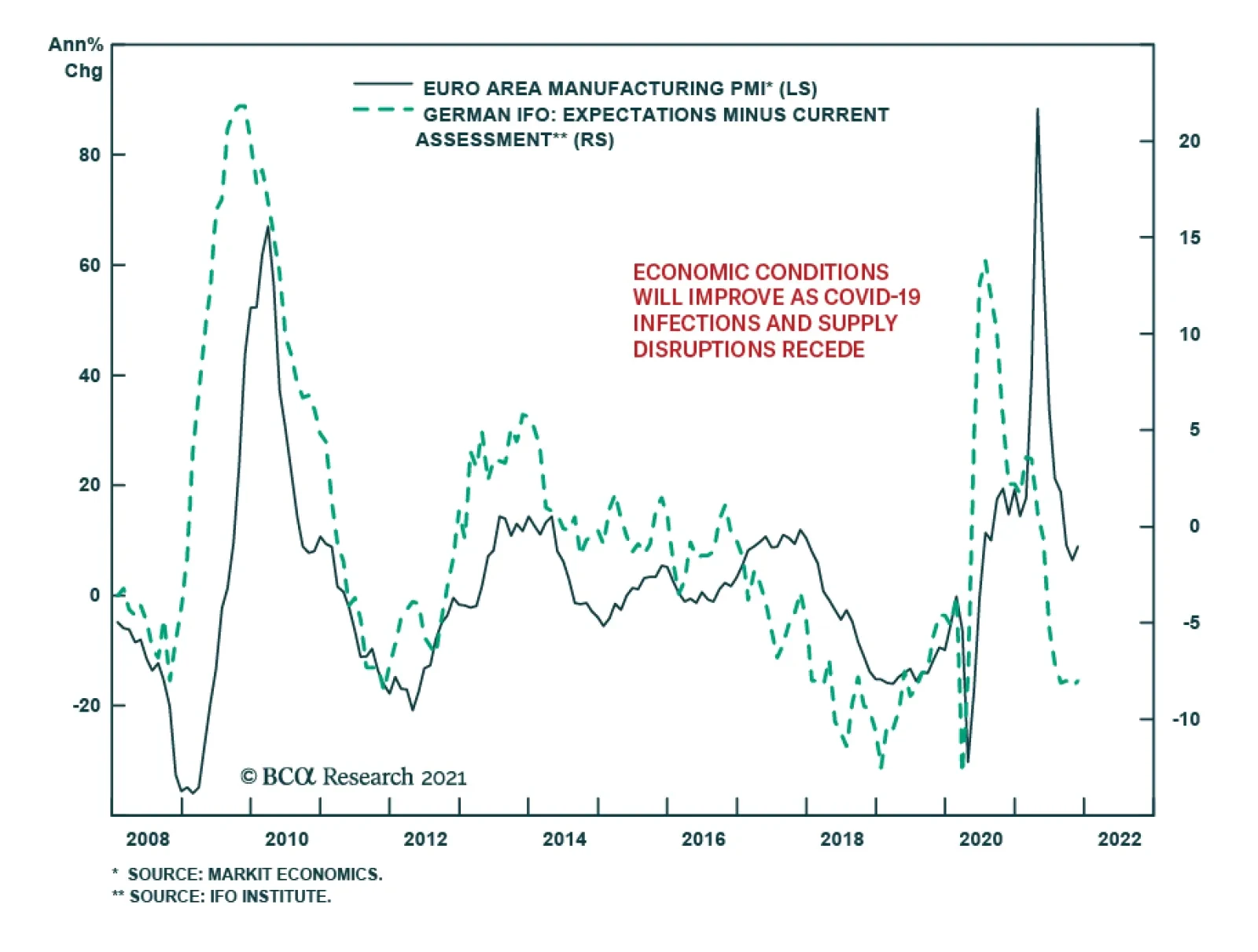

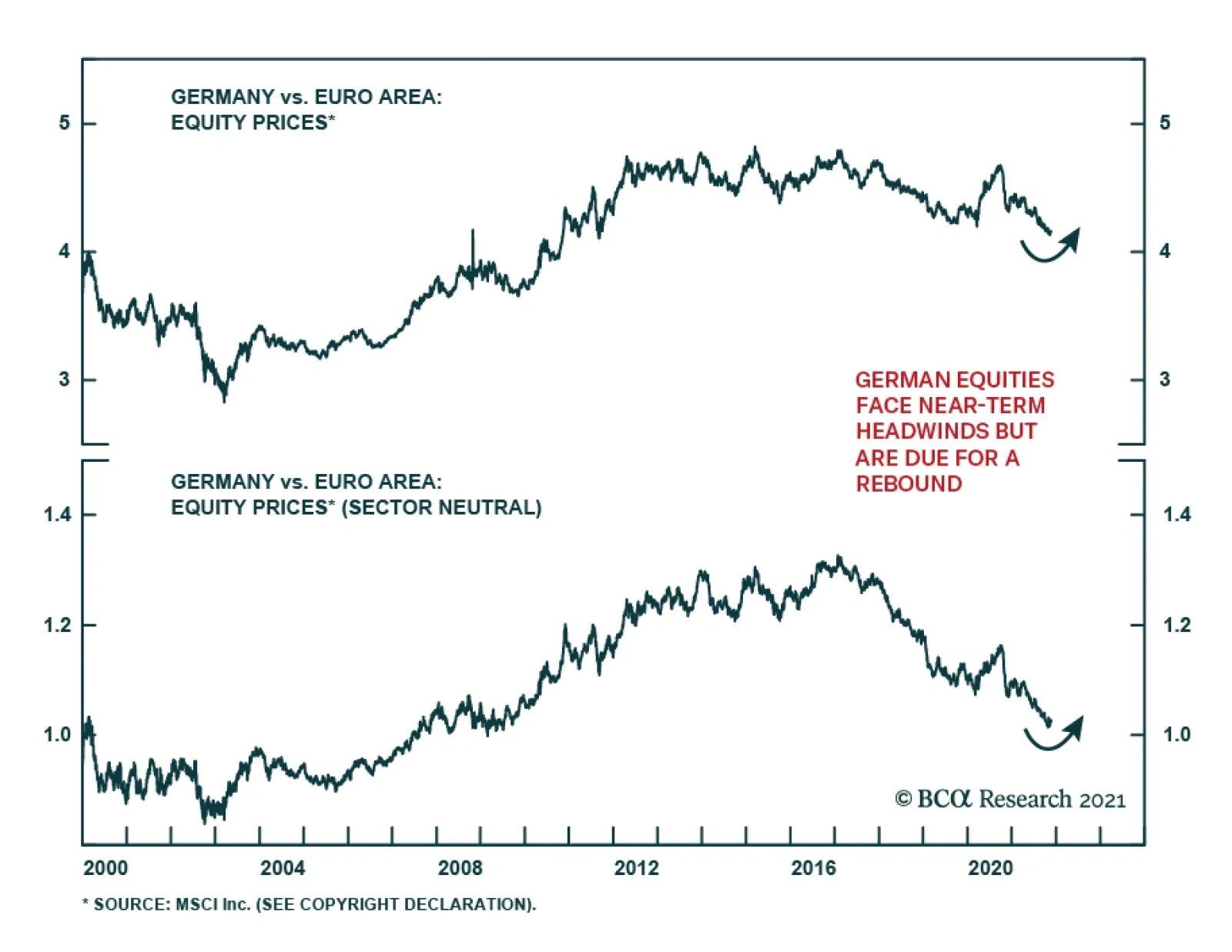

Euro Area

BCA Research is proud to announce a new feature to help clients get the most out of our research: an Executive Summary cover page on each of the BCA Research Reports. We created these summaries to help you quickly capture the main points of each report through an at-a-glance read of key insights, chart of the day, investment recommendations and a bottom line. For a deeper analysis, you may refer to the full BCA Research Report. Executive Summary Risk Premium In EU Gas Prices

Long-Term EU Gas Volatility Will Increase

Long-Term EU Gas Volatility Will Increase

Regardless of whether Russia invades all, part of or none of Ukraine again, its current standoff with the West will force the EU to reconfigure its gas markets to assure reliability of supplies, and remove geopolitical supply disruptions. We expect the EU's renewable energy taxonomy scheduled for release Wednesday will include natgas as a sustainable fuel, which will help build more diversified sources of supply and deeper spot and term markets. Success here will increase market share of natgas in EU power generation. In the short run (1-2 years), neither the EU nor Russia can afford Gazprom's pipeline supplies to be significantly curtailed. Over the medium term (3-5 years), alternative supplies from US and Qatari LNG exports will be required to deepen EU gas-market liquidity and supply. Longer term (i.e., beyond 2025), EU energy markets will remain volatile as the renewable-energy transition progresses. High and volatile natgas prices will translate into persistent EU inflation – particularly food prices, because of higher fertilizer costs, and base metals' prices. Shortages in these markets will slow the energy transition, and raise its price tag. Bottom Line: The Russian standoff with the West over Ukraine puts a higher risk premium in EU gas prices. We remain long commodity-index exposure (S&P GSCI, and COMT ETF), and the XME ETF. We are getting long the SPDR S&P Oil & Gas Exploration & Production ETF (XOP) at tonight's close. Feature We expect the EU's financial taxonomy for renewable energy scheduled for release Wednesday will include natgas as a sustainable fuel. This will help in building out more diversified sources of supply and deeper spot and term markets. Success here will increase the market share of natgas in the EU's power generation (Chart of the Week). This coincides with natural gas supply uncertainty, arising from geopolitical tensions. On the back of already-low inventory levels, European natural gas markets are forced to handicap the odds of a major curtailment of Russian pipeline gas supplies resulting from another invasion of Ukraine (Chart 2). This is keeping a significantly increased risk premium embedded in natgas prices: Russian exports to the EU account for 40% of total gas supplies. Germany is particularly exposed, as ~65% of its gas comes from Russia (Chart 3). Chart of the WeekEU Natgas Generation Will Rise In Energy Transition

