Euro Area

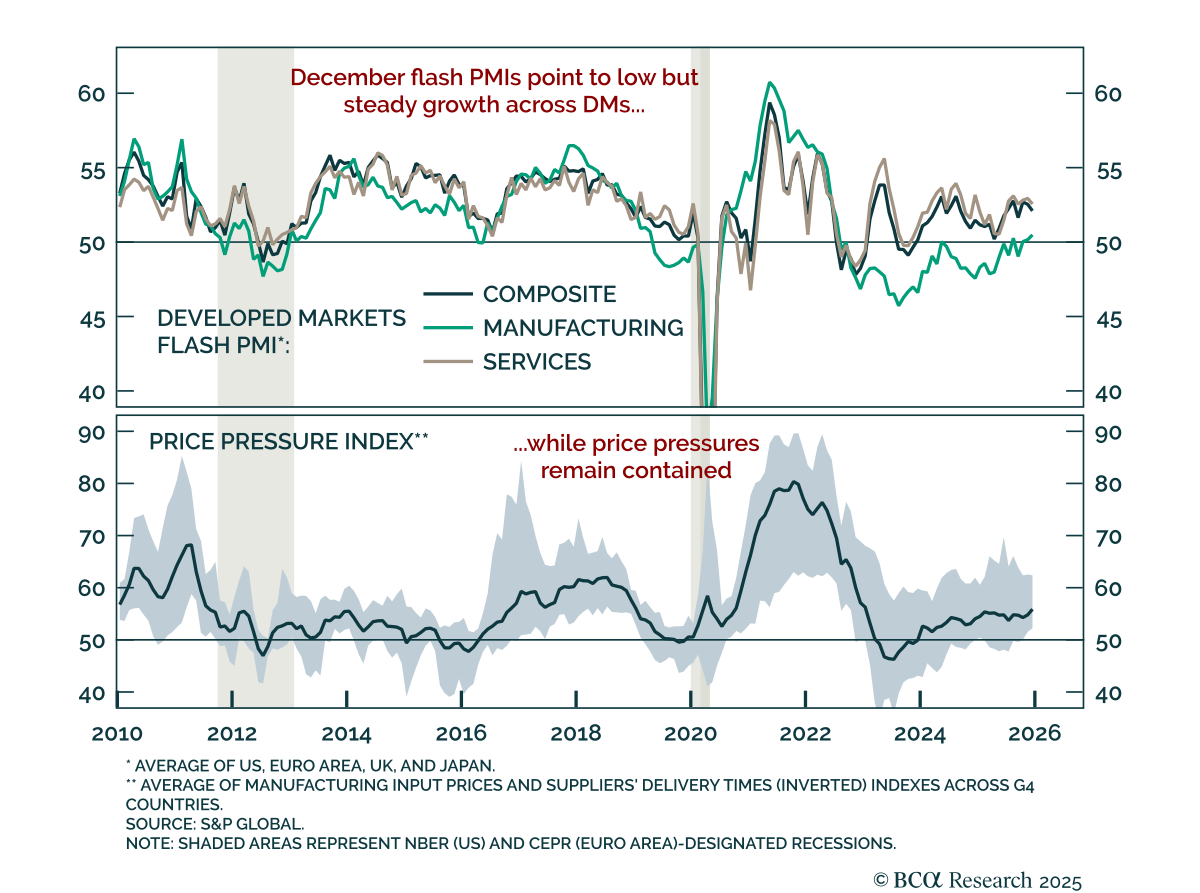

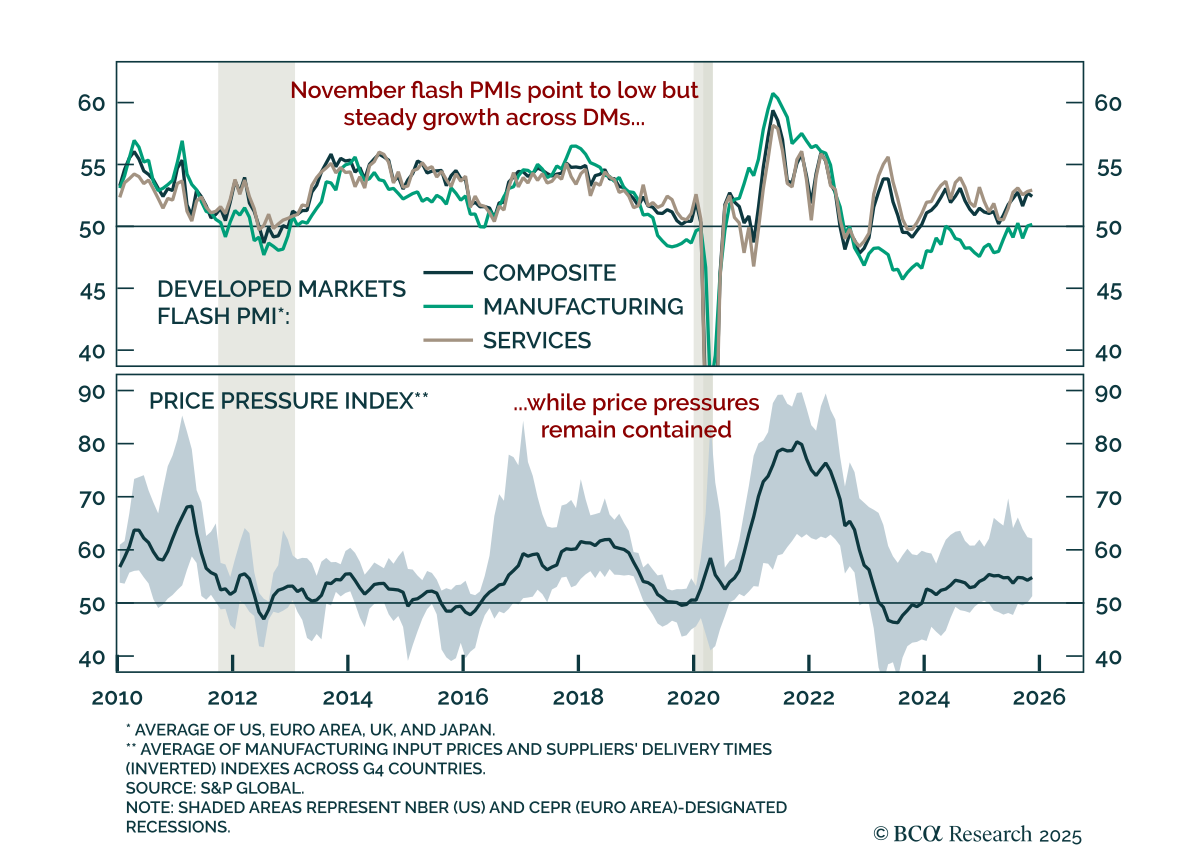

Maintain an underweight in industrial commodities as flash PMIs confirm weak global growth momentum. December flash PMIs for developed markets pointed to subdued activity. The US composite slowed to 53 from 54.2, a six-month low, with both manufacturing and…

