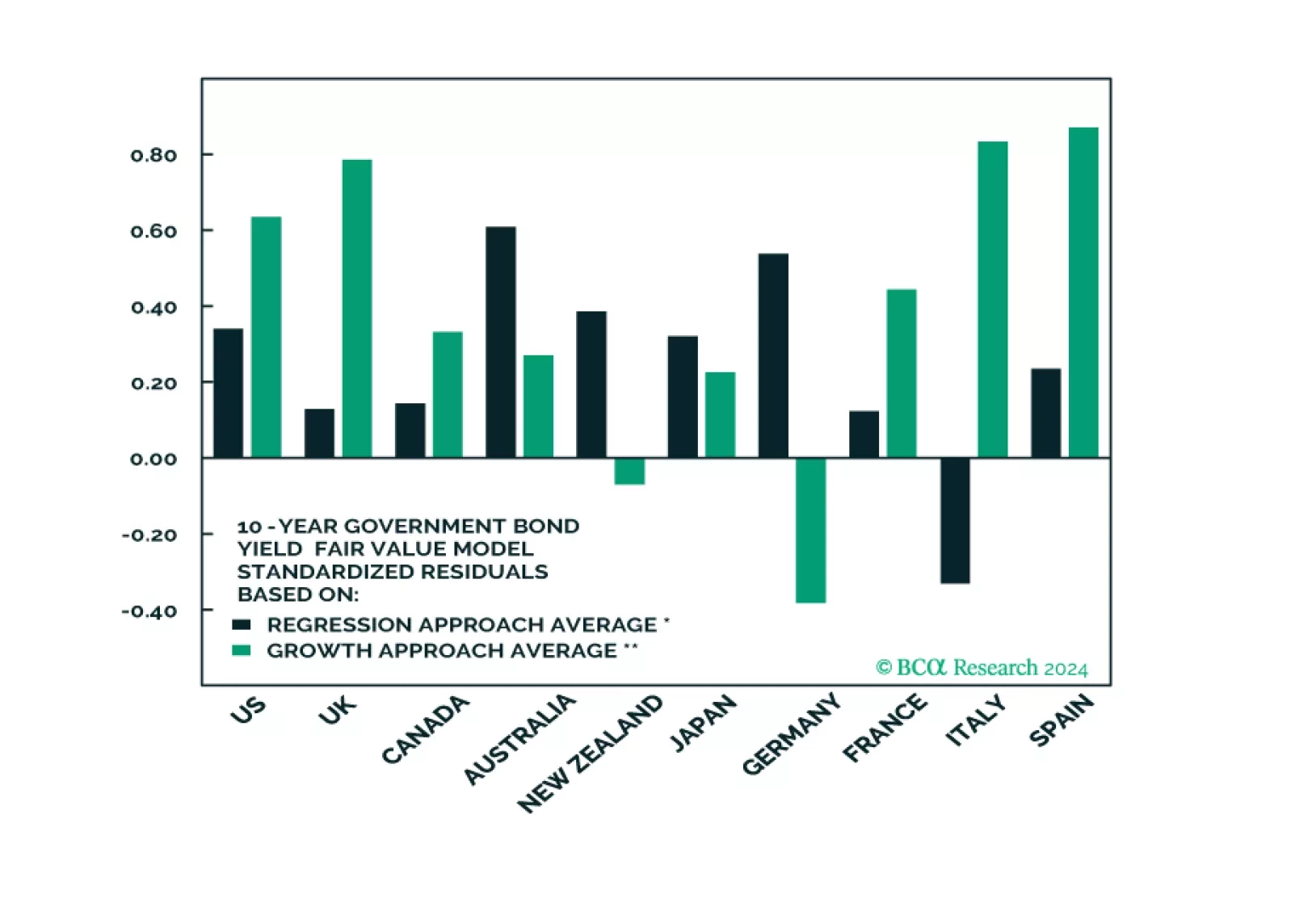

In this Special Report we assess the absolute and relative attractiveness of developed market government bonds using several fair value models. Longer-term investors who are focused on value should overweight US long-maturity bonds, and favor Spanish, Australian, and potentially UK government bonds within a DM ex-US allocation.

