Euro Area

Dear Client, Next week, there will not be a written European Investment Strategy report; instead we will host a Webcast on April 26 with Chester Ntonifor, BCA’s Foreign Exchange Strategist. Regards, Mathieu Savary Executive Summary Cyclicals Are Not Cheap Enough

Cyclicals Are Not Cheap Enough

Cyclicals Are Not Cheap Enough

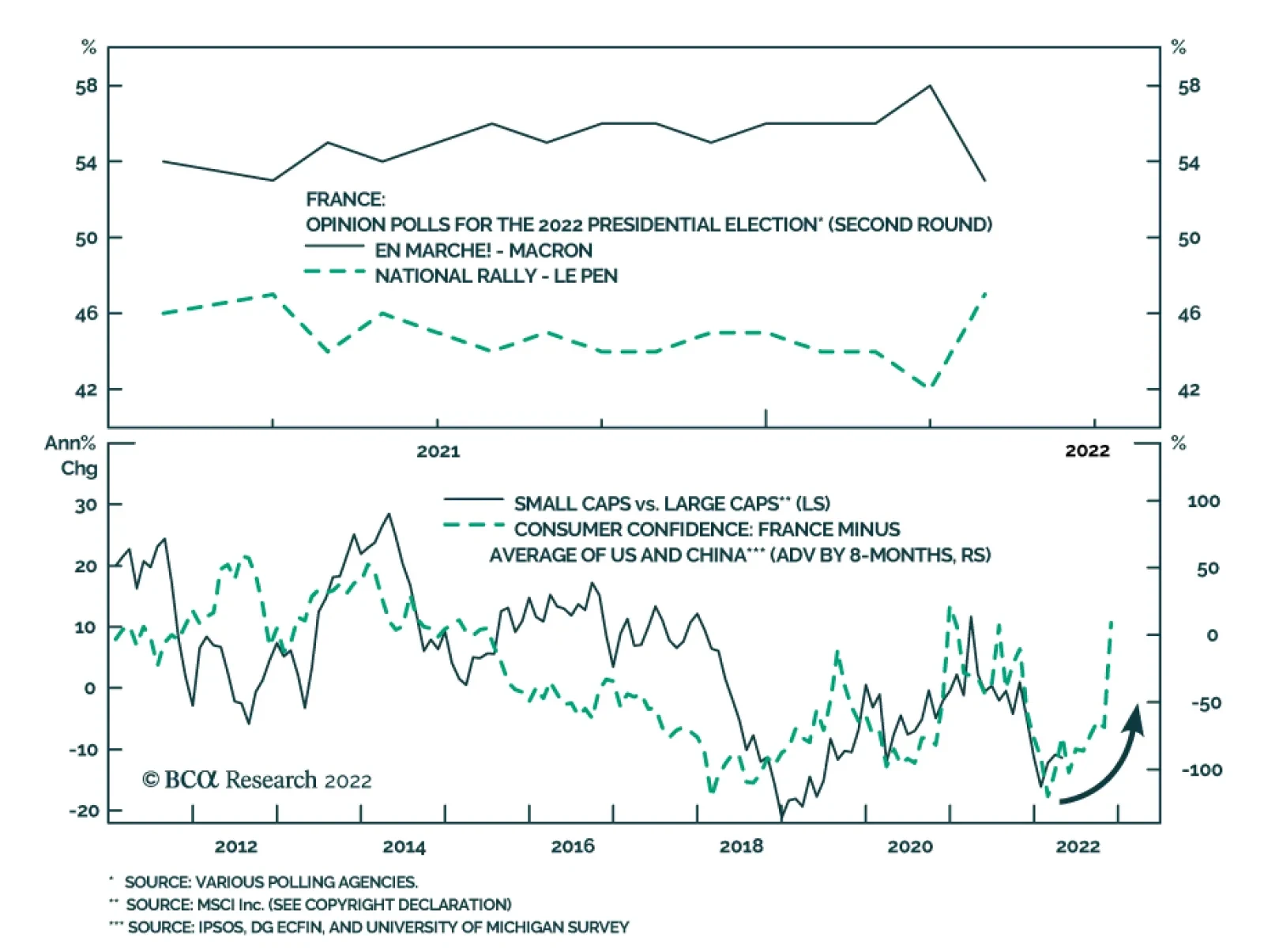

Global growth remains fragile as China’s economy becomes increasingly affected by COVID containment measures. The US economy is likely to slow down significantly in the coming months, while Europe flirts with a recession. This time around, monetary policy is unlikely to provide a relief valve. While European equities may inch higher in the coming months, cyclical stocks do not offer the necessary valuation discount relative to defensive equities to compensate investors against these risks. Heed the rotational patterns to guide near-term country and sector allocation. The French election remains an important source of risk, even though President Emmanuel Macron is still the favorite. Bottom Line: Maintain a modest positive bias toward equities, but overweight defensive stocks at the expense of cyclicals. Focus on short-term capital protection by favoring small-cap over momentum stocks, materials over energy, and UK equities over French ones. Chart 1So Far, Defensives Win

Plenty Of Risks For Cyclical Stocks

Plenty Of Risks For Cyclical Stocks

European equities have experienced a very volatile first quarter, with a maximum drawdown of nearly 23%. Since their March 7th low, they have rebounded 18% but remain 13% below the January 5th high. Apart from the energy sector, defensives have been running the show so far this year (Chart 1). We wrote four weeks ago that the European market is likely to have made its low for the year, but that the volatility of the first quarter of 2022 is likely to continue. We still hold this view. For now, we recommend investors stay long European equities, but defensive sector and country stances are appropriate. Cyclical stocks have corrected, but front-loaded global economic risks create additional downside. Economic Risks Abound The global economic environment remains fragile as headwinds continue to build. Cyclical equities do not seem to have fully discounted this threat. China’s economic outlook constitutes the first hindrance to global growth. COVID cases in Shanghai are surging and many Chinese cities are also witnessing an acceleration in new cases (Chart 2). The Communist Party is still adamant about its zero-tolerance policy, which suggests that these severe lockdowns will become the norm around the country. This situation creates significant downside for Chinese domestic demand, which will prompt a growth slowdown. The service sector is already feeling the pain from the lockdowns. The March import numbers also highlight an abrupt slowdown in the goods sector (Chart 3). In CNY terms, imports contracted 1.7% annually. This is a nominal number. Both global goods and commodity inflation are elevated, and thus, import volumes are weakening sharply. Furthermore, a recent Reuters article indicated that Chinese crude oil imports have already contracted 14% annually. Chart 2China's COVID Problem

China's COVID Problem

China's COVID Problem

Chart 3Slowing Chinese Domestic Demand

Slowing Chinese Domestic Demand

Slowing Chinese Domestic Demand

Chart 4Declining Shipping Costs, But For How Long?

Declining Shipping Costs, But For How Long?

Declining Shipping Costs, But For How Long?

China’s COVID policy also risks adding new supply chain bottlenecks. Freight within the country is grinding to a halt and ships are queuing up outside the port of Shanghai. As lockdowns multiply around China, risks to global supply chains will increase, hence, the recent decline in shipping rates out of China may soon be undone (Chart 4). This represents a major risk for the global economy, as it would tighten constraints to global economic activity. It also threatens European profitability, as PPI inflation would outpace CPI inflation for longer than anticipated (Chart 4, bottom panel). The US also shows signs of weakness. While a US recession is unlikely, a meaningful deceleration is probable. US consumers are feeling the pinch from surging food and energy prices. Consequently, real wages are contracting 1.8% annually and consumer confidence has plunged (Chart 5). Thankfully, US households have accumulated $185 billion in excess savings since the pandemic began and their net worth has increased by $33 trillion, which should prevent a complete meltdown. Nevertheless, a further deterioration in retail sales is still very likely. Businesses are also increasingly worried. The March NFIB survey shows that Small Business Optimism is falling quickly and that few companies believe it is a good time to expand (Chart 5, bottom panel). Adding to these stresses, the most cyclical sector of the US economy is weakening rapidly. The recent rise in US mortgage rates to 5% is causing a collapse in mortgage applications for house purchases and is behind the 30% tumble suffered by homebuilder stocks (Chart 6). Chart 5US Confidence Is Falling