Long-Term EU Gas Volatility Will Increase

Long-Term EU Gas Volatility Will Increase

BCA’s Geopolitical Strategy desk upgraded the odds of Russia invading Ukraine to 75% from 50% in its latest research report.1 Our colleagues, however, keep the probability of Russia invading all of Ukraine low. Their analysis concludes Russia will only invade a part of Ukraine, so as to argue for lighter sanctions being imposed on it by the West, as opposed to having to incur the full wrath of US and EU sanctions. The other 25% of the probability space includes a diplomatic settlement between the West and Russia. Chart 2Risk Premium In EU Gas Prices

Long-Term EU Gas Volatility Will Increase

Long-Term EU Gas Volatility Will Increase

While Russia has been trying to diversify its customer base – by increasing natgas exports to China, e.g. – data from the BP Statistical Review of World Energy shows ~ 78% of total natural gas exports (pipeline + LNG) from Russia went to the EU in 2020.2 Chart 3EU Highly Dependent On Russian Gas

Long-Term EU Gas Volatility Will Increase

Long-Term EU Gas Volatility Will Increase

In light of the fact that Russia likely will face watered-down sanctions, and the EU’s gargantuan share of total Russian exports, we do not believe Europe’s largest natural gas exporter will stop all supply to the EU now or in the near future. In case Russia does go through with its invasion, it likely will cut off natural gas supply to Ukraine, implying Europe will loose slightly more than 6% of total natgas imports as opposed to 40% in the event of a halt to all natgas exports to Europe (Chart 4). Gas consumption of the EU-27 in 2021 was ~ 500 Bcm, according to the Oxford Institute For Energy Studies (OIES). Some 85% of EU gas consumption was met by imports. Chart 4Imports Cover Most EU Gas Consumption

Long-Term EU Gas Volatility Will Increase

Long-Term EU Gas Volatility Will Increase

Can The EU Mitigate The Loss Of Russian Gas? The EU and the US have entered discussions with other countries to plug the potential 6% reduction in imports from Russia. While in theory, there is enough spare pipeline capacity to import natural gas from existing and new sources (Chart 5), practical limitations may prevent this from occurring.3 The US is working with the EU to ensure energy supply security in case Russia cuts off natural gas supply. However, as can be seen in Chart 6, Panel 1, the US currently is and likely will continue to export nearly at capacity until end-2023. Panel 2 shows global liquefaction also is nearly at capacity. Chart 5EU Gas Import Capacity Exists, But Filling It Will Be Problematic

Long-Term EU Gas Volatility Will Increase

Long-Term EU Gas Volatility Will Increase

Chart 6US LNG Export Capacity Maxed Out

Long-Term EU Gas Volatility Will Increase

Long-Term EU Gas Volatility Will Increase

While an increase in gas production at the earthquake-prone Groningen field in the Netherlands is theoretically viable, it will induce a public backlash, as was evidenced when the Dutch government announced plans to double output from the field earlier this year. In the short run, facing few sources of alternate gas supply, the EU will need to focus on curtailing demand. Fossil fuels will need to be considered as an alternative for electricity and heating, since nuclear is not used in all EU countries. The depth of this crisis and the Dutch TTF price rise will be capped by the fact that we expect the EU to lose a relatively small fraction of total imports. Further, while we expect Dutch TTF prices to be volatile and face upward pressure, any price increases also will be capped by the fact that the colder-than-expected Northern Hemisphere winter has not yet materialized, and the warmer Spring and Summer months will be approaching soon. Medium-, Long-Term EU Gas Supply On the supply side, over the medium- and long-term, the EU will need to deepen and stabilize its gas supply, so that firms and households can rationally forecast and allocate spending and investment. This would include finding back-up or alternative supplies to Russian imports, which carry with them uncertain geopolitical risk. If Brussels includes natural gas as a sustainable fuel in its energy taxonomy, over the medium term (3-5 years), alternative supplies from US and Qatari LNG exports will be required to deepen EU gas-market liquidity and supply. Longer term (i.e., beyond 2025), EU energy markets will remain volatile as the renewable-energy transition progresses. Natgas will be a critical component of this transition, until utility-scale battery storage is able to support renewable generation and grid stability. We believe over the remainder of this decade, high and volatile natgas prices will translate into persistent EU inflation, as pricing pressures spill into oil and coal markets at the margin, as happened over the course of last year. This will work in the other direction as well – e.g., higher coal prices will spill over into gas and oil markets as price pressures incentivize fuel switching at the margin. Food prices will be right in the inflationary cross-hairs, given the fertilizer required to produce the grains and beans consumed globally consists mostly of natgas in urea and ammonia fertilizers (Chart 7). This will feed into higher food prices (Chart 8). Chart 7High Natgas Prices Will Show Up In High Fertilizer Prices

High Natgas Prices Will Show Up In High Fertilizer Prices

High Natgas Prices Will Show Up In High Fertilizer Prices

Chart 8… And Higher Food Prices

Long-Term EU Gas Volatility Will Increase

Long-Term EU Gas Volatility Will Increase

Base metals' prices also will be upwardly biased as natgas price volatility remains elevated. Supply shortages in natgas markets will, at the margin, slow the energy transition by reducing reliable energy supplies in the EU, forcing states to compete for back-up and replacement supply in the global LNG markets. Fuel-switching into oil, gas and coal will transmit EU gas volatility to markets globally. Tight energy and base metals markets also will feed directly into higher inflation and inflation expectations (Chart 9). Chart 9Higher Commodity Prices Will Pressure Inflation Higher

Higher Commodity Prices Will Pressure Inflation Higher

Higher Commodity Prices Will Pressure Inflation Higher

Investment Implications The standoff between the West and Russia over the latter's amassing of troops on the Ukraine border, plus the marked increase in the tempo of Russian naval operations, will keep the risk premium in EU natgas prices high. This is not a sustainable equilibrium over the medium- to long-term. We expect little if any curtailment of Russian natgas exports over the short term; however, prudence suggests EU member states will be forced to find back-up and alternative gas supplies over the medium- to longer-term, as the global renewable-energy transition gains traction. The knock-on effects from the current European geopolitical standoff are keeping EU natgas prices elevated via a higher risk premium to cover possible supply losses. This will feed into other markets – particularly metals and ags – which will feed directly into inflation and inflation expectations. We remain long commodity index exposure – the S&P GSCI and the COMT ETF – and metals producers via the XME ETF. At tonight's close, we will be getting long the SPDR S&P Oil & Gas Exploration & Production ETF (XOP). Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish OPEC 2.0's decision to stay with its policy of returning 400k b/d every month appeared to be a foregone conclusion in the markets. In our January 2022 balances and price forecasts, we anticipated a larger increase, given the producer coalition led by Saudi Arabia and Russia has fallen significantly behind its goal of returning 400k b/d to the market monthly due to declining production among OPEC 2.0 member states ex-Gulf GCC member states, chiefly KSA, UAE and Kuwait (Iraq's exports fell in December and January; production data have not been released). In the past, KSA has said it will not make up for production shortfalls of OPEC 2.0 member states, and would abide by its production allocation. The upside risk to prices remains, in our estimation, and we continue to expect KSA and its GCC allies to increase output if production from the price-taking cohort led by the US shale-oil producers fails to materialize in over the coming months. Failure to cover production shortfalls among OPEC 2.0 member states would lift Brent prices by $6/bbl above our baseline forecast, which assumed higher production from the GCC states would be forthcoming at Wednesday's OPEC 2.0 meeting (Chart 10, brown curve). Base Metals: Bullish An environmental committee in Chile's Senate voted out a proposed bill that would, among other things, reportedly make it easier for the government to seize mines developed and operated by private companies. The proposed legislation still has a long road ahead of it, but copper prices rallied earlier in the week as this news broke. Even if the odds of the bill's passage are slim, a watered down version of the proposed legislation would markedly change the economic proposition of developing and maintaining copper mines in Chile (Chart 11). We continue to follow this closely. Chart 10

