Euro Area

Executive Summary Ebbing Stagflation Fear Will Prompt Rerating

Ebbing Stagflation Fear Will Prompt Rerating

Ebbing Stagflation Fear Will Prompt Rerating

European inflation will rise further before peaking this summer. Core CPI will reach between 2.8% and 3.2% by year-end before receding. The combination of stabilizing growth and the eventual peak in inflation will cause stagflation fears to recede. European assets have greater upside. Cyclicals, small-caps, and financials will be major beneficiaries of declining stagflation fears. The underperformance of UK small-cap stocks is nearing its end. UK large-cap equities are a tactical sell against Eurozone and Swedish shares. TACTICAL INCEPTION DATE RETURN SINCE INCEPTION (%) COMMENT EQUITIES Buy European & Swedish Equities / Sell UK Large Caps Stocks 03/21/2022 Bottom Line: Stagflation fears are near an apex as commodity inflation recedes. A peak in these fears will allow European asset prices to perform strongly over the coming quarters. Despite a glimmer of hope that Ukraine and Russia may find a diplomatic end to the war, the reality on the ground is that the conflict has intensified. Although the hostilities are worsening and the European Central Bank (ECB) surprised the markets with its hawkish tone, European assets have begun to catch a bid. The crucial question for investors is whether this rebound constitutes a new trend or a counter-trend move? Our view about Europe is optimistic right now. The path is not a direct line upward. The recent optimism about the outcome of the Russia-Ukraine talks is premature; however, we are getting to the point when markets are becoming desensitized to the war and energy prices are losing steam. Moreover, the increasing number of statements by Chinese economic authorities pointing toward greater stimulus and support to alleviate the pain created by China’s stringent zero-COVID policy are another positive omen. Higher Inflation For Some Time European headline inflation is set to exceed 7% this summer and core CPI will increase between 2.8% and 3.2% by the end of 2022. Related Report European Investment StrategySpring Stagflation The main force that will push inflation higher in Europe remains commodity prices. Energy inflation is extremely strong at already 32% per annum (Chart 1). It will increase further because of both the recent jump in Brent prices to EUR122/bbl on March 8 and the upsurge in natural gas prices, which were as high as EUR212/MWh on the same day before settling to EUR106/MWh last Friday. The impact of energy prices will not be limited to headline inflation and will filter through to core CPI (Chart 1, bottom panel). The average monthly percentage change in the Eurozone core CPI inflation stands at 0.25% for the past six months (compared to an average of 0.09% over the past ten years), or the period when energy-prices inflation has been the strongest. Assuming monthly inflation remains at such an elevated level, annual core CPI will hit 3.3% in the Eurozone by the end of 2022 (Chart 2). Chart 2Core CPI to Rise Further

Core CPI to Rise Further

Core CPI to Rise Further

Chart 1Energy Inflation: Alive And Well

Energy Inflation: Alive And Well

Energy Inflation: Alive And Well

The picture is not entirely bleak. Many forces suggest that these inflationary forces will recede before year-end in Europe. Energy prices are peaking, which is consistent with a diminishing inflationary impulse from that space. We showed two weeks ago that the massive backwardation of oil curves, the heavy bullish sentiment, and the high level of risk-reversals were consistent with a severe but transitory adjustment in the energy market. Oil markets will experience further volatility, as uncertainty around peace/ceasefire negotiations continues to evolve in Ukraine. Nonetheless, the peak in energy prices has most likely been reached. BCA’s energy strategists expect Brent to average $93/bbl in 2022 and in 2023. The potential for a decline in headline CPI after the summer is not limited to energy prices. Dramatic moves in the commodity market, from metals to agricultural resources, have made headlines. Yet, the rate of change of commodity prices is decelerating, hence, the commodity impulse to inflation is slowing sharply. As Chart 3 shows, this is a harbinger of a slowdown in European headline CPI. Related Report European Investment StrategyFallout From Ukraine Looking beyond commodity markets, the recent deceleration in European economic activity also suggests weaker inflation in the latter half of 2022. Germany will likely suffer a recession because it already registered a negative GDP growth in Q4 2021. Q1 2022 growth will be even worse because of the country’s high exposure to both China and fossil fuel prices. More broadly, the recent deceleration in the rate of change of both the manufacturing and services PMIs is consistent with an imminent peak in the second derivative of goods and services CPI (Chart 4). Chart 3Commodity Impulse Is Peaking

Commodity Impulse Is Peaking

Commodity Impulse Is Peaking

Chart 4Inflation's Maximum Momentum Is Now

Inflation's Maximum Momentum Is Now

Inflation's Maximum Momentum Is Now

Underlying drivers of inflation also remain tame in Europe. European negotiated wages are only expanding at a 1.5% annual rate, which translates into unit labor costs growth of 1% (Chart 5). This contrast with the US, where wages are expanding at a 4.3% annual rate. A peak in inflation, however, does not mean that CPI readings will fall below the ECB’s 2% threshold anytime soon. The European economy continues to face supply shortages that the Ukrainian conflict exacerbates (Chart 6). Moreover, the recent wave of COVID-19 in China increases the risk of disruptions in supply chains, as highlighted by the closure of Foxconn factories in Shenzhen. Finally, inflation has yet to peak; mathematically, it will take a long time before it falls back below levels targeted by Frankfurt. Chart 5The European Labor Market Is Not Inflationary

The European Labor Market Is Not Inflationary

The European Labor Market Is Not Inflationary

Chart 6Not Blemish-Free

Not Blemish-Free

Not Blemish-Free

Bottom Line: European headline inflation will peak this summer, probably above 7%. Additionally, core CPI is likely to reach between 2.8% and 3.2% in the second half of 2022. As a result of a decline in the commodity impulse, inflation will decelerate afterward, but it will remain above the ECB’s 2% target for most of 2023. Hopes For Growth Two weeks ago, we wrote that Europe was facing a stagflation episode in the coming one to two quarters, but that, ultimately, economic activity will recover well. Recent evidence confirms that assessment. Chart 7A Coming Chinese Tailwind?

A Coming Chinese Tailwind?

A Coming Chinese Tailwind?

The tone of Chinese policymakers is becoming more aggressive, in favor of supporting the economy. On March 16, Vice-Premier Liu He highlighted that Beijing was readying to support property and tech shares and that it will do more to stimulate the economy. True, this response was made in part to address the need to close cities affected by the sudden spike of Omicron cases around China. Nonetheless, the global experience with Omicron demonstrates that, as spectacular and violent the surge in cases may be, it is short-lived. Meanwhile, the impact of stimulus filters through the economy over many months. As a result, Europe will experience the impact of China’s Omicron-induced slowdown, while it also suffers from the growth-sapping effects of the Ukrainian conflict; however, it will also enjoy the positive effect on growth of a rising credit impulse over several subsequent quarters (Chart 7). Beyond China, the other themes we have discussed in recent weeks remain valid. First, European fiscal policy will become looser, as governments prepare to fight the slowdown caused by the war, while also increasing infrastructure spending to wean Europe off Russian energy. Moreover, European military spending is well below NATO’s 2% objective. This will not remain the case, as military expenditure may leap from less than EUR100bn per year to nearly EUR400bn per year over the coming decade. Second, European spending on consumer durable goods still lags well behind the trajectory of the US. With the energy drag at its apex today, consumer spending on durable goods will be able to catch up in the latter half of the year, especially with the household savings rate standing at 15% or 2.5 percentage points above its pre-COVID level. Bottom Line: European growth will be very low in the coming quarters. Germany is likely to face a technical recession as Q1 2022 data filters in. Nonetheless, Chinese stimulus, European fiscal support, pent-up demand, and a declining energy drag will allow growth to recover in the latter half of the year. As a result, we agree with the European Commission estimates that European growth will slow markedly this year. Market Implications In the context of a transitory shock to European economic activity and a coming peak in inflation, European stock prices have likely bottomed. Chart 8Depressed Sentiment To Help Beta