US Confidence Is Falling

US Confidence Is Falling

Chart 6Tarnished US Housing Outlook

Tarnished US Housing Outlook

Tarnished US Housing Outlook

Europe is in a situation worse than the US and is at risk of a recession in the first half of 2022, or, at least, a very severe growth slowdown. As we highlighted six weeks ago, the energy shock in Europe is larger than it is in the US; moreover, Europe does not enjoy the counterweight of a large commodity sector. Recent data confirm that a slowdown is imminent. The ZEW Expectations survey, the German Ifo, and the European Commission’s Consumer Confidence data are all collapsing, which is consistent with a severe shock (Chart 7). To add insult to injury, bond yields continue to rise; therefore, the only relief valve for the region is a weak currency. Global monetary policy is unlikely to come to the rescue of investors anytime soon. The Fed began lifting rates in March and, if the actions of the Bank of Canada and the Reserve Bank of New Zealand are any indication, the FOMC will increase rates by 50bps in May. The OIS curve expects a Fed Funds rate at 2.2% by year-end, which seems appropriate. With a backdrop of weakening growth, a flat yield curve and an additional increase in real rates will feed risk aversion, especially against the cyclical sectors of the market (Chart 8). Chart 7Severe Slowdown In Europe... Or Worse

Severe Slowdown In Europe... Or Worse

Severe Slowdown In Europe... Or Worse

Chart 8Slowing Growth Meets Higher Real Rates

Slowing Growth Meets Higher Real Rates

Slowing Growth Meets Higher Real Rates

The liquidity tightening is not a phenomenon unique to the US. 63% of global central banks have removed monetary accommodation over the past three months (Chart 9). Moreover, our BCA Monetary Index continues to deteriorate. While we cannot characterize global monetary policy as being anywhere close to tight right now, cyclical equities remain vulnerable to the liquidity slowdown. Bottom Line: The global economy is likely to deteriorate in the coming months. The impact of COVID-19 on Chinese growth will only increase, while Europe flirts with a recession in the first half of the year. Meanwhile, US growth faces swelling headwinds. Expect a meaningful deterioration in global economic surprises (Chart 10). In this context, tighter policy will feed risk aversion, which will create a particularly strong headwind for cyclical stocks. Chart 9A Global Tightening

A Global Tightening

A Global Tightening

Chart 10Economic Surprises Will Fall

Economic Surprises Will Fall

Economic Surprises Will Fall

European Cyclicals Remain Vulnerable This backdrop is not equity-friendly and points to meagre returns over the next three to six months. Nonetheless, European stocks will not generate negative returns over this time frame because European benchmarks already discount a significant portion of the negative news, as illustrated by the surge in their earnings yield (Chart 11). Importantly, inflation in Europe should peak over the summer as the commodity impulse is decelerating (Chart 11, bottom panel). Therefore, fears of stagflation will recede, which will help aggregate European shares (Chart 12). Chart 11European Stocks Already Discount A Lot

European Stocks Already Discount A Lot

European Stocks Already Discount A Lot

Chart 12Ebbing Stagflation Fears Will Help European Equities

Ebbing Stagflation Fears Will Help European Equities

Ebbing Stagflation Fears Will Help European Equities

The consequence of the additional slowdown in global growth is likely to be reflected in the relative performance of European cyclical sectors. Already, Swedish economic growth and asset prices have deteriorated (Chart 13). This poor performance does not bode well for cyclical assets, considering the heightened sensitivity of Swedish assets to the global industrial cycle. More signals point to downside for the cyclical/defensive split. While the short-term momentum of the performance of cyclicals relative to defensives is becoming oversold, its 40-week rate of change has yet to reach a paroxysm (Chart 14). Additionally, cyclicals have not experienced the kind of valuation discount associated with a full discounting of the economic and monetary headwinds described in the previous section (Chart 14, bottom panel). Chart 13Heed Sweden's Message

Heed Sweden's Message

Heed Sweden's Message

Chart 14Cyclicals Are Not Cheap Enough

Cyclicals Are Not Cheap Enough Cyclicals Are Not Cheap Enough

Cyclicals Are Not Cheap Enough Cyclicals Are Not Cheap Enough

The commodity sector is also at risk of a pullback. China’s economic slowdown is likely to hurt commodity demand. While this will not end the secular commodity bull market underpinned by a lack of supply capacity, it could easily cause a significant correction in commodity prices. If, as we anticipate, inflation slows this summer, the inflation-hedging demand for commodities will also pause. These dynamics would hurt mining stocks, which have avoided a serious pullback, as well as the energy sector. Thus, a correction in commodities would cause additional weaknesses for the cyclicals-to-defensives ratio (Chart 15). Yields create a supplemental risk. Historically, rising US yields and inflation expectations correlate with an outperformance of cyclical shares. However, in 2022, cyclicals have bifurcated from yields and CPI swaps (Chart 16), because higher yields currently do not signal reflation but stagflation. If yields rise further, it will hurt growth prospects and damage cyclicals. If they fall, it will likely reflect increasing growth fears, which is also negative for cyclicals. Moreover, falling yields will hurt the profit margins of financials, which are a large component of cyclicals. Therefore, cyclicals seem stuck in a lose-lose situation with respect to yields. Chart 15The Commodity Link

The Commodity Link

The Commodity Link

Chart 16Yields and Cyclicals: A Lose-Lose Proposition

Yields and Cyclicals: A Lose-Lose Proposition

Yields and Cyclicals: A Lose-Lose Proposition

The strength in the dollar creates the last major hurdle for cyclicals. A strong dollar both tightens global financials conditions and indicates weak growth ahead. Consequently, it often heralds a period of softness in the cyclicals-to-defensives ratio (Chart 17). How should investors position themselves? We have a long-held preference for telecommunication services stocks over consumer discretionary equities and for healthcare relative to tech shares. These trades have respectively generated hefty gains of 32% and 13% since June 2021, but they are becoming long in the tooth (Chart 18). Chart 17A Strong Dollar Hurts Cyclicals

A Strong Dollar Hurts Cyclicals

A Strong Dollar Hurts Cyclicals

Chart 18Hedges Have Performed Strongly

Hedges Have Performed Strongly

Hedges Have Performed Strongly

Related Report European Investment StrategyThe Great Rotation As an alternative, we recommend investors stay nimble and use our Excess Returns Rotation Approach expanded in a Special Report two months ago. Below, you will find the new trades suggested by this process. Bottom Line: Cyclicals remain vulnerable. They have not reached the kind of valuation discount necessary to compensate investors for weaker growth and tighter monetary policy. To hedge against these risks, we recommended selling consumer discretionary relative to telecom stocks and tech shares relative to healthcare. However, investors should not add to those trades to mitigate against further weaknesses in cyclical stocks. Instead, investors should focus on relative rotational patterns (see next section). Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Excess Returns Rotation Maps: An Update1 European Investment Styles The most noteworthy move comes from small-cap stocks, going from the “Lagging” quadrant to the “Leading” one rapidly (Chart 19). This is consistent with our view that European small-cap equities’ outperformance has further to run. The attractiveness of value stocks is thinning relative to growth stocks (Table 1). Chart 19Relative Rotation Graph: European Investment Styles

Plenty Of Risks For Cyclical Stocks

Plenty Of Risks For Cyclical Stocks

Table 1European Investment Styles Positioning

Plenty Of Risks For Cyclical Stocks

Plenty Of Risks For Cyclical Stocks

Trade Recommendations (12-Month Horizon): Volatility stocks relative to momentum (unchanged) Small-cap stocks relative to momentum (new) European Sectors Chart 20 illustrates the wild ride in European equity markets in the wake of the Ukraine/Russia conflict. Most sectors experienced violent swings, moving rapidly across several quadrants. Only consumer discretionary, tech, and utilities stocks have remained in the same quadrant, the former two in “Lagging” and the latter in “Leading.” Interestingly, the European energy sector has moved into the “Weakening” quadrant (Table 2). We are taking profit on our Long Energy / Short Financials recommendation. It delivered 14% returns since mid-February and is getting long in the tooth. Chart 20Relative Rotation Graph: European Sectors

Plenty Of Risks For Cyclical Stocks

Plenty Of Risks For Cyclical Stocks

Table 2European Sectors Positioning

Plenty Of Risks For Cyclical Stocks

Plenty Of Risks For Cyclical Stocks

Trade Recommendations (12-Month Horizon): Materials over energy (unchanged) Energy over financials (unchanged) Tech over communication services (unchanged) Utilities over healthcare (new) Communication services over healthcare (new) Consumer discretionary over healthcare (new) European National Markets Sectoral biases dictate the rotational patterns exhibited by European national bourses (Chart 21). The cyclicality of the German, French, and Italian markets caused them to lag behind their European counterparts. Meanwhile, the Dutch market remains solidly in the Lagging quadrant, mirroring tech equities. Only Spain and Sweden have shown signs of improvement over the past twelve weeks and should outperform the European benchmark over the short term (Table 3). Chart 21Relative Rotation Graph: European National Markets