Brent Forecast Restored To $80/bbl For 2022

Brent Forecast Restored To $80/bbl For 2022

Chart 11

Bullish For Copper Prices

Bullish For Copper Prices

Footnotes 1 Please see All Bets Are Off ... Well, Some (A GeoRisk Update), published by BCA Research's Geopolitical Strategy service 27 January 2022. It is available at gps.bcaresearch.com. 2 Please see bp's Statistical Review of World Energy 2021 | 70th edition. 3 Norway, the EU’s second largest gas exporter after Russia stated that its natural gas production is at the limit. Apart from the issue of production, current LNG flows will need to be redirected from Asia and the Americas. Defaulting on long-term contracts to redirect fuel to Europe could mire exporters’ relationships with importing countries. Finally, infrastructure in the Eastern and Central section of the EU may not be equipped to receive supplies from the West, thus increasing costs and time associated with putting these systems in place. Investment Views and Themes Strategic Recommendations Trades Closed in 2021

Image

BCA Research is proud to announce a new feature to help clients get the most out of our research: an Executive Summary cover page on each of the BCA Research Reports. We created these summaries to help you quickly capture the main points of each report through an at-a-glance read of key insights, chart of the day, investment recommendations and a bottom line. For a deeper analysis, you may refer to the full BCA Research Report. Executive Summary Cyclical UST Curve Flattening, But With Unusually Low Rate Expectations

Deciphering The Messages From The US Treasury Curve

Deciphering The Messages From The US Treasury Curve

The US Treasury curve is unusually flat given high US inflation and with the Fed not having begun to raise interest rates. The dichotomy between deeply negative real interest rates and a flattening yield curve is not only evident in the US, but in other major developed countries like Germany and the UK. A low term premium on longer-term US Treasury yields is one factor keeping the curve so flat, but the term premium will likely rise as the Fed begins to hike rates. An overly flat US Treasury curve more likely reflects a belief that the neutral real fed funds rate (r-star) is actually negative. This is consistent with markets pricing in a very low peak in the funds rate for the upcoming tightening cycle, despite the current high inflation and tight labor market. Bottom Line: The Fed will hike by less than the market expects in 2022 and longer-term Treasury yields remain too low versus even a moderate 2-2.5% peak in the fed funds rate. Stay in US curve steepeners, as the Treasury curve is already too flat and will not flatten as much as discounted in forward rates this year. Feature Last week’s FOMC meeting essentially confirmed that the Fed will begin lifting rates in March and deliver multiple rate hikes this year. This was considered a hawkish surprise as the Fed signaled imminently tighter monetary policy even with the elevated financial market volatility seen so far in 2022. Fed Chair Jerome Powell noted that the US economy was in a stronger position compared to the 2016-18 tightening cycle, justifying a faster pace of hikes – and an accelerated pace of QE tapering – this time around. Markets have responded to the increasingly hawkish guidance of the Fed by pushing up rate expectations for 2022, continuing a path dating back to last September’s FOMC meeting when the Fed first signaled that QE tapering was imminent (Chart 1). There are now 163bps of Fed rate hikes by year-end discounted in the US overnight index swap (OIS) curve. Some Wall Street investment banks are calling for the Fed to hike as much as 6 or 7 times in 2022. We see this as much too aggressive. Chart 1Fed Hawkishness Pushing Up Rate Expectations For 2022/23 - But Not Beyond That

Fed Hawkishness Pushing Up Rate Expectations For 2022/23 - But Not Beyond That

Fed Hawkishness Pushing Up Rate Expectations For 2022/23 - But Not Beyond That

Our base case scenario calls for the Fed to lift rates “only” 3-4 times this year. The persistently high inflation that is troubling the Fed is likely to peak in the first half of 2022, taking some heat off the FOMC to move as aggressively as discounted in markets this year. Although inflation will remain high enough, and the labor market tight enough, to keep the Fed on a tightening path into 2023. The US Treasury Curve Looks Too Flat What is unique about the upcoming Fed tightening cycle is that it is starting with such a flat US Treasury curve. The spread between the 2-year and 10-year yield now sits at 61bps, the lowest level since October 2020. This dynamic is not unique to the US, as yield curves are quite flat in other major countries where policy rates are near 0% and inflation remains relatively high, like the UK and Germany (Chart 2). In the US, the modest slope of the Treasury curve is notably unusual given a growth and inflation backdrop that would be more consistent with much higher bond yields: The US unemployment rate fell to 3.9% in December, well within the range of full employment estimates from FOMC members (Chart 3, top panel) Chart 2Bond Bearish Yield Curve Flattening In The US & UK

Bond Bearish Yield Curve Flattening In The US & UK

Bond Bearish Yield Curve Flattening In The US & UK

US labor costs are accelerating; the wages and salaries component of the Employment Cost Index for Private Industry Workers rose to a 38-year high of 5.0% on a year-over-year basis in Q4/2021 (middle panel) Chart 3Challenges To The Fed's Inflation Fighting Credibility

Challenges To The Fed's Inflation Fighting Credibility

Challenges To The Fed's Inflation Fighting Credibility

Higher inflation is becoming more embedded in medium term consumer inflation expectations measures like the University of Michigan 5-10 year ahead series that climbed to 3.1% last month (bottom panel). Importantly, market-based measures of inflation expectations have pulled back, even with little sign of inflation pressures easing. The 5-year TIPS breakeven, 5-years forward has fallen 35bps from the October 2021 peak of 2.41%. The bulk of that decline occurred in January of this year, alongside a rising trend in real TIPS yields as markets began pricing in a faster pace of Fed rate hikes. TIPS breakevens can often be something of a “vote of confidence” by the markets in the appropriateness of the Fed’s policy stance; rising when policy appears overly stimulative and vice versa. Thus, the decline in the TIPS 5-year/5-year forward breakeven, which climbed steadily higher since the Fed introduced massive monetary easing in March 2020 in response to the pandemic, can be interpreted as a sign that markets agree with the Fed’s recent hawkish turn. However, while the move in TIPS breakevens is sensible, the flatness of the Treasury curve appears unusual. In Chart 4, where we look at the previous times since 1975 that the 2-year/10-year US Treasury spread flattened to 70bps (just above the current level). In past cycles, the Treasury curve would be flattening into such a level after the Fed had already hiked rates a few times, which is obviously not the case today. Also, US unemployment was typically approaching, or falling through, the full employment NAIRU when the 2/10 Treasury curve fell to 70bps, suggesting diminished spare economic capacity and rising inflation pressures – similar to the current backdrop. Chart 4The UST Curve Is Unusually Flat Right Now

The UST Curve Is Unusually Flat Right Now

The UST Curve Is Unusually Flat Right Now

Chart 5UST Curve Too Flat Relative To Inflation Pressures

UST Curve Too Flat Relative To Inflation Pressures

UST Curve Too Flat Relative To Inflation Pressures

In those past cycles, the funds rate was rising at a faster pace than that of core inflation, suggesting that the Fed was pushing up real interest rates. The backdrop looks very different today, with US realized inflation soaring and the real funds rate now deeply negative. In the top panel of Chart 5, we show a “cycle-on-cycle” chart of the 2/10 Treasury curve versus an average of the previous five instances where the curve flattened to 70bps. The green line is the median outcome of all the cycles, while the shaded region represents the range of all the outcomes. In the other panels of the chart, we show US economic variables (the Conference Board leading economic index and the ISM Manufacturing index) and US inflation variables (the wages and salaries component of the Employment Cost Index and the US Congressional Budget Office estimate of the US output gap). The panels are all lined up so that the vertical line in the middle of the chart represents the date that the 2/10 curve falls to 70bps. The conclusion from Chart 5 is that the US economic variables shown are currently at the high end of the range of past curve flattening episodes, but the inflation variables are well above the high end of the historical range. In other words, the current modest slope of the 2/10 Treasury curve is in line with US growth momentum but is too flat relative to US inflation trends. So Why Isn’t The US Treasury Curve Steeper? There are a few possible reasons why the US curve is as flat as it is before the Fed has even begun tightening amid above-trend US growth and very high US inflation: Fears of a deeper financial market selloff The Fed believes strongly in the role of financial conditions in transmitting its monetary policy into the US economy. That often means that, during tightening cycles, the Fed hikes rates “until something breaks” in the financial markets, like a major equity market downturn or a big widening in corporate credit spreads. Such moves act as a brake on US growth through negative wealth effects for investors and by raising the cost of capital for businesses – reducing the need for additional Fed tightening. If bond investors thought that a major market selloff was likely before the Fed could successfully lift rates back to neutral (or even restrictive) levels during a tightening cycle, then they would discount a lower peak level of the funds rate. This would also lower the expected peak level of longer-term Treasury yields, resulting in a flatter Treasury yield curve. Given the current elevated valuations on so many asset classes – like equities, corporate credit and housing – it is likely that the relatively flat Treasury curve incorporates some believe that the Fed will have difficulty delivering a lot of rate hikes in this cycle. However, it should be noted that the US financial conditions remain quite accommodative, even after the recent equity market turbulence (Chart 6), and represent no impediment to US growth that reduces how much tightening the Fed will need to do. Longer-term bond term premia are too low A relatively flat yield curve could reflect a lack of a term premium on longer-maturity bonds. That is certainly the case when looking at the slope of the 2/10 government yield curve in the US, as well as in the UK and Germany (Chart 7).1 Chart 6US Financial Conditions Are No Impediment To US Growth

US Financial Conditions Are No Impediment To US Growth

US Financial Conditions Are No Impediment To US Growth

Chart 7Flatter Yield Curves? Or Just Lower Bond Term Premia?

