Euro Area

The resilience of the US economy has led economists to consistently revise up their consensus real GDP growth forecast for 2024, which now stands at 2.4%, up from 0.6% in July 2023. Conversely, the 2024 consensus Eurozone growth estimate has been trending…

Flash estimates for several European PMIs were released Tuesday. The results for manufacturing activity were somewhat disappointing. The German manufacturing PMI increased from 41.9 to 42.2, but underperformed expectations of 42.7. France’s manufacturing…

Euro Area small caps typically outperform large caps whenever the trade weighted euro appreciates and underperform whenever it depreciates. The rationale is simple. Most European large cap companies are large multinationals that export their products outside…

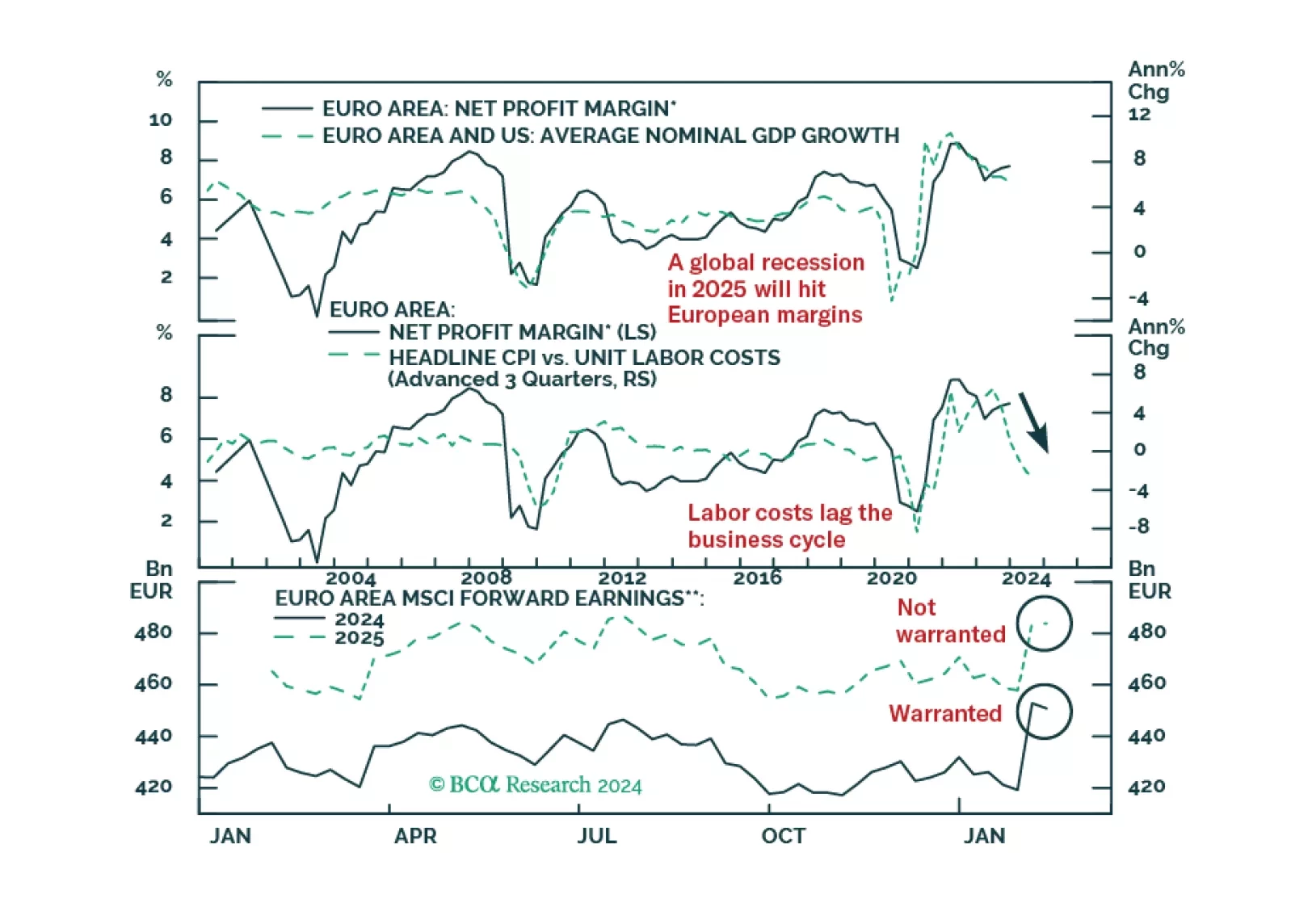

According to BCA Research's European Investment Strategy service, European profit margins have downside because they are both elevated and procyclical. European net margins stand at 7.7% above their long-term average of 5%. Analyst expectations…

European profits margins are elevated. Will a mild recession be enough to bring them down?