Plenty Of Risks For Cyclical Stocks

Plenty Of Risks For Cyclical Stocks

Table 3European National Markets Positioning

Plenty Of Risks For Cyclical Stocks

Plenty Of Risks For Cyclical Stocks

Trade Recommendations (12-Month Horizon): UK stocks over Dutch ones (new) UK stocks over French ones (new) Italian stocks over Swedish ones (new) UK stocks over Swedish ones (new) French Elections: Preparing For The Second Round The first round of the French presidential elections did not surprise. As in 2017, incumbent President Emmanuel Macron will face Marine Le Pen in the second round. Beyond this expected outcome, two important takeaways will be crucial in the second round: The collapse of traditional right-wing (Les Républicains) and left-wing (Parti Socialiste) parties. Far-left candidate Jean-Luc Mélenchon surprised to the upside with 22% of votes, right behind Marine Le Pen. The key implication is that the vote transfer has become more favorable to Macron (Diagram 1). In 2017, Marine Le Pen created the surprise and bested center-right candidate François Fillon by the narrowest of margins. As a result, Le Pen’s attempt to appeal to Fillon’s voters was a real threat. Today, the third largest pool of voters belongs to far-left candidate Mélenchon, who has already called upon his voters “not to give a single vote to Marine Le Pen.” Diagram 1Extrapolating France’s First-Round Election To The Second Round

Plenty Of Risks For Cyclical Stocks

Plenty Of Risks For Cyclical Stocks

How does it translate into voting intentions for the second round? Assuming a full transfer of votes from the defeated candidates based on the support they made public, Macron will crush Marine Le Pen as he did in 2017. However, this is unlikely, since many voters feel stuck between a rock and a hard place, and may decide not to vote. Related Report European Investment StrategyFrance: Macron And Macro Assuming Macron obtains only half of the voting intentions from other parties, while Marine Le Pen retains the full support from other far-right candidates’ voters, acquires half of the center-right votes, and secures a quarter of Mélenchon’s votes, the outcome will be much narrower at 53.4% vs. 46.6% in favor of Macron. This is in line with national polls. Two weeks ago, we presented the investment implications of a second Macron mandate. Since then, we have received many questions about the market consequences should Marine Le Pen enjoy a surprise victory. While this is not our base-case, we cannot rule out the possibility of a negative shock to the markets. Chart 22A Le Pen Surprise Victory Would Hurt The Euro

A Le Pen Surprise Victory Would Hurt The Euro

A Le Pen Surprise Victory Would Hurt The Euro

The only certainty within this very uncertain outcome is that Marine Le Pen would be constrained by a strong opposition in the Assemblée Nationale. Although she has changed her stance on “Frexit,” her presidency would undoubtfully carry an increased geopolitical risk within the European Union (EU) and hurt European unity and integration efforts. Thus, the resulting French isolationism would be synonymous with a weaker euro (Chart 22). French assets would be de-rated because her presidency would reverse previous reform efforts, which would hurt trend GDP growth, productivity, and the role of France within the EU. These trends are not only negative for stocks, but they would also put long-term upward pressure on OATs yields as French public finances would deteriorate meaningfully under a populist Le Pen presidency. In this context, underweighting both French equities and government bonds would be warranted. Jeremie Peloso, Associate Editor JeremieP@bcaresearch.com Footnotes Tactical Recommendations Cyclical Recommendations Structural Recommendations

Executive Summary Macron Still Favored, But Le Pen Cannot Be Ruled Out

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

Macron is still favored to win the French election but Le Pen’s odds are 45%. Le Pen would halt France’s neoliberal structural reforms, paralyze EU policymaking, and help Russia’s leverage in Ukraine. But she would lack legislative support and would not fatally wound the EU or NATO. European political risk will remain high in Germany, Italy, and Spain. Favor UK equities on a relative basis. Financial markets are complacent about Russian geopolitical risk again. Steer clear of eastern European assets. Do not bottom feed in Chinese stocks. China faces social unrest. North Korean geopolitical risk is back. Australia’s election is an opportunity, not a risk. Stay bullish on Latin America. Prefer Brazil over India. Stay negative on Turkey and Pakistan. Trade Recommendation Inception Date Return TACTICALLY LONG US 10-YEAR TREASURY 2022-04-14 Bottom Line: Go long the US 10-year Treasury on geopolitical risk and near-term peak in inflation. Feature Last year we declared that European political risk had reached a bottom and had nowhere to go but up. Great power rivalry with Russia primarily drove this view but we also argued that our structural theme of populism and nationalism would feed into it. Related Report Geopolitical StrategyThe Geopolitical Consequences Of The Ukraine War In other words, the triumph of the center-left political establishment in the aftermath of Covid-19 would be temporary. The narrow French presidential race highlights this trend. President Emmanuel Macron is still favored but Marine Le Pen, his far-right, anti-establishment opponent, could pull off an upset victory on April 24. The one thing investors can be sure of is that France’s ability to pursue neoliberal structural reforms will be limited even if Macron wins, since he will lack the mandate he received in 2017. Our GeoRisk Indicators this month suggest that global political trends are feeding into today’s stagflationary macroeconomic context. Market Complacent About Russia Again Global financial markets are becoming complacent about European security once again. Markets have begun to price a slightly lower geopolitical risk for Russia after it withdrew military forces from around Kyiv in an open admission that it failed to overthrow the government. However, western sanctions are rising, not falling, and Russia’s retreat from Kyiv means it will need to be more aggressive in the south and east (Chart 1). Chart 1Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

Russia has not achieved its core aim of a militarily neutral Ukraine – so it will escalate the military effort to achieve its aim. Any military failure in the east and south would humiliate the Putin regime and make it more unpredictable and dangerous. The West has doubled down on providing Ukraine with arms and hitting Russia with sanctions (e.g. imposing a ban on Russian coal). Germany prevented an overnight ban on Russian oil and natural gas imports but the EU is diversifying away from Russian energy rapidly. Sanctions that eat away at Russia’s export revenues will force it to take a more aggressive posture now, to achieve a favorable ceasefire before funding runs out. Sweden and Finland are reviewing whether to join NATO, with recommendations due by June. Russia will rattle sabers to underscore its red line against NATO enlargement and will continue to threaten “serious military-political repercussions” if these states try to join. We would guess they would remain neutral as a decision to join NATO could lead to a larger war. Bottom Line: Global equities will remain volatile due to a second phase of the war and potential Russian threats against Ukraine’s backers. European equities and currency, especially in emerging Europe, will suffer a persistent risk premium until a ceasefire is concluded. What If Le Pen Wins In France? By contrast with the war in Ukraine, the French election is a short-term source of political risk. A surprise Le Pen victory would shake up the European political establishment but investors should bear in mind that it would not revolutionize the continent or the world, as Le Pen’s powers would be limited. Unlike President Trump in 2017, she would not take office with her party gaining full control of the legislature. Le Pen rallied into the first round of the election on April 10, garnering 23% of the vote, up from 21% in 2017. This is not a huge increase in support but her odds of winning this time are much better than in 2017 because the country has suffered a series of material shocks to its stability. Voters are less enthusiastic about President Macron and his centrist political platform. Macron, the favorite of the political establishment, received 28% of the first-round vote, up from 24% in 2017. Thus he cannot be said to have disappointed expectations, though he is vulnerable. The euro remains weak against the dollar and unlikely to rally until Russian geopolitical risk and French political risk are decided. The market is not fully pricing French risk as things stand (Chart 2). Chart 2France: GeoRisk Indicator

France: GeoRisk Indicator

France: GeoRisk Indicator

The first-round election results show mixed trends. The political establishment suffered but so did the right-wing parties (Table 1). The main explanation is that left-wing, anti-establishment candidate Jean-Luc Mélenchon beat expectations while the center-right Republicans collapsed. Macron is leading Le Pen by only five percentage points in the second-round opinion polling as we go to press (Chart 3). Macron has maintained this gap throughout the race so far and both candidates are very well known to voters. But Le Pen demonstrated significant momentum in the first round and momentum should never be underestimated. Table 1Results Of France’s First-Round Election

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

Chart 3French Election: Macron Maintains Lead

French Election: Macron Maintains Lead

French Election: Macron Maintains Lead

Are the polls accurate? Anti-establishment candidates outperformed their polling by 7 percentage points in the first round. Macron, the right-wing candidates, and the pro-establishment candidates all underperformed their March and April polls (Chart 4). Hence investors should expect polls to underrate Le Pen in the second round. Chart 4French Polls Fairly Accurate Versus First-Round Results

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

Given the above points, it is critical to determine which candidate will gather the most support from voters whose first preference got knocked out in the first round. The strength of anti-establishment feeling means that the incumbent is vulnerable while ideological camps may not be as predictable as usual. Mélenchon has asked his voters not to give a single vote to Le Pen but he has not endorsed Macron. About 21% of his supporters say they will vote for Le Pen. Only a little more of them said they would vote for Macron, at 27% (Chart 5). Chart 5To Whom Will Voters Drift?