Flatter Yield Curves? Or Just Lower Bond Term Premia?

Flatter Yield Curves? Or Just Lower Bond Term Premia?

The term premium is the defined as the extra yield that investors require to commit to own a longer-maturity bond instead of the compounded yield from a series of shorter-maturity bonds. The latter can also be expressed as the “expected path of short-term interest rates”, which is often proxied by an average expected path of the monetary policy rate over the life of the longer-maturity bond. So the term premium on a 10-year US Treasury yield is the difference between the actual 10-year Treasury yield and the expected (or average) path of the fed funds rate over the next ten years. The term premium can also be thought of as a risk premium to holding longer-term bonds. On that basis, the term premium should correlate to measures of bond risk, like bond price volatility or inflation volatility. That is definitely true in the US, where the 10-year Treasury term premium shows a strong correlation to the MOVE index of Treasury market option-implied volatility or a longer-term standard deviation of headline CPI inflation (Chart 8). Estimated term premia can also rise during periods of slowing economic growth momentum, but that is typically due to a rapid decline in the expected path of interest rates rather than a rise in bond risk premia (in this case, this is probably more accurately described as a rise in bond uncertainty). Currently, a low term premium on US Treasury yields is justified by the relatively low level of bond volatility and solid US growth momentum. However, the term premium looks far too low compared to the more volatile US inflation seen since the start of the COVID-19 pandemic. With the Fed set to respond to that higher inflation with rate hikes, rising real interest rate expectations could also give a lift to the Treasury term premium. Our favorite proxy for the market expectation of the peak/terminal real short-term interest rate for the major developed market economies is the 5-year/5-year forward OIS rate minus the 5-year/5-year forward CPI swap rate. That “real” 5-year/5-year forward rate measure is typically well correlated to our estimates of the 10-year term premium in the US, Germany and the UK (Chart 9). This correlation likely reflects the level of certainty bond investors have over the likely future path of real interest rates. When there is more uncertainty about how high rates will eventually go to in a tightening cycle, a higher term premium is required. The opposite is true during periods of very low and stable interest rates. Chart 8Drivers Of US Term Premia Pointing Upward

Drivers Of US Term Premia Pointing Upward

Drivers Of US Term Premia Pointing Upward

Chart 9Bond Term Premia Positively Correlated To Real Rate Expectations

Bond Term Premia Positively Correlated To Real Rate Expectations

Bond Term Premia Positively Correlated To Real Rate Expectations

Chart 10Global Yield Curves Are Too Flat Versus Real Policy Rates

Global Yield Curves Are Too Flat Versus Real Policy Rates

Global Yield Curves Are Too Flat Versus Real Policy Rates

Currently, the estimated 10-year US term premium is increasing alongside a rising market-implied path for the real fed funds rate. We anticipate these trends will continue as the Fed lift rates over the next couple of years, boosting longer-term Treasury yields and potentially putting some steepening pressure on the US Treasury curve (or at least limiting the degree of flattening as the Fed tightens). Markets believe that the neutral real rate (r*) is negative Historically, yield curve slopes for government bonds were well correlated to the level of real interest rates, measured as the central bank policy rate minus headline inflation. That relationship has broken down in the US, with the Treasury curve flattening in the face of soaring US inflation and an unchanged fed funds rate (Chart 10). Similar dynamics can also be seen in the German and UK yield curves. The most plausible reason for such a dramatic shift in the relationship between curve slopes and real policy rates is that bond investors now believe that the neutral real interest rate, a.k.a. “r-star”, is negative … and perhaps deeply so. The New York Fed has produced estimates of the US r-star dating back to the 1960s. The gap between the real fed funds rate and that r-star estimate has typically been fairly well correlated to the slope of the Treasury curve (Chart 11). When the real fed funds rate is below r-star, indicating that the policy is accommodative, the Treasury curve is usually steepening, and vice versa. Under this framework, the recent flattening trend of the Treasury curve would indicate that policy is actually getting tighter, despite the falling, and deeply negative, real fed funds rate of -5.4% (deflated by core inflation). Chart 11UST Curve Slope Is Positively Correlated To The 'Real Policy Gap'

UST Curve Slope Is Positively Correlated To The 'Real Policy Gap'

UST Curve Slope Is Positively Correlated To The 'Real Policy Gap'

The last known estimate of r-star from the New York Fed was 0%, but no update has been provided for almost two years. Blame the pandemic for that. The sharp lockdown-fueled collapse in US GDP growth in 2020, and the rapid recovery in growth as the economy reopened, made it impossible to estimate the the “neutral” level of real interest rates given such massive swings in demand that were not related to monetary policy. One way to try and “back out” the implicit pricing of r-star currently embedded in US Treasury yields is to estimate a model linking the gap between the real fed funds rate and r-star to the slope of the Treasury curve. We did just that, with the results presented in Chart 12. This model estimates the “Real Policy Gap”, or r-star minus the real fed funds rate, as a function of the 2/10 Treasury curve slope. In other words, the model shows the Real Policy Gap that is consistent with the current slope of the curve. Chart 12Current UST Yield Curve Makes Slope Sense ... If The Fed Followed The Taylor Rule With 7% Inflation

Current UST Yield Curve Makes Slope Sense ... If The Fed Followed The Taylor Rule With 7% Inflation

Current UST Yield Curve Makes Slope Sense ... If The Fed Followed The Taylor Rule With 7% Inflation

The model estimates that the current 2/10 curve slope is consistent with a Real Policy Gap of 96bps. With US core CPI inflation currently at 5%, and assuming r-star is still 0% as per the last New York Fed estimate, the fed funds rate would have to rise to 4% to justify the current slope of the 2/10 curve. While that may sound like an implausibly large increase in the funds rate, similar results are produced using straightforward Taylor Rules.2 We can also use our Real Policy Gap model to infer the level of inflation that is consistent with a Gap of 96bps, for various combinations of the funds rate and r-star. Those are shown in Table 1. Assuming the funds rate rises in line with current market expectations to 1.7% and r-star remains close to 0%, the current slope of the 2/10 Treasury curve suggests a fall in US inflation to just around 3% - still above the Fed’s inflation target - from the current 5%. Table 1The UST Curve Slope Has Already Discounted A Big Drop In US Inflation

Deciphering The Messages From The US Treasury Curve

Deciphering The Messages From The US Treasury Curve

We see this as the most plausible reason for the relatively flat level of the 2/10 US Treasury curve. Markets expect somewhat lower US inflation and a moderate rise in the funds rate over the next couple of years, making the real funds rate less negative but not pushing it above a negative r-star expectation. This would suggest upside risk for US Treasury yields, and potential bearish steepening pressure, as markets come to realize that the neutral real fed funds rate is actually positive, not negative. Fight The Forwards, Stay In US Treasury Curve Steepeners While it may sound counter-intuitive with the Fed set to begin a rate hiking cycle, we continue to see better value in tactically positioning in US Treasury curve steepening trades. Specifically, we are keeping our recommended trade in our Tactical Overlay on page 19, where we are long a 2-year Treasury bullet versus a duration-neutral barbell of cash (a 3-month US Treasury bill) and a 10-year Treasury bond. The trade is currently underwater, but we see good reasons to expect the performance to rebound over the next few months. The front end of the curve now discounts more hikes than we expect will unfold in 2022, which should limit further increases in the 2-year Treasury yield. At the same time, the 10-year yield looks too low relative to the expected cyclical peak for the fed funds rate (Chart 13). One way we can assess this is by comparing 5-year/5-year forward Treasury rates to survey estimates of the longer run, or terminal, fed funds rate. The median FOMC forecast (or “dot”) for the terminal funds rate is 2.5%, the median terminal rate forecast from the New York Fed’s Survey of Primary Dealers is 2.25% and the median terminal rate forecast from the New York Fed’s Survey of Market Participants is 2%. This sets a range of estimates of the longer-run terminal rate of 2-2.5%, in line with the current expectations of the BCA Research bond services. The current 5-year/5-year forward Treasury rate is 2.0%, at the low end of that range. We see those forwards rising to the upper part of that 2-2.5% range by the end of 2022, which will push the 10-year Treasury yield toward our year-end target of 2.25%. Chart 13The 5-Year/5-Year UST Forward Rate Is Too Low