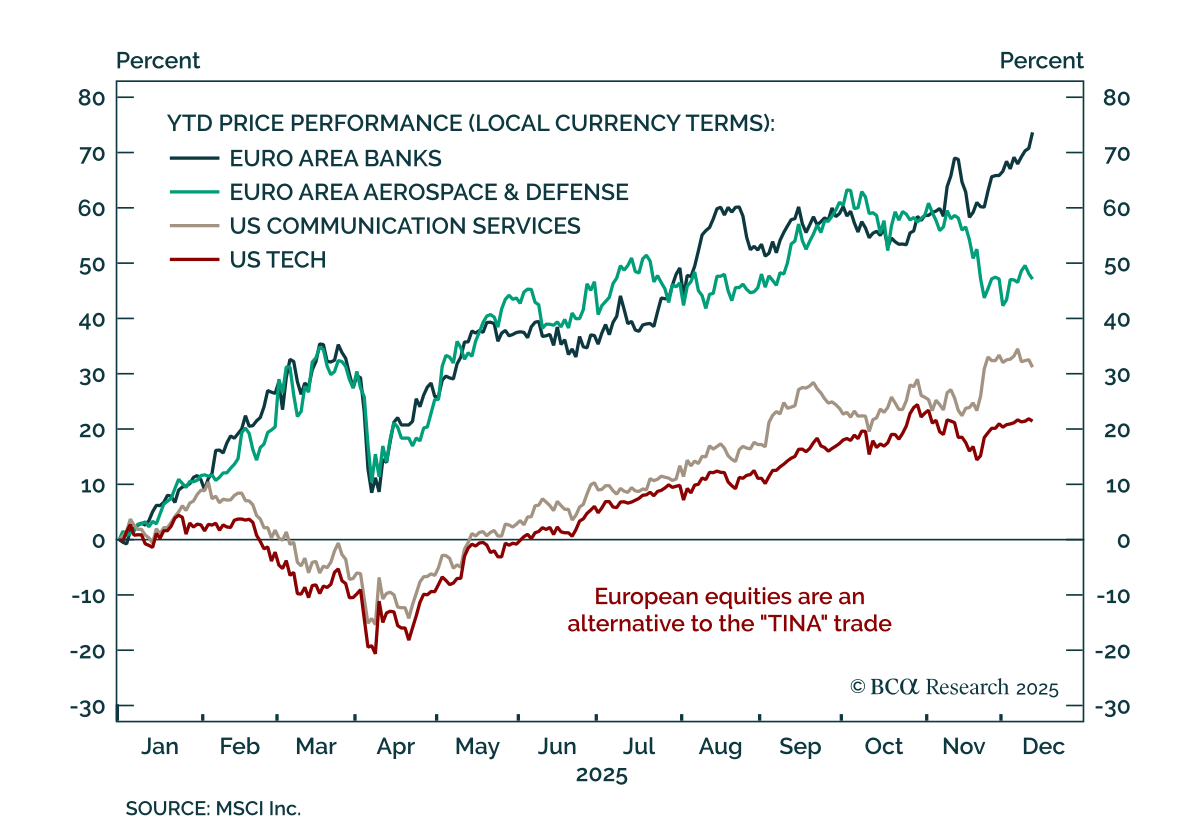

Europe’s equity outperformance is real, and even stronger once adjusted for FX. Our Chart Of The Week comes from Jeremie Peloso, Chief European Investment Strategist. Banks and defense stocks (not tech and communication services) have powered Europe’s…