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

Diagram 1, courtesy of our European Investment Strategy, illustrates that Macron is favored in both scenarios but Le Pen comes within striking distance under certain conservative assumptions about vote switching. Diagram 1Extrapolating France’s First-Round Election To The Second Round

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

Macron’s approval rating has improved since the pandemic. This is unlike the situation in other liberal democracies (Chart 6). Chart 6Macron Handled Pandemic Reasonably Well

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

The pandemic is fading and the economy reviving. Unemployment has fallen from 8.9% to 7.4% over the course of the pandemic. Real wage growth, at 5.8%, is higher than the 3.3% that prevailed when Macron took office in 2017 (Chart 7). Chart 7Real Wages A Boon For Macron

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

But these positives do not rule out a Le Pen surprise. The nation has suffered not one but a series of historic shocks – the pandemic, inflation, and the war in Ukraine. Inflation is rising at 5.1%, pushing the “Misery Index” (inflation plus unemployment) to 12%, higher than when Macron took office, even if lower than the EU average (Chart 8). Chart 8Misery Index The Key Threat To Macron

Misery Index The Key Threat To Macron

Misery Index The Key Threat To Macron

Le Pen has moderated her populist message and rebranded her party in recent years to better align with the median French voter. She claims that she will not pursue a withdrawal from the European Union or the Euro Area currency union. This puts her on the right side of the one issue that disqualified her from the presidency in the past. Yet French trust in the EU is declining markedly, which suggests that Le Pen is in step with the median voter on wanting greater French autonomy (Chart 9). Le Pen’s well-known sympathy toward Vladimir Putin and Russia is a liability in the context of Russian aggression in Ukraine. Only 35% of French people had a positive opinion of Russia back in 2019, whereas 50% had a favorable view of NATO, and the gap has likely grown as a result of the invasion (Chart 10). However, the historic bout of inflation suggests that economic policy could be the most salient issue for voters rather than foreign policy. Chart 9Le Pen Only Electable Because She Accepted Europe

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

Chart 10Le Pen’s NATO Stance Not Disqualifying

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen’s economic platform is fiscally liberal and protectionist, which will appeal to voters upset over the rising cost of living and pressures of globalization. She wants to cut the income tax and value-added tax, while reversing Macron’s attempt at raising the retirement age and reforming the pension system. France’s tax rates on income, and on gasoline and diesel, are higher than the OECD average. In other words, Macron is running on painful structural reform while Le Pen is running on fiscal largesse. This is another reason to take seriously the risk of a Le Pen victory. What should investors expect if Le Pen pulls off an upset? France’s attempt at neoliberal structural reforms would grind to a halt. While Le Pen may not be able to pass domestic legislation, she would be able to halt the implementation of Macron’s reforms. Productivity and the fiscal outlook would suffer. Le Pen’s ability to change domestic policy will be limited by the National Assembly, which is due for elections from June 12-19. Her party, the National Rally (formerly the Front National), has never won more than 20% of local elections and performed poorly in the 2017 legislative vote. Investors should wait to see the results of the legislative election before drawing any conclusions about Le Pen’s ability to change domestic policy. France’s foreign policy would diverge from Europe’s. If Le Pen takes the presidency, she will put France at odds with Brussels, Berlin, and Washington, in much the same way that President Trump did. She would paralyze European policymaking. Yet Le Pen alone cannot take France out of the EU. The French public’s negative view of the EU is not the same as a majority desire to leave the bloc – and support for the euro currency stands at 69%. Le Pen does not have the support for “Frexit,” French exit from the EU. Moreover European states face immense pressures to work together in the context of global Great Power Rivalry. Independently they are small compared to the US, Russia, and China. Hence the EU will continue to consolidate as a geopolitical entity over the long run. Russia, however, would benefit from Le Pen’s presidency in the context of Ukraine ceasefire talks. EU sanctions efforts would freeze in place. Le Pen could try to take France out of NATO, though she would face extreme opposition from the military and political establishment. If she succeeded on her own executive authority, the result would be a division among NATO’s ranks in the face of Russia. This cannot be ruled out: if the US and Russia are fighting a new Cold War, then it is not unfathomable that France would revert to its Cold War posture of strategic independence. However, while France withdrew from NATO’s integrated military command from 1966-2009, it never withdrew fully from the alliance and was always still implicated in mutual defense. In today’s context, NATO’s deterrent capability would not be much diminished but Le Pen’s administration would be isolated. Russia would be unable to give any material support to France’s economy or national defense. Bottom Line: Macron is still favored for re-election but investors should upgrade Le Pen’s chances to a subjective 45%. If she wins, the euro will suffer a temporary pullback and French government bond spreads will widen over German bunds. The medium-term view on French equities and bonds will depend on her political capability, which depends on the outcome of the legislative election from June 12-19. She will likely be stymied at home and only capable of tinkering with foreign policy. But if she has legislative support, her agenda is fiscally stimulative and would produce a short-term sugar high for French corporate earnings. However, it would be negative for long-term productivity. UK, Italy, Spain: Who Else Faces Populism? Chart 11Rest Of Europe: GeoRisk Indicators

Rest Of Europe: GeoRisk Indicators

Rest Of Europe: GeoRisk Indicators

Between Russian geopolitical risk and French political risk, other European countries are likely to see their own geopolitical risk premium rise (Chart 11). But these countries have their own domestic political dynamics that contribute to the reemergence of European political risk. Germany’s domestic political risk is relatively low but it faces continued geopolitical risk in the form of Russia tensions, China’s faltering economy, and potentially French populism (Chart 11, top panel). In Italy, the national unity coalition that took shape under Prime Minister Mario Draghi was an expedient undertaken in the face of the pandemic. As the pandemic fades, a backlash will take shape among the large group of voters who oppose the EU and Italian political establishment. The Italian establishment has distributed the EU recovery funds and secured the Italian presidency as a check on future populist governments. But it may not be able to do more than that before the next general election in June 2023, which means that populism will reemerge and increase the political risk premium in Italian assets going forward (Chart 11, second panel). Spain is still a “divided nation” susceptible to a rise in political risk ahead of the general election due by December 10, 2023. However, the conservative People’s Party, the chief opposition party, has suffered from renewed infighting, which gives temporary relief to the ruling Socialist Worker’s Party of Prime Minister Pedro Sanchez. The Russia-Ukraine issue caused some minor divisions within the government but they are not yet leading to any major political crisis, as nationwide pro-Ukraine sentiment is largely unified. The Andalusia regional election, which is expected this November, will be a check point for the People’s Party’s new leadership and a test run for next year’s general election. Andalusia is the most populous autonomous community in Spain, consisting about 17% of the seats in the congress (the lower house). The risk for Sanchez and the Socialists is that the opposition has a strong popular base and this fact combined with the stagflationary backdrop will keep political polarization high and undermine the government’s staying power (Chart 11, third panel). While Prime Minister Boris Johnson has survived the scandal over attending social events during Covid lockdowns, as we expected, nevertheless the Labour Party is starting to make a comeback that will gain momentum ahead of the 2024 general election. Labour is unlikely to embrace fiscal austerity or attempt to reverse Brexit anytime soon. Hence the UK’s inflationary backdrop will persist (Chart 11, fourth panel). Bottom Line: European political risk has bottomed and will rise in the coming months and years, although the EU and Eurozone will survive. We still favor UK equities over developed market equities (excluding the US) because they are heavily tilted toward consumer staples and energy sectors. Stay long GBP-CZK. Favor European defense stocks over tech. Prefer Spanish stocks over Italian. China: Social Unrest More Likely China’s historic confluence of internal and external risks continues – and hence it is too soon for global investors to try to bottom-feed on Chinese investable equities (Chart 12). A tactical opportunity might emerge for non-US investors in 2023 but now is not the right time to buy. Chart 12China: GeoRisk Indicator