The 5-Year/5-Year UST Forward Rate Is Too Low

The 5-Year/5-Year UST Forward Rate Is Too Low

Chart 14Stay In UST Curve Steepeners, Even With Fed Liftoff Imminent

Stay In UST Curve Steepeners, Even With Fed Liftoff Imminent

Stay In UST Curve Steepeners, Even With Fed Liftoff Imminent

Some of our colleagues within the BCA family see the longer-term neutral funds rate as considerably higher than survey estimates, perhaps as high as 3-4%. We are sympathetic to that view, but it will take signs of US economic resiliency in the face of rate hikes before bond investors – and more importantly, the Fed – arrive at that conclusion. This would make steepening trades more attractive on a strategic, or medium-term, basis as the market realizes that the Fed is further behind the policy curve (i.e. the funds rate even further below a higher terminal rate) than previously envisioned. For now, we do not see the US Treasury curve flattening at the pace discounted in the Treasury forward curve over the next 3-6 months (Chart 14, top panel). However, this will be more of a carry trade by betting against the forwards over time. A bearish steepening of the Treasury curve with a swift upward move in the 10-year Treasury yield is less likely with bond investor/trader positioning already quite short (bottom two panels). Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 The term premium estimates shown here are derived from our own in-house framework. For those familiar with the various term premium estimates on the 10-year US Treasury yield produced by the Fed, our estimates are currently in line with those produced by the ACM model and the Kim & Wright model. 2 A fun US Taylor Rule calculator, which can be used to generate Taylor Rules under a variety of assumptions, is available on the Atlanta Fed’s website here. GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

Deciphering The Messages From The US Treasury Curve

Deciphering The Messages From The US Treasury Curve

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index Global Fixed Income - Strategic Recommendations* Duration Regional Allocation Spread Product Tactical Overlay Trades

Highlights US Vs. Europe: Growth and inflation momentum remains stronger in the US versus Europe. The latter is taking the bigger economic hit from more severe Omicron economic restrictions and a greater exposure to slowing Chinese demand. European inflation has accelerated, but remains slower and less broad-based than elevated US inflation. The backdrop remains more negative for US fixed income compared to Europe. UST-Bund Spread: With markets already priced for multiple Fed rate hikes in 2022, it is now harder to earn significant returns shorting US Treasuries outright compared to 2021. We prefer positioning for higher US bond yields through less-volatile US Treasury-German Bund spread widening positions, with the ECB unlikely to deliver even the single discounted 2022 rate hike. We recommend the position both as a structural allocation in bond portfolios (underweight the US versus Germany) and as a tactical trade (selling US Treasury futures versus Bund futures). Feature Chart of the WeekUS Bond Yields & Bond Volatility Are Both Rising

US Bond Yields & Bond Volatility Are Both Rising

US Bond Yields & Bond Volatility Are Both Rising

Global fixed income markets are off to a volatile start in 2022, on the back of significant repricing of US interest rate expectations. The 10-year US Treasury yield now sits at 1.85%, up +34bps so far in January and is up +72bps from the August 4/2021 intraday low of 1.13%. The 2-year US yield, which is even more sensitive to changes in Fed expectations, is 1.04%, up +31bps so far this month and up +87bps since early August 2021. Yields are rising in other countries as well, with the 10-year benchmark government bond yield up year-to-date in the UK (+24bps), Canada (+45bps) and even Germany (+18bps) where the Bund yield is threatening to return to positive territory. US Treasuries are selling off as markets have heeded the hawkish shift in the Fed’s interest rate guidance. The US overnight index swap (OIS) curve now discounting 89bps of Fed rate hikes in 2022. Bond volatility further out the Treasury curve has increased as yields have moved higher, with the realized volatility of the Bloomberg 7-10 US Treasury index now at an 19-month high (Chart of the Week). We continue to recommend a defensive strategic posture towards direct US Treasuries with below-benchmark exposure on both duration and country allocations in global bond portfolios. However, we prefer a more efficient way to position for the same theme of rising US yields – betting on a wider 10-year US Treasury-German Bund spread. US Growth & Inflation Fundamentals Support A More Hawkish Fed The rise in global bond yields seen in recent weeks has inflicted damage on risk assets, but not in a consistent fashion. Equity markets have taken the brunt of the hit, with the S&P 500 down around -3% so far in January with the tech-heavy NASDAQ down -6%. Yet the MSCI emerging market equity index is up around +1%, European equities are flat and global high-yield corporate bond spreads are essentially unchanged so far this month. While higher bond yields are reflecting expectations of more global monetary tightening over the next year, medium-term interest rate expectations remain subdued. Our proxy for the market pricing of terminal interest rate expectations – 5-year OIS rates, 5-years forward – remains at or below pre-pandemic levels in the US, the UK, Canada and the euro area (Chart 2). Risk assets are performing relatively well in the face of higher bond yields because markets still do not believe that a major increase in interest rates will be needed in the current global tightening cycle. We see this – the likelihood that interest rates will have to rise much more than markets expect - as the biggest vulnerability for global bond markets over the next couple of years. The US remains the “poster child” for this view. In the US, core CPI inflation accelerated to an 31-year high of 5.5% in December. The pickup in US inflation continues to be broad-based, with the Cleveland Fed median CPI and trimmed mean CPI inflation measures reaching 3.8% and 4.8%, respectively (Chart 3). This massive run-up in US inflation has filtered through to medium-term household inflation expectations; the preliminary University of Michigan consumer survey for January showed that inflation 5-10 years out is expected to be 3.1% - the highest level in 13 years. Chart 2Rising Yields Are Not A Threat To Risk Assets ... Yet

Rising Yields Are Not A Threat To Risk Assets ... Yet

Rising Yields Are Not A Threat To Risk Assets ... Yet

Chart 3The Fed Cannot Ignore Elevated Inflation Expectations

The Fed Cannot Ignore Elevated Inflation Expectations

The Fed Cannot Ignore Elevated Inflation Expectations

Chart 4US Demand Steadily Normalizing From The Pandemic Shock

US Demand Steadily Normalizing From The Pandemic Shock

US Demand Steadily Normalizing From The Pandemic Shock

While much of the run-up in US inflation over the past year has been fueled by supply chain disruption and high energy prices, there is still a robust demand component to the high inflation. Consumer spending on goods remains elevated versus its pre-pandemic trend, while services spending is steadily returning back to the pre-pandemic pace (Chart 4). The overall US unemployment rate is now down to 3.9%, the lowest level since February 2020, with broad-based strength in the US labor market across most industries (bottom panel). The rise in consumer inflation expectations has to be most worrisome to Fed officials. Yes, market-based inflation expectations have already seen a significant run-up since the mid-2020 lows, and have even drifted down a bit of late on the back of the more hawkish rhetoric from the Fed. However, survey-based measures of inflation expectations tend to be less volatile than market-based measures, and typically follow trends in realized inflation, which is not slowing down in the US. In other words, rising household inflation expectations are a more reliable indication that an inflationary mindset is becoming entrenched in consumer behavior. US inflation dynamics are transitioning away from supply-driven goods inflation toward more lasting domestically driven forces like tight labor markets, faster wage growth and rising housing costs (Chart 5). Measures of supply chain disruption like global shipping costs are showing signs of peaking (top panel), while commodity price momentum has clearly rolled over – both should eventually feed into slower goods inflation this year. At the same time, tight labor markets will continue to boost US employment costs, which historically have been strongly correlated to US services inflation (middle panel). Chart 5US Inflation Pressures Remain Intense

US Inflation Pressures Remain Intense

US Inflation Pressures Remain Intense

Meanwhile, shelter costs, which represents 32% of the US CPI index, were up 4.2% on a year-over-year basis in December and are likely to continue accelerating given a dearth of housing supply versus demand that is pushing up both house prices and rents (bottom panel). Tying it all together, there are good reasons why the Fed has ramped up the hawkish rhetoric over the past couple of months. However, with the US OIS curve now discounting between 3-4 rate hikes in 2022, it will be harder to generate a second consecutive year of negative returns in the US Treasury market this year. Dating back to the early 1970s, there have only been five calendar years where the Bloomberg US Treasury index delivered an outright negative total return: 1994, 1999, 2009, 2013 and 2021 (Chart 6). None of the four cases prior to last year saw negative returns in the following year, as Treasury yields fell in 1995, 2000, 2010, 2014. Yet even the episodes that saw consecutive years of US yield increases – 1974-75, 1977-81, 1987-88, 2005-06 and 2015-16 – did not see outright negative returns from the Bloomberg US Treasury index. Chart 6Negative Return Years For US Treasuries Are Rare

Negative Return Years For US Treasuries Are Rare

Negative Return Years For US Treasuries Are Rare

Given the starting point of deeply negative real US bond yields, and interest rate expectations that remain too low beyond 2022, we still see value in staying below-benchmark on US duration exposure on a medium-term basis. However, we see a more efficient way to play for higher Treasury yields this year by positioning US Treasury underweights/shorts versus overweights/longs in government bonds in a region where discounted rate hikes will not happen – Europe. The ECB Is In No Hurry To Hike Rates The same supply driven factors that have pushed up US inflation over the past year have also lifted inflation in the euro area. Headline HICP inflation reached an 30-year high of 5.0% in December, while core HICP inflation hit an all-time high of 2.6%. The European Central Bank (ECB), however, is unlikely to deliver any rate hikes in 2022 even with the high inflation, for several reasons (Chart 7): Growth momentum entering 2022 was soft, thanks to Omicron related economic restrictions at the end of 2021 and also weak demand for European exports from China. It will take time for both of those factors to reverse, thus reducing any growth related pressure to tighten monetary policy. Inflation expectations are not exceeding the ECB 2% inflation target, with the 5-year/5-year forward EUR CPI swap now at 1.9% even with headline inflation of 5.0%. The surge in European energy prices will eventually subside in the first half of 2022, which will reduce inflationary pressure on the ECB to tighten. The ECB is ending its pandemic emergency bond buying program (PEPP) in March, and is only partially replacing that buying activity by upsizing its existing pre-pandemic asset purchase program (APP). The ECB will not want to compound the effect of this “tapering” of bond buying by also hiking interest rates, which would surely tighten financial conditions further through higher Italian government bond yields, rising corporate bond yields and a firmer euro. There is little evidence to date showing any pass-through of higher energy-fueled inflation into more domestically-driven inflation. Euro area wage growth was only 1.3% as of the latest available data in Q3/2021 (which is still well after realized inflation had started to accelerate), highlighting the lack of visible “second round” effects on euro area inflation from high energy prices that would prompt the ECB to consider rate hikes (Chart 8). Chart 7An ECB Rate Hike In 2022 Is Unlikely