Depressed Sentiment To Help Beta

Depressed Sentiment To Help Beta

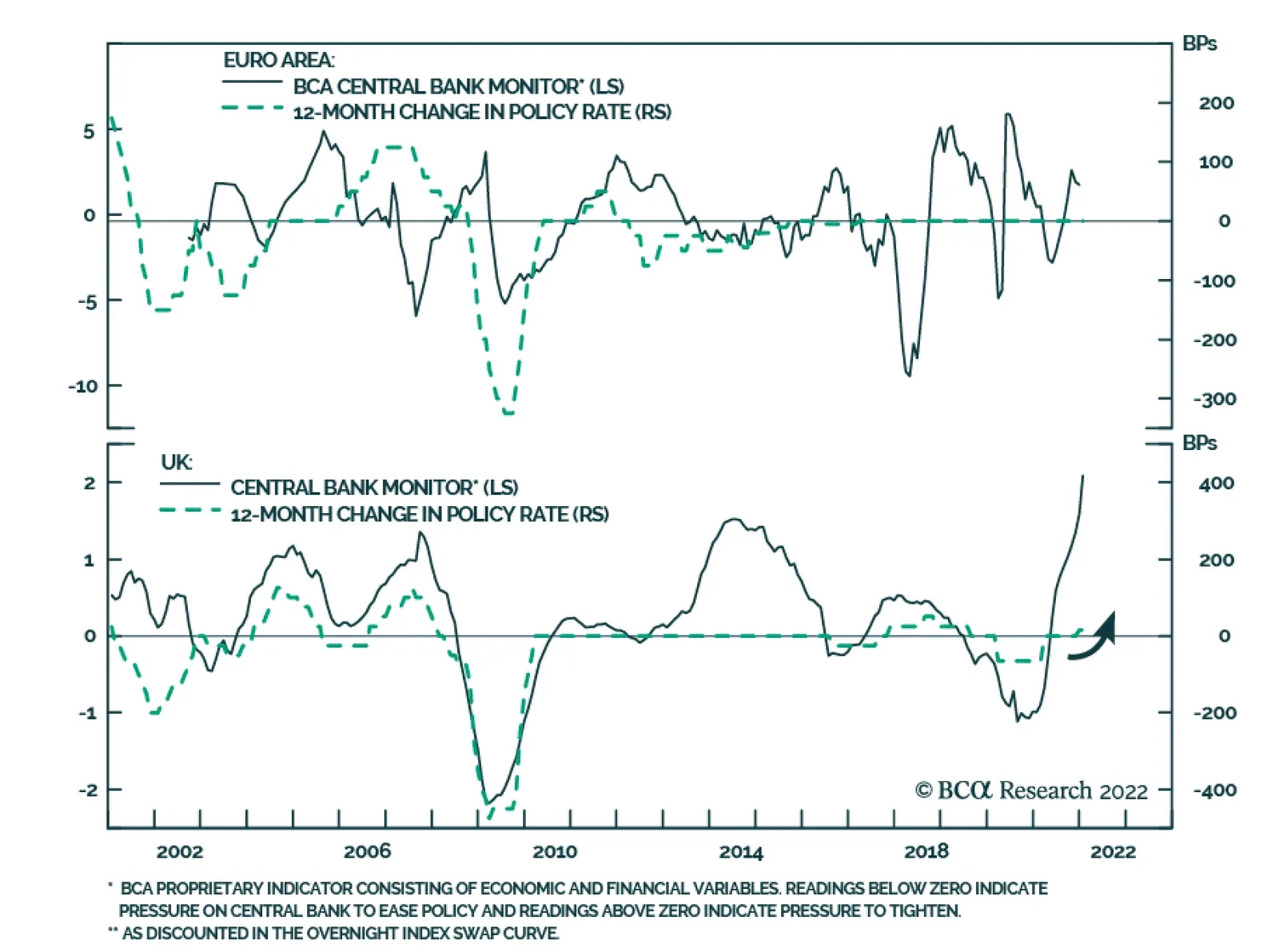

Sentiment has reached levels normally linked with a durable market floor. The NAAIM Exposure Index has fallen to a point from which global markets often recover. Europe’s high beta nature increases the odds that European equities will greatly benefit in that context (Chart 8). Valuations confirm that sentiment toward European assets has reached a capitulation stage. The annual rate of change of the earnings yields in the earnings yields has hit 73%, which is consistent with a market bottom (Chart 9). More importantly, the change in European forward P/E tracks closely our European Stagflation Sentiment Proxy (ESSP), based on the difference between the Growth and Inflation Expectations’ components of the ZEW survey (Chart 10). For now, our ESSP indicates that stagflation fears in Europe have never been so widespread, but these fears will likely dissipate as energy inflation declines. This process will lift European earnings multiples. Chart 9Bad News Discounted?

Bad News Discounted?

Bad News Discounted?

Chart 10Ebbing Stagflation Fear Will Prompt Rerating

Ebbing Stagflation Fear Will Prompt Rerating

Ebbing Stagflation Fear Will Prompt Rerating

Earnings revisions will likely bottom soon as well. The ESSP is currently consistent with a dramatic decline in European net earnings revisions (Chart 10, bottom panel). It will take a few more weeks for lower earnings revisions to be fully reflected. However, they follow market moves and, as such, the 17% decline in the MSCI Europe Index that took place earlier this year already anticipates their fall. Consequently, as stagflation fears recede, earnings revisions will rise in tandem with equity prices. Chart 11Maximum Pressure On Corporate Spreads

Maximum Pressure On Corporate Spreads

Maximum Pressure On Corporate Spreads

A decline in stagflation fears is also consistent with a decrease in European credit spreads in the coming months (Chart 11). This observation corroborates the analysis from the Special Report we published jointly with BCA’s Global Fixed-Income Strategy team last week. In terms of sectoral implications, a decline in stagflation fears is often associated with a rebound in the performance of small-cap equities relative to large-cap ones (Chart 12, top panel). This reflects the greater sensitivity of small-cap equities to domestic economic conditions compared to large-cap stocks. Moreover, small-cap equities had been oversold relative to their large-cap counterparts but now, momentum is improving (Chart 12). As a result, it is time to buy these equities. Similarly, financials have suffered greatly from the recent events associated with the Ukrainian conflict. European financial institutions have not only been penalized for their modest exposure to Russia, they have also historically declined when stagflation fears are prevalent (Chart 13). This relationship reflects poor lending activity when the economy weakens, and the risk of a policy-induced recession caused by high inflation. Financials will continue their sharp rebound as stagflation fears dissipate. Chart 13Financials Have Suffered Enough

Financials Have Suffered Enough

Financials Have Suffered Enough

Chart 12Small-Caps Time To Shine

Small-Caps Time To Shine

Small-Caps Time To Shine

The dynamics in inflation alone are very important. As Table 1 highlights, in periods of elevated inflation over the past 20 years, financials underperform the broad market by 11.3% on average. It is also a period of pain for small-cap equities and cyclicals. Logically, exiting the current environment will offer opportunities in European cyclical equities and for financials in particular. Table 1Who Suffers From High Inflation?

Is Europe Turning The Corner?

Is Europe Turning The Corner?

Chart 14Long Industrials & Materials / Short Energy

Long Industrials & Materials / Short Energy

Long Industrials & Materials / Short Energy

Finally, a pair trade buying industrials and materials at the expense of energy makes sense today. Materials and industrials suffer relative to energy equities when stagflation rises, especially in periods when these fears reflect rising energy pressures (Chart 14). A reversal in relative earnings revisions in favor of materials and industrials will propel this position higher. Bottom Line: Sentiment toward European assets reached a selling climax in recent weeks. Stagflation fears in Europe have reached an apex, and their reversal will lift both multiples and earnings revisions in the subsequent quarters. Diminishing stagflation fears will also boost the appeal of European corporate credit, contributing to an easing in financial conditions. Small-cap stocks, cyclicals, and financials will reap the greatest benefits from this adjustment. Going long materials and industrials at the expense of energy stocks is an attractive pair trade. Key Risk: A Policy Mistake The view above is not without risks. The number one threat to European growth and assets is a policy mistake from the ECB. On March 10, 2022, the ECB’s policy statement and President Christine Lagarde’s press conference showed that the Governing Council (GC) will decrease asset purchases faster than anticipated. Chart 15Will The ECB Repeat It Past Mistakes?

Will The ECB Repeat It Past Mistakes?

Will The ECB Repeat It Past Mistakes?