China: GeoRisk Indicator

China: GeoRisk Indicator

In domestic politics, the reversion to autocracy under Xi is exacerbating the economic slowdown. True, Beijing is stimulating the economy by means of its traditional monetary and fiscal tools. The latest data show that the total social financing impulse is reviving, primarily on the back of local government bonds (Chart 13). Yet overall social financing is weaker because private sector sentiment remains downbeat. The government is pursuing excessively stringent social restrictions in the face of the pandemic. Beijing is doubling down on “Covid Zero” policy by locking down massive cities such as Shanghai. The restrictions will fail to prevent the virus from spreading. They are likely to engender social unrest, which we flagged as our top “Black Swan” risk this year and is looking more likely. Lockdowns will also obstruct production and global supply chains, pushing up global goods inflation. Meanwhile the property sector continues to slump on the back of weak domestic demand, large debt levels, excess capacity, regulatory scrutiny, and negative sentiment. Consumer borrowing appetite and general animal spirits are weak in the face of the pandemic and repressive political environment (Chart 14). Chart 13China's Stimulus Has Clearly Arrived

China's Stimulus Has Clearly Arrived

China's Stimulus Has Clearly Arrived

Chart 14Yet Chinese Animal Spirits Still Suffering

Yet Chinese Animal Spirits Still Suffering

Yet Chinese Animal Spirits Still Suffering

Hence China will be exporting slow growth and inflation – stagflation – to the rest of the world until after the party congress. At that point President Xi will feel politically secure enough to “let 100 flowers bloom” and try to improve economic sentiment at home and abroad. This will be a temporary phenomenon (as were the original 100 flowers under Chairman Mao) but it will be notable for 2023. In foreign politics, Russia’s attack on Ukraine has accelerated the process of Russo-Chinese alliance formation. This partnership will hasten US containment strategy toward China and impose a much faster economic transition on China as it pursues self-sufficiency. The result will be a revival of US-China tensions. The implications are negative for the rest of Asia Pacific: Taiwanese geopolitical risk will continue rising for reasons we have outlined in previous reports. In addition, Taiwanese equities are finally starting to fall off from the pandemic-induced semiconductor rally (Chart 15). The US and others are also pursuing semiconductor supply security, which will reduce Taiwan’s comparative advantage. Chart 15Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

South Korea faces paralysis and rising tensions with North Korea. The presidential election on May 9 brought the conservatives back into the Blue House. The conservative People Power Party’s candidate, Yoon Suk-yeol, eked out a narrow victory that leaves him without much political capital. His hands are also tied by the National Assembly, at least for the next two years. He will attempt to reorient South Korean foreign policy toward the US alliance and away from China. He will walk away from the “Moonshine” policy of engagement with North Korea, which yielded no fruit over the past five years. North Korea has responded by threatening a nuclear missile test, restarting intercontinental ballistic missile tests for the first time since 2017, and adopting a more aggressive nuclear deterrence policy in which any South Korean attack will ostensibly be punished by a massive nuclear strike. Tensions on the peninsula are set to rise (Chart 16). Three US aircraft carrier groups are around Japan today, despite the war in Europe (where two are placed), suggesting high threat levels. Chart 16South Korea: GeoRisk Indicator

South Korea: GeoRisk Indicator

South Korea: GeoRisk Indicator

Australia’s elections present opportunity rather than risk. Prime Minister Scott Morrison formally scheduled them for May 21. The Australian Labor Party is leading in public opinion and will perform well. The election threatens a change of parties but not a drastic change in national policy – populist parties are weak. No major improvement in China relations should be expected. Any temporary improvement, as with the Biden administration, will be subject to reversal due to China’s long-term challenge to the liberal international order. Cyclically the Australian dollar and equities stand to benefit from the global commodity upcycle as well as relative geopolitical security due to American security guarantees (Chart 17). Chart 17Australia: GeoRisk Indicator

Australia: GeoRisk Indicator

Australia: GeoRisk Indicator

Bottom Line: China’s reversion to autocracy will keep global sentiment negative on Chinese equities until 2023 at earliest. Stay short the renminbi and Taiwanese dollar. Favor the Japanese yen over the Korean won. Favor South Korean over Taiwanese equities. Look favorably on the Australian dollar. Turkey, South Africa, And … Canada Turkish geopolitical risk will remain elevated in the context of a rampant Russia, NATO’s revival and tensions with Russia, the threat of commerce destruction and accidents in the Black Sea region, domestic economic mismanagement, foreign military adventures, and the threat posed to the aging Erdogan regime by the political opposition in the wake of the pandemic and the lead-up to the 2023 elections (Chart 18). Chart 18Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

While we are tactically bullish on South African equities and currency, we expect South African political risk to rise steadily into the 2024 general election. Almost a year has passed since the civil unrest episode of 2021. Covid-19 lockdowns have been lifted and the national state of disaster has ended, which has helped quell social tensions. This is evident in the decline of our South Africa GeoRisk indicator from 2021 highs (Chart 19). While fiscal austerity is under way in South Africa, we have argued that fiscal policy will reverse course in time for the 2024 election. In this year’s fiscal budget, the budget deficit is projected to narrow from -6% to -4.2% over the next two years. Government has increased tax revenue collection through structural reforms that are rooting out corruption and wasteful expenditure. But the ANC will have to tap into government spending to shore up lost support come 2024. Thus South Africa benefits tactically from commodity prices but cyclically the currency is vulnerable. Chart 19South Africa: GeoRisk Indicator

South Africa: GeoRisk Indicator

South Africa: GeoRisk Indicator

Canadian political risk will rise but that should not deter investors from favoring Canadian assets that are not exposed to the property bubble. Prime Minister Justin Trudeau has had a net negative approval rating since early 2021 and his government is losing political capital due to inflation, social unrest, and rising difficulties with housing affordability (Chart 20). While he does not face an election until 2025, the Conservative Party is developing more effective messaging. Chart 20Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

India Will Stay Neutral But Lean Toward The West Chart 21Sino-Pak Alliance’s Geopolitical Power Is Thrice That Of India

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

US President Joe Biden has openly expressed his administration’s displeasure regarding India’s response to Russia’s invasion of Ukraine. This has led many to question the strength of Indo-US relations and the direction of India’s geopolitical alignments. To complicate matters, China’s overtures towards India have turned positive lately, leading clients to ask if a realignment in Indo-China relations is nigh. To accurately assess India’s long-term geopolitical propensities, it is important to draw a distinction between ‘cyclical’ and ‘structural’ dynamics that are at play today. Such a distinction yields crystal-clear answers about India’s strategic geopolitical leanings. In specific: Indo-US Relations Will Strengthen On A Strategic Horizon: As the US’s and China’s grand strategies collide, minor and major geopolitical earthquakes are bound to take place in South Asia and the Indo-Pacific. Against this backdrop, India will strategically align with the US to strengthen its hand in the region (Chart 21). While the Russo-Ukrainian war is a major global geopolitical event, for India this is a side-show at best. True, India will retain aspects of its historic good relations with Russia. Yet countering China’s encirclement of India is a far more fundamental concern for India. Since Russia has broken with Europe, and China cannot reject Russia’s alliance, India will gradually align with the US and its allies. India And China Will End Up As A Conflicting Dyad: Strategic conflict between the two Asian powers is likely because China’s naval development and its Eurasian strategy threaten India’s national security and geopolitical imperatives, while India’s alliances are adding to China’s distrust of India. Thus any improvement in Sino-Indian diplomatic relations will be short-lived. The US will constantly provide leeway for India in its attempts to court India as a key player in the containment strategy against China. The US and its allies are the premier maritime powers and upholders of the liberal world order – India serves its national interest better by joining them rather than joining China in a risky attempt to confront the US navy and revolutionize the world order. Indo-Russian Relations Are Bound To Fade In The Long Run: India will lean towards the US over the next few years for reasons of security and economics. But India’s movement into America’s sphere of influence will be slow – and that is by design. India is testing waters with America through networks like the Quadrilateral Dialogue. It sees its historic relationship with Russia as a matter of necessity in the short run and a useful diversification strategy in the long run. True, India will maintain a trading relationship with Russia for defense goods and cheap oil. But this trade will be transactional and is not reason enough for India to join Russia and China in opposing US global leadership. While these factors will mean that Indo-Russian relations are amicable over a cyclical horizon, this relationship is bound to fade over a strategic horizon as China and Russia grow closer and the US pursues its grand strategy of countering China and Russia. Bottom Line: India may appear to be neutral about the Russo-Ukrainian war but India will shed its historical stance of neutrality and veer towards America’s sphere of influence on a strategic timeframe. India is fully aware of its strategic importance to both the American camp and the Russo-Chinese camp. It thus has the luxury of making its leanings explicit after extracting most from both sides. Long Brazil / Short India Brazil’s equity markets have been on a tear. MSCI Brazil has outperformed MSCI EM by 49% in 2022 YTD. Brazil’s markets have done well because Brazil is a commodity exporter and the war in Ukraine has little bearing on faraway Latin America. This rally will have legs although Brazil’s political risks will likely pick back up in advance of the election (Chart 22). The reduction in Brazil’s geopolitical risk so far this year has been driven mainly by the fact that the currency has bounced on the surge in commodity prices. In addition, former President Lula da Silva is the current favorite to win the 2022 presidential elections – Lula is a known quantity and not repugnant to global financial institutions (Chart 23). Chart 22Brazil's Markets Have Benefitted From Rising Commodity Prices