An ECB Rate Hike In 2022 Is Unlikely

An ECB Rate Hike In 2022 Is Unlikely

Chart 8Limited 'Second Round' Effects From Energy-Driven European Inflation

Limited 'Second Round' Effects From Energy-Driven European Inflation

Limited 'Second Round' Effects From Energy-Driven European Inflation

The EUR OIS curve is discounting 7bps of rate hikes by year-end. Even that modest amount will not be delivered, which will limit how much further European government bond yields will rise this year. A Better Mousetrap: Playing UST Bearishness Through UST-Bund Spread Widening Trades Combining our view of an increasingly hawkish Fed and a still-dovish ECB produces our highest conviction investment recommendation for 2022: positioning for a wider 10-year US Treasury/Germany Bund spread. This can be done by underweighting the US versus core Europe in global bond portfolios, or shorting US Treasury futures versus German Bund futures as we are already recommending in our Tactical Trade Overlay (see page 15). A Treasury-Bund spread widening view is a more efficient way to play for a more hawkish Fed and higher US Treasury yields, for several reasons: There are many examples over past 30 years where the Treasury-Bund spread widened in consecutive years (Chart 9). This is in contrast to the fewer occurrences of consecutive years of rising Treasury yields shown earlier in this report. Thus, there are better odds that last year’s Treasury-Bund spread widening can be repeated in 2022. Chart 9Consecutive Years Of A Rising UST-Bund Spread Happen Often

Consecutive Years Of A Rising UST-Bund Spread Happen Often

Consecutive Years Of A Rising UST-Bund Spread Happen Often

The realized volatility of Treasury-Bund spread trades is almost always lower than that of an outright short position in US Treasuries, but the direction of returns of the two trades is similar (Chart 10). This shows that there is directionality in the Treasury-Bund spread (i.e. it is driven far more by the movements of US yields), but that is a welcome feature given our more bearish view on US Treasuries. The Treasury-Bund spread remains well below fair value on our fundamental valuation model, with fair value increasing due to widening US-European inflation differentials (Chart 11). Tighter relative monetary policies this year (more tapering and rate hikes from the Fed compared to the ECB) also favor a wider fair value spread on our model. Chart 10UST-Bund Wideners Have Lower Volatility Than Outright UST Shorts

UST-Bund Wideners Have Lower Volatility Than Outright UST Shorts

UST-Bund Wideners Have Lower Volatility Than Outright UST Shorts

Chart 11The UST-Bund Spread Looks Very Cheap On Our Model

The UST-Bund Spread Looks Very Cheap On Our Model

The UST-Bund Spread Looks Very Cheap On Our Model

The gap between our 24-month discounters, which measure the change in policy interest rates over the next two years discounted in OIS curves, for the US and euro area is a reliable leading indicator of the 10-year Treasury-Bund spread (Chart 12, bottom panel). The “discounter spread” is currently calling for the Treasury-Bund spread to widen by more than the current path discounted in US Treasury and German Bund forward rates. Chart 12Position For More UST-Bund Spread Widening In 2022

Position For More UST-Bund Spread Widening In 2022

Position For More UST-Bund Spread Widening In 2022

Chart 13UST-Bund Spread Is Not Technically Stretched

UST-Bund Spread Is Not Technically Stretched

UST-Bund Spread Is Not Technically Stretched

The Treasury-Bund spread is not stretched from a technical perspective (Chart 13). The spread is sitting right at its 200-day moving average and the 26-week change in the spread (a measure of price momentum) is rising but remains well below previous peak levels that have capped past spread increases. Summing it all up, the case is strong for including US-Germany spread widening positions as core holdings in investor portfolios in 2022. The current spread is 185bps and we have a year-end target of 225bps. Bottom Line: With markets already priced for multiple Fed rate hikes in 2022, it is now harder to earn significant returns shorting US Treasuries outright compared to 2021. We prefer positioning for higher US bond yields through less-volatile US Treasury-German Bund spread widening positions, with the ECB unlikely to deliver even the single discounted 2022 rate hike. We recommend the position both as a structural allocation in bond portfolios (underweight the US versus Germany) and as a tactical trade (selling US Treasury futures versus Bund futures). Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Recommendations Duration Regional Allocation Spread Product Tactical Trades GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

Image

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Highlights 2022 Key Views & Allocations: Translating our 2022 global fixed income Key Views into recommended positioning within our model bond portfolio results in the following conclusions to begin the year. Target a moderate level of overall portfolio risk, maintain below-benchmark overall duration exposure, make developed market government bond country allocations based on relative expected central bank hawkishness (underweight the US, UK and Canada; overweight Germany, France, Italy, Australia, Japan), and be selective on allocations to global spread product (overweight high-yield with a bias toward Europe over the US, neutral global investment grade, underweight emerging market hard currency debt). Specific Allocation Changes: Much of the current positioning in our model bond portfolio already reflects our 2022 investment themes. The only significant changes we make to begin the year are reducing emerging market USD-denominated corporate bond exposure to underweight, and shifting some high-yield corporate bond exposure from the US to Europe. Feature In our last report of 2021, we published our 2022 Key Views, outlining the themes and investment implications of the 2022 BCA Outlook for global fixed income markets. In this report, our first of the new year, we translate those views into more specific recommendations and allocations within the BCA Research Global Fixed Income Strategy model bond portfolio. The main takeaways are that another year of expected above-trend global growth, even after the risks to start the year from the Omicron variant, will further absorb spare capacity across the developed economies. Realized inflation will slow from the elevated readings of 2021, but will remain high enough to force central banks – led by the US Federal Reserve – to incrementally remove highly accommodative monetary policies put in place during the pandemic. The backdrop for global bond markets will turn far less friendly as a result, with higher bond yields (led by US Treasuries), flatter yield curves and much weaker returns on spread products that have benefited from easy monetary policies like investment grade corporate debt and emerging market (EM) hard currency debt. Against this challenging backdrop for overall fixed income returns, bond investors will need to focus more on relative exposures between countries, sectors and credit ratings to generate outperformance versus benchmarks. Our recommended portfolio allocations to begin 2022 reflect that shift (Table 1). Table 1GFIS Model Bond Portfolio Recommended Positioning For The Next Six Months

Our Model Bond Portfolio Strategy To Begin 2022: Choosing Our Battles Wisely

Our Model Bond Portfolio Strategy To Begin 2022: Choosing Our Battles Wisely

A Review Of The Model Bond Portfolio Performance In 2021 Chart 12021 Performance: A Positive, Yet Volatile, Year

2021 Performance: A Positive, Yet Volatile, Year

2021 Performance: A Positive, Yet Volatile, Year

Before we begin our discussion of the model bond portfolio for 2022, we will take a final look back at the performance of the portfolio in 2021. Last year, the model bond portfolio delivered a small negative total return (hedged into US dollars) of -0.51%, but this still outperformed its custom benchmark index by +36bps (Chart 1).1 It was a very challenging year for global fixed income markets, in aggregate, with significant swings in bond yields (i.e. US Treasuries were up in Q1, down in Q2/Q3, up then down in Q4) and credit spreads (US high-yield spreads fell in H1/2021 and were rangebound in H2/2021, while EM hard currency spreads were stable in H1/2021 before steadily widening during the rest of the year). Over the full year, the government bond portion of the portfolio outperformed the custom benchmark index by +27bps while the spread product segment outperformed by +9bps (Table 2). The bulk of that government bond outperformance occurred during the first quarter of the year when global bond yields surged higher as COVID-19 vaccines began to be distributed and economic optimism improved in response – trends that benefited the below-benchmark duration tilt within the portfolio. The credit market outperformance was more evenly spread out during the final nine months of the year. Table 2GFIS Model Bond Portfolio Full Year 2021 Overall Return Attribution

Our Model Bond Portfolio Strategy To Begin 2022: Choosing Our Battles Wisely

Our Model Bond Portfolio Strategy To Begin 2022: Choosing Our Battles Wisely

In terms of specific country exposures on government debt (Chart 2), our underweight stance on US Treasuries (both in allocation and duration exposure) generated virtually all of the full-year outperformance of the government bond portion of the portfolio (+38bps versus the benchmark). The biggest underperformer was the UK (-9bps), concentrated at the very end of the year as Gilt yields declined on the back of the Omicron surge, to the detriment of our underweight stance. All other country allocations provided little excess return, in aggregate, over the full year in 2021 – although there was significant variance of those returns during the year.