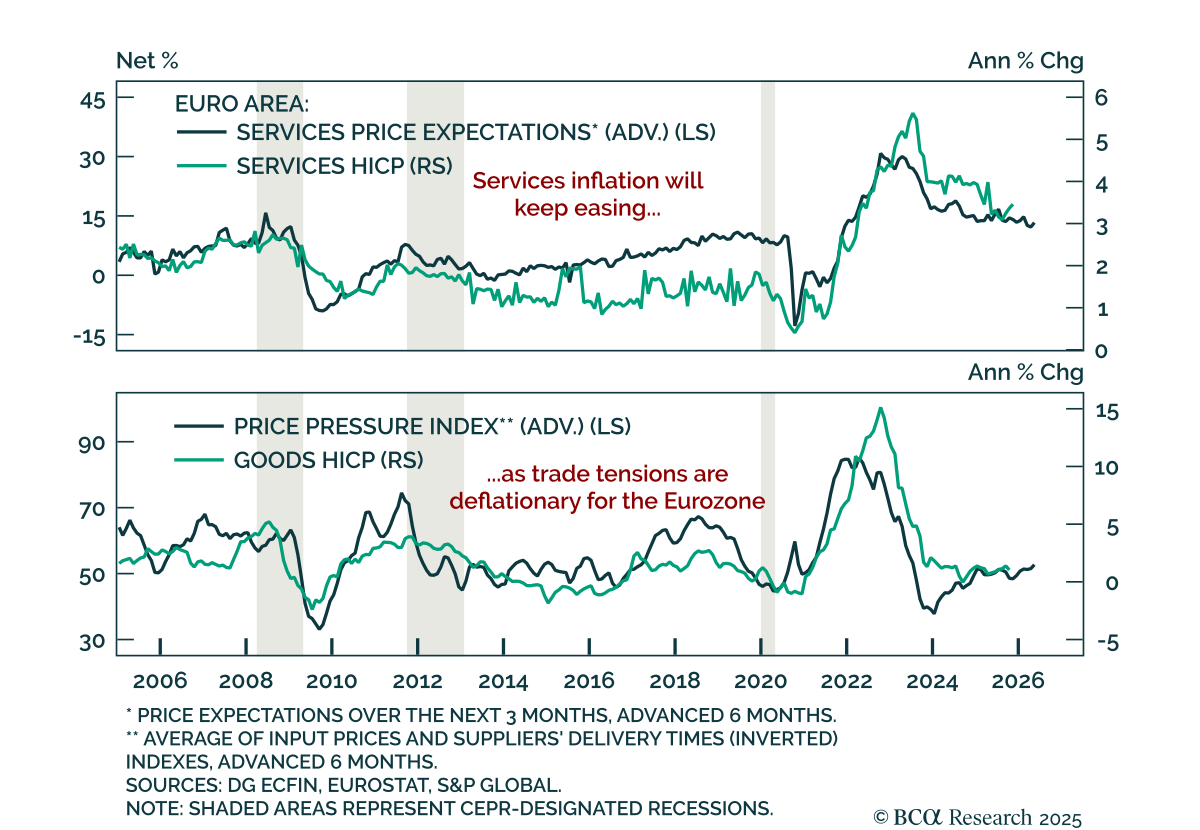

Favor US assets over European ones as weak Eurozone momentum and soft inflation keep tactical pressure on EUR. November Eurozone inflation came in slightly above estimates, with headline HICP at 2.2% y/y versus 2.1% in October and core steady at 2.4%. The…

The November Ifo survey disappointed, highlighting weakening expectations for Germany and limited near-term upside for European growth. The Business Climate Index fell to 88.1 from 88.4, driven by expectations dropping to 90.6 from 91.6, while current…

November flash PMIs confirmed sluggish global momentum, reinforcing a defensive stance with tactical support for the USD. The US composite PMI rose to 54.8, driven by stronger services but weaker manufacturing. The Euro area showed a similar pattern, with…