Optimism about the future continues to boost investor confidence in the Euro Area. The ZEW Expectations series for the Eurozone (+10.4 to 43.9) and Germany (+11.2 to 42.9) surged and are now both at their highest in 26 months. Although investors’…

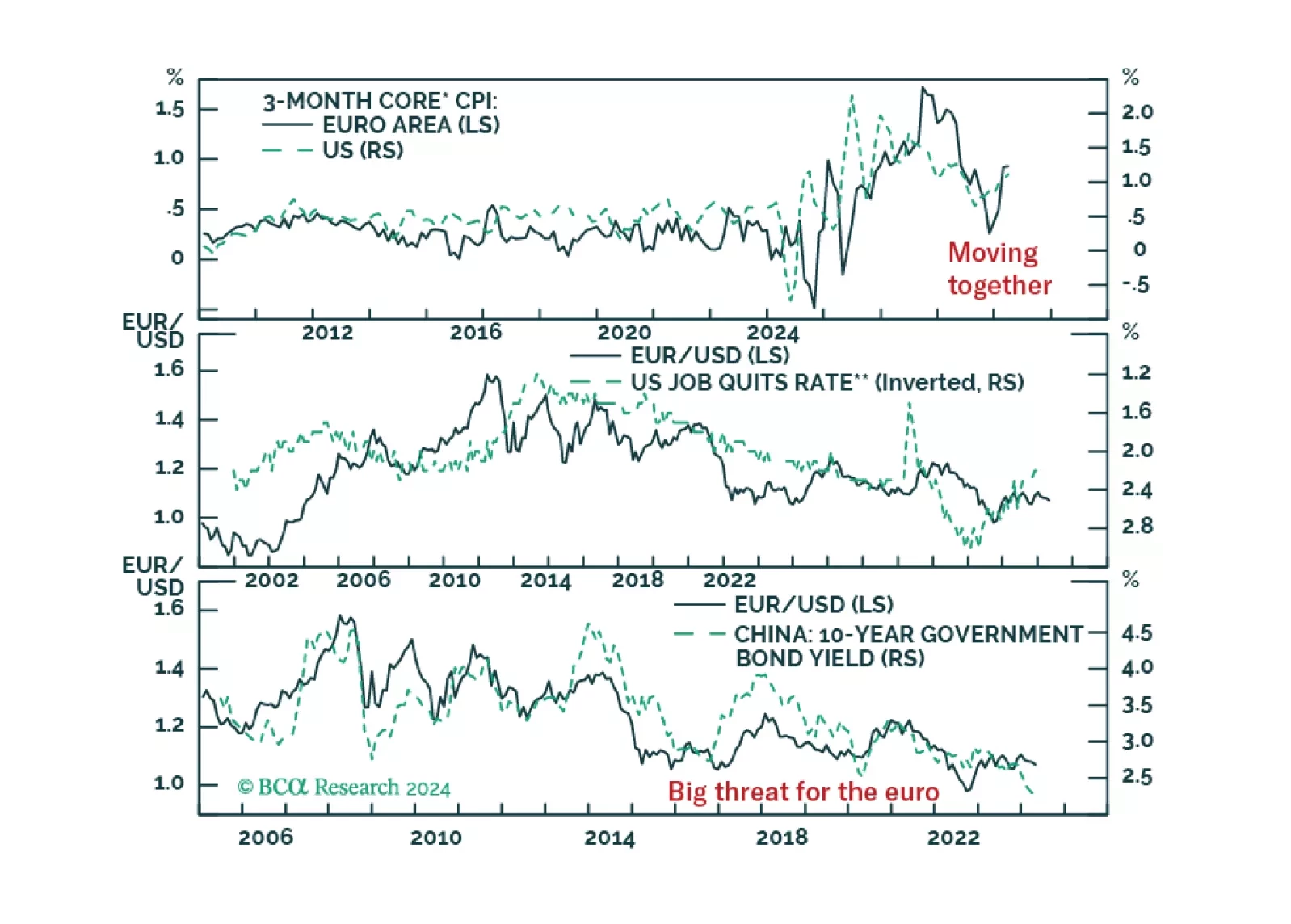

According to BCA Research’s European Investment Strategy service, a tactical buying opportunity for EUR/USD is approaching. However, this will not lead to a renewed bull market, only to a bounce toward 1.10-1.12. Sentiment toward the euro is becoming…

EUR/USD collapsed in the wake of last week’s hotter-than-expected US CPI report. Is this pessimism warranted and will the euro’s trading range that has prevailed since 2023 breakdown?

In this report, we present our quarterly review of our Model Bond Portfolio. The anti-growth bias of the portfolio allocations hurt the portfolio performance in Q1/2024 as global growth surprised to the upside. However, we anticipate some recovery of the underperformance in our base case scenario for the next six months.

US, European and Japanese small caps have underperformed their large cap counterparts by 22.6%, 15.3% and 10.1% respectively since 2021. They now face conflicting forces. On the one hand, they are extremely beaten down and cheap, potentially offering a good…