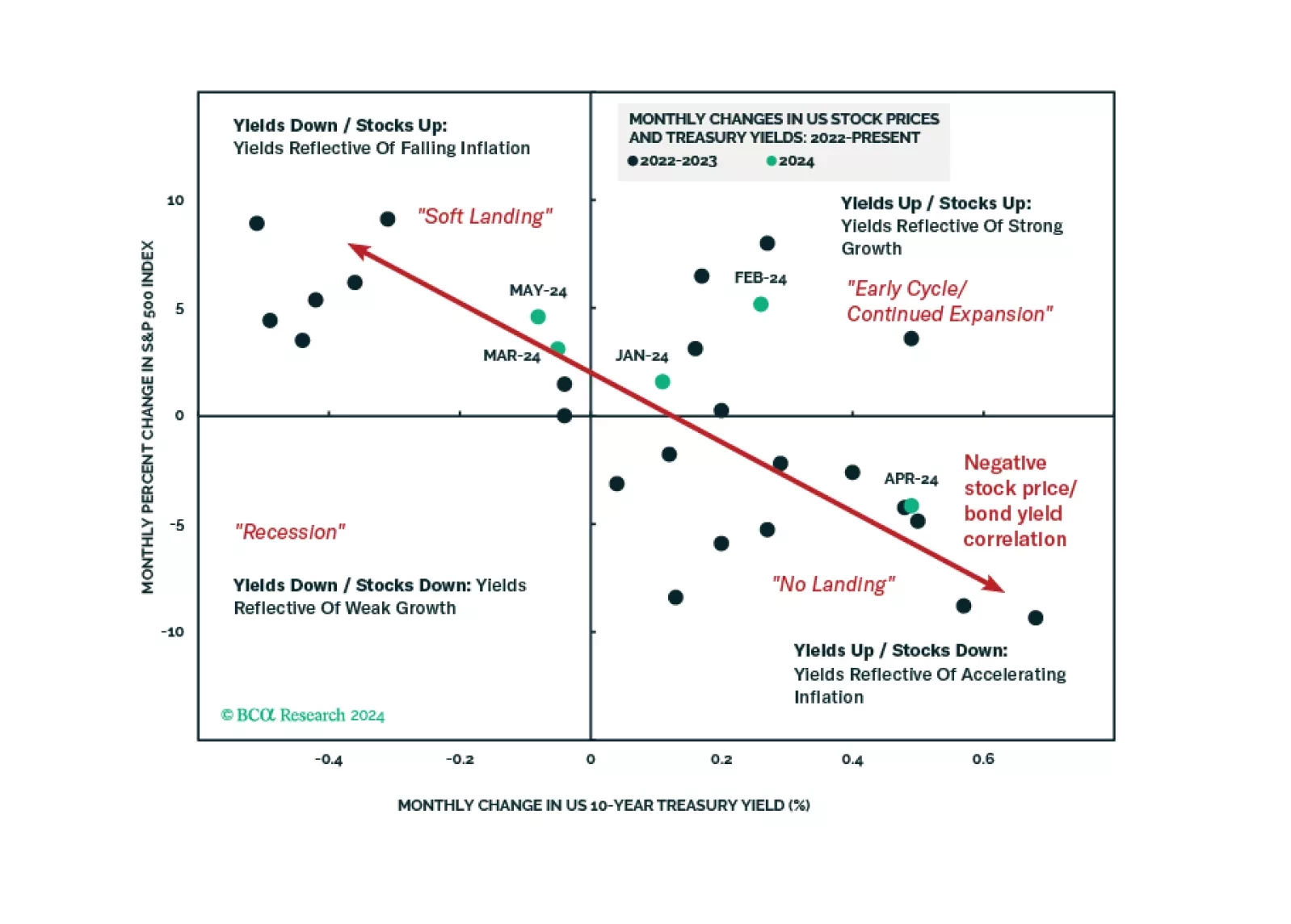

Looking at economic activity, global monetary policy seems restrictive, however, the behavior of financial markets tells a different story. What gives?