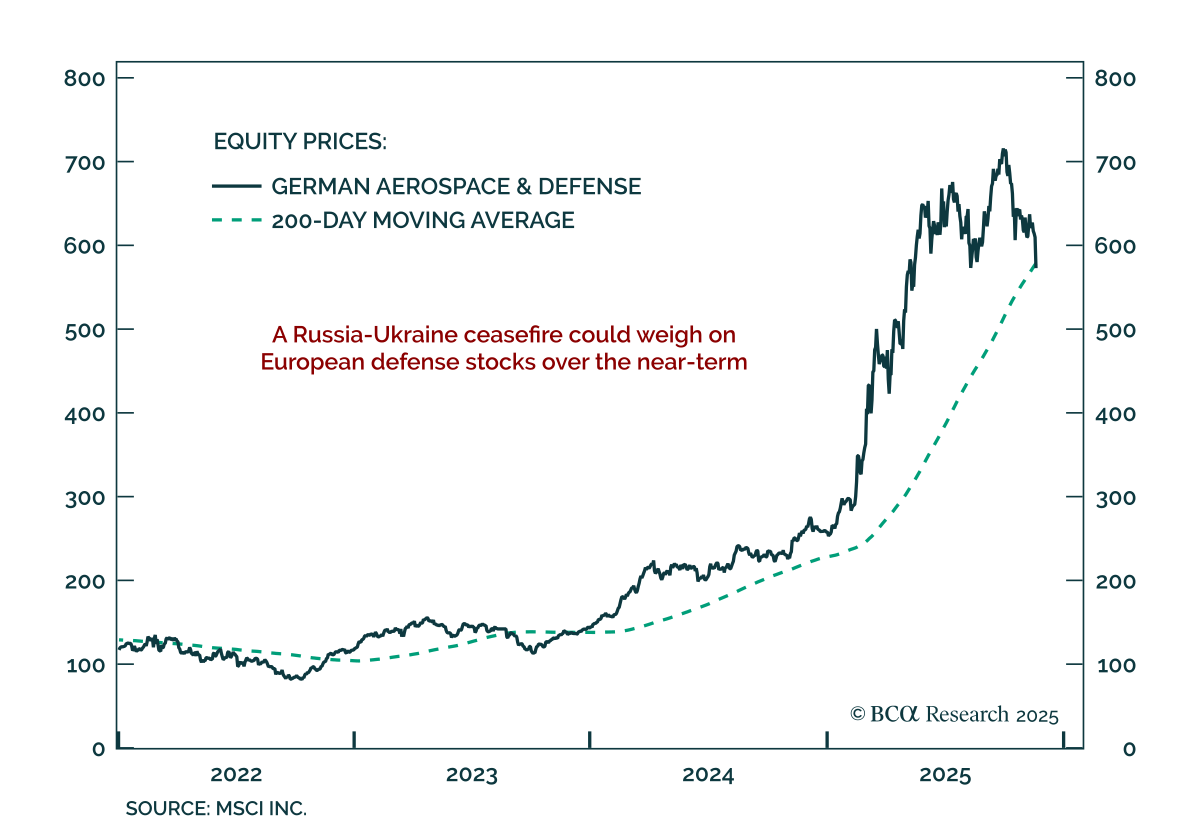

Reports of a potential US–Russia peace proposal revived speculation about a ceasefire, creating short-term downside risks for European defense equities. The 28-point framework, led by Trump’s negotiator, signals that both sides are exploring terms for a…

