Euro Area

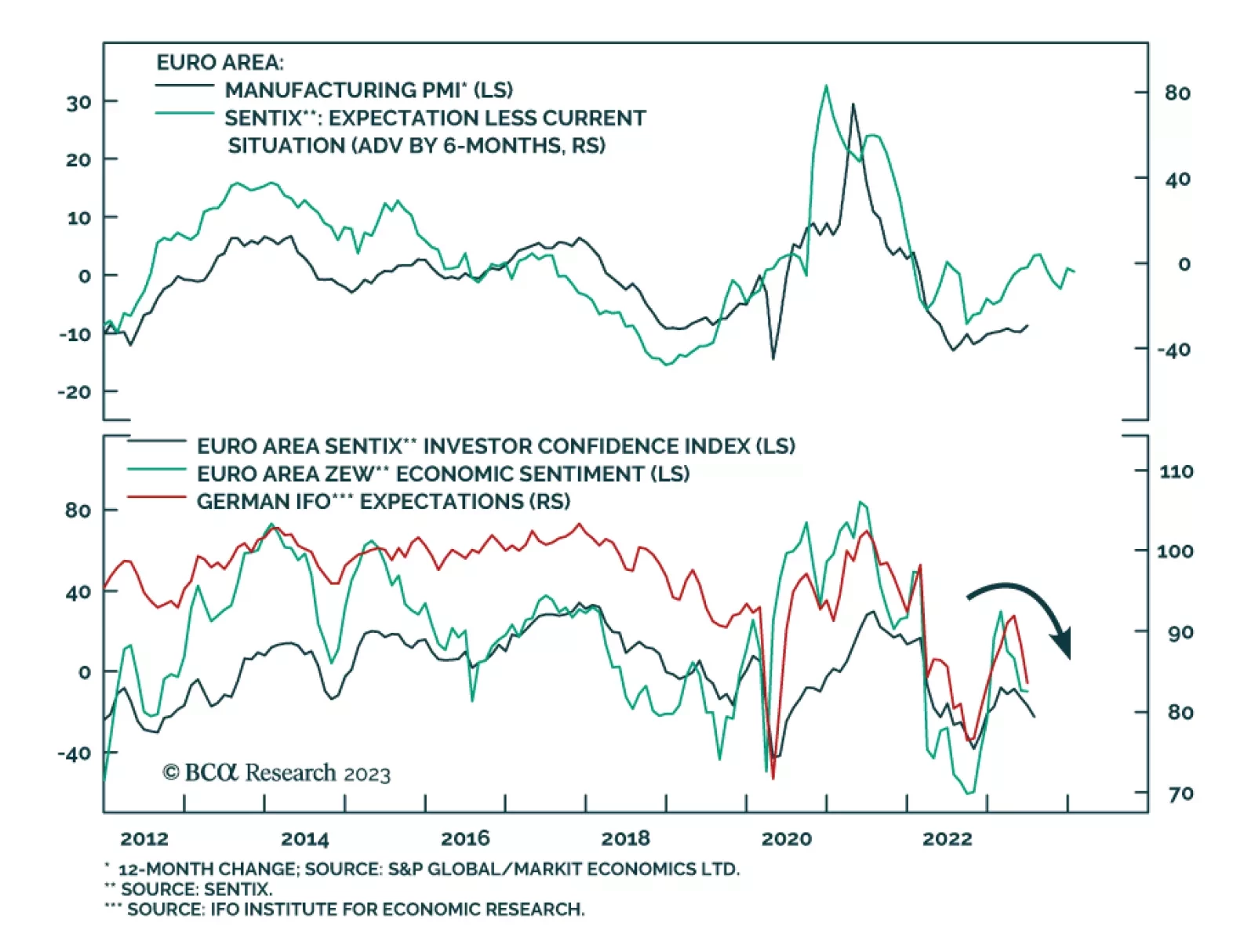

On Monday, the Eurozone Sentix sent a pessimistic signal about investor confidence in the Eurozone economy. The headline index dropped from -17.0 to -22.5 in July, significantly below expectations of a more muted deterioration to -17.9. Both the Expectations…