Brazil's Markets Have Benefitted From Rising Commodity Prices

Brazil's Markets Have Benefitted From Rising Commodity Prices

Chart 23Brazil: Watch Out For Political Impact Of Commodity Prices

Brazil: Watch Out For Political Impact Of Commodity Prices

Brazil: Watch Out For Political Impact Of Commodity Prices

Whilst there is no denying that the first-round effects of the Ukraine war have been positive for Brazil, there is a need to watch out for the second-round effects of the war as Latin America’s largest economy heads towards elections. Surging prices will affect two key constituencies in Brazil: consumers and farmers. Consumer price inflation in Brazil has been ascendant and adding to Brazil’s median voter’s economic miseries. Rising inflation will thus undermine President Jair Bolsonaro’s re-election prospects further. The fact that energy prices are a potent polling issue is evinced by the fact that Bolsonaro recently sacked the chief executive of Petrobras (i.e. Brazil’s largest listed company) over rising fuel costs. Furthermore, Brazil is a leading exporter of farm produce and hence also a large importer of fertilizers. Fertilizer prices have surged since the war broke out. This is problematic for Brazil since Russia and Belarus account for a lion’s share of Brazil’s fertilizer imports. Much like inflation in general, the surge in fertilizer prices will affect the elections because some of the regions that support Bolsonaro also happen to be regions whose reliance on agriculture is meaningful (Map 1). They will suffer from higher input prices. Map 1States That Supported Bolso, Could Be Affected By Fertilizer Price Surge

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

Chart 24Long Brazil Financials / Short India

Long Brazil Financials / Short India

Long Brazil Financials / Short India

Given that Bolsonaro continues to lag Lula on popularity ratings – and given the adverse effect that higher commodity prices will have on Brazil’s voters – we expect Bolsonaro to resort to fiscal populism or attacks on Brazil’s institutions in a last-ditch effort to cling to power. He could even be emboldened by the fact that Sérgio Moro, the former judge and corruption fighter, decided to pull out of the presidential race. This could provide a fillip to Bolso’s popularity. Bottom Line: Brazil currently offers a buying opportunity owing to attractive valuations and high commodity prices. But investors should stay wary of latent political risks in Brazil, which could manifest themselves as presidential elections draw closer. We urge investors to take-on only selective tactical exposure in Brazil for now. Equities appear cheap but political and macro risks abound. To play the rally yet stave off political risk, we suggest a tactical pair trade: Long Brazil Financials / Short India (Chart 24). Whilst we remain constructive on India on a strategic horizon, for the next 12 months we worry about near-term macro and geopolitical headwinds as well as India’s rich valuations. Don’t Buy Into Pakistan’s Government Change Chart 25Pakistan’s Military Is Unusually Influential

Le Pen And Other Hurdles (GeoRisk Update)

Le Pen And Other Hurdles (GeoRisk Update)

The newest phase in Pakistan’s endless cycle of political instability has begun. Prime Minister Imran Khan has been ousted. A new coalition government and a new prime minister, Shehbaz Sharif, have assumed power. Prime Minister Sharif’s appointment may make it appear like risks imposed by Pakistan have abated. After all, Sharif is seen as a good administrator and has signaled an interest in mending ties with India. But despite the appearance of a regime change, geopolitical risks imposed by Pakistan remain intact for three sets of reasons: Military Is Still In Charge: Pakistan’s military has been and remains the primary power center in the country (Chart 25). Former Prime Minister Khan’s rise to power was possible owing to the military’s support and he fell for the same reason. Since the military influences the civil administration as well as foreign policy, a lasting improvement in Indo-Pak relations is highly unlikely. Risk Of “Rally Round The Flag” Diversion: General elections are due in Pakistan by October 2023. Sharif is acutely aware of the stiff competition he will face at these elections. His competitors exist outside as well as inside his government. One such contender is Bilawal Bhutto-Zardari of the Pakistan People’s Party (PPP), which is a key coalition partner of the new government that assumed power. Imran Khan himself is still popular and will plot to return to power. Against such a backdrop the newly elected PM is highly unlikely to pursue an improvement in Indo-Pak relations. Such a strategy will adversely affect his popularity and may also upset the military. Hence we highlight the risk of the February 2021 Indo-Pak ceasefire being violated in the run up to Pakistan’s general elections. India’s government has no reason to prevent tensions, given its own political calculations and the benefits of nationalism. Internal Social Instability Poor: Pakistan is young but the country can be likened to a social tinderbox. Many poor youths, a weak economy, and inadequate political valves to release social tensions make for an explosive combination. Pakistan remains a source of geopolitical risk for the South Asian region. Some clients have inquired as to whether the change of government in Pakistan implies closer relations with the United States. The US has less need for Pakistan now that it has withdrawn from Afghanistan. It is focused on countering Russia and China. As such the US has great need of courting India and less need of courting Pakistan. Pakistan will remain China’s ally and will struggle to retain significant US assistance. Bottom Line: We remain strategic sellers of Pakistani equities. Pakistan must contend with high internal social instability, a weak democracy, a weak economy and an unusually influential military. As long as the military remains excessively influential in Pakistan, its foreign policy stance towards India will stay hostile. Yet the military will remain influential because Pakistan exists in a permanent geopolitical competition with India. And until Pakistan’s economy improves structurally and endemically, its alliance with China will stay strong. Investment Takeaways Cyclically go long US 10-year Treasuries. Geopolitical risks are historically high and rising but complacency is returning to markets. Meanwhile inflation is nearing a cyclical peak. Favor US stocks over global. It is too soon to go long euro or European assets, especially emerging Europe. Favor UK equities over developed markets (excluding the US). Stay long GBP-CZK. Favor European defense stocks over European tech. Stay short the Chinese renminbi and Taiwanese dollar. Favor the Japanese yen over the Korean won. Favor South Korean over Taiwanese equities. Matt Gertken Chief Geopolitical Strategist mattg@bcaresearch.com Ritika Mankar, CFA Editor/Strategist ritika.mankar@bcaresearch.com Jesse Anak Kuri Associate Editor Jesse.Kuri@bcaresearch.com Yushu Ma Research Analyst yushu.ma@bcaresearch.com Guy Russell Senior Analyst GuyR@bcaresearch.com Alice Brocheux Research Associate alice.brocheux@bcaresearch.com Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Regional Geopolitical Risk Matrix Section III: Geopolitical Calendar

Executive Summary The structural downtrend in Chinese bond yields has a lot further to go, because it is helping to let the air out gently of stratospheric valuations in the real estate sector, and thereby preventing a hard landing for the Chinese economy. In the US, flagging mortgage and housing market activity is weighing on an already slowing economy. Buy US T-bonds. The long T-bond yield is close to a peak. Switch equity exposure into long-duration sectors such as healthcare and biotech. Go overweight US homebuilders versus US insurers. The peak in bond yields will also take pressure off US homebuilder shares whose recent collapse has been the mirror-image of the surge in the 30-year mortgage rate. Fractal trading watchlist: Basic resources; Switzerland versus Germany; and USD/EUR. The Collapse In US Homebuilder Shares Is The Mirror-Image Of The Surge In The Mortgage Rate