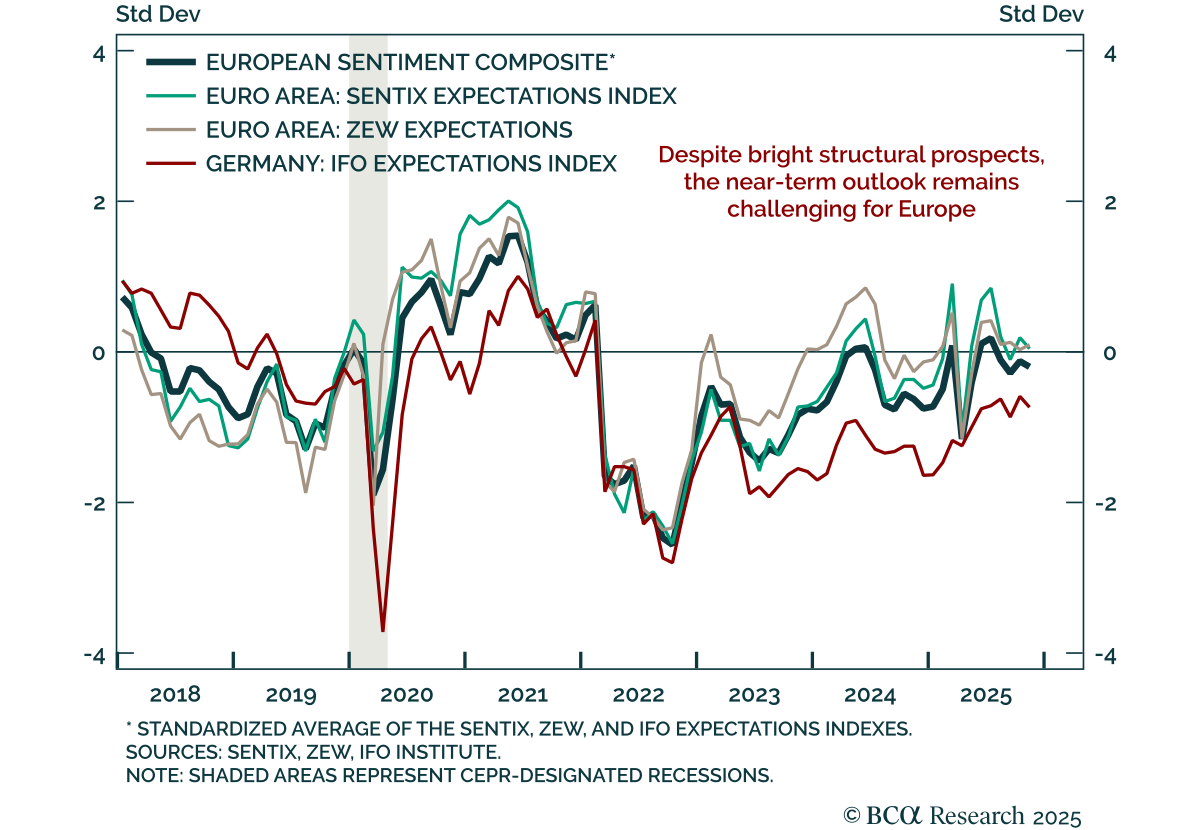

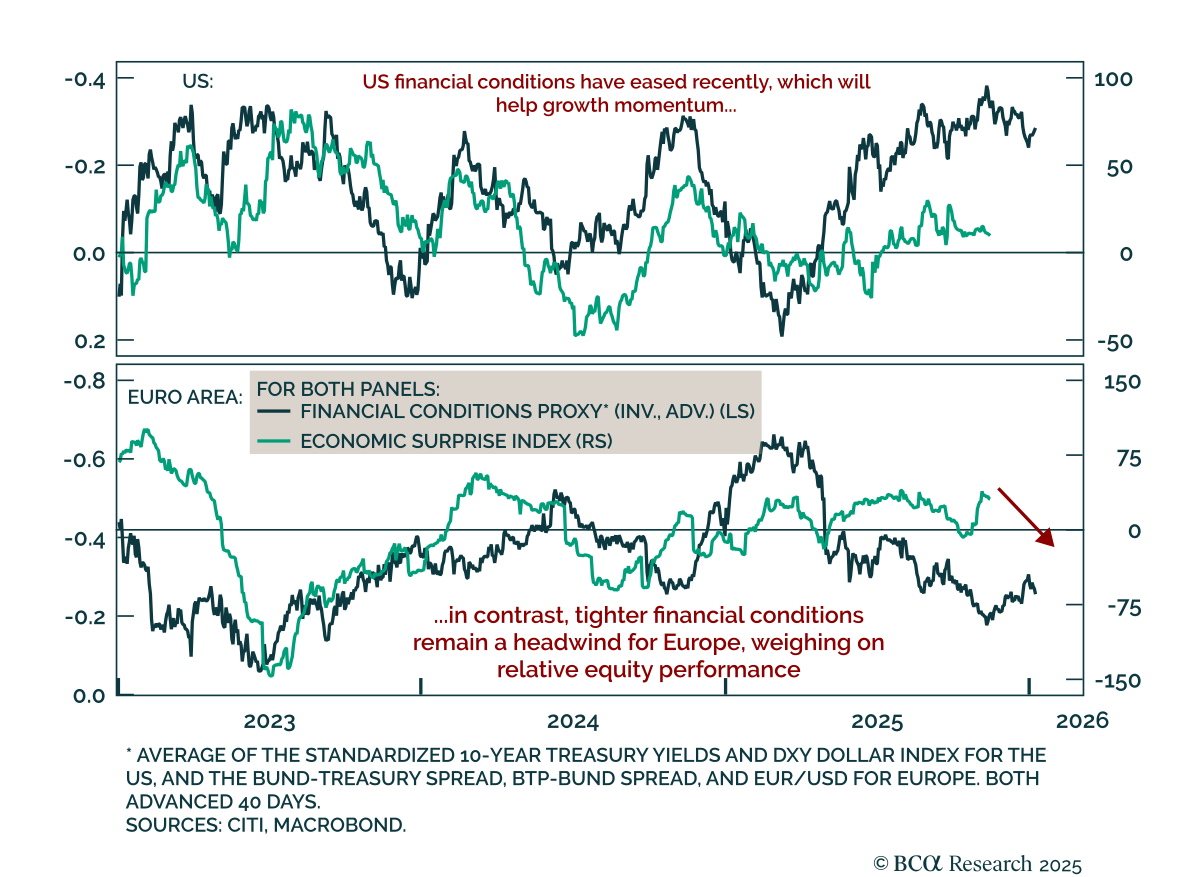

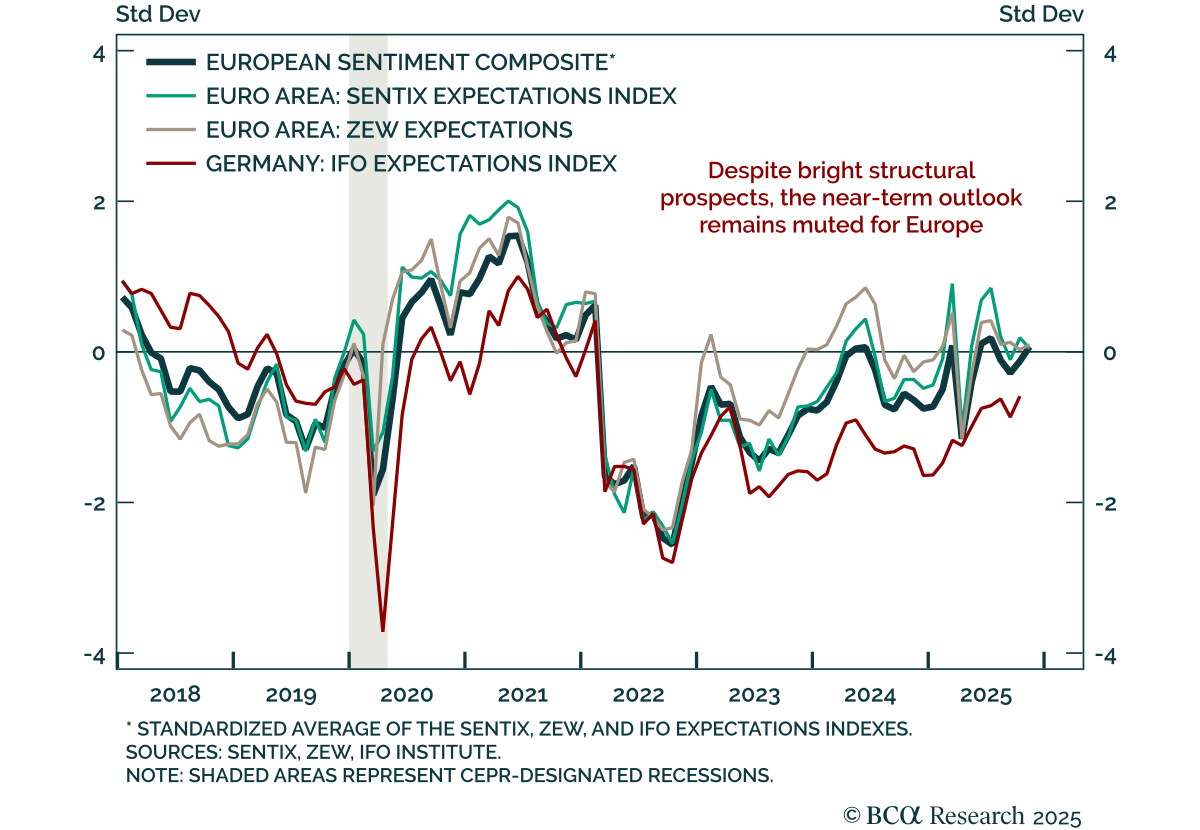

European sentiment remains mixed, with growth momentum failing to pick up despite brighter long-term prospects. Economic surprises have improved since mid-October, but tight financial conditions, driven by a strong euro and higher Bund yields since the start…