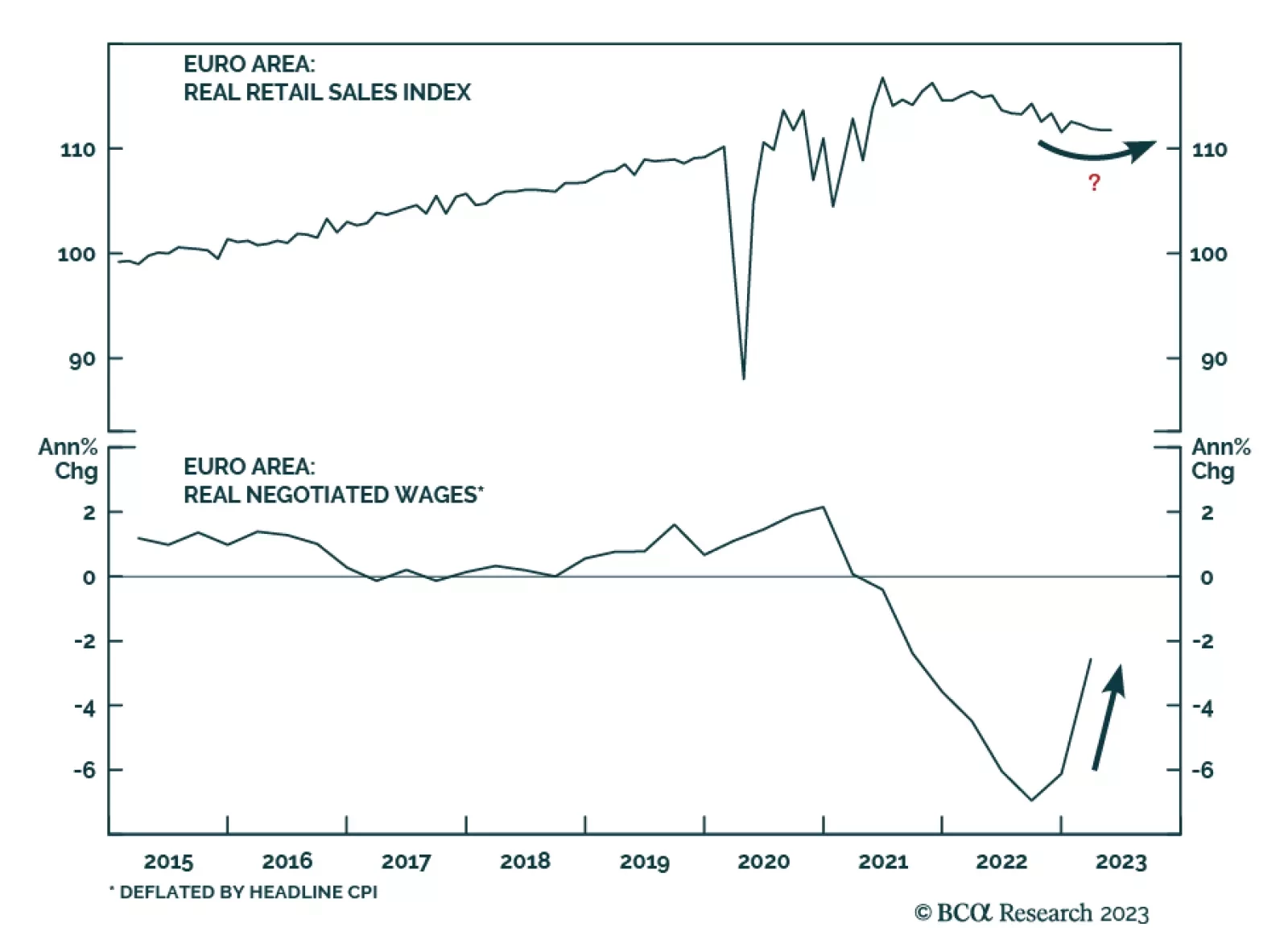

Yesterday we highlighted that falling producer prices foreshadow lower CPI inflation in the Eurozone and argued that this dynamic is positive for the bloc’s consumption outlook. Easing price pressures will ultimately lift real wages, reducing the drag on…

Eurozone producer prices fell by more than anticipated in May. The -1.5% y/y decrease – which marked the first annual drop since December 2020 – was more pronounced than expectations of a -1.3% y/y decline and followed a downwardly revised 0.9% y/y increase…