Chart 2

Within spread product (Chart 3), the biggest gains were seen in US high-yield (+19bps) where we remained overweight throughout 2021. The largest drag on performance came from UK investment grade corporates (-9bps), although this all came in Q1/2021 where we maintained an overweight stance at the time and spreads widened. Other spread product sectors delivered little in the way of excess return, although that should not be a surprise as we maintained a neutral stance on US and euro area investment grade corporates – which have a combined 18% weighting within the model bond portfolio custom benchmark index – throughout 2021.

Chart 3

In the end, our recommended portfolio tilts during 2021 were generally on the right side of the market, with our overweights outperforming in an overall down year for bond returns (Chart 4). The numbers would have been even better without the drag on performance in the fourth quarter (-17bps for the entire portfolio). That came entirely from our two biggest government bond underweights – US Treasuries and UK Gilts – which saw significant bond yield declines in response to the emergence of the Omicron variant. (the detailed breakdown of the Q4/2021 performance can be found in the Appendix on pages 19-23).

Chart 4

Importantly, the surge in bond yields seen in the first week of 2022 has already resulted in a full recovery of that Q4/2021 underperformance, providing a good start to the new year for our model portfolio. Top-Down Bond Market Implications Of Our Key Views We now present the specific fixed income investment recommendations that derive from those themes, described along the following lines: overall portfolio risk, overall duration exposure, country allocations within government bonds, yield curve allocations within countries, and corporate credit allocations by country and credit rating. Overall Portfolio Duration Exposure: BELOW BENCHMARK As we concluded in our 2022 Key Views report, longer-maturity government bond yields are now too low given the mix of very high inflation and very low unemployment seen in many countries. While we expect inflation to come down this year from the very rapid pace of 2021, it will not be by enough to force central banks off the path towards rate hikes that already began at the end of last year in places like the UK and New Zealand. The Fed is now signaling that multiple US rate hikes are likely in 2022, while even some European Central Bank (ECB) officials are expressing concern over very high European inflation. Longer maturity bond yields remain too low, in our view, because investors are discounting very low terminal rates – the peak level of policy rates to be reached in the next monetary tightening cycle. (Chart 5). An upward adjustment of global interest rate expectations is likely this year as central banks like the Fed and the Bank of England (BoE) deliver on expected rate hikes, with more tightening necessary beyond 2022. This will be the primary driver of the rise in global bond yields that we expect this year - an outcome that has already begun in the first week of 2022. Chart 5Global Government Bond Yields Vulnerable To Hawkish Repricing

Global Government Bond Yields Vulnerable To Hawkish Repricing

Global Government Bond Yields Vulnerable To Hawkish Repricing

Chart 6Staying Below-Benchmark On Overall Duration Exposure

Staying Below-Benchmark On Overall Duration Exposure

Staying Below-Benchmark On Overall Duration Exposure

We ended 2021 with a model bond portfolio duration that was -0.65 years below that of the custom performance benchmark (Chart 6). We feel comfortable maintaining that position, in that size, to begin the new year. Government Bond Country Allocation: OVERWEIGHT THE EURO AREA (CORE & PERIPHERY), JAPAN & AUSTRALIA; UNDERWEIGHT THE US, UK & CANADA Our country allocation decisions within our model bond portfolio entering 2022 are based on a simple framework. We are overweighting countries where central banks are less likely to raise rates this year, and vice versa. We expect the largest increase in developed market bond yields in 2022 to occur in the US, as markets are still not priced for the cumulative tightening that the Fed will likely deliver over the next couple of years. Markets are also underpricing how much the Bank of England and Bank of Canada will need to raise rates over the full tightening cycle, even with multiple hikes discounted for 2022. We see the necessary upward repricing of post-2022 rate expectations in all three of those countries – the US, UK and Canada – justifying underweight allocations in our model portfolio. Chart 7Our Recommended DM Government Bond Allocations To Start 2022

Our Recommended DM Government Bond Allocations To Start 2022

Our Recommended DM Government Bond Allocations To Start 2022

The opposite is true in core Europe and Australia. Overnight index swap (OIS) curves are discounting multiple rate hikes this year from the Reserve Bank of Australia (RBA) and even an ECB rate hike later in 2022. As we discussed in our Key Views report, there is still not enough evidence pointing to rapid wage growth in Australia or Europe that would force the RBA and ECB to turn more hawkish than their current forward guidance which calls for no rate hikes in 2022. While both central banks may talk about the possibility that monetary policy will need to be tightened, we expect the actual rate hikes to occur in 2023 and not 2022. Thus, both markets justify overweight allocations in our model bond portfolio. We are also maintaining an overweight to Japanese government bonds, as Japanese inflation remains far too low – even in an environment of high energy prices and global supply chain disruption – for the Bank of Japan to contemplate any tightening of monetary policy. The country allocations within the model portfolio as of the end of 2021 all fit with the above analysis, thus we see no major changes that need to be made to begin 2022 (Chart 7).2 The only significant move made was to slightly bump up the size of the overweights in Italy and Spain, to be funded by the reduction in EM corporate bond exposure (as we discuss below). We continue to see a positive case for owning Peripheral European government bonds for the relatively high yields within Europe, with the ECB maintaining an overall dovish policy stance in 2022 even as it scales back the size of its bond buying activity starting in March. Inflation-Linked Bond Allocations: MAINTAIN A NEUTRAL OVERALL ALLOCATION TO GLOBAL LINKERS Chart 8Our Recommended Inflation-Linked Bond Allocations To Start 2022

Our Recommended Inflation-Linked Bond Allocations To Start 2022

Our Recommended Inflation-Linked Bond Allocations To Start 2022

Inflation-linked bonds have been a necessary part of bond investors' portfolios since the lows in global inflation breakeven spreads were seen in mid-2020. Now, with inflation expectations at or above central bank inflation targets in most developed market countries, and with realized inflation likely to subside from current levels this year, the backdrop no longer justifies structural overweights to linkers across all countries. We are sticking with our end-2021 overall neutral allocation to global inflation-linked bonds, focusing more on country allocations based on our inflation breakeven valuation indicators, as discussed in our 2022 Key Views report (Chart 8). This means maintaining a neutral stance on US TIPS and linkers (vs. nominal government bonds) in Canada, Australia and Japan. We are also staying with underweight positions in linkers (vs. nominals) in the UK, Germany, France and Italy where breakevens appear too high based on our indicators. Spread Product Allocation: MAINTAIN A SMALL OVERWEIGHT TO GLOBAL SPREAD PRODUCT FOCUSED ON EUROPEAN & US HIGH-YIELD CORPORATES, WHILE UNDERWEIGHTING EM CREDIT Chart 9Negative Real Yields: Global Bonds' Biggest Vulnerability

Negative Real Yields: Global Bonds' Biggest Vulnerability

Negative Real Yields: Global Bonds' Biggest Vulnerability

Our expectation of above-trend global growth in 2022, with still relatively high inflation (compared to pre-pandemic levels), should be positive for spread products like corporate bonds that benefit from strong nominal economic (and revenue) growth. However, the less accommodative global monetary policy backdrop we also expect is a potential negative for credit market performance - specially as rate hikes put upward pressure on deeply negative real interest rates, most notably in the US (Chart 9). Thus, we are entering 2022 with a cautious, but still positive, overall position on spread product in our model bond portfolio. We are focusing more on credit valuation, however - both in absolute terms and between countries and sectors – to try and generate outperformance for the credit portion of the portfolio. We are maintaining a neutral stance on investment grade corporates in the US, euro area and UK given the tight spread valuations in those markets. We prefer to focus our corporate credit exposure on overweights to high-yield bonds in the US and Europe, but with a marginal preference for European junk bonds over US equivalents as we discussed in our 2022 Key Views report (Chart 10). Within EM USD-denominated credit, we remain cautious entering 2022 given the poor fundamental backdrop for EM credit: slowing momentum of Chinese economic growth and global commodity prices, a firmer US dollar, and a less-accommodative global monetary policy backdrop (Chart 11). Thus, an underweight stance on EM credit is appropriate within the portfolio to start the year. Chart 10Increase Euro High-Yield Exposure Vs US High-Yield