It is important to keep in mind the dynamics of 2011. Back then, the ECB opted to increase interest rates as European headline CPI was drifting toward 2.6% on the back of rising energy prices. According to our ESSP, the April 2011 interest rates hike took place at the greatest level of stagflation fears recorded until the current moment (Chart 15). Lured by rising inflation, the ECB ignored underlying weaknesses in European economic activity, which wreaked havoc on European financial markets and growth. If the ECB were to increase rates as growth remains soft, a similar outcome would take place. For now, the ECB’s communications continue to de-emphasize the need for rate hikes in the near term, which suggests that the GC is cognizant of the risk created by weak growth over the coming months. Waiting until next year, when activity will be stronger and the output gap will be closed, will offer the ECB a better avenue to lift rates durably. This risk warrants close monitoring of the ECB’s communication over the coming months. If headline inflation does not peak by the summer, the ECB is likely to repeat its past error, which will substantially hurt European assets. Our optimism is tempered by this threat. UK Outperformance Long In The Tooth? Last week, the Bank of England (BoE) increased the Bank Rate by 25bps to 0.75%, in a move that was widely expected. Yet, the pound fell 0.7% against the euro and gilt yields fell 6 bps. This market reaction reflected the BoE’s choice to temper its forward guidance. The central bank is now expected to increase interest rates to 2.2% next year, before they decline in 2024. The dovish projection of the BoE shows the MPC’s concerns over the impact of higher energy costs and rising National Insurance contributions on household spending. In the BoE’s opinion, the economy is very inflationary right now, but it will slow, which will mitigate the inflationary impact down the road. We share the BoE’s worries about the UK’s near-term economic outlook. The combination of higher taxes, higher interest rates, and rising energy costs will have an impact on growth. However, the rapid decline in small-cap stocks, which have massively underperformed their large cap-counterparts, already discounts considerable bad news (Chart 16). Additionally, small-cap equities relative to EPS have begun to stabilize, while relative P/E and price-to-book ratios have also corrected their overvaluations. In this context, UK small-cap equities are becoming attractive. Chart 17UK vs Eurozone: A Stagflation Bet

UK vs Eurozone: A Stagflation Bet

UK vs Eurozone: A Stagflation Bet

Chart 16UK Small-Cap Stocks Have Purged Their Excesses

UK Small-Cap Stocks Have Purged Their Excesses

UK Small-Cap Stocks Have Purged Their Excesses

In contrast to small-cap stocks, UK large-cap equities have greatly benefited from the global stagflation scare. The UK large-cap benchmark had the right sector mix for the current environment, overweighting defensive names as well as energy and resources. It is likely that when stagflation fears recede, UK equities will undo their outperformance (Chart 17). Technically, UK equities are massively overbought against Euro Area and Swedish stocks, both of which have been greatly impacted by stagflation fears and their pro-cyclical biases (Chart 18 & 19). An attractive tactical bet will be to sell UK large-cap stocks while buying Eurozone and Swedish equities, as energy inflation declines and as China’s stimulus boosts global industrial activity in the latter half of 2022 Bottom Line: Move to overweight UK small-cap stocks within UK equity portfolios. Go long Euro Area and Swedish equities relative to UK large-cap stocks as a tactical bet. Chart 18UK Overbought Relative To Euro Area...

UK Overbought Relative To Euro Area...

UK Overbought Relative To Euro Area...

Chart 19… And Sweden

... And Sweden

... And Sweden

Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Tactical Recommendations Cyclical Recommendations Structural Recommendations Closed Trades

Executive Summary On a tactical (3-month) horizon, the inflationary impulse from soaring energy and food prices combined with the choke on growth from sanctions will weigh on both the global economy and the global stock market. As such, bond yields could nudge higher, the global stock market has yet to reach its crisis bottom, and the US dollar will rally. But on a cyclical (12-month) horizon, the short-term inflationary impulse combined with sanctions will be massively demand-destructive, at which point the cavalry of lower bond yields will charge to the rescue. Therefore: Overweight the 30-year T-bond and the 30-year Chinese bond, both in absolute terms and relative to other 30-year sovereign bonds. Overweight equities. Overweight long-duration US equities versus short-duration non-US equities. Fractal trading watchlist: Brent crude oil, and oil equities versus banks equities. The DAX Has Sold Off ##br##Because It Expects Profits To Plunge…

The DAX Has Sold Off Because It Expects Profits To Plunge...

The DAX Has Sold Off Because It Expects Profits To Plunge...

…But The S&P 500 Has Sold Off ##br##Because The Long Bond Has Sold Off

...But The S&P 500 Has Sold Off Because The Long Bond Has Sold Off

...But The S&P 500 Has Sold Off Because The Long Bond Has Sold Off

Bottom Line: In the Ukraine crisis, the protection from lower bond yields and fiscal loosening will not come as quickly and as powerfully as it did during the pandemic. If anything, the fixation on inflation and sanctions may increase short-term pain for both the economy and the stock market, before the cavalry of lower bond yields ultimately charges to the rescue. Feature Given the onset of the largest military conflict in Europe since the Second World War, with the potential to escalate to nuclear conflict, you would have thought that the global stock market would have crashed. Yet since Russia’s full-scale invasion of Ukraine on February 24 to the time of writing, the world stock market is down a modest 4 percent, while the US stock market is barely down at all. Is this the stock market’s ‘Wile E Coyote’ moment, in which it pedals hopelessly in thin air before plunging down the chasm? Is this the stock market’s ‘Wile E Coyote’ moment, in which it pedals hopelessly in thin air before plunging down the chasm? Admittedly, since the invasion, European bourses have fallen – for example, Germany’s DAX by 10 percent. And stock markets were already falling before the invasion, meaning that this year the DAX is down 20 percent while the S&P 500 is down 12 percent. But there is a crucial difference. While the DAX year-to-date plunge is due to an expected full-blooded profits recession that the Ukraine crisis will unleash, the S&P 500 year-to-date decline is due to the sell-off in the long-duration bond (Chart I-1 and Chart I-2). This difference in drivers will also explain the fate of these markets as the crisis evolves, just as in the pandemic. Chart I-1The DAX Has Sold Off Because It Expects Profits To Plunge...

The DAX Has Sold Off Because It Expects Profits To Plunge...

The DAX Has Sold Off Because It Expects Profits To Plunge...

Chart I-2...But The S&P 500 Has Sold Off Because The Long Bond Has Sold Off

...But The S&P 500 Has Sold Off Because The Long Bond Has Sold Off

...But The S&P 500 Has Sold Off Because The Long Bond Has Sold Off

During The Pandemic, Central Banks And Governments Saved The Day… We can think of a stock market as a real-time calculator of the profits ‘run-rate.’ In this regard, the real-time stock market is several weeks ahead of analysts, whose profits estimates take time to collect, collate, and record. For example, during the pandemic, the stock market had already discounted a collapse in profits six weeks before analysts’ official estimates (Chart I-3 and Chart I-4). Chart I-3The German Stock Market Is Several Weeks Ahead Of Analysts

The German Stock Market Is Several Weeks Ahead Of Analysts

The German Stock Market Is Several Weeks Ahead Of Analysts

Chart I-4The US Stock Market Is Several Weeks Ahead ##br##Of Analysts

The US Stock Market Is Several Weeks Ahead Of Analysts

The US Stock Market Is Several Weeks Ahead Of Analysts

We can also think of a stock market as a bond with a variable rather than a fixed income. Just as with a bond, every stock market has a ‘duration’ which establishes which bond it most behaves like when bond yields change. It turns out that the long-duration US stock market has the same duration as a 30-year bond, while the shorter-duration German stock market has the same duration as a 7-year bond. Pulling this together, and assuming no change to the very long-term structural growth story, we can say that: The US stock market = US profits multiplied by the 30-year bond price (Chart I-5 and Chart I-6). The German stock market = German profits multiplied by the 7-year bond price (Chart I-7 and Chart I-8). Chart I-5US Profits Multiplied By The 30-Year Bond Price...

US Profits Multiplied By The 30-Year Bond Price...

US Profits Multiplied By The 30-Year Bond Price...

Chart I-6...Equals The US Stock Market

...Equals The US Stock Market

...Equals The US Stock Market

Chart I-7German Profits Multiplied By The 7-Year Bond Price...

German Profits Multiplied By The 7-Year Bond Price...

German Profits Multiplied By The 7-Year Bond Price...