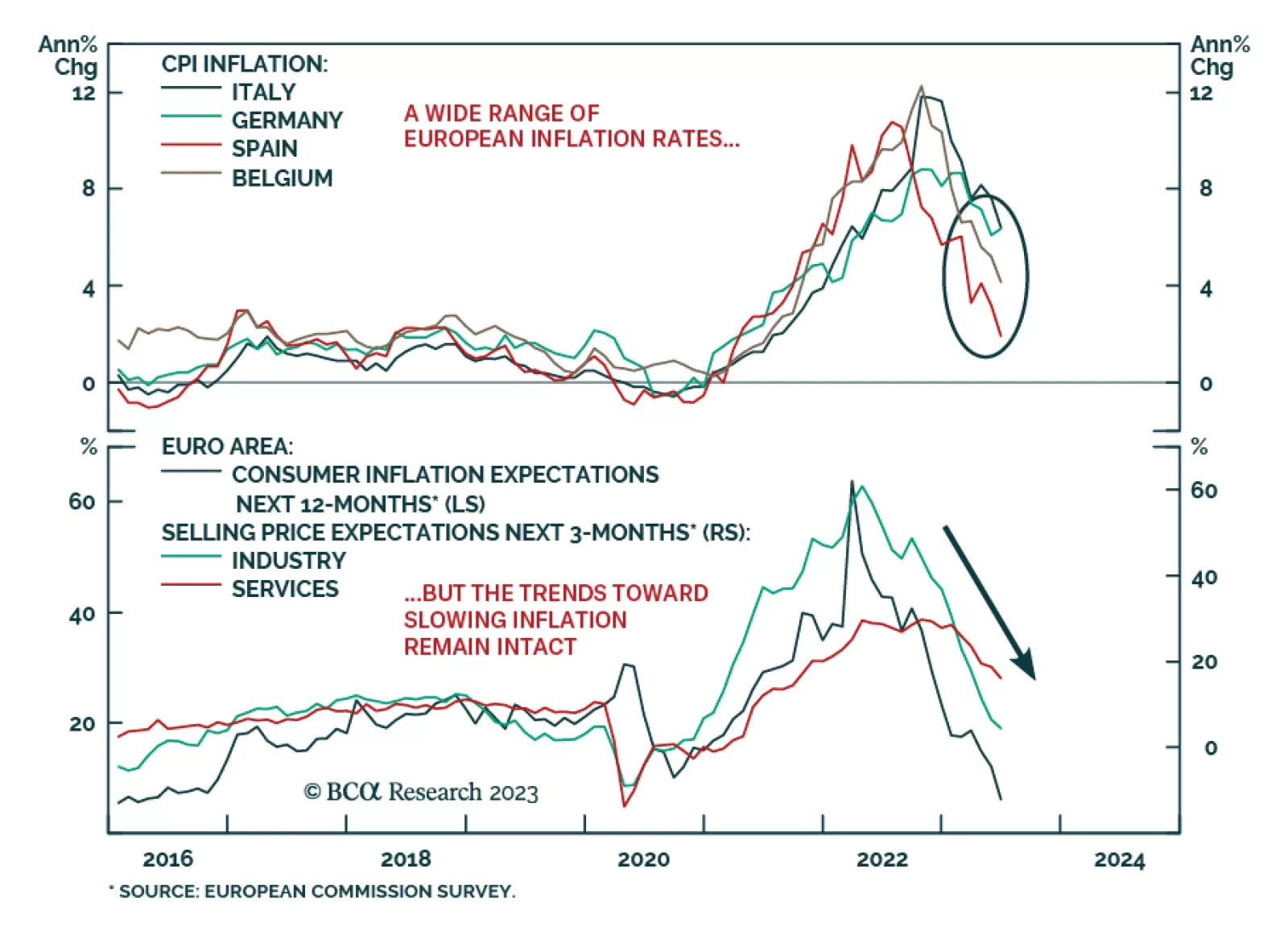

The preliminary inflation prints for June in the major euro area economies highlight a growing divergence in inflation outcomes. There was good news: headline CPI inflation in Italy fell to 6.7% in June from 8.0% in May, while Spanish headline inflation fell…

Our Counterpoint service argues that it is not enough that inflation stabilizes at 3 percent for inflation expectations to be anchored and central banks must make inflation undershoot 2 percent for some time to prevent a repeat of the 1970s. The team…