Increase Euro High-Yield Exposure Vs US High-Yield

Increase Euro High-Yield Exposure Vs US High-Yield

Chart 11Reduce EM USD-Denominated Corporate Debt Exposure To Underweight

Reduce EM USD-Denominated Corporate Debt Exposure To Underweight

Reduce EM USD-Denominated Corporate Debt Exposure To Underweight

Chart 12

Finally, we are entering 2022 with the same relative tilt within US mortgage-backed securities (MBS) that we maintained during the latter half of 2021, with an overweight stance on agency commercial MBS and an underweight on agency residential MBS. Based on our outlook for 2022, we are immediately making two marginal changes to the spread product allocations to the model bond portfolio: Reducing the size of our US high-yield overweight and using the proceeds to increase the size of the European high-yield overweight Reducing our EM USD-denominated corporate bond allocation to underweight from neutral, and placing the proceeds into Italian and Spanish government bonds (hedged into USD) to limit the reduction in the portfolio yield from the EM downgrade. The above moves will lower our overall credit overweight versus government bonds from 5% to 4%, all coming from the EM to Italy/Spain switch (Chart 12). Overall Portfolio Risk: MODERATE The changes made to our spread product allocations had no material impact on the estimated tracking error of the model portfolio – the relative volatility versus that of the benchmark. The tracking error is 78bps, still below our self-imposed limit of 100bps but above the lows seen in early 2021 (Chart 13). That higher tracking error is likely related to our underweight stance on US Treasuries, given the rise in bond volatility evident in measures like the MOVE index (bottom panel). Nonetheless, a moderate level of portfolio risk is reasonable given the combination of solid global economic growth, but with tighter global monetary policy, that we expect in 2022. Chart 13Keeping Overall Portfolio Risk At Moderate Levels

Keeping Overall Portfolio Risk At Moderate Levels

Keeping Overall Portfolio Risk At Moderate Levels

Chart 14Positive Portfolio Carry Via Selective Spread Product Overweights

Positive Portfolio Carry Via Selective Spread Product Overweights

Positive Portfolio Carry Via Selective Spread Product Overweights

The overweights to US high-yield, European high-yield and Italian government bonds all contribute to the model bond portfolio having a yield that begins 2022 modestly higher (+14bps) than that of the benchmark index (Chart 14). Portfolio Scenario Analysis For The Next Six Months After making all the changes to our model portfolio allocations, which can be seen in the tables on pages 24-25, we now turn to our regular quarterly scenario analysis to determine the return expectations for the portfolio during the first half of 2022. On the credit side of the portfolio, we use risk-factor-based regression models to forecast future yield changes for global spread product sectors as a function of four major factors - the VIX, oil prices, the US dollar and the fed funds rate (Table 2A). For the government bond side of the portfolio, we avoid using regression models and instead use a yield-beta driven framework, taking forecasts for changes in US Treasury yields and translating those in changes in non-US bond yields by applying a historical yield beta (Table 2B).

Chart

Chart

For our scenario analysis over the next six months, we use a base case scenario plus two alternate “tail risk” scenarios, based on the following descriptions and inputs: Base Case Omicron related economic weakness is visible in some major economies (euro area, Canada), but the US stays resiliently strong and the US labor market continues to tighten. China is a growth laggard, but this will lead to policymakers providing more macro stimulus (credit, monetary, fiscal) starting in Q2/2022. Inflation pressures from supply chain disruption remain stubbornly strong and realized global inflation rates stay elevated for longer. Developed market central banks continue dialing back pandemic-era monetary policy accommodation, led by Fed tapering and a June 2022 liftoff of the funds rate. There is a mild initial bear steepening of the US Treasury curve with additional widening of US inflation breakevens in Q1/2022, leading to bear flattening in Q2 in the run-up to liftoff – the net effect is a parallel shift higher in the entire yield curve. The VIX index stays near current levels at 20, both the US dollar and oil prices are broadly unchanged and the fed funds rate is increased to 0.25%. Hawkish Fed The Omicron wave is short-lived with limited impact on global growth, which remains well above trend. Global inflation only declines moderately from current elevated levels, both from persistent supply squeezes and faster wage growth. China loosens monetary/credit policies and announces new fiscal stimulus in late Q1/2022 – a positive surprise for global growth expectations. Developed economy central banks turn even more hawkish. Fed liftoff is in March, with another hike in June. The US Treasury curve bear-flattens as US inflation breakevens reach their cyclical peak. The VIX index climbs to 25, the US dollar depreciates by -3% (pulled in opposing directions by strong global growth but relatively higher US interest rates), oil prices climb +10% and the fed funds rate is increased to 0.5%. Pessimistic Scenario The Omicron wave persists in many major countries (including the US) and leads to extended lockdowns and weaker consumer spending. Global growth momentum slows sharply. China does not signal adequate stimulus to offset its slowdown, while a weakened Biden administration passes much smaller US fiscal stimulus. Supply chain disruptions persist and are made worse by Omicron, keeping inflation elevated even as growth slows (stagflation). Developed economy central banks, stuck between slowing growth and elevated inflation, are unable to ease in response to economic weakness. The Fed goes for a slower taper that still ends in June, but liftoff is delayed until at least September. The US Treasury curve bull steepens modestly as the front end prices out 2022 hikes. US inflation breakevens remain sticky due to persistent realized inflation. The VIX index climbs to 30, the US dollar appreciates by +5% on a safe haven bid, oil prices fall -10% and the fed funds rate remains at 0%. The excess return scenarios for the model bond portfolio, using the above inputs in our simple quantitative return forecast framework, are shown in Table 3A. The US Treasury yield assumptions are shown in Table 3B. For the more visually inclined, we present charts showing the model inputs and Treasury yield projections in Chart 15 and Chart 16, respectively.

Chart

Chart

Chart 15Risk Factor Assumptions For The Scenario Analysis

Risk Factor Assumptions For The Scenario Analysis

Risk Factor Assumptions For The Scenario Analysis

Chart 16US Treasury Yield Assumptions For The Scenario Analysis

US Treasury Yield Assumptions For The Scenario Analysis

US Treasury Yield Assumptions For The Scenario Analysis

The model bond portfolio is expected to deliver an excess return over its performance benchmark during the next six months of +54bps in the Base Case and +31bps in the Hawkish Fed scenario, but is projected to underperform by -9bps in the Pessimistic scenario. Importantly, there is virtually no expected excess return from the credit side of model bond portfolio in the Hawkish Fed scenario, even with strong global growth. A faster-than-expected pace of Fed rate hikes in the first half of 2022 would be a clear signal to downgrade exposure to the riskier parts of the fixed income universe like US high-yield. Although in that Hawkish Fed scenario, greater-than-expected China stimulus and a weaker US dollar would also represent signals to begin adding back emerging market credit exposure. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Our model bond portfolio custom benchmark index is the Bloomberg Barclays Global Aggregate Index, but with allocations to global high-yield corporate debt and USD-denominated emerging market debt replacing very high quality spread product (i.e. AA-rated). We believe this to be more indicative of the typical internal benchmark used by global multi-sector fixed income managers. 2 We also made very slight adjustments within the US, Japan, Germany and France allocations to refine our allocations across the various maturity buckets while keeping the overall portfolio duration unchanged entering 2022. Appendix

Image

Image

Image

Image

Image

Recommendations Duration Regional Allocation Spread Product Tactical Trades GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

Image

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Image

We have entered a new phase of the cycle, with central banks in most developed markets turning more hawkish (the Bank of England surprisingly hiking in December, and the Fed signaling three rate hikes for 2022). How much does this matter for equities and other risk assets? Our view is that, as long as economic growth continues to be strong (and we think it will), and provided that central banks don’t overdo the tightening (and, with inflation likely to come down this year, we think excess tightening is unlikely), the hawkish turn might temporarily raise volatility and cause the occasional correction, but it does not undermine the case for equities to outperform bonds over the next 12 months. We remain overweight global equities. Economic growth is likely to continue to be well above trend for the next year or two (Chart 1), driven by (1) consumers spending some of the $5 trillion of excess savings they have accumulated in the G10 economies, (2) the unprecedented wealth effect from recent stock and house price rises (Chart 2), and (3) strong capex as companies strive to increase capacity to meet the consumer demand (Chart 3). The upsurge in Covid cases in December (Chart 4) will undoubtedly slow growth temporarily. But the signs are that the now-prevalent Omicron variant is mild, and its rapid spread could help the developed world achieve “herd immunity” thanks to widespread vaccination and natural immunity, though emerging countries – especially China – may continue to struggle. Chart 1Growth Will Continue To Be Above Trend

Growth Will Continue To Be Above Trend

Growth Will Continue To Be Above Trend

Chart 2Growth Will Be Boosted By The Wealth Effect...

Growth Will Be Boosted By The Wealth Effect...

Growth Will Be Boosted By The Wealth Effect...

Chart 3...And Capex To Increase Production

...And Capex To Increase Production

...And Capex To Increase Production

With US growth very strong – the Atlanta Fed Nowcast suggests Q4 QoQ annualized real GDP growth was 7.6% – and core PCE inflation 4.1%, it is hardly surprising that the Fed wants to accelerate the rate at which it withdraws accommodation. The FOMC dots, which see three rate hikes this year and another three in 2023, are unexceptional and close to what the futures market has already been (and still is) pricing in (Chart 5). Chart 4Covid Cases Not Leading to Hospitalizations And Deaths

Covid Cases Not Leading to Hospitalizations And Deaths

Covid Cases Not Leading to Hospitalizations And Deaths

Chart 6Fed Hikes Have Usually Caused Only A Short-Lived Selloff

Fed Hikes Have Usually Caused Only A Short-Lived Selloff

Fed Hikes Have Usually Caused Only A Short-Lived Selloff

Chart 5The Futures Market Is In Line With The FOMC Dots

The Futures Market Is In Line With The FOMC Dots

The Futures Market Is In Line With The FOMC Dots