Chart I-8...Equals The German Stock Market

...Equals The German Stock Market

...Equals The German Stock Market

When bond yields rise – as happened through December and January – the greater scope for a price decline in the long-duration 30-year bond will hurt the US stock market both absolutely and relatively. But when bond yields decline – as happened at the start of the pandemic – this same high leverage to the 30-year bond price can protect the US stock market. When bond yields decline, the high leverage to the 30-year bond price can protect the US stock market. During the pandemic, the 30-year T-bond price surged by 35 percent, which more than neutralised the decline in US profits. Supported by this surge in the 30-year bond price combined with massive fiscal stimulus that underpinned demand, the pandemic bear market lasted barely a month. What’s more, the US stock market was back at an all-time high just four months later, much quicker than the German stock market. …But This Time The Cavalry May Take Longer To Arrive Unfortunately, this time the rescue act may take longer. One important difference is that during the pandemic, governments quickly unleashed tax cuts and stimulus payments to shore up demand. Whereas now, they are unleashing sanctions on Russia. This will choke Russia, but will also choke demand in the sanctioning economy. Another crucial difference is that as the pandemic took hold in March 2020, the Federal Reserve slashed the Fed funds rate by 1.5 percent. But at its March 2022 meeting, the Fed will almost certainly raise the interest rate (Chart I-9). Chart I-9As The Pandemic Took Hold, The Fed Could Slash Rates. Not Now.

As The Pandemic Took Hold, The Fed Could Slash Rates. Not Now.

As The Pandemic Took Hold, The Fed Could Slash Rates. Not Now.

As the pandemic was unequivocally a deflationary shock at its outset, it was countered with a massive stimulatory response from both central banks and governments. In contrast, the Ukraine crisis has unleashed a new inflationary shock from soaring energy and food prices. And this on top of the pandemic’s second-round inflationary effects which have already dislocated inflation into uncomfortable territory. Our high conviction view is that this inflationary impulse combined with sanctions will be massively demand-destructive, and thereby ultimately morph into a deflationary shock. Yet the danger is that myopic policymakers and markets are not chess players who think several moves ahead. Instead, by fixating on the immediate inflationary impulse from soaring energy and food prices, they will make the wrong move. In the Ukraine crisis, the big risk is that the protection from lower bond yields and fiscal loosening will not come as quickly and as powerfully as it did during the pandemic. If anything, the fixation on inflation and sanctions may increase short-term pain for both the economy and the stock market. Compared with the pandemic, both the sell-off and the recovery will take longer to play out. In the Ukraine crisis, the big risk is that the protection from lower bond yields and fiscal loosening will not come as quickly and as powerfully as it did during the pandemic. One further thought. The Ukraine crisis has ‘cancelled’ Covid from the news and our fears, as if it were just a bad dream. Yet the virus has not disappeared and will continue to replicate and mutate freely. Probably even more so, now that we have dismissed it, and Europe’s largest refugee crisis in decades has given it a happy hunting ground. Hence, do not dismiss another wave of infections later this year. The Investment Conclusions Continuing our chess metaphor, a tactical investment should consider only the next one or two moves, a cyclical investment should be based on the next five moves, while a long-term structural investment (which we will not cover in this report) should visualise the board after twenty moves. All of which leads to several investment conclusions: On a tactical (3-month) horizon, the inflationary impulse from soaring energy and food prices combined with the choke on growth from sanctions will weigh on both the global economy and the global stock market. As such, bond yields could nudge higher, the global stock market has yet to reach its crisis bottom, and the US dollar will rally (Chart I-10). Chart I-10When Stock Markets Sell Off, The Dollar Rallies

When Stock Markets Sell Off, The Dollar Rallies

When Stock Markets Sell Off, The Dollar Rallies

But on a cyclical (12-month) horizon, the short-term inflationary impulse combined with sanctions will be massively demand-destructive, at which point the cavalry of lower bond yields will charge to the rescue. Therefore: Overweight the 30-year T-bond and the 30-year Chinese bond, both in absolute terms and relative to other 30-year sovereign bonds. Overweight equities. Overweight long-duration US equities versus short-duration non-US equities. How Can Fractal Analysis Help In A Crisis? When prices are being driven by fundamentals, events and catalysts, as they are now, how can fractal analysis help investors? The answer is that it can identify when a small event or catalyst can have a massive effect in reversing a trend. In this regard, the extreme rally in crude oil has reached fragility on both its 65-day and 130-day fractal structures. Meaning that any event or catalyst that reduces fears of a supply constraint will cause an outsized reversal (Chart I-11). Chart I-11The Extreme Rally In Crude Oil Is Fractally Fragile

The Extreme Rally In Crude Oil Is Fractally Fragile

The Extreme Rally In Crude Oil Is Fractally Fragile

Equally interesting, the huge outperformance of oil equities versus bank equities is reaching the point of fragility on its 260-day fractal structure that has reliably signalled major switching points between the sectors (Chart I-12). Given the fast-moving developments in the crisis, we are not initiating any new trades this week, but stay tuned. Chart I-12The Huge Outperformance Of Oil Equities Versus Banks Equities Is Approaching A Reversal

The Huge Outperformance Of Oil Equities Versus Banks Equities Is Approaching A Reversal

The Huge Outperformance Of Oil Equities Versus Banks Equities Is Approaching A Reversal

Fractal Trading Watchlist Biotech To Rebound

Biotech Is Starting To Reverse

Biotech Is Starting To Reverse

US Healthcare Vs. Software Approaching A Reversal

US Healthcare Vs. Software Approaching A Reversal

US Healthcare Vs. Software Approaching A Reversal

Norway's Outperformance Could End

Norway's Outperformance Could End

Norway's Outperformance Could End

Greece’s Brief Outperformance To End

Greece Is Snapping Back

Greece Is Snapping Back

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Fractal Trading System Fractal Trades

Are We In A Slow-Motion Crash?

Are We In A Slow-Motion Crash?

Are We In A Slow-Motion Crash?

Are We In A Slow-Motion Crash?

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields ##br##- Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields ##br##- Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields ##br##- Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields ##br##- Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Executive Summary Will The War Stall The Expected Downturn In Inflation This Year?

Will The War Stall The Expected Downturn In Inflation This Year?

Will The War Stall The Expected Downturn In Inflation This Year?

The Russia/Ukraine conflict is impacting financial markets across numerous channels – uncertainty, risk aversion, growth expectations & inflation expectations – but all have a common link through soaring commodity prices, most notably for oil. For global bond investors, allocations to inflation-linked bonds are a necessary hedge to the war and the associated commodity shock, particularly with breakevens in most countries re-establishing the link to oil prices. We recommend investors maintain neutral allocations to inflation-linked bonds versus nominal government bonds across the developed world until there is greater clarity on future global oil production. Markets are discounting a peak in interest rates at the low end of the Bank of Canada’s neutral range, which is reasonable given high household debt levels in Canada. This creates an opportunity for bond investors to go long Canadian government bonds versus US Treasuries. Bottom Line: The supply premium on global oil prices will persist until there are signs of more global oil production or less chaos in the Ukraine – neither of which is imminent. Maintain neutral allocations to inflation-linked bonds versus nominal government debt across the developed markets. Feature Chart 1A Broad-Based Surge In Commodity Prices

A Broad-Based Surge In Commodity Prices

A Broad-Based Surge In Commodity Prices

The Russia/Ukraine war has sent an inflationary shock though the world through a very traditional source – rising commodity prices. Energy prices are getting most of the attention, with oil prices back to levels last seen in 2008 and US gasoline prices now above $4 per gallon. The commodity rally is not just in energy, though. Industrial metals prices have also gone up substantially, with the spot prices for copper and aluminum hitting an all-time-high and 16-year-high, respectively (Chart 1). Agricultural commodities have seen even larger increases, with the price of wheat up 22% and the price of corn up 11% since the Russian invasion began on February 24th. Europe is acutely exposed to the war-driven spike in energy prices given its reliance on Russia for natural gas supplies. Natural gas prices in Europe have spiked a staggering 117% since the invasion started, exacerbating a sharp demand/supply imbalance dating back to the reopening of Europe’s economy from COVID lockdowns one year ago (Chart 2). To date, booming energy prices have fueled a huge rise in headline inflation rates in the euro area – producer prices were up 31% on a year-over-year basis in January – but with little trickle down to core inflation which was only up 2.3% in January. High energy prices are not only a problem for global growth and inflation, but also for the future policy moves by central banks. Inflation rates boosted over the past year by commodity supply squeezes and supply chain disruptions were set to decline this year, but the Ukraine shock has thrown that into question. If the benchmark Brent oil price were to hit $150/bbl, this would end the decelerating trend for energy price inflation momentum, on a year-over-year basis, that has been in place since mid-2021 (Chart 3). That means a higher floor for the energy component of inflation indices, and thus overall headline inflation rates, throughout the major economies in the coming months. Chart 2Europe's Reliance On Russian Natural Gas Is A Big Problem

Europe's Reliance On Russian Natural Gas Is A Big Problem

Europe's Reliance On Russian Natural Gas Is A Big Problem

Chart 3Will The War Stall The Expected Downturn In Inflation This Year?