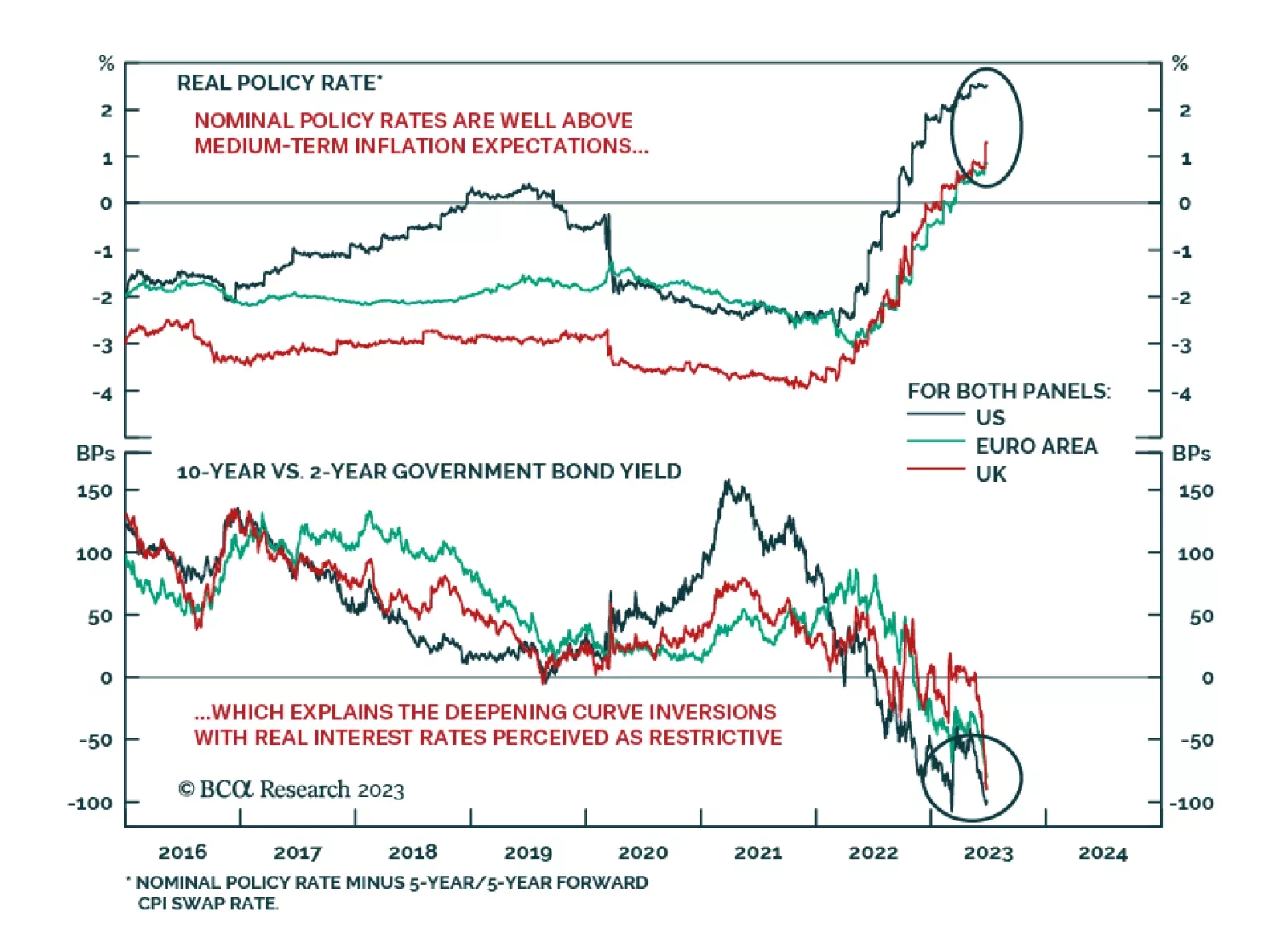

Has the yield curve lost its ability to “predict” recessions? The widely-followed 2-year/10-year US Treasury curve now sits at -100bps, but it has been inverted since April 2022. Investors have seemingly been on “recession watch” ever since, even though the…

This week’s Special Report updates our US default rate forecast and considers whether corporate bond spreads offer value given the trend in credit fundamentals. We also consider the relative value proposition between investment grade and high-yield credit and between European and US corporate bonds.

