Euro Area

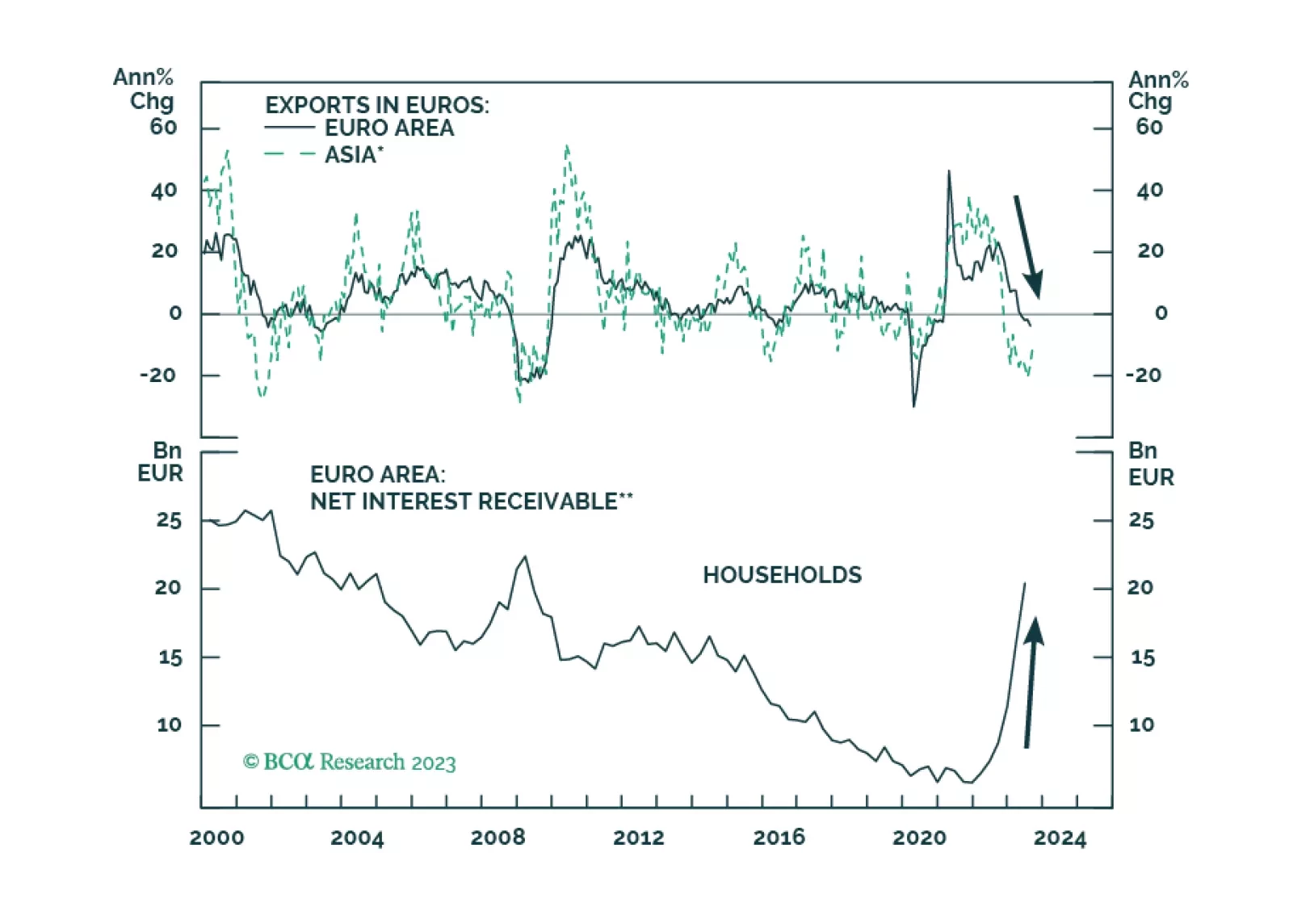

Europe’s weak patch is not about the ECB’s policy tightening, at least not yet. 2024 is another story, and the ECB’s policy will prompt a Eurozone’s recession around the summer.

In this report, we present the quarterly review of the Global Fixed Income Strategy Model Bond Portfolio. The portfolio remains positioned for slower global growth momentum over the next 6-12 months, favoring government bonds over corporate debt. The portfolio also favors government bonds in countries flirting with recession where policy rates are too high (core Europe & the UK).

Yields remain the force dominating the evolution of markets. A peak in yields would help European assets rebound, but the war in the Middle East could push higher energy prices, with negative consequences for Europe.

European auto stocks are cheap, but even if European carmakers can rise to the challenge created by Chinese EVs, shareholders will suffer.