Will The War Stall The Expected Downturn In Inflation This Year?

Will The War Stall The Expected Downturn In Inflation This Year?

Chart 4The Oil Price Spike Makes Life More Difficult for CBs

The Oil Price Spike Makes Life More Difficult for CBs

The Oil Price Spike Makes Life More Difficult for CBs

How will bond markets respond to higher-than-expected inflation? Rate hike expectations have been highly correlated to the trend of headline inflation in the US, Europe, UK, Canada and Australia over the past year (Chart 4). Currently, overnight index swap (OIS) curves are still discounting between 5-6 rate hikes from the Fed, the Bank of England, the Bank of Canada and the Reserve Bank of Australia before the end of 2022. A single rate hike is still priced into the European OIS curve, even with the Ukraine shock. Global bond yields have been volatile, but surprisingly resilient despite the worries about war and commodity inflation. The 10-year Treasury yield has been trading in a range between 1.7% and 2% since the Russian offensive began, while the 10-year German Bund yield has hovered around 0%. Bond markets are pricing in a stagflation-type outcome of slowing growth and rising inflation, as multiple rate hikes are still discounted despite the geopolitical risks from the war. That reduces the value of using increased duration exposure to position for risk-off moves in a bond portfolio. At the same time, real bond yields are falling and breakeven rates are rising for global inflation-linked bonds – a part of the fixed income universe that looks to offer good protection against the uncertainties of war. Inflation-Linked Bonds – A Good Hedge Against War Risks Since the Russian invasion began, breakeven inflation rates on 10-year inflation-linked bonds have moved higher in the US (+13bps), Canada (+19bps), Australia (+15bps) and even Japan (+15bps). The moves have been even more significant on the European continent – 10-year breakevens have shot up in the UK (+23bps), Germany (+45bps), France (+31bps) and Italy (+36bps). Chart 5Inflation Breakevens Are Rising, Especially In Europe

Inflation Breakevens Are Rising, Especially In Europe

Inflation Breakevens Are Rising, Especially In Europe

The absolute levels of breakevens in Europe are high in the context of recent history (Chart 5). However, breakevens also look a bit stretched in other countries like the US. Our preferred metric to evaluate the upside potential for inflation-linked bonds is our Comprehensive Breakeven Indicators (CBI). The CBI for each country is comprised of three components: the deviation of 10-year breakevens from our model-implied fair value, the spread between 10-year breakevens and longer-term survey-based inflation expectations (the “inflation risk premium”) and the gap between actual inflation and the central bank inflation target. Those three components are all standardized and added together with equal weights to come up with the CBI. A higher CBI reading suggests less potential for inflation breakevens to widen, and vice versa. Currently, the CBIs for the eight countries in our Model Bond Portfolio universe are close to or above zero, suggesting more limited scope for breakevens to widen further (Chart 6). Only in Canada is the CBI below zero, and only slightly so as high realized Canadian inflation is offset by breakevens trading below both fair value and survey-based measures of inflation (Chart 7). Chart 6Global Inflation Breakeven Valuations Are Not That Cheap

A Crude Awakening For Bond Investors

A Crude Awakening For Bond Investors

In the US, the CBI is above zero mostly because of high realized US inflation. In Europe, the CBIs of the UK, Germany and Italy all are well above zero, while in France the CBI is close to zero. The UK has the highest CBI in our eight-country universe, with all three components contributing roughly equally (Chart 8). The Japanese CBI is also just above the zero line. Chart 7Some Mixed Signals On Inflation Breakeven Valuations

Some Mixed Signals On Inflation Breakeven Valuations

Some Mixed Signals On Inflation Breakeven Valuations

Chart 8European Breakevens Have Adjusted Sharply To The Energy Shock

European Breakevens Have Adjusted Sharply To The Energy Shock

European Breakevens Have Adjusted Sharply To The Energy Shock

We have been recommending a relative cautious allocation to global breakeven bonds in recent months. We saw the upside potential on breakevens as capped given the dearth of “cheap” signals on breakevens from our CBIs, especially with central banks moving towards monetary tightening in response to elevated inflation – moves intended to restore inflation-fighting credibility with bond markets. Yet the Ukraine commodity shock has boosted inflation breakevens even in countries with modest underlying (non-commodity) inflation like Japan and the euro area. We now see greater value in owning inflation-linked bonds in global bond portfolios as a hedge against the inflation risks stemming from the Ukraine and the worsening geopolitical tensions between the West and Russia. This is true even without the typical positive signal for breakevens from having CBIs below zero. We recommend that fixed income investors maintain a neutral allocation to inflation-linked bonds in dedicated government bond portfolios across the entire developed market “linker” universe. In our model bond portfolio, we had been allocating to linkers based off the signal from the CBIs, but in the current stagflationary war environment, we see country allocations as secondary to having neutral exposure to linkers in all countries. The new weightings to inflation-linked bonds are shown in the model bond portfolio tables on pages 12-14.1 Bottom Line: For global fixed income investors, allocations to inflation-linked bonds are a necessary hedge to the war and the associated commodity shock, particularly with breakevens in most countries re-establishing the link to oil prices. Canada Update: BoC Liftoff At Last The Bank of Canada (BoC) raised its policy interest rate by 25bps to 0.5% last week, commencing the start of the first rate hike cycle since 2018. The move was no surprise after BoC Governor Tiff Macklem signaled at the January monetary policy meeting that the start of a rate hiking cycle was imminent. The Canadian Overnight Index Swap (OIS) curve is discounting another 171bps of hikes in 2022, with a peak rate of 1.98% reached by March 2023 - near the low-end of the BoC’s range of neutral rate estimates between 1.75% and 2.75% (Chart 9). Chart 9Markets Discounting A Shallow BoC Rate Hiking Cycle, Even With High Inflation

Markets Discounting A Shallow BoC Rate Hiking Cycle, Even With High Inflation

Markets Discounting A Shallow BoC Rate Hiking Cycle, Even With High Inflation

The BoC noted that the Canadian economy was recovering faster than expected from the effects of the Omicron variant and the associated restrictions on activity, coming off a robust 6.7% annualized real GDP growth rate in Q4/2021. The BoC now estimates that economic slack created by the pandemic shock has been fully absorbed, with the unemployment rate at 6.5%. Canadian headline inflation reached a 32-year high of 5.1% in January (Chart 10) – a level that Governor Macklem bluntly called “too high” in a speech the day following the rate hike. The BoC’s CPI-trim measure that excludes the most volatile components is also at an elevated reading of 4%, suggesting that the higher inflation is broad based. The BoC sees persistent high inflation as a risk to the stability of medium-term inflation expectations, thus justifying tighter monetary policy. According the latest BoC Survey of Consumer Expectations, Canadians expect inflation to be 4.1% over the next two years and 3.5% over the next five years, both of which are above the BoC’s 1-3% inflation target band. So with a robust economy, tight labor market, inflation well above the BoC target and elevated consumer inflation expectations showing no signs of settling, why is the OIS curve discounting such a relatively low peak in the BoC policy rate? The answer lies with Canada’s housing bubble and the associated high household debt levels. In a recent Special Report, our colleagues at The Bank Credit Analyst estimated that the neutral rate in Canada was no higher than 1.75%- the previous peak in rates during the 2017-2018 tightening cycle. A big reason for that was the high level of Canadian household debt, which now sits at 180% of disposable income. This compares to the equivalent measure in the US of 124%, showing that unlike their southern neighbors, Canadian households had little appetite for deleveraging after the 2008 financial crisis (Chart 11). Chart 10Good Reasons For A More Aggressive BoC