In this Insight, we discuss the currency and bond market implications of last week’s ECB and Bank of Japan policy meetings. The conclusion: the ECB is on a path to an overly hawkish policy mistake, while the Bank of Japan’s dovish stance is growing more unsustainable.

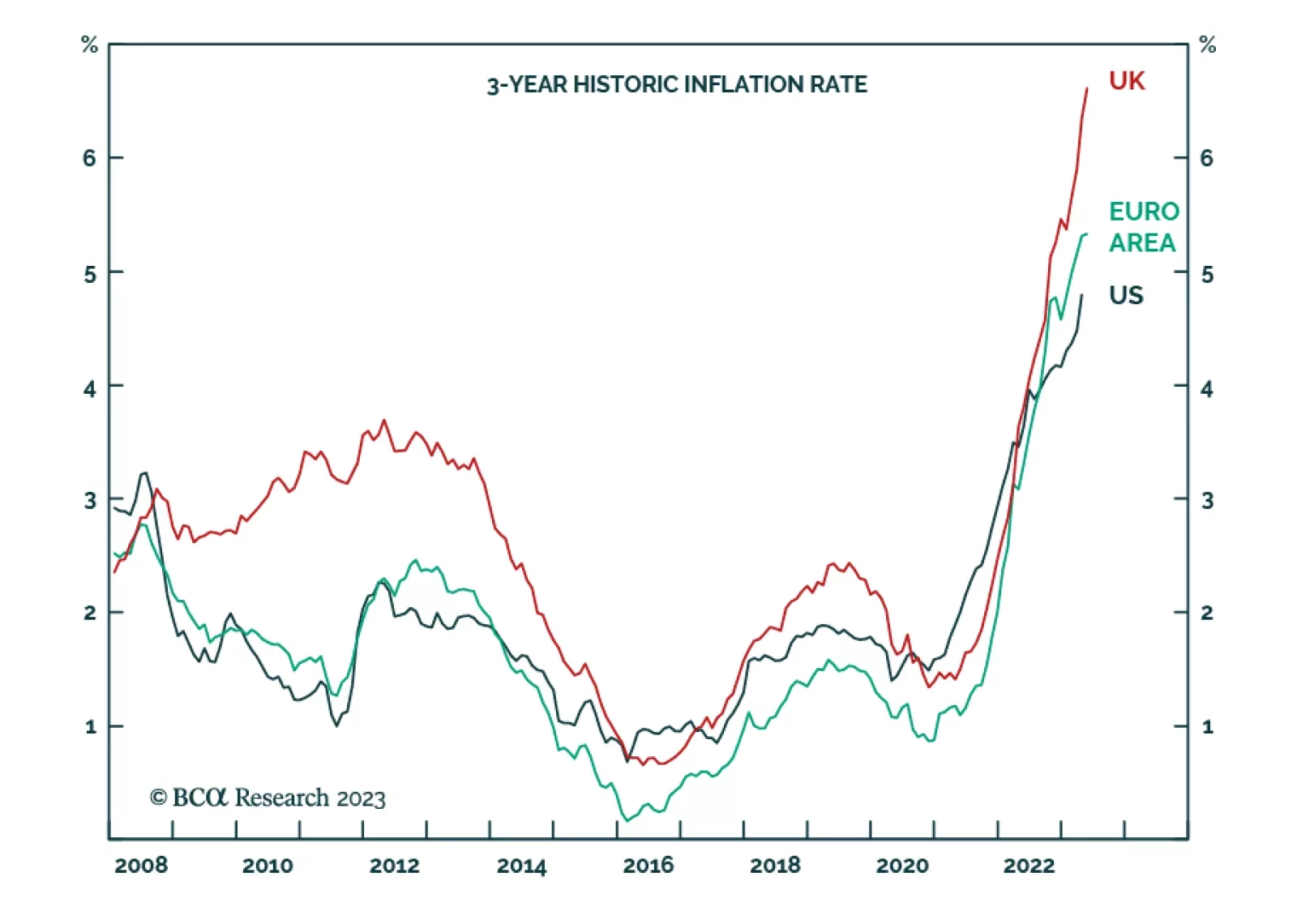

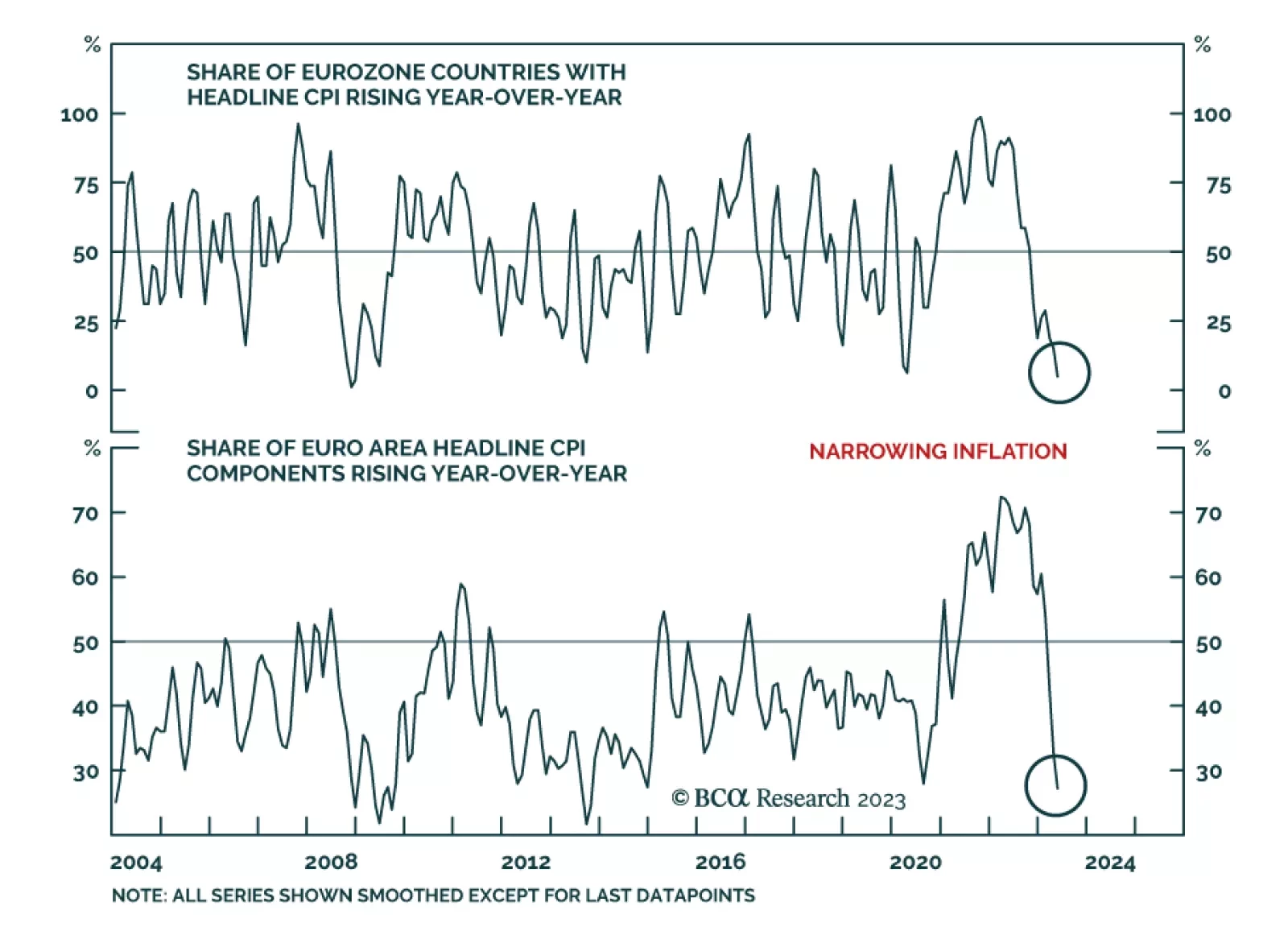

According to BCA Research’s European Investment Strategy service Eurozone inflation likely to diminish further. First, policy is tight. The impact on leading economic variables is already visible, with M1 collapsing, credit demand plunging, credit…

The Eurozone just experienced two consecutive quarters of GDP contraction. For the remainder of the year, can growth pick up or will the ECB decimate activity?