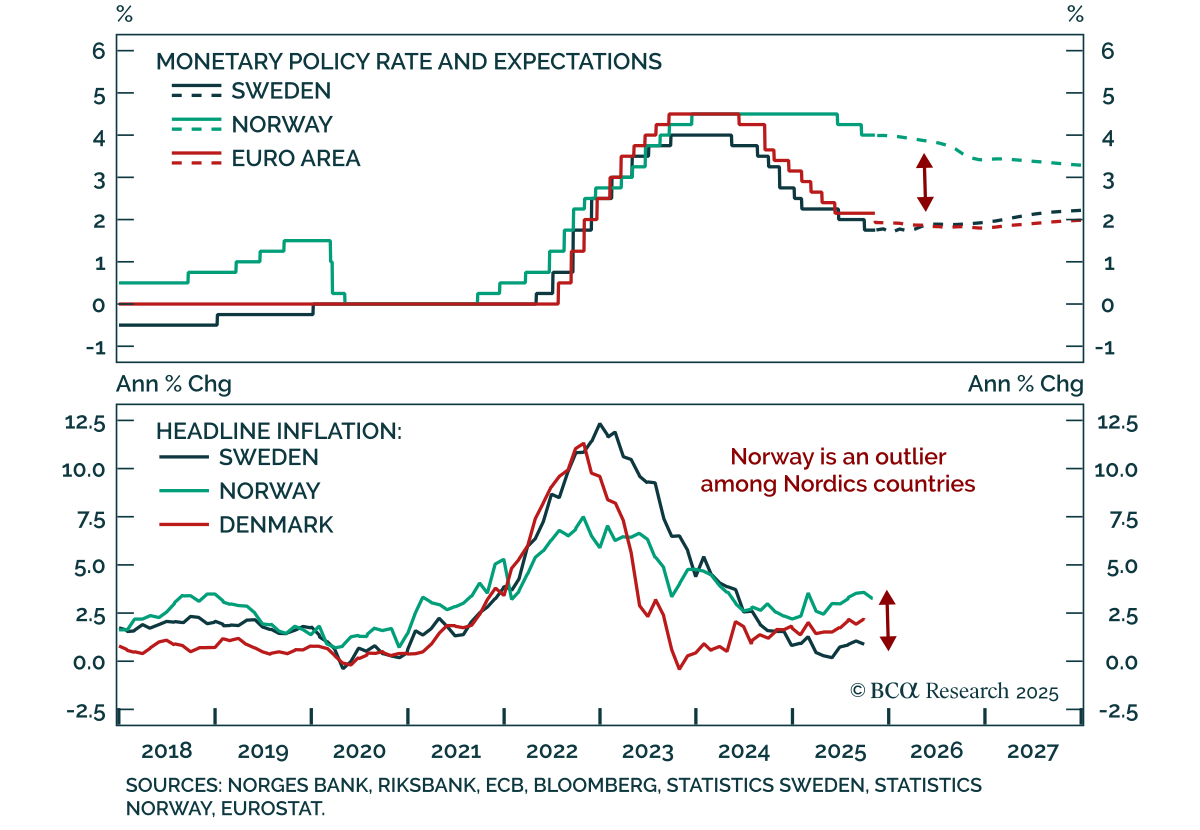

Our European strategists turn overweight Swedish equities and initiate a short NOK/SEK position as Nordic central banks pause but their economies diverge. Sweden’s recovery and stable inflation allow the Riksbank to join the “easing-cycle-complete” club,…

The November ZEW survey confirmed mixed sentiment in Europe, showing growth momentum is not taking off yet. Euro area growth expectations ticked up to 25.0 from 22.7, while German expectations missed estimates, edging down to 38.5 from 39.3. Current…

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.