Good Reasons For A More Aggressive BoC

Good Reasons For A More Aggressive BoC

Chart 11A Big Reason For A Less Aggressive BoC

A Big Reason For A Less Aggressive BoC

A Big Reason For A Less Aggressive BoC

Chart 12Position For Narrower Canada-US Bond Spreads

Position For Narrower Canada-US Bond Spreads

Position For Narrower Canada-US Bond Spreads

The Bank Credit Analyst report estimated that if the BoC hiked rates to 2.5% over the next two years – just below the high end of the BoC neutral range – the Canadian household debt service ratio would climb to a new high of 15.5% (bottom panel). This would greatly restrict Canadian consumer spending and likely trigger a sharp pullback in both housing demand and real estate prices. The conclusion: the neutral interest rate in Canada is likely closer to the peak seen during the previous 2018/19 hiking cycle around 1.75%. We have been recommending an underweight stance on Canadian government bonds in global fixed income portfolios dating back to the spring of 2021. However, with markets now discounting a peak in rates within plausible estimates of neutral, the window for additional underperformance of Canadian government bonds may be closing - but not equally versus all developed economies. We have found that a useful leading indicator of 10-year cross-country government bond yield spreads is the differential between our 24-month discounters. The discounters measure the cumulative amount of short-term interest rate increases over the next two years priced into OIS curves. Currently the “discounter gaps” are signaling room for Canadian spread widening versus the UK and Japan and, to a lesser extent, core Europe (Chart 12). However, the discounter gap is pointing to significant potential for narrowing of the Canada-US 10-year spread over the next year (top panel). This would occur even if the BoC follows the Fed with rate hikes in 2022, as the Fed is likely to deliver more increases in 2023/24 than the BoC. This week, we are introducing two new recommended positions to benefit from narrower Canada-US government bond spreads: We are reducing the size of our underweight position in our model bond portfolio in half, offset by a reduction in the allocation to US Treasuries (see the table on page 13). We are introducing a new trade in our Tactical Overlay, going long Canadian 10-year government bond futures versus selling 10-year US Treasury futures on a duration-matched basis (the specific details of the trade can be found in the table on page 15) We are maintaining our cyclical underweight recommendation on Canada, in a global bond portfolio context, given the potential for Canadian yield spreads to widen versus core Europe, Japan and the UK. That underweight recommendation will be more concentrated versus countries relative to the US. Bottom Line: Markets are discounting a peak in interest rates at the low end of the Bank of Canada’s neutral range, which is reasonable given high household debt levels in Canada. This creates an opportunity for bond investors to go long Canadian government bonds versus US Treasuries. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 The allocations to inflation-linked bonds shown in the model bond portfolio reflect both the recommended country weights and the recommended weighting of linkers versus nominal bonds within each country. For example, we are neutral US TIPS versus nominal bonds within the US Treasury component of the portfolio, but since we are also underweight the US as a country allocation, the TIPS allocation is below the custom benchmark index weight. GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

A Crude Awakening For Bond Investors

A Crude Awakening For Bond Investors

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index Global Fixed Income - Strategic Recommendations* Cyclical Recommendations (6-18 Months)

A Crude Awakening For Bond Investors

A Crude Awakening For Bond Investors

Tactical Overlay Trades

Executive Summary Nuclear Worries Take Center Stage

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

Vladimir Putin has now committed himself to orchestrating a regime change in Kyiv. Anything less would be seen as a defeat for him. Assuming he succeeds, and it is far from obvious that he will, the resulting insurgency will drain Russian resources. Along with continued sanctions, this will lead to a further deterioration in Russian living standards and growing domestic discontent. If Putin concludes that he has no future, the risk is that he will decide that no one else should have a future either. Although there is a huge margin of error around any estimate, subjectively, we would assign an uncomfortably high 10% chance of a civilization-ending global nuclear war over the next 12 months. These odds place some credence on Brandon Carter’s highly controversial Doomsday Argument. Even if World War III is ultimately averted, markets could experience a freak-out moment over the next few weeks, similar to what happened at the outset of the pandemic. Google searches for nuclear war are already spiking. Despite the risk of nuclear war, it makes sense to stay constructive on stocks over the next 12 months. If an ICBM is heading your way, the size and composition of your portfolio becomes irrelevant. Thus, from a purely financial perspective, you should largely ignore existential risk, even if you do care about it greatly from a personal perspective. Bottom Line: The risk of Armageddon has risen dramatically. Stay bullish on stocks over a 12-month horizon. All In on Sanctions In the criminal justice system, there is a reason why the punishment for armed robbery is lower than for murder. If the punishment were the same, an armed robber would have a perverse incentive to kill his victim in order to better conceal his crime. The same logic applies, or at least used to apply, to geopolitics: You do not impose maximum sanctions from the get-go because that removes your ability to influence your enemy with the threat of further sanctions. Following Russia’s invasion of Ukraine, the West chose to go all in on sanctions, levying every type imaginable with the exception of those entailing a big cost to the West (such as cutting off Russian energy exports). Most notably, many Russian banks have been blocked from the SWIFT messaging system while the Russian central bank’s foreign exchange reserves have been frozen. Even FIFA has barred Russia from international competition, just weeks before it was set to participate in the qualifying rounds of the 2022 World Cup. At this point, there is not much more that can be done on the sanctions front. This leaves military intervention as the only avenue available to further pressure Russia. A growing chorus of Western pundits, some of whom could not have picked out Ukraine on a map two weeks ago, have begun clamoring for regime change… this time, in Moscow. As one might imagine, this is not something that sits well with Putin. Last week, he declared that “No matter who tries to stand in our way or … create threats for our country and our people, they must know that Russia will respond immediately, and the consequences will be such as you have never seen in your entire history.” To ensure there was no uncertainty about what he was talking about, he proceeded to place Russia’s nuclear forces on “special regime of combat duty.” Yes, It’s Possible The Putin regime has used nuclear weapons of a sort in the past. The FSB likely orchestrated the poisoning of Alexander Litvinenko with polonium-210 in 2006, leaving traces of the radioactive substance scattered in dozens of places across London. As former US presidential advisor and Putin biographer Fiona Hill said in a recent interview with Politico, “Every time you think, “No, he wouldn’t, would he?” Well, yes, he would.” Admittedly, there is a big difference between dropping polonium into a cup of tea at the Millennium hotel in Mayfair and dropping a 10-megaton nuclear bomb on London or any other major Western city. Still, if Putin feels that he has no future, he may try to take everyone down with him. The collapse in the ruble, and what is sure to be a major plunge of living standards across Russia, could foment internal opposition to Putin. A quiet retirement is not an option for him. Based on the latest exchange rates, Russia’s GDP is smaller than Mexico’s and barely higher than that of Illinois (Chart 1). While denying gas to Europe is a very real threat, it has a limited shelf life. Europe will aggressively build out infrastructure to process LNG imports. Chart 1Russia's Economic Power Has Faded

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

In a few years, the one viable weapon that Russia will have at its disposal is its nuclear arsenal. As Dutch historian Jolle Demmers has said, “It is precisely the decline and contraction of Russian power, coupled with the possession of nuclear weapons and a tormented repressive president, that poses great risks.” Some of the world’s most prominent strategic thinkers flagged these risks before the invasion, but with little effect. The Mother of All Risks In simulated war games, it is generally difficult to get participants to cross the nuclear threshold, but once they do, a full-blown nuclear exchange usually ensues.1 The idea of “limited” nuclear war is a mirage. How high are the odds of such a full-blown war? I must confess that my own feelings on the matter are heavily colored by my writings on existential risk. As I argued in Section XII of my special report, “Life, Death, and Finance in the Cosmic Multiverse,” we are probably greatly understating existential risk, especially when we look prospectively into the future. Although there is a huge margin of error around any estimate, subjectively, we would assign an uncomfortably high 10% chance of a civilization-ending global nuclear war over the next 12 months. These odds place some credence on Brandon Carter’s highly controversial Doomsday argument (See Box 1). A Paradox for Investors For investors, existential risk represents a paradoxical concept. If an ICBM is heading your way, the question of whether you are overweight or underweight stocks would be pretty far down on your list of priorities. And even if you were inclined to think about your portfolio, how would you alter it? In a full-blown global nuclear war, most stocks would go to zero while governments would probably be forced to default or inflate away their debt. Gold might retain some value – provided that you kept it in your physical possession – but even then, you would still have trouble exchanging it for anything of value if nothing of value were available to purchase. This means that from a purely financial perspective, you should largely ignore existential risk, even if you do care greatly about it from a personal perspective. What, then, can we say about the current market environment? I touched on many of the key issues in Monday’s Special Alert, in which we tactically downgraded global equities from overweight to neutral. I encourage readers to consult that report for our latest market views. In the remainder of today’s report, allow me to elaborate on a couple of key themes. A Freak-Out Moment Is Coming Chart 2Nuclear Worries Take Center Stage

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

The market today reminds me of early 2020. We wrote a report on February 21 of that year entitled “Markets Too Complacent About The Coronavirus,” in which we noted that a full-blown pandemic “could lead to 20 million deaths worldwide,” and that “This would likely trigger a global downturn as deep as the Great Recession of 2008/09, with the only consolation being that the recovery would be much more rapid than the one following the financial crisis.” Many saw that report as alarmist, just as they saw our subsequent decision to upgrade stocks in March as cavalier. Even if you knew in February 2020 that the S&P 500 would reach an all-time high later that year, you should have still shorted equities aggressively on a tactical basis. I feel the same way about the present. Google searches for nuclear war are spiking (Chart 2). A freak-out moment is coming, which will present a good buying opportunity for investors. Just to be on the safe side, I picked up a couple of bottles of Potassium Iodide earlier this week. When I checked the pharmacy again yesterday, all the bottles were sold out. They are now being hawked on Amazon for ten times the regular price. From Cold War to Hot Economy? The spike in commodity prices – especially energy prices – will have a negative near-term impact on global growth, while also limiting the ability of central banks to slow the pace of planned rate hikes (Chart 3). In general, inflation expectations and oil prices move together (Chart 4). Chart 3Central Banks: Caught Between A Rock And A Hard Place

Central Banks: Caught Between A Rock And A Hard Place

Central Banks: Caught Between A Rock And A Hard Place

Chart 4Inflation Expectations And Oil Prices Go Hand-In-Hand

Inflation Expectations And Oil Prices Go Hand-In-Hand

Inflation Expectations And Oil Prices Go Hand-In-Hand

Assuming the geopolitical situation stabilizes in a few months, oil prices should come down. The forward curve for oil is heavily backwardated now: The spot price for Brent is $111/bbl while the December 2022 price is $93/bbl (Chart 5). BCA’s commodity strategists expect the price of Brent oil to fall to $88/bbl by year-end. The decline in energy prices should provide some relief to global growth and risk assets in the back half of the year, which is one reason we are more constructive on equities over a 12-month horizon than a 3-month horizon. Looking out beyond the next year or two, the new cold war will lead to higher, not lower, interest rates. Increased spending on defense and alternative energy sources will prop up aggregate demand, especially in Europe where the need to diversify away from Russian gas is greatest. As Chart 6 shows, capex in the euro area cratered following the euro debt crisis. Capital spending via the Recovery Fund and other sources will rise significantly over the next few years. Chart 5The Brent Curve Is Heavily Backwardated

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

Chart 6European Capex Is Poised To Increase

European Capex Is Poised To Increase

European Capex Is Poised To Increase

In addition, the shift to a multipolar world will expedite the retreat from globalization. Rising globalization was an important force restraining inflation – and interest rates – over the past few decades. Lastly, the ever-present danger of war could prompt households to reduce savings. It does not make sense to save for a rainy day if that day never arrives. Lower savings implies a higher equilibrium rate of interest. As we discussed in our recent report entitled “A Two-Stage Fed Tightening Cycle,” after raising rates modesty this year, the Fed will resume hiking rates towards the end of 2023 or in 2024, as it becomes clear that the neutral rate in nominal terms is closer to 3%-to-4% rather than the 2% that the market assumes. The secular bull market in equities will likely end at that point. In summary, equity investors should be somewhat cautious over the next three months, more optimistic over a 12-month horizon, but more cautious again over a longer-term horizon of 2-to-5 years. Box 1The Doomsday Argument In A Nutshell

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 For example, an article from the Center for Arms Control and Non-Proliferation discusses a Reagan administration war game called “Proud Prophet,” an exercise the Americans hatched to test the theory of limited nuclear strikes. The result of this exercise was that the “Soviet Union perceived even a low-yield nuclear strike as an attack, and responded with a massive missile salvo.” Global Investment Strategy View Matrix

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

Special Trade Recommendations Current MacroQuant Model Scores

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

Executive Summary Upgrade Global Duration Exposure To Neutral

Upgrade Global Duration Exposure To Neutral

Upgrade Global Duration Exposure To Neutral

The Russian invasion of Ukraine is a stagflationary shock that comes at a difficult time for developed market central banks that have been laying the groundwork for a tightening cycle. We tactically upgraded our recommended duration exposure in the US to neutral last week, as the market was pricing in too much Fed tightening in 2022. We are doing similar upgrades in non-US government bonds this week for the same reason. We are maintaining our cyclical country allocations, however, as those remain in line with interest rate pricing beyond 2022. We are underweight markets where terminal rate expectations remain too low (the US, UK & Canada) and overweight countries where markets are discounting too many rate hikes in 2023/24 (Germany, Japan, Australia). In light of the instability caused by the Russian invasion of Ukraine, we are reducing weightings in our model bond portfolio to credit sectors highly exposed to the war - European high-yield and emerging market hard currency debt. Bottom Line: The Ukraine war comes at a time when global growth momentum was already starting to roll over and with global inflation momentum set to peak soon. Upgrade duration exposure to neutral from underweight in global bond portfolios. Feature Among the tail risks that investors contemplated in their planning for 2022, World War III was likely not ranked too highly on the list. The horrific images of the Russian invasion of Ukraine – and the sharp response of the West to isolate Russia through unprecedented economic and financial sanctions - have shocked global financial markets that had been focused on relatively mundane concerns like the timing of interest rate hikes. BCA sent a short note to all clients late last week that discussed the investment implications of the invasion for several asset classes. In this report, we consider the bond market ramifications of war in Eastern Europe. Our main conclusion is that the Ukraine situation will produce a brief “stagflationary” shock that will boost global inflation and slow global growth, on the margin. High energy prices will be the main driver of that stagflation, given the uncertainties over the availability of Russian oil and natural gas supplies (Chart 1). Tighter financial conditions - beyond what has already occurred so far this year as global equity and credit markets have sold off (Chart 2) – will also contribute to the moderation of the pace of global growth. Chart 1A Mild Inflationary Shock From The Russian Invasion

A Mild Inflationary Shock From The Russian Invasion

A Mild Inflationary Shock From The Russian Invasion

Chart 2The Ukraine War Is Adding To 2022 Risk-Off Trends

The Ukraine War Is Adding To 2022 Risk-Off Trends

The Ukraine War Is Adding To 2022 Risk-Off Trends

The stagflation shock should be relatively short, perhaps 3-6 months. BCA’s Commodity & Energy Strategy service expects OPEC to eventually supply more oil to the global market – a move that was already likely before the Russian invasion – helping to reduce the Russian supply premium in oil prices. Putin will likely have to be satisfied with claiming eastern Ukraine rather than being stuck in a protracted battle with fierce Ukrainian resistance while Russia suffers under crippling sanctions. BCA’s Geopolitical Strategy service does not expect the conflict to spread beyond Ukraine’s borders, as neither Russia nor NATO have an interest in war with each other (despite the nuclear saber-rattling by Russian President Putin in response to Western sanctions). A mild bout of stagflation will only delay, and not derail, the cyclical move towards tighter global monetary policies in response to elevated inflation and tightening labor markets, particularly in the US. This will take some of the upward pressure off global bond yields as central banks will be less hawkish than expected in 2022, but does not change the outlook for higher bond yields in 2023 and 2024. In terms of changes to our fixed income investment recommendations, and the allocations to our Model Bond Portfolio, we come to the following three conclusions. Upgrade Tactical Non-US Duration Exposure To Neutral We recently upgraded our recommended tactical duration exposure in the US to neutral, with the Fed likely to deliver fewer rate hikes this year than what is discounted by markets. The Ukraine situation makes it even more likely that the Fed will underwhelm expectations. A 50bp rate hike at the March FOMC meeting is now off the table, as the equity and credit market selloffs in response to the conflict have tightened US (and global) financial conditions on the margin. However, the war is not enough of a negative shock to US growth to derail the Fed from starting a gradual tightening process this month with a 25bp hike. Our decision to change our US duration stance was largely predicated on a view that US inflation will soon peak and slow significantly over the rest of 2022. However, there is a strong case to increase non-US duration exposure, as well. Our Global Duration Indicator - comprised of leading cyclical growth indicators and which itself leads the year-over-year change in our “Major Countries” GDP-weighted aggregate of 10-year government bond yields by around six months - peaked back in February 2021 (Chart 3). The Global Duration Indicator is now at a “neutral” level consistent with more stable bond yield momentum. Declines in the ZEW economic expectations survey in the US and Europe, and in our global leading economic indicator, are the main culprits behind the fall in the Global Duration Indicator (Chart 4). Chart 3Upgrade Global Duration Exposure To Neutral