The Collapse In US Homebuilder Shares Is The Mirror-Image Of The Surge In The Mortgage Rate

The Collapse In US Homebuilder Shares Is The Mirror-Image Of The Surge In The Mortgage Rate

Bottom Line: The global bond yield cannot rise much further before it destabilises the $350 trillion global real estate market and thereby destabilises the global economy. Feature Quietly and largely unnoticed, Chinese long-dated bond yields have been drifting lower (Chart I-1 and Chart I-2). At a time that surging bond yields elsewhere in the world have grabbed all the attention, the largely unnoticed contrarian move in Chinese bond yields through the past year is significant because of something else that has gone largely unnoticed: Chinese real estate has become by far the largest asset-class in the world, worth $100 trillion.1 Chart I-1The Contrarian Downdrift In The Chinese 30-Year Bond Yield

The Contrarian Downdrift In The Chinese 30-Year Bond Yield

The Contrarian Downdrift In The Chinese 30-Year Bond Yield

Chart I-2The Contrarian Downdrift In The Chinese 10-Year Bond Yield

The Contrarian Downdrift In The Chinese 10-Year Bond Yield

The Contrarian Downdrift In The Chinese 10-Year Bond Yield

Chinese Real Estate Is Trading On A Stratospheric Valuation The $100 trillion valuation of Chinese real estate market is greater than the $90 trillion global economy, is more than twice the size of the $45 trillion US real estate market and the $45 trillion US stock market, and dwarfs the $18 trillion Chinese economy. Suffice to say, Chinese real estate’s pre-eminence as the world’s largest asset-class is mostly due to its stratospheric valuation. Prime residential rental yields in Guangzhou, Shanghai, Hangzhou, Shenzhen and Beijing have collapsed to 1.5 percent, the lowest rental yields in the world and less than half the global average of 3 percent. Versus rents therefore, Chinese real estate is now twice as expensive as in the rest of the world (Chart I-3). Chart I-3Versus Rents, Chinese Real Estate Is The Most Expensive In The World

$350 Trillion Of Global Real Estate Can’t Swallow Higher Bond Yields

$350 Trillion Of Global Real Estate Can’t Swallow Higher Bond Yields

To corroborate this point, while the US real asset market is worth around two times US annual GDP, the Chinese real estate market is worth more than five times China’s annual GDP! The structural downtrend in Chinese bond yields has a lot further to go. Crucially, the downward drift in Chinese bond yields is alleviating some of the pressure on the extremely highly valued Chinese real estate market – as it helps to let the air out gently of the stratospheric valuations, and thereby avoid a hard landing for the Chinese economy. Hence, the structural downtrend in Chinese bond yields has a lot further to go. The Surge In US Mortgage Rates Is Taking Its Toll Meanwhile, in the rest of the world, the surge in bond yields poses a major threat to the decade long housing boom. Versus rents, US house prices are the most expensive ever – more expensive even than during the early 2000s so-called ‘housing bubble’. For the first time since 2008, the US 30-year mortgage rate is higher than the prime residential rental yield. Until recently, the historically low rental yield on US real estate was justified by an extremely low bond yield. But the recent surge in the bond yield has changed all that. For the first time since 2008, the US 30-year mortgage rate is higher than the prime residential rental yield2 (Chart I-4). Chart I-4The US 30-Year Mortgage Rate Is Now Higher Than The Prime Residential Rental Yield

The US 30-Year Mortgage Rate Is Now Higher Than The Prime Residential Rental Yield

The US 30-Year Mortgage Rate Is Now Higher Than The Prime Residential Rental Yield

The surge in US mortgage rates is taking its toll. Since the end of January, US mortgage applications for home purchase have fallen by almost a fifth (Chart I-5), and the lower demand for home purchase mortgages is starting to weigh on home construction (Chart I-6). Building permits for new private housing units were already falling in February, but a more up-to-date sign of the pain is the 35 percent collapse in US homebuilder shares. Chart I-5US Mortgage Applications For Home Purchase Have Fallen By Almost A Fifth

US Mortgage Applications For Home Purchase Have Fallen By Almost A Fifth

US Mortgage Applications For Home Purchase Have Fallen By Almost A Fifth

Chart I-6The Lower Demand For Home Purchase Mortgages Is Starting To Weigh On Home Construction

The Lower Demand For Home Purchase Mortgages Is Starting To Weigh On Home Construction

The Lower Demand For Home Purchase Mortgages Is Starting To Weigh On Home Construction

$350 Trillion Of Global Real Estate Can’t Swallow Higher Bond Yields Mortgage rates drive real estate rental yields because of the arbitrage between buying versus renting a similar home. Given a fixed annual budget for housing, I must choose between how much home I can buy – which depends on the mortgage rate, versus how much home I can rent – which depends on the rental yield. The arbitrage should make me indifferent between the two options. As a simple example of this arbitrage, let’s assume my annual budget for housing is $10k, and both the mortgage rate and rental yield are 4 percent. I will be indifferent between spending the $10k on interest on a $250k mortgage loan to buy the home, or spending the $10k to rent a similar $250k home. If the mortgage rate rises to 5 percent, then the maximum loan that my $10k of interest payment will afford me falls to $200k, reducing my maximum bid to buy the home. If I am the marginal bidder, then the home price will fall to $200k, so that the $10k rent on the similar valued home will also equate to a higher rental yield of 5 percent. In practice, the simple arbitrage described above is complicated by several factors: the maximum loan-to-value that a lender will offer on the home; the different transaction costs of buying versus renting; and the fact that people prefer to buy than to rent because buying a home is an investment which also provides a consumption service – shelter, whereas renting a home only provides the consumption service. Nevertheless, these complications do not diminish the overarching connection between mortgage rates and rental yields. The lion’s share of the real estate boom has come from a massive valuation uplift, which in turn has come from structurally lower bond yields. All of which brings us to the decade long global real estate boom that has doubled the value of global real estate market to an eye-watering $350 trillion, four times the size of the $90 trillion global economy. During this unprecedented boom, global rents have risen by 40 percent, tracking world nominal GDP, as they should. This means that the lion’s share of the real estate boom has come from a massive valuation uplift, which in turn has come from structurally lower bond yields (Chart I-7). Chart I-7The Lion's Share Of The Global Real Estate Boom Has Come From A Massive Uplift In Valuations

The Lion's Share Of The Global Real Estate Boom Has Come From A Massive Uplift In Valuations

The Lion's Share Of The Global Real Estate Boom Has Come From A Massive Uplift In Valuations

Since the global financial crisis, there has been an excellent empirical relationship between the global long-dated bond yield (US/China average) and the global rental yield. The important takeaway is that the global bond yield cannot rise much further before it destabilises the $350 trillion global real estate market and thereby destabilises the global economy (Chart I-8). Chart I-8The Global Bond Yield Cannot Rise Much Further Before It Destabilises The $350 Trillion Global Real Estate Market

The Global Bond Yield Cannot Rise Much Further Before It Destabilises The $350 Trillion Global Real Estate Market

The Global Bond Yield Cannot Rise Much Further Before It Destabilises The $350 Trillion Global Real Estate Market

Some Investment Conclusions The good news is that the recent rise in the global bond yield has been limited by the downdrift in Chinese bond yields. Given the massive overvaluation of Chinese real estate, the structural downtrend in Chinese bond yields has a lot further to go. Meanwhile in the US, unless bond yields back down quickly, flagging mortgage and housing market activity will weigh on an already slowing economy. If US bond yields don’t back down quickly, the feedback from consequent slowdown in the economy will ultimately bring yields down anyway. As I explained last week in Fat-Tailed Inflation Signals A Peak In Bond Yields I do expect the long T-bond yield to back down relatively quickly. The sharp drop in US core inflation to just 0.3 percent month-on-month in March signals that inflation is peaking. Hence, medium to long term investors should be buying US T-bonds, and switching equity exposure into long-duration sectors such as healthcare and biotech. Finally, a peak in bond yields will also take pressure off US homebuilder shares whose recent collapse has been the mirror-image of the surge in the 30-year mortgage rate (Chart I-9). Hence, go overweight US homebuilders versus US insurers. Chart I-9The Collapse In US Homebuilder Shares Is The Mirror-Image Of The Surge In The Mortgage Rate

The Collapse In US Homebuilder Shares Is The Mirror-Image Of The Surge In The Mortgage Rate