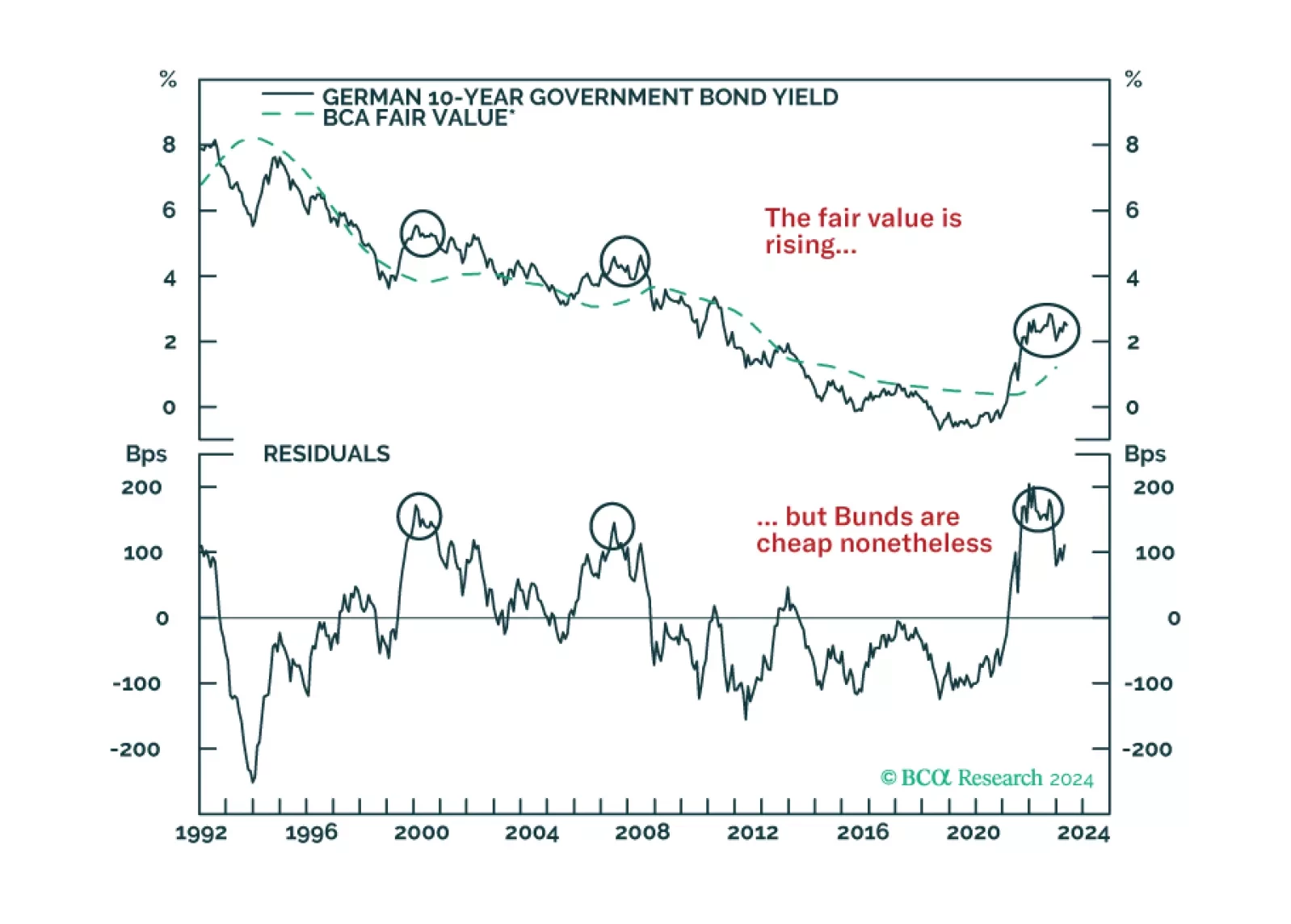

German Bunds have cheapened considerably, and the ECB is about to start cutting rates. Does this combination guarantee immediate profits from buying these bonds?