Upgrade Global Duration Exposure To Neutral

Upgrade Global Duration Exposure To Neutral

Chart 4Growth Expectations Have Turned Less Bond Bearish ... For Now

Growth Expectations Have Turned Less Bond Bearish ... For Now

Growth Expectations Have Turned Less Bond Bearish ... For Now

While the ZEW series have rebounded in the first two months of 2022, which could set the stage for a move back to higher yields later this year, the Ukraine situation will likely hurt economic expectations (particularly in Europe) in the near-term. We expect our Global Duration Indicator to continue signaling a more neutral backdrop for global bond yields over the next few months. In our Model Bond Portfolio on pages 13-14, we are expressing our view change by increasing the duration for all countries such that the overall duration of the portfolio is in line with the custom benchmark index (7.5 years). Importantly, we view this as only a tactical view change for the next few months, as developed economy interest rate markets are still discounting too few rate hikes – and in some countries like the UK and US, actual rate cuts – in 2023/24 (Chart 5). Chart 5Priced For Short, Shallow Hiking Cycles

Priced For Short, Shallow Hiking Cycles

Priced For Short, Shallow Hiking Cycles

Maintain Cyclical Government Bond Country Allocations That Favor Lower Inflation Regions Chart 6Oil Is Inflationary Now, Will Be Disinflationary Later

Oil Is Inflationary Now, Will Be Disinflationary Later

Oil Is Inflationary Now, Will Be Disinflationary Later

While we are neutralizing our global duration stance over a tactical time horizon (0-6 months), we are sticking with our current recommended cyclical (6-18 months) government bond country allocations. These are based on underlying inflation trends and the expected monetary policy response over the next couple of years. As noted earlier, BCA’s commodity strategists expect oil prices to fall from current war-elevated levels in response to increased supply from OPEC. The benchmark Brent oil price is forecasted to reach $88/bbl at the end of this year and $87/bbl and the end of 2023. The result will be a sharp decline in the year-over-year growth rate of oil prices that will help bring down headline inflation in all countries (Chart 6). Lower energy inflation, however, will not be the only factor reducing overall inflation across the developed world. Goods price inflation should also slow from current elevated levels over the next 6-12 months, as consumer spending patterns shift away from goods towards services with fewer pandemic-related restrictions on activity. Less goods spending will help ease some of the severe supply chain disruptions that have fueled the surge in global goods price inflation over the past year. That process has likely already begun – indices of global shipping costs have peaked and supplier delivery times have been shortening according to global manufacturing PMI surveys. The shift from less goods spending towards more services spending will lead to trends in overall inflation being determined more by services prices than goods prices. The central banks in countries that have higher underlying inflation, as evidenced by faster services inflation, will be under more pressure to tighten policy over the next couple of years. Therefore, our current cyclical recommended country allocations (and our Model Bond Portfolio weightings) within developed market government bonds reflect the relative trends in services inflation. We are currently recommending underweights in the US, UK and Canada where services inflation is currently close to 4%, well above the central bank 2% inflation targets (Chart 7). At the same time, we are recommending overweights in core Europe (Germany and France) and Australia, where services inflation is around 2.5%, and Japan where services prices are deflating (Chart 8). Chart 7Higher Underlying Inflation In Our Recommended Underweights

Higher Underlying Inflation In Our Recommended Underweights

Higher Underlying Inflation In Our Recommended Underweights

Chart 8Lower Underlying Inflation In Our Recommended Overweights

Lower Underlying Inflation In Our Recommended Overweights

Lower Underlying Inflation In Our Recommended Overweights

Chart 9Faster Wage Growth In Our Recommended Underweights

Faster Wage Growth In Our Recommended Underweights

Faster Wage Growth In Our Recommended Underweights

The trends in services inflation are also reflected in wage growth in those same groups of countries – much higher in the US, UK and Canada compared to Australia, the euro area and Japan (Chart 9). We expect these relative trends to continue over the next 12-24 months, with higher underlying inflation pressures forcing the Fed, the Bank of England (BoE) and the Bank of Canada (BoC) to be much more hawkish, on a relative basis, than the European Central Bank (ECB), the Reserve Bank of Australia (RBA) and the Bank of Japan (BoJ). Our current bond allocations not only fit with underlying inflation trends, but also with market-based interest rate expectations. In Table 1, we show the pricing of interest rate expectations over the next few years, taken from Overnight Index Swap (OIS) forwards. We show the OIS projection for 1-month interest rates 12 months from now and 24 months from now. We also include 5-year/5-year forward OIS rates as a measure of market expectations of the terminal rate, a.k.a. the peak central bank policy rate over the next tightening cycle. In the table, we also added neutral policy rate estimates taken from central bank sources.1 Table 1Medium-Term Interest Rate Expectations Still Too Low In The US & UK

Adjusting Our Bond Recommendations For A More Uncertain World

Adjusting Our Bond Recommendations For A More Uncertain World

In the US and UK, the OIS rate projections two years out, as well as the 5-year/5-year forward rate, are below the range of neutral rate estimates. This justifies an underweight stance on both US Treasuries and UK Gilts with both the Fed and BoE now in tightening cycles. In Japan and Australia, the OIS projections are already within the range of neutral rate estimates, but the RBA and, especially, the BoJ are not yet signaling a need to begin normalizing the level of policy rates. This justifies an overweight stance on Australian government bonds and Japanese government bonds. In the euro area, OIS projections are below the range of neutral rate estimates, but the ECB is now signaling that any monetary tightening actions will need to be delayed because of the growth uncertainties stemming from the Ukraine conflict and high energy prices. Thus, an overweight stance on core European government debt is still warranted. In Canada, the OIS projections are within the range of neutral rate estimates, but the BoC has been preparing markets for a series of rate hikes. This makes our underweight stance on Canadian government bonds a more “mixed” call, although we remain confident that Canadian bonds will underperform in a global bond portfolio context versus European and Japanese government bonds. In sum, we see our recommended country allocations as the most efficient way to express our cyclical (medium-term) central bank views, given the strong link between forward interest rate expectations and longer-term bond yields (Chart 10). This is why we are not making changes to our country allocation recommendations alongside our move to tactically upgrade our global duration stance to neutral. Chart 10Too Much Tightening Priced Over The Next Year

Too Much Tightening Priced Over The Next Year

Too Much Tightening Priced Over The Next Year

Chart 11Bond Markets Not Priced For A Relatively More Hawkish Fed

Bond Markets Not Priced For A Relatively More Hawkish Fed

Bond Markets Not Priced For A Relatively More Hawkish Fed

Given our high-conviction view that markets are underestimating how high the Fed will need to lift interest rates in the upcoming tightening cycle – likely more than any other major developed economy central bank - positioning for US Treasury market underperformance on a 1-2 year horizon still looks like an attractive bet with forward rates priced for little change in US/non-US bond spreads (Chart 11). A wider US Treasury-German Bund spread remains our highest conviction cross-country spread recommendation. Reduce Spread Product Exposure In Europe & Emerging Markets Chart 12Cut EM & European High-Yield Exposure, But Stay O/W Italian BTPs

Cut EM & European High-Yield Exposure, But Stay O/W Italian BTPs

Cut EM & European High-Yield Exposure, But Stay O/W Italian BTPs