The Collapse In US Homebuilder Shares Is The Mirror-Image Of The Surge In The Mortgage Rate

Fractal Trading Watchlist Given that inflation hedging investment demand has driven at least part of the strong rally in basic resources, a peak in inflation and bond yields threatens to unwind the recent outperformance of basic resources shares. This is corroborated by the extremely fragile 130-day fractal structure (Chart I-10). Accordingly, the recommended trade is to short basic resources (GNR) versus the broad market, setting the profit target and symmetrical stop-loss at 11.5 percent. This week we are also adding to our watchlist: Switzerland versus Germany; and USD/EUR. The full list of 20 investments that are experiencing or approaching turning points is available on our website: cpt.bcaresearch.com Chart I-10The Outperformance Of Basic Resources Is Vulnerable To Reversal

The Outperformance Of Basic Resources Is Vulnerable To Reversal

The Outperformance Of Basic Resources Is Vulnerable To Reversal

Switzerland's Outperformance Vs. Germany Could End

Switzerland's Outperformance Vs. Germany Could End

Switzerland's Outperformance Vs. Germany Could End

The Rally In USD/EUR Could End

The Rally In USD/EUR Could End

The Rally In USD/EUR Could End

Chart 1The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

Chart 2The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

Chart 3AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

Chart 4Canada Versus Japan Is Vulnerable To Reversal

Canada Versus Japan Is Vulnerable To Reversal

Canada Versus Japan Is Vulnerable To Reversal

Chart 5Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Chart 6US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

Chart 7Bitcoin's 65-Day Fractal Support Is Holding For Now

Bitcoin's 65-Day Fractal Support Is Holding For Now

Bitcoin's 65-Day Fractal Support Is Holding For Now

Chart 8A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Chart 9Biotech Is A Major Buy

Biotech Is A Major Buy

Biotech Is A Major Buy

Chart 10CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

Chart 11Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Chart 12Norway's Outperformance Could End

Norway's Outperformance Could End

Norway's Outperformance Could End

Chart 13Greece's Brief Outperformance To End

Greece's Brief Outperformance To End

Greece's Brief Outperformance To End

Chart 14BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

Chart 15The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

Chart 16The Outperformance Of Resources Versus Biotech Is Vulnerable To Reversal

The Outperformance Of Resources Versus Biotech Is Vulnerable To Reversal

The Outperformance Of Resources Versus Biotech Is Vulnerable To Reversal

Chart 17Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Chart 18US Homebuilders' Underperformance Is At A Potential Turning Point

US Homebuilders' Underperformance Is At A Potential Turning Point

US Homebuilders' Underperformance Is At A Potential Turning Point

Chart 19Fractal Trading Watch List

Fractal Trading Watch List

Fractal Trading Watch List

Chart 20Fractal Trading Watch List

Fractal Trading Watch List

Fractal Trading Watch List

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 We estimate the value of Chinese real estate at the end of 2021 to be $97 trillion, comprising residential $85 trillion, commercial $6 trillion, and agricultural $6 trillion. The source is: the Savills September 2021 report ‘The total value of global real estate’, which valued the global real estate market to the end of 2020; and the February 2022 report ‘Savills Prime Residential Index: World Cities’ which allowed us to update the valuations to the end of 2021. 2 The US prime residential rental yield is the simple average of the prime residential rental yields in New York, Miami, Los Angeles and San Francisco. Source: Savills. Fractal Trading System Fractal Trades

$350 Trillion Of Global Real Estate Can’t Swallow Higher Bond Yields

$350 Trillion Of Global Real Estate Can’t Swallow Higher Bond Yields

$350 Trillion Of Global Real Estate Can’t Swallow Higher Bond Yields

$350 Trillion Of Global Real Estate Can’t Swallow Higher Bond Yields

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-5Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Results of the first round of the French presidential election show France’s centrist President Emmanuel Macron ahead with 28% of the votes, while far-right challenger Marine Le Pen captured second place with 23% of the votes. The two are now heading for a…

Executive Summary From Net Borrower To Net Lenders

From Net Borrower To Net Lenders

From Net Borrower To Net Lenders

Yields are rising across Europe. Peripheral spreads are unlikely to experience the same violent widening as last decade. Europe now has a buyer of last resort. Italy and Spain have moved from current account deficit to current account surplus nations. However, Italy and Spain are not conducting the kind of structural reforms necessary to cause public debt-to-GDP ratios to fall back below the Maastricht Treaty criteria. Nonetheless, based on our stress tests, Italian and Spanish yields can rise significantly more before debt-servicing costs become a major problem in these nations. Economic activity, not Spanish or Italian public finances, is the true constraint on European yields. Bottom Line: German yields can rise above 2% without causing a public finance crisis in Italy and Spain. To reach this level, however, nominal growth in Europe must remain robust. As a result, any pullback in yields caused by oversold conditions in the bond market will be temporary. Year-to-date, German 10-year yields have risen more than 80bps, while spreads have widened in the periphery. This has supercharged the interest rate moves: Italian BTP yields and Spanish Bono yields are up nearly 120bps and 110bps, respectively. As a result, Italian government bonds now offer a 2.4% yield, a level not experienced durably since the first half of 2019. Meanwhile, Spanish yields are close to 1.7%—their highest levels since 2017. Investors are increasingly concerned by the damage levied by higher yields in Southern Europe. Since 2018, Italian public debt has risen by 32% of GDP to 170% of GDP, and Spanish public debt has risen by 28% of GDP to 138% of GDP. These higher debt burdens beg the following question: How high can European yields rise before a new sovereign debt crisis engulfs the Eurozone? Private sector financial balances and the balance of payments in the periphery are now very different from what they were between 2008 and 2012. As a result, the odds of a similar crisis are much lower than last decade, which should allow German yields to rise further in the coming years. Italy and Spain have moved on from experiencing an EM-style balance of payment crisis with explosive debt market dynamics. They are now stuck in a Japanese scenario of excess private sector savings and low economic growth. “This Time Is Different” These might be the four most dangerous words in finance, but understanding the differences between the present situation and the sovereign debt crisis is essential to assessing the impact of higher yields on Italian and Spanish public finances. Chart 1From Net Borrower To Net Lenders

From Net Borrower To Net Lenders

From Net Borrower To Net Lenders

The most important transformation in the Southern European economies is the rise in private sector savings. From 1999 to 2013, Italy’s private sector financial balance averaged 2.2% of GDP. Constant government deficits resulted in a significant national dissaving, forcing the country to borrow from abroad as expressed by a current account deficit that lasted from 2000 to 2013 (Chart 1, top panel). At the present moment, Italy’s current account is in a surplus equal to 3.5% of GDP, as private savings stand at 13% of GDP, up from 5% before COVID-19. The change is even more dramatic in Spain. The Spanish private sector financial balance was in a large deficit from 1999 to 2008, which averaged 5.6% of GDP and reached a nadir of 11.3% of GDP in 2007. As a result, Spain relied on foreign lending between 1980 and 2012, with a current account deficit that averaged 3% of GDP over that period (Chart 1, second panel). The switch from the status of foreign borrower to the status of surplus nation is fundamental. A country where excess private savings are so abundant they can finance large public deficits and still generate current account surpluses will experience more limited pressure on borrowing costs than a country that needs to borrow from abroad. Japan is a perfect example. Elevated public borrowing ends up being a vehicle to absorb private sector excess savings and does not constitute profligacy. Despite higher debt loads, Italy’s public finances seem more sustainable than those of Spain. The International Monetary Fund’s (IMF) October 2021 Fiscal Monitor forecast shows the Italian primary budget balance, both on an absolute basis and on a cyclically-adjusted basis, moving from -6% and -2.9% of GDP, respectively, closer to zero by 2026 (Chart 2). In Spain, primary budget balances, both on an absolute basis and on a cyclically-adjusted basis, are anticipated to improve from -8.9% and -3.4% of GDP, respectively, to -2.5% of GDP by 2026. Despite these deficits, the IMF also expects public debt to decrease by 10% of GDP to 146% in Italy and to remain flat at 120% of GDP in Spain (Chart 3). Importantly, in both cases, the upward pressure on public debt will be limited over the next five years because private savings are already high and unlikely to rise further. Chart 2Public Deficits Will Narrow Further

Public Deficits Will Narrow Further

Public Deficits Will Narrow Further

Chart 3Debt Will Stay High, So Will Private Savings

Debt Will Stay High, So Will Private Savings

Debt Will Stay High, So